India Insecticide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.86 Billion |

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

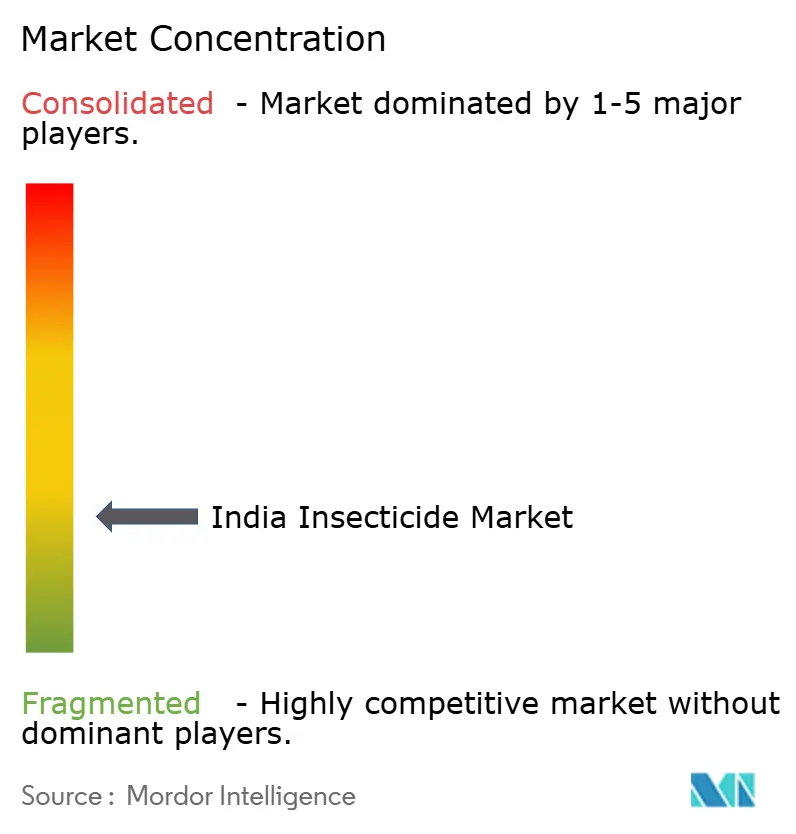

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Insecticide Market Analysis by Mordor Intelligence

The India insecticide market size is expected to grow from USD 1.86 billion in 2025 to USD 1.93 billion in 2026 and is forecast to reach USD 2.33 billion by 2031 at 3.82% CAGR over 2026-2031. Steady demand comes from low per-hectare consumption, widening coverage of precision spraying technologies, and the push for integrated pest management protocols. Tight farm economics continue to tilt farmer choices toward molecules that combine broad-spectrum control with favorable price-performance ratios. Contract manufacturing opportunities expand as multinational firms diversify supply chains away from China, allowing domestic producers to climb the value chain. Market concentration remains low. Established local champions and global innovators jockey for shelf space in an increasingly digital distribution environment.

Key Report Takeaways

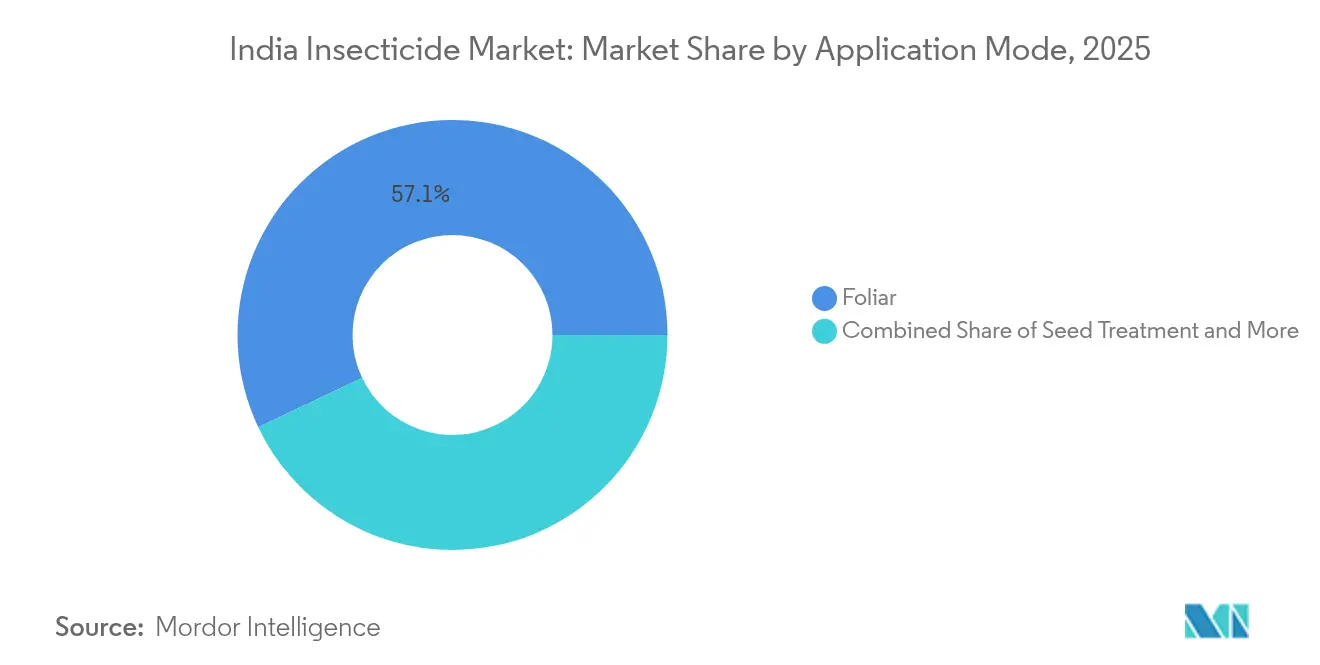

- Foliar application commanded 57.05% of the India insecticide market share in 2025, while seed treatment is projected to advance at a 4.05% CAGR through 2031.

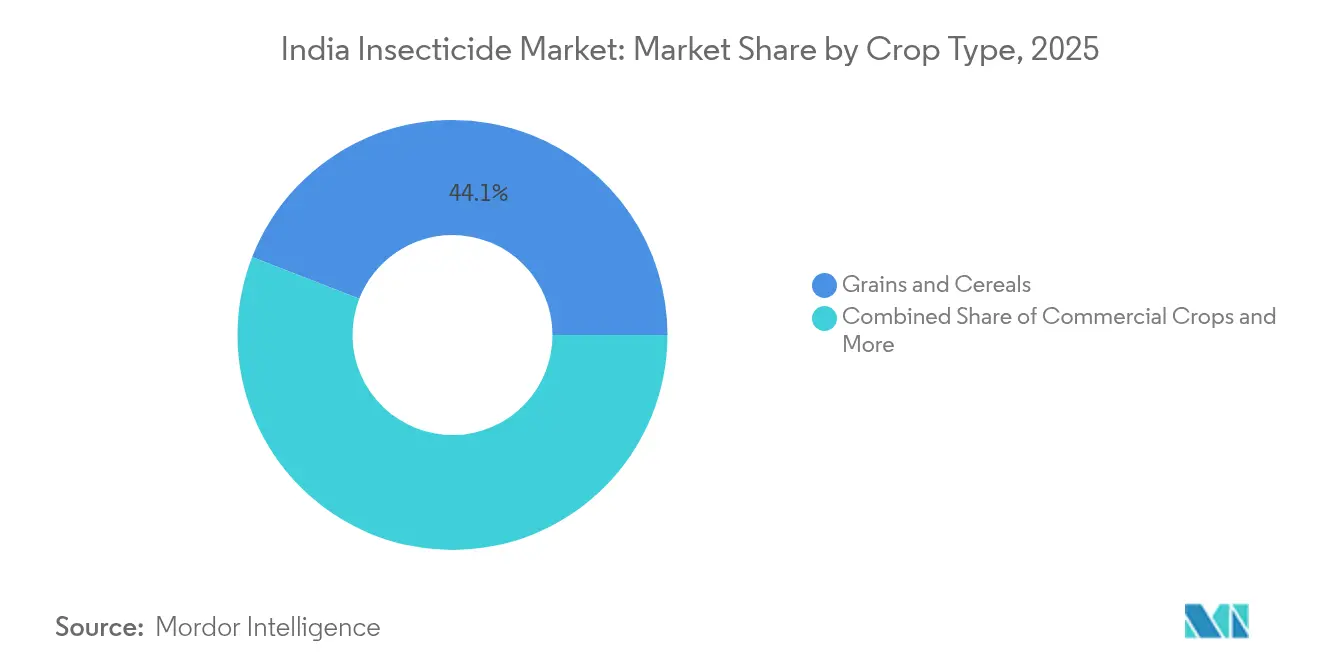

- Grains and cereals accounted for a 44.10% share of the India insecticide market size in 2025; commercial crops are forecast to expand at a 4.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Insecticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low per-hectare pesticide consumption leaves large headroom for growth | +1.2% | Pan-India, with higher potential in Eastern states | Medium term (2-4 years) |

| Government drone-spraying subsidies reduce application cost and widen usage | +0.8% | National, with early gains in Punjab, Haryana, Maharashtra | Short term (≤ 2 years) |

| Rising incidence of insecticide-resistant pests spurs demand for next-gen molecules | +1.1% | Cotton belt states, rice-growing regions | Long term (≥ 4 years) |

| Shift of global supply chains from China to India boosts contract manufacturing | +0.7% | Gujarat, Maharashtra are manufacturing hubs | Medium term (2-4 years) |

| Growing public vector-control spend (NVBDCP) enlarges non-crop demand | +0.4% | Urban centers, malaria-endemic regions | Short term (≤ 2 years) |

| Surge in e-commerce ag-input platforms improves last-mile availability | +0.6% | Tier-2 and Tier-3 cities, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low per-hectare pesticide consumption leaves large headroom for growth

Per-hectare pesticide consumption averages 0.6 kg in India versus the global mean of 2.7 kg, leaving ample room for volume growth as farm commercialization deepens[1]Source: Food and Agriculture Organization, “Pesticide Use Statistics Global Report 2024,” FAO.ORG. Uptake is most pronounced in the eastern region, where modernization programs intersect with severe pest incidence after erratic monsoons. Public extension campaigns that showcase safe-use protocols reduce farmer hesitation over chemical exposure. Input financiers increasingly bundle crop protection products with seasonal credit lines, streamlining access for smallholders. Over the forecast horizon, these converging factors anchor a stable demand floor for the India insecticide market.

Government drone-spraying subsidies reduce application cost and widen usage

The Namo Drone Didi initiative reimburses 80% of drone costs for women’s self-help groups, sharply lowering entry barriers to aerial spraying[2]Source: Ministry of Agriculture and Farmers Welfare, “Agricultural Statistics at a Glance 2024,” AGRICOOP.NIC.IN. Early pilots in Punjab and Haryana reveal chemical savings of 25% alongside superior canopy penetration. Lower unit costs entice growers of high-value vegetables and cotton to adopt multi-crop service contracts that bundle drones, analytics, and calibrated insecticide doses. Equipment makers partner with formulators to pre-load optimal tank-mix recommendations, reinforcing brand preference and boosting repeat purchases across the India insecticide market.

Rising incidence of insecticide-resistant pests spurs demand for next-gen molecules

Resistance in pink bollworm and rice stem borer populations now limits the efficacy of traditional pyrethroids, pushing growers toward diamide and spinosyn classes that command higher price points[3]Source: Indian Council of Agricultural Research, “Pest Management Research Updates 2024,” ICAR.ORG.IN. Multiyear rotation protocols institutionalize multi-product packages, elevating average selling prices and widening the addressable revenue pool. Domestic research pipelines respond: 5 new insecticide actives received clearance in 2024, the largest cohort on record. Portfolio depth thus becomes a core differentiator across the India insecticide market.

Shift of global supply chains from China to India boosts contract manufacturing

India's emergence as a preferred alternative to Chinese agrochemical manufacturing gained momentum following anti-dumping duties imposed on Chinese glyphosate and other key active ingredients, creating opportunities for domestic contract manufacturers to serve global markets. The shift accelerated as multinational companies diversified supply chains to reduce geopolitical risks, with India's established pharmaceutical manufacturing infrastructure providing a natural foundation for agrochemical production expansion. The supply chain diversification trend creates opportunities for Indian manufacturers to move beyond generic production toward custom synthesis of patented molecules, capturing higher margins and building long-term customer relationships with global agrochemical companies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chinese price dumping squeezes margins of Indian formulators | -0.9% | National, particularly affecting generic formulations | Short term (≤ 2 years) |

| Regulatory Bottlenecks Delay Innovation Commercialization | -0.6% | National regulatory bottleneck | Medium term (2-4 years) |

| State-wise bans on hazardous actives create portfolio gaps | -0.4% | Varying by state, significant in Kerala, Punjab | Long term (≥ 4 years) |

| Climate-driven erratic rainfall lowers spray opportunities in kharif season | -0.5% | Monsoon-dependent regions, Central and Western India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chinese price dumping squeezes margins of Indian formulators

Chinese manufacturers' aggressive pricing strategies, enabled by scale economies and government support, continue to pressure Indian formulator margins despite anti-dumping measures on select products. The price differential for key active ingredients like glyphosate and 2,4-D remains substantial, with Chinese suppliers offering prices 15-20% below Indian production costs even after duty adjustments. Chinese competition particularly affects smaller Indian formulators who lack the scale to achieve competitive production costs or the resources to develop proprietary products that command premium pricing.

Regulatory Bottlenecks Delay Innovation Commercialization

The Central Insecticides Board and Registration Committee's lengthy approval processes, averaging 18-24 months for new active ingredient registrations, significantly delay the commercialization of innovative products and reduce the effective patent life for novel molecules. The registration backlog has grown as regulatory scrutiny intensifies following environmental and health concerns, with comprehensive toxicology and environmental fate studies now required for all new submissions. Recent initiatives to digitize the registration process and establish clear timelines represent positive steps, but implementation remains inconsistent across different product categories and active ingredient classes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Precision Technologies Drive Transformation

Foliar formats retained 57.05% market share within the India insecticide market in 2025 due to universal equipment availability and immediate visual efficacy. High compatibility with tank-mix nutrients keeps demand resilient even as integrated pest management gains ground. Seed treatment, though a modest base, is projected to grow at 4.05% CAGR through 2031, reflecting farmer preference for preventive protection during germination. Growth accelerates as certified-seed schemes bundle pre-dosed coatings, guaranteeing quality and uniformity.

Chemigation and fumigation remain niche but critical in high-value protected cultivation and stored grain ecosystems. Soil treatment expands in potato and sugarcane belts beset by nematodes. Bundled service offerings that blend drone foliar passes with in-furrow treatments mark a shift toward outcome-based advisory models. As traceability mandates tighten, QR-coded labels tied to geotagged spray logs enhance stewardship credibility and reinforce brand stickiness across the India insecticide market.

By Crop Type: Commercial Crops Lead Value Creation

Grains and cereals accounted for 44.10% of the India insecticide market share in 2025, anchored by rice and wheat’s twin-season cycles and government procurement guarantees. Staple food security imperatives shield demand even when raw-material inflation compresses grower margins. Commercial crops such as cotton, sugarcane, and spices register a 4.02% CAGR to 2031, aided by export orientation and superior per-hectare value capture. Rising resistance management costs in cotton propel the adoption of premium chemistries.

Fruits and vegetables enjoy structural tailwinds from urban dietary shifts toward higher nutritional diversity. Pulses and oilseeds, though exposed to weather volatility, benefit from minimum support price revisions that incentivize better pest management. Turf and ornamental usage remains small but expanding in line with urban landscaping projects and golf course construction. Crop-specific label expansion for biologicals creates complementary opportunities within the broader India insecticide market.

Geography Analysis

Northern states Punjab, Haryana, and Uttar Pradesh collectively command modest share of national insecticide usage, reflecting intensive wheat-rice rotations and high mechanization. Subsidized electricity for irrigation supports multiple sprays, and organized retail penetration ensures product availability year-round. Western India, led by Maharashtra and Gujarat, contributes another 24.62% share, benefiting from commercial cotton, sugarcane, and horticulture clusters situated near ports that streamline import-export flows.

Southern states, including Karnataka, Andhra Pradesh, and Tamil Nadu, offer strong upsides as growers diversify into export-oriented chilies, coffee, and plantation crops. Higher literacy rates facilitate rapid uptake of QR-coded stewardship instructions, reducing misuse incidents. Eastern India, West Bengal, Bihar, and Odisha, present the steepest growth curve given historically low base consumption. Government-backed farm mechanization programs and improved rural road connectivity amplify distribution reach into these underpenetrated zones.

Regional policy divergence shapes product strategies. Kerala’s proactive toxicology norms accelerate the shift toward eco-friendly actives, whereas Punjab’s aerial-spray guidelines institutionalize drone corridors. Climate shifts alter pest migration patterns; warmer winters allow pink bollworm survival in Northwestern cotton, pulling insecticide demand forward into earlier phenological windows. The compound effect of these dynamics sustains a balanced regional demand mix, underpinning nationwide resilience for the India insecticide market.

Competitive Landscape

The India insecticide market displays low concentration. Domestic leaders UPL Limited, PI Industries, and Dhanuka Agritech leverage multi-channel distribution and backward-integrated manufacturing to hold sizable rural mindshare. Global innovators Bayer AG, BASF SE, and Syngenta Group focus on patented molecules and digital agronomy platforms, capturing the high-margin tip of the demand pyramid.

Anti-dumping levies on selected Chinese actives open white space for local producers, evidenced by PI Industries' revenue surge in Q1 FY25. Strategic moves center on portfolio breadth and technology integration: UPL’s acquisition of Advanta Seeds aligns genetic traits with crop-protection offerings, while Dhanuka partners with drone start-ups to augment precision-spray services. Compliance prowess becomes a competitive moat as QR-code traceability norms take effect, favoring firms with digitized supply chains.

Multinationals raise localization efforts, setting up formulation units to qualify for public tenders linked to the National Vector Borne Disease Control Program. Meanwhile, mid-tier Indian companies pivot to custom synthesis for export markets, capturing higher margins and mitigating domestic weather-linked demand swings. Competitive positioning therefore hinges on innovation speed, regulatory agility, and the capacity to deliver bundled solutions that elevate farmer profitability across the India insecticide market.

India Insecticide Industry Leaders

FMC Corporation

PI Industries

Sumitomo Chemical Co. Ltd

UPL Limited

ADAMA Agricultural Solutions Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: New insecticide labeling rules mandating QR codes for product traceability came into effect, requiring manufacturers to invest in digital infrastructure and supply chain monitoring systems. The regulation aims to combat counterfeit products and improve environmental monitoring of pesticide usage patterns.

- May 2025: India received exemption for chlorpyrifos use in specific crops at the Stockholm Convention, allowing continued domestic production and use while global restrictions tighten. This regulatory victory provides Indian manufacturers with competitive advantages in export markets and domestic applications where alternatives remain limited.

- May 2024: BASF launched Efficon insecticide and Prexio Active for rice cultivation in India, expanding its crop protection portfolio to address evolving pest resistance patterns and integrated pest management requirements. The products target stem borer complexes and provide extended residual activity for season-long protection.

India Insecticide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Insecticides are chemicals used to control or prevent insects from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms