Integrated Pest Management Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

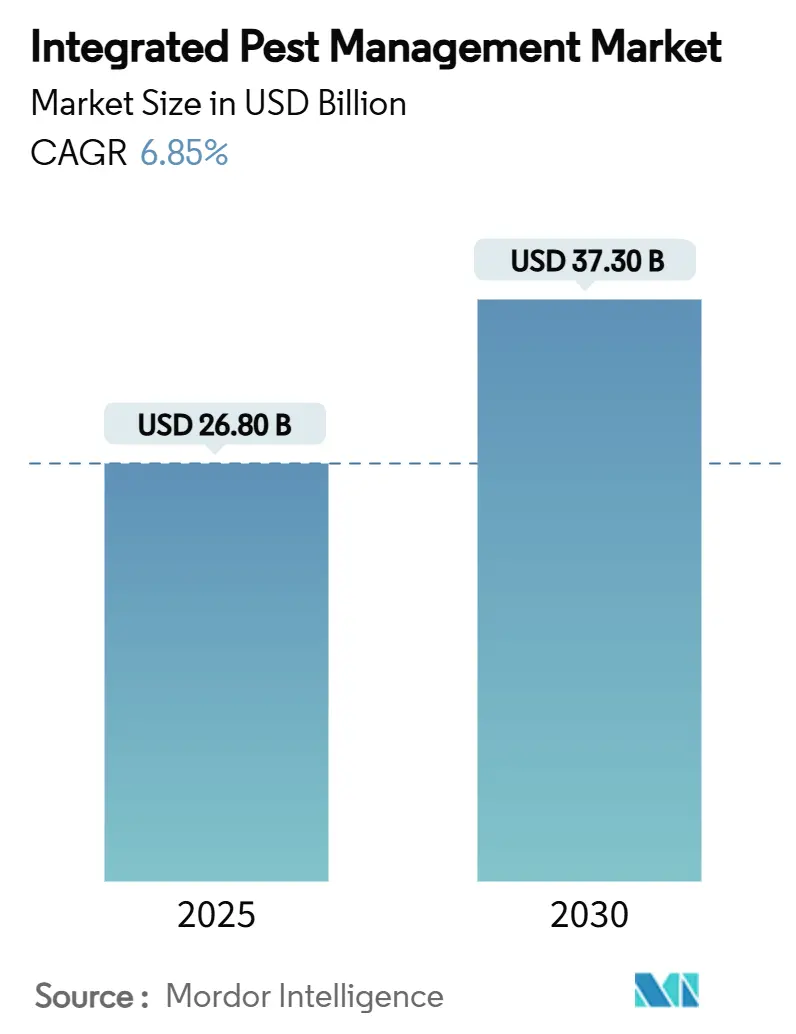

| Market Size (2025) | USD 26.80 Billion |

| Market Size (2030) | USD 37.30 Billion |

| Growth Rate (2025 - 2030) | 6.85% CAGR |

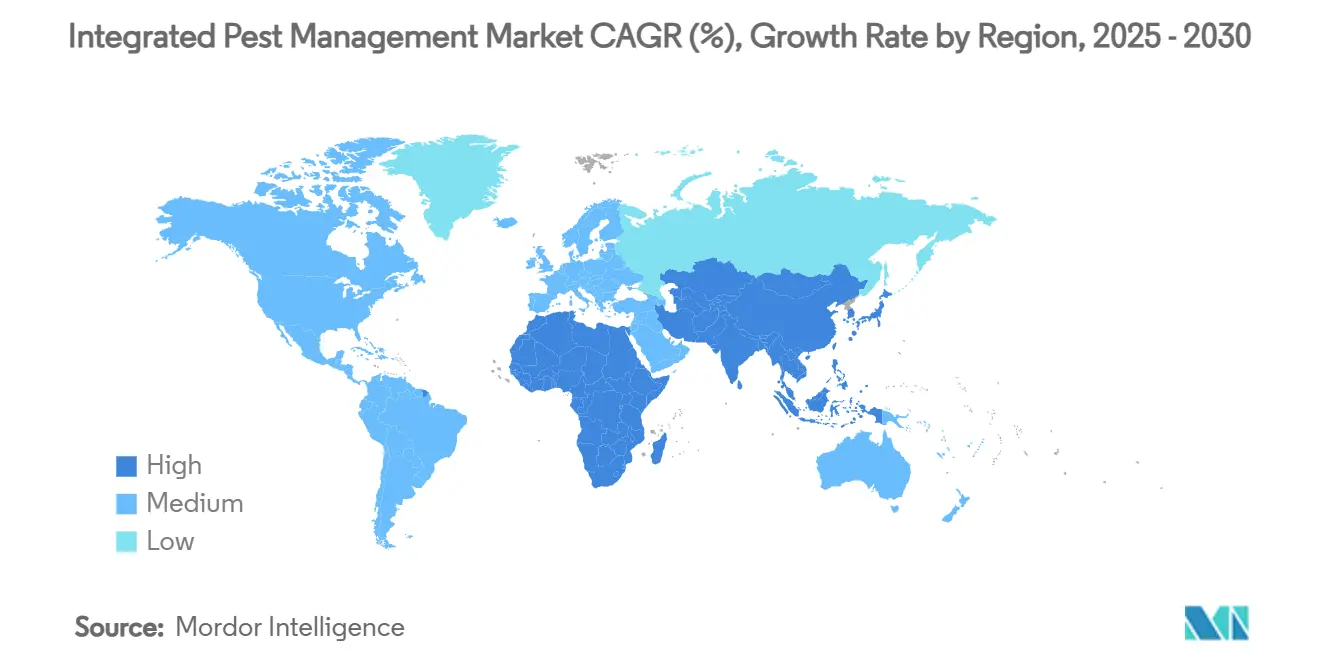

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Integrated Pest Management Market Analysis by Mordor Intelligence

The Integrated Pest Management market size is valued at USD 26.8 billion in 2025 and is projected to reach USD 37.3 billion by 2030, advancing at a 6.85% CAGR. Demand pivots toward hybrid crop-protection programs that lower chemical footprints and improve export compliance, while artificial-intelligence platforms close the timing gap between scouting and treatment. Recent venture-capital inflows totaling USD 3.7 billion validate commercial momentum for digital and biological technologies that enhance return on investment. Regulatory targets in the European Union and California amplify the requirement for residue-compliant solutions, prompting growers to adopt multi-tactic programs that blend biological agents, reduced-risk chemistries, and data analytics. Competitive dynamics increasingly reward firms that bundle AI decision support with field-proven biologicals, creating a new premium tier within the Integrated Pest Management market.

Key Report Takeaways

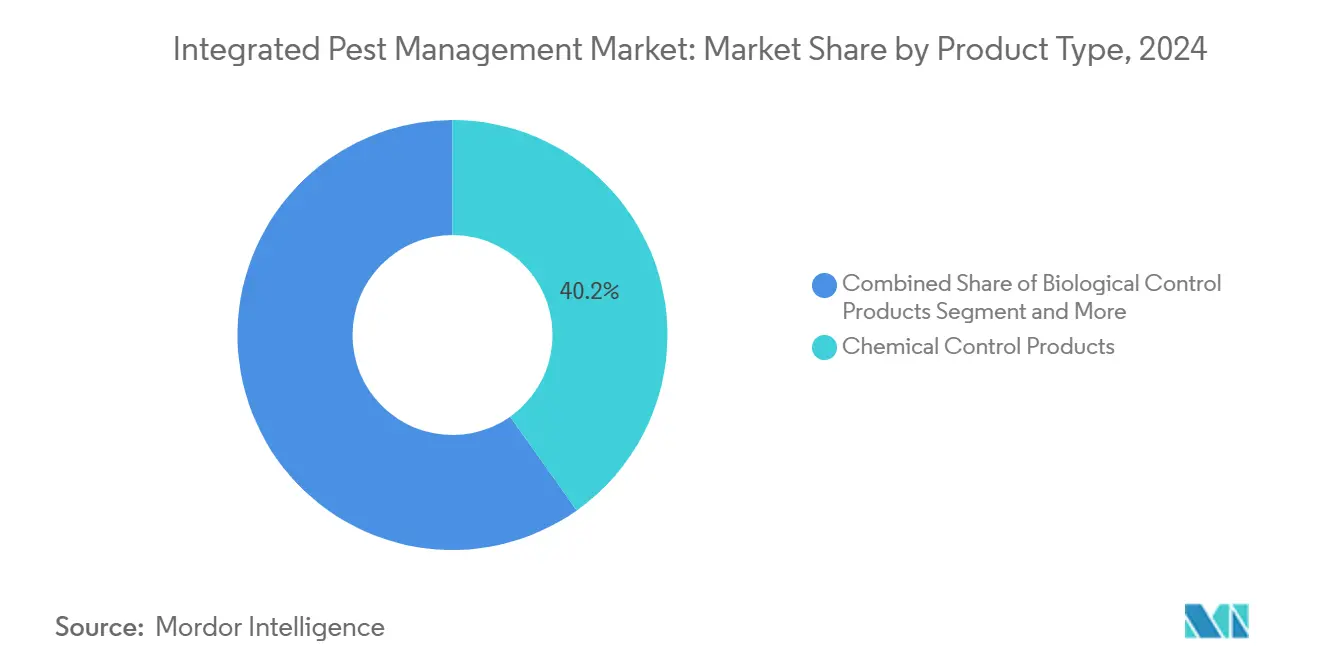

- By product type, chemical control products held 40.2% of the Integrated Pest Management market share in 2024, while biological control products are forecast to expand at an 8.8% CAGR through 2030.

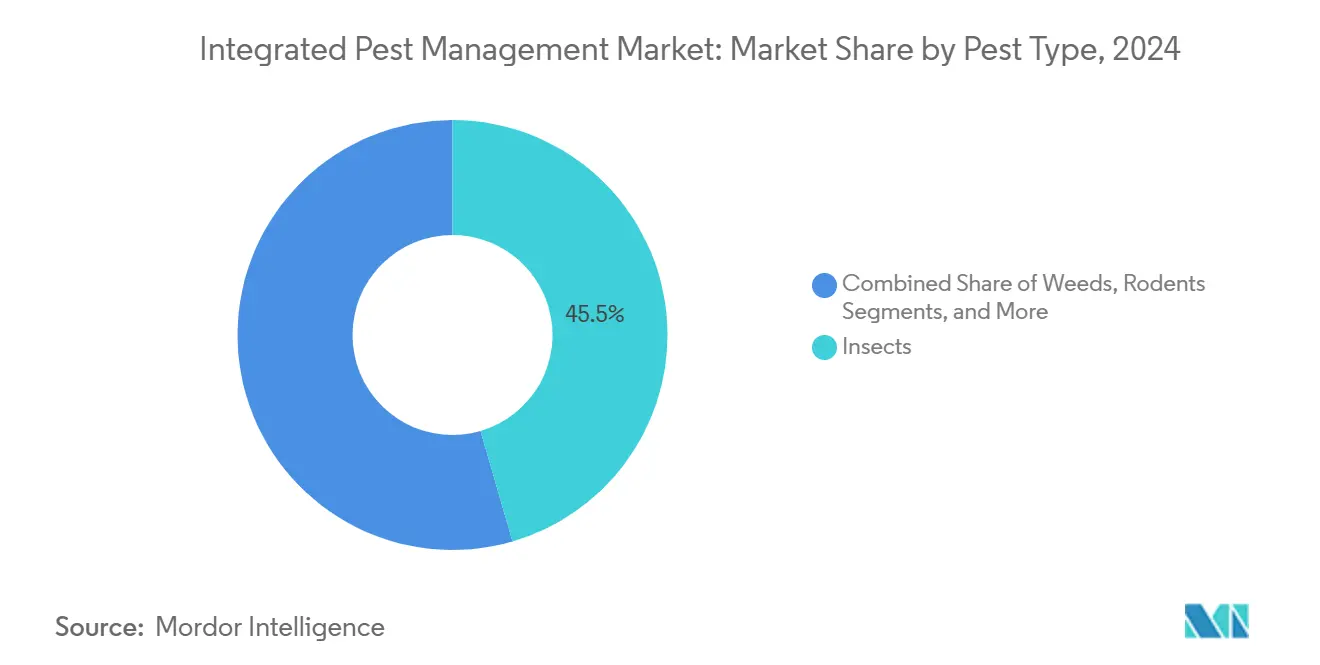

- By pest type, insects led with 45.5% revenue share in 2024, while rodent control applications are projected to advance at an 8.2% CAGR to 2030.

- By end user, agriculture accounted for a 52.0% share of the Integrated Pest Management market size in 2024, and livestock facilities are progressing at a 6.0% CAGR through 2030.

- By geography, North America retained a 36.8% share in 2024, whereas Asia-Pacific is positioned for the fastest growth at a 7.5% CAGR until 2030.

Global Integrated Pest Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing restrictions on chemical pesticide residues in export crops | +1.5% | Global, early enforcement in European Union and North America | Medium term (2-4 years) |

| Rapid adoption of precision-agriculture decision-support tools | +0.8% | North America and European Union core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Subsidies and cost-share programs for sustainable crop protection | +1.2% | North America, European Union, emerging Asia-Pacific markets | Medium term (2-4 years) |

| Escalating pesticide-resistance incidents in major row crops | +0.9% | Global, acute in intensive farming regions | Short term (≤ 2 years) |

| Corporate carbon-footprint targets driving low-toxicity solutions | +0.6% | Global, led by multinational corporations | Long term (≥ 4 years) |

| Venture-capital funding for AI-enabled monitoring platforms | +0.4% | North America and European Union, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Restrictions on Chemical Pesticide Residues in Export Crops

Importing regions are tightening maximum residue limits, forcing exporters to revamp protection programs toward integrated approaches. The European Union lowered Maximum Residue Limits (MRLs) for thiacloprid, zoxamide, acetamiprid, and penconazole in May 2025, thereby shifting procurement standards across global value chains. California’s neonicotinoid restrictions, effective January 2025, prohibit retail sales of imidacloprid and related compounds, creating a USD 2.1 billion opening for biological substitutes.[1]California Department of Pesticide Regulation, “New ban on certain pesticides goes into effect Jan 1,” ucanr.edu Parallel policies in the United Kingdom mandate 10% pesticide-risk reduction by 2030, embedding IPM practices into national action plans. Exporters now treat Integrated Pest Management adoption as an entry requirement rather than a niche practice, prompting record demand for residue-compliant biologicals. Trading companies increasingly favor suppliers who document IPM protocols to guarantee shipment acceptance under the strictest destination rules.

Rapid Adoption of Precision-Agriculture Decision-Support Tools

Artificial-intelligence platforms are replacing manual scouting through continuous sensor monitoring that predicts pest pressure. Syngenta’s Cropwise AI, launched in September 2024, already covers 70 million hectares across the United States and Brazil, with European roll-out slated for 2026. In 2024, FMC’s partnership with CropVue has deployed 6,000 IoT units to generate real-time infestation alerts. Field trials show that precise nozzle control technologies, such as the Stratus AirSprayer, lower application costs of USD 2.85 per acre while curbing drift. Growers gain predictable yield preservation because analytics recommend interventions before economic thresholds are crossed. Growing labor shortages further favor automated scouting, accelerating software subscription uptake across large estates.

Subsidies and Cost-Share Programs for Sustainable Crop Protection

Government funding narrows the adoption gap by offsetting high startup expenses associated with multi-tactic programs. Maryland’s Cover Crop Program reimburses USD 105 per acre for soil-health practices that bundle IPM, while USDA’s EQIP (Environmental Quality Incentives Program) prioritizes projects that reduce chemical exposure in high-value produce belts. Hawaii’s Coffee Berry Borer Subsidy demonstrates pest-specific assistance, reimbursing growers for biological controls that protect export revenues. These incentives cluster adoption within regions, amplifying landscape-level biological control effectiveness as contiguous farms coordinate releases. As subsidy frameworks shift toward regenerative-agriculture metrics, integrated pest management solutions that prove both environmental and economic returns attract the lion’s share of public funds.

Escalating Pesticide-Resistance Incidents in Major Row Crops

Resistance accelerates the pivot away from single-mode-of-action chemistries toward integrated rotations. In European cereals, herbicide-resistant grass weeds now impact 30 million hectares, prompting FMC and Bayer to commercialize Isoflex active by 2026. Bayer’s Vyconic soybeans, introduced at Commodity Classic 2025, stack five herbicide tolerances to maintain efficacy in resistant fields. Resistance drives up crop-loss risk, convincing growers to diversify into biologicals and cultural tactics to prolong chemical life cycles. Corteva and BASF are co-developing trait stacks to reach growers early in the 2030s, illustrating how genetics, chemistry, and biologicals converge within IPM programs. Insurance underwriters increasingly factor documented resistance-management plans into premium calculations, rewarding farms that deploy Integrated Pest Management protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory definitions of integrated practices | −0.7% | Global, acute in cross-border trade | Medium term (2-4 years) |

| High upfront cost of multi-tactic implementation for smallholders | −0.5% | Developing markets and small-scale regions | Short term (≤ 2 years) |

| Limited field efficacy data in tropical and arid climates | −0.4% | Sub-Saharan Africa, Southeast Asia, Middle East | Long term (≥ 4 years) |

| Slow technology-transfer from research stations to growers | −0.3% | Global, pronounced in developing markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Definitions of Integrated Practices

Divergent certification rules force multinational growers to juggle parallel compliance systems, raising transaction costs. The OECD’s (Organisation for Economic Co-operation and Development) harmonization push struggles against national authorities guarding local protocols. California’s 2025 decision to classify chitosan as a minimum-risk active contrasts with the federal Environmental Protection Agency's outlines, illustrating inconsistency within a single market.[2]California Department of Pesticide Regulation, “DPR-25-001—Addition of Chitosan to List of Active Ingredients Allowed in Exempted Minimum Risk Pesticides,” cdpr.ca.gov Australia’s independent review of ag-chem laws proceeds without alignment to European models, further complicating product registrations. Biological-control approvals face duplicated data requirements in each jurisdiction, delaying launches. Exporters incur audits under multiple labels, slowing broad-scale adoption of Integrated Pest Management programs.

High Upfront Cost of Multi-Tactic Implementation for Smallholders

Integrated Pest Management demands concurrent investment in monitoring hardware, biological agents, habitat manipulation, and training, stretching the cash flow of smallholders. Studies in Malawi, Uganda, Bangladesh, Bolivia, and Nepal identify startup costs as the principal obstacle to IPM uptake. Traditional microfinance covers single-input purchases rather than holistic system upgrades, limiting loan availability. Economic returns often accrue over several seasons through lower input bills and soil-health benefits, yet smallholders need immediate profit to meet subsistence needs. Collective action models mitigate costs, but coverage remains uneven in regions with the highest poverty density, constraining CAGR contribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chemical Dominance Persists While Biologicals Accelerate

Chemical control products capture 40.2% of the Integrated Pest Management market share in 2024 due to entrenched distribution and broad-spectrum efficacy. Biologicals deliver the fastest growth at an 8.8% CAGR as the EPA extended tolerance exemptions for Beauveria bassiana, Trichoderma atroviride, and Bacillus strains in 2024.[3]Environmental Protection Agency, “Tolerance Exemptions for Beauveria bassiana and Related Microbial Pesticides,” epa.gov The Integrated Pest Management market size for biologicals in arable crops is poised to expand rapidly as hybrid programs optimize dose rates and application windows. Mechanical and physical tools benefit from robotic weeders and UV-C fungal suppressants that integrate seamlessly into data-driven schedules. Cultural products leverage cover-crop adoption supported by subsidy schemes, reinforcing soil health and biodiversity.

Second-generation bioinsecticides from Bayer and pheromone-based mating disruption from FMC illustrate a pipeline shifting toward living organisms and semiochemicals. Precision sprayers retrofit onto legacy boom rigs, allowing site-specific chemical deployment that sustains efficacy while lowering residues. As resistance escalates, growers blend biologicals with micro-dosed synthetics to safeguard yield, reinforcing a convergent competitive field where product labels blur into service bundles.

By End User: Agriculture Dominates, Livestock Facilities Emerge

Agriculture commands 52.0% of the Integrated Pest Management market share in 2024, spanning broadacre grains and high-value horticulture. IPM deployment in greenhouse vegetables and vertical farms capitalizes on enclosed environments where beneficial insects thrive. Livestock units register a 6.0% CAGR as facility managers tackle fly control and zoonotic disease vectors with integrated hygiene, biological larvicides, and strategic bait stations.

Forestry programs integrate pheromone trapping and drone-based bioagent dispersal to curb invasive bark beetles, while controlled environment horticulture embraces banker-plant systems that sustain predator populations year-round. Area-wide suppression campaigns build community-level resistance management for fruit flies, lowering quarantine risk and securing export premiums. Precision livestock farming platforms now link pest-pressure metrics to water and feed IoT networks, enabling holistic welfare management.

By Pest Type: Insect Leadership with Rapid Rodent Upswing

Insects dominate at 45.5% revenue share in 2024, reflecting high economic injury across row, specialty, and perennial crops. The Integrated Pest Management market size for rodents, although smaller, posts an 8.2% CAGR through 2030 as urban encroachment and biosecure livestock facilities demand non-toxic solutions. Precision vision systems now detect lepidopteran larvae at sub-threshold levels, enabling timed releases of parasitoid wasps that preserve beneficial populations. Species-specific pheromones curb mouse activity in feed mills without contaminating produce, aligning with stricter food-safety audits.

Weed management gains urgency where herbicide resistance spreads, promoting integrated rotations with cover crops, inter-row cultivation, and allelopathic varieties. Fungal pathogen suppression leverages microbial antagonists combined with canopy airflow management to lower leaf wetness. Mite and nematode challenges open niche markets for predatory mites and entomopathogenic nematodes applied via irrigation lines, creating product-service ecosystems around fertigation equipment.

Geography Analysis

North America’s leadership as the largest region with a share of 36.8% in 2024 stems from integrated extension networks, venture-capital density, and policy incentives. USDA EQIP disbursed record funds in 2024 for IPM pivots, and Canada’s Prairie provinces are trialling drone seeding of beneficial nematodes in canola. Canada's Pest Management Centre aids growers through its Pesticide Risk Reduction Program by implementing Integrated Pest Management (IPM) strategies. The program emphasises biopesticides, cultural practices, and decision-support tools to minimise pesticide usage while protecting crop health across greenhouse vegetables, ornamentals, cereals, and pulses. California’s differentiated neonicotinoid rules push innovation in pistachios and almonds, forcing rapid biological adoption.

Asia-Pacific’s acceleration as the fastest-growing region with a CAGR of 7.5% rests on public and private capital collaboration. India’s agritech startup ecosystem supplies low-cost pheromone traps to millions of smallholders, simplifying the adoption of Integrated Pest Management market routines. In April 2025, CABI (Centre for Agriculture and Bioscience International) and CIRAD (French Agricultural Research Centre for International Development) signed an MoU to bolster Integrated Pest Management (IPM) practices in Southeast Asia, empowering smallholder farmers with sustainable, science-based solutions. China channels subsidies toward beneficial insectaries to protect greenhouse vegetables destined for urban mega-markets. Australia exports residue-free grains into Japanese channels that reward verified IPM documentation, closing the incentive loop for growers.

Europe’s policy-driven trajectory tightens chemical-use ceilings, stimulating the Integrated Pest Management market. Germany’s Lower-Saxony horticulture cooperatives standardize biocontrol release schedules across member farms, pooling procurement power. France’s EcoPhyto II+ plan mandates IPM audits, tying insurance discounts to compliance records. The United Kingdom drafts post-Brexit frameworks that favor outcome-based subsidies that reward measurable pesticide-use reduction. In January 2025, the European Union's Horizon Europe project IPMorama has initiated trials to develop advanced Integrated Pest Management (IPM) strategies for wheat, potatoes, and grain legumes. The project emphasizes breeding pest-resistant crop varieties, implementing genetic markers, and testing variety-specific IPM approaches at the farm level.

Competitive Landscape

The Integrated Pest Management arena shows moderate concentration, with Syngenta Group, Bayer AG, BASF SE, Corteva Agriscience, and FMC Corporation controlling about 50% of global revenue and using their scale to blend chemistry, biology, and digital analytics into single-vendor packages. Syngenta Group anchors this model through Cropwise AI, which already guides treatments across 70 million hectares and feeds proprietary field data back into its biological and chemical Research and Development pipelines. Bayer links seed traits, bioinsecticide launches planned for arable crops by 2028, and a 30% greenhouse-gas reduction commitment that pushes downstream growers toward low-toxicity inputs. These incumbents rely on global regulatory expertise and deep distribution networks to keep smaller rivals from reaching scale, yet the heterogeneous nature of IPM solutions leaves pockets of opportunity for specialists.

Mid-tier biological leaders and venture-backed disruptors are exploiting those gaps by focusing on rapid innovation cycles and localised manufacturing. Koppert secured EUR 140 million (USD 151.2 million) in 2024 to expand insectary capacity on three continents. In July 2025, Biobest’s USD 233 million cumulative funding bankrolls acquisitions of regional biocontrol firms that own country-specific registrations, giving the Belgian group a pathway into markets where global chemical players face regulatory delays. Early-stage companies such as Dilepix and CropVue monetize software subscriptions that turn mobile phones and IoT sensors into low-cost scouting networks, attracting smallholders unable to afford premium drones or satellite imagery. These agile entrants often partner with incumbents for distribution while retaining intellectual-property ownership, preserving optionality for future exits.

Collaborations between legacy agrochemical firms and technology startups are reshaping competitive boundaries and accelerating time-to-market for integrated offers. FMC Corporation’s co-development of Isoflex active with Bayer AG tackles grass-weed resistance on 30 million European cereal hectares and pairs the new chemistry with pheromone-based monitoring supplied by its CropVue alliance. Syngenta Group divested its FarMore vegetable seed-treatment platform to Gowan SeedTech in 2024, freeing capital for digital and biological investments that enhance platform breadth. As regulatory pressure intensifies, competitive advantage is tilting toward vendors that can deliver a turnkey stack of real-time diagnostics, resistance-diverse actives, and verifiable sustainability metrics without inflating growers’ operating costs.

Integrated Pest Management Industry Leaders

Syngenta Group

Bayer AG

BASF SE

Corteva Agriscience

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Suterra introduced the CheckMate Grape Mealybug dispenser, which provides pheromone-based control throughout the growing season to prevent pest mating and reduce virus spread in vineyards. The product, validated through multiple years of testing, delivers effective pest management without chemical residues and integrates with existing IPM programs.

- June 2025: FMC Corporation obtained regulatory approval in Ukraine for its Tremisia fungicide, which introduced fluindapyr technology to the EMEA region. The fungicide targets diseases in sunflower, oilseed rape, and wheat crops, protecting more than 10 million hectares.

- March 2025: FMC Corporation and Bayer AG formed a partnership to market Isoflex active herbicide in the European Union and Great Britain. The herbicide targets resistant grass weeds in cereals and oilseed rape crops. The agreement expands FMC Corporation's market presence and introduces a Group 13 herbicide that provides sustained weed control.

- January 2025: Bayer AG formed a partnership with Ecospray, a UK company, to distribute Velsinum, a biological nematicide derived from garlic, in Europe, the Middle East, and Africa beginning in 2026. The product, which leaves no chemical residue, provides an environmentally sustainable alternative to conventional nematicides and improves root health and soil conditions in potato and vegetable cultivation.

Global Integrated Pest Management Market Report Scope

| Cultural Control Products |

| Chemical Control Products |

| Biological Control Products |

| Mechanical and Physical Control Tools |

| Insects |

| Weeds |

| Rodents |

| Fungi |

| Others |

| Agriculture |

| Horticulture |

| Forestry |

| Livestock Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Cultural Control Products | |

| Chemical Control Products | ||

| Biological Control Products | ||

| Mechanical and Physical Control Tools | ||

| By Pest Type | Insects | |

| Weeds | ||

| Rodents | ||

| Fungi | ||

| Others | ||

| By End User | Agriculture | |

| Horticulture | ||

| Forestry | ||

| Livestock Facilities | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current valuation of the Integrated Pest Management market?

The market is projected to be valued at USD 26.8 billion in 2025 and is expected to reach USD 37.3 billion by 2030.

Which product category leads global revenue?

Chemical control products lead with a 40.2% share, although biologicals are growing fastest.

Which region is expanding most quickly?

Asia-Pacific posts the highest forecast growth at a 7.5% CAGR through 2030.

Why are biological solutions gaining traction?

Regulatory residue limits, corporate carbon targets, and escalating resistance challenge reliance on synthetic chemistries, driving demand for biological agents.

How concentrated is supplier power in this market?

The top five companies account for roughly 50% of global sales, indicating moderate concentration with space for new entrants.

What technology trends are reshaping pest control decisions?

Artificial-intelligence platforms, IoT sensors, and precision sprayers enable predictive, site-specific interventions that lower costs and residues.

Page last updated on: