Infrared (IR) LED Chip Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 10.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

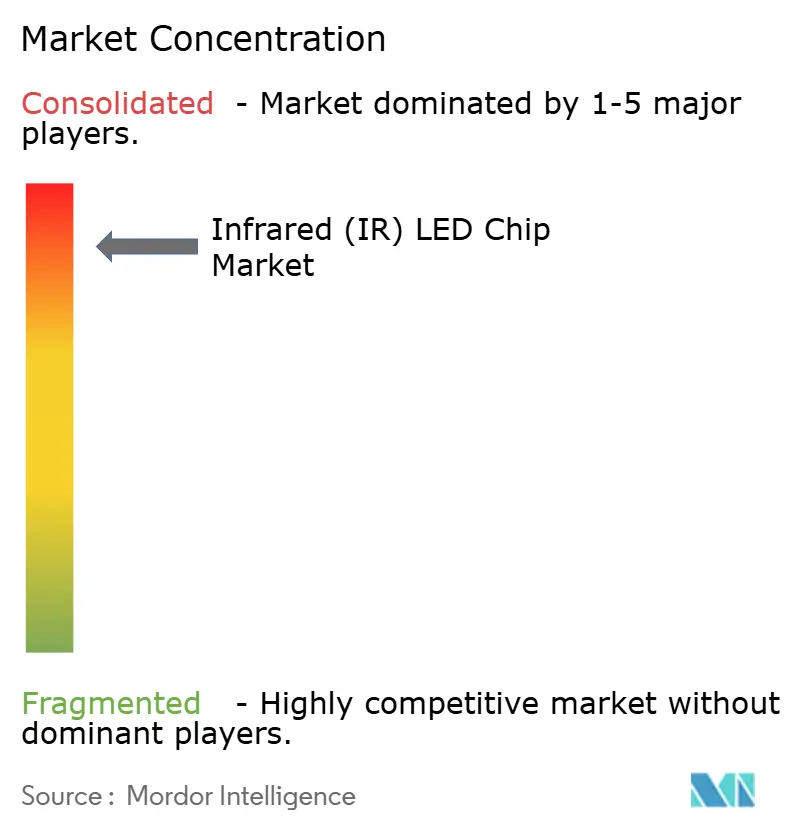

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infrared (IR) LED Chip Market Analysis by Mordor Intelligence

The infrared (IR) LED chip market size is expected to increase from USD 1.61 billion in 2025 to USD 1.79 billion in 2026 and reach USD 2.89 billion by 2031, growing at a CAGR of 10.1% over 2026-2031. Robust demand comes from three converging trends: automotive safety mandates that embed eye-safe near-infrared emitters in driver-monitoring systems, biometric authentication inside consumer devices, and the shift toward short-wave infrared hyperspectral imaging used for industrial sorting. Tight regulatory timelines in North America, Europe, and China are accelerating design-ins for automotive grade chips, while smartphone leaders migrate to under-display facial recognition that favors compact, high-flux emitters. Simultaneously, food processors and recyclers are adopting 1,000-1,700 nanometer emitters that reveal chemical signatures invisible to visible light, opening a premium pricing tier centered on spectral purity and radiant intensity. Competitive pressure remains elevated because vertically integrated Asian suppliers are scaling new metal-organic chemical vapor deposition reactors, shortening lead times, and launching price campaigns that ripple through the global infrared LED chip market.

Key Report Takeaways

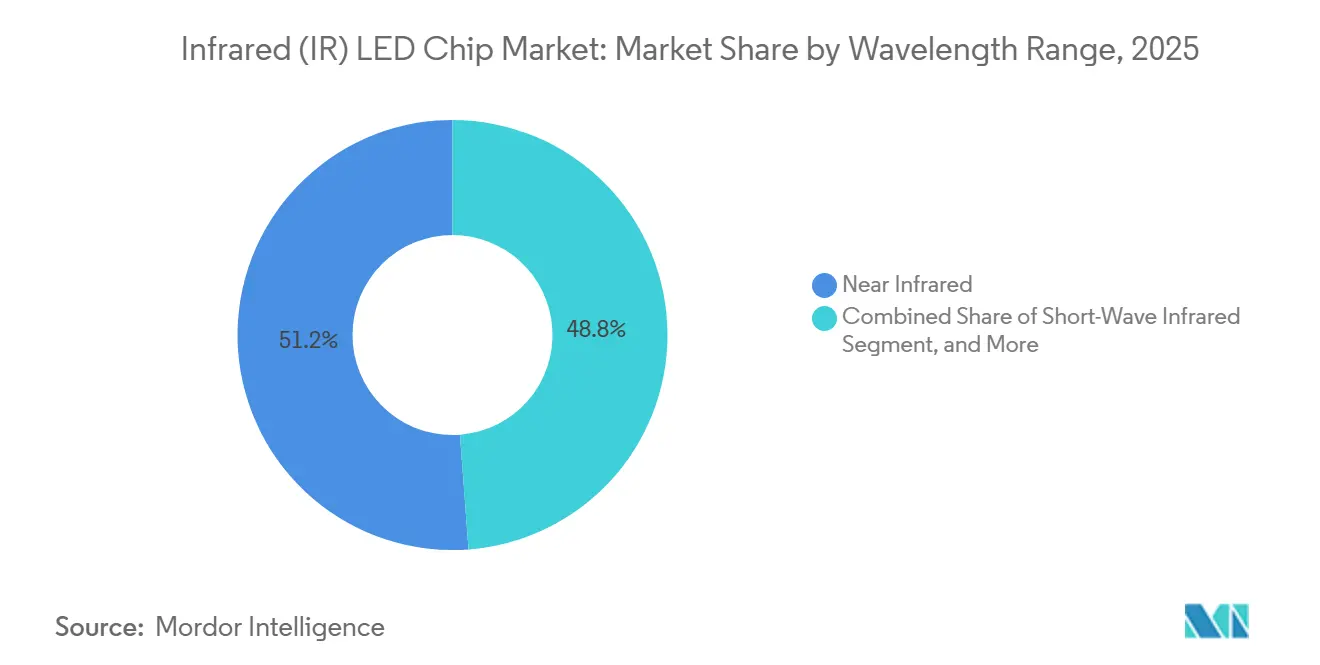

- By wavelength range, the 850-950 nanometer segment captured 51.19% of revenue in 2025, while the short-wave infrared band is projected to expand at a 10.68% CAGR through 2031.

- By power output, devices rated 1-5 watts held 41.58% of the infrared (IR) LED chip market share in 2025, but emitters above 5 watts are forecast to grow at a 10.95% CAGR over the same period.

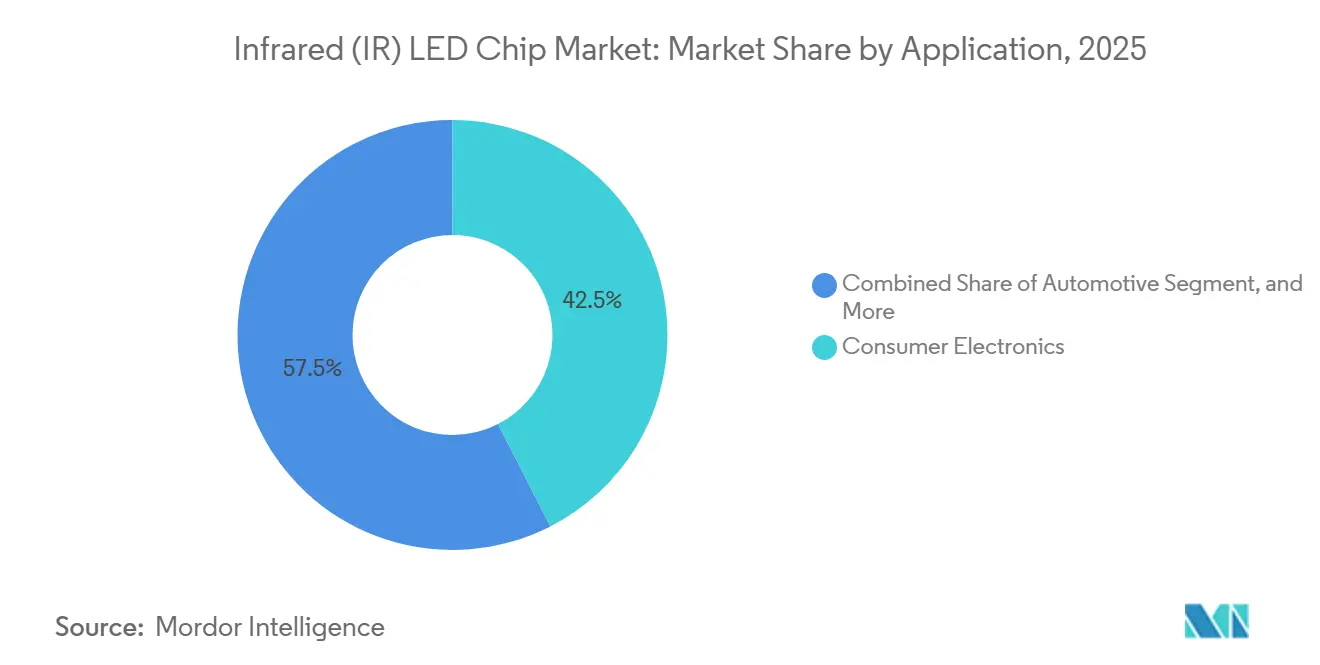

- By application, consumer electronics led with 42.48% revenue share of the infrared (IR) LED chip market in 2025; automotive modules are positioned to advance at an 11.05% CAGR to 2031.

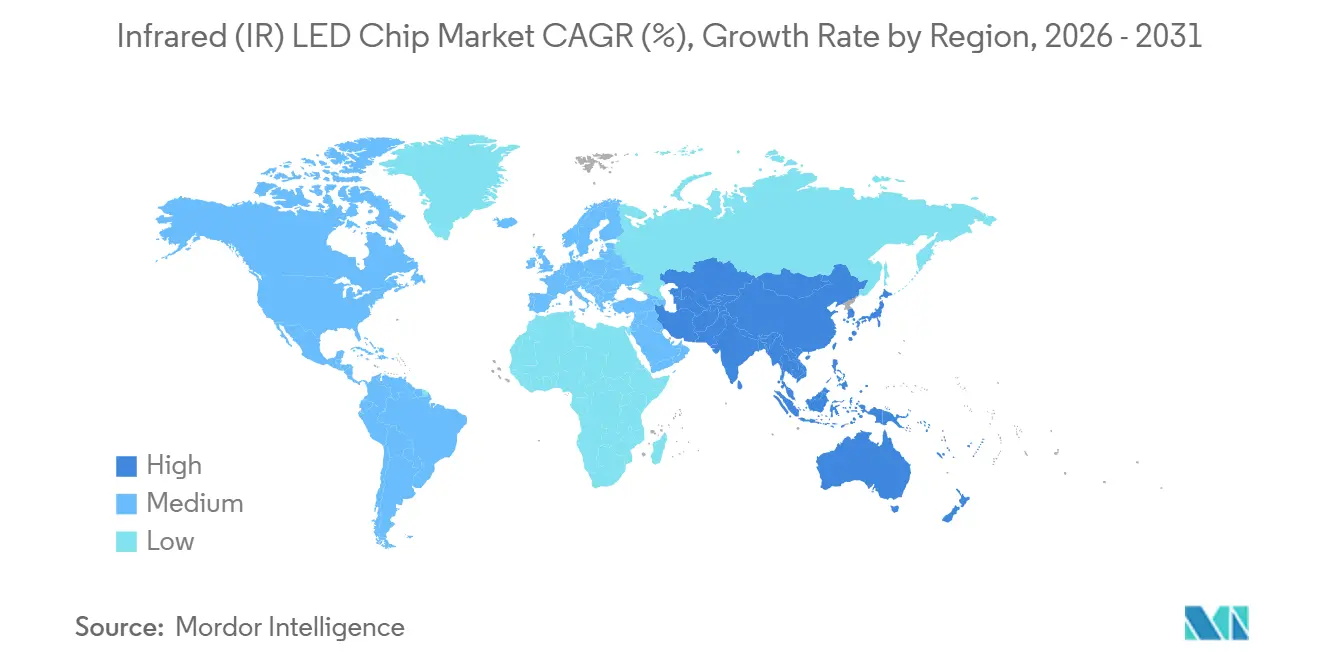

- By geography, Asia-Pacific accounted for 49.53% of revenue in 2025 and is expected to post an 11.22% CAGR, the fastest regional growth to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Infrared (IR) LED Chip Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption in Consumer Electronics | +2.8% | Asia-Pacific hubs, North America design centers | Medium term (2-4 years) |

| Expansion of Automotive Driver Monitoring and ADAS Systems | +2.5% | North America, Europe, China | Short term (≤ 2 years) |

| Growing Demand for Night-Vision Security and Surveillance Cameras | +1.9% | Middle East, Asia-Pacific, North America | Medium term (2-4 years) |

| Increasing Use in Healthcare Diagnostics and Wearable Devices | +1.2% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Integration with SWIR Hyperspectral Imaging for Sorting | +1.1% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Contactless Smart-Retail Shelves Using Low-Power Arrays | +0.5% | North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption In Consumer Electronics

Smartphone makers are repositioning infrared emitters behind organic light-emitting diode displays to enable under-screen facial recognition, a redesign that favors miniaturized chips that deliver high radiant flux through absorptive stack layers.[1]TechInsights Analysts, “Apple iPhone 17 Teardown,” TechInsights, techinsights.com Beyond handsets, tablets, smart speakers, and augmented-reality headsets, 850-nanometer arrays are embedded for gesture recognition and depth mapping. Consumer wearables benefit from FDA-cleared therapy masks that use 830-850-nanometer LEDs to stimulate collagen, widening the total addressable market. Diversification into beauty and wellness reduces dependence on cyclical phone refreshes and supports recurring demand for compact, high-efficiency chips. The result is steady pull-through for the infrared LED chip market as device makers seek thinner packages and tighter wavelength bins to maintain biometric accuracy.

Expansion Of Automotive Driver Monitoring And ADAS Systems

Euro NCAP’s 2026 protocol awards up to 25 safety points for eye-tracking driver monitoring, effectively making near-infrared illumination mandatory in passenger cars.[2]Smart Eye Editorial Team, “Driver Monitoring System 2.0 Requirements,” Smart Eye Blog, smart-eye.com U.S. and Chinese regulators are drafting similar language, synchronizing global demand for AEC-Q102 qualified emitters that remain wavelength-stable from -40 °C to 125 °C. Suppliers respond with five-junction laser diodes that lift peak optical power while easing current draw and heat generation, enabling LiDAR modules to detect objects beyond 200 meters. Tier-one integrators have begun high-volume qualification, anchoring multiyear supply agreements that lock in share for leading foundries. These mandates accelerate adoption curves and reinforce the pivotal role of the infrared LED chip market in the safety electronics roadmap.

Growing Demand For Night-Vision Security And Surveillance Cameras

Public-safety agencies and logistics operators deploy infrared-illuminated cameras that capture clear imagery in total darkness, reducing theft and improving situational awareness. The 850 nanometer band dominates perimeter surveillance since its faint red glow serves as a deterrent, whereas covert intelligence platforms select 940 nanometer chips despite lower radiant efficiency. Smart-city roll-outs across Middle Eastern and Asian megacities integrate these cameras for traffic analytics and crowd management, underpinned by falling component costs in the infrared LED chip market. EU privacy regulation imposes stringent biometric conditions, tempering uptake in Europe but boosting deployments in jurisdictions with lighter oversight. Overall, municipal infrastructure grants and private security budgets sustain mid-term momentum for high-volume medium-power emitters.

Increasing Use In Healthcare Diagnostics And Wearable Devices

Near-infrared photoplethysmography enables non-invasive monitoring of oxygen saturation and heart-rate variability in smart rings and fitness bands, though glucose sensing remains experimental due to confounding skin factors. FDA-cleared PressureSafe systems leverage infrared imaging to detect pressure injuries in hospitals, validating medical use cases that demand stringent photobiological safety and electromagnetic compatibility. Cosmetic therapy masks that employ 830-850 nanometer chips reached mainstream retail in 2025, expanding channel diversity beyond clinical settings. Device makers with ISO 13485 quality systems and proven reliability testing gain an edge, supporting premium unit economics. As healthcare shifts toward continuous, non-invasive monitoring, the infrared LED chip market benefits from design-win stickiness and longer product life cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Price Competition Compressing Margins | -1.8% | Global, most acute in Asia-Pacific | Short term (≤ 2 years) |

| Thermal Management Challenges at High Radiant Flux | -0.9% | Global, automotive and industrial nodes | Medium term (2-4 years) |

| Supply-Chain Vulnerability to Gallium and Arsenic Restrictions | -1.2% | North America and Europe import-dependent | Medium term (2-4 years) |

| Privacy Concerns Limiting Biometric Deployments | -0.6% | Europe, parts of North America, selective Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition Compressing Margins

Chinese producers lifted average selling prices 5-10% in 2025 to offset raw material inflation, yet global LED packaging revenue still slipped 4%, signaling oversupply in commodity grades. Vertical integration offers partial insulation, with Taiwanese and European incumbents focusing on microLED and laser architectures to escape price wars.[3]U.S. International Trade Commission Staff, “Critical Minerals Trade Dependence,” USITC, usitc.gov Sanan’s pending acquisition of Lumileds adds cost synergy that could pressure European automotive LED pricing. Smaller suppliers without differentiated intellectual property face margin squeeze and potential exit, a dynamic that keeps consolidation high throughout the infrared LED chip industry.

Supply-Chain Vulnerability To Gallium And Arsenic Restrictions

China controls an overwhelming share of gallium output, and export licensing rules introduced in 2023 tightened supplies, pushing spot prices up 150% by mid-2025.[4]Center for Strategic and International Studies Analysts, “Gallium Price Spike After Export Curbs,” CSIS, csis.org North American and European photonics firms depend on these inputs for aluminum gallium arsenide wafers, making them sensitive to geopolitical disruptions. While recycling initiatives and silicon carbide substrate substitution are under study, commercial readiness is years away, leaving the infrared LED chip market exposed to raw-material volatility. Strategic stockpiling and long-term sourcing contracts have become critical risk-mitigation levers for automotive and defense suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wavelength Range: Short-Wave Infrared Gains Industrial Traction

The near-infrared band between 850-950 nanometers accounted for more than half of the infrared (IR) LED chip market 2025 revenue, reflecting its seamless pairing with low-cost silicon photodetectors and entrenched position in smartphones, automotive driver monitoring, and security cameras. Short-wave infrared devices spanning 1,000-1,700 nanometers are projected to register the fastest growth at 10.68% annually through 2031 as food processors and recyclers adopt hyperspectral sorters that identify polymers and moisture levels invisible to visible-light systems.

Cimbria’s SEA.HY sorter and Imec’s snapshot imager demonstrate how precise wavelength control improves classification accuracy in real-time processing lines. European Union recycling mandates and North American food-safety regulations act as pull factors, supporting premium pricing for chips with tighter spectral bins. Although extended-infrared solutions beyond 1,700 nanometers cater to aerospace, the higher cost of indium gallium arsenide detectors constrains volume. Continuous innovation in epi-wafer uniformity and packaging heatsinks strengthens the value proposition of short-wave solutions within the broader infrared (IR) LED chip market.

By Power Output: High-Power Emitters Propel Automotive LiDAR

Medium-power chips rated 1-5 watts satisfied 41.58% of demand in 2025 thanks to their balance of size and brightness for consumer electronics and surveillance. High-power devices above 5 watts are forecast to show a 10.95% CAGR as Level 3 autonomy demands longer detection ranges and brighter illumination for high-speed machine vision.

The latest five-junction laser diodes raise optical power while keeping current draw manageable, simplifying thermal design and extending module life. Hesai’s 1,440-channel LiDAR and Innoviz’s blockage-resilient sensors underscore how optical power density, rather than raw flux alone, defines next-generation performance. Low-power emitters below 1 watt remain vital for proximity sensors and remote controls but face mature replacement cycles. Superior thermal substrates and chip-on-board architectures continue to be differentiators as the infrared (IR) LED chip market moves toward higher radiant densities.

By Application: Automotive Momentum Accelerates

Consumer electronics retained 42.48% share in 2025 because of the vast smartphone installed base, yet automotive modules are set to climb at an 11.05% CAGR, buoyed by safety ratings and conditional autonomy launches. LiDAR-rich vehicles entering mass production require eye-safe infrared emitters for ranging beyond 200 meters, driving demand for high-reliability chips with AEC-Q102 pedigree.

Industrial machine vision capitalizes on robust 850- and 940-nanometer sources that power break-beam sensors and optical encoders on high-speed production lines. Security and surveillance remain core, especially in rapidly urbanizing Asia-Pacific and the Middle East. Healthcare and cosmetic therapy devices add a diversification layer, broadening revenue streams for suppliers that qualify to medical safety standards. Collectively, these dynamics reinforce a pivot toward precision-sensing use cases across the infrared (IR) LED chip market.

Geography Analysis

Asia-Pacific generated 49.53% of the infrared (IR) LED chip market's 2025 revenue and is on track for an 11.22% CAGR as Chinese, Taiwanese, and South Korean vendors expand epitaxial and packaging capacity. Sanan Optoelectronics posted RMB 8.987 billion (USD 1.24 billion) first-half-2025 revenue, up 17.03%, reflecting deeper penetration into premium automotive and consumer segments. Taiwan’s Ennostar shifts toward microLED and vertical-cavity surface-emitting lasers to escape commodity pricing, while Japanese suppliers focus on discrete power devices supporting automotive quality standards. Vertical integration within regional industrial parks compresses cycle times and underpins the infrared LED chip market’s competitive cost base.

North America and Europe advance more slowly but play a pivotal role in automotive qualification and defense programs. ams OSRAM secured EUR 227 million (USD 256 million) of EU funding to build a EUR 1.4 billion (USD 1.58 billion) back-end facility in Austria, a strategic hedge against Asian supply risk. Patent cross-licensing between ams OSRAM and Nichia resolves litigation distraction and channels investment into next-generation emitters. These regions also anchor compliance testing for photobiological safety and electromagnetic compatibility, locking in design-wins from global carmakers and medical device firms.

South America, the Middle East, and Africa hold smaller shares but benefit from infrastructure projects that require night-vision surveillance and traffic analytics. The Middle East prioritizes critical-asset protection, supporting large-scale deployments of covert 940 nanometer cameras. European privacy legislation may slow biometric roll-outs, but suppliers able to navigate fragmented regulations capture geographically balanced growth. Consequently, regional dynamics preserve Asia-Pacific’s supply dominance while sustaining premium niches elsewhere within the infrared LED chip market.

Competitive Landscape

The top ten manufacturers account for 93% of the global capacity of the infrared (IR) LED chip market, indicating high concentration. Sanan Optoelectronics, HC Semitek, Changlight, and MTC lead mainland China, while Ennostar dominates Taiwan, and ams OSRAM, Nichia, and Lumileds command premium automotive and defense contracts. Sanan’s USD 239 million acquisition of Lumileds, expected to close in Q1 2026, pairs low-cost Chinese manufacturing with European automotive credentials, potentially intensifying price competition at the high end.

ams OSRAM’s patent cross-license with Nichia removes barriers to joint customer engagements, and its five-junction laser diode showcases a pipeline shift toward higher-margin LiDAR components. Everlight’s 2026 lawsuit against Lumileds over flip-chip packaging highlights how intellectual property remains a live battleground that can disrupt supply chains. Cree LED’s OptiLamp pixel-intelligent displays illustrate diversification beyond illumination into smart signage, demonstrating how packaging know-how translates into new verticals.

White-space opportunities lie in short-wave infrared hyperspectral imaging, where incumbents lack application expertise and end users seek co-engineered modules. Smaller firms focusing on microchannel ceramic substrates or corona-wind cooling can secure defensible niches by solving thermal bottlenecks that limit radiant density. Overall, the infrared LED chip market rewards suppliers that combine scale economics with specialized packaging, thermal, and optical competencies.

Infrared (IR) LED Chip Industry Leaders

ams OSRAM AG

Nichia Corporation

Everlight Electronics Co., Ltd.

Epistar Corporation

Vishay Intertechnology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Everlight Electronics filed a patent infringement lawsuit in the U.S. District Court of Delaware against Lumileds over flip-chip packaging patents, seeking damages and a permanent injunction.

- February 2026: Cree LED launched OptiLamp LEDs, integrating driver intelligence into every pixel and eliminating external driver integrated circuits, with a live demonstration at ISE 2026 in Barcelona.

- February 2026: Cree Lighting signed a long-term contract manufacturing agreement with a U.S. lighting company to restore delivery performance amid restructuring-related constraints.

- January 2026: Cree LED and Blizzard Lighting settled a display LED patent dispute, with Blizzard receiving a limited license to Cree LED patents.

Global Infrared (IR) LED Chip Market Report Scope

The Infrared (IR) LED Chip Market Report is Segmented by Wavelength Range (Near Infrared, Short-Wave Infrared, Extended Infrared), Power Output (Low Power, Medium Power, High Power), Application (Consumer Electronics, Automotive, Industrial and Machine Vision, Security and Surveillance, Healthcare and Medical), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Near Infrared |

| Short-Wave Infrared |

| Extended Infrared |

| Low Power |

| Medium Power |

| High Power |

| Consumer Electronics |

| Automotive |

| Industrial and Machine Vision |

| Security and Surveillance |

| Healthcare and Medical |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Wavelength Range | Near Infrared | |

| Short-Wave Infrared | ||

| Extended Infrared | ||

| By Power Output | Low Power | |

| Medium Power | ||

| High Power | ||

| By Application | Consumer Electronics | |

| Automotive | ||

| Industrial and Machine Vision | ||

| Security and Surveillance | ||

| Healthcare and Medical | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast will revenue grow for infrared emitter suppliers serving automotive programs?

Automotive modules are projected to grow at an 11.05% CAGR through 2031 as safety mandates make driver-monitoring and LiDAR standard features.

Which wavelength band currently dominates global demand?

Near-infrared chips in the 850-950 nanometer band held 51.19% of 2025 revenue due to widespread use in smartphones, security cameras, and driver-monitoring.

What drives the short-wave infrared opportunity in industry?

Food processors, recyclers, and pharmaceutical lines adopt 1,000-1,700 nanometer hyperspectral imaging to classify materials and detect moisture, lifting demand for high-purity emitters.

Why are suppliers investing in new European capacity?

Ams OSRAM’s Austrian back-end plant reduces reliance on Asian packaging, meets local automotive qualification needs, and secures public funding support.

How are raw-material risks being managed?

Firms negotiate long-term gallium contracts and diversify substrate options to mitigate exposure to Chinese export controls that recently lifted gallium prices by 150%.

Which companies are most likely to shape pricing trends?

Sanan Optoelectronics, Ennostar, and ams OSRAM influence global pricing because they combine large epi-wafer capacity with strong positions in key end markets.

Page last updated on: