Online Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

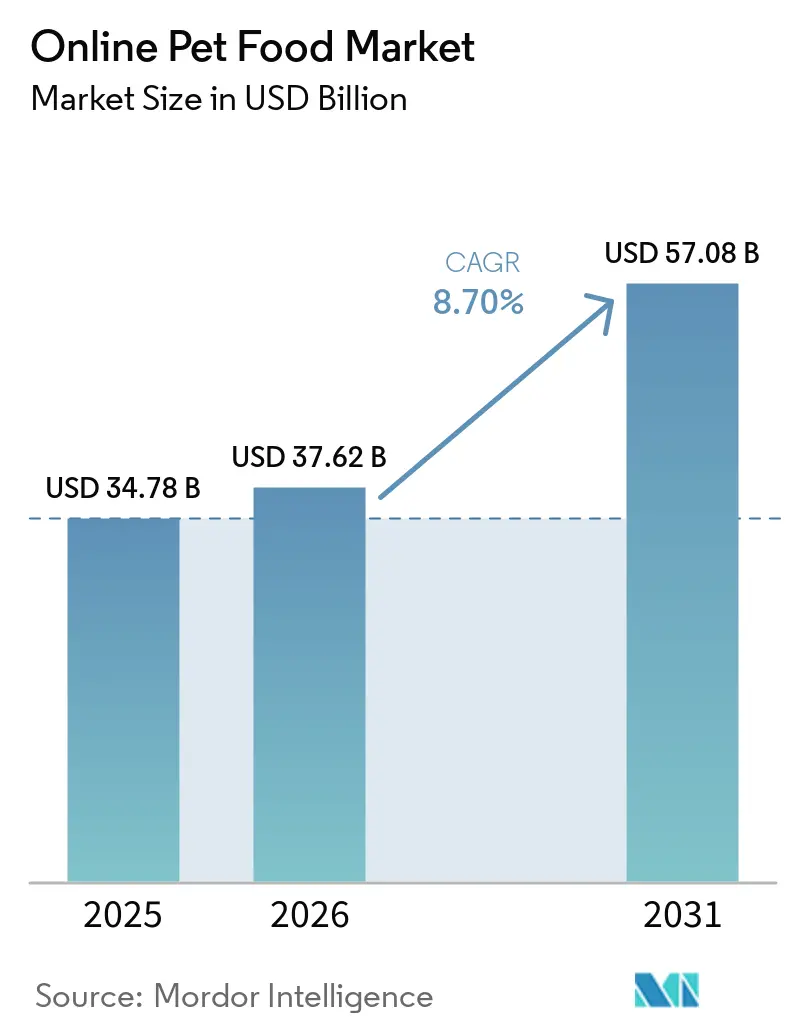

| Market Size (2026) | USD 37.62 Billion |

| Market Size (2031) | USD 57.08 Billion |

| Growth Rate (2026 - 2031) | 8.70% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Pet Food Market Analysis by Mordor Intelligence

The online pet food market size was valued at USD 34.78 billion in 2025 and is projected to reach USD 37.62 billion in 2026 and USD 57.08 billion by 2031, registering a CAGR of 8.7% between 2026 and 2031. This growth is driven by an increasing number of households purchasing pet food through digital channels as part of their regular refill routines, rather than as occasional convenience purchases. The market is further supported by subscription programs, mobile commerce, and recommendation tools that simplify and streamline repeat ordering across major countries. Digital sellers benefit from enhanced data capture, improved reorder visibility, and reduced service friction once households are enrolled, enabling steady gains in market share from physical retail over time. However, challenges such as shipping costs, platform fees, compliance requirements, and ranking fluctuations on large marketplaces continue to impact profitability, particularly for smaller brands with limited scale.

Key Report Takeaways

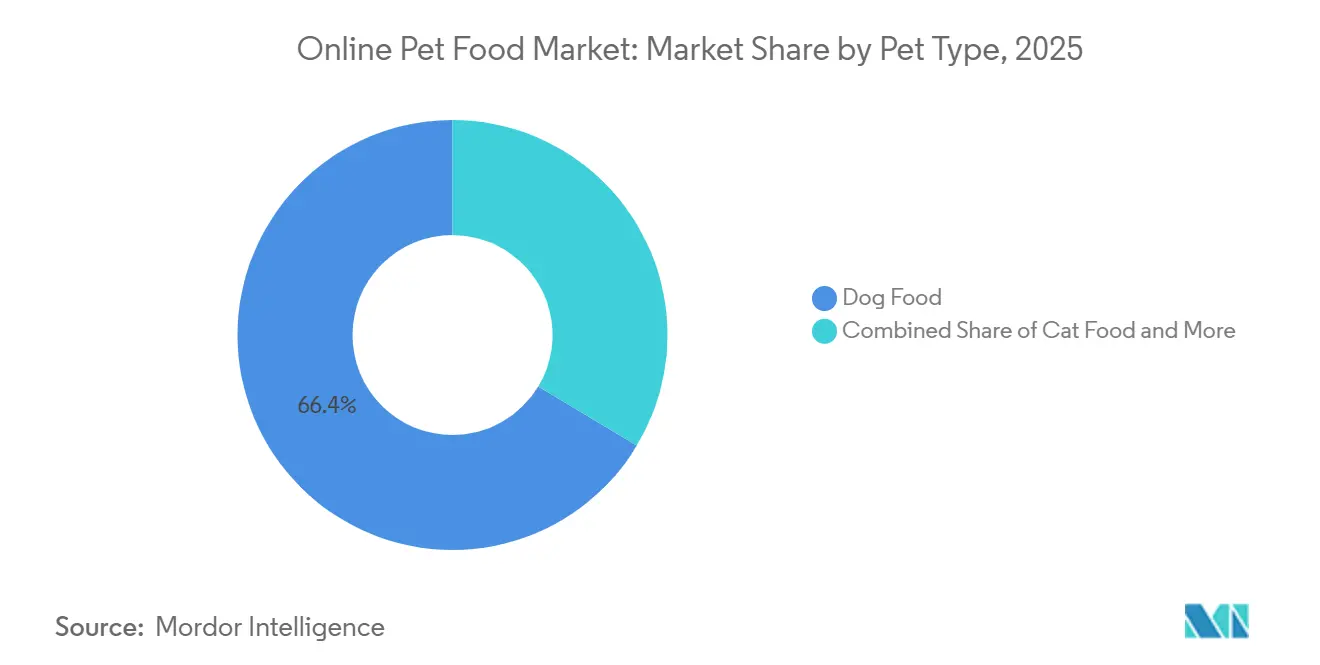

- By pet type, the online pet food market share for the dog food segment held the largest 66.4% of revenue share in 2025, while cat food is projected to grow at the fastest CAGR of 8.6% from 2026 to 2031.

- By product form, dry food accounted for the largest 42.5% revenue share in 2025, while freeze-dried and air-dried products are forecast to grow at the fastest CAGR of 9.8% from 2026 to 2031.

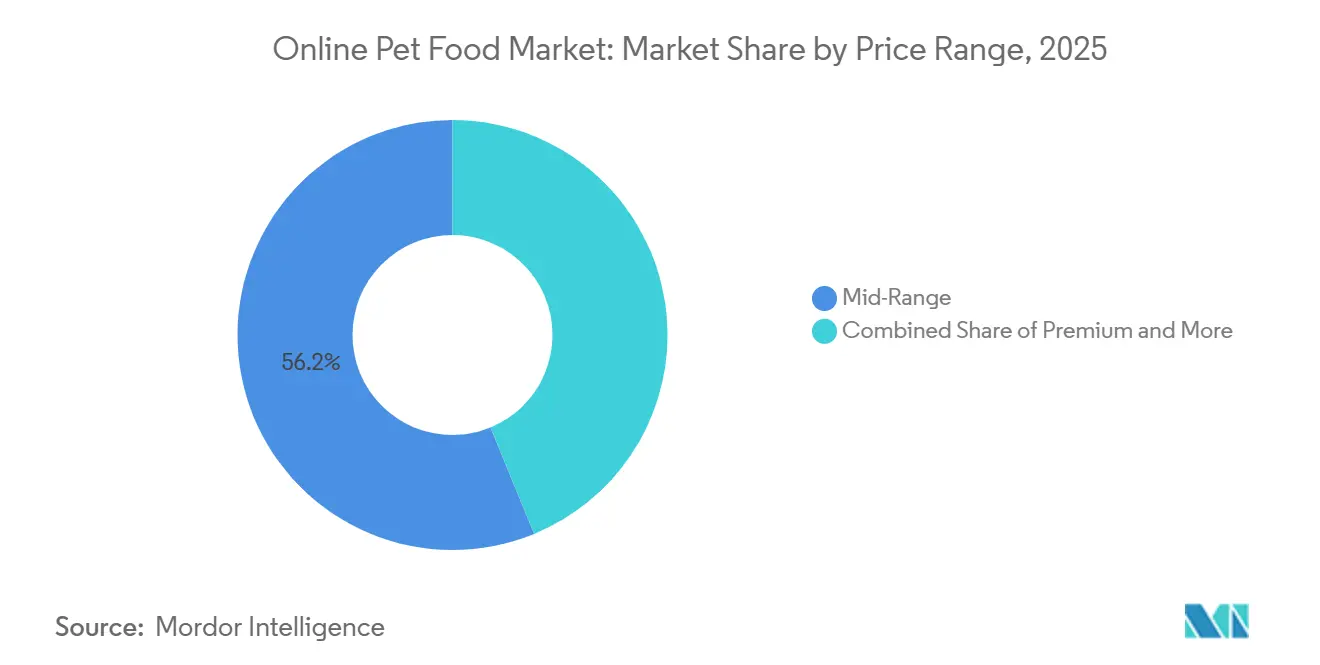

- By price range, mid-range products captured the largest 56.2% of revenue share in 2025, while premium products are projected to grow at the fastest CAGR of 8.2% from 2026 to 2031.

- By channel and sales model, the third-party marketplace segment held the largest 41.7% of revenue share in 2025, while subscription platforms are forecast to grow at the fastest CAGR of 14.9% from 2026 to 2031.

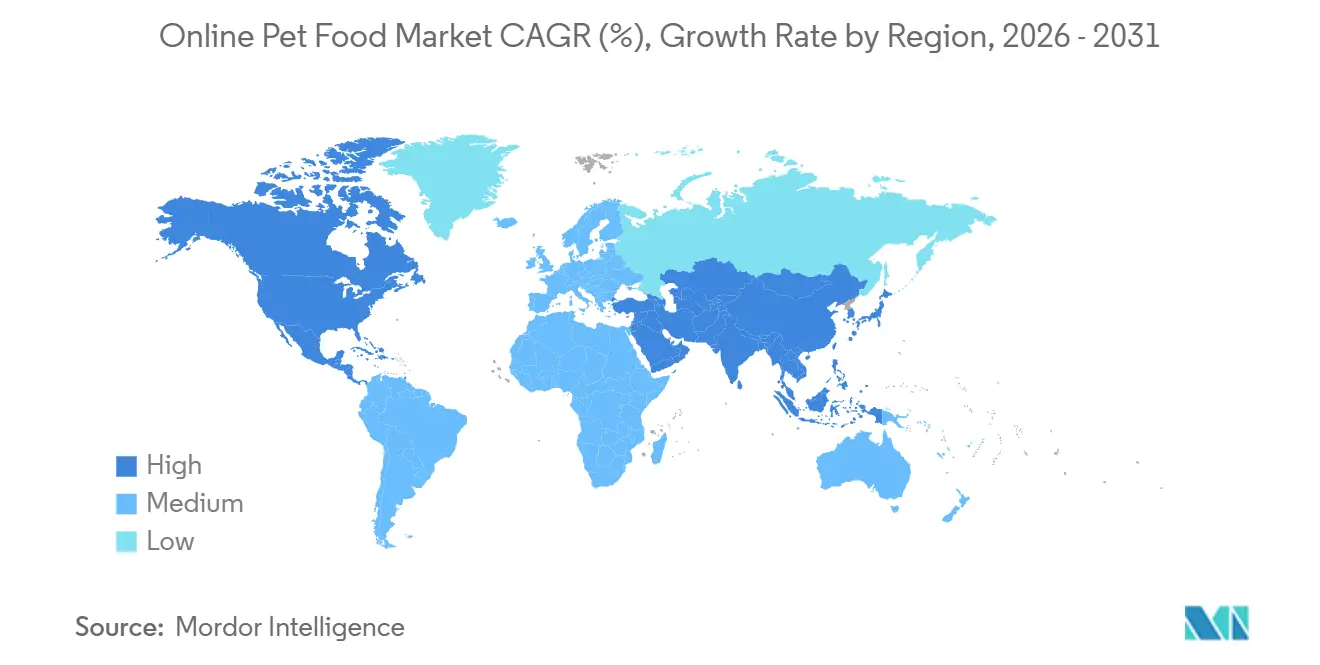

- By geography, North America held the largest 40.3% revenue share in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 8.8% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Online Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription-led replenishment economics | +1.7% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Premium and health-focused pet humanization | +1.6% | Global, concentrated in North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| Mobile-first marketplace reach and last-mile convenience | +1.3% | Asia-Pacific core, with spillover to the Middle East and Africa and South America | Medium term (2-4 years) |

| Wider online assortment and price transparency | +0.9% | Global | Short term (≤ 2 years) |

| AI-enabled personalized nutrition and data feedback loops | +0.8% | North America and the European Union, with early gains in Asia-Pacific | Long term (≥ 4 years) |

| Social commerce and petfluencer-led discovery | +0.5% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Subscription-Led Replenishment Economics

Autoship and subscription programs have become a fundamental commercial model in the online pet food market, transforming routine refill purchases into recurring revenue streams. Once a household establishes a feeding schedule, the reorder process becomes straightforward, predictable, and less prone to disruption. This model enables operators to forecast demand more accurately and manage inventory with reduced volatility compared to one-time order systems. The increased predictability also allows larger platforms to maintain margins, even as customer acquisition costs rise. The online pet food market benefits significantly from this approach, as repeat orders enhance customer retention and increase customer lifetime value. For instance, Chewy, Inc. reported that Autoship customer sales accounted for 83.3% of its net sales till the second Q2 in fiscal year 2025, highlighting the strong integration of recurring purchase behavior within the category[1]Source: Chewy, Inc., “Chewy Announces Second Quarter 2025 Financial Results,” investor.chewy.com..

Premium and Health-Focused Pet Humanization

Pet humanization continues to drive increased spending per animal, encouraging consumers to prioritize better ingredients, transparent labeling, and specialized feeding options in the online pet food market. Households that consider pets as family members are more inclined to invest in functional formulas, breed-specific diets, and life-stage nutrition. Online platforms facilitate this trend by offering a broader selection of premium products compared to physical store shelves. This expanded range enables brands to market condition-specific, age-specific, and ingredient-focused food without relying on limited shelf space. Additionally, it provides specialist retailers and direct-to-consumer brands with a distinct opportunity to differentiate themselves from mass-market retailers. The financial commitment to this trend remained robust, with the American Pet Products Association reporting that total United States pet industry spending reached USD 158 billion in 2025[2]Source: American Pet Products Association, “U.S. Pet Industry Reaches $158 Billion in 2025, Poised for Continued Growth in 2026,” americanpetproducts.org..

Mobile-First Marketplace Reach and Last-Mile Convenience

The increasing use of mobile shopping applications, digital payment systems, and advanced fulfillment networks is enhancing the convenience of online pet food purchases and fostering repeat buying behavior. This trend is particularly prominent in the United Kingdom, where e-commerce has become a significant retail channel. According to the United Kingdom Department for Business and Trade, retail e-commerce sales are projected to represent 38.1% of the United Kingdom’s total retail sales by 2025, underscoring the growing dependence on online platforms for routine consumer purchases. As pet food requires frequent replenishment, the growth of mobile-first commerce and efficient home delivery services is driving consumer preference for online purchasing, contributing to the expansion of the online pet food market.

Wider Online Assortment and Price Transparency

The online pet food market provides a broader product range compared to physical stores, particularly in areas such as specialized nutrition, exotic proteins, and therapeutic diets. This is significant as pet owners increasingly seek products tailored to specific breeds, ages, health requirements, or feeding preferences. The extensive assortment also benefits smaller niche segments, as they are not constrained by the limited shelf space of local stores. Additionally, digital price comparison tools enable buyers to evaluate options more effectively before making a purchase. This increased transparency shifts purchasing decisions from habitual in-store shopping to more deliberate online purchases. The combination of extensive product variety and price transparency offers online platforms a competitive advantage in the pet food market, particularly for consumers who regularly replenish their pet food supplies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bulky-bag shipping costs and delivery margin compression | -1.5% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Multi-jurisdiction pet food labeling and recall compliance | -0.9% | North America and the European Union, with spillover to Asia-Pacific and the Middle East and Africa | Long term (≥ 4 years) |

| Marketplace take-rates and retail media cost inflation | -0.8% | Global | Medium term (2-4 years) |

| Marketplace seller-policy shifts and unauthorized-seller disruption | -0.5% | North America and the European Union | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bulky-Bag Shipping Costs and Delivery Margin Compression

The physical weight and size of pet food present a fundamental cost challenge for the online pet food market. Large bags of dry food occupy significant space within delivery networks, while fresh or frozen products require additional handling, further increasing costs. These factors make offering free shipping difficult unless operators achieve significant scale, optimize routing density, or benefit from high repeat purchase rates. While subscription models can help mitigate this challenge, they do not eliminate it, particularly as brands often subsidize initial orders to attract customers. Smaller direct-to-consumer companies face greater pressure due to limited warehouse capacity, which increases shipping distances. As a result, logistics efficiency remains a key differentiator between larger, scaled operators and smaller competitors in the online pet food market.

Multi-Jurisdiction Pet Food Labeling and Recall Compliance

The online pet food market is encountering increasing compliance challenges as manufacturers address diverse regulatory frameworks across countries. In September 2024, the United States Food and Drug Administration (FDA) announced the withdrawal of specific Answers Pet Food dog food products after samples tested positive for Salmonella and Listeria monocytogenes. This required companies to promptly notify customers and update digital product information across online platforms. Such incidents can quickly gain traction through customer reviews and social media, amplifying reputational risks. Additionally, the need to adhere to varying labeling, traceability, and recall requirements across different jurisdictions increases compliance costs, thereby restraining the growth of the online pet food market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dog Food Dominates, Cat Food Gains Speed

The online pet food market share for the dog food segment accounted for the largest 66.4% of the market in 2025, making it the largest pet type segment in the online pet food market. This dominance is attributed to the higher feeding requirements of dogs, wider product availability, and stronger recurring purchase patterns. Dog owners frequently buy dry food, wet food, treats, functional nutrition products, and veterinary diets through online channels, creating opportunities for repeat transactions. Subscription-based ordering models are particularly effective in this segment due to predictable feeding schedules. Additionally, the segment benefits from larger basket sizes, contributing to strong customer retention and consistent purchasing activity across online retail platforms.

The online pet food market size for the cat food segment is projected to grow at the fastest CAGR of 8.6% from 2026 to 2031, making it the fastest-growing pet type segment in the online pet food market. This growth is driven by increasing pet ownership in urban households and rising demand for premium nutrition solutions tailored to specific health needs. Cat owners often seek products addressing digestion, hydration, weight management, and age-related requirements, fostering product diversification and premiumization. Online channels offer convenient access to specialized formulations that may not be widely available in physical stores. The other pet food category remains comparatively smaller but continues to benefit from the extensive product assortment and accessibility offered through digital retail platforms. This category leverages the convenience of online channels to reach niche customer segments and support steady growth.

By Product Form: Dry Food Anchors Volume, Freeze-Dried Challenges the Premium Ceiling

Dry food held the largest 42.5% share in 2025, which kept it as the leading product form by value. This dominance is attributed to its extended shelf life, ease of storage, and compatibility with recurring delivery programs. Consumers often prefer purchasing dry food in larger quantities online, as it eliminates the inconvenience of transporting heavy bags from physical stores. Additionally, this format offers flexibility to cater to various pet sizes, life stages, and dietary needs. Wet food continues to hold a significant share due to its suitability for hydration-focused feeding routines, while treats drive additional spending through impulse purchases and routine rewards.

Freeze-dried and air-dried products are projected to grow at the fastest 9.8% CAGR from 2026 to 2031, making them the fastest-growing product form in the online pet food market. Rising consumer interest in minimally processed nutrition and ingredient transparency is driving the adoption of these products. Many pet owners view these formats as nutritionally beneficial while maintaining convenience and storage stability. Online retail platforms allow brands to effectively communicate detailed ingredient information, feeding instructions, and product benefits, which is less feasible with traditional shelf displays. Fresh and frozen products are also gaining traction among premium buyers, particularly in regions where direct delivery infrastructure supports specialized handling and consistent product quality.

By Price Range: Mid-Range Holds the Volume Center, Premium Accelerates

Mid-range products accounted for the largest 56.2% share in 2025, making them the largest price segment in the online pet food market. This category appeals to consumers seeking a balance between affordability and nutritional quality. Many consumers perceive these products as offering significant improvements over entry-level options without incurring the higher costs associated with premium formulations. Manufacturers are focusing on enhancing ingredient quality, product claims, and packaging within this segment to attract value-conscious buyers. Additionally, loyalty programs and multipack offerings contribute to encouraging repeat purchases. These factors collectively sustain demand across a wide consumer base.

Premium products are forecast to grow at the fastest CAGR of 8.2% from 2026 to 2031, making them the fastest-growing price tier in the online pet food market. This growth is driven by rising interest in functional ingredients, clean-label formulations, and nutrition tailored to specific life stages or health conditions. Digital platforms facilitate this trend by offering detailed product information, customer reviews, and comparison tools that help justify higher price points. Consumers are increasingly prioritizing perceived quality and long-term wellness benefits when choosing pet food products. While economy offerings remain relevant for budget-conscious households, purchasing behavior is shifting toward products that deliver greater value and differentiated nutritional benefits.

By Channel and Sales Model: Marketplace Leads, Subscription Platform Accelerates

Third-party marketplace platforms held the largest 41.7% share in 2025, which kept them as the largest channel in the online pet food market. This dominance is attributed to their broad product selection, convenient purchasing processes, established payment systems, and efficient fulfillment capabilities. These platforms allow consumers to compare multiple brands and price points in one location, streamlining routine purchasing decisions. Specialist online retailers also play a significant role by offering category expertise, personalized recommendations, and loyalty-driven engagement strategies. Additionally, direct-to-consumer websites and veterinary online stores enhance channel diversity by providing greater control over customer relationships and specialized product offerings.

Subscription platforms are forecast to grow at the fastest CAGR of 14.9% from 2026 to 2031, making them the fastest-growing channel in the online pet food market. Their growth is driven by predictable replenishment cycles, improved customer retention, and the convenience of automated ordering. Subscription models help reduce the risk of missed purchases while enabling consumers to manage recurring household expenses more effectively. These platforms also foster long-term relationships through personalized recommendations and tailored product selections. Meanwhile, veterinary online stores continue to gain importance as they cater to the demand for therapeutic and prescription nutrition products, offering trusted purchasing environments and ongoing guidance for pet owners.

Geography Analysis

North America accounted for the largest 40.3% share in 2025, giving it the largest regional position in the online pet food market. The region benefits from a mature e-commerce ecosystem, high pet ownership rates, and widespread consumer acceptance of recurring online purchases. Consumers are comfortable ordering large pet food packages through digital channels, supported by advanced fulfillment networks and reliable delivery services. The presence of established online retailers, subscription-based purchasing programs, and extensive product availability further strengthens regional demand.

Asia-Pacific is forecast to grow at the fastest CAGR of 8.8% from 2026 to 2031, making it the fastest-growing regional block in the online pet food market. Growth is supported by rising pet ownership, increasing digital payment adoption, and expanding access to mobile commerce platforms. Consumers across major regional markets are becoming more willing to purchase pet food through online channels due to convenience, broader product selection, and competitive pricing. The region also benefits from growing awareness of pet health and nutrition, encouraging demand for premium and specialized products.

Europe is the second-largest regional market in the online pet food industry, with Germany, the United Kingdom, and France acting as major demand hubs. The region benefits from robust consumer spending on pet care, a well-established digital retail infrastructure, and the increasing adoption of subscription-based purchasing models. According to European Pet Food Industry Federation (FEDIAF) statistics cited by the Animal Economics in 2025, Europe hosts 352 million pets, including 129 million cats and 106 million dogs, highlighting a significant consumer base that drives pet food purchases through online channels. Increasing pet ownership and the growing demand for premium pet nutrition continue to fuel e-commerce growth in the region[3]Source: European Pet Food Industry Federation (FEDIAF), cited in The Animal Economics, “FEDIAF Statistics: Europe Is Home to 352 Million Pets,” theanimaleconomics.com., demonstrating the substantial consumer base supporting pet-related purchases across the region.

Competitive Landscape

The online pet food market remains moderately consolidated at the global level, including key major players such as Amazon.com, Inc., Chewy, Inc., Zooplus SE (Hellman & Friedman LLC), PetSmart LLC (BC Partners LLP), and Petco Health and Wellness Company, Inc., with competition coming from marketplaces, specialist pet retailers, direct-to-consumer brands, and pet food manufacturers. Large platforms benefit from broad product assortments, fulfillment scale, and strong customer acquisition capabilities, while specialist retailers compete through category expertise, loyalty programs, and personalized shopping experiences. Major pet food companies continue to maintain multi-channel distribution strategies to maximize visibility across online touchpoints. Competition increasingly extends beyond product availability, with retailers focusing on convenience, customer retention, and service differentiation to strengthen long-term relationships with pet owners.

Leading participants are expanding their capabilities beyond traditional retail by integrating services that improve customer engagement and retention. Online platforms are investing in subscription programs, veterinary support, digital health tools, and personalized nutrition recommendations to increase customer lifetime value. Manufacturers are also strengthening their direct consumer relationships through dedicated online storefronts and enhanced digital marketing strategies. At the same time, premium and specialized nutrition providers continue to enter the market with differentiated offerings targeting specific health conditions, life stages, and dietary preferences. These developments are increasing competitive intensity across both mass-market and premium product categories.

Strategic investments and acquisitions continue to reshape the competitive environment. In April 2026, Chewy, Inc. announced its acquisition of Modern Animal, expanding its presence into veterinary care and strengthening integration between pet health services and product purchasing. According to Chewy, Inc., the company ended fiscal year 2025 with 21.3 million active customers, demonstrating the scale that leading online platforms can achieve through recurring customer relationships and digital engagement. This combination of commerce and healthcare capabilities highlights the growing importance of ecosystem-based competition across the pet care sector.

Online Pet Food Industry Leaders

Amazon.com, Inc.

Chewy, Inc.

Zooplus SE (Hellman & Friedman LLC)

PetSmart LLC (BC Partners LLP)

Petco Health and Wellness Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Chewy, Inc. has announced an agreement to acquire Modern Animal, a technology-driven veterinary care provider, to enhance its integrated pet healthcare ecosystem. Upon completion, this acquisition is projected to expand Chewy Vet Care from 18 to 47 locations across the United States and generate over USD 125 million in annualized run-rate revenue, strengthening the integration of veterinary services with online pet platforms.

- October 2025: Chewy, Inc., acquired SmartPak Equine, LLC (SmartEquine) from Covetrus, Inc. through an all-cash transaction funded by Chewy, Inc.'s existing balance sheet. The transaction expands Chewy, Inc.'s subscription commerce model into the equine health and nutrition market.

- June 2025: Amazon.com, Inc., has expanded its South Africa marketplace by including pet food and pet supplies, thereby enhancing its consumables portfolio and bolstering its online pet retail presence in the country.

Global Online Pet Food Market Report Scope

Online pet food refers to pet nutrition products available through digital channels, including e-commerce marketplaces, pet retail websites, brand-owned platforms, and subscription services. These channels offer pet owners convenient access to a wide range of products, home delivery, and recurring purchase options. The Online Pet Food Market Report is Segmented by Pet Type (Dog Food, Cat Food, and More), by Product Form (Dry Food, Wet Food, Snacks and Treats, and More), by Price Range (Economy, Mid-Range, and More), by Channel (Third-Party Marketplace, Specialist Online Retailer, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Dog Food |

| Cat Food |

| Other Pet Food |

| Dry Food |

| Wet Food |

| Snacks and Treats |

| Fresh and Frozen |

| Freeze-Dried and Air-Dried |

| Economy |

| Mid-Range |

| Premium |

| Third-Party Marketplace |

| Specialist Online Pet Retailer |

| Brand-Owned Direct-to-Consumer Website |

| Subscription Platform |

| Veterinary-Enabled Online Store |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Pet Type | Dog Food | |

| Cat Food | ||

| Other Pet Food | ||

| By Product Form | Dry Food | |

| Wet Food | ||

| Snacks and Treats | ||

| Fresh and Frozen | ||

| Freeze-Dried and Air-Dried | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Channel and Sales Model | Third-Party Marketplace | |

| Specialist Online Pet Retailer | ||

| Brand-Owned Direct-to-Consumer Website | ||

| Subscription Platform | ||

| Veterinary-Enabled Online Store | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving growth in online pet food sales globally?

Growth is being supported by subscription-based reordering, mobile commerce, premium feeding habits, and broader online assortment. The market is projected to rise from USD 37.62 billion in 2026 to USD 57.08 billion by 2031 at the fastest 8.7% CAGR from 2026 to 2031.

Which pet type contributes the most revenue online?

Dog food leads the category, with the largest 66.4% of total value in 2025.

Which product format is growing the fastest online?

Freeze-dried and air-dried food is the fastest-growing format, with a fastest 9.8% CAGR from 2026 to 2031.

Why are subscription platforms gaining share so quickly?

Subscription platforms are forecast to grow at the fastest 14.9% CAGR from 2026 to 2031.

Page last updated on: