Pet Insect Repellents Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

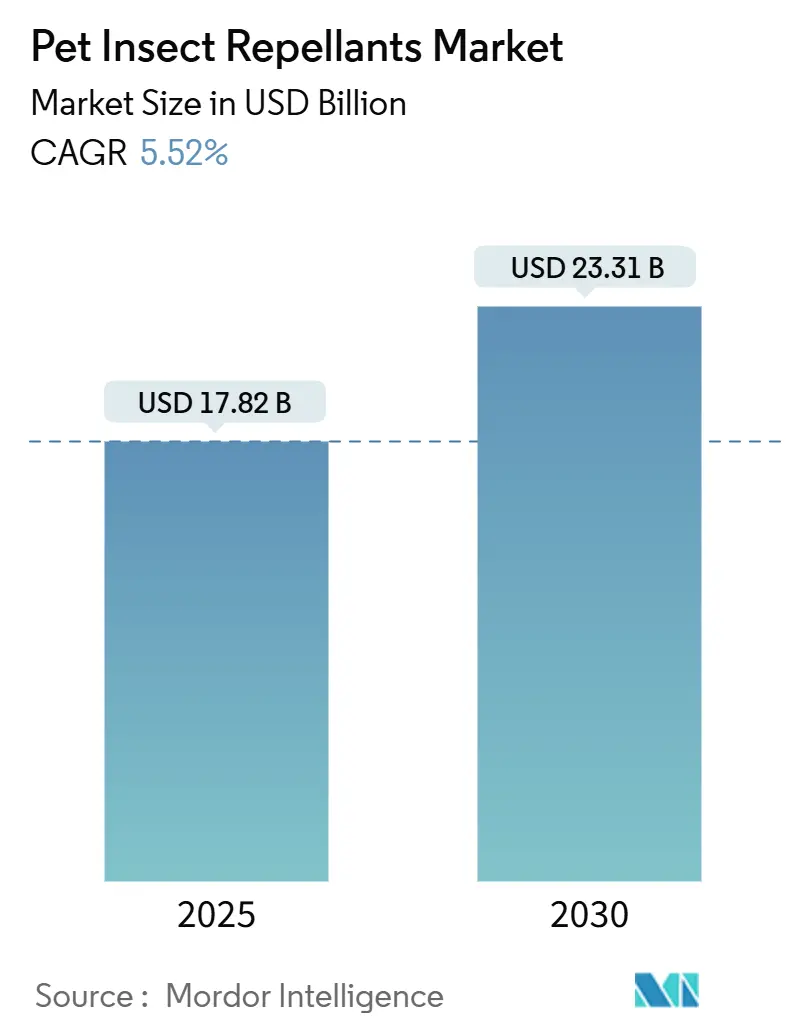

| Market Size (2025) | USD 17.82 Billion |

| Market Size (2030) | USD 23.31 Billion |

| Growth Rate (2025 - 2030) | 5.52% CAGR |

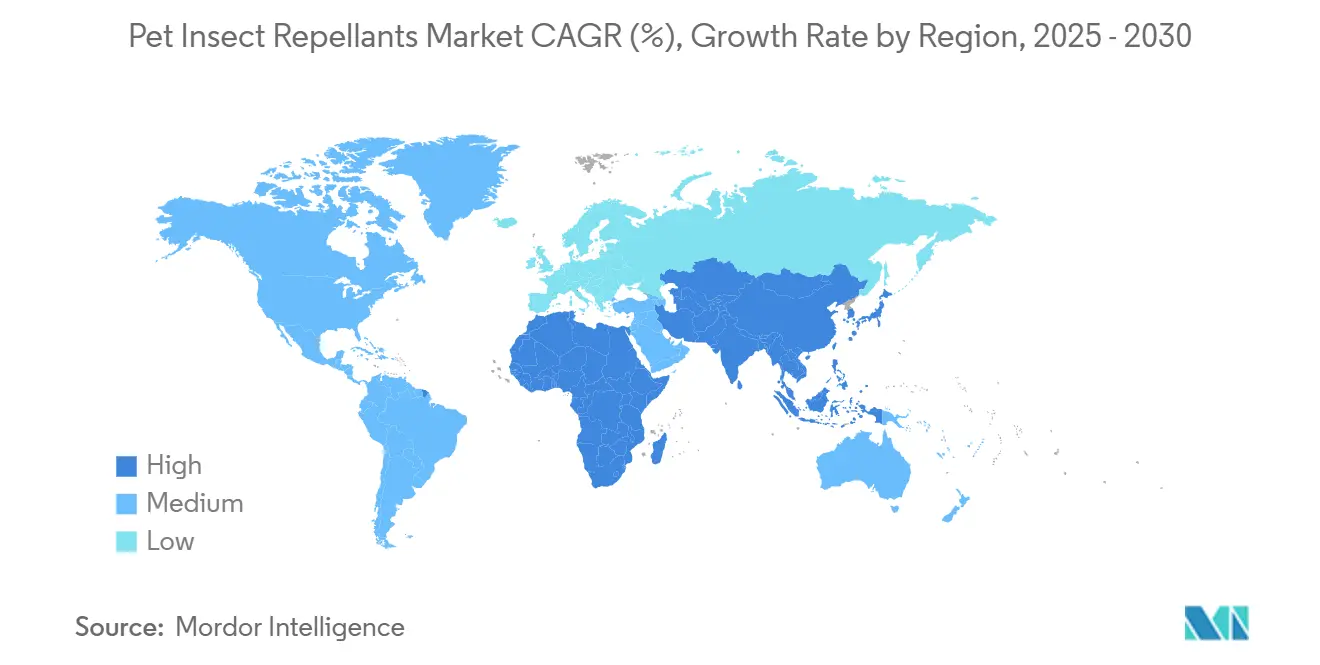

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Insect Repellents Market Analysis by Mordor Intelligence

The pet insect repellents market size is USD 17.82 billion in 2025 and is projected to reach USD 23.31 billion by 2030, growing at a CAGR of 5.52% during the forecast period. The market growth is driven by increasing pet ownership, climate-related vector growth, and premium product preferences among Gen Z households. Gen Z represents 18.8 million of American pet-owning households, showing a 43.5% year-over-year increase, with significant spending on preventive health products. Extended warm weather periods have transformed flea and tick prevention from a seasonal to a year-round necessity. The market is experiencing strong growth in long-acting systemic formulations, driven by veterinarians' preference for products with simplified dosing schedules. E-commerce has emerged as the fastest-growing distribution channel, as most pet owners now purchase parasite control products online.

Key Report Takeaways

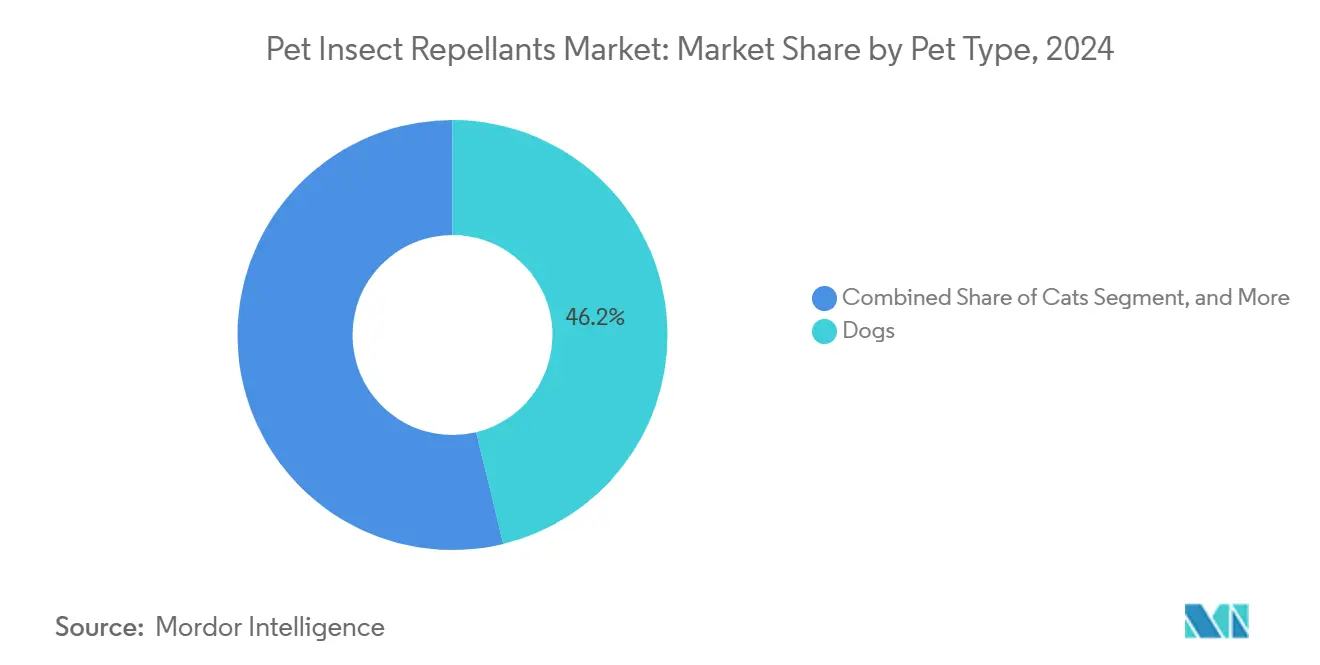

- By pet type, dogs led with 46.2% of the pet insect repellents market share in 2024, while cats are forecast to expand at a 7.8% CAGR through 2030.

- By insect type, fleas captured 52.6% of the pet insect repellents market size in 2024, whereas ticks are set to grow at a 6.4% CAGR to 2030.

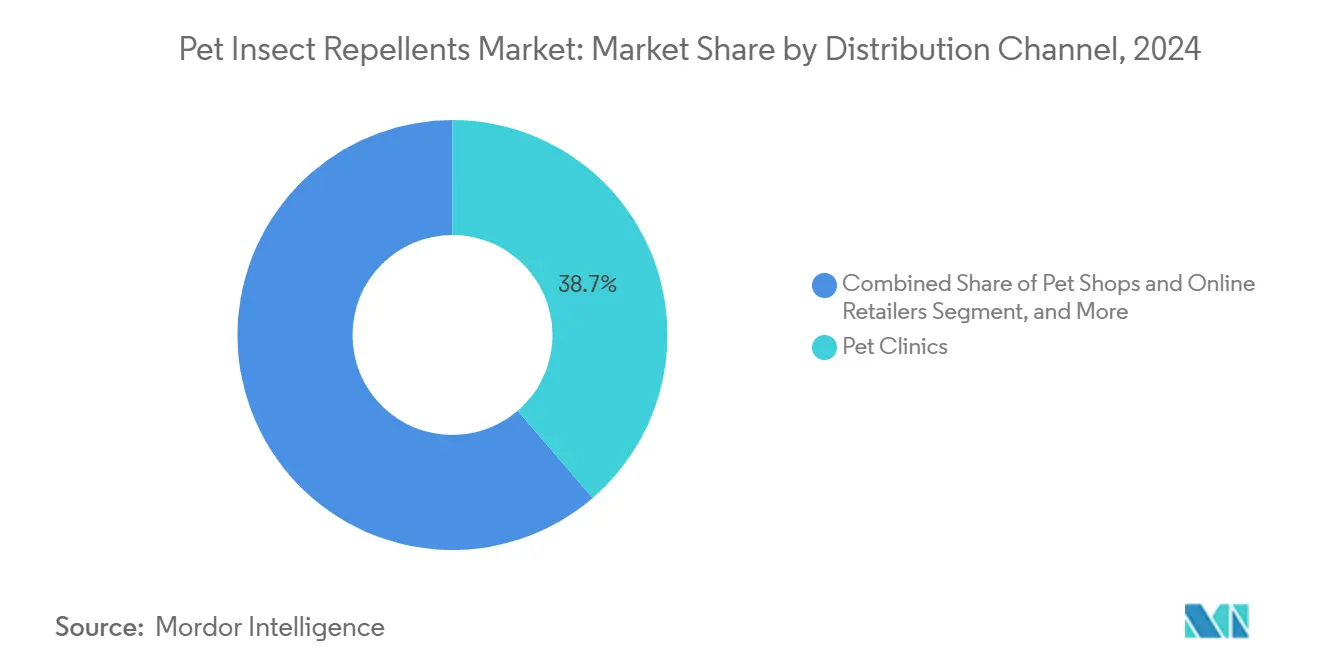

- By distribution channel, pet clinics held a 38.7% share of the market revenue in 2024, and pet shops and online retailers are forecast to register a 7.3% CAGR through 2030.

- By geography, North America accounted for 44.5% of the market revenue in 2024, while the Asia-Pacific region is forecast to grow at a CAGR of 6.6% through 2030.

- The market is moderately consolidated, with the top five companies - Phibro Animal Health Corporation (Zoetis Inc.), Elanco Animal Health Incorporated, Boehringer Ingelheim International GmbH, Merck & Co., Inc., and Virbac SA collectively holding the majority of the market share in 2024.

Global Pet Insect Repellents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding companion-animal ownership in developed economies | +1.0% | North America and Europe | Medium term (2-4 years) |

| Year-round vector proliferation from climate change | +1.3% | Global, temperate zones | Long term (≥ 4 years) |

| Shift toward long-acting systemic formulations | +0.8% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Premiumization of pet wellness spend in Gen-Z households | +0.6% | Global, led by developed markets | Short term (≤ 2 years) |

| Growth of e-commerce channels for vet products | +0.5% | Global, fastest in Asia-Pacific | Short term (≤ 2 years) |

| AI-based tick hotspot forecasting integrated into product bundling | +0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Companion-Animal Ownership in Developed Economies

Pet ownership in the United States increased to 94 million households in 2024, up from 82 million in 2023, with Gen Z households being the predominant owners of multiple pets. The higher number of pets per household drives increased demand for flea and tick products. Urbanization trends and delayed parenthood have redirected discretionary income toward pet care. The average annual expenditure on household pets reached USD 1,332 in 2024, with preventive care accounting for an increasing portion of spending. The established veterinary networks in North America and Europe enable regular parasite screening, supporting demand for premium products. The Food and Drug Administration Center for Veterinary Medicine's oversight strengthens consumer trust in product safety.

Year-Round Vector Proliferation from Climate Change

Climate change has altered vector seasonality and geographic distribution, extending transmission periods and creating a need for year-round protection. Rising temperatures allow tick species like Ixodes scapularis to expand northward and maintain longer active seasons[1]Source: U.S. Global Change Research Program, “Changing Ecosystems and Infectious Diseases,” toolkit.climate.gov. Ticks now emerge two to three weeks earlier on average, increasing exposure periods for dogs and cats. The 2025 emergence of the Asian longhorned tick in the United States led to label expansions for products including Simparica Trio and Bravecto. Veterinary reports indicate increased cases of canine ehrlichiosis and Lyme disease in previously low-risk states, highlighting the importance of continuous protection. The associated costs encourage pet owners to choose combination products that target multiple vectors.

Shift Toward Long-Acting Systemic Formulations

The industry is shifting toward extended-duration formulations that reduce dosing frequency while maintaining efficacy, addressing compliance challenges in treatment outcomes. Monthly dosing remains problematic, leading to increased adoption of injectable or extended-release chewables that provide up to 12 months of protection per dose. Merck & Co., Inc.'s long-acting Bravecto injection received a positive opinion from the Committee for Veterinary Medicinal Products in March 2025, providing year-long protection. Clinical trials demonstrate equal or superior efficacy compared to monthly doses, while preventing gaps that can occur with missed doses. Elanco's Credelio Quattro combines four active ingredients to target six parasite classes, reflecting the industry trend toward comprehensive solutions. These developments enable veterinarians to improve treatment outcomes and offer premium products to owners concerned about compliance.

Premiumization of Pet Wellness Spend in Gen-Z Households

Gen Z pet owners exhibit distinct purchasing patterns, focusing on premium products and wellness solutions, which contributes to market value growth. According to surveys, 78% of Gen Z dog owners and 71% of cat owners use calming products, showing high adoption of specialized health solutions, including preventive parasite control. In Asian markets, Gen Z households allocate 50-100 USD monthly for pet care, exceeding traditional spending levels and supporting premium product segments. Product discovery primarily occurs through social media platforms, including TikTok and Instagram, prompting manufacturers to adapt their marketing approaches to visual content and influencer collaborations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event recalls undermining consumer trust | -0.8% | Global, mainly developed markets | Short term (≤ 2 years) |

| Price sensitivity in emerging economies | -0.6% | Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Growing popularity of insect-repellent substitutes | -0.4% | Global | Medium term (2-4 years) |

| Supply bottlenecks for key actives | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Recalls Undermining Consumer Trust

The market expansion faces constraints due to regulatory recalls and safety concerns related to isoxazoline-class compounds, which particularly affect premium product segments. The Food and Drug Administration's reports of neurologic adverse events have intensified scrutiny of isoxazoline compounds. Between 2018 and 2022, the Environmental Protection Agency documented 842 neonicotinoid poisoning incidents, with four human fatalities linked to pet treatments[2]Source: Env. Health Perspectives Authors, “Human acute poisoning incidents linked to neonicotinoids,” Environmental Health Perspectives, ehponline.org. Product recalls have diminished consumer confidence, especially for premium and newly introduced products. Companies offering single-ingredient alternatives with established safety records use this uncertainty to their advantage. The implementation of stricter labeling requirements by regulatory agencies has extended new-product approval timelines and increased pharmacovigilance program costs.

Price Sensitivity in Emerging Economies

Economic constraints in developing markets restrict the adoption of premium parasiticide formulations, despite increasing pet ownership rates. Registration fees across the Association of Southeast Asian Nations (ASEAN) range from USD 350 to USD 10,500, with local trial requirements increasing launch costs[3]Source: Asian Animal Health Association, “ASEAN AH Regulatory Benchmarking Survey,” asiananimalhealth.org. Import duties and currency fluctuations raise retail prices by 15-25%. Price elasticity values of -1.2 to -1.8 indicate that minor price increases significantly reduce demand, particularly for combination and injectable products. Limited local manufacturing capabilities for complex active pharmaceutical ingredients necessitate imports, adding costs through distribution chains and regulatory compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dogs Dominate Despite Cat Acceleration

Dogs account for 46.2% of the insect repellent market share in 2024, driven by their higher exposure to parasites through outdoor activities and larger body surface areas that require protection. The segment's growth stems from established veterinary protocols and increased owner awareness of tick-borne diseases, such as Lyme disease and ehrlichiosis, which primarily affect dogs. The development of combination products enhances this segment, with Elanco Animal Health Incorporated's Credelio Quattro offering protection against six parasite types in a single monthly dose.

The cat segment is projected to grow at a 7.8% CAGR through 2030, driven by the increasing number of indoor-outdoor cat populations and heightened awareness of flea-transmitted diseases, including bartonellosis and tapeworm infections. The segment's expansion aligns with demographic trends toward apartment living, where cats are preferred pets among young urban professionals. In 2024, Revolution Plus received FDA approval for tapeworm prevention through flea control, addressing specific feline health needs. Birds and other animals represent smaller market segments but show consistent growth as exotic pet ownership increases, particularly in urban areas.

By Insect Type: Flea Dominance Faces Tick Challenge

Fleas command 52.6% of the insect repellents market size in 2024, maintaining historical dominance through year-round reproduction cycles and rapid environmental infestation potential that requires sustained treatment protocols. Ctenocephalides felis represents the primary target species across geographic markets, with female fleas producing up to 50 eggs daily under optimal conditions that create persistent household contamination risks. The segment benefits from established consumer awareness and veterinary education programs that emphasize environmental control alongside pet treatment.

Ticks exhibit accelerated growth at a 6.4% CAGR through 2030, driven by climate-enabled geographic expansion and emerging species threats, including Asian longhorned tick establishment across multiple United States states. In 2024, regulatory label expansions demonstrate the tick segment's strategic importance, with major manufacturers securing Food and Drug Administration approvals for Haemaphysalis longicornis treatment across multiple product lines, including Zoetis' Simparica Trio and Merck's Bravecto formulations, DVM360. Flies, bees, and other insects represent niche segments with specialized applications, particularly in rural and agricultural settings where livestock-companion animal interfaces create unique exposure scenarios. Mites and worms categorized under "other insects" demonstrate consistent demand through dermatological applications and internal parasite control, though growth remains constrained by diagnostic complexity and treatment duration requirements.

By Distribution Channel: Pet Clinics Lead Digital Disruption

Pet clinics maintain 38.7% of the insect repellents market share in 2024, supported by their professional expertise and diagnostic capabilities. These clinics effectively position premium products and recommend combination therapies. The veterinary channel's strength stems from prescription-only medicine regulations, which create distribution advantages for systemic parasiticides and combination formulations. The segment's stability is reinforced through value-added services, including parasite testing, vaccination protocols, and wellness plans that incorporate preventive treatments.

Pet shops and online retailers show the highest growth rate at 7.3% CAGR through 2030, driven by omnichannel purchasing trends and direct-to-consumer market development. Digital platforms offer subscription models and automated delivery services that enhance treatment compliance while reducing costs through bulk purchasing. Other distribution channels, including pest control companies and direct pet owner purchases, remain fragmented with specific applications. Regulatory restrictions on prescription-only medicines and requirements for professional oversight of systemic treatments limit their growth.

Geography Analysis

North America held 44.5% of the pet insect repellents market share in 2024. This dominance stems from high per-pet spending, widespread veterinary services, and efficient Food and Drug Administration approval processes that take 12 to 18 months. The region's advanced diagnostic capabilities and professional education programs encourage preventive treatment adoption. While climate change extends protection requirements beyond traditional seasons in temperate zones, market maturity limits growth as penetration rates near saturation among current pet populations.

Asia-Pacific is projected to grow at a 6.6% CAGR through 2030. Pet ownership is projected to increase to 170-200 million animals by 2024, driving the adoption of related products. Urban millennials' preference for smaller dog breeds and cats increases the need for indoor parasite prevention. Distribution channels expand through e-commerce platforms such as Alibaba's Tmall, while local companies develop herbal alternatives to meet sustainability requirements.

Europe maintains mid-single-digit growth through premiumization and European Medicines Agency regulatory harmonization. Long-lasting injectable treatments appeal to busy pet owners, while strict pharmacovigilance supports the adoption of new chemical formulations. South America and Africa, despite smaller market shares, offer growth opportunities. Brazil's expanding veterinary networks and South Africa's rising urban pet ownership provide entry points for international companies prepared to address regulatory requirements.

Competitive Landscape

The market is moderately consolidated, with the top five companies - Phibro Animal Health Corporation (Zoetis Inc.), Elanco Animal Health Incorporated, Boehringer Ingelheim International GmbH, Merck & Co., Inc., and Virbac SA collectively holding the majority of the insect repellents market share in 2024. Companies compete through product differentiation in dosing duration and protection spectrum, as demonstrated by Merck's 12-month Bravecto injection and Elanco's Credelio Quattro launch in January 2025.

The industry's growth strategies include mergers and acquisitions, while biotechnology companies develop new technologies such as RNA interference and microencapsulation that could affect traditional chemical-based products. Patent applications show increased research focus on new delivery methods and combination active ingredients. Isoxazoline-class compounds dominate recent regulatory submissions, though safety concerns create opportunities for alternative chemical formulations. Companies enhance their market position through partnerships with digital pharmacies and subscription services, utilizing customer data for sales optimization.

Environmental sustainability has become a significant factor in market positioning, particularly among younger consumers. Companies incorporate recyclable packaging and carbon-neutral shipping practices to differentiate their products, while retailers' environmental requirements influence product placement and market share. The market demonstrates diverse pricing approaches, with companies offering value packs in price-sensitive regions and premium injectable products in developed markets.

Pet Insect Repellents Industry Leaders

Phibro Animal Health Corporation (Zoetis Inc.)

Elanco Animal Health Incorporated

Boehringer Ingelheim International GmbH

Merck & Co., Inc.

Virbac SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Merck & Co., Inc. received U.S. Food and Drug Administration (FDA) approval for Bravecto Quantum (fluralaner for extended-release injectable suspension), an injectable product that provides year-long protection against fleas and ticks in dogs. The FDA approval of Bravecto Quantum offers veterinarians and pet owners a highly effective treatment option for flea and tick prevention in dogs.

- January 2025: Boehringer Ingelheim International GmbH launched a new chewable tablet, Frontpro, for treating fleas and ticks in dogs. The tablet provides effective protection against fleas and ticks while complementing the regular care and veterinary advice pet owners receive.

- October 2024: The U.S. Food and Drug Administration (FDA) approved Elanco Animal Health Incorporated's Credelio Quattro (lotilaner, moxidectin, praziquantel, and pyrantel chewable tablets). The product is the most comprehensive oral parasiticide for dogs, protecting against six parasite types: fleas, ticks, heartworms, roundworms, hookworms, and tapeworms. The medication is available as a monthly chewable tablet for dogs aged eight weeks and older.

Global Pet Insect Repellents Market Report Scope

Pet insect repellent refers to the chemicals that help pets avoid being bitten by insects such as ticks, flies, and fleas, among others. The study was carried out in terms of the B2C category.

The Global Pet Insect Repellent Market is segmented by Pet Type( Dog, Cat, Birds, and Other Animals), Insect Type (Ticks, Flies, Bees, Fleas, and Other Insect Types); By End User/Application( Pet Clinic, Pet Shops, and Other End Users); and By Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers the market size and forecasts in value (USD million) for all the above segments.

| Dogs |

| Cats |

| Birds |

| Other Animals |

| Fleas |

| Ticks |

| Flies |

| Bees |

| Other Insect Type |

| Pet Clinics |

| Pet Shops and Online Retailers |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Pet Type | Dogs | |

| Cats | ||

| Birds | ||

| Other Animals | ||

| By Insect Type | Fleas | |

| Ticks | ||

| Flies | ||

| Bees | ||

| Other Insect Type | ||

| By Distribution Channel | Pet Clinics | |

| Pet Shops and Online Retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the global pet insect repellants market in 2025?

The market is valued at USD 17.82 billion in 2025 and is projected to reach USD 23.31 billion by 2030.

Which companion animal leads demand for parasite repellants?

Dogs command the largest share at 46.2% because of higher outdoor exposure and well-established veterinary protocols.

Why is Asia-Pacific the fastest-growing region?

Rapid pet adoption, robust e-commerce infrastructure, and rising disposable income push Asia-Pacific to a 6.6% CAGR through 2030.

How does climate change affect product demand?

Warmer temperatures lengthen flea and tick seasons, creating year-round exposure risks that drive continuous product usage.

Page last updated on: