Africa Insecticide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

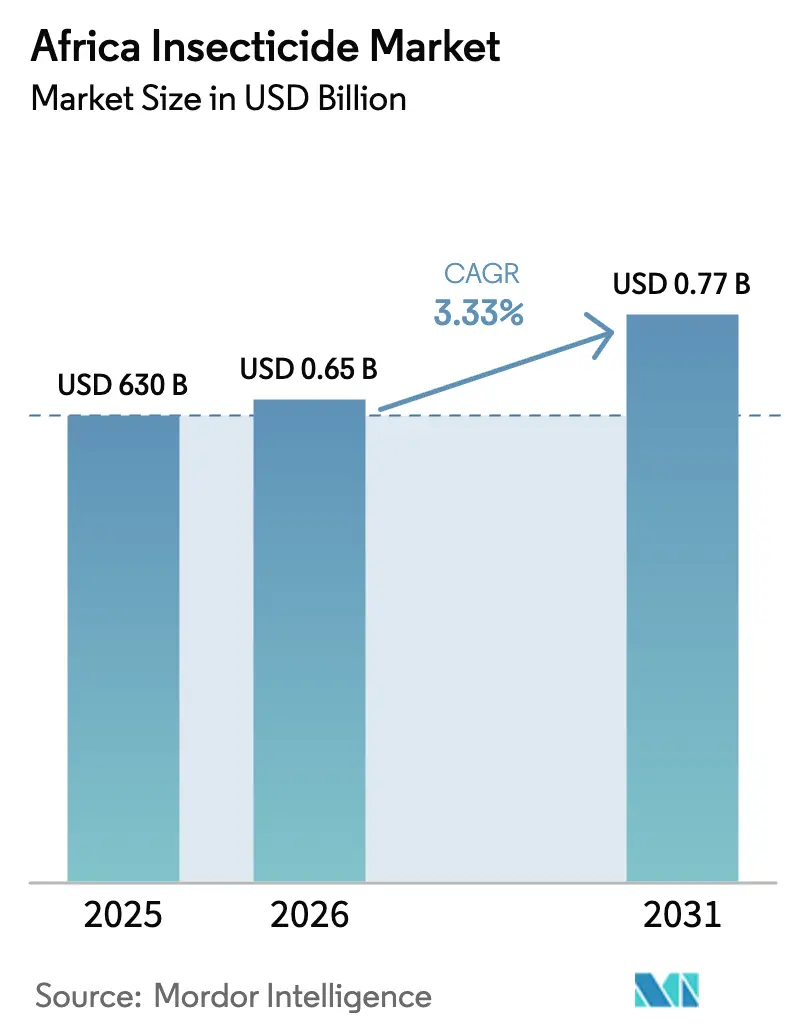

| Base Year Market Size (2025) | USD 630 Billion |

| Market Size (2026) | USD 0.65 Billion |

| Market Size (2031) | USD 0.77 Billion |

| Growth Rate (2026 - 2031) | 3.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Insecticide Market Analysis by Mordor Intelligence

The Africa insecticide market size was valued at USD 630 million in 2025 and estimated to grow from USD 650 million in 2026 to reach USD 770 million by 2031, at a CAGR of 3.33% during the forecast period (2026-2031). The Africa insecticide market gains momentum from rising demand for European Union Maximum Residue Limit compliant active ingredients, climate variability that intensifies pest outbreaks, and credit programs that lift input affordability. Adoption of precision spraying, localized formulation plants, and biological chemistry rounds out the growth story while counterfeit trade, slow francophone registrations, soft grain prices, and resistance buildup act as counterweights. Climate volatility, particularly El Niño and La Niña cycles intensifying insect pest pressure across Southern Africa, creates sustained demand for protective insecticides even as counterfeit products and regulatory bottlenecks constrain market expansion.

Key Report Takeaways

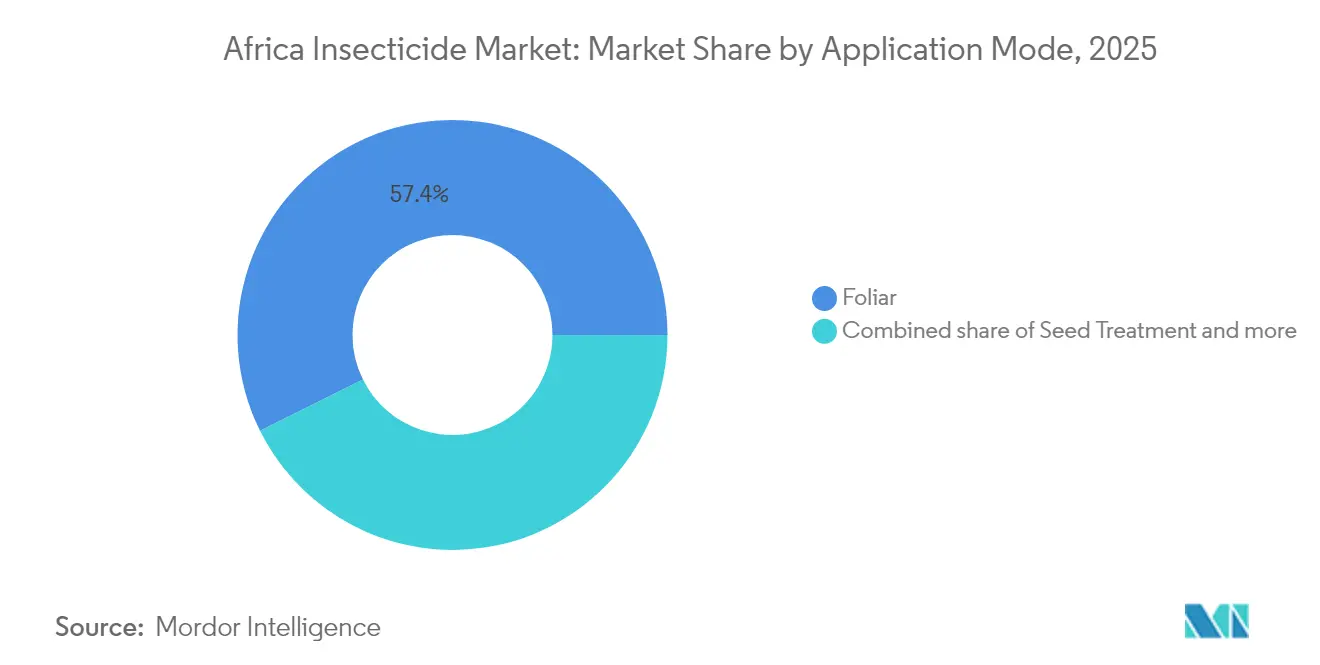

- By application mode, foliar treatments accounted for 57.35% of Africa insecticide market share in 2025, while seed treatment is forecast to expand at a 3.46% CAGR through 2031.

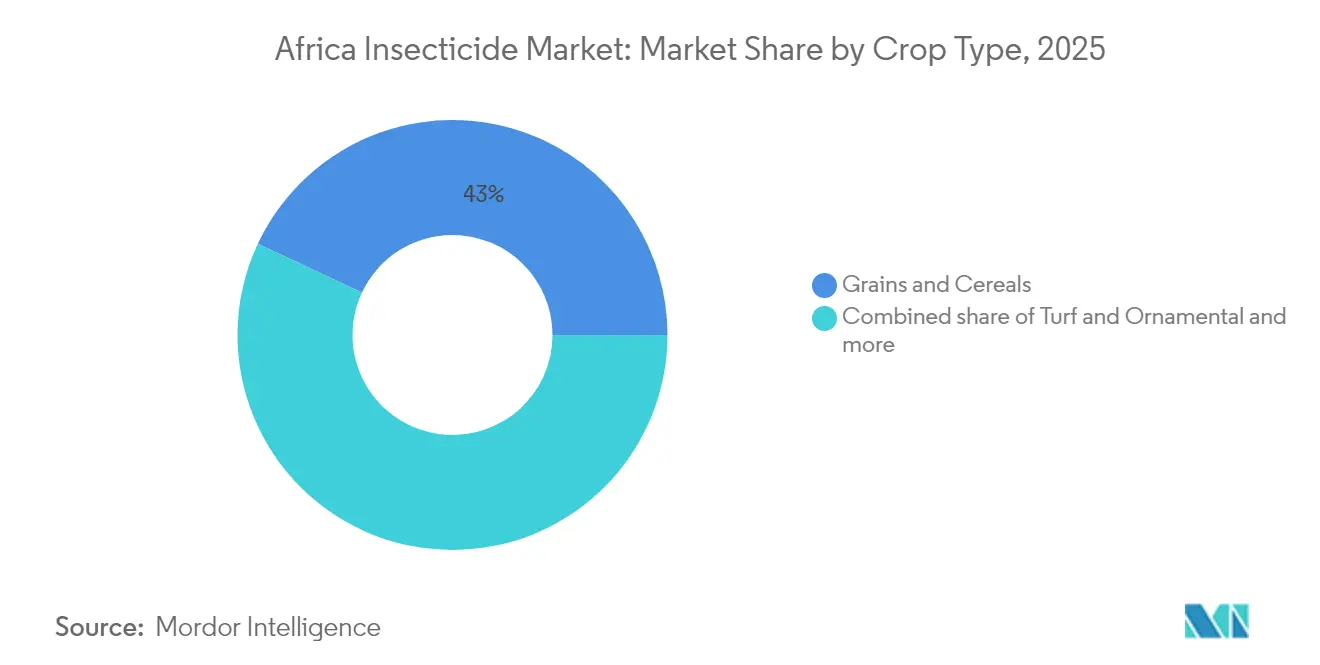

- By crop type, grains and cereals held 43.02% of the Africa insecticide market size in 2025 and turf and ornamental crops are advancing at a 3.46% CAGR through 2031.

- By geography, South Africa led with a 14.96% share in 2025 and is projected to grow at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Insecticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in European Union Maximum Residue Limit compliant active ingredients adoption | +0.8% | South Africa, Kenya, Egypt, and Ghana | Medium term (2-4 years) |

| Climate-driven spike in insect pest pressure | +0.6% | Southern Africa core, spillover to East Africa | Short term (≤ 2 years) |

| Expansion of commercial horticulture under greenhouse nets | +0.5% | South Africa, Kenya, and Egypt | Long term (≥ 4 years) |

| Government-backed warehouse-receipt financing unlocking input credit | +0.4% | Nigeria, Ghana, Tanzania, and Kenya | Medium term (2-4 years) |

| Surge in drone-enabled precision spraying service start-ups | +0.3% | South Africa, Kenya, and Nigeria | Long term (≥ 4 years) |

| VC funding for bio-insecticide scale-ups across East Africa | +0.2% | Kenya, Uganda, Tanzania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in European Union Maximum Residue Limit-Compliant Active Ingredients Adoption

Export-oriented African producers are rapidly transitioning to European Union Maximum Residue Limit-compliant insecticides as premium market access becomes contingent on residue certification. This shift particularly benefits South African citrus and table grape exporters, where European Union-approved pyrethroids and neonicotinoids command 15-20% price premiums over conventional alternatives. Kenya's flower industry has accelerated adoption of (Insecticide Resistance Action Committee) IRAC-approved rotation programs to maintain certification for European auction houses, driving demand for newer chemistry classes despite higher input costs. The European Food Safety Authority's 2024 updates to MRL thresholds for key insecticide groups created immediate compliance pressure, with non-compliant residues triggering automatic shipment rejections[1]Source: European Food Safety Authority, “MRL Database,” EFSA.EUROPA.EU.

Climate-Driven Spike in Insect Pest Pressure

El Niño and La Niña weather patterns alter temperature and precipitation across Southern and Eastern Africa, creating optimal conditions for insect pest proliferation and extending traditional spraying seasons by 4-6 weeks. South Africa's maize belt experienced unprecedented armyworm and stem borer outbreaks during the 2024 growing season, with insecticide application frequencies increasing from 2-3 to 4-5 treatments per season. Tanzania's coffee regions report similar pest pressure escalation, particularly for coffee berry borer and antestia bugs, forcing smallholder cooperatives to adopt preventive spraying programs previously considered economically unviable.

Expansion of Commercial Horticulture Under Greenhouse Nets

Protected agriculture infrastructure across Africa expanded by an estimated 12-15% annually from 2024, driven by water scarcity concerns and export quality requirements that favor controlled environment production. South Africa's Western Cape province leads this transition with over 8,000 hectares under protective structures, requiring intensive insecticide programs to manage enclosed pest populations like thrips, aphids, and whiteflies. Kenya's flower industry has invested heavily in shade net houses and greenhouse facilities, creating year-round insecticide demand patterns that contrast sharply with seasonal field applications.

Government-Backed Warehouse-Receipt Financing Unlocking Input Credit

Warehouse receipt systems enable smallholder farmers to access seasonal credit using stored grain as collateral, directly translating to increased insecticide purchasing power during critical application windows. Nigeria's Anchor Borrowers Programme expanded to cover 4.2 million farmers in 2024, with participating cooperatives reporting 35-40% increases in insecticide adoption rates compared to non-participants. Ghana's Agricultural Development Bank launched commodity-backed lending specifically targeting input financing, allowing farmers to secure insecticide supplies at planting rather than waiting for harvest proceeds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating counterfeit and illegal insecticide trade | -0.5% | Nigeria, Ghana, Côte d'Ivoire, and Mali | Short term (≤ 2 years) |

| Slow product-registration timelines in francophone West Africa | -0.4% | Côte d'Ivoire, Senegal, Mali, and Burkina Faso | Long term (≥ 4 years) |

| Farm-gate price squeeze from softening grain prices | -0.3% | Global, with acute impact in Nigeria, and Tanzania | Medium term (2-4 years) |

| Rapid resistance buildup to single-site insecticides | -0.3% | South Africa, Kenya, and Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Counterfeit and Illegal Insecticide Trade

Counterfeit insecticides represent an estimated 20-30% of total market volumes across West Africa, undermining legitimate product demand while creating crop protection failures that erode farmer confidence in chemical inputs. Nigeria's National Agency for Food and Drug Administration and Control seized over 2,000 metric tons of illegal pesticides in 2024, with counterfeit insecticides comprising 35% of confiscated products due to their consistent demand across diverse crop systems. The Economic Community of West African States established a regional pesticide tracking system in 2024, but implementation remains inconsistent across member countries with varying enforcement capabilities [2]Source: Economic Community of West African States, “Pesticide Tracking System,” ECOWAS.INT.

Slow Product-Registration Timelines in Francophone West Africa

Regulatory approval processes for new insecticide active ingredients average 3-4 years in francophone West African countries compared to 18-24 months in South Africa, creating market entry barriers that favor established generic products over innovative chemistry. Côte d'Ivoire's pesticide registration committee evaluates fewer than 20 new products annually due to limited technical capacity and bureaucratic procedures that require multiple ministerial approvals. Senegal's regulatory framework mandates local efficacy trials for all insecticide registrations, extending approval timelines while increasing costs for international manufacturers seeking market entry. The West African Economic and Monetary Union's harmonized pesticide regulations, intended to streamline approvals, face implementation challenges due to differing national standards and limited cross-border regulatory coordination.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Foliar Dominance Drives Market Evolution

Foliar application commands 57.35% market share in 2025, reflecting its immediate efficacy advantages for commercial horticulture operations where pest outbreaks require rapid intervention capabilities. This dominance stems from the method's versatility across diverse crop types and its compatibility with existing spray equipment infrastructure that most African farmers already possess. The segment's prominence is further strengthened by its quick absorption and rapid action characteristics, making it particularly effective for immediate pest control chemical needs. Farmers across Africa have increasingly recognized the importance of timely and targeted treatment through foliar application to address pest pressures, ultimately improving crop health and productivity.

Seed treatment represents the fastest-growing segment at 3.46% CAGR through 2031, driven by its cost-effectiveness for large-scale grain production and reduced environmental exposure compared to broadcast applications. Chemigation gains traction in irrigated systems, particularly in Egypt's Nile Delta and South Africa's Western Cape, where fertigation infrastructure enables precise insecticide delivery through existing irrigation networks.

By Crop Type: Grains Lead While Specialty Segments Accelerate

Commercial crops and grains and cereals collectively represent 43.02% of insecticide demand in 2025, driven by Africa's position as a major grain producer where even modest yield improvements generate substantial economic returns. Maize, wheat, and rice production across Nigeria, South Africa, and Egypt creates consistent baseline demand for insecticide applications, particularly during peak pest seasons when armyworm, stem borer, and rice stem borer pressure peaks.

Turf and ornamental applications emerge as the fastest-growing segment at 3.46% CAGR, reflecting urbanization trends and golf course development across major African cities where aesthetic standards require intensive pest management programs. The Turf and Ornamental segment, while smaller in scale, serves specialized markets including Kenya's prominent flower export industry, which supplies to over 60 nations globally. Each of these segments faces unique pest challenges and requires specific agricultural chemical solutions tailored to their particular needs.

Geography Analysis

South Africa dominates the regional market with 14.96% share in 2025 and projects 5.24% CAGR through 2031, benefiting from established distribution networks, sophisticated regulatory frameworks, and export-oriented agriculture that demands premium insecticide solutions. The country's wine industry drives high-value insecticide consumption for mealybug and thrips control, while its citrus and deciduous fruit sectors require intensive pest management programs to maintain international market access against false codling moth and fruit fly infestations.

Nigeria represents the largest absolute market opportunity despite regulatory challenges, with its diverse agricultural base spanning rice, maize, cocoa, and vegetable production across multiple agro-ecological zones. The country's 200 million population creates substantial food security imperatives that drive government support for agricultural intensification, including insecticide adoption programs targeting smallholder farmers. Egypt's irrigated agriculture system enables year-round production cycles that generate consistent insecticide demand, particularly in the Nile Delta where intensive vegetable production for European export markets requires weekly application schedules during peak pest seasons. Kenya, Ghana, and Tanzania represent emerging growth markets where increasing commercial agriculture adoption and export orientation drive insecticide demand acceleration. Kenya's flower industry leads regional insecticide intensity, with greenhouse operations applying products on 7-10 day intervals to maintain European market quality standards against thrips, aphids, and whitefly infestations. Côte d'Ivoire's position as the world's largest cocoa producer creates substantial market potential, though slow regulatory approval processes and limited distribution infrastructure constrain growth relative to other regional markets.

Competitive Landscape

The Africa insecticide market exhibits moderate concentration with the top players including BASF SE, FMC Corporation, Bayer AG, Syngenta AG Group, and Nufarm. These companies leverage their international expertise and robust supply chains to maintain market leadership, while regional players primarily serve specific geographic areas or crop segments. The market exhibits moderate consolidation, with the top five players commanding a significant share, though there remains space for specialized players focusing on niche segments or specific regional markets.

The industry has experienced strategic consolidation through mergers and acquisitions, as evidenced by significant deals like Bayer's acquisition of Monsanto and UPL's purchase of Arysta LifeScience. These consolidations have reshaped the competitive landscape by creating stronger entities with expanded product portfolios and enhanced market reach. Local companies and distributors play crucial roles as partners to global manufacturers, providing essential market access and local expertise while helping navigate regional regulatory requirements and distribution challenges.

Success in the African insecticide market increasingly depends on companies' ability to develop sustainable and environmentally friendly solutions while maintaining product efficacy. Market leaders are investing in bio-based alternatives and integrated pest management solutions, recognizing the growing importance of sustainable agriculture. Companies are also focusing on developing resistance management strategies and improving product formulations to address evolving pest challenges while meeting stringent regulatory requirements. Building strong relationships with local farming communities and providing comprehensive technical support have become essential elements for maintaining market position.

Africa Insecticide Industry Leaders

BASF SE

FMC Corporation

Bayer AG

Syngenta AG Group

Nufarm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

- May 2022: UPL partnered with Bayer for Spirotetramat insecticide to develop new pest management solutions. Through this long-term global data access and supply agreement with Bayer, specifically for addressing farmer demands regarding resistance management and difficult-to-control sucking pests, UPL will develop, register, and distribute new unique solutions, including Spirotetramat, using its experience in insecticides and worldwide research and development network.

- November 2021: Syngenta Crop Protection introduced the Plinazolin technology, a new active ingredient with a unique Mode of Action (IRAC Group 30) for insect control to assist farmers in protecting their crops from a variety of pests.

Africa Insecticide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type. South Africa are covered as segments by Country.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| South Africa |

| Rest of Africa |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental | |

| Geography | South Africa |

| Rest of Africa |

Market Definition

- Function - Insecticides are chemicals used to control or prevent insects from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms