Flexible LED Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

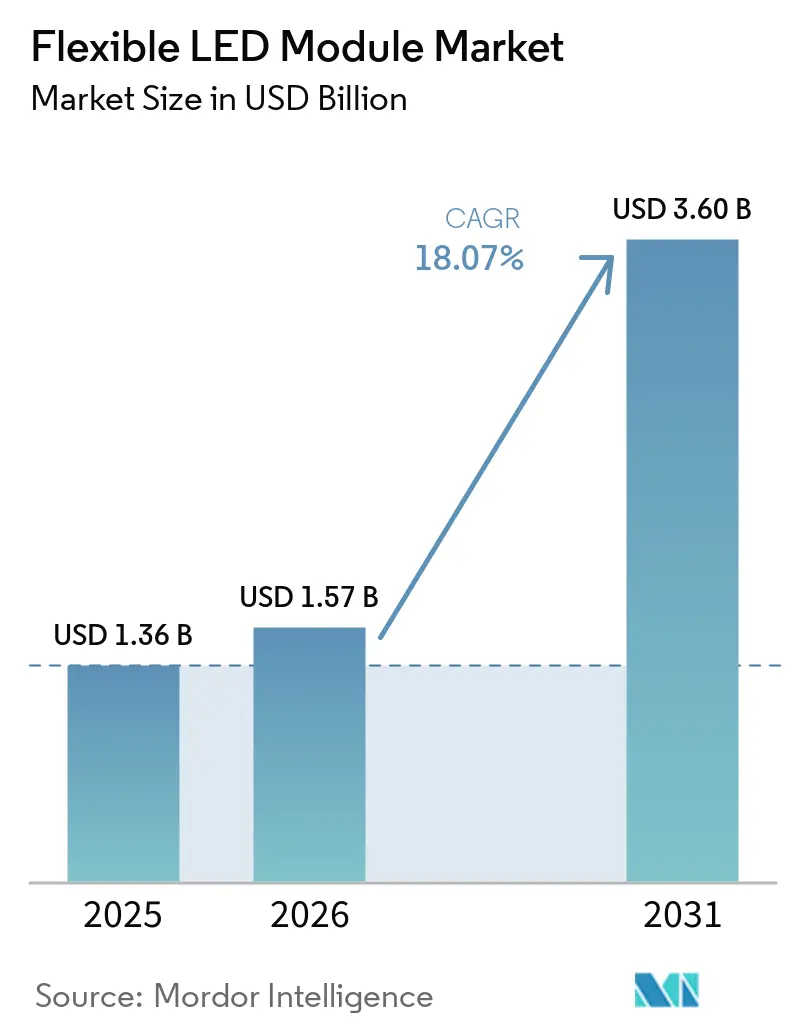

| Market Size (2026) | USD 1.57 Billion |

| Market Size (2031) | USD 3.60 Billion |

| Growth Rate (2026 - 2031) | 18.07% CAGR |

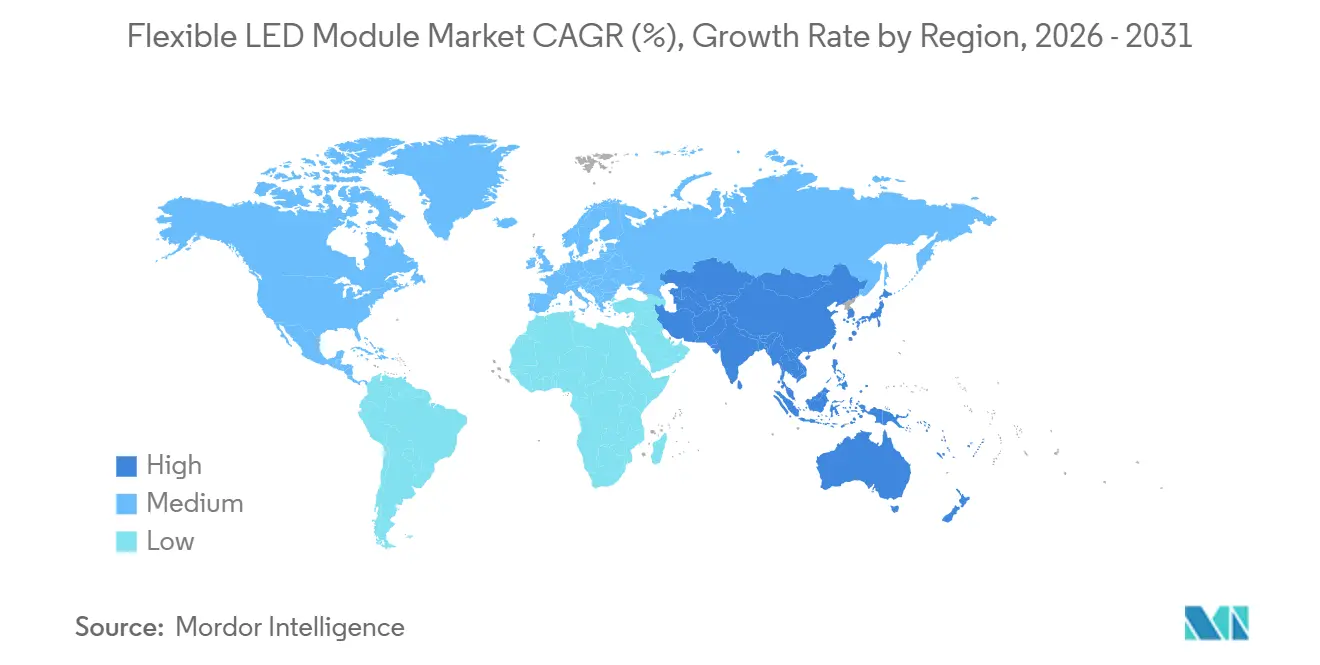

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

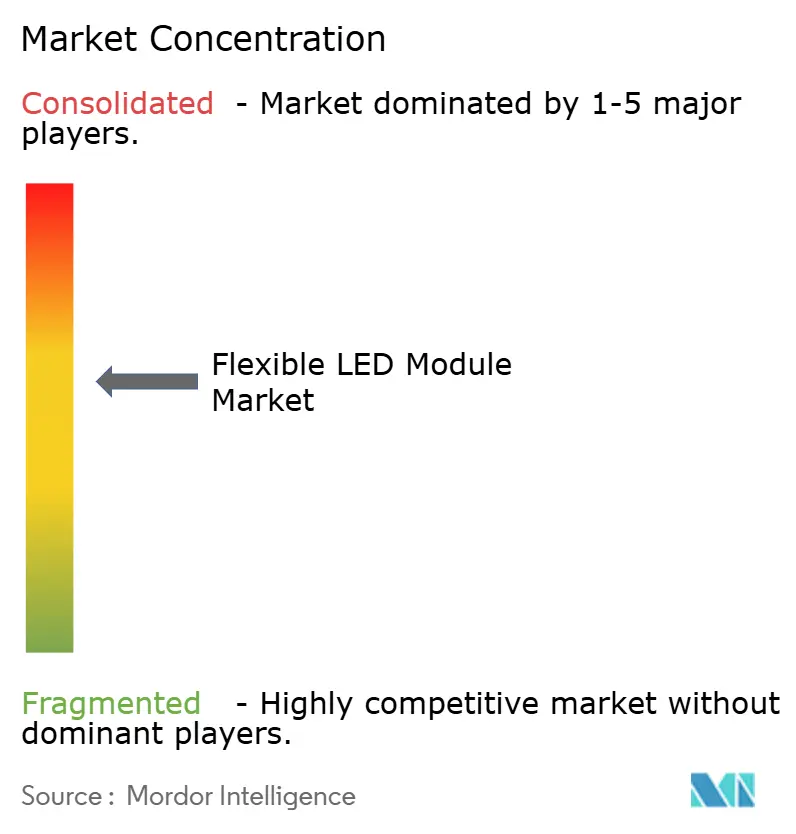

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible LED Module Market Analysis by Mordor Intelligence

The flexible LED module market size is expected to increase from USD 1.36 billion in 2025 to USD 1.57 billion in 2026 and reach USD 3.60 billion by 2031, growing at a CAGR of 18.07% over 2026-2031. Expanding adoption in premium automotive cabins, curved façade lighting, and non-planar digital signage keeps capital flowing into new capacity even as rare-earth costs climb. Mini-LED and micro-LED innovations amplify luminance and reliability, moving the flexible LED module market toward high-pixel-density cockpit displays and augmented-reality head-up units. Regulatory pushes such as California Title 24 2025 and EN IEC 60598-1:2024 raise the energy-efficiency and safety bar, nudging suppliers to embed advanced drivers and photobiological safeguards. Competitive pressure intensifies as Chinese glass-substrate lines scale, and patent cross-licensing among incumbents clears pathways for faster time-to-market.

Key Report Takeaways

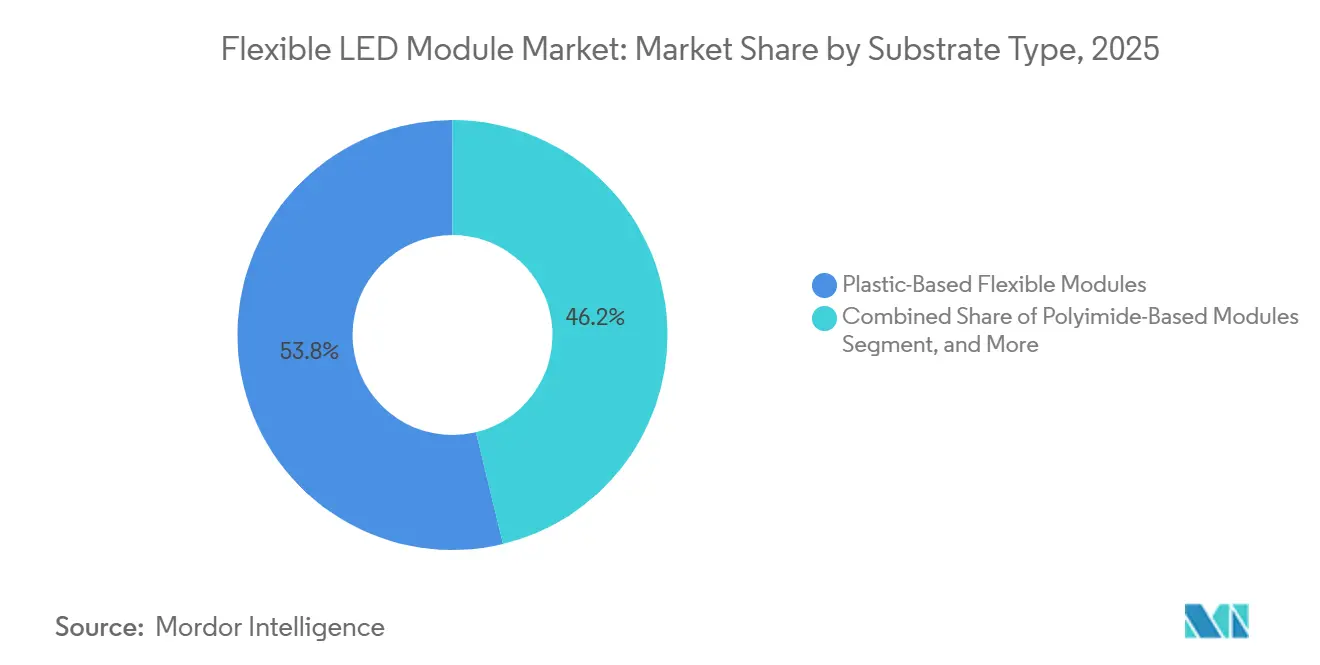

- By substrate type, plastic-based solutions held 53.78% of the flexible LED module market share in 2025, while polyimide modules are forecast to expand at an 18.56% CAGR through 2031.

- By form factor, strips accounted for 63.85% of 2025 volume, whereas panels are projected to grow at an 18.71% CAGR to 2031.

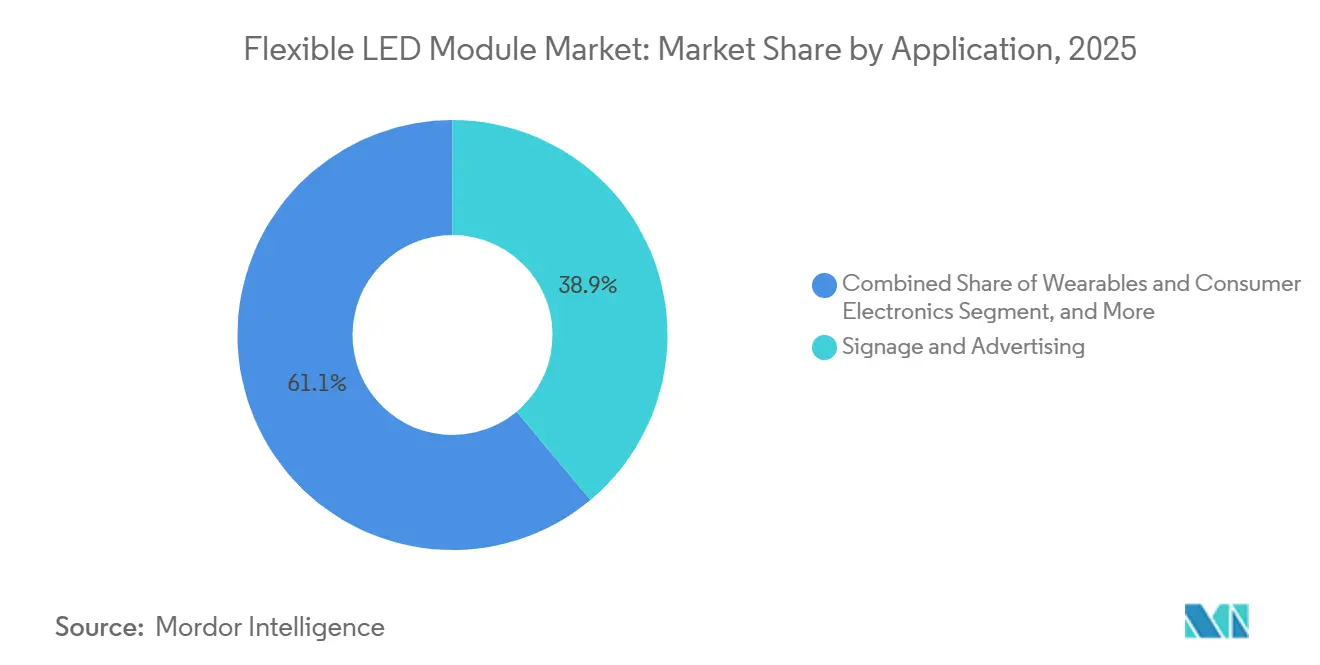

- By application, signage and advertising led with 38.92% revenue share in 2025, while automotive lighting records the highest projected CAGR at 18.86% through 2031.

- By geography, the Asia Pacific accounted for 67.89% of revenue in 2025 and is advancing at a 18.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flexible LED Module Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid adoption of flexible LED strips in architectural and decorative lighting projects | +3.2% | North America and Europe core, global spill-over | Medium term (2-4 years) |

| Increasing demand for energy-efficient signage and advertising solutions | +2.8% | Asia Pacific and North America | Short term (≤ 2 years) |

| Automotive OEM integration of interior ambient lighting for differentiation | +4.1% | Europe and Asia Pacific premium segments | Medium term (2-4 years) |

| Mini-LED and micro-LED backlighting driving high-density flexible modules for curved cockpit displays | +3.5% | Global automotive hubs, strongest in Europe and China | Medium term (2-4 years) |

| Rising popularity of wearables and flexible consumer electronics displays | +2.3% | Asia Pacific core, North America spill-over | Medium term (2-4 years) |

| Emergence of ultra-thin polyimide substrates enabling foldable lighting in smart textiles | +1.9% | Asia Pacific and Europe R&D centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Flexible LED Strips in Architectural and Decorative Lighting Projects

Flexible strips now replace rigid extrusions on curving coves, columns, and feature walls, delivering seam-free illumination at radii as small as 10 millimeters. The U.S. Department of Energy’s Solid-State Lighting V6.0 specification, effective in 2026, mandates 150 lumens-per-watt efficacy and smart dimming, accelerating upgrades in hospitality and retail.[1]U.S. Department of Energy, “Solid-State Lighting V6.0 Specification,” energy.gov European regulation EN IEC 60598-1:2024 tightens flicker and photobiological thresholds, lengthening certification lead times but boosting designer confidence in long-term reliability.[2]European Committee for Electrotechnical Standardization, “EN IEC 60598-1:2024,” cenelec.eu Chip-on-board neon-replacement strips cut power draw by 40% compared to legacy neon while lasting beyond 50 000 hours, a shift that trims maintenance budgets. Wide thermal envelopes from -40 °C to 105 °C enable installations from Nordic ski resorts to Gulf shopping malls, thereby broadening the flexible LED module market footprint.

Increasing Demand for Energy-Efficient Signage and Advertising Solutions

Municipal luminance caps and rising electricity tariffs push operators toward high-efficiency, flexible panels with integrated photovoltaic cells and real-time power logging. California Title 24 2025 compels outdoor billboards to auto-dim, reinforcing demand for modules with luminous efficacy exceeding 150 lumens-per-watt and embedded daylight sensors. Retailers report 30% lower installation labor when curved video walls ship as bendable panels rather than tiled, rigid cabinets, shortening payback to less than 2 years in prime storefronts. 4 000-nit curved micro-LED displays launched at CES 2025 let brands reach sunlit outdoor audiences where OLED fades. Cylindrical kiosks and wrap-around pillars made viable by flexible modules unlock new rentable surface area in transit hubs, driving incremental advertising yields.

Automotive OEM Integration of Interior Ambient Lighting for Differentiation

Luxury brands weave flexible strips along dashboards, door panels, and footwells to create mood-responsive cabins that strengthen model identity. Mini-LED and micro-LED backlit clusters exceed 300 pixels-per-inch and support 1 000-plus local dimming zones, matching OLED contrast without burn-in risk over 15-year vehicle lifecycles. Panoramic roof-mounted displays demonstrated at CES 2026 simulate skylight patterns, showing future premium differentiation vectors.[3]BOE Technology Group, “Ultra-High Brightness Micro-LED HUD Debut,” boe.com Tier-1 suppliers cite 20% reductions in wiring harnesses because narrow strips snake through tight crevices unreachable by rigid boards, trimming assembly time and warranty exposure. Compliance with IEC 60810:2017 vibration and EMC rules underscores the maturing safety profile of automotive-grade flexible modules.

Mini-LED And Micro-LED Backlighting Driving High-Density Flexible Modules for Curved Cockpit Displays

Curved clusters need uniform luminance across compound radii, a feat rigid boards cannot achieve without parallax artifacts. Flexible mini-LED backlights spread thousands of emitters closer to the bend, preserving image integrity at oblique viewing angles. Demonstrations of 50 000-nit micro-LED HUD units validate daylight readability for augmented-reality overlays, supporting advanced driver-assistance system rollouts. Smart mirrors and brake lights using flexible micro-LED matrices respond under 100 milliseconds, meeting stringent safety codes. Adherence to IEC 62717 thermal tests confirms the lifespan even when cabin temperatures reach 85 °C, providing automakers with confidence in warranty cost containment.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High initial costs of advanced flexible LED modules versus rigid alternatives | -2.1% | Global, sharpest in price-sensitive markets | Short term (≤ 2 years) |

| Supply chain price volatility for key semiconductors and rare earth phosphors | -1.7% | Asia Pacific manufacturing clusters | Short term (≤ 2 years) |

| Heat management challenges limiting lifespan at tight bending radii | -1.4% | Automotive and outdoor signage | Medium term (2-4 years) |

| Lack of uniform global bend-testing standards complicating OEM qualification cycles | -1.2% | Automotive and aerospace | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Costs of Advanced Flexible LED Modules Versus Rigid Alternatives

Polyimide modules still carry 40%-60% premiums over FR-4 boards because roll-to-roll lines operate at smaller volumes and rely on high-temperature polymers. Automotive mini-LED backlights for curved clusters cost between USD 80 and USD 120, roughly double rigid LCD backlights, constricting adoption in value-segment vehicles. Signage operators in emerging economies see capex exceeding USD 300 per square meter, lengthening payback periods when power tariffs remain below USD 0.10 per kilowatt-hour. Mass-transfer equipment costing more than USD 5 million per line limits entry to cash-rich firms, dampening competitive pricing pressure. Until JEDEC-like footprint standards emerge, tool reuse across projects remains limited, slowing cost-down curves.

Supply Chain Price Volatility for Key Semiconductors and Rare Earth Phosphors

China’s export controls on europium and terbium in October 2025 spiked spot prices 25% within three months, squeezing phosphor margins for LED makers without fixed contracts. Automotive-grade driver IC lead times stretched to 52 weeks, forcing board redesigns or premium brokerage buys that inflate the bill of materials. Gallium nitride wafer capacity tightened as foundries favored higher-margin power devices, compelling flexible LED module industry leaders to secure multi-year offtakes or risk stalled ramps. Vertical integration moves, such as San’an Optoelectronics' acquisition of Lumileds, mitigate exposure but require capital in excess of USD 1 billion and a multi-year execution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Type: Thermal Stability Drives Polyimide Upswing

Polyimide modules are advancing at a 18.56% CAGR, driven by cockpit displays and wearables that flex beyond 180 degrees while withstanding temperatures from -40 °C to 125 °C. The flexible LED module market for polyimide solutions benefits from glass-transition temperatures above 300 °C, enabling reflow profiles that are unsuitable for PET or polycarbonate. Continuous laser-assisted transfer places micro-LEDs within ±10 micrometers, securing luminance uniformity across curved dashboards. Plastic-based substrates still dominate cost-sensitive architectural lighting because their tooling is 30% cheaper, and bend radii above 20 millimeters relax mechanical stress. As voice-controlled smart-home systems proliferate, demand for tighter radii and elevated heat loads should gradually shift volume toward polyimide.

In non-automotive strip lighting, plastics remain adequate where ambient temperatures stay below 60 °C and mechanical flexing is infrequent. Yet mini-LED backlights with thousand-zone local dimming create hotspot currents that plastics cannot dissipate efficiently, nudging premium signage buyers toward polyimide. Hybrid metal-core flex and ceramic-filled polymers fill niches, such as industrial high-bay luminaires that need thermal conductivity above 2 W m-K. Cost parity is expected after 2028 as roll-to-roll yields climb and resin prices fall, pivoting a larger slice of the flexible LED module market toward high-performance substrates.

By Form Factor: Panel Growth Mirrors Wearable and Cockpit Curves

Strip formats owned 63.85% of 2025 shipments because electricians cut lengths on-site and chain them via simple connectors. However, panel and sheet modules are on a trajectory to outpace the market at an 18.71% CAGR, as smartwatch bezels, AR headsets, and curved dashboards require seam-free illumination. The flexible LED module market share for strips will gradually dilute as panel roll-to-roll lines halve costs by 2028. Wide-angle Hi-Micro panel technology achieves 0.6-millimeter pixel pitch, bridging the gap between signage and immersive control rooms.

Panels let automakers wrap instrument clusters across multiple viewing planes while preserving pixel homogeneity, a task beyond the capability of narrow strips. Retailers value continuous panels for cylindrical video columns where visible strip borders disrupt content. Strips will remain relevant for linear coves and footwell accents, but increasing demand for high-resolution imagery and custom geometries tilts momentum toward panels, particularly in consumer electronics, where bezel aesthetics drive brand perception.

By Application: Automotive Lighting Surges Past Signage Momentum

Signage and advertising accounted for 38.92% of 2025 revenue as flexible walls enlivened flagship stores and transit hubs, yet automotive lighting is accelerating fastest at a 18.86% CAGR through 2031. High-density micro-LED cockpit modules meeting 300 ppi and 10 000-nit specs attract premium OEM spending, propelling the flexible LED module market deeper into transportation interiors. Adaptive ambient packages now command USD 500-USD 1 200 options pricing in luxury vehicles, lifting supplier margins.

Wearables expand application diversity by integrating sub-millimeter panels into health trackers and phototherapy patches, niches with FDA and CE pathways that justify premium price points. Smart textiles remain exploratory but promising; gallium-alloy wiring that survives 8 000 stretch cycles indicates future revenue streams once washability and cost hurdles are overcome.[4]NHK Science and Technology Research Laboratories, “Stretchable Full-Color Display Progress,” nhk.or.jp

Geography Analysis

Asia Pacific led with 67.89% of 2025 revenue and is set to grow at an 18.81% CAGR, anchored by China’s aggressive capacity adds and South Korea’s USD 350 million government stimulus for intelligent LEDs. Investments such as Chenxian Optoelectronics’ RMB 3 billion (USD 417 million) expansion of its glass-substrate micro-LED capacity underscore regional momentum. Taiwan’s mass-transfer precision within ±1 micrometer cements the island as a hub for next-gen display subcontracting.

North America benefits from stringent energy codes such as Title 24 2025 and IECC 2024, which catalyze retrofits with high-efficiency modules, while leading entertainment venues install curved 8K signage to heighten visitor engagement. Europe follows with architectural refurbishments that favor low-flicker, flicker-safe flexible strips under EN IEC 60598-1, and premium automakers in Germany integrate micro-LED clusters to differentiate digital dashboards.

South America, the Middle East, and Africa hold smaller shares, but exhibit pockets of high growth tied to megaprojects such as Saudi Arabia’s USD 877 billion infrastructure pipeline and Brazil’s new smart-stadium builds ahead of continental sporting events. Suppliers entering these regions tailor packages for high-ambient-temperature operation and multi-voltage grids, positioning the flexible LED module market for long-term geographic diversification.

Competitive Landscape

Market concentration is moderate: Samsung Electronics, LG Innotek, Nichia, Seoul Semiconductor, and ams OSRAM together account for a significant share of revenue, yet rising Chinese players challenge incumbents. Nationstar and BOE accelerate glass-substrate micro-LED lines, aiming to halve cost curves by 2028, while Leyard deploys Hi-Micro panels at sub-0.6-millimeter pitch for immersive indoor walls. Patent cross-licensing between Nichia and ams OSRAM in 2025 reduces litigation risk and broadens access to matrix headlamp technology.

San’an Optoelectronics and Inari Amertron’s acquisition of Lumileds transferred 600-plus patent families, creating an IP arsenal that supports mainland module localization. Litigation remains a lever; Everlight’s 2026 infringement suit against Seoul Semiconductor could reshape royalty flows if the court rules in favor of the plaintiff. Start-ups such as VueReal pursue automotive mirrors and brake lights with micro-LED arrays that deliver sub-100-millisecond response times, signaling niche disruption.

Incumbents leverage certification infrastructure to meet IEC 62031:2026 safety and proprietary bend-fatigue demands, while newcomers tout agile pilot lines for rapid OEM prototypes. With glass-substrate fabs coming online and roll-to-roll yields improving, the flexible LED module industry is approaching a phase in which cost leadership and IP depth jointly dictate market-share trajectory.

Flexible LED Module Industry Leaders

Samsung Electronics Co., Ltd.

Nichia Corporation

OSRAM GmbH (ams-OSRAM)

Seoul Semiconductor Co., Ltd.

CreeLED Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Everlight Electronics filed a U.S. lawsuit alleging Seoul Semiconductor’s WICOP HF flip-chip LEDs infringe multiple patents.

- January 2026: Chenxian Optoelectronics committed RMB 3 billion (USD 417 million) to expand glass-substrate micro-LED capacity by 22 000 m² per year.

- January 2026: AUO showcased a Virtual Sky Canopy micro-LED cockpit at CES 2026.

- January 2026: Tianma launched a 49.6-inch curved ACRUS display and mini-LED HUD rated 10 000-12 000 nits at CES 2026.

Global Flexible LED Module Market Report Scope

The Flexible LED Module Market Report is Segmented by Substrate Type (Plastic-Based Flexible Modules, Polyimide-Based Modules, Other Substrate Type), Form Factor (Strip/Linear Flexible Modules and Panel/Sheet Flexible Modules), Application (Signage and Advertising, Automotive Lighting, Wearables and Consumer Electronics, Architectural and Decorative Lighting, Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Plastic-Based Flexible Modules |

| Polyimide-Based Modules |

| Other Substrate Type |

| Strip / Linear Flexible Modules |

| Panel / Sheet Flexible Modules |

| Signage and Advertising |

| Automotive Lighting (Interior and Ambient) |

| Wearables and Consumer Electronics |

| Architectural and Decorative Lighting |

| Other Applications (Medical, Specialty) |

| North America |

| Europe |

| Asia-Pacific |

| South America |

| Middle East and Africa |

| By Substrate Type | Plastic-Based Flexible Modules |

| Polyimide-Based Modules | |

| Other Substrate Type | |

| By Form Factor | Strip / Linear Flexible Modules |

| Panel / Sheet Flexible Modules | |

| By Application | Signage and Advertising |

| Automotive Lighting (Interior and Ambient) | |

| Wearables and Consumer Electronics | |

| Architectural and Decorative Lighting | |

| Other Applications (Medical, Specialty) | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the main catalyst behind the rising use of flexible LED modules inside vehicle cabins?

Premium automakers deploy ambient-lighting strips and curved mini-LED clusters to differentiate interiors, reduce wiring complexity by 20%, and meet IEC 60810:2017 safety standards.

How quickly are polyimide-based modules expanding compared with plastic substrates?

Polyimide solutions are advancing at a 18.56% CAGR through 2031, supported by their 300 °C glass-transition temperature, which enables tighter bend radii and high-current mini-LED backlights.

Which geography currently delivers the largest revenue for suppliers?

Asia Pacific accounts for 67.89% of 2025 global sales and grows at an 18.81% CAGR, driven by Chinese capacity additions and South Korea’s USD 350 million stimulus for intelligent LEDs.

Why do flexible modules still carry a premium over rigid alternatives?

Roll-to-roll volumes remain lower, polyimide materials cost more, and mass-transfer tools exceed USD 5 million per line, keeping module prices 40-60% above FR-4 boards.

How are new energy regulations affecting digital-signage projects?

Codes like California Title 24 2025 enforce automatic dimming, pushing operators toward high-efficacy panels with integrated sensors that cut energy use and speed two-year paybacks.

Will panels or strips dominate shipments over the next five years?

Strips retain volume leadership today, but panels are forecast to outpace them at an 18.71% CAGR as wearables, curved dashboards, and cylindrical video walls need seam-free illumination.

Page last updated on: