Insect-Based Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 10.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

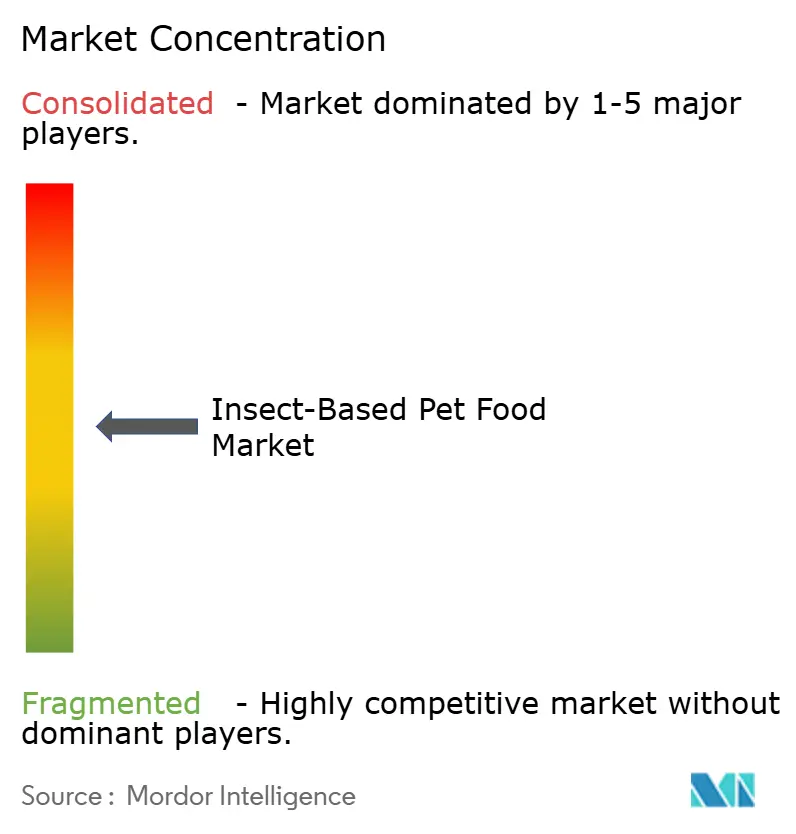

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insect-Based Pet Food Market Analysis by Mordor Intelligence

The insect-based pet food market size was valued at USD 0.95 billion in 2025 and is projected to grow from USD 1.05 billion in 2026 to USD 1.73 billion by 2031, growing at a CAGR of 10.50% from 2026 to 2031. Regulatory clearances in North America and Europe have removed the legal barriers that once discouraged large manufacturers from formulating insect protein. Early adopters pay a premium of 1.5 to 2 times the cost of chicken-based diets because the lower carbon footprint aligns with their sustainability goals. Ingredient suppliers now integrate with food processors to capture waste heat and feed streams, improving margins while reducing emissions. At the same time, direct-to-consumer brands collect subscription data to refine formulations and deepen loyalty in an environment where product launches move at start-up speed[1]Source: United States Food and Drug Administration, “GRAS Notice AGRN 80 – Black Soldier Fly Larvae Oil,” fda.gov .

Key Report Takeaways

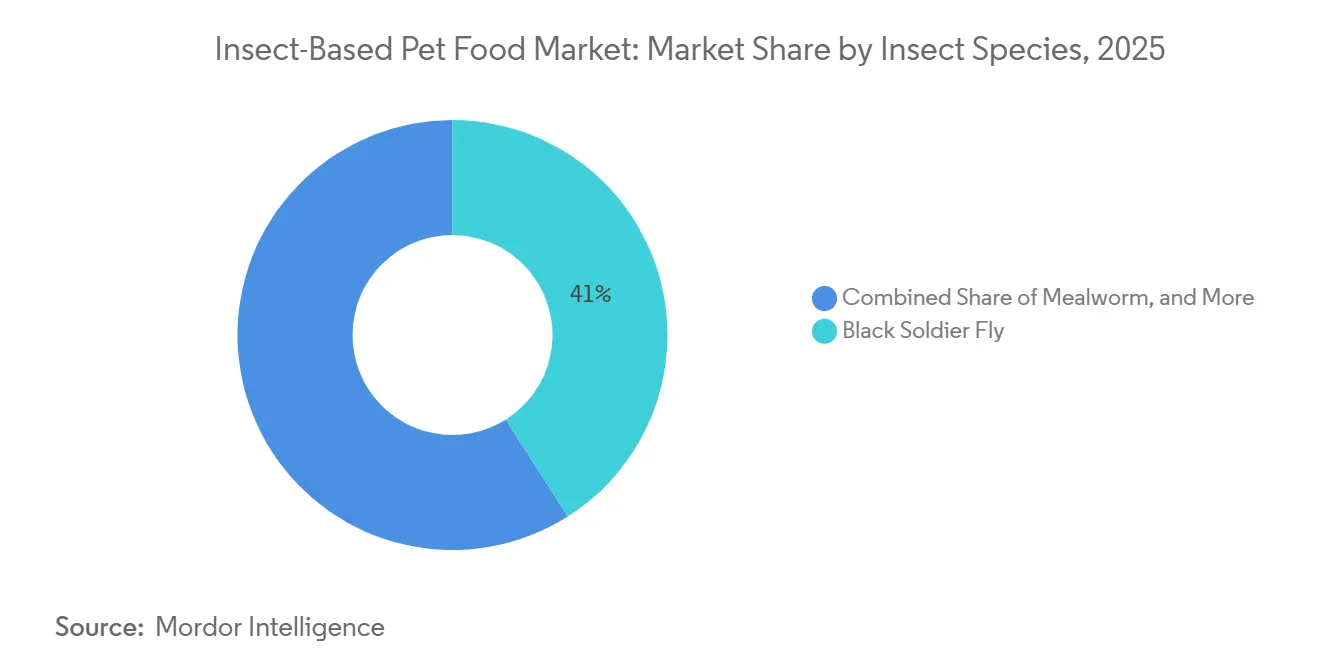

- By insect species, black soldier fly held the largest share, accounting for 41% of the insect-based pet food market share in 2025, while house cricket protein is projected to expand at the fastest 15% CAGR through 2026-2031.

- By pet type, dogs held the largest share, accounting for 66% share of the insect-based pet food market size in 2025, and cats are projected to expand at the fastest 13.5% CAGR from 2026 to 2031.

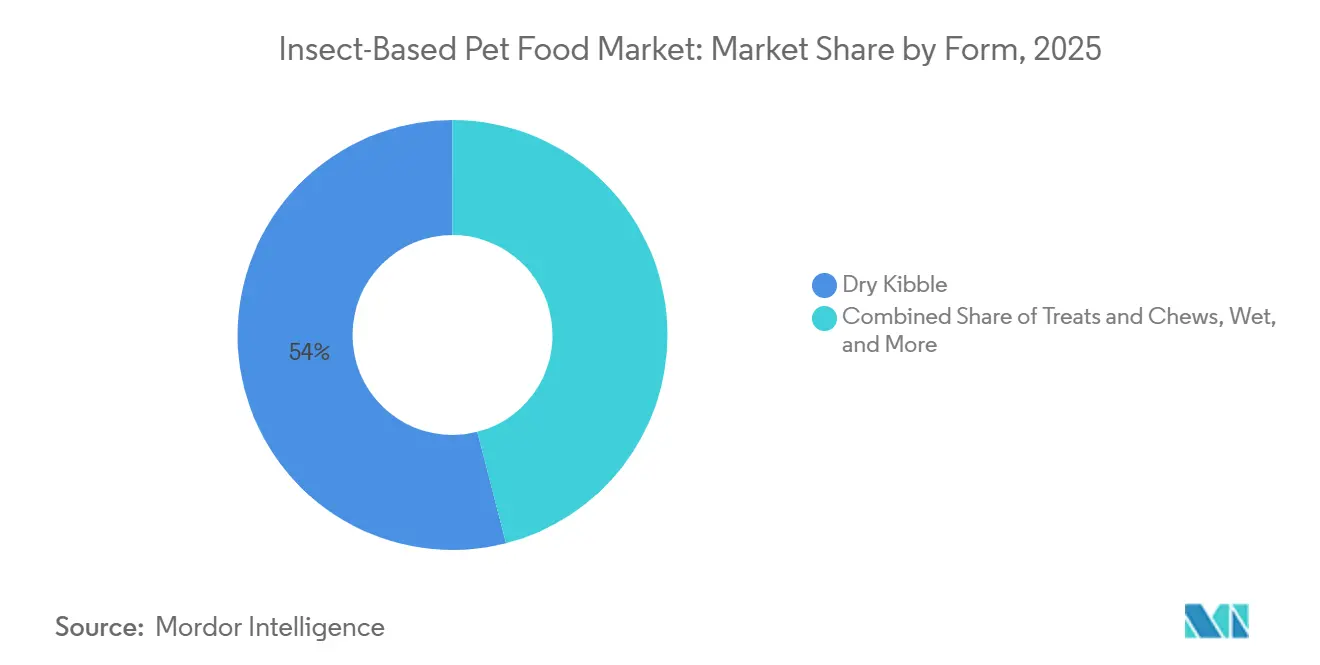

- By form, dry kibble held the largest share, accounting for 54% share of the insect-based pet food market in 2025, and wet formats are forecast to grow at a 15.4% CAGR over 2026-2031.

- By distribution channel, online platforms held the largest share, accounting for 48% of the insect-based pet food market in 2025, and are projected to grow at a 14.8% CAGR from 2026 to 2031.

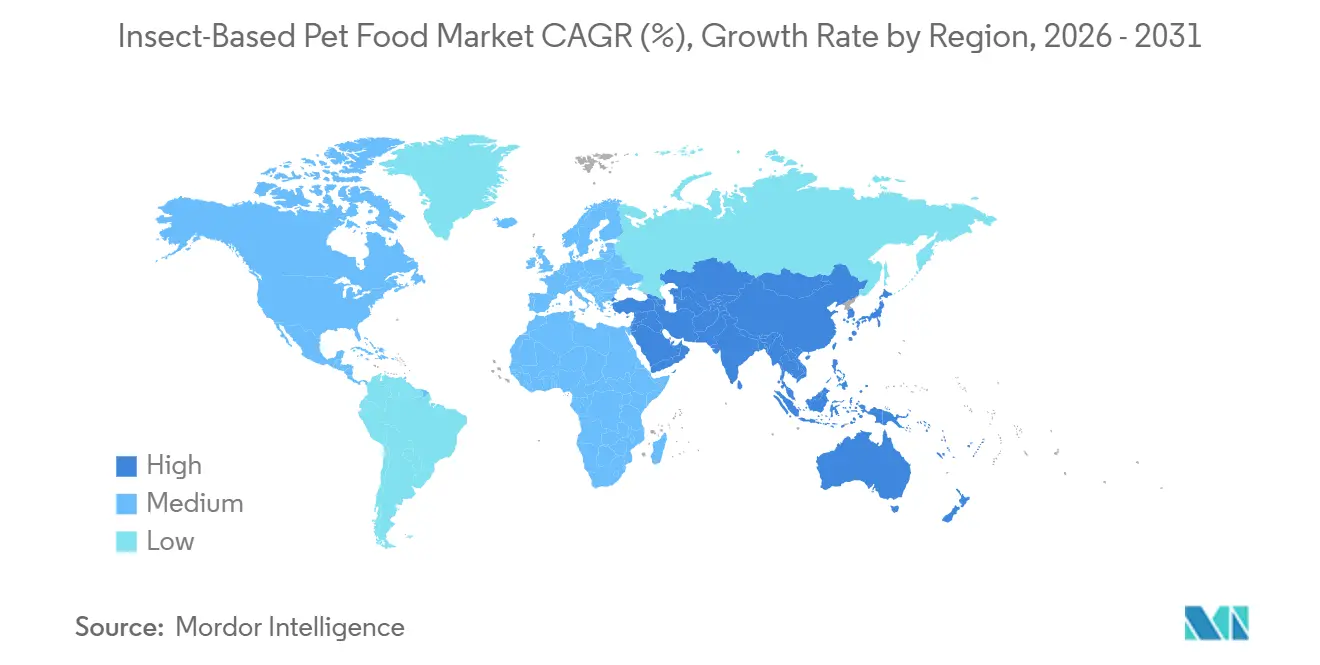

- By geography, Europe accounted for the largest 35.0% market share in 2025, while Asia-Pacific is projected to grow at the fastest 14.8% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Insect-Based Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for sustainable proteins | +7.2% | Global, strongest in Europe, North America, and urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory approvals for insect protein inclusion | +6.8% | North America and Europe core, spillover to the Asia-Pacific and the Middle East | Short term (≤ 2 years) |

| High protein digestibility and hypoallergenic appeal | +5.1% | Global, led by veterinary channels in North America and Europe | Medium term (2-4 years) |

| Lower carbon and water footprint versus meat sources | +4.9% | Europe and Asia-Pacific lead, North America follows | Long term (≥ 4 years) |

| Surplus insect meal from waste management tie-ups | +3.6% | Europe and Asia-Pacific urban centers | Medium term (2-4 years) |

| Subscription-based direct-to-consumer models | +3.2% | North America and Europe, with early uptake in Australia and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Sustainable Proteins

Pet owners increasingly track the environmental score of companion animal diets and reward brands that cut emissions. A 2025 survey of Australian households showed that 70.3% preferred feeding insects to pets overeating insects themselves, demonstrating that pet food offers a comfortable stepping stone into alternative proteins. Multinational firms responded quickly, such as Mars Petcare, which sponsored the Next Generation Pet Food Program in 2024 and followed with an innovation accelerator in 2025. Consumers remain willing to pay premium prices when the ecological benefit is explicit on the pack. As volumes climb and costs rise, the premium is projected to narrow, bringing mainstream shoppers into the insect-based pet food market.

Regulatory Approvals for Insect Protein Inclusion

The insect-based pet food market is experiencing growth due to increasing regulatory recognition of insect-derived ingredients in North America. In January 2025, the Association of American Feed Control Officials (AAFCO) granted official status to dried black soldier fly larvae for use in adult dog and cat food, broadening the regulatory framework for insect protein in companion animal nutrition[2]Source: Association of American Feed Control Officials (AAFCO), Ingredient Definitions Committee Midyear Meeting Agenda, January 21, 2025, aafco.org. Additionally, in October 2024, the U.S. Food and Drug Administration (FDA) issued guidance indicating it generally does not intend to enforce actions against ingredients listed in the 2024 AAFCO Official Publication. These regulatory advancements lower market-entry barriers, foster product innovation, and attract investment in insect-based pet nutrition, thereby driving market growth.

High Protein Digestibility and Hypoallergenic Appeal

Defatted insect meals provide amino acid profiles that rival those of poultry and include chitin fiber, which supports gut health. Clinical veterinarians now prescribe insect-based elimination diets for dogs with chronic dermatitis or digestive sensitivity. Trials published in 2025 reported 80% of dogs consuming black soldier fly treats to the point of full consumption, demonstrating palatability once flavor hurdles are overcome. Premium brands position their products as functional solutions rather than novelties, which reinforces repeat buying. Digestibility scores above 80% keep the nutrient-per-calorie ratio competitive with meat, avoiding the need for large inclusion rates that would inflate cost.

Lower Carbon and Water Footprint Versus Meat Sources

Life-cycle assessments document that black soldier fly meal emits almost 80% less carbon dioxide than poultry meal. European producers co-locate insect farms with food-processing plants to recycle waste heat and water. In 2024, InnovaFeed SAS opened a plant next to Archer Daniels Midland in Illinois that upcycles crop residues into 60,000 metric tons of protein annually. Although critics note that temperate farms burn energy for warmth, integration strategies still tip the carbon balance in favor of insects. Governments eager to meet climate targets increasingly cite insect protein in circular-economy roadmaps, strengthening long-term demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited large-scale insect farming capacity | -4.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Price premium over poultry and meat by-products | -3.9% | Global, strongest in South America, Africa, and rural Asia-Pacific | Medium term (2-4 years) |

| Palatability concerns for finicky pets | -2.7% | Global, especially in feline diets | Short term (≤ 2 years) |

| Cultural resistance in major pet food markets | -2.4% | North America, the Middle East, and parts of the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Large-Scale Insect Farming Capacity

Few facilities surpass the 10,000 metric tons annual threshold required by multinational buyers. Aspire Food Group’s 150,000-square-foot cricket plant in Ontario never reached its designed output and entered receivership in 2025, highlighting scale risks. Disease outbreaks and temperature swings can wipe out an entire cohort within days, forcing costly biosecurity upgrades. Capacity shortages oblige brands to multi-source, which lifts logistics overhead and complicates traceability audits under Hazard Analysis and Critical Control Points certification. Until automated rearing and breeding lines mature, the insect-based pet food market will rely on a narrow supplier pool, limiting growth.

Price Premium Over Poultry and Meat By-products

Manufacturing costs remain high because larvae continue to consume paid feed inputs, such as wheat bran. Ynsect secured EUR 160 million (USD 176 million) in fresh capital in 2023, yet filed for safeguard protection the next year, proving that volume alone does not instantly erase the premium. Pricing is most sensitive in South America and Africa, where disposable income is thin. As rendering plants turn slaughter by-products into cheap meal, shoppers without sustainability priorities will continue to select meat-based diets. Economies of scale, feedstock subsidies, and co-location with food plants are the clearest levers to compress cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insect Species: Black Soldier Fly Leads as House Cricket Accelerates

Black soldier fly held the largest 41% share of the insect-based pet food market size in 2025, underscoring its established farming scale and regulatory acceptance. House cricket protein is the fastest segment, projected to advance at a 15.0% CAGR over 2026-2031 as palatability trials confirm strong acceptance among both dogs and cats. The clear gap between a dominant share and the swiftest growth highlights how early infrastructure advantages contrast with emerging consumer preferences. Together, these two species frame the competitive core of the category, with black soldier fly anchoring volumes and house cricket setting the innovation pace.

The insect-based pet food market for black soldier fly products benefits from integrated plants that convert food-processing residues into protein, oil, and fertilizer, creating a circular-economy storyline that resonates with European retailers. Capacity expansion loans from the European Investment Bank in 2024 funded new facilities in Poland that will supply more than 100 brands with black soldier fly meal and oil[3]Source: European Investment Bank, “EIB Group Financing in Poland Rose to EUR 5.7 Billion in 2024,” eib.org. Cricket farms in Southeast Asia plan to leverage warmer climates to keep energy intensity low and reinforce price competitiveness. Continuous breeding improvements are projected to increase output per square meter, helping producers meet rising demand from premium treat manufacturers. Over the forecast horizon, black soldier fly is set to stay the largest segment, while house cricket will record the swiftest advance in premium and specialty formulations.

By Pet Type: Dogs Dominate while Cats Gain Speed

Dogs commanded the largest 66% market share in the insect-based pet food market size in 2025, driven by higher daily feed volumes and early adopter enthusiasm. Cats, while smaller today, are forecast to have the fastest demand trajectory, with a 13.5% CAGR for 2026-2031, owing to their hypoallergenic positioning and improving wet-food palatability. The contrast shows dogs generate stable core revenue, whereas felines inject accelerated growth that ingredient suppliers cannot ignore. This split encourages manufacturers to balance bulk canine inventories with agile feline launches to optimize portfolio risk.

Birds, reptiles, and small mammals together occupy a marginal position, yet they validate insects as a natural prey source in specialty channels. Hybrid households with multiple pet species increasingly sample insect treats across animals, offering a modest cross-sell boost. Veterinary endorsements for elimination diets in both dogs and cats are increasingly spilling over into these niche categories. Even so, scale constraints and lower feeding volumes mean these segments will stay supplementary relative to the largest dog base and the fastest cat surge.

By Form: Dry Kibble Retains Lead while Wet and Canned Formats Surge

Dry kibble retained the largest 54% of the insect-based pet food market share in 2025 because extrusion lines handle up to 30% insect inclusion without texture problems and offer a long shelf life. Wet recipes post the fastest 15.4% CAGR through 2026-2031 as higher moisture improves aroma and flavor, particularly for cats. This divergence forces producers to split capital between maintaining high-volume kibble runs and expanding retort capacity for moist foods. Strategic allocation ensures supply keeps pace with both the steady volume leader and the rapid climber.

Treats and chews accounted for about one-third of 2025 revenue, acting as trial products that ease consumers into full insect diets. Functional powders and toppers remain small but command premium price points in veterinary clinics where targeted nutrition justifies higher margins. Manufacturers leverage these ancillary formats to showcase versatility and to smooth raw-material utilization across product lines. Collectively, the secondary forms add resilience to the portfolio even though they trail the largest kibble and the fastest wet segments.

By Distribution Channel: Online Expansion Outpaces All Others

Online platforms dominated the insect-based pet food market, accounting for 48% of the market in 2025, and are also the fastest-growing channel, projected to expand at a 14.8% CAGR over 2026-2031 as subscriptions lock in repeat orders. Digital storefronts let brands communicate sustainability metrics and gather real-time feedback, reinforcing customer loyalty at a lower acquisition cost. The dual distinction of being both the largest and fastest makes online indispensable for scaling insect-based pet food. Investment in fulfillment technology and data analytics, therefore, remains a top strategic priority.

Pet specialty stores followed at roughly one-third share, benefiting from knowledgeable staff who can address palatability and nutrition queries on the spot. Veterinary clinics stay a small but trusted outlet where professional endorsement validates hypoallergenic claims, especially for sensitive pets. Supermarkets and hypermarkets capture single-digit market share because price premiums still limit mainstream adoption, though private-label launches could expand their role once costs decline. This multichannel mix provides balance, yet the momentum clearly rests with the expansive reach and speed of online commerce.

Geography Analysis

Europe accounted for the largest 35.0% of the insect-based pet food market share in 2025, maintaining its position as the leading regional market. The region benefits from a well-established regulatory framework, advanced insect farming capabilities, and strong consumer acceptance of sustainable pet nutrition products. Increasing awareness of environmental sustainability and circular economy principles has driven pet owners to adopt alternative protein sources for companion animals. Additionally, the presence of leading insect protein producers, extensive research and development activities, and a mature premium pet food industry continue to support market growth. Strong retail distribution networks and greater product availability across both specialty and mainstream channels further strengthen Europe’s leadership in the global insect-based pet food market.

The Asia-Pacific region is the fastest-growing market, with a projected CAGR of 14.8% during 2026–2031. This growth is driven by increasing pet ownership, higher spending on premium pet nutrition, and rising consumer awareness of sustainable protein alternatives. Additionally, the region is experiencing growing interest in circular economy initiatives that focus on converting food waste into high-value insect protein ingredients. Expanding pet food manufacturing capabilities, increasing investment in insect farming technologies, and the gradual commercialization of novel protein-based pet diets are further enhancing market opportunities. Consequently, the Asia-Pacific region is becoming a significant growth area for insect-based pet food producers and investors.

North America benefits from recent Association of American Feed Control Officials and United States Food and Drug Administration clearances that unlocked mainstream formulation, while Canada rebuilds capacity after earlier production setbacks. The Middle East is gaining traction among affluent pet owners who view hypoallergenic insect diets as a premium wellness upgrade, although cultural perceptions still temper mass uptake. South America remains price-sensitive, but pockets in Brazil and Argentina show steady acceptance of sustainability labeling among younger consumers. Africa’s early adopters cluster in South Africa and Kenya, leveraging e-commerce channels to bypass limited brick-and-mortar assortments. Across all regions, rising climate policy pressure and advances in farming automation are anticipated to compress costs and broaden the distribution of insect ingredients. Public-private funding in Europe and Asia is catalyzing new facilities that will feed both domestic and export markets, while North American producers co-locate with grain processors to secure affordable feedstock streams. As supply solidifies, retailers in slower-moving regions plan pilot assortments that could pivot to full rollouts once pricing narrows toward conventional meat proteins. Collectively, these geographic dynamics position the category to broaden its footprint well beyond the largest European base and the fastest Asia-Pacific growth corridor.

Competitive Landscape

The insect-based pet food market is moderately concentrated, with the top five players accounting for the majority of 2025 revenue. Yora Pet Foods Ltd. builds its position through an online-first model that highlights life-cycle carbon savings to justify premium pricing. Nestlé Purina PetCare Company (Nestlé S.A.) scales faster by blending insect meal with chicken in hybrid recipes that feel familiar to mainstream shoppers. The contrast shows how a niche specialist and a global conglomerate use very different playbooks to defend share and grow volume.

Mars Petcare (Mars Inc.) supports category expansion through marketing that frames insects as inputs for the circular economy rather than exotic ingredients. EnviroFlight LLC (Darling Ingredients Inc.) focuses on black soldier fly oil that enhances skin and coat health in premium lines, securing supply through in-house rearing capacity. Jiminy’s LLC turns product awards into retail listings, proving that third-party validation still matters at the shelf. Collectively, these firms leverage distinctive assets, brand equity, raw-material control, or influencer buzz to address the same sustainability-driven demand wave.

Across the board, companies deepen vertical integration, file patents on automated farming, and pilot franchise models that lower capital hurdles for regional growers. Multinationals monitor distressed assets, aiming to acquire capacity as soon as unit costs fall. Public-sector grants in Europe and North America also funnel new funding into expansion plants, easing the strain of high upfront spending. As economies of scale improve and regulations clarify, these strategic moves are anticipated to widen product availability and accelerate global market adoption.

Insect-Based Pet Food Industry Leaders

Yora Pet Foods Ltd.

Nestlé Purina PetCare Company (Nestlé S.A.)

Mars Petcare (Mars Inc.)

EnviroFlight LLC (Darling Ingredients Inc.)

Jiminy’s LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: InnovaFeed SAS and IRBI formed the FrenchFly research partnership under France 2030 funding to optimize black soldier fly biology and production efficiency. The collaboration should improve yield and cost profiles, enabling ingredient suppliers to scale volumes that meet rising formulation demand.

- June 2025: Mars Petcare (Mars Inc.), Big Idea Ventures, and Givaudan launched the 2025 Global Pet Food Innovation Program to accelerate the development of alternative proteins. The initiative funnels resources and expertise into start-ups, helping bring novel insect-based products to market more quickly and sustaining category momentum.

- April 2025: REPLOID Group opened a customer-operated insect rearing plant in Bavaria, processing 40 metric tons of organic residues daily into pet-grade protein and fertilizer. This new capacity lowers raw-material constraints for European brands and is projected to support faster market growth by widening the regional supply base.

Global Insect-Based Pet Food Market Report Scope

Insect-based pet foods offer sustainable, hypoallergenic, and nutrient-rich alternatives to traditional meat-based diets, utilizing ingredients such as black soldier fly larvae, mealworms, and crickets. The Insect Based Pet Food Market Report is Segmented by Insect Species (Black Soldier Fly, Mealworm, House Cricket, and Others), by Pet Type (Dogs, Cats, and Others), by Form (Dry Kibble, Treats and Chews, Wet, and Powdered Supplements), by Distribution Channel (Pet Specialty Stores, Online, Supermarkets and Hypermarkets, and Veterinary Clinics), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Black Soldier Fly |

| Mealworm |

| House Cricket |

| Others |

| Dogs |

| Cats |

| Others (Birds, Reptiles, and Small Mammals) |

| Dry Kibble |

| Treats and Chews |

| Wet |

| Powdered Supplements |

| Pet Specialty Stores |

| Online (DTC, Marketplaces) |

| Supermarkets and Hypermarkets |

| Veterinary Clinics |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| New Zeland | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Insect Species | Black Soldier Fly | |

| Mealworm | ||

| House Cricket | ||

| Others | ||

| By Pet Type | Dogs | |

| Cats | ||

| Others (Birds, Reptiles, and Small Mammals) | ||

| By Form | Dry Kibble | |

| Treats and Chews | ||

| Wet | ||

| Powdered Supplements | ||

| By Distribution Channel | Pet Specialty Stores | |

| Online (DTC, Marketplaces) | ||

| Supermarkets and Hypermarkets | ||

| Veterinary Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| New Zeland | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the insect based pet food market?

The insect based pet food market size reached USD 1.05 billion in 2026 and is projected to reach USD 1.73 billion by 2031.

How fast is the sector projected to grow over 2026-2031?

The market is forecast to register a 10.50% CAGR during 2026-2031, driven by regulatory approvals and sustainability demand.

Which insect species holds the largest revenue share?

Black soldier fly ingredients led with 41% share in 2025, reflecting mature farming infrastructure.

Which region will grow the fastest through 2031?

Asia-Pacific is projected to expand at the strongest 14.8% CAGR as urban pet ownership rises and governments push circular food systems.

Who are the leading commercial brands today?

Yora Pet Foods Ltd., Nestlé Purina PetCare Company (Nestlé S.A.), Mars Petcare (Mars Inc.), EnviroFlight LLC (Darling Ingredients Inc.), and Jiminy’s LLC are the leading brands.

Why do veterinarians recommend insect protein diets?

Insect meals deliver high digestibility and hypoallergenic properties, making them suitable for pets with poultry or beef sensitivities and supporting clinical nutrition strategies.

Page last updated on: