Insect Growth Regulators Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

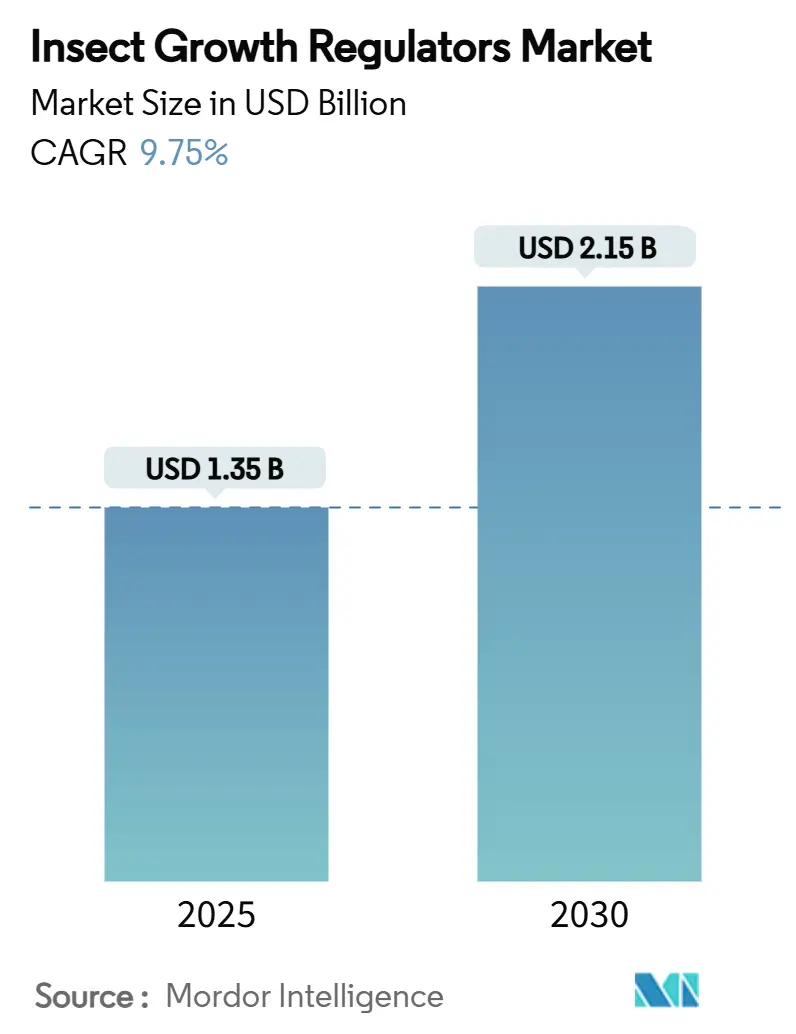

| Market Size (2025) | USD 1.35 Billion |

| Market Size (2030) | USD 2.15 Billion |

| Growth Rate (2025 - 2030) | 9.75% CAGR |

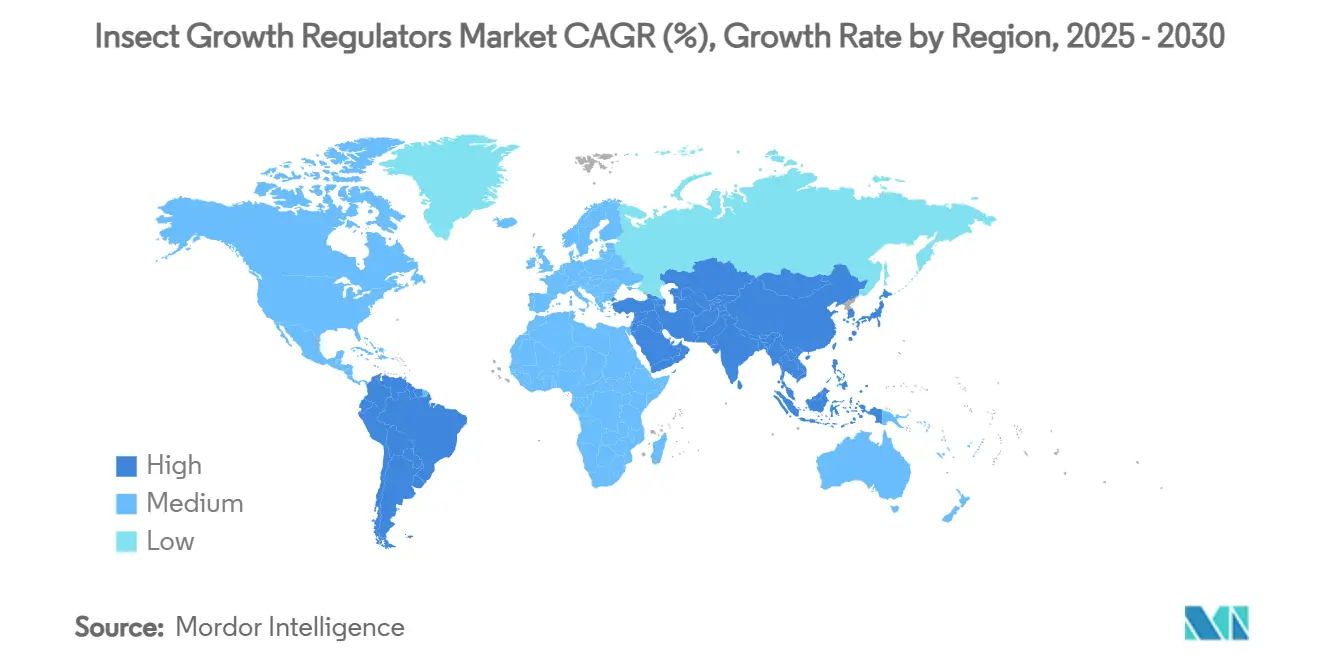

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

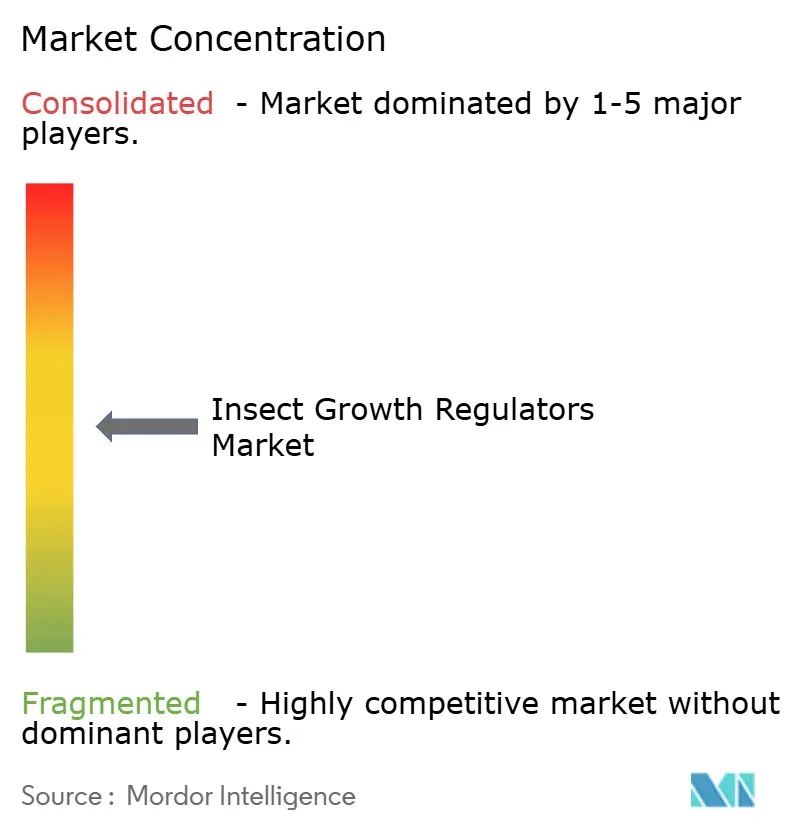

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insect Growth Regulators Market Analysis by Mordor Intelligence

The insect growth regulators market size touched USD 1.35 billion in 2025 and is forecast to expand to USD 2.15 billion by 2030, translating into a 9.75% CAGR over the period. The acceleration links directly to mounting residue limitations, escalating resistance to pyrethroids and organophosphates, and the integration of precision-agriculture technologies that cut application waste while meeting strict food safety mandates[1]Source: United States Environmental Protection Agency, “Pesticide Tolerances,” epa.gov . Agricultural exporters increasingly rely on the insect growth regulators market to safeguard access to premium distribution channels that now enforce private residue thresholds tighter than government standards. Tight supply conditions for traditional adulticides, coupled with policy incentives for integrated pest management, further amplify demand for low-toxicity chemistry that protects both pollinators and applicator health. Producers also value the compatibility of insect growth regulators with biological control agents, enabling season-long rotation programs that delay resistance across lepidopteran, coleopteran, and dipteran pest complexes. Capital inflows toward drone-based spray services and feed-through technologies signal enduring opportunities for formulation innovators willing to address niche use patterns in protected cultivation and livestock housing.

Key Report Takeaways

- By product type, chitin synthesis inhibitors captured 42.0% of the insect growth regulators market share in 2024, while juvenile hormone analogs are projected to post the fastest growth rate of 11.80% from 2024 to 2030.

- By Form, liquid concentrates accounted for 51.30% of the insect growth regulators market size in 2024, while aerosols and foggers are forecast to grow at a 10.50% CAGR through 2030.

- By application, open cultivated crops dominated revenue with a 46.80% share in 2024, while protected cultivated crops are set to record a 12.90% CAGR, the highest among all uses.

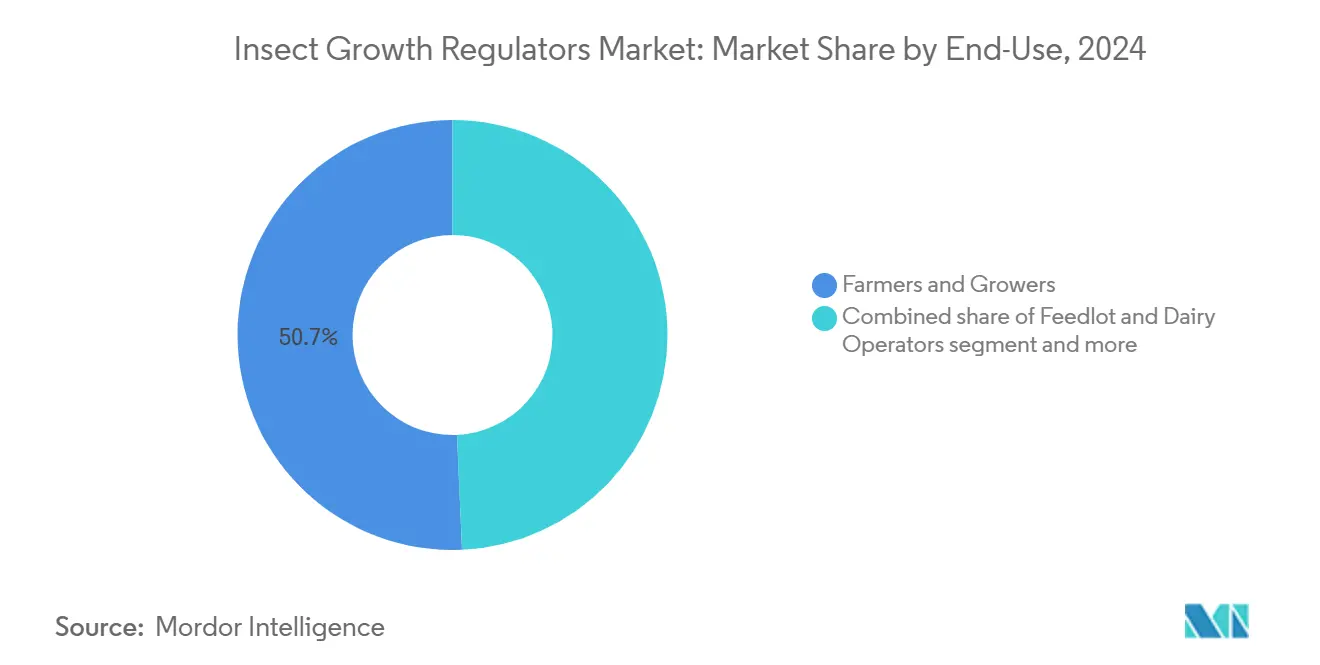

- By end use, farmers and growers held 50.70% of spending in 2024, whereas Agricultural Pest-Management Service Providers are projected to advance at a 13.50% CAGR during the outlook period.

- By geography, North America led with a 33.50% share in 2024, and Asia-Pacific is on track for the highest 11.40% CAGR through 2030.

- The top five players commanded 57.30% of global revenue in 2024, indicating a moderately consolidated market structure.

Global Insect Growth Regulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent maximum-residue limits favor low-toxicity IGRs | +1.8% | Global, with the strongest impact in North America and Europe | Medium term (2-4 years) |

| Resistance to pyrethroids and organophosphates drives rotation to IGRs | +2.1% | Global, particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Adoption of precision-agriculture spray drones enables targeted IGR use | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Growth of protected cultivation needing residue-free controls | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Inclusion of feed-through IGRs to boost livestock weight-gain efficiency | +1.4% | Global, with early gains in North America and South America | Medium term (2-4 years) |

| Government subsidies for integrated pest-management in staple crops | +1.1% | Asia-Pacific, expanding to Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Maximum-Residue Limits Favor Low-Toxicity IGRs

Regulators tightened tolerances across a range of export crops in 2024, with the United States Environmental Protection Agency setting an upper level of 0.01 ppm for flupyradifurone residues in several fruits and vegetables[2]Source: United States Environmental Protection Agency, “Pesticide Tolerances,” epa.gov. Parallel European curbs on neonicotinoid residues in honey magnify the pull toward chemistry that spares pollinators while keeping residue loads minimal. Chitin synthesis inhibitors such as diflubenzuron meet these dual objectives by degrading quickly in soil yet persisting long enough to interrupt larval molting. Private food-retail standards tighten the compliance loop further, allowing growers who adopt insect growth regulators to command premium price tiers in organic and conventional produce channels.

Resistance to Pyrethroids and Organophosphates Drives Rotation to IGRs

Field reports from Asia-Pacific and the Midwest United States document loss of efficacy for conventional adulticides against key coleopteran and lepidopteran pests. Laboratory screenings show Tribolium castaneum populations surviving three times the labeled rate of deltamethrin, while Rhyzopertha dominica demonstrates cross-resistance to organophosphates. Extension agents, therefore, prescribe rotation schemes that incorporate insect growth regulators to lessen selection pressure on remaining adulticide tools. The economic incentive is clear: growers deploying integrated programs avoid yield losses that would otherwise exceed the cost premium of insect growth regulators by a factor of four in stored grain settings.

Adoption of Precision-Agriculture Spray Drones Enables Targeted IGR Use

Unmanned aerial vehicle fleets now cover over 2 million hectares of paddy and horticulture acreage across China and Southeast Asia. Multi-rotor platforms deliver droplet densities averaging 45 droplets per square centimeter, surpassing ground rigs and making high-value insect growth regulators financially feasible for spot or border treatments. Real-time prescription mapping couples multispectral imagery with pest scouting data to direct IGR sprays precisely where larval hotspots occur, reducing gram-per-hectare rates by up to 30% without compromising control. Lower active-ingredient load improves applicator safety ratings and accelerates regulatory approvals for new drone-ready labels.

Growth of Protected Cultivation Needing Residue-Free Controls

Greenhouse acreage grew 6.4% in North America during 2024, while vertical farms attracted USD 870 million in venture funding. In controlled environments, the absence of natural predators and the premium placed on pesticide-free branding intensify demand for developmental inhibitors that break pest life cycles quietly. Certification bodies for leafy greens cap detectable residues at near-zero, forcing growers toward insect growth regulators that operate at parts-per-billion rates yet align with organic transition plans. Combination products that layer IGR chemistry with entomopathogenic fungi extend protection breadth and minimize resistance risk[3]Source: BASF, “Biological Insecticides by BASF,” agriculture.basf.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slower knock-down versus adulticides limits farmer acceptance | -1.3% | Global, particularly in developing markets | Short term (≤ 2 years) |

| Unclear regulatory pathway for nano-encapsulated IGR formulations | -0.8% | North America and Europe | Medium term (2-4 years) |

| Emerging cross-resistance in coleopteran grain pests | -1.1% | Global, with a concentration in Asia-Pacific | Medium term (2-4 years) |

| Supply volatility for benzoylurea intermediates sourced from China | -0.9% | Global supply chain impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Slower Knock-Down Versus Adulticides Limits Farmer Acceptance

The visible delay between IGR application and pest mortality often discourages growers who equate successful control with immediate insect drop. In smallholder systems where scouting resources are scarce, the absence of quick visual feedback can lead to redundant adulticide sprays that undercut the economics of adopting developmental inhibitors. Training campaigns led by extension specialists and manufacturers must therefore emphasize larval counts and damage thresholds rather than adult knockdown as success metrics. Until awareness spreads, this perception gap caps rapid penetration of the insect growth regulators market in less mechanized regions.

Unclear Regulatory Pathway for Nano-Encapsulated IGR Formulations

Packaged payloads of diflubenzuron in polymer nanospheres promise longer residual control and reduced leaching, yet regulators in the United States and European Union are still drafting risk-assessment frameworks for nano-enabled crop protection. Absence of standardized soil and aquatic toxicity assays raises dossier costs and lengthens time-to-market by three to five years compared with conventional emulsifiable concentrates. Start-ups that pioneer these platforms must shoulder prolonged uncertainty, and their investors typically demand premium returns that can inflate final product pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chitin Synthesis Inhibitors Hold the Lead

In 2024, chitin synthesis inhibitors seized 42.0% of the insect growth regulators market share, a result of their versatility across lepidopteran and coleopteran pest spectra in both field and stored-grain settings. The segment benefits from decades of residue dossier data that expedite registrations in new markets, while continuous formulation tweaks reduce photodegradation, extending spray intervals. Syngenta’s 2025 launch of Advion Trio, which combines pyriproxyfen with novaluron, exemplifies the pivot toward multi-mode blends that enhance efficacy without escalating residue loads. Over the forecast horizon, juvenile hormone analogs are predicted to post an 11.80% CAGR, reflecting their rapid uptake in feed-through livestock products and their favorable compatibility with pollinator protection goals. Ecdysone agonists, although smaller in value, form a strategic buffer against resistance build-up in high-rotation crop systems, solidifying their place in integrated programs.

Biochemical refinements underpin the chitin synthesis inhibitor leadership within the insect growth regulators market. Benzoylurea derivatives now integrate ultraviolet stabilizers that slash active-ingredient breakdown by 36% under field conditions, elevating cost competitiveness against generic pyrethroids. Meanwhile, patent expirations open space for regional formulators to develop low-cost off-patent alternatives tailored to local pest complexes. For juvenile hormone analogs, the introduction of high-purity methoprene crystals supports granular formulations suitable for broad-acre rice paddies, expanding beyond niche stored-grain uses.

By Form: Liquid Concentrates Remain Predominant

Liquid concentrates accounted for 51.30% of the revenue in 2024, as they are used seamlessly in ground rigs, aerial booms, and drone tanks worldwide. High solubility in hydrocarbon carriers enables tank mixing with foliar fertilizers and biological inoculants, supporting growers who strive for single-pass efficiency. Aerosols and foggers, although accounting for a limited share of sales, are projected to grow at a 10.50% CAGR due to their value in sealed environments, such as grain silos and broiler houses, where uniform vapor distribution is crucial. Baits and granules hold steady, serving tree fruit orchards and turfgrass sectors that favor slow release.

Liquid concentrate dominance is poised to continue, as precision-agriculture platforms rely on the known flow dynamics that these formulations deliver reliably. Manufacturers are developing low-viscosity emulsions that are compatible with electric nozzle pulse-width modulation, allowing for variable-rate deployment across a single pass. In contrast, foggers attract investment as warehouse automation rises with robotic units moving along programmable paths, dispersing micron-sized droplets that infiltrate pest harborage sites. Sustained innovation in packaging, such as recyclable stainless-steel canisters, bolsters adoption among sustainability-focused operators.

By Application: Open Cultivated Crops Drive Absolute Demand

Open cultivated crops accounted for 46.80% of the insect growth regulator market share in 2024, as maize, soybean, and cotton producers integrate insect growth regulators to mitigate resistance in complex pest landscapes. Many national IPM subsidy schemes center on these staples, distributing cost-sharing vouchers that directly stimulate purchases. Protected cultivated crops, currently a limited share, are expected to expand at the fastest rate, with a 12.90% CAGR, owing to consumers’ willingness to pay for residue-free tomatoes, peppers, and leafy greens. Stored grain and livestock housing applications collectively sustain a steady baseline, thriving on continuous needs for season-long pest suppression.

The open-cultivated crops segment exemplifies the operational flexibility of the insect growth regulator market. Diflubenzuron applied through center-pivot irrigation reaches soil-dwelling larvae that conventional foliar adulticides miss, while pyriproxyfen seed treatments protect emerging shoots from early infestations without additional field passes. Within protected horticulture, foggable juvenile hormone analogs maintain whitefly suppression inside vertical farms where environmental controls facilitate micro-dose efficacy. Synergies with biological predators further entrench insect growth regulators as the chemical backbone of closed-loop IPM in controlled environments.

By End Use: Farmers and Growers Dominate Purchases

Farmers and growers comprised 50.70% of the 2024 demand, reflecting direct sourcing habits and long-standing relationships with ag-input distributors. Extension networks and digital advisory apps disseminate threshold-based treatment guidelines, reducing knowledge barriers and promoting repeat orders for insect growth regulators. Agricultural Pest-Management Service Providers, although representing a smaller baseline, are on track for the highest 13.50% CAGR because large storage complexes, commercial greenhouses, and urban structures often outsource pest control to certified experts.

Several factors accelerate contractor growth, such as regulatory scrutiny over application logging pushes warehouse operators to engage licensed applicators armed with calibrated fogging devices and data capture systems. Second, insurers now provide policy discounts when third-party professionals oversee IGR treatments, reducing compliance risk. Meanwhile, grower loyalty programs that bundle rebates on drone services and resistance-monitoring tests incentivize farm-level buyers to maintain their leading share.

Geography Analysis

North America retained its leadership position with 33.50% of 2024 sales, owing to a strong regulatory foundation and rapid technology adoption. The United States Environmental Protection Agency maintains clear tolerance schedules for over 15 active insect growth regulator ingredients, giving registrants predictable pathways. Precision-agriculture adoption is particularly advanced in the western United States, where spray drones cover specialty crops such as strawberries and lettuce, validating high-cost per-acre applications. The region’s insect growth regulators market size is anticipated to increase from USD 452 million in 2025 to USD 642 million by 2030, a 7.2% CAGR driven by the adoption of feed-through solutions in the beef and dairy sectors.

Asia-Pacific represents the most dynamic arena, projected at an 11.40% CAGR through 2030 as mechanization and cooperative spray services scale rapidly. China’s prohibition of certain highly toxic pesticides in 2024 immediately shifted procurement budgets toward insect growth regulators that can satisfy both domestic safety objectives and export residue demands. Concurrently, drone fleets supported by provincial subsidies enable variable-rate IGR deployment across fragmented rice terraces, easing entry for smallholders who previously lacked equipment capital. The region’s protected cultivation boom, particularly in Japan, South Korea, and Vietnam, further pulls through high-purity juvenile hormone analogs suited to hydroponic lettuce and strawberry systems.

Europe delivers steady growth anchored in stringent food safety legislation and consumer-driven retailer standards that rank chemical residues near the top of sustainability scorecards. Greenhouse vegetable production in the Netherlands, Spain, and Italy now routinely integrates diflubenzuron fogging cycles, replacing older neonicotinoids restricted for pollinator concerns. Eastern European markets add momentum as the Common Agricultural Policy extends eco-scheme payments that reward IPM adoption. Beyond Europe, South America records an 8.6% CAGR spurred by resistance management programs in soybean, maize, and cotton belts, while Africa’s growth remains nascent but promising due to new intergovernmental initiatives supporting safer crop-protection portfolios.

Competitive Landscape

The insect growth regulators market remains moderately consolidated, with the top five suppliers capturing 57.30% of global revenue in 2024. BASF SE leads with a prominent share, owing to its diverse portfolio, followed by Bayer AG and Syngenta Group. Competitive intensity centers on formulation science, specifically nano-encapsulation, controlled-release matrices, and drone-compatible blends that extend residual performance and cut active-ingredient loads. Bayer’s 2025 introduction of Plenexos, a ketoenol class innovation, promises systemic activity across sucking pests while aligning with stewardship goals.

Leading firms leverage digital agronomy platforms to embed insect growth regulators into data-driven advisory models, guiding application timing and dosage. Syngenta Group's Cropwise system, for example, couples scouting imagery with predictive models to recommend Advion Trio rotation windows, boosting on-label success while gathering anonymized performance data for future research and development direction. Smaller regional formulators carve out niches by tailoring off-patent chitin synthesis inhibitors to local pest spectra, often forming distribution alliances with drone service providers to reach fragmented smallholder markets.

Supply-chain resilience also guides strategic decisions; several leading producers secure alternative benzoylurea intermediate capacity in Eastern Europe and South America to hedge against potential production shocks in the Asia-Pacific region. With agrochemical spending on digital tools projected to rise 11% in 2024, firms that combine chemical innovation with application technology partnerships are poised to strengthen their positions as adoption accelerates across diverse cropping systems.

Insect Growth Regulators Industry Leaders

BASF SE

Bayer AG

Syngenta AG

Corteva Agriscience

Sumitomo Chemical Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bayer AG unveiled Plenexos insecticide, a next-generation ketoenol that moves through leaves and roots to protect crops such as cotton, tomatoes, and lettuce from sap-feeding pests, while meeting tougher sustainability targets ahead of its multi-country rollout in 2026.

- March 2024: Syngenta Group released Advion Trio cockroach gel bait, the first gel to combine pyriproxyfen, novaluron, and indoxacarb, providing pest-management professionals with a single tube that disrupts roach growth while delivering a fast knock-down.

Global Insect Growth Regulators Market Report Scope

| Chitin Synthesis Inhibitors |

| Juvenile Hormone Analogs |

| Ecdysone Agonists |

| Liquid Concentrates |

| Baits and Granules |

| Aerosols and Foggers |

| Open Cultivated Crops |

| Protected Cultivated Crops |

| Stored Grain Facilities |

| Livestock Housing and Feed-Through |

| Agricultural Pest-Management Service Providers |

| Farmers and Growers |

| Feedlot and Dairy Operators |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Product Type | Chitin Synthesis Inhibitors | |

| Juvenile Hormone Analogs | ||

| Ecdysone Agonists | ||

| By Form | Liquid Concentrates | |

| Baits and Granules | ||

| Aerosols and Foggers | ||

| By Application | Open Cultivated Crops | |

| Protected Cultivated Crops | ||

| Stored Grain Facilities | ||

| Livestock Housing and Feed-Through | ||

| By End Use | Agricultural Pest-Management Service Providers | |

| Farmers and Growers | ||

| Feedlot and Dairy Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the insect growth regulators market?

The market was valued at USD 1.35 billion in 2025 and is forecast to reach USD 2.15 billion by 2030.

Which product category leads the insect growth regulators market?

Chitin synthesis inhibitors lead with 42.0% revenue share in 2024.

Which region is growing the fastest for insect growth regulators?

Asia-Pacific is projected to post the highest 11.40% CAGR between 2025 and 2030 due to technology adoption and regulatory shifts.

Why are insect growth regulators preferred over conventional adulticides?

They deliver low residue profiles, reduce resistance build-up, and align with integrated pest management programs while remaining effective against larval stages.

How are drones influencing the adoption of insect growth regulators?

Spray drones enable precise, variable-rate applications that make high-value IGRs cost-effective for precision treatments, accelerating uptake in fragmented farm landscapes.

What role do insect growth regulators play in livestock production?

Feed-through formulations suppress fly emergence in manure, improving weight gain and feed-conversion efficiency while reducing the need for on-animal sprays.

Page last updated on: