China Insecticide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Insecticide Market Analysis by Mordor Intelligence

The China insecticide market size was valued at USD 1.64 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 2.24 billion by 2031, at a CAGR of 5.38% during the forecast period (2026-2031). Robust demand arises from high-efficacy chemistries that allow compliance with China’s zero-growth pesticide policy while sustaining crop yields. Digital farming platforms and drone-based spraying services improve application precision and lower chemical volumes, which promotes premium formulations. Specialty crop expansion in fruits such as blueberries and cherries fuels niche demand for low-residue products that satisfy export standards. Resistance issues in rice pests accelerate the shift toward novel modes of action and integrated pest management. Environmental regulations spur manufacturing upgrades and create openings for bio-based alternatives and patented green chemistries.

Key Report Takeaways

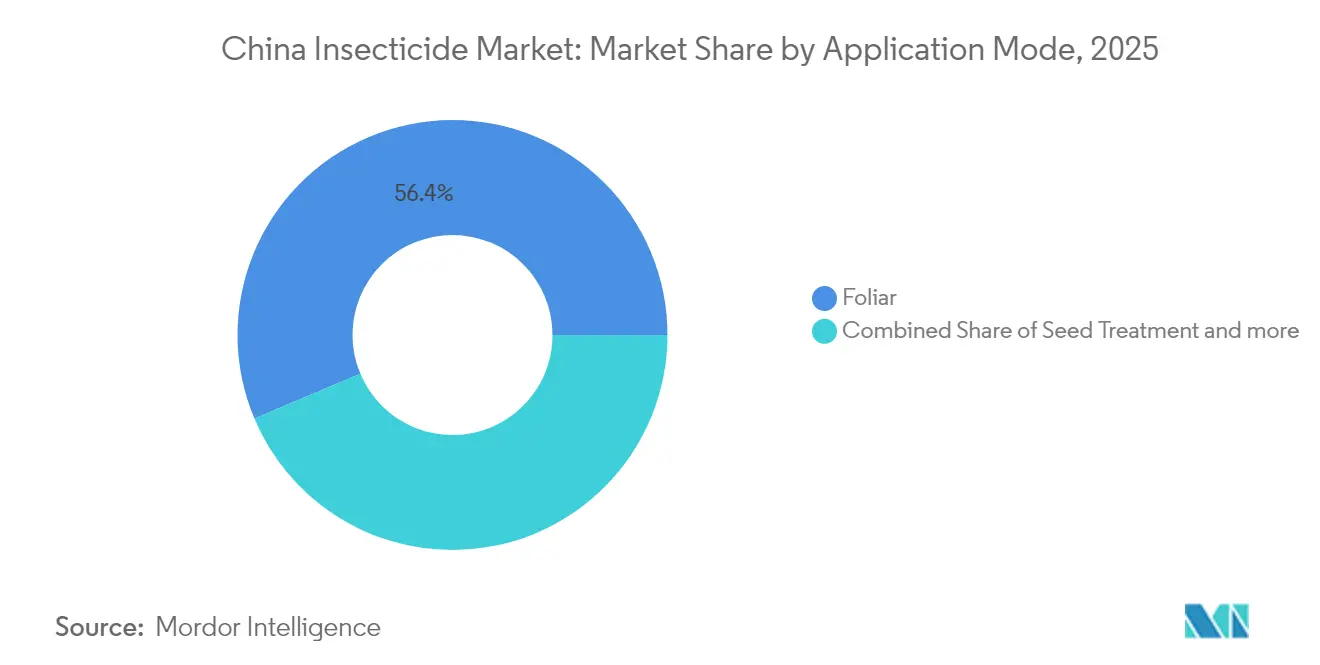

- By application mode, foliar treatments held 56.35% of the China insecticide market share in 2025, whereas seed treatment is forecast to grow at a 5.78% CAGR through 2031.

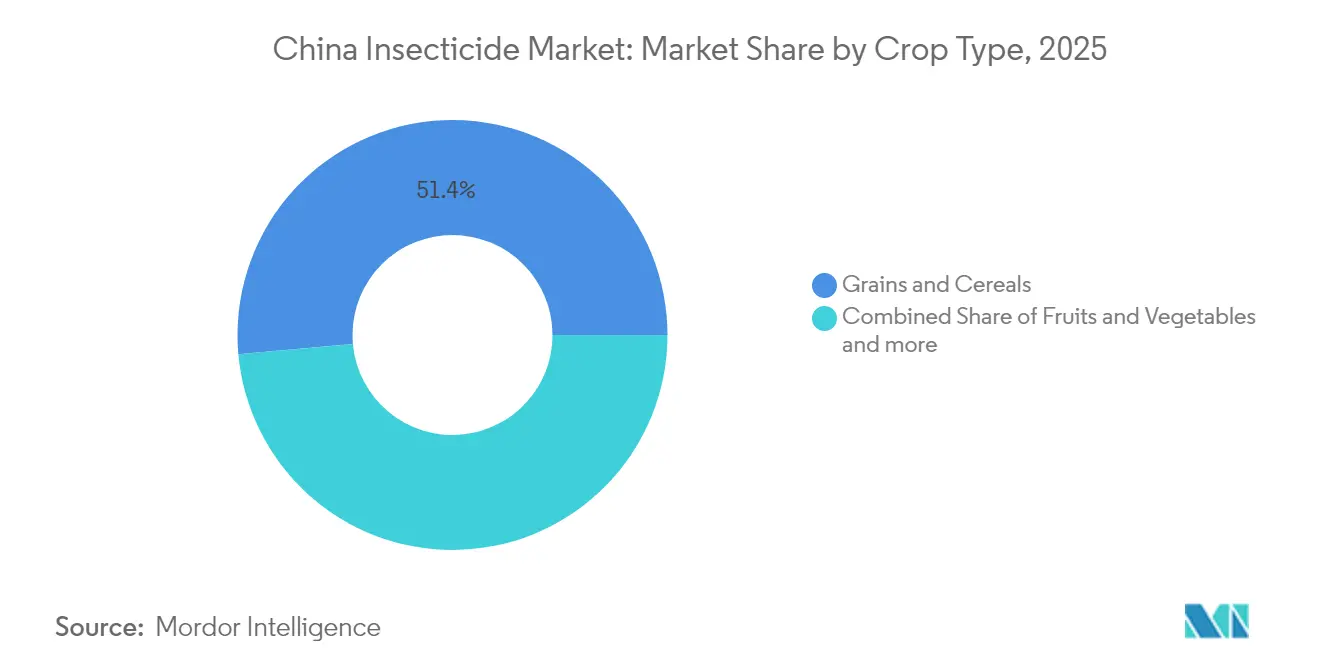

- By crop type, grains and cereals commanded 51.42% of the China insecticide market size in 2025, while fruits and vegetables are projected to expand at a 5.83% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Insecticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent enforcement of zero-growth pesticide policy drives premium insecticide demand | +1.2% | National, strongest in East and Central China | Medium term (2-4 years) |

| Rapid penetration of digital farming platforms linking drone‐based spraying services with smallholders | +0.8% | East China, Central China, expanding to Southwest | Short term (≤ 2 years) |

| Emergence of patented green chemistry actives unlocked by China’s accelerated registration pathway | +0.9% | National, with early adoption in South China | Medium term (2-4 years) |

| Growth in export-oriented high-value specialty crops | +0.7% | South China, Southwest China, and selective Northeast regions | Long term (≥ 4 years) |

| Increased adoption of RNA-interference bio-insecticides by large state farms | +0.6% | North China, Northeast China state farm clusters | Long term (≥ 4 years) |

| Government subsidies for low-toxicity formulations in ecological conservation zones | +0.5% | National, concentrated in ecological priority zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Enforcement of Zero-Growth Pesticide Policy Drives Premium Insecticide Demand

China's zero-growth pesticide policy, rigorously enforced since 2024, has created a structural shift toward higher-efficacy insecticides as farmers face volume caps on chemical applications. The Ministry of Agriculture and Rural Affairs reported a 3.2% reduction in total pesticide usage in 2024 while maintaining crop yields, forcing agricultural producers to invest in premium formulations with enhanced biological activity [1]Source: Ministry of Agriculture and Rural Affairs, “National Pesticide Usage Statistics 2024,” MOA.GOV.CN. This regulatory pressure particularly benefits manufacturers of diamide and spinosyn chemistries, which deliver superior pest control at lower application rates compared to legacy organophosphates. Provincial enforcement varies significantly, with Jiangsu and Shandong provinces implementing the strictest monitoring systems through digital application tracking. The policy's long-term impact extends beyond volume reduction, as it accelerates the phase-out of older chemistry classes and creates market opportunities for next-generation insecticide technologies. Compliance frameworks under the National Development and Reform Commission ensure consistent implementation across agricultural regions, though enforcement intensity correlates directly with local environmental protection priorities.

Rapid Penetration of Digital Farming Platforms Linking Drone-Based Spraying Services with Smallholders

Digital farming cooperatives have emerged as a critical distribution channel, connecting smallholder farmers with professional drone spraying services that optimize insecticide application timing and dosage. The China Agricultural Machinery Industry Association reported that drone-based pesticide applications covered 67 million hectares in 2024, representing a 34% increase from the previous year. These platforms integrate weather data, pest monitoring sensors, and AI-driven application algorithms to reduce insecticide usage by up to 25% while maintaining efficacy levels. Rural service cooperatives bundle equipment access, technical expertise, and chemical procurement, creating new value chains that bypass traditional distribution networks. The model particularly benefits manufacturers of water-dispersible granules and suspension concentrates, which perform optimally in precision application systems. Early adopters in Anhui and Hubei provinces demonstrate that digitally-managed pest control programs achieve 15-20% higher yields compared to conventional spraying methods, driving rapid expansion across grain-producing regions.

Emergence of Patented Green Chemistry Actives Unlocked by China's Accelerated Registration Pathway

China's fast-track registration system for low-toxicity insecticides, implemented in 2024, has reduced approval timelines from 3-4 years to 18-24 months for qualifying green chemistry molecules. The National Pesticide Registration Center processed 47 new active ingredient applications under this pathway in 2024, with 23 receiving conditional approvals for field testing. This regulatory innovation particularly benefits international companies with robust R&D pipelines, as they can introduce novel chemistries to the Chinese market more rapidly than previously possible. Domestic manufacturers are responding by increasing R&D investments and forming joint ventures with global partners to access patented technologies. The accelerated pathway prioritizes molecules with favorable environmental profiles, including reduced persistence, lower toxicity to non-target species, and minimal groundwater contamination potential. Regulatory influence from the Ministry of Ecology and Environment ensures that approved products meet stringent environmental safety standards, creating competitive advantages for companies investing in sustainable chemistry platforms.

Growth in Export-Oriented High-Value Specialty Crops

China's expanding production of export-quality fruits, particularly blueberries and cherries, has created demand for specialized insecticide programs that meet international residue standards while managing complex pest pressures. Export volumes of fresh blueberries reached 28,000 tons in 2024, requiring intensive pest management protocols to satisfy importing countries' maximum residue limits. These high-value crops command premium prices that justify expensive insecticide treatments, including multiple applications of different chemistry classes to prevent resistance development. Specialty crop producers increasingly adopt integrated pest management approaches that combine biological controls, pheromone traps, and targeted chemical interventions. The trend particularly benefits manufacturers of selective insecticides with short pre-harvest intervals and favorable residue profiles. Regional concentration in Shandong, Liaoning, and Yunnan provinces creates localized demand spikes that influence distribution strategies and technical service requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising resistance to pyrethroids and neonicotinoids in major rice pests | -0.9% | South China, Central China rice regions | Short term (≤ 2 years) |

| Stringent effluent discharge norms closing legacy manufacturing plants | -0.6% | East China, Central China industrial zones | Medium term (2-4 years) |

| Growing consumer pushback on pesticide residues in e-commerce grocery channels | -0.4% | National, strongest in tier-1 cities | Medium term (2-4 years) |

| Volatility in technical grade active ingredient prices due to dual-control energy policy | -0.7% | National, concentrated in chemical manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Resistance to Pyrethroids and Neonicotinoids in Major Rice Pests

Widespread resistance development in rice planthoppers and stem borers to commonly used pyrethroid and neonicotinoid insecticides has reduced treatment efficacy and forced costly chemistry rotations across major rice-producing regions. The China Rice Research Institute documented resistance ratios exceeding 100-fold for key pyrethroid compounds in Hunan and Jiangxi provinces, rendering these products ineffective against target pests [2]Source: China Rice Research Institute, “Pest Resistance Monitoring Report 2024,” CNRRI.CN. This resistance crisis particularly impacts smallholder farmers who lack access to alternative chemistry classes and technical expertise for resistance management. The problem is compounded by historical over-reliance on single modes of action and inadequate rotation strategies, creating selection pressure that accelerates resistance evolution. Manufacturers face increased R&D costs to develop novel active ingredients and resistance management programs, while farmers experience yield losses and higher treatment costs.

Stringent Effluent Discharge Norms Closing Legacy Manufacturing Plants

Tightened wastewater discharge standards under China's updated Environmental Protection Law have forced the closure of numerous small-scale insecticide manufacturing facilities, reducing domestic production capacity and increasing import dependence. The Ministry of Ecology and Environment reported that 127 chemical manufacturing plants failed to meet new effluent standards in 2024, with 43 facilities permanently shuttered. These closures particularly affect producers of older chemistry classes like organophosphates and carbamates, which generate complex wastewater streams requiring expensive treatment infrastructure. Surviving manufacturers face substantial capital investments to upgrade treatment facilities, with compliance costs ranging from CNY 50-200 million (USD 7-28 million) per facility. The consolidation benefits larger companies with modern production infrastructure while creating supply shortages for price-sensitive market segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Precision Technologies Drive Seed Treatment Growth

Foliar applications maintain market leadership with a 56.35% share in 2025, benefiting from established farmer practices and broad-spectrum pest control capabilities across diverse crop types. Soil treatment applications serve specialized markets, including root pest management and systemic protection, while chemigation gains traction in modernized irrigation systems. This significant market position is attributed to the method's effectiveness in providing targeted pest control across China's diverse agricultural landscape, which includes staple crops like rice, wheat, and corn, as well as fruits and vegetables. The rapid adoption of modern agricultural practices, including mechanization and advanced farming techniques, has further strengthened the foliar segment's market leadership.

Seed treatment represents the fastest-growing application mode with a 5.78% CAGR through 2031, driven by precision agriculture adoption and integrated pest management strategies that target pests at the earliest crop development stages. The China Seed Association reported that treated seed sales increased 28% in 2024, with corn and soybean representing the largest volume segments. Fumigation remains limited to high-value greenhouse operations and quarantine treatments. Seed treatment formulations increasingly incorporate multiple active ingredients and biological enhancers, creating premium market segments with higher per-unit values.

By Crop Type: Specialty Fruits Outpace Traditional Grains

Grains and cereals retain the largest market share at 51.42% in 2025, supported by food security policies and extensive cultivation areas across major agricultural provinces. his significant market position is primarily driven by the extensive cultivation of crops like rice, wheat, and maize across China's vast agricultural landscape. The segment's dominance is reinforced by increased access to information through digital platforms and government initiatives that promote awareness about the benefits of using commercial insecticide products. Farmers in this segment are increasingly adopting modern agricultural practices and integrated pest management strategies to combat various pest challenges, including aphids, locusts, stem borers, and fall armyworms that cause significant damage to grain crops. The Chinese government's focus on food security and self-sufficiency in grain production has also contributed to the sustained growth of insecticide usage in this segment.

Fruits and vegetables emerge as the fastest-growing crop segment at 5.83% CAGR through 2031, reflecting China's agricultural transition toward higher-value specialty crops that command premium prices and justify intensive pest management investments. Export-oriented fruit production, particularly blueberries and cherries, drives demand for specialized insecticide programs that meet international residue standards while managing complex pest pressures . The expansion of fruit and vegetable cultivation areas, driven by rising domestic demand and changing dietary preferences, is creating a stronger need for effective pest control product solutions. Additionally, the growing emphasis on producing high-quality fruits and vegetables for both domestic consumption and export markets is pushing farmers to invest more in crop protection measures, including advanced contact insecticide products.

Geography Analysis

East China is the largest regional buyer of insecticides, supported by high-intensity vegetable and fruit cultivation in Jiangsu and Shandong that favors premium foliar products. Drone spraying covers 45% of cropland in the region, and digital recordkeeping platforms enjoy broad farmer adoption. Proximity to Shanghai and other consumption hubs raises quality requirements, encouraging growers to pay for low-residue solutions that can clear rigorous e-commerce audits.

Central China shows the fastest growth and is propelled by modernization programs that integrate precision agronomy into vast rice paddies in Hunan and Hubei. Persistent resistance issues accelerate the replacement of older pyrethroids with diamides, and local cooperatives invest in unmanned aerial vehicles to optimize spray windows. Government rice revitalization funds help finance these upgrades, delivering a double boost of technology and purchasing power for higher-priced solutions.

South and Southwest China sustain year-round pest pressure that calls for intensive management strategies. Specialty fruit production in Yunnan and Guangxi triggers strong seasonal demand for selective insecticides with short re-entry intervals. High humidity favors fungal disease complexes, which leads to combined fungicide plus insecticide tank mixes and novel formulations that withstand heavy rainfall. North and Northeast China rely mainly on grains and oilseeds where cost control is paramount, though state farms in Heilongjiang pioneer RNA-interference trials. Long winters create a compressed sales season, requiring distributors to carry ample pre-spring inventory and robust logistical networks.

Competitive Landscape

The Chinese insecticide market exhibits a fragmented structure with both multinational corporations and domestic players holding significant market positions. Top players like Syngenta AG, FMC Corporation, Bayer AG, Corteva Agriscience, and UPL Limited are leveraging their advanced research capabilities and extensive product portfolios, while domestic companies such as Jiangsu Yangnong Chemical and Wynca Group capitalize on their local market knowledge and established distribution networks. The market shows moderate consolidation, with the top players accounting for a significant share while leaving room for smaller specialized manufacturers to serve specific market segments or regional demands.

The market has witnessed strategic consolidation through mergers and acquisitions, as companies seek to strengthen their market position and expand their technological capabilities. These M&A activities have been driven by the need to acquire new technologies, expand product portfolios, and enhance market reach. Companies are increasingly focusing on vertical integration strategies, acquiring or partnering with local manufacturers and distributors to strengthen their supply chain and market presence. This trend has led to the emergence of stronger, more integrated players capable of offering comprehensive crop protection chemical solutions.

For incumbent companies to maintain and expand their market share, developing innovative products that address emerging pest challenges while meeting environmental regulations has become crucial. Success factors include investing in research and development to create new active ingredients, improving formulation technologies, and developing integrated pest management solutions. Companies must also strengthen their distribution networks, particularly in rural areas, while building strong relationships with agricultural cooperatives and large-scale farmers. Additionally, establishing local manufacturing facilities and research centers helps companies better understand and respond to regional market needs.

China Insecticide Industry Leaders

Syngenta AG

FMC Corporation

Bayer AG

Corteva Agriscience

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Syngenta Group announced a USD 180 million expansion of its Nantong manufacturing facility to increase production capacity for diamide insecticides by 40%, targeting growing demand from specialty crop producers. The investment includes advanced wastewater treatment infrastructure to meet stringent environmental discharge standards and automated production lines that reduce manufacturing costs by an estimated 15%.

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

- May 2022: UPL partnered with Bayer for Spirotetramat insecticide to develop new pest management solutions. Through this long-term global data access and supply agreement with Bayer, specifically for addressing farmer demands regarding resistance management and difficult-to-control sucking pests, UPL will develop, register, and distribute new unique solutions, including Spirotetramat, using its experience in insecticides and worldwide research and development network.

China Insecticide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Insecticides are chemicals used to control or prevent insects from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms