Instant Cereals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.27 Billion |

| Market Size (2031) | USD 30.86 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

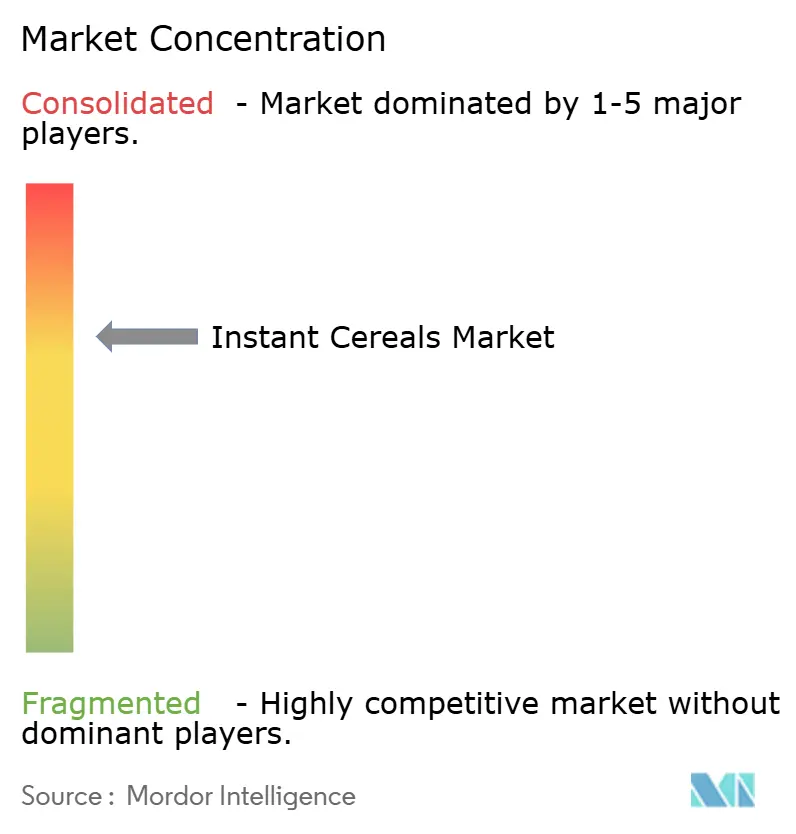

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Instant Cereals Market Analysis by Mordor Intelligence

The instant cereals market size is expected to increase from USD 23.13 billion in 2025 to USD 24.27 billion in 2026 and reach USD 30.86 billion by 2031, growing at a CAGR of 4.92% over 2026-2031. Rising demand for convenient breakfasts, rapid urbanization in Asia-Pacific, and stricter sugar-reduction mandates are reshaping product portfolios and pricing strategies across the instant cereals market. Technology-enabled reformulation is accelerating whole-grain and high-protein launches, while direct-to-consumer (DTC) brands are eroding incumbent share by offering gluten-free and low-carb options at premium price points. Consolidation among multinational players seeks scale economies to manage higher compliance costs, and capital expenditure is gravitating toward Asia-Pacific extrusion hubs. Commodity price volatility remains a swing factor for margins, yet favorable oat pricing in 2026 is cushioning reformulation outlays.

Key Report Takeaways

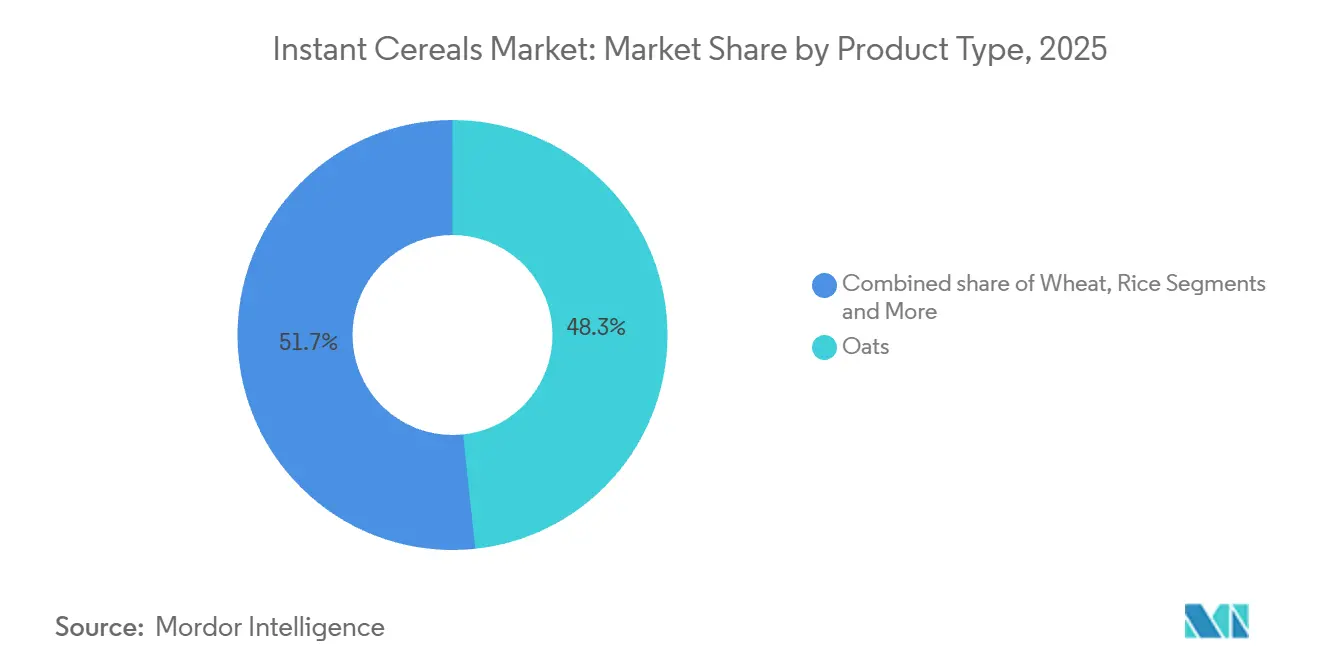

- By product type, oats captured 48.31% of the instant cereals market share in 2025, whereas corn-based cereals are forecast to grow at a 5.26% CAGR through 2031.

- By flavor, flavored variants held 70.92% share in 2025; unflavored lines are set to grow at a 6.08% CAGR to 2031.

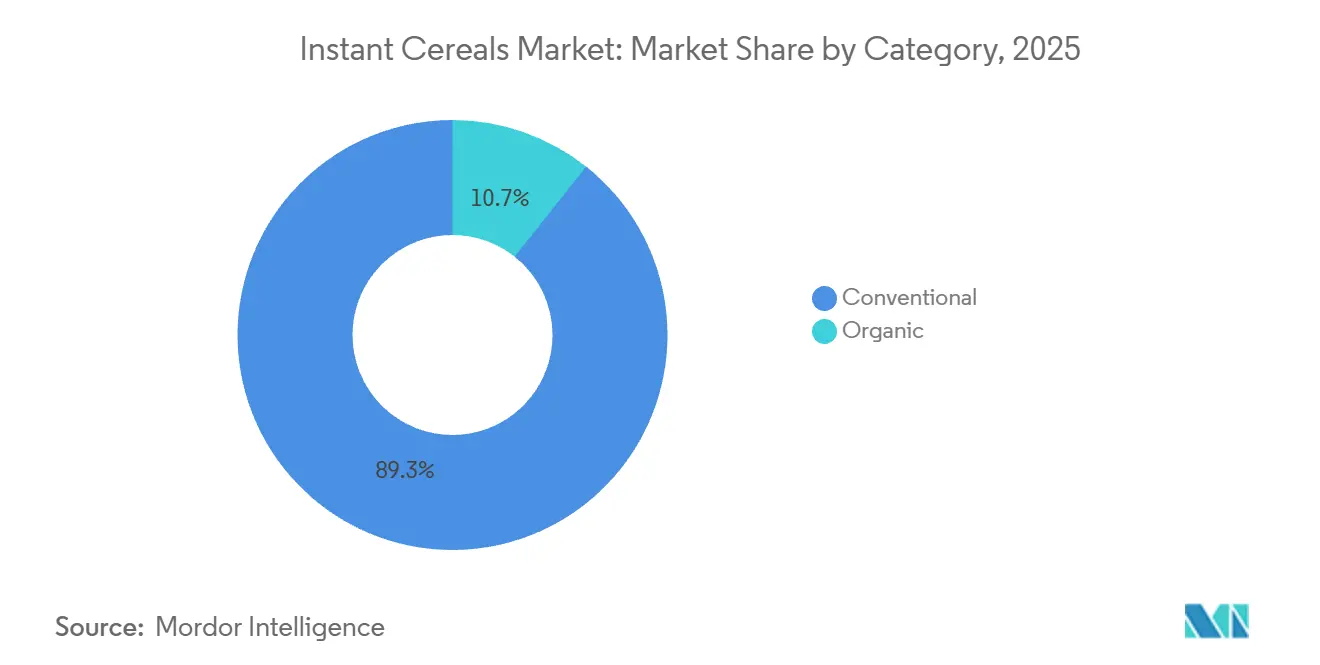

- By category, conventional products commanded 89.32% share in 2025, while organic products are projected to expand at a 6.73% CAGR.

- By distribution channel, supermarkets/hypermarkets led with 44.76% share in 2025; online retail stores are poised for a 5.82% CAGR.

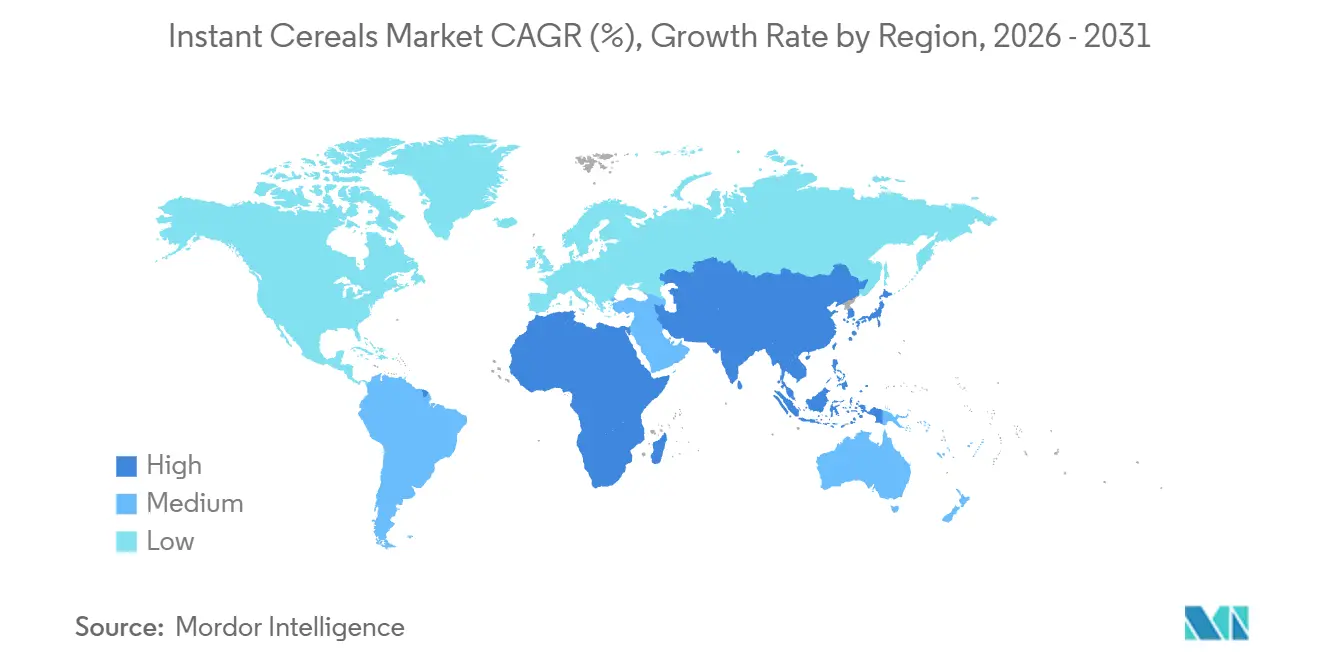

- By geography, North America contributed 35.88% revenue share in 2025, and Asia-Pacific is predicted to grow at the fastest 6.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Instant Cereals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenience and on-the-go breakfasts | +1.2% | Global, with peak intensity in Asia-Pacific urban centers and North American metro areas | Short term (≤ 2 years) |

| Rising health focus on whole-grain and high-protein formulations | +0.9% | North America & Europe (regulatory push), Asia-Pacific (aspirational wellness) | Medium term (2-4 years) |

| Introduction of new flavors, plant-based ingredients, and regional customizations | +0.7% | Asia-Pacific (localized porridge formats), Latin America (tropical fruit flavors), North America (protein blends) | Medium term (2-4 years) |

| Increasing availability for diverse dietary preferences | +0.5% | Global, with early gains in North America (gluten-free, vegan), Europe (allergen labeling compliance) | Long term (≥ 4 years) |

| Advances in food processing technology | +0.4% | Global, concentrated in manufacturing hubs (North America, Europe, China) | Long term (≥ 4 years) |

| Influence of urbanization and modern lifestyles | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health Focus on Whole-Grain and High-Protein Formulations

Consumer demand for functional breakfast options has catalyzed a fundamental reformulation trend across the instant cereals industry, with manufacturers increasingly positioning products as vehicles for essential nutrients rather than mere convenience foods. The USDA's emphasis on making half of grain consumption whole grains has created regulatory tailwinds, while research demonstrating that breakfast cereal consumption correlates with higher vitamin and mineral intake provides scientific validation for health claims[1]Source: U.S. Department of Agriculture, “Make Half Your Grains Whole Grains", myplate.gov. The protein fortification movement has gained particular traction among younger demographics. This health positioning strategy extends beyond protein to encompass fiber enhancement, with manufacturers leveraging β-glucan extraction technologies to maximize the cholesterol-lowering benefits that provide FDA-approved health claims for oat-based products. The convergence of regulatory support, scientific validation, and consumer demand creates a self-reinforcing cycle that positions health-focused formulations as the primary growth engine for premium market segments.

Demand for Convenience and On-the-Go Breakfasts

In Asia-Pacific megacities, where many workers face commutes exceeding 90 minutes, urbanization is shrinking the time available for breakfast preparation. This has led to a surge in the popularity of single-serve instant porridge formats, which can be rehydrated in under three minutes. This quick rehydration time is backed by peer-reviewed studies, highlighting an optimized instant cereal drink's rehydration at just 2.73 seconds. Furthermore, the U.S. Department of Agriculture's move to allow SNAP online purchases at over 390 retailer chains by 2025 has made instant cereals more accessible to lower-income families. This shift has effectively eliminated a previous distribution hurdle, which had limited premium instant oatmeal sales to specialty brick-and-mortar stores. Meanwhile, PepsiCo's initiatives, like the Quaker Bowl of Growth in India and Quaker Qrece in Guatemala and Mexico, showcase how global giants are customizing portion sizes and flavors to resonate with local breakfast habits. This approach not only taps into established distribution channels but also reduces the risks associated with reformulating products.

Introduction of New Flavors, Plant-Based Ingredients, and Regional Customizations

Flavor innovation has evolved beyond traditional profiles like cinnamon and maple. Manufacturers now infuse plant-based proteins, microalgae, and region-specific ingredients to set their products apart. A 2025 study highlighted that adding just 1% Spirulina platensis to sorghum-based instant cereal flakes garnered a notable sensory acceptance score of 6.06 out of 7 from children aged 10-12. This formulation boasted an impressive nutritional profile, delivering 12.56% protein and 4.68% dietary fiber per 100 grams. PepsiCo's Quaker Oat "Rice" in Brazil showcases a keen understanding of local preferences, adapting its product to closely resemble rice in texture and appearance. In Indonesia, sensory evaluations indicated a clear consumer preference for plant milk alternatives made from red rice and white sorghum over those derived from rice bran. This insight points to the potential for cereal-based dairy substitutes to rival traditional instant oatmeal, provided they're tailored to local tastes. General Mills made waves in November 2025 with its launch of Kernza perennial grain cereals, a move underscoring its commitment to sustainability and appealing to eco-conscious consumers ready to invest in regenerative agriculture.

Increasing availability for diverse dietary preferences

Rapid urbanization across Asia-Pacific markets has transformed breakfast consumption patterns, with traditional rice-based morning meals being replaced by convenient cereal options that align with modern work schedules. In 2024, 35% of India's total population lived in cities, showing an increase in urbanization of more than 4% in the last decade[2]Source: The World Bank Group, “Urban population (% of total population) - India", data.worldbank.org. Research indicates that urbanization influences food consumption through multiple factors beyond income, including food accessibility, time constraints, and exposure to Western dietary patterns. This effect is particularly evident in markets like China and India, where rising disposable incomes align with improved cold-chain distribution capabilities for packaged breakfast products. Urban consumers show increased willingness to pay premium prices for products offering health benefits and convenience. The urbanization trend creates compounding effects: infrastructure improvements enable wider product distribution, while cultural shifts toward Western breakfast habits expand the market. This positions urban market penetration as a primary growth strategy for international instant cereals manufacturers in emerging economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar-content scrutiny and High Fat, Sugar, and Salt (HFSS) regulations | -0.9% | North America and EU, expanding to other regions | Short term (≤ 2 years) |

| Competition from alternative options | -1.1% | Global, particularly intense in developed markets | Medium term (2-4 years) |

| High raw material costs | -0.8% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Quality perceptions regarding high processing | -0.5% | Developed markets with high health awareness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sugar-Content Scrutiny and High Fat, Sugar, and Salt (HFSS) Regulations

Regulatory pressure surrounding sugar content has intensified globally, with the United Kingdom's implementation of HFSS advertising restrictions effective October 2025 serving as a bellwether for broader regulatory trends that could reshape product formulations and marketing strategies across the instant cereals industry. The United Kingdom regulations impose a 9 pm watershed for television advertising and complete online advertising bans for products exceeding specific sugar, fat, and salt thresholds, directly impacting traditional breakfast cereal marketing approaches[3]Source: UK Department of Health & Social Care, “Restricting advertising of less healthy food or drink on TV and online: products in scope", gov.uk. The regulatory environment has created a bifurcated market where compliant products gain competitive advantages in regulated channels while traditional formulations face increasing distribution constraints. The regulatory trend extends beyond sugar to encompass broader nutritional profiling models that evaluate products holistically, creating complexity for manufacturers who must balance taste preferences, regulatory compliance, and cost considerations while maintaining brand positioning and consumer loyalty in an increasingly regulated environment.

Competition from Alternative Breakfast Options

Instant cereals face growing competition from yogurt, smoothie bowls, cereal bars, and coffee-shop takeaways, which offer similar convenience with unique nutritional benefits. In North America, the hot cereal market declined by 3.7% year-over-year to USD 1.93 billion in the 52 weeks ending December 28, 2025, as consumers shifted to Greek yogurt and protein shakes that provide more protein per calorie without preparation. Quaker Oats, despite generating over USD 1 billion in sales, saw a 5.8% revenue drop, highlighting the impact of these alternatives. In Europe, on-the-go bakery items like croissants and savory pastries are reducing cereal consumption, especially among younger consumers who prefer indulgence over nutrition. Cereal bars and muffins, which don’t require milk or hot water, contributed to a GBP 78 million decline in UK sales of core cereals like corn flakes and muesli in one year. In Asia-Pacific, traditional breakfasts such as congee in China, idli in India, and nasi lemak in Malaysia remain culturally dominant, limiting instant cereal growth outside cities. To compete, instant cereal makers must offer better taste, nutrition, or sustainability compared to traditional and modern breakfast options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oats Anchor Market, Corn Gains on Gluten-Free Wave

In 2025, oats held a 48.31% share of the instant cereals market, driven by their association with heart health and whole-grain benefits. Bob's Red Mill reported a 6.4% sales increase, reaching USD 132.86 million by December 28, 2025, fueled by its Overnight Protein Oats launch with 10 grams of protein per serving. Quaker Oats introduced Protein Standard oats in spring 2025, targeting fitness enthusiasts seeking muscle recovery benefits. Oat prices dropped to USD 3.12 per bushel in January 2026 from USD 3.92 in 2023-2024, easing reformulation costs for manufacturers. Finland's annual oatmeal consumption of 30-34 kilograms per person highlights oats' cultural significance in Nordic breakfasts. However, HFSS regulations penalizing sugary flavored oatmeal are pushing producers toward unflavored or naturally sweetened options.

Corn-based instant cereals are projected to grow at a 5.26% CAGR from 2026 to 2031, the fastest among all types, due to their gluten-free and allergen-friendly appeal. Research shows adding 20% quinoa at 650 rpm extrusion improves protein and fiber while maintaining texture, supporting corn-based functional cereals. Corn fits well with traditional dishes like Mexico's atole and Southeast Asia's congee, easily adapted to instant formats. In January 2026, corn's Market Year Average price was USD 4.10 per bushel, remaining cost-competitive against wheat (USD 5.01) and rice (USD 13.60 per hundredweight). Improved supply chains, exports, logistics, and storage have boosted corn availability, reducing risks seen in 2021-2022. Flavor innovations, such as sweet-savory blends and global cuisine influences, are helping corn-based cereals attract younger consumers seeking variety in breakfast options.

By Flavor: Flavored Variants Dominate, Unflavored Surges on Health Pivot

In 2025, flavored instant cereals held a 70.92% market share, driven by consumer demand for variety and the convenience of pre-sweetened options. Post Consumer Brands launched OREO PUFFS in January 2025, leveraging its confectionery brand to attract younger consumers. Similarly, Kellogg's introduced High Protein Bites in April 2025, offering 13-14 grams of protein to compete with protein bars. However, flavored cereals face challenges like the USDA's 6-gram added sugar limit for Child and Adult Care Food Program cereals, forcing reformulations with non-nutritive sweeteners or smaller portions. Additionally, HFSS advertising restrictions in the UK and Scotland limit promotions of high-sugar cereals during peak hours and in prominent retail spaces.

Unflavored instant cereals are growing at a 6.08% CAGR from 2026 to 2031, the fastest among flavor types, as health-conscious consumers seek customization and sugar control. Purely Elizabeth's sales grew 40% year-over-year to USD 12.85 million by December 28, 2025, showing demand for organic, lightly sweetened oatmeal that consumers enhance with fresh ingredients. Unflavored cereals align with clean-label trends and meet USDA and HFSS standards without reformulation, ensuring access to institutional buyers. A 2026 study on jali and garut flour-based cereals achieved a high desirability score of 0.996, proving unflavored options can succeed with good texture and mouthfeel. The segment also benefits from savory cereals with vegetables and herbs, appealing to Asian and European tastes. Premium pricing in organic and specialty markets offsets lower sales volumes with higher margins.

By Category: Conventional Holds Share, Organic Outpaces on Certification Demand

In 2025, conventional instant cereals held 89.32% of the market, driven by strong distribution networks, low prices, and consumer familiarity. Bulk purchases of non-organic oats, corn, and wheat at commodity prices of USD 3.12, USD 4.10, and USD 5.01 per bushel in January 2026 helped manufacturers keep retail prices below USD 0.30 per serving, appealing to cost-conscious households. Despite a 5.8% sales decline, Quaker Oats earned over USD 1 billion in the 52 weeks ending December 28, 2025, showing the segment's volume stability even as premium products gain traction. Government programs like the USDA's USD 2.4 billion Child Nutrition allocation for fiscal year 2026 favor conventional cereals due to their low cost per serving. However, rising input costs, including a 12% increase in fertilizer prices (index 115.3 in January 2026), and reformulation expenses for sugar reduction are squeezing margins.

Organic instant cereals are expected to grow at a 6.73% CAGR from 2026 to 2031, the fastest among all categories. Growth is fueled by more certifications and consumers willing to pay for non-GMO and pesticide-free claims. One Degree Organic Foods saw USD 50.07 million in sales with 32% growth in the 52 weeks ending December 28, 2025, showing the value of USDA Organic and Non-GMO Project Verified labels. Purely Elizabeth's 40% sales growth in the same period, led by organic oatmeal and granola, highlights the segment's appeal to health-conscious, affluent consumers. Regulatory frameworks like the USDA National Organic Program and EU Organic Regulation (EU) 2018/848 simplify certification, reducing barriers for new brands. Organic cereals command 30-50% higher prices than conventional ones due to perceived quality and sustainability. However, limited organic grain supply, with oats and wheat priced 50-100% higher than conventional, and high certification costs challenge smaller manufacturers' profitability.

By Distribution Channel: Online Retail Accelerates Growth

In 2025, supermarkets and hypermarkets led instant cereal distribution with a 44.76% share, supported by high foot traffic, wide product ranges, and competitive pricing. This dominance is strong in North America and Europe, where retailers like Walmart, Tesco, and Carrefour dedicate significant shelf space to instant cereals, boosting visibility and impulse buys. However, the UK's HFSS regulations, effective in 2025, restrict the prominent placement of high-sugar cereals, pushing these products to less visible aisles and reducing their sales share. Private-label cereals, such as Tesco's own-brand oatmeal and Walmart's Great Value line, priced 20-30% lower than branded options, attract budget-conscious consumers, especially as inflation pressures incomes. Growth, however, is limited by retailer demands for slotting fees, promotions, and markdowns, which heavily impact smaller brands.

Online retail is set to grow at a 5.82% CAGR from 2026 to 2031, the fastest among distribution channels. Direct-to-consumer (DTC) models, bypassing traditional retailers, drive this growth by offering higher margins. For instance, Magic Spoon, after gaining over 1 million customers through its DTC model, expanded to Target in 2025. The USDA's 2025 expansion of SNAP online purchasing to over 390 retailers has made e-commerce more accessible to low-income households. Subscription models from brands like Catalina Crunch and Magic Spoon ensure steady revenue and lower customer acquisition costs. Online platforms also help manufacturers use consumer data for personalized recommendations, optimized pack sizes, and low-risk product testing. However, challenges like high last-mile delivery costs (15-25% of product prices) and consumer reluctance to pay shipping fees for groceries remain. Quick-commerce platforms like Instacart, DoorDash, and Getir, offering under-30-minute deliveries in cities, are blurring the lines between online and offline shopping, increasing competition for shelf space in dark stores and micro-fulfillment centers.

Geography Analysis

North America maintains a dominant market position with 35.88% share in 2025. This leadership stems from established consumer breakfast habits, comprehensive cold-chain distribution infrastructure, and strong brand loyalty that creates entry barriers for international competitors. The region's mature retail networks, marketing capabilities, and supportive regulatory frameworks enable health claims and product innovation. However, North America faces growth limitations from market saturation, evolving demographic preferences, and increasing competition from alternative breakfast options.

Asia-Pacific demonstrates the highest growth rate at 6.89% CAGR through 2031. This growth results from urbanization, increasing disposable incomes, and a shift toward Western breakfast habits, expanding beyond traditional rice-based morning meals. China and India's large populations, improving retail infrastructure, and growing health consciousness among urban consumers support market expansion. The region's diverse cultural preferences create opportunities for localized products, including rice-based cereals that combine traditional preferences with modern convenience.

Europe maintains a stable market position with established organic and health-focused consumer segments driving premium product demand. The region adapts to HFSS regulatory requirements that influence marketing strategies and product formulations. The Middle East and Africa, and South America represent emerging markets with growth potential driven by urbanization, infrastructure development, and increasing Western breakfast adoption. These regions offer market expansion opportunities but require consideration of local preferences, price sensitivity, and distribution challenges. Success depends on manufacturers' ability to invest in market development and consumer education.

Competitive Landscape

The instant cereals market exhibits moderate consolidation, characterized by established multinational players maintaining significant market shares through brand equity, distribution networks, and economies of scale, while facing increasing pressure from health-focused startups, private label alternatives, and cross-category competition that challenges traditional competitive dynamics. Key players in the market include Post Holdings Inc., Nestlé S.A., PepsiCo Inc., General Mills Inc., Kellanova.

Technology adoption has emerged as a critical competitive differentiator, with companies investing in advanced processing techniques like ultrahigh-pressure treatment and enzymatic hydrolysis to improve product quality, extend shelf life, and enable new product formats that address evolving consumer preferences. Patent filings in oat processing technologies, including rapid hydrolysis processes for oat-based beverages and differential pressure explosion puffing methods, demonstrate the industry's focus on technological innovation as a source of competitive advantage.

White-space opportunities exist in functional nutrition positioning, sustainable sourcing practices, and direct-to-consumer channels that enable premium pricing and deeper consumer relationships, while emerging disruptors leverage clean-label positioning, subscription models, and social media marketing to capture market share from established players who may be constrained by legacy brand positioning and traditional retail relationships.

Instant Cereals Industry Leaders

-

Post Holdings Inc.

-

Nestlé S.A.

-

PepsiCo Inc.

-

General Mills Inc.

-

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nestlé has expanded its breakfast cereal portfolio with the launch of Chocapic Protein and Lion Protein, two new variants of its iconic chocolate‑flavored cereals enriched with extra protein, according to the brand.

- July 2025: Ferrero Group completed its USD 3.1 billion acquisition of WK Kellogg Co for USD 23 per share, gaining control of iconic breakfast cereal brands including Frosted Flakes and Special K while establishing Battle Creek, Michigan as its North American cereal headquarters.

- January 2025: Kodiak Cakes, in collaboration with its chief brand officer Zac Efron, introduced apple brown sugar pecan oatmeal. The instant oatmeal product contains 100% whole grain, prebiotic fiber, and 14 grams of protein. The formulation includes pumpkin seeds, chia seeds, and cranberry seeds.

Global Instant Cereals Market Report Scope

| Oats |

| Wheat |

| Rice |

| Corn |

| Others |

| Flavored |

| Unflavored |

| Conventional |

| Organic |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Oats | |

| Wheat | ||

| Rice | ||

| Corn | ||

| Others | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the instant cereals market be by 2031?

The instant cereals market size is projected to reach USD 30.86 billion by 2031, expanding at a 4.92% CAGR from 2026-2031.

Which product type leads global revenue?

Oats retained 48.31% instant cereals market share in 2025, driven by strong health associations.

Which region is growing fastest through 2031?

Asia-Pacific is forecast to grow at a 6.89% CAGR, outpacing all other regions due to rapid urbanization and hot cereal preferences.

Which channel will capture incremental sales?

Online retail, growing 5.82% annually, will add the most new sales through subscription models and expanded SNAP e-commerce access.

Page last updated on: