Insect Pest Control Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

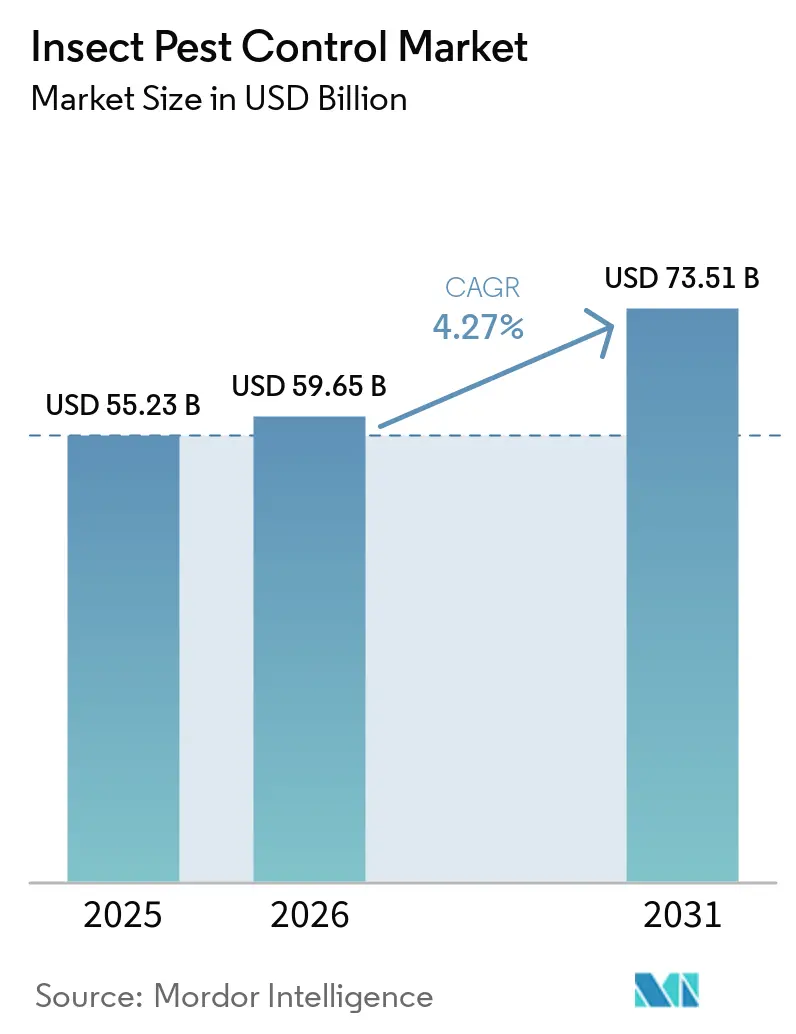

| Market Size (2026) | USD 59.65 Billion |

| Market Size (2031) | USD 73.51 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insect Pest Control Market Analysis by Mordor Intelligence

The insect pest control market size is anticipated to increase from USD 55.23 billion in 2025 to USD 59.65 billion in 2026 and reach USD 73.51 billion by 2031, growing at a CAGR of 4.27% over 2026-2031. The insect pest control market is being shaped by persistent crop-loss risk, as insect pests still destroy 20-40% of global crop output annually, as per the Food and Agricultural Organization, which keeps control spending essential across major farming systems. The insect pest control market is also moving toward lower-residue programs as the United States Environmental Protection Agency (EPA) tightened mitigation rules in 2025, and several export-oriented crop chains are placing greater emphasis on residue compliance. Biological products are gaining a larger role in crop protection, particularly in Brazil, where the bioinputs market reached USD 1.1 billion (BRL 6.2 billion) in 2025, according to CropLife Brasil, reflecting continued expansion in biologically treated acreage and the adoption of integrated pest management [1]Source: CropLife Brasil, “Mercado de Bioinsumos Cresce em Valor e Área Tratada em 2025,” croplifebrasil.org. Suppliers are increasingly aligning their insect control portfolios with integrated crop systems that incorporate foliar, seed-applied, and biological solutions into a unified farm management approach. This trend was highlighted by Pro Farm Group’s 2025 United States Environmental Protection Agency (EPA) registration of its RinoTec biological insecticide and nematicide platform, along with broader industry investments in multi-mode pest management systems aimed at addressing resistance pressure, residue limits, and application flexibility concurrently.

Key Report Takeaways

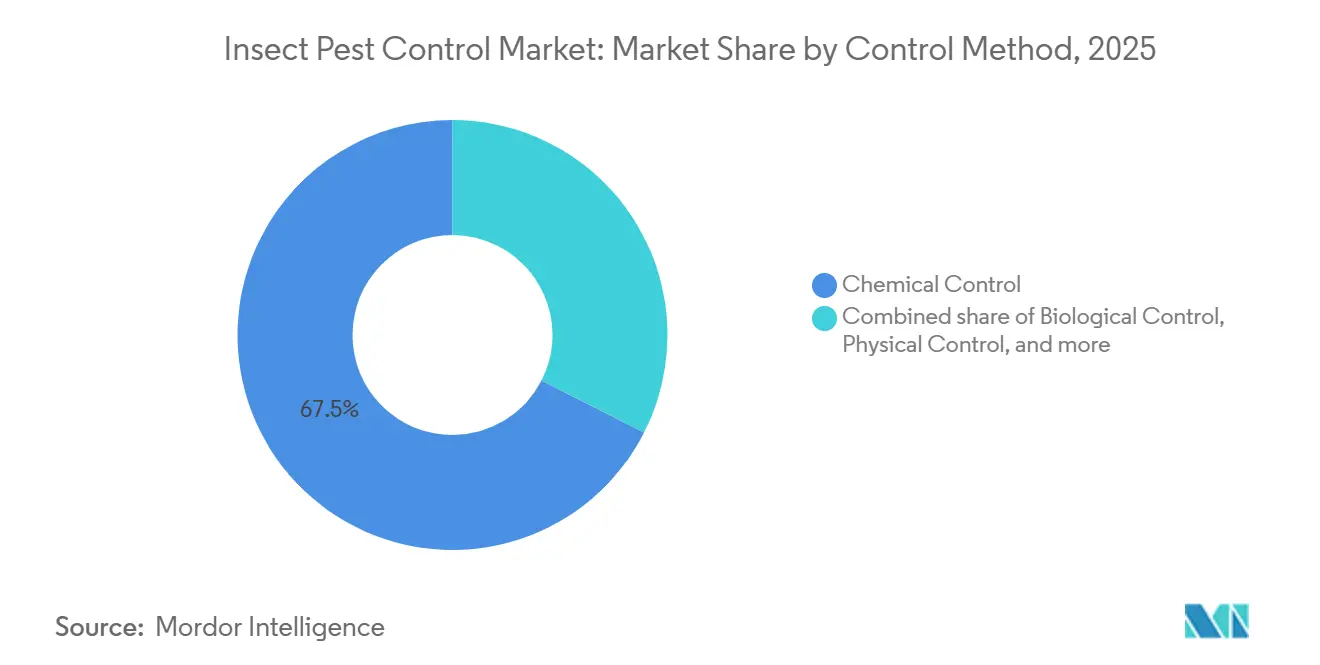

- By control method, chemical control was the largest segment, accounting for 67.5% of the insect pest control market share in 2025, while biological control is the fastest-growing segment at a projected 6.3% CAGR during 2026-2031.

- By crop type, grains and cereals were the largest segment, accounting for 41.1% of the insect pest control market size in 2025, while fruits and vegetables will be the fastest-growing segment at a forecasted CAGR of 5.9% during 2026-2031.

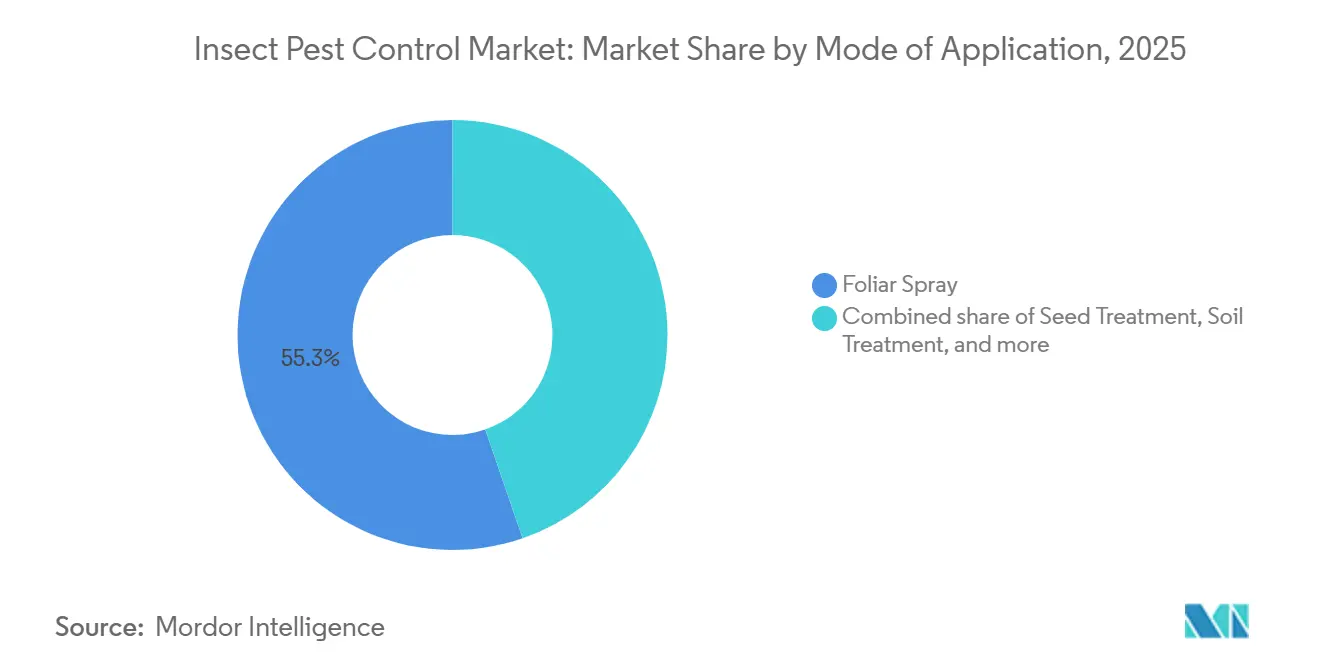

- By mode of application, foliar spray was the largest segment, with a 55.3% revenue share in 2025, while seed treatment is the fastest-growing segment, with a projected 5.1% CAGR during 2026-2031.

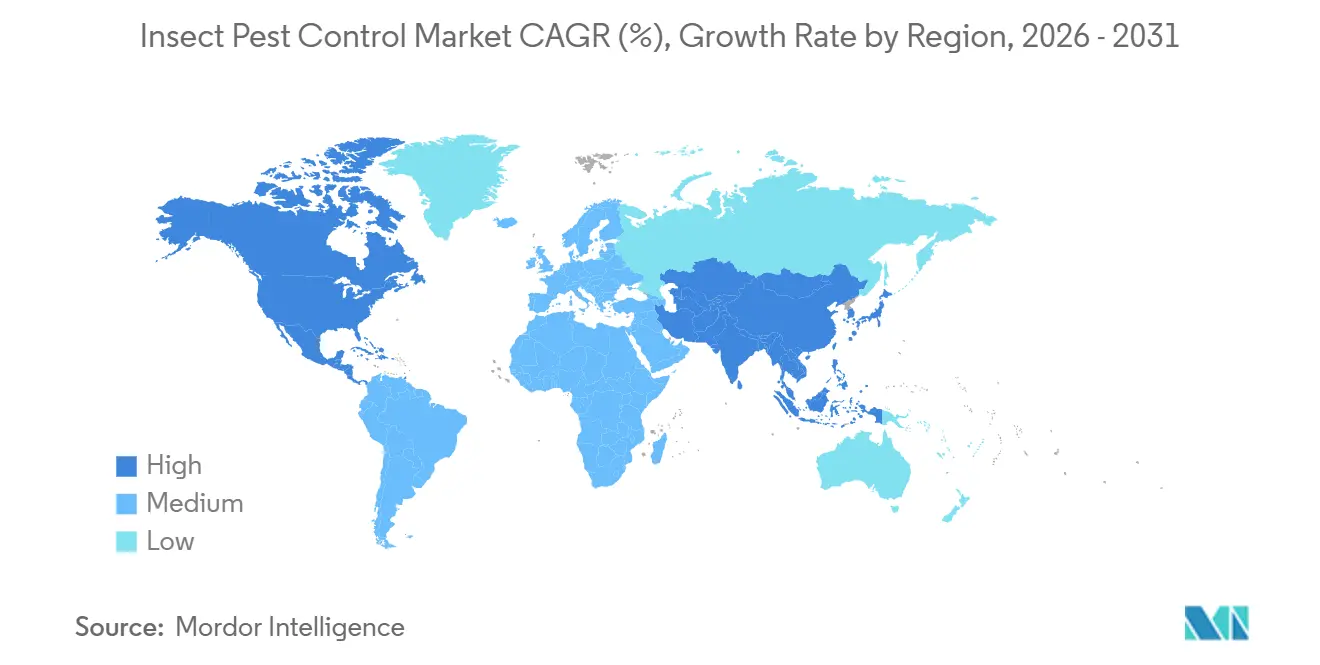

- By geography, North America was the largest segment with 37.6% revenue share in 2025, while Asia-Pacific will be the fastest segment at a 5.6% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Insect Pest Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising insect pressure and crop-Loss risk | +1.2% | Global, strongest in Africa, Asia-Pacific, and South America | Short term (≤ 2 years) |

| Regulatory and retailer push for lower-residue programs | +0.8% | North America and Europe, expanding into export-oriented Asia-Pacific and South America | Medium term (2–4 years) |

| Fast adoption of biological control and bioinsecticides | +1.0% | Global, led by Brazil and China | Medium term (2–4 years) |

| Precision scouting, drones, and AI improve treatment timing | +0.6% | North America and China with rising digital agriculture adoption | Medium term (2–4 years) |

| Protected-crop and nursery expansion lifts biocontrol demand | +0.5% | North America, Europe, Middle East, and Asia-Pacific horticulture hubs | Long term (≥ 4 years) |

| Seed-treatment and insect-protection trait stacking | +0.5% | North America and Brazil, especially in large row-crop systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Insect Pressure and Crop-Loss Risk

Global crop production continues to face severe pressure from insect-driven yield losses, which remain one of the most persistent threats to farm profitability. In 2025, the Crop Protection Network anticipated that invertebrate pests reduced corn yields by 4.0% across 29 United States states during the 2024 season, resulting in losses exceeding 610 million bushels, demonstrating the continuing economic burden of insect infestations on modern agriculture. This keeps insect control spending hard to defer even when farm margins tighten, because yield protection remains central to grower economics. The insect pest control market also gains from the rising need to manage multiple pest species within the same season, especially in crops with repeated infestation cycles. That pattern supports a stronger demand for broad programs and favors suppliers that can offer several modes of action within the same insect pest control market.

Regulatory and Retailer Push for Lower-Residue Programs

Tighter environmental oversight and stricter retailer standards are accelerating the shift toward more selective and lower-residue insect control programs. The United States Environmental Protection Agency (EPA) finalized its Insecticide Strategy on April 29, 2025, covering nearly 83 million treated acres and requiring mitigation measures such as spray-drift buffers and runoff controls. In Europe, compliance pressure remains high as pesticide use and documentation receive closer scrutiny, including the broader shift toward digital recording and traceability in farm practices[2]Source: Umweltbundesamt, “Plant Protection Products in Agriculture,”umweltbundesamt.de. This raises the value of products that fit integrated pest management (IPM) programs and creates more room for biologicals, pheromone tools, and selective chemistry. The insect pest control market, therefore, shows a clear split between premium programs built around compliance and commodity programs that face greater substitution pressure.

Fast Adoption of Biological Control and Bioinsecticides

Biological crop protection is moving from a niche segment into a mainstream component of modern insect management programs. China’s National Agricultural Technology Extension and Service Center (NATESC) included biological control and rotation programs in its national technical plans for both 2025 and 2026. Syngenta Group launched WeevilTrak Plus, featuring Atexzo insecticide (IRAC Group 30) for turf insect management, simplifying annual bluegrass weevil control programs while improving resistance management and expanding control against billbugs and turf caterpillars. The development highlights how suppliers are increasingly combining novel active ingredients, rotational strategies, and integrated pest management approaches to reduce dependence on conventional single-mode insecticide programs. This trend is changing the insect pest control market by giving growers more practical rotation options when resistance, residue, and export requirements limit the use of conventional chemistry.

Precision Scouting, Drones, and AI Improve Treatment Timing

Precision agriculture technologies are reshaping insect control practices by improving how outbreaks are detected, timed, and treated across large-scale farming systems. China has emerged as one of the strongest examples of this transition, operating more than 250,000 agricultural drones by 2025 and formally incorporating drone-based pheromone dispensing and aerial delivery of biological agents into its 2025 and 2026 national crop pest-control plans. Similar precision-application trends are expanding across North America, Europe, and parts of South America as labor shortages, resistance management, and input-efficiency pressures intensify. This shift supports stronger demand for premium insect-control programs that combine chemistry, biologicals, monitoring tools, and application support within integrated crop-protection systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resistance to legacy chemistries | -0.80% | Global, strongest in Europe, North America, Brazil, India, and China | Short term (≤ 2 years) |

| Registration and MRL pressure on active ingredients | -0.50% | United States, Europe, and Japan, especially in export-oriented crop systems | Medium term (2–4 years) |

| Generic erosion of blockbuster insecticides | -0.60% | North America, South America, China, and India | Short term (≤ 2 years) |

| Shelf-life and field-performance variability in biologicals | -0.40% | South America, Africa, and South Asia with weaker storage infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Resistance to Legacy Chemistries

The insect pest control market faces a clear limit due to rising resistance to older chemistries across several key pest complexes. The official 2026 integrated pest management guidance in Baden-Württemberg reported super-kdr resistance in oilseed rape flea beetle populations in the Rhine Plain and Kraichgau regions of Germany and advised growers to use alternative active ingredients in those hotspots. This raises program costs because growers need rotations, mixtures, and newer active ingredients instead of lower-cost repeat applications. It also shortens the commercially useful life of established products and increases the importance of novel modes of action, such as Syngenta Group’s IRAC group 30 insecticides [3]Source: Syngenta US, “Syngenta Announces Foliar Brand Names for In-Season Insect Management Portfolio in the U.S.,” Syngenta US Newsroom, syngenta-us.com. The result is that the insect pest control market keeps growing, but legacy products within it face a harder path to stable volume and pricing.

Registration and MRL Pressure on Active Ingredients

The insect pest control market is constrained by longer registration timelines and stricter residue and use conditions on established active ingredients. The United States Environmental Protection Agency (EPA) final Insecticide Strategy introduced a structured mitigation framework in 2025 that narrows use flexibility for some conventional products. Bayer AG stated that the expiry of the Movento registration in Europe was a key factor behind its 12.2% decline in insecticide sales in 2025, on a currency- and portfolio-adjusted basis. These conditions raise defense costs for product portfolios and favor larger companies that can fund re-registration, stewardship, and data generation at scale. The insect pest control market, therefore, remains attractive, but the regulatory burden makes it harder for smaller regional suppliers to keep broad active ingredient coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Control Method: Chemical Scale Meets Biological Momentum

Chemical control accounted for 67.5% of the insect pest control market share in 2025, maintaining its position as the largest segment by a wide margin. This position reflects its long record in broad-acre crops, strong distribution coverage, and the ability to address many pest complexes across grains, cotton, oilseeds, and plantation crops. The chemical side of the insect pest control industry also remains commercially important because newer synthetic molecules still command higher pricing than older generic classes. Biological control is the fastest-growing segment, with a 6.3% CAGR during 2026-2031, indicating that growth is shifting toward programs built around residue management and resistance rotation. China’s 2025 and 2026 technical plans provided additional policy support for biological rotations, thereby strengthening adoption in one of the world's largest crop protection systems.

Bayer AG expanded its biological crop protection platform through a new multi-year partnership with Ginkgo Bioworks to accelerate the development of microbial products for pest management and sustainable agriculture applications. The practical outcome is that the insect pest control market is no longer simply separating chemical and biological programs, because many growers now use both within the same seasonal plan. That mixed model should maintain the chemical scale while enabling biological products to capture a larger share of the fastest-growing segment of the insect pest control market.

By Crop Type: High-Value Produce Drives Complexity Premium

Grains and cereals accounted for 41.1% of the insect pest control market in 2025 and remained the largest crop segment, driven by their large planted area and recurring pest pressure. A 2025 study published in Frontiers in Agronomy found that Fall Armyworm infestations across sub-Saharan Africa continue to cause annual economic losses of up to USD 13 billion in maize, rice, sorghum, and sugarcane production, highlighting the scale of economic risk in cereal production systems. Corteva Agriscience reported USD 1,669 million in insecticide sales in 2025, reflecting its strong exposure to row-crop systems such as corn and soybean. Plantation crops add steady demand, where export sensitivity and intensive monocropping raise the need for structured insect control programs.

Fruits and vegetables are the fastest-growing crop segment, with a 5.9% CAGR during 2026-2031, driven by residue sensitivity and protected cultivation, which favor more complex programs. ADAMA Agricultural Solutions Ltd. launched Ateka insecticide in the United States in March 2026 for sucking pests in fruit and vegetable crops, underscoring the company's commercial focus on horticulture. The crop profile of the insect pest control industry becomes more attractive as growers move from yield-only decisions toward yield-plus-residue compliance and shorter pre-harvest intervals. That shift gives biologicals and selective chemistry more room in high-value produce than in large commodity crops. For that reason, the insect pest control market is seeing the most rapid crop-level change in fruits and vegetables, even though grains and cereals still hold the largest base.

By Mode of Application: Foliar Scale, Seed-Applied Speed

Foliar spray accounted for 55.3% of the insect pest control market in 2025 and remained the largest application mode, as it fits nearly every crop system and supports both chemical and biological products. Foliar programs remain central in the insect pest control market because growers can respond quickly to visible infestations and adjust treatment choices by crop stage and pest mix. Seed treatment is the fastest-growing mode, with a 5.1% CAGR during 2026-2031, as more growers prefer early-season preventive control and tighter integration with planting schedules. Syngenta Group’s Equento and Opello products show how suppliers are extending insect control value into seed and at-planting positions. Soil treatment also remains relevant for crops exposed to root-feeding and soil-dwelling pests that foliar products cannot effectively address.

Biological innovation adds flexibility across application modes rather than staying in a single narrow channel. Pro Farm Group’s RinoTec Technology received United States Environmental Protection Agency (EPA) registration in 2025 as a biological insecticide and nematicide platform designed for both soil and foliar pest control applications across row and specialty crops. BioWorks Inc. also received United States Environmental Protection Agency (EPA) approval in 2025 for PRINCIPLE WP, a Beauveria bassiana-based biological insecticide labeled for foliar spray, soil drench, dipping, and aerial applications. These approvals reflect the broader expansion of biological insect-control tools into mainstream commercial agriculture programs.

Geography Analysis

North America accounted for 37.6% of the insect pest control market share in 2025, making it the largest regional segment. The region benefits from established integrated pest management systems, high adoption of premium chemistry, and a strong pipeline of biological and seed-applied products. The United States Environmental Protection Agency (EPA) final Insecticide Strategy in 2025 strengthened the case for precision-applied and lower-residue programs across nearly 83 million treated acres. Europe remains an important high-value region where regulatory attrition and more stringent documentation standards are changing the product mix faster than the total treated area, supporting continued substitution toward selective chemistry and biological tools.

Asia-Pacific is the fastest-growing regional segment, with a 5.6% CAGR during 2026-2031, and remains central to future demand expansion in the insect pest control market. China is a major driver because its 2025 and 2026 major crop pest plans formalized biological control plus rotation programs, and projected very large pest incidence across rice and corn systems. This gives the region a strong mix of volume demand, policy-backed biological adoption, and rising crop intensity. South America remains a potential growth region for insect pest control due to the expansion of soybean and corn acreage in Brazil and Argentina, which has increased the number of insect treatment cycles required per season. Brazil’s National Supply Company (CONAB) has projected a record soybean harvest for the 2025/26 season of 180.1 million metric tons, driving demand for caterpillar, stink bug, and sucking-pest control programs in large-scale row-crop systems. Additionally, pest resistance is prompting growers to adopt rotational insecticide programs, seed treatments, and biological insect-control solutions.

The Middle East and Africa remain smaller in absolute terms, but both offer significant growth opportunities in the insect pest control market. Protected cultivation in Gulf countries and Turkey is widening the addressable base for biological and low-residue insect management in vegetables, ornamentals, and nursery crops. Africa has strong long-term demand because invasive pest pressure remains high, particularly in maize and other staple crops. Andermatt Africa announced a 2025 partnership with Provivi to develop and distribute next-generation pest control solutions in East Africa, which signals rising commercial interest in pheromone-based systems for smallholder agriculture.

Competitive Landscape

The insect pest control market is fragmented, featuring major multinational suppliers alongside regional and biological control companies. In 2025, Syngenta Group reported Crop Protection sales of USD 13.7 billion, while FMC Corporation generated approximately USD 1.6 billion from insecticide products. Other major participants, including Bayer AG, BASF SE, and Corteva Agriscience, also maintained significant global positions in insect pest management, highlighting the commercial scale and competitive depth of the insect pest control market.

Recent strategies have focused on addressing biological portfolio gaps, protecting premium chemistry, and expanding crop cycle control options. BASF SE acquired AgBiTech in 2026, strengthening its biological insect control presence in the United States, Australia, and Brazil. In 2025, Corteva Agriscience launched Goltrevo and Varpelgo, showcasing the integration of biologicals and nature-inspired chemistry. FMC Corporation expanded its diamide-based insecticide portfolio and precision application partnerships in 2025 and 2026 to enhance resistance management in row crops and specialty agriculture. These developments show that competition now centers on portfolio breadth across conventional chemistry, biologicals, seed treatments, and integrated crop-protection systems.

Competitive positioning in the insect pest control industry is increasingly defined by the gap between innovation-driven companies and suppliers that depend more heavily on post-patent portfolios. Biotalys NV reached the first research milestone in its partnership with Syngenta Group in April 2026 for protein-based bioinsecticides, underscoring the continued value of its proprietary discovery platforms. At the same time, FMC Corporation’s annual report makes clear that generic erosion in diamides is already affecting lower-specification channels. This means the insect pest control market rewards innovation but also punishes slow portfolio renewal as patent protection fades. Competitive pressure is therefore rising most quickly in the overlap between mainstream crop protection companies and established biological specialists such as Koppert Biological Systems and Andermatt Group AG.

Insect Pest Control Industry Leaders

BASF SE

Bayer AG

Syngenta AG

FMC Corporation

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: BASF SE commissioned its new BioHub fermentation plant in Ludwigshafen, Germany, to manufacture the biological building block for Inscalis insecticide, derived from Penicillium coprobium, and biological fungicides, strengthening supply chain resilience for its growing biosolutions portfolio.

- April 2026: Biotalys NV achieved the first research milestone in its bioinsecticide partnership with Syngenta Group, using AGROBODY technology to produce protein-based biocontrols targeting resistant insect populations, with initial laboratory tests showing promising in vitro results against key insect molecular targets.

- April 2026: India’s Central Insecticides Board and Registration Committee granted regulatory approval to Peptech Biosciences for its BTK 10% water-soluble liquid insecticide used to control Helicoverpa armigera in red gram crops. Developed using technology from the National Bureau of Agricultural Insect Resources, the product offers easy application and helps reduce residue-related concerns for farmers.

Global Insect Pest Control Market Report Scope

The insect pest control market includes chemical, biological, and physical products used to prevent, suppress, or eliminate insect damage across agricultural crops and controlled growing systems. It covers foliar, seed, soil, fumigation, and related application modes used in grains and cereals, fruits and vegetables, oilseeds and pulses, plantation crops, turf and ornamentals, across all major regions. The Insect Pest Control Market is Segmented by Control Method (Chemical, Biological, Physical), by Crop Type (Grains and Cereals, Fruits and Vegetables, Oilseeds and Pulses, and More), by Mode of Application (Foliar Spray, Seed Treatment, Soil Treatment, and More), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). Market Forecasts in Value (USD).

| Chemical Control |

| Biological Control |

| Physical Control |

| Grains and Cereals |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Plantation Crops |

| Turf and Ornamentals |

| Foliar Spray |

| Seed Treatment |

| Soil Treatment |

| Chemigation |

| Fumigation and Space Treatment |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Control Method | Chemical Control | |

| Biological Control | ||

| Physical Control | ||

| By Crop Type | Grains and Cereals | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Plantation Crops | ||

| Turf and Ornamentals | ||

| By Mode of Application | Foliar Spray | |

| Seed Treatment | ||

| Soil Treatment | ||

| Chemigation | ||

| Fumigation and Space Treatment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the insect pest control market?

The insect pest control market is valued at USD 59.65 billion in 2026 and is projected to reach USD 73.51 billion by 2031 at a 4.27% CAGR during 2026-2031.

Which control method holds the largest share?

Chemical control is the largest segment, with 67.5% share in 2025, although biological control is growing faster at a 6.3% CAGR during 2026-2031.

Which crop group is expanding the fastest?

Fruits and vegetables are the fastest crop segment at a 5.9% CAGR during 2026-2031 because residue-sensitive export chains and protected cultivation favor more selective programs.

Which region leads global demand?

North America is the largest regional segment with 37.6% share in 2025, while Asia-Pacific is the fastest regional segment at a 5.6% CAGR during 2026-2031.

How concentrated is competition among suppliers?

The insect pest control market was fragmented in 2025, which means scale matters, but the space still leaves meaningful room for regional suppliers, generics companies, and biological specialists.

Page last updated on: