LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 36.15 Billion |

| Market Size (2031) | USD 56.59 Billion |

| Growth Rate (2026 - 2031) | 9.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LED Chips Market Analysis by Mordor Intelligence

The LED chips market size is projected to expand from USD 33.47 billion in 2025 and USD 36.15 billion in 2026 to USD 56.59 billion by 2031, registering a CAGR of 9.38% between 2026 to 2031. Momentum is shifting from simple lamp replacements toward premium displays, smart luminaires, and automotive systems that demand tighter binning tolerances, higher current densities, and enhanced thermal interfaces. Display original-equipment makers accelerated mini-LED adoption in televisions, monitors, and laptops during 2025, while tier-1 automotive suppliers pushed LED headlamps into mid-segment vehicles that previously relied on halogen technology. Regulatory energy-efficiency mandates in the European Union, China, India, and Vietnam reinforced baseline demand for general lighting, yet value creation is migrating to quantum-dot on-chip architectures and micro-LED mass-transfer breakthroughs that enable color-rich, high-luminance applications. Competitive differentiation is therefore moving away from raw epitaxial capacity toward process innovation, intellectual-property portfolios, and the ability to integrate chips with optics, drivers, and software.

Key Report Takeaways

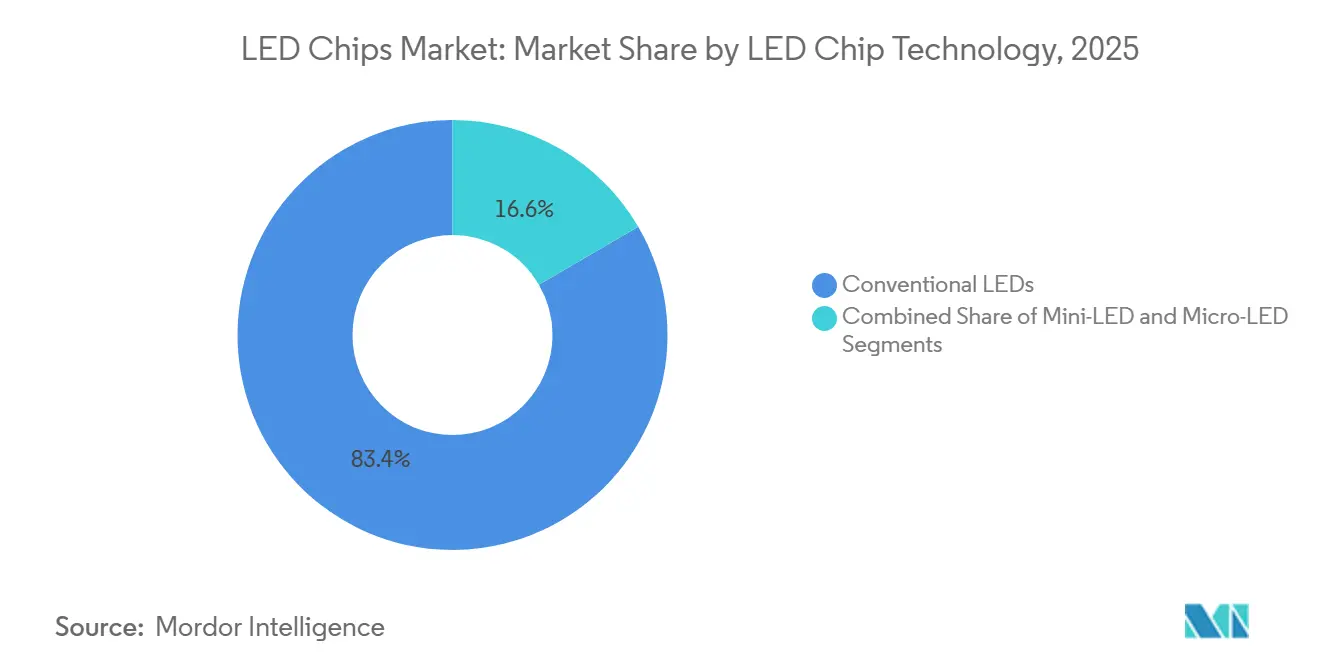

- By LED chip technology, conventional LEDs commanded 83.40% of the LED chips market share in 2025, while micro-LED chips are forecast to expand at an 11.23% CAGR between 2026-2031.

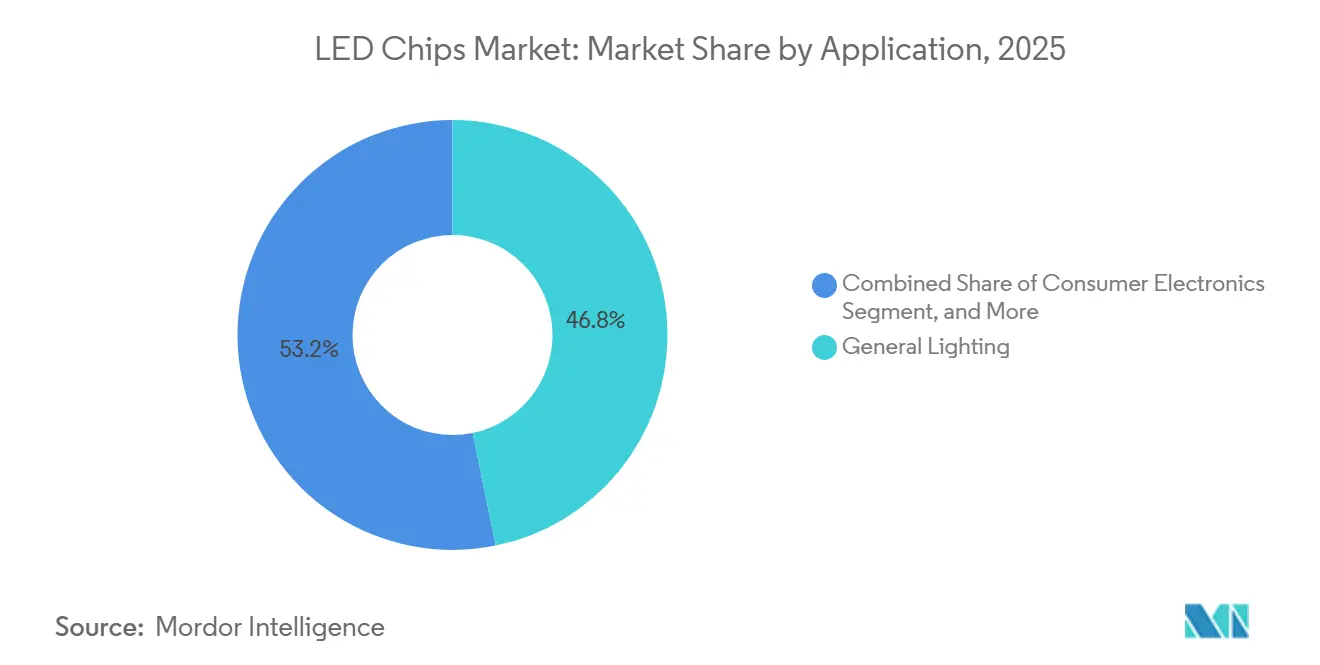

- By application, general lighting accounted for 46.78% of the LED chips market in 2025, and automotive applications are advancing at a 12.55% CAGR through 2031.

- By semiconductor material, gallium nitride and indium gallium nitride compounds captured 82.45% of the LED chip market share in 2025, whereas alternative materials are projected to grow at a 11.88% CAGR from 2026-2031.

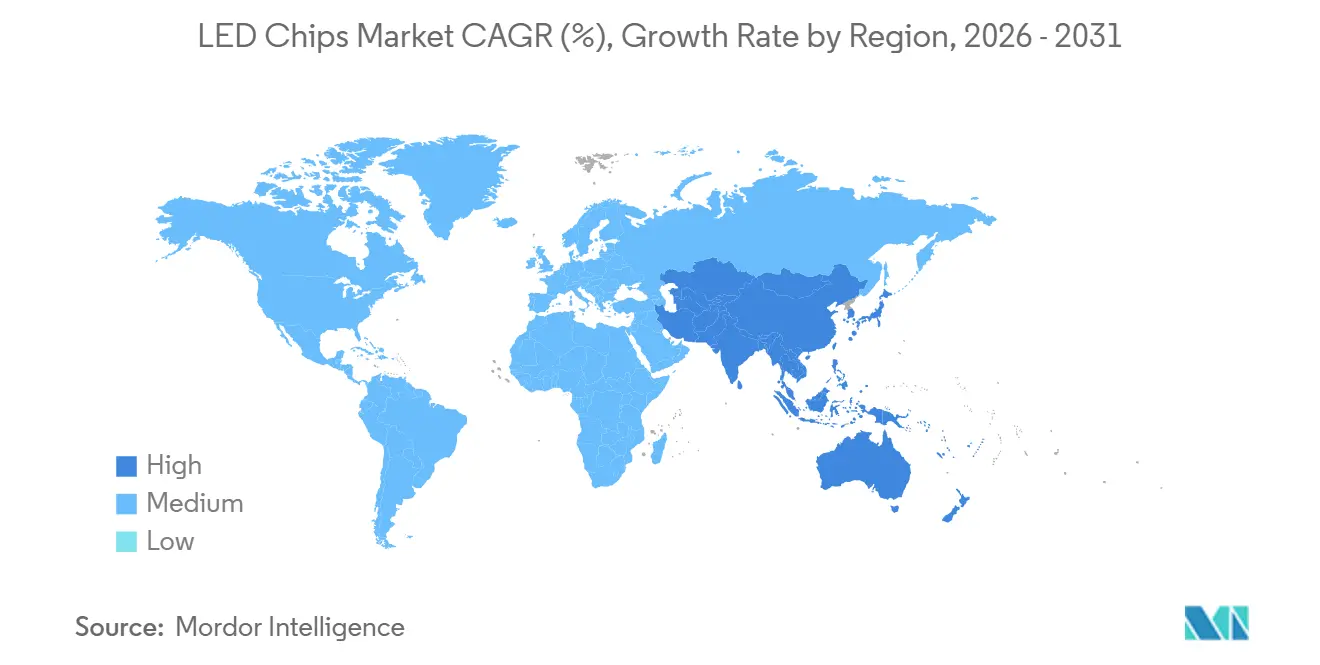

- By geography, the Asia Pacific held 62.46% of the LED chip market share in 2025 and is projected to grow at a 11.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Display OEM Shift to Mini-LED Backlighting | +2.8% | Global, concentrated in Asia Pacific (China, South Korea, Taiwan) and North America premium segments | Medium term (2-4 years) |

| Rising Adoption of LED Headlamps in Mid-Segment Vehicles | +2.1% | Global, with early gains in Europe, China, and North America; spillover to India and Southeast Asia | Medium term (2-4 years) |

| Energy-Efficiency Mandates in Major Economies | +1.6% | Europe, China, India, Vietnam, North America | Short term (≤ 2 years) |

| Quantum-Dot On-Chip Architectures Enabling Wider Color Gamut | +1.2% | Global, led by premium display manufacturers in Asia Pacific and North America | Long term (≥ 4 years) |

| Smart Lighting Integration With IoT Platforms | +0.9% | Global, with early adoption in North America and Europe; expanding to Asia Pacific urban centers | Medium term (2-4 years) |

| GaN-on-Diamond Substrates Reducing Thermal Resistance | +0.5% | Niche applications in automotive, high-power industrial lighting, and micro-LED displays; global R&D centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Display OEM Shift to Mini-LED Backlighting

Mini-LED backlighting moved from a niche to the mainstream in premium televisions and monitors during 2025-2026, allowing LCD panels to rival OLEDs on contrast ratio and peak brightness while retaining cost advantages in large formats. TCL’s second-generation Super Quantum Dot Mini-LED sets launched at CES 2026 embedded thousands of tightly binned chips, pushing luminance near HDR1000 levels and forcing rivals to catch up on performance or risk share loss. Samsung, LG Display, and BOE expanded panel capacity and adopted chip-scale packaging, which places up to 1,000 dies per pulse, trimming assembly time and improving yields. Because each premium panel now consumes far more chips than an edge-lit equivalent, suppliers that meet stringent current-density and thermal demands defend pricing even as commodity ASPs slide.

Rising Adoption of LED Headlamps in Mid-Segment Vehicles

LED penetration leaped from luxury to volume car segments once European adaptive-beam regulations converged with Chinese consumer demand for premium aesthetics in 2025. Nichia and Infineon’s bi-LED projector module combines high- and low-beam functions into a single compact assembly, reducing costs enough for mid-segment models while ensuring automotive-grade reliability.[1]LEDinside, “Seoul Semiconductor and OMINSU Vietnam Form Strategic Alliance for Global Market Expansion,” ledinside.com Major lamp makers such as Koito and Valeo expanded lines dedicated to electric vehicles that rely on energy-saving lighting to extend driving range, lifting chip demand despite unit size reductions.

Energy-Efficiency Mandates in Major Economies

Policies in the European Union, China, India, and Vietnam eliminated halogen and fluorescent lamps from mainstream channels by tightening lumen-per-watt thresholds and mandating product registries. India’s UJALA program alone moved 368.7 million bulbs by January 2025, compressing retail prices and unlocking large-scale chip demand.[2]Press Information Bureau, “UJALA: 10 Years of Energy-Efficient Lighting,” pib.gov.in As developing markets replicate bulk-procurement models, baseline volume growth persists even where replacement cycles approach maturity in advanced economies.

Quantum-Dot On-Chip Architectures Enabling Wider Color Gamut

Embedding quantum dots directly atop blue dies enables near-100% DCI-P3 coverage and cuts optical losses that plague separate films, a breakthrough TCL demonstrated publicly at CES 2026. Laboratory work published in 2025 reported external-quantum-efficiency gains from optimized nanostructures, accelerating commercialization among vertically integrated makers with in-house quantum-dot synthesis. The resulting performance tier commands price premiums that offset materials cost, reinforcing technology-driven rather than volume-driven competition.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent ASP Erosion Due to Asian Overcapacity | -1.8% | Global, originating from China and Taiwan capacity additions; affects all regions | Short term (≤ 2 years) |

| High Capital Expenditure for Micro-LED Mass Transfer | -1.3% | Global, concentrated in Asia Pacific and North America R&D centers and pilot production lines | Medium term (2-4 years) |

| Gallium and Rare-Earth Supply Chain Vulnerabilities | -0.7% | Global, with supply concentration in China; affects all downstream markets | Long term (≥ 4 years) |

| Stringent Blue-Light Hazard Regulations in Europe | -0.4% | Europe, with spillover to markets adopting IEC 62471 standards | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent ASP Erosion Due To Asian Overcapacity

Chinese and Taiwanese wafer expansions once again outran demand growth in 2025-2026, dragging commodity chip prices lower and squeezing second-tier producers operating aging MOCVD lines.[3]Inside Lighting, “The Top Lighting Acquisitions of 2025,” inside.lighting Attempts to raise prices in early 2025 fizzled as soft residential lighting demand and aggressive Taiwanese offers undercut the market. Marginal fabs fell below cash costs, prompting consolidation moves such as San’an Optoelectronics' acquisition of Lumileds and Inari Amertron’s acquisition of Lumileds. The oversupply reinforces a bifurcated LED chips market, with cut-throat pricing in general lighting but firmer margins in automotive, display, and specialty niches where performance, not lumen cost, dictates vendor selection.

High Capital Expenditure for Micro-LED Mass Transfer

Commercializing micro-LED displays requires laser or pick-and-place systems capable of positioning millions of sub-100 micron dies at defect-free yields, a feat that still commands nine-figure investments. Industry benchmark assembly yields trail mature LCD lines by 10-25 points, inflating rework and scrap costs. Only deep-pocketed panel makers such as BOE and CSOT can field proprietary multi-chip transfer tools, locking smaller chip vendors out of volume production unless they partner upstream. The spending burden lengthens payback periods and concentrates the early micro-LED opportunity within a handful of vertically integrated constellations, delaying broad-based demand but raising eventual barriers to entry once high-volume lines stabilize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Micro-LED Gains Momentum Despite Manufacturing Hurdles

Conventional LEDs maintained an 83.40% market share of LED chips in 2025 because entrenched supply chains and proven reliability still outweigh the performance advantages of newer architectures in high-volume lighting, signage, and LED display applications. Mini-LED adoption in premium televisions and monitors during 2025-2026 pushed chip counts per panel up by an order of magnitude, cushioning suppliers against ASP pressure even as die size shrank.[4]PatSnap, “Optimizing Cost-per-Lumen in Mini LED Manufacturing,” eureka.patsnap.com

Micro-LED chips, forecast to expand at an 11.23% CAGR, moved from prototyping into commercial reference modules for augmented-reality glasses at CES 2026, where JBD’s Hummingbird II Polychrome projector earned an Innovation Award. Despite mass-transfer yields hovering at 70-85%, recent patents covering multi-chip placement and AI-based defect detection are narrowing the cost gap with mini-LED, positioning micro-LED to penetrate high-luminance niches as processes mature.

By Semiconductor Material: GaN Dominance Faces Niche Challenges

Gallium nitride and indium gallium nitride accounted for 82.45% of the LED chip market share in 2025, owing to their unmatched efficiency in blue and white emitters that dominate lighting, backlighting, and automotive headlamps. Aluminum gallium indium phosphide serves red and amber needs in automotive signaling and horticulture, and is expanding at an 11.88% CAGR as spectral-specific applications proliferate. Emerging GaN-on-diamond substrates slash thermal resistance, enabling higher drive currents in high-power lamps without efficiency droop, a benefit particularly valued in compact automotive modules.

Material selection is also hostage to supply risk; China controls a significant share of refined gallium, and rare-earth phosphor chains are similarly concentrated, exposing global producers to geopolitical volatility. The LED chips market, therefore, sees R&D into alternative color-conversion schemes, including quantum-dot encapsulants and perovskite coatings, which could lessen dependence on scarce minerals while unlocking broader color gamut and higher efficacy.

By Application: Automotive Outpaces General Lighting Growth

General lighting accounted for 46.78% of the 2025 LED chips market, anchored by ongoing retrofits in homes, offices, and streets, yet its growth rate is moderating as penetration approaches saturation in developed economies. Mini-LED backlighting for televisions, monitors, and tablets supplies a counter-cyclical lift, offsetting OLED incursions in smartphones. Automotive lighting, forecast to surge at a 12.55% CAGR, is the clear volume and value engine, propelled by adaptive driving-beam mandates and consumer demand for distinctive styling cues.

Electric-vehicle platforms further accentuate adoption by valuing low-power, high-luminance headlamps that extend driving range. Concurrently, micro-LED-based augmented-reality head-up displays and interior ambient systems promise to raise chip counts per vehicle. These dynamics collectively diversify the LED chips market beyond replacement bulbs, insulating it from the commoditization squeeze affecting general-illumination SKUs.

Geography Analysis

Asia Pacific dominated the LED chips market with a 62.46% share in 2025, supported by concentrated epitaxial wafer capacity across China, Taiwan, South Korea, and Japan, and by large-scale demand programs such as India’s UJALA scheme, which had distributed 368.7 million bulbs by January 2025. San’an Optoelectronics operates one of the world’s largest clusters of MOCVD tools in Xiamen, enabling price leadership on commodity lamp dies, while Epistar in Taiwan has focused on high-performance chips for automotive and premium displays. South Korea’s Samsung LED and LG Innotek capture value from internal panel divisions that specify mini-LED and micro-LED backlighting, anchoring a regional ecosystem that stretches from sapphire ingot slicing to complete module export. Southeast Asia is emerging as a secondary manufacturing hub, illustrated by Seoul Semiconductor’s 2025 technology-transfer alliance with OMINSU Vietnam, which positions Vietnam as a supplier to brands in Europe and North America seeking China-plus-one sourcing. The region’s forecast CAGR of 11.97% through 2031 is also underpinned by rising urbanization and sustained government procurement of smart-city street lighting.

North America and Europe together account for a much smaller portion of the LED chips market, but deliver steady premium demand as regulations tighten on blue-light hazard, circular-economy design, and local content. Potential United States tariffs of up to 145% on Chinese LED components have already pushed companies such as Fusion Optix to consolidate Vermont-based LEDdynamics capacity as a hedge against import costs. The European Union’s Ecodesign directive, coupled with mandatory EPREL registration, is steering luminaires toward higher-efficacy chips and documented lifetime data, rewarding suppliers that can demonstrate rigorous photobiological testing. At the same time, premium automotive programs adopting adaptive-beam headlamps provide a growing market for high-reliability dies manufactured in Austria, Germany, and the Netherlands. These structural factors are expected to keep regional buyers focused on differentiated rather than commodity devices, anchoring mid-single-digit revenue growth even as global price pressure persists.

South America, the Middle East, and Africa have smaller installed bases, yet municipal street-lighting retrofits and expanding grid access create an attractive frontier for the LED chip market. Brazilian state tenders for LED luminaires require domestic-content thresholds that channel demand toward regional packagers able to source dies from Asia Pacific on favorable terms, while Gulf Cooperation Council nations fund showcase smart-city corridors that specify tunable-white and connected lamps. African governments are piloting bulk-procurement programs modeled on UJALA, though the limited scale keeps unit prices higher than in India or China. Vendors face fragmented safety and labeling rules ranging from Singapore’s Mandatory Energy Labeling Scheme to South Africa’s NRCS electrical approvals that complicate logistics but also deter the dumping of low-quality product. As policy harmonization improves and electricity access expands, these regions are projected to increase their combined share of the global LED chip market over the next decade.

Competitive Landscape

The LED chips market is moderately concentrated, with a small cadre of vertically integrated producers accounting for most high-volume epitaxial output while dozens of fabless design houses compete in niches. San’an Optoelectronics and Inari Amertron’s joint USD 239 million purchase of Lumileds in December 2025 shows how distressed Western assets can be redeployed under multi-jurisdiction ownership structures that sidestep earlier CFIUS objections. ams-OSRAM has committed EUR 588 million (USD 664 million) to expand its automotive-grade and high-power capacity, betting that reliability and thermal headroom will remain price-defensible despite a decline in commodity ASPs. Nichia, Samsung LED, LG Innotek, and Seoul Semiconductor maintain broad patent estates that block low-cost imitators and underpin multi-year supply agreements with tier-1 automotive lamp makers.

Process innovation rather than wafer count is now the key battleground. Patent CN118712309A introduces chip-scale packaging geometries that lower optical losses, while U.S. application US20240339575A1 details current-spreading structures that mitigate droop at high currents, both pointing to upside in margins for intellectual-property owners. VueReal, Aledia, and other venture-backed firms are betting on laser-assisted or vertical GaN-on-silicon micro-LED processes to leapfrog incumbent cost structures; however, the capital-intensive nature of mass-transfer equipment still favors larger panel integrators such as BOE and CSOT, which can afford pilot lines. Geopolitical constraints on gallium exports, which are concentrated at 98% in China, also pose systemic risk, prompting Japanese, European, and U.S. players to investigate recycling loops and alternative phosphor chemistries that decouple them from critical-mineral exposure.

Competition is further complicated by end-market bifurcation. General lighting dies trade almost exclusively on a lumen-per-dollar basis, inviting relentless undercutting from surplus Asian capacity, whereas automotive, display, horticulture, and ultraviolet disinfection segments can absorb price premiums for tight binning, high CRI, and extended thermal cycles. As a result, leading suppliers are splitting their product portfolios: one track focused on ultra-low-cost replacement lamps, and a second track optimized for high-value applications such as quantum-dot on-chip mini-LED displays or matrix headlamps. Companies that master both volume cost control and specialty innovation are likely to consolidate share as weaker players exit or merge under financial strain.

LED Chips Industry Leaders

Nichia Corporation

Lumileds Holding B.V.

ams-OSRAM AG

Samsung Electronics Co., Ltd. (Samsung LED)

Cree LED, an SGH Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cellid and JBD unveiled commercial-ready micro-LED projector modules for augmented-reality glasses at CES 2026, with JBD’s Hummingbird II Polychrome unit receiving a CES Innovation Award.

- January 2026: TCL introduced second-generation Super Quantum Dot Mini-LED televisions, embedding quantum dots directly on chips to reach near-100% DCI-P3 gamut.

- December 2025: San’an Optoelectronics and Inari Amertron completed a joint USD 239 million acquisition of Lumileds Holding, consolidating distressed assets under a China-Malaysia vehicle.

- September 2025: PatSnap identified multi-chip mass-transfer innovations capable of placing 1,000-3,000 mini-LED dies simultaneously, highlighting BOE’s and CSOT’s proprietary systems.

Global LED Chips Market Report Scope

The LED Chips Market Report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, AlGaInP, and Other Materials), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| South America | |

| Middle East and Africa |

| By LED Chip Technology | Conventional LEDs | |

| Mini-LED | ||

| Micro-LED | ||

| By Semiconductor Material | GaN / InGaN | |

| AlGaInP | ||

| Other Semiconductor Materials | ||

| By Application | General Lighting | |

| Automotive | ||

| Backlighting / Displays | ||

| Consumer Electronics | ||

| Industrial / Specialty Lighting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the LED chips market, and how fast is it growing?

The LED chips market stood at USD 36.15 billion in 2026 and is projected to reach USD 56.59 billion by 2031, reflecting a 9.38% CAGR over 2026-2031.

Which region accounts for the largest share of global LED chip revenues?

Asia Pacific dominates with a 62.46% share thanks to its extensive epitaxial wafer capacity and government-driven demand programs.

Why are micro-LED chips important for future display applications?

Micro-LED architectures deliver higher luminance, longer lifetime, and superior energy efficiency, positioning them for augmented-reality wearables and premium public displays once mass-transfer yields improve.

How are automakers influencing demand for LED chips?

Adaptive driving-beam mandates and consumer desire for distinctive lighting designs are pushing LED headlamps into mid-segment vehicles, driving a 12.55% CAGR in automotive applications through 2031.

What risks could disrupt the supply chain for LED chips?

Persistent ASP erosion from Asian overcapacity, gallium supply concentration in China, and high capital costs for micro-LED mass transfer pose the greatest threats to stable growth.

How are energy-efficiency policies shaping the global LED chips market?

Regulations in the European Union, China, India, and Vietnam have phased out low-efficacy lamps, ensuring a steady baseline of replacement demand even as unit prices fall.

Page last updated on: