Mini LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

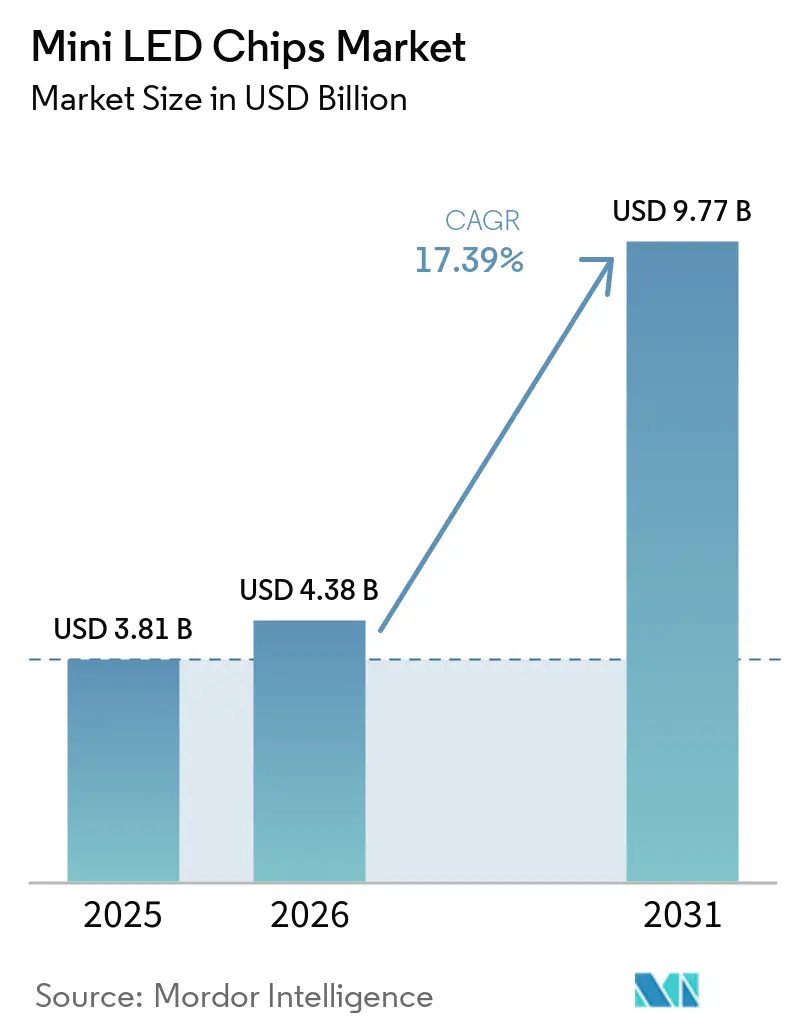

| Market Size (2026) | USD 4.38 Billion |

| Market Size (2031) | USD 9.77 Billion |

| Growth Rate (2026 - 2031) | 17.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mini LED Chips Market Analysis by Mordor Intelligence

The Mini LED Chips market size is projected to expand from USD 3.81 billion in 2025 and USD 4.38 billion in 2026 to USD 9.77 billion by 2031, registering a CAGR of 17.39% between 2026 to 2031. Continued migration from conventional LED backlighting and OLED toward mini-LED architectures is improving display economics by delivering high dynamic range at lower capital intensity. Mini-LED televisions dominated 2026 trade-show floors, underscoring shipment momentum that is set to exceed 20 million units as consumers prioritize brightness and screen size over emissive alternatives. Asia Pacific leads demand thanks to Chinese appliance-replacement subsidies that help local brands capture premium segments formerly held by Korean players. Concurrently, breakthroughs in GaN-on-silicon epitaxy and laser-assisted mass transfer are suppressing per-chip costs just as vertically integrated panel makers deepen competition across the Mini LED Chips market.

Key Report Takeaways

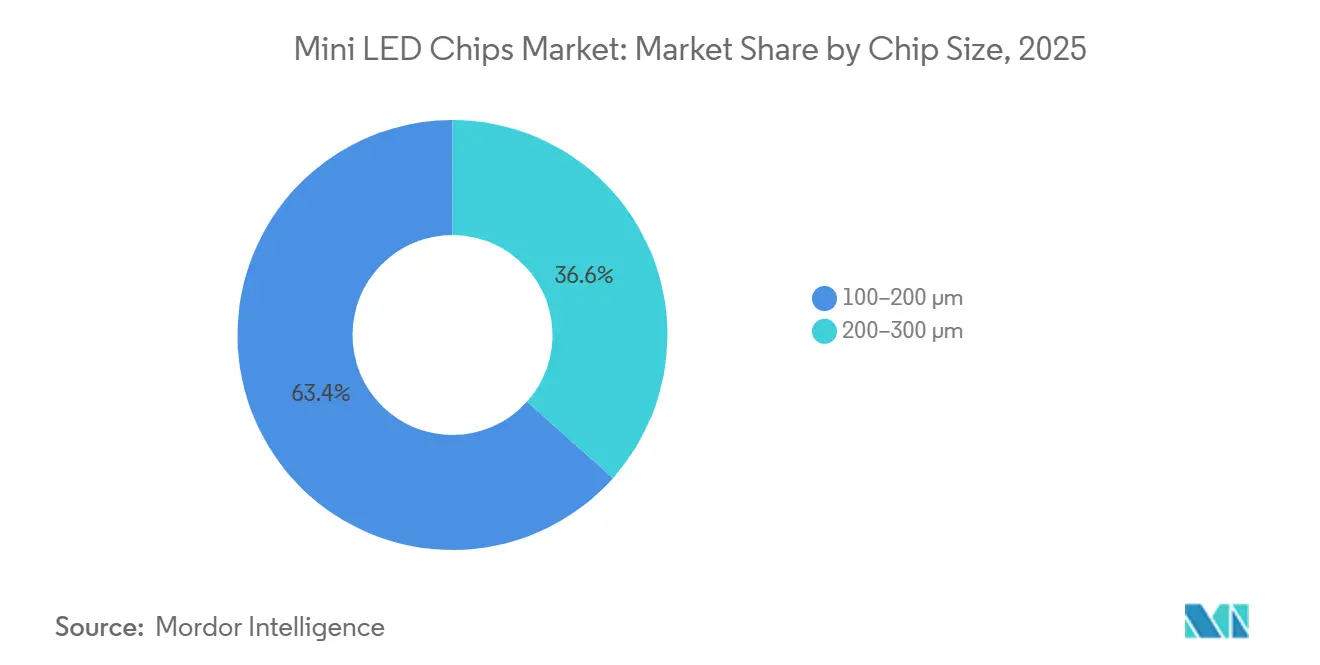

- By chip size, the 100-200 µm category led with 63.40% of the Mini LED Chips market share in 2025, while 200-300 µm chips are projected to advance at a 20.56% CAGR through 2031.

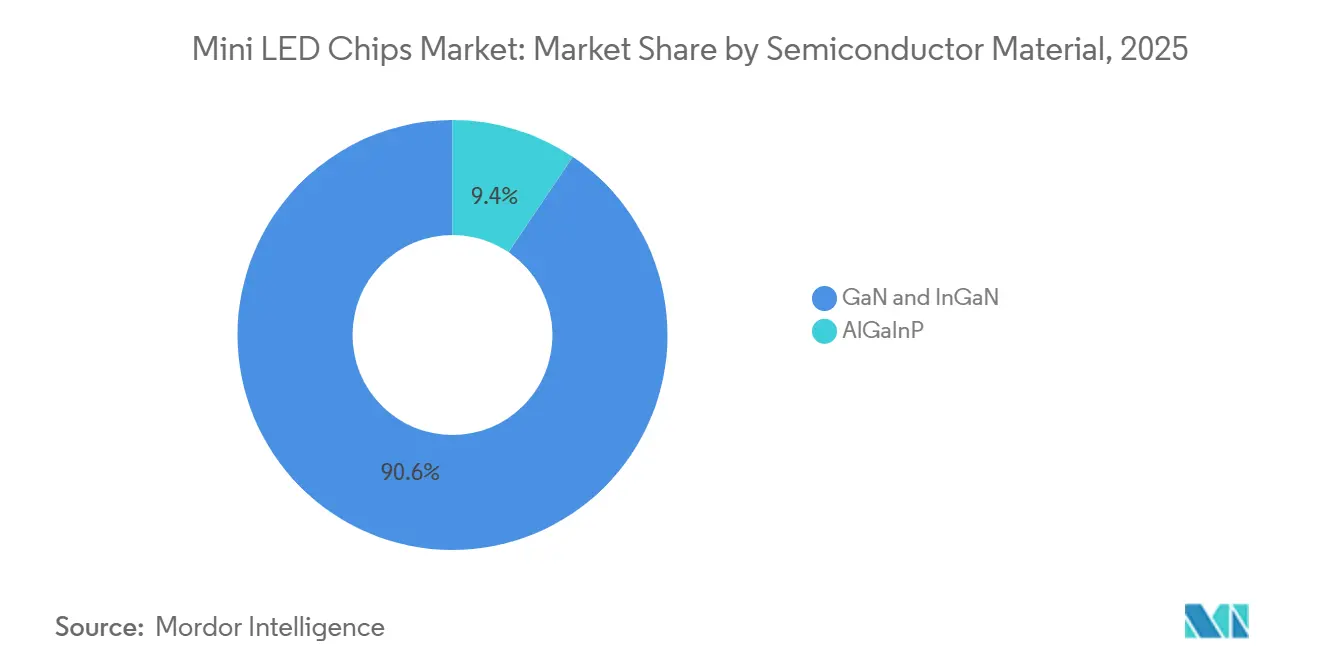

- By semiconductor material, GaN and InGaN captured 90.56% revenue share in 2025, whereas AlGaInP devices are poised to grow at a 20.77% CAGR to 2031.

- By application, television backlighting accounted for 37.80% of the Mini LED Chips market size in 2025, and automotive displays are forecast to expand at a 21.20% CAGR between 2026 and 2031.

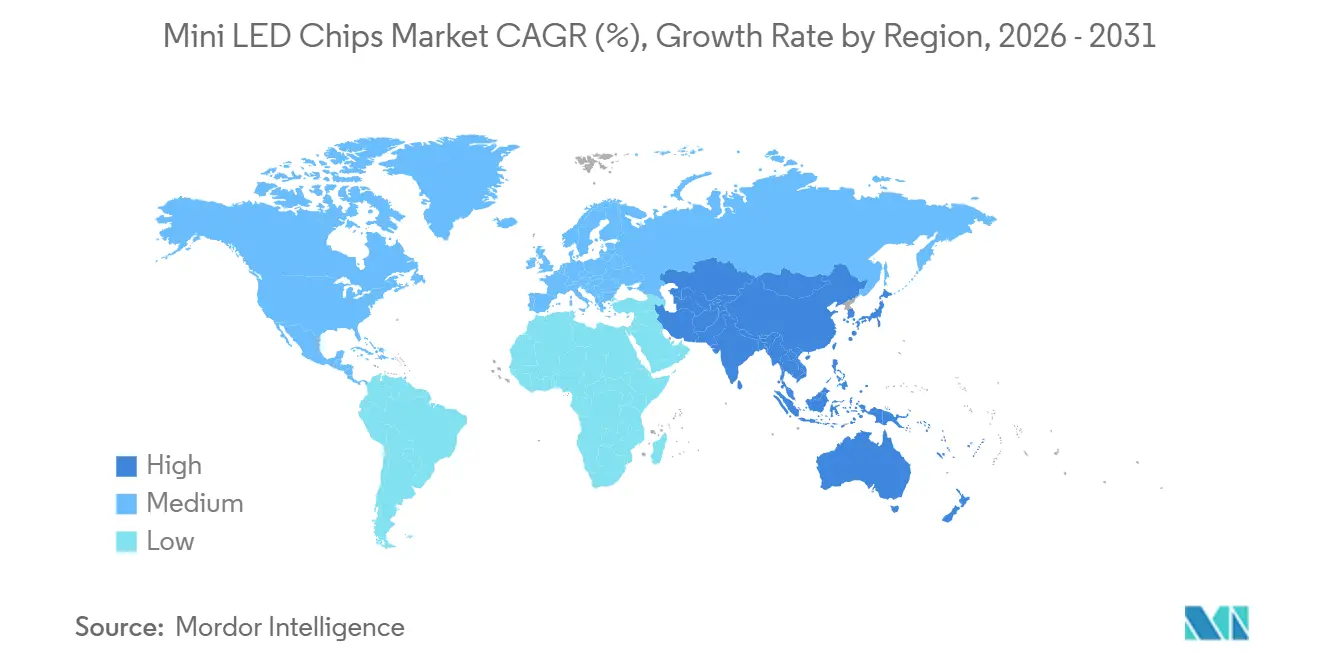

- By geography, the Asia Pacific accounted for 60.76% of global revenue in 2025 and is set to grow at a 21.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mini LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging Demand for High-Brightness HDR Television Panels | +4.2% | Global, with the Asia-Pacific core and spill-over to North America and Europe | Medium term (2-4 years) |

| Advanced GaN-on-Si Epitaxy Enabling Larger Wafer Yields | +3.8% | Global, led by Taiwan and China epi-wafer manufacturers | Long term (≥ 4 years) |

| Regional Subsidies Accelerating Mini LED Capacity Build-Out in China | +3.5% | China, with indirect pricing pressure on global markets | Short term (≤ 2 years) |

| Rapid Cost Decline in Mass-Transfer Equipment | +2.9% | Global, concentrated in Taiwan, Korea, and China assembly hubs | Medium term (2-4 years) |

| OEM Preference for Longer-Lifetime Backlights in Gaming Monitors | +1.6% | North America, Europe, and the Asia-Pacific gaming markets | Short term (≤ 2 years) |

| Regulatory Push for Energy-Efficient Automotive Cockpit Displays | +1.4% | Europe (EU ecodesign), China (energy labels), North America (CAFE-related) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for High-Brightness HDR Television Panels

Trade-show floors in 2026 were crowded with televisions boasting up to 20,000 local-dimming zones and 10,000 nits peak brightness, narrowing the perceived advantage of emissive technologies at premium screen sizes.[1]TCL Central, “TCL X11L SQD-Mini LED TVs Launched at CES 2026,” tclcentral.com Chinese brands captured a significant share of global TV unit shipments by early 2026 after pairing aggressive zone counts with subsidy-supported pricing. Samsung retained the top revenue position in the United States by expanding its Neo QLED range and adding new mini-LED SKUs that target brightness-oriented consumers. Panel makers are optimizing thermal architectures and dimming algorithms to sustain brightness across larger diagonals, a shift that amplifies zone counts without proportional cost jumps. As consumers equate luminance headroom with picture quality, the mini LED chips market benefits from a virtuous upgrade cycle across both developed and emerging regions.

Advanced GaN-on-Si Epitaxy Enabling Larger Wafer Yields

Partnerships between materials specialists and high-volume LED manufacturers are bringing 200 mm GaN-on-silicon wafers into commercial production, reducing substrate costs while increasing die counts per run. Demonstrations of lattice-compatible AlN buffer layers delivered external quantum-efficiency gains of more than 30%, validating that silicon substrates can meet brightness targets formerly reserved for sapphire. Foundry-style tool sets already in place for power devices lower incremental capex, creating a glide-path to 300 mm adoption that aligns with broader semiconductor scaling roadmaps. Higher on-wafer and wafer-to-wafer uniformity improves bin-yield economics, helping panel makers lock in long-term cost reduction trajectories. These advantages reinforce vertical integration plays and accelerate the migration of the mini LED chips market toward silicon-centric supply chains.

Regional Subsidies Accelerating Mini LED Capacity Build-Out in China

Provincial and national programs co-finance clean rooms, tooling, and working capital, enabling domestic manufacturers to ramp capacity faster than self-funded peers abroad. Subsidy-backed scale allowed TCL and Hisense to surpass Samsung in global mini-LED TV share during 2024, setting new price floors that ripple through worldwide channels. San’an Optoelectronics invested USD 1.68 billion in Hubei for a facility targeting more than 2 million chips annually, though equipment-delivery delays pushed the usable-state milestone to mid-2026. Government incentives mitigate these delays by offsetting depreciation and financing costs, allowing firms to maintain aggressive output targets despite macroeconomic uncertainty. Accelerated Chinese production intensifies global competition and compresses learning curves, lifting adoption across the mini LED chips market.

Rapid Cost Decline in Mass-Transfer Equipment

Laser-assisted transfer platforms now achieve sub-micron placement accuracy with yields above 99%, slashing per-chip assembly costs for high-zone-count backlights.[2]Luo Cheng et al., “Laser-Assisted Mass Transfer Technology for Microlight-Emitting Diodes,” Nanomanufacturing and Metrology, doi.org Blister-type dynamic release layers demonstrated single-step transfer yields of 99.3% for sub-30 µm dice, validating scalable mechanics for future micro-LED crossover. Equipment makers integrate digital micromirror devices and galvanometer scanning to push throughput toward 14 million chips per hour, a pace that directly lowers line-level amortization. As cycle times fall, manufacturers can justify higher zone densities without breaching cost envelopes, expanding endpoint demand across televisions, monitors, and automotive cockpits. The resulting productivity gains underpin the mini LED chip market's double-digit growth trajectory over the forecast horizon.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Competition from OLED and Emerging Micro-LED Technologies | -2.8% | Global, with premium-segment pressure in North America, Europe, and developed APAC | Medium term (2-4 years) |

| High Capital Intensity of Clean-Room Bonding Lines | -2.1% | Global, acute in regions with limited subsidy support (North America, Europe) | Long term (≥ 4 years) |

| Supply-Chain Volatility for Sapphire and Rare-Earth Phosphors | -1.3% | Global, with exposure concentrated in supply chains reliant on single-source sapphire or phosphor suppliers | Short term (≤ 2 years) |

| Complex Thermal Management Requirements for Dense LED Arrays | -0.9% | Global, particularly in automotive and high-brightness display applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from OLED and Emerging Micro-LED Technologies

Apple’s 2025 iPad Pro launch showed tandem OLED panels hitting 1,000 nits full-screen brightness and a 2,000,000:1 contrast ratio, capabilities that erode mini-LED’s advantage in thin-and-light devices.[3]Apple, “Apple Introduces the Powerful New iPad Pro With the M5 Chip,” apple.com OLED price erosion is cascading into the 55-inch and 65-inch television tiers, forcing mini-LED brands to escalate zone counts and peak luminance just to sustain premiums. Meanwhile, GaN-on-Si partnerships targeting 200 mm wafers position micro-LED for future cost parity, raising the prospect of technological leapfrog within the forecast window. This two-front squeeze shortens the window during which mini-LED can command higher margins, tempering growth expectations in certain premium segments. Vendors must therefore sharpen value propositions around brightness, lifetime, and screen size to defend share.

High Capital Intensity of Clean-Room Bonding Lines

Mid-scale chip-on-glass facilities routinely exceed USD 50 million in upfront investment, a hurdle that limits participation to conglomerates or subsidy-backed newcomers. TCL’s USD 70 million purchase of Prima underscores the premium that panel makers place on in-house chip control, while also highlighting the financial burden of backward integration. Operators in North America and Europe bear higher effective costs because they lack the tax credits and low-interest financing available in China, widening the global competitiveness gap. Rapid node evolution compounds risk, since tooling optimized for 100-200 µm dice may require costly retrofits to handle larger or sub-100 µm formats. These dynamics slow greenfield investments outside the Asia Pacific and cap capacity growth in higher-cost regions for the mini LED chip market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chip Size: Larger Dies Expand Automotive And Ultra-Large Displays

The 100-200 µm category captured 63.40% of the Mini LED Chips market share in 2025, cementing its role in high-zone televisions and gaming monitors. Smaller dice let set makers pack more local-dimming zones into mainstream panel sizes, suppressing halo artifacts while preserving aggressive retail price points. The resulting volumes anchor unit economics that still favor sapphire substrates and proven mass-transfer jigs. Yet panel buyers are signaling appetite for even richer contrast, nudging suppliers toward higher zone counts that strain inspection throughput and yield management. Continuous refinements in die singulation and sidewall passivation aim to sustain brightness at ever-smaller footprints, protecting the mainstream role of this size class through 2031.

The 200-300 µm group is projected to expand at a 20.56% CAGR, lifting the Mini LED Chips market size for larger chip formats as automakers and ultra-large TV vendors simplify driver architectures.[4]AUO, “Smart Cockpit – Display HMI,” auo.comFewer, brighter dice per zone cut placement reduces placement time and driver count, easing thermal design for curved cockpit displays that stretch pillar to pillar. Automotive original equipment manufacturers also gain compliance headroom under energy-efficiency mandates because larger dice operate at lower current density. Suppliers therefore invest in GaN-on-Si lines that balance die-count reduction with chip-on-glass bonding precision, a trade-off that continues to favor larger dice in display areas above 1 m². The convergence of cost, reliability, and integration advantages positions this size class to narrow the volume gap with mainstream formats by the end of the forecast window.

By Semiconductor Material: Red Efficiency Gains Unlock Full-Color Adoption

GaN and InGaN devices accounted for 90.56% of 2025 revenue, as they remain the default blue and green emitters for television and monitor backlights. Their mature epitaxy, robust defect management, and compatibility with phosphor down-conversion continue to set the performance bar on brightness and reliability. Foundry migration to 200 mm silicon wafers further reduces substrate cost, reinforcing their incumbency while opening integration paths with logic wafers for future interactive functions. Manufacturers will continue optimizing buffer structures and surface treatments to increase external-quantum efficiency, especially for green dice that have historically lagged behind blue counterparts. Sustained improvements ensure GaN-based material systems anchor baseline economics for most backlight arrays through 2031.

AlGaInP chips, though still a minority, are forecast to post a 20.77% CAGR as sidewall engineering restores energy efficiency at micron scales. Multi-layer dielectric passivation and steam-oxidation treatments cut leakage and recover radiative recombination, enabling red subpixels that no longer bottleneck overall luminous efficacy. As a result, the Mini LED Chips market share for AlGaInP is poised to rise in direct-view RGB signage and full-color automotive clusters where phosphor conversion is impractical. Equipment makers are recalibrating lift-off chemistries to accommodate the softer III-V lattice while safeguarding high-throughput mass transfer. These advances collectively move the ecosystem closer to balanced RGB mini-LED stacks, reducing reliance on color-filter or quantum-dot conversion layers.

By Application: Automotive Displays Accelerate, Televisions Hold Scale Lead

Television backlighting held 37.80% of the Mini LED Chips market in 2025 and should retain absolute-volume leadership as brands roll out higher zone counts down the mid-tier price ladder. Mainstream 65-inch models that once carried hundreds of zones now ship with thousands, a progression that swells chip demand even as preset prices decline. Manufacturers differentiate on brightness, algorithmic dimming, and quantum-dot gamut, which collectively extend the lifespan of liquid-crystal display architectures against emissive rivals. Retail promotions tied to sports events and holiday seasons further stabilize shipment rhythm, sustaining predictable chip procurement cycles for upstream suppliers. Consequently, the television segment remains the anchor tenant that provides volume scale for backend assembly lines worldwide.

Automotive cockpit displays are set to grow at a 21.20% CAGR as original equipment manufacturers integrate local-dimming panels into clusters, center stacks, and e-mirrors. High brightness under direct sunlight, long lifetime at elevated cabin temperatures, and fine-grained dimming for night-mode compliance give mini-LED an edge over OLED in safety-critical applications. Supply chains already validate vibration resistance and wide operating-temperature ranges, reducing homologation barriers for new platform launches. Larger dice and matrix drivers cut harness complexity, helping automakers meet weight and power budgets mandated by fuel-economy regulations. Together, these factors elevate automotive from a niche into a strategic growth pillar that diversifies demand beyond consumer electronics.

Geography Analysis

Asia Pacific accounted for 60.76% of mini LED chip revenue in 2025, and the region is forecast to grow at a 21.54% CAGR through 2031 as Chinese subsidies, Taiwanese epitaxy expertise, and Korean panel investments converge into a self-reinforcing supply network. Provincial grants lower capital costs for new fabs, while Shenzhen and Xiamen clusters shorten learning cycles on mass transfer and driver IC packaging. Taiwan’s move to 200 mm GaN-on-silicon epitaxy leverages existing semiconductor infrastructure, raising output without proportional tool spend. Korea’s display majors defend share by pushing RGB mini-LED TV lineups, anchoring premium LCD differentiation even as they scale OLED fabs.

North America contributes a smaller volume but outsized revenue thanks to high-end gaming monitors and premium televisions that favor mega-zone backlights. Brands such as Samsung, Acer, and ViewSonic capture enthusiast demand with sets and displays certified to HDR1000 and above. Retail analytics show consumers choosing mini-LED for peak brightness that OLED cannot sustain during daytime viewing, especially in large suburban living rooms. Automotive rollouts support the regional mix as Detroit and Silicon Valley startups adopt curved cockpit panels sourced from Asian fabs yet tuned to U.S. infotainment stacks. Regulatory headwinds are mild, but the Inflation Reduction Act’s manufacturing credits could spur localized assembly of driver boards and final modules, nudging partial supply migration stateside.

Europe accounts for a modest share but sets technology direction through ecodesign regulations that push energy efficiency.[5]European Union, “Ecodesign and Energy Labelling — Electronic Displays,” eur-lex.europa.eu German premium-car brands deploy mini-LED clusters and passenger displays to meet readability standards under bright ambient light, catalyzing partnerships with Taiwanese and Japanese module makers. European retailers promote mini-LED televisions as sustainable upgrades, citing lower power consumption per nit compared to plasma sets being replaced. However, elevated electricity prices temper overall screen-upgrade cycles, moderating unit growth compared with Asia Pacific. Industrial adoption in medical imaging and broadcast studios offers an incremental avenue, leveraging mini-LED’s stable luminance and long lifetime.

Competitive Landscape

The mini LED chips market remains moderately fragmented as vertically integrated television brands, traditional LED suppliers, and semiconductor foundries vie for control of key process steps. TCL CSOT’s January 2026 acquisition of an 80% stake in Prima for CNY 490 million (USD 70 million) signals deeper backward integration after ramping a 6,000 m² video-wall line in Suzhou during 2025. Samsung and LG counter this encroachment by refreshing Neo QLED assortments and showcasing AI-enhanced RGB mini-LED backlights at CES 2026, reinforcing their premium positioning in the United States and Europe. Chinese panel makers also tap domestic subsidies to expand clean-room bonding, eroding Korean players’ early-mover cost advantages.

Epitaxial wafer specialists are scaling GaN-on-silicon formats to 200 mm, enabling foundry-style cost curves that appeal to fab-less display innovators. ALLOS Semiconductor and Ennostar’s partnership exemplifies this trend by combining proprietary buffer designs with high-volume LED infrastructure to offer brighter dice at lower wafer costs. San’an Optoelectronics, with a USD 1.68 billion project in Hubei, targets annual output exceeding 2 million chips, though equipment delays have shifted full ramp to mid-2026. Such capacity expansions compress average selling prices and accelerate the diffusion of technology into monitors and automotive clusters.

Equipment vendors are emerging as strategic gatekeepers by unlocking mass-transfer yields above 99% at throughputs approaching 14 million chips per hour. Cree LED’s February 2026 launch of OptiLamp embeds driver intelligence in each pixel, allowing 1/1 scan operation that simplifies system integration and trims power budgets for direct-view signage. Nichia’s µPLS Mini extends matrix-style headlamp applications, enabling adaptive pixel control for dynamic projections on road surfaces.

Mini LED Chips Industry Leaders

Epistar Corporation

Samsung Electronics Co. Ltd.

LG Display Co. Ltd.

AUO Corporation

San’an Optoelectronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cree LED unveiled OptiLamp LEDs, integrating driver intelligence into each pixel for true 1/1 scan operation and 24-bit control, with a live demonstration scheduled with LED Studio at ISE 2026 in Barcelona.

- January 2026: TCL CSOT acquired an 80% equity stake in Prima for CNY 490 million (USD 70 million), securing in-house chip capacity that complements its Suzhou mini-LED video-wall line.

- January 2026: TCL Electronics and Sony signed a memorandum of understanding to form a global home-entertainment joint venture, planning to leverage TCL’s mini-LED supply chain when operations begin in Apr 2027.

- January 2026: ALLOS Semiconductor and Ennostar partnered to commercialize 200 mm GaN-on-Si epiwafers, combining ALLOS’s buffer technology with Ennostar’s high-volume LED infrastructure.

Global Mini LED Chips Market Report Scope

The Mini LED Chips Market Report is Segmented by Chip Size (100-200 µm and 200-300 µm), Semiconductor Material (GaN/InGaN and AlGaInP), Application (Television Backlighting, Gaming Monitors and Laptops, Tablets and Smartphones, Automotive Displays, VR/AR Displays, and Other Applications), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 100–200 µm |

| 200–300 µm |

| GaN / InGaN |

| AlGaInP |

| Television Backlighting |

| Gaming Monitors and Laptops |

| Tablets and Smartphones |

| Automotive Displays (Instrument Cluster, HUD, Infotainment) |

| VR/AR Displays |

| Other Applications (Industrial Displays, Medical Displays) |

| North America |

| Europe |

| Asia Pacific |

| South America |

| Middle East and Africa |

| By Chip Size | 100–200 µm |

| 200–300 µm | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| By Application | Television Backlighting |

| Gaming Monitors and Laptops | |

| Tablets and Smartphones | |

| Automotive Displays (Instrument Cluster, HUD, Infotainment) | |

| VR/AR Displays | |

| Other Applications (Industrial Displays, Medical Displays) | |

| By Geography | North America |

| Europe | |

| Asia Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the projected size of the mini-LED chips sector by 2031?

The market is forecast to reach USD 9.77 billion by 2031, rising from USD 4.38 billion in 2026.

Which region leads demand for mini-LED chips?

Asia Pacific holds the largest share, driven by Chinese subsidies, Taiwanese epitaxy, and Korean display investments.

Why are automotive makers adopting mini-LED backlights?

Mini LEDs deliver high brightness in sunlight, long lifetime at cabin temperatures, and energy efficiency that helps meet regulatory targets.

How does GaN-on-silicon influence cost structures?

Moving to 200 mm silicon wafers boosts die counts per run and leverages existing semiconductor tooling, lowering per-chip costs.

What technology threatens mini-LED’s premium window?

OLED price erosion in near-term devices and the longer-term rise of micro-LED pose competitive pressures on mini-LED value propositions.

Which chip size category is expanding fastest?

Chips measuring 200-300 µm are growing at a 20.56% CAGR as they simplify driver architectures for large televisions and automotive displays.

Page last updated on: