Instant Tea Premix Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 2.73 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

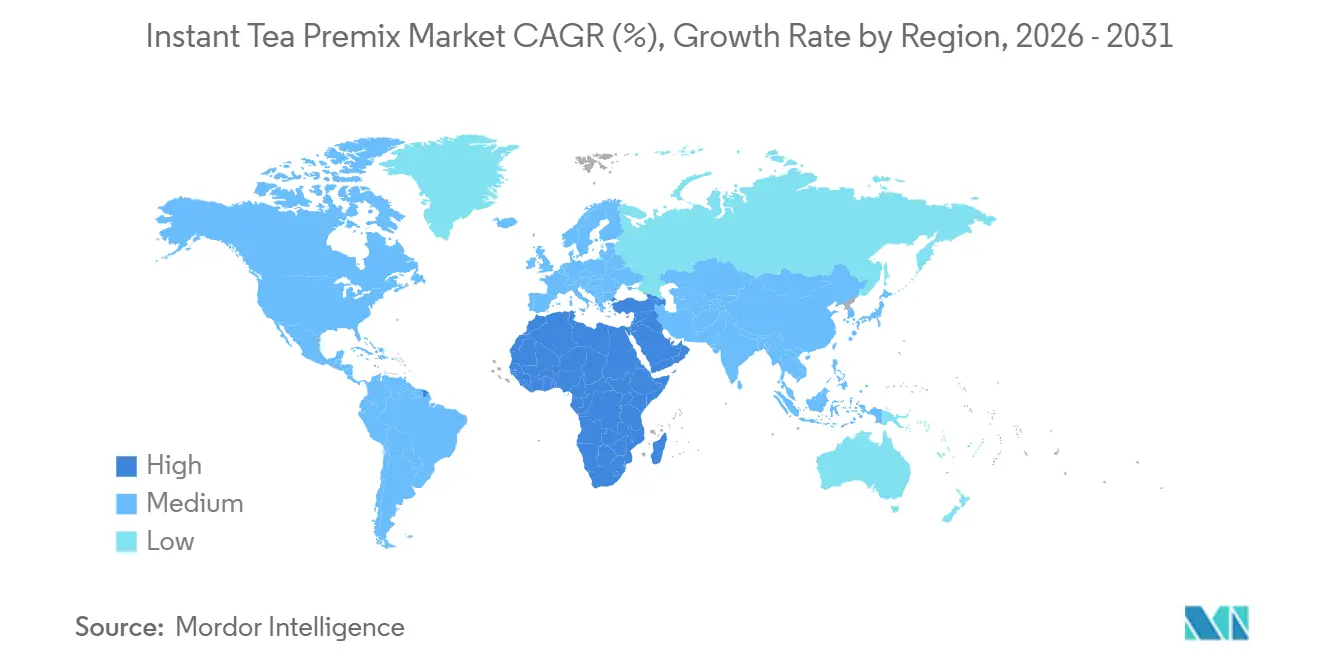

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

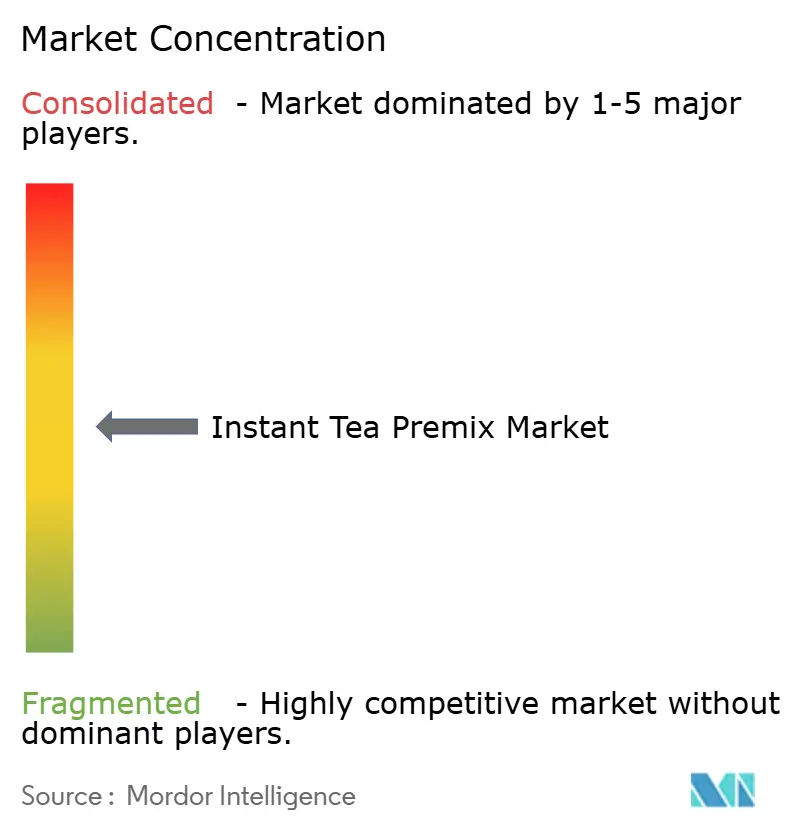

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Instant Tea Premix Market Analysis by Mordor Intelligence

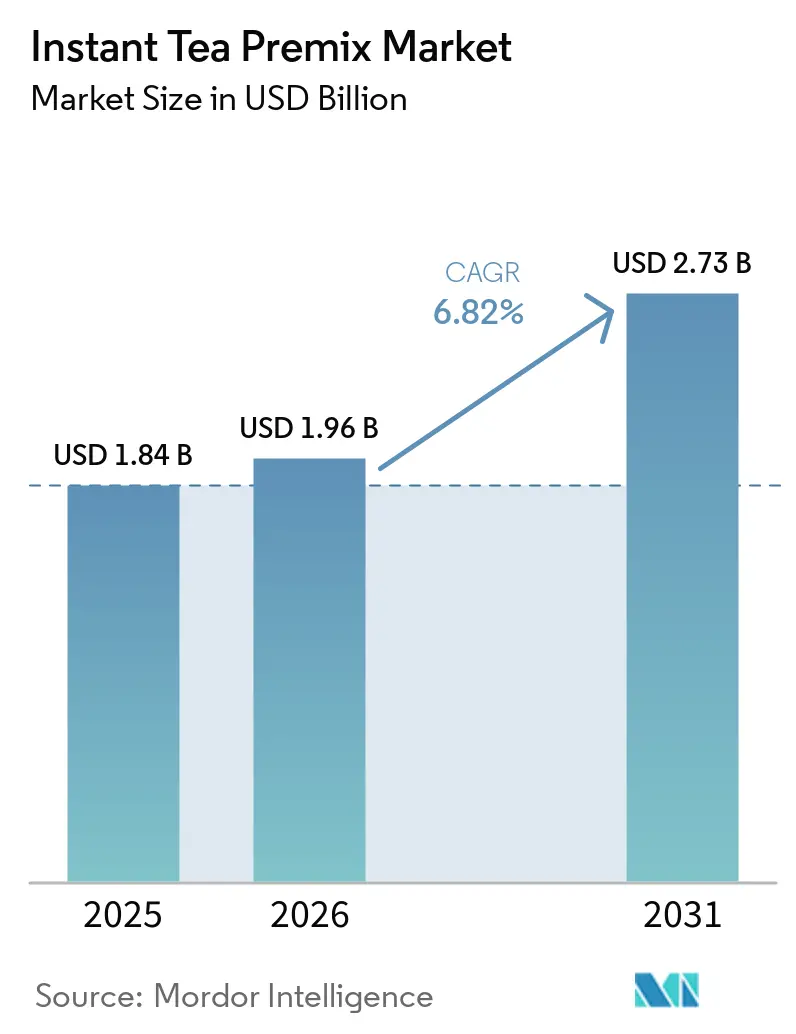

The Instant Tea Premix Market is expected to grow from USD 1.84 billion in 2025 to USD 2.73 billion by 2031, at a CAGR of 6.82% from 2026 to 2031. Urban consumers are driving demand for convenient tea options, while regulatory frameworks like FSSAI’s licensing tiers ensure quality and build consumer trust. Asia-Pacific leads in volume, with the Middle East & Africa showing the fastest growth. Rising demand for organic certifications, driven by preferences for “pesticide-free” products linked to wellness, further supports market growth. Innovations in manufacturing, such as ultrasonic extraction and superfine grinding, enhance solubility and preserve polyphenols, delivering flavors closer to brewed tea. Coupled with advancements in e-commerce analytics, AI-driven flavor discovery, and compostable packaging, these factors position market leaders to outpace the broader beverage sector's growth.

Key Report Takeaways

- By category, conventional products held 85.43% of the instant tea premix market share in 2025, and organic variants are projected to expand at a 7.01% CAGR through 2031.

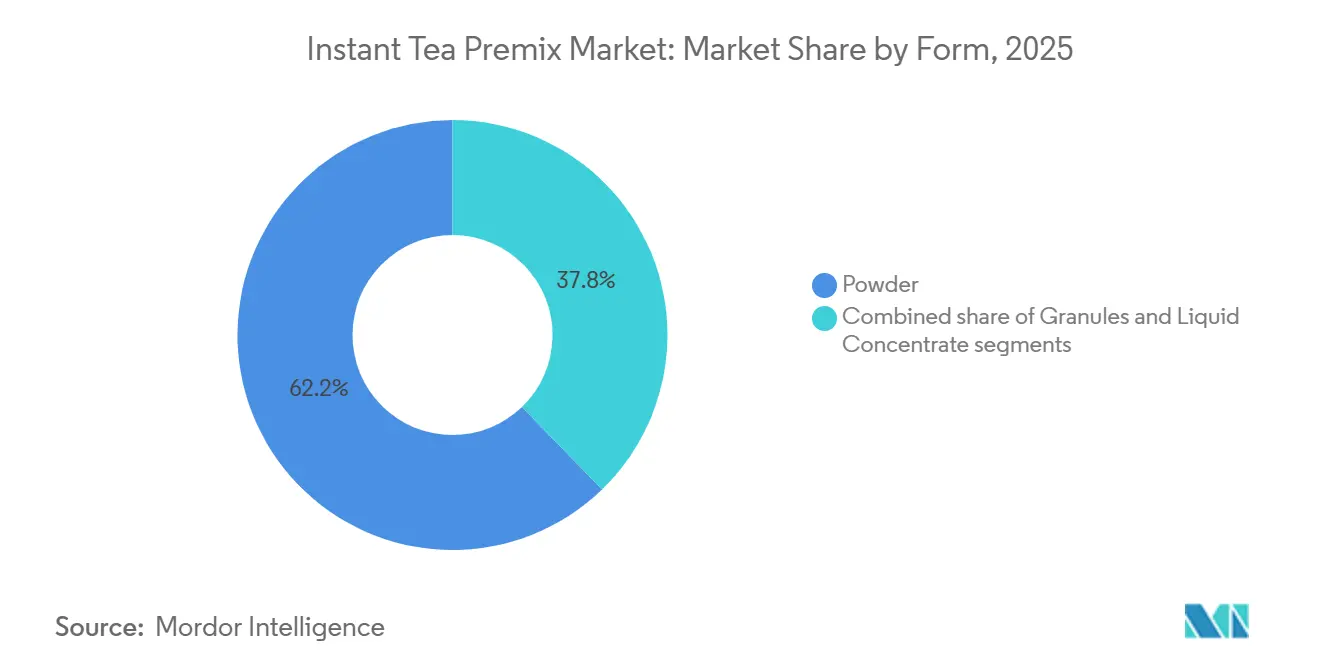

- By form, powder commanded 62.23% share of the instant tea premix market size in 2025, and liquid concentrates are forecast to post the fastest growth at an 8.21% CAGR between 2026 and 2031.

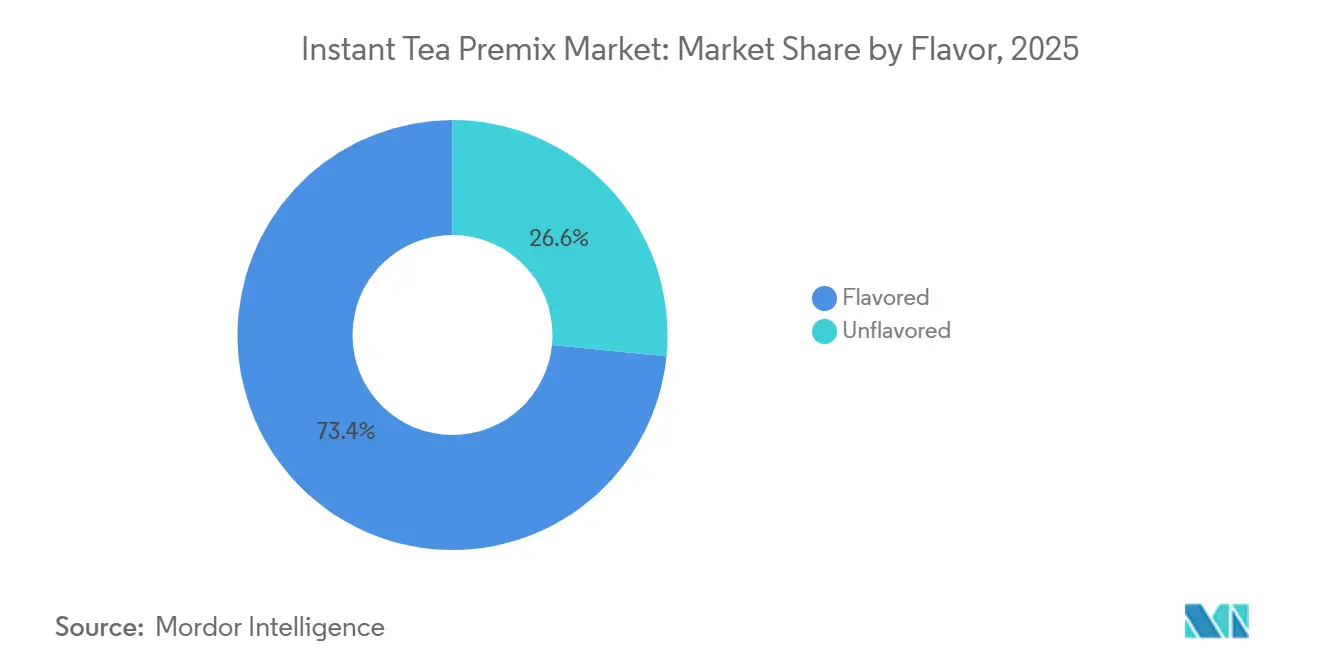

- By flavor, flavored premixes captured 73.42% revenue share in 2025 and are projected to grow at a 6.98% CAGR between 2026 and 2031.

- By packaging, single-serve sachets led with 41.35% share during 2025, while pouches will climb at a 9.21% CAGR through 2031.

- By distribution channel, retail led with 63.88% share during 2025, and foodservice/HoReCa is projected to pace ahead with a 7.26% CAGR to 2031.

- By geography, Asia-Pacific led with 51.31% share during 2025, and Middle East and Africa is projected to pace ahead with a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Instant Tea Premix Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for convenience and rapid preparation | +1.8% | Global, with peak intensity in North America, Europe, and APAC urban centers | Short term (≤ 2 years) |

| Continuous flavor innovation | +1.3% | Global, led by North America and Europe for premium variants, APAC for traditional-modern fusion | Medium term (2-4 years) |

| Growth of e-commerce and omnichannel distribution | +1.2% | APAC core, expanding rapidly to MEA and South America | Medium term (2-4 years) |

| Increased demand for "better-for-you" instant tea premixes | +1.1% | North America and Europe primary, spillover to APAC affluent urban segments | Long term (≥ 4 years) |

| Technology-enabled personalization | +0.9% | North America and Europe digital-first markets, early adoption in APAC tier-1 cities | Long term (≥ 4 years) |

| Cultural adaptation and localization | +0.8% | APAC, MEA, and South America where regional flavor preferences diverge from Western norms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for convenience and rapid preparation

The growing time constraints among working populations are driving the adoption of instant tea premixes, which reduce preparation times from the traditional 3-5 minutes to under 30 seconds for cold-soluble variants. Nestlé’s NESCAFÉ Ice Roast, launched in April 2024, dissolves instantly in cold water, catering to on-the-go consumers during commutes and outdoor activities. This trend extends to institutional buyers, such as hospitals, corporate cafeterias, and educational institutions, which are replacing traditional tea brewing equipment with instant dispensers to cut labor costs and minimize waste from over-brewed tea. According to the Indian Directorate General of Commercial Intelligence and Statistics, instant tea processing methods like spray-drying and freeze-drying produce water-soluble granules that preserve catechin content and enable ambient storage. Quick-service restaurants are also adopting instant premixes to ensure consistent flavor across franchise networks, addressing the variability in brewed tea caused by differences in water temperature, steeping time, and tea-to-water ratios.

Continuous flavor innovation

Flavor diversification in the instant tea market now extends beyond traditional options like lemon and peach to include functional blends with adaptogens, botanicals, and regional spices. A 2026 study in the Foods journal revealed that GABA-enriched instant white tea, developed using optimized spray-drying techniques, retained 87% of its gamma-aminobutyric acid content, appealing to stress-conscious consumers. In January 2026, Flavor Dynamics introduced encapsulated flavor systems that release aroma compounds upon dissolution, replicating the sensory experience of freshly brewed tea. Matcha-infused instant premixes gained popularity in China's tier-1 cities in 2025, prompting increased domestic matcha production to meet the demand for premium green tea. Regional localization strategies have also emerged, with brands offering masala chai premixes in India, yuzu-ginger blends in Japan, and mint-based formulations in the Middle East, catering to local tastes while maintaining convenience.

Growth of e-commerce and omnichannel distribution

Niche instant tea brands are utilizing online retail channels to bypass traditional gatekeepers and directly target health-conscious consumers willing to pay premiums for organic, fair-trade, or single-origin variants. E-commerce platforms secure recurring revenue through subscription models while offering personalized recommendations based on purchase histories and flavor preferences. Established players are adopting omnichannel strategies, integrating online storefronts with physical retail outlets, enabling consumers to discover products in supermarkets and reorder via mobile apps with home delivery. Quick-commerce platforms in urban centers, offering 10-15 minute delivery windows, drive impulse purchases of instant tea premixes positioned as healthier alternatives to carbonated soft drinks. Additionally, digital channels foster direct-to-consumer feedback loops, allowing manufacturers to refine flavor profiles and packaging formats using real-time consumer sentiment analysis from reviews and social media engagement.

Increased demand for “better-for-you” instant tea premixes

Health-conscious consumers are increasingly scrutinizing ingredient lists, driving a shift toward natural sweeteners like stevia and monk fruit. The U.S. Food and Drug Administration's ongoing evaluation of food additive safety encourages manufacturers to proactively remove controversial ingredients, even in markets with lenient regulations. Brands are incorporating functional ingredients such as vitamin C, zinc, and probiotics into instant tea premixes, positioning them as immunity-boosting beverages rather than mere refreshers. In 2024, the Food Safety and Standards Authority of India updated its nutraceutical regulations, providing a framework for health claims on fortified instant tea products, legitimizing their functional positioning in one of the world's largest tea-consuming nations. Organic certification, which raises retail prices by 15-25%, appeals to affluent consumers in North America and Europe who associate organic labels with superior quality and environmental stewardship, despite limited scientific evidence to differentiate the nutritional profiles of organic and conventional tea.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and labelling complexity | -0.9% | Global, most acute in EU and North America with stringent food safety frameworks | Medium term (2-4 years) |

| Supply chain and sourcing challenges | -0.8% | Global, concentrated in tea-producing regions (India, Kenya, China, Sri Lanka) with climate vulnerability | Short term (≤ 2 years) |

| Artisanal and functional beverages pose stiff competition | -0.7% | North America and Europe premium segments, emerging in APAC affluent demographics | Long term (≥ 4 years) |

| Price sensitivity with premium products | -0.6% | APAC developing markets, South America, MEA price-conscious segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory and labelling complexity

Regulatory compliance complexities are posing significant challenges for market entry and operations. For instance, FDA mandates comprehensive labeling for tea packaging, including identity statements, content declarations, and nutritional information. Across markets, regulatory landscapes differ markedly. Take FSSAI, for example: it stipulates varying license types based on annual turnover, Basic for under INR 12 lakhs, State for INR 12 lakhs to INR 20 crores, and Central for above INR 20 crores. This creates a compliance maze for manufacturers navigating multiple jurisdictions. Labeling disputes have emerged as notable legal risks[1]Source: Food Safety and Standards Authority of India, "FSSAI Food License Registration for Tea Powder Manufacturers", fssai.gov.in. A case in point is PepsiCo's class action lawsuit concerning Pure Leaf's "Brewed in USA" claims, which faced scrutiny due to overseas tea leaf sourcing. This underscores the heightened consumer sensitivity to transparency regarding product origins. International trade regulations further complicate matters. Imported tea products must adhere to the FDA's prior notice and tariff regulations, all while meeting the same safety standards as their domestic counterparts. Moreover, health claim substantiation is tightening. Regulatory bodies now demand robust scientific evidence for claims related to disease risk reduction. This escalation in scrutiny translates to increased compliance costs and elongated development timelines. Notably, these regulatory challenges weigh heavily on smaller manufacturers. Lacking the resources for exhaustive compliance programs, they risk ceding market share to larger players adept at navigating the regulatory landscape.

Supply chain and sourcing challenges

Climate change is fundamentally disrupting tea supply chains, with Indian production falling to 90.92 million kgs in May 2024, the lowest in over a decade, due to extreme weather events including heatwaves and floods. Even a modest temperature rise of 1 degree Celsius can lead to a minimum 5% drop in tea productivity. Furthermore, geopolitical tensions in areas like the Red Sea are unsettling established trade routes, amplifying vulnerabilities in the supply chain. For manufacturers of instant tea premixes, the challenge of relocating tea production to alternative regions is exacerbated by time lags and the specific requirements of tea cultivation, heightening concerns over supply security. Adding to the complexity, 60% of the world's tea is produced by smallholder farmers, many of whom grapple with the dual challenges of climate adaptation and the push for sustainable practices[2]Source: International Institute for Sustainable Development, "Global Tea Production Continues To Grow, Though The Gap In Demand Narrowed As The Covid-19 Pandemic Fuelled Consumption", iisd.org. These farmers often lack the necessary support, making sustainability compliance a costly endeavor. Price fluctuations in the tea market are exerting pressure on profit margins. With potential price hikes of up to 20% due to supply disruptions, manufacturers are increasingly turning to advanced hedging strategies and diversifying their supplier base. As climate-related stresses impact the quality of tea leaves and their bioactive compounds, challenges in quality control are mounting. This necessitates more rigorous testing protocols and robust supplier certification programs to ensure consistency in instant tea premix formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Leadership Challenged by Liquid Innovation

In 2025, powder formats captured a dominant 62.23% of the market share, leveraging lightweight packaging to cut shipping costs and ambient storage to sidestep cold chain demands. These powder formats are ideal for single-serve sachets, prioritizing portion control and longevity over quick dissolution. This is especially beneficial in regions with limited refrigeration. Within the powder category, granulated variants boast better flowability and less clumping than their fine counterparts. However, they do come with a trade-off: a slightly extended dissolution time that some consumers might find less convenient.

Liquid concentrates are poised for an 8.21% CAGR surge through 2031, fueled by their growing adoption in the foodservice sector. Here, the emphasis on portion control and consistent flavor delivery justifies the higher per-unit costs. Addressing past shelf life concerns that hindered the liquid format's uptake, the National Research Development Corporation of India unveiled a ready-to-serve tea concentrate technology. This innovation ensures flavor stability for six months at ambient temperatures. Finlays, a tea processor with estates in Kenya, China, and Chile, is supplying these liquid concentrates to café chains. While innovations like aseptic pouches and bag-in-box systems are extending the shelf life of liquid concentrates and preserving their polyphenol content, these advanced packaging formats are still seen as too pricey for the budget-conscious retail segment.

By Category: Conventional Dominance Amid Organic Acceleration

In 2025, conventional instant tea premixes captured a dominant 85.43% of the market share, bolstered by competitive pricing and well-established distribution networks in mass-market retail. These conventional products benefit from economies of scale, sourcing commodity-grade tea leaves from major estates in Kenya, Sri Lanka, and Assam, India. This strategic sourcing allows them to price retail products 30-40% lower than their organic counterparts. In foodservice settings, where cost per serving is paramount, conventional variants reign supreme. Here, consumers show a diminished inclination to pay a premium for organic certification, especially during out-of-home dining experiences.

From 2026 to 2031, organic instant tea premixes are projected to grow at a robust 7.01% CAGR, outpacing the broader market. This growth is driven by tightening regulations on pesticide residues and a surge in consumer health consciousness. The Tea Board of India noted a rise in organic tea imports for the 2024-2025 period, underscoring a robust domestic appetite for internationally certified products. While the instant processing methods, like industrial spray-drying or freeze-drying, might raise eyebrows among purists, many environmentally conscious consumers still gravitate towards organic certification. They link chemical-free farming to benefits like biodiversity preservation and diminished water pollution. This premium positioning empowers organic brands to set prices 50-70% higher in specialty retail and e-commerce platforms. Such pricing strategies resonate with affluent consumers in North America and Western Europe, regions where organic foods account for over 10% of grocery sales.

By Flavor: Flavored Variants Drive Market Leadership and Growth

In 2025, flavored instant tea premixes dominated the market with a 73.42% share and are projected to expand at a 6.98% CAGR through 2031. This growth is driven by ongoing innovations in botanical blends and functional ingredients. While lemon and peach lead in volume, newer entrants are introducing turmeric, ginger, hibiscus, and elderflower, aiming to stand out with health benefits and sensory appeal. In 2025, the China Ministry of Agriculture highlighted a surge in domestic interest for matcha-flavored instant premixes, underscoring consumers' readiness to pay a premium for authenticity and antioxidant benefits. Flavored variants allow manufacturers to mask the astringency and bitterness often found in unflavored instant teas, especially those derived from lower-grade tea dust and fannings instead of whole leaves.

Unflavored instant tea premixes cater to purists who value the genuine tea taste and to institutional buyers prioritizing cost over flavor complexity. These products resonate with consumers who prefer to customize their drinks with sweeteners, milk, or lemon, thus controlling the final taste rather than relying on the manufacturer's choice. In certain Asian and Middle Eastern cultures, unflavored variants align with traditional tea practices, where spices or herbs are added during consumption, not pre-mixed. Yet, unflavored options are increasingly challenged by premium loose-leaf teas and tea bags, as discerning consumers question if instant processing can truly match their desired authentic flavor experience.

By Packaging: Single-Serve Convenience Meets Sustainable Innovation

In 2025, single-serve sachets and sticks captured a dominant 41.35% share of the market, particularly excelling in on-the-go consumption and institutional settings. Their portion-controlled design minimizes waste, making them ideal for airlines, hotels, and office pantries. These individual servings not only eliminate the need for measuring tools but also curtail pilferage, a common issue with bulk containers. Furthermore, sachets offer flavor variety packs, enabling consumers to sample multiple variants without the commitment of large quantities. This feature significantly lowers the trial barriers for new product launches.

From 2026 to 2031, pouches are projected to grow at a robust 9.21% CAGR, driven by resealable standup formats that combine convenience with multi-serve functionality for households. Flexible packaging innovations reduce material usage compared to rigid jars and canisters, appealing to environmentally conscious consumers and manufacturers aiming to cut packaging costs and carbon footprints. Pouches hold larger volumes than sachets while occupying less shelf space than jars, optimizing retail display efficiency and household storage. However, they face perception challenges in premium markets, where glass jars and metal tins signal quality and giftability, limiting their adoption for high-end organic and specialty products. Jars and canisters remain relevant for bulk purchases in price clubs and wholesale channels, while tins are preferred for gifting and premium positioning despite higher material costs.

By Distribution Channel: Retail Dominance Amid Foodservice Acceleration

In 2025, retail channels, including supermarkets, hypermarkets, convenience stores, online platforms, and specialty outlets, held a dominant 63.88% market share. Supermarkets and hypermarkets, with their mass-market reach, leverage end-aisle displays and temporary price cuts to entice price-sensitive shoppers. Online platforms capitalize on subscription models and tailored recommendations, appealing to consumers who value convenience and prefer a 1-2 day delivery over immediate in-store purchases. Specialty stores, targeting the premium and organic market, employ knowledgeable staff to educate consumers on product origins, processing methods, and health benefits, justifying higher price points.

Foodservice and HoReCa sectors are projected to grow at a 7.26% CAGR through 2031. Café chains increasingly adopt instant premixes to standardize flavors, reduce labor costs, and improve efficiency during peak hours. A USDA Foreign Agricultural Service report highlighted that in Burma, hotels, restaurants, and cafés are adopting instant beverage solutions to meet rising consumer demand for quick service while maintaining perceived quality. European foodservice operators, like Moka Professional and Bicom, use instant tea concentrates to eliminate inconsistencies from manual brewing while offering diverse hot and cold tea options. Quick-service restaurants leverage instant premixes to introduce seasonal flavors, enabling rapid menu innovation without investing in new brewing equipment or extensive staff training. However, specialty tea houses and upscale restaurants resist this trend, valuing freshly brewed tea as a differentiator and fearing instant formats could dilute their premium image.

Geography Analysis

In 2025, Asia-Pacific holds a 51.31% share of the global instant tea premixes market, driven by strong tea consumption traditions, well-established supply chains, and increasing disposable incomes in key countries such as China, India, Japan, and Australia. The region's dominance is attributed to its cultural connection to tea, rapid urbanization, and a growing preference for convenient beverage options. China leads the market within Asia-Pacific, with consumer behavior segmented into four groups: Confident Early Adopters, Early Adopters, Late Adopters, and Cautious Laggards. Younger, educated, and higher-income consumers are the primary drivers of innovation adoption in the country. As per the National Bureau of Statistics of China, the average annual per capita disposable income for Chinese households reached approximately 43,377 yuan in 2025, up from 39,218 in 2023, signaling heightened demand[3]Source: National Bureau of Statistics of China, "Average annual per capita disposable income of households in China from 1990 to 2024", stats.gov.cn.. In India, regulatory frameworks like FSSAI licensing and domestic production capabilities shape the market. However, climate-related challenges have caused a 30% decline in production in 2024 compared to 2023. Vietnam's tea market emphasizes quality through traceability and OCOP certification, with consumers favoring products with higher certifications but showing reluctance toward online purchases.

The Middle East and Africa are on track to achieve a CAGR of 7.12% through 2031. This growth is driven by urban population expansion, heightened health awareness, and a burgeoning café culture in nations such as Saudi Arabia, UAE, South Africa, and Nigeria. With the MENA branded coffee shop market set to grow to 11,163 outlets in 2024, there's a surge in distribution opportunities for instant tea premixes. The region's youthful demographic, armed with rising disposable incomes and global beverage trend exposure via digital media and travel, further fuels this growth. Manufacturers eyeing success in these markets are tailoring products to resonate with local tastes and consumption habits, all while honoring religious and cultural norms.

North America and Europe, boasting mature markets with established consumption patterns and sophisticated distribution networks, focus on premium product positioning, health benefits, and sustainability. North America leads the fruit and herbal tea segment, supported by strong marketing and a health-conscious consumer base. European markets prioritize organic certifications and ethical sourcing. Both regions face supply chain challenges due to climate change's impact on traditional tea-producing nations, creating opportunities for alternative sourcing strategies and technological innovations. Regulatory complexities in these markets require comprehensive compliance programs, which enhance consumer trust through quality assurance. Growth is driven by rising demand for functional beverages offering specific health benefits. South America, with its growing middle class and increased exposure to global beverage trends, presents a promising opportunity. However, unlocking this potential requires significant investments in distribution infrastructure and consumer education.

Competitive Landscape

The instant tea premix market is moderately concentrated, with a handful of established players like Nestlé S.A., Unilever plc, Tata Consumer Products Limited, Girnar Food and Beverages Pvt. Ltd., Gujarat Tea Processors and Packers Limited (GTPPL) holding significant market shares. Leveraging strong brand equity, expansive distribution networks, and a commitment to continuous product innovation, these companies maintain a competitive edge. Meanwhile, regional brands and newcomers are carving out niches with unique flavors and functional blends, responding to shifting consumer tastes. This interplay of established dominance and emerging diversity fosters robust competition and spurs product differentiation.

Opportunities abound in personalized nutrition, eco-friendly packaging, and tapping into burgeoning markets, especially in the rapidly growing café cultures of the Middle East and Africa. New challengers are upending traditional models, utilizing direct-to-consumer strategies, forging partnerships with specialty retailers, and positioning their products as artisanal and health-focused. The landscape is further shifting as companies like TreeHouse Foods pursue vertical integration, acquiring private-label tea manufacturers to bolster their blending and sourcing prowess.

Patent activity is surging in processing technologies, highlighted by Unilever's global patent for "tea juice" extraction, marking a leap in flavor enhancement and product uniqueness. As climate change poses sourcing hurdles, companies are turning supply chain resilience into a competitive edge. They're diversifying supplier networks and championing sustainable sourcing to guarantee consistent product quality and availability.

Instant Tea Premix Industry Leaders

-

Nestlé S.A.

-

Unilever plc

-

Tata Consumer Products Limited

-

Girnar Food and Beverages Pvt. Ltd.

-

Gujarat Tea Processors and Packers Limited (GTPPL) (Wagh Bakri)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Jivraj9 launched a new TVC with Neena Gupta on instant tea mix convenience. The film, featuring brand ambassador Neena Gupta, marks the third TVC in the campaign and focuses on the ease of enjoying homemade-style chai in 30 seconds.

- May 2025: Kaytea introduced a new range of instant iced tea powder products, aiming to bring 'next generation hydration' to the United Kingdom market. The powders were available in three flavours – Peach & Mango, Lemon, and Classic Milk Tea. According to the brand, the new products are designed for easy preparation; the pre-blended powders could simply be stirred into hot water and topped with ice or mixed with cold water in a blender.

- May 2025: Continental Coffee has expanded its tea premix line with the launch of its new Lemon Iced Tea Premix. According to the brand, it is available in both 400g pouches and 140g stick packs, targeting convenience and ready-to-drink trends.

Global Instant Tea Premix Market Report Scope

| Conventional |

| Organic |

| Powder |

| Granules |

| Liquid Concentrate |

| Flavored |

| Unflavored |

| Single-Serve Sachets/Sticks |

| Jars/Canisters |

| Pouches |

| Tins |

| Bulk Packs |

| Foodservice/HoReCa | |

| Retail | Supermarkets/ Hypermarkets |

| Convenience Stores | |

| Online retail stores | |

| Specialty Stores | |

| Other distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Conventional | |

| Organic | ||

| By Form | Powder | |

| Granules | ||

| Liquid Concentrate | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Packaging | Single-Serve Sachets/Sticks | |

| Jars/Canisters | ||

| Pouches | ||

| Tins | ||

| Bulk Packs | ||

| By Distribution Channel | Foodservice/HoReCa | |

| Retail | Supermarkets/ Hypermarkets | |

| Convenience Stores | ||

| Online retail stores | ||

| Specialty Stores | ||

| Other distribution channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for instant tea premixes be by 2031?

It is forecast to hit USD 2.73 billion, reflecting a 6.82% CAGR from 2026-2031.

Which region contributes most sales today?

Asia-Pacific leads at 51.31% of 2025 revenue thanks to entrenched tea culture and urban convenience trends.

What is the fastest-growing form factor?

Shelf-stable liquid concentrates are projected to grow at 8.21% CAGR as foodservice chains demand precise portion control.

Which distribution channel is rising quickest?

Foodservice and HoReCa outlets are pacing at a 7.26% CAGR because standardized premixes raise throughput and cut training costs.

Page last updated on: