United States LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

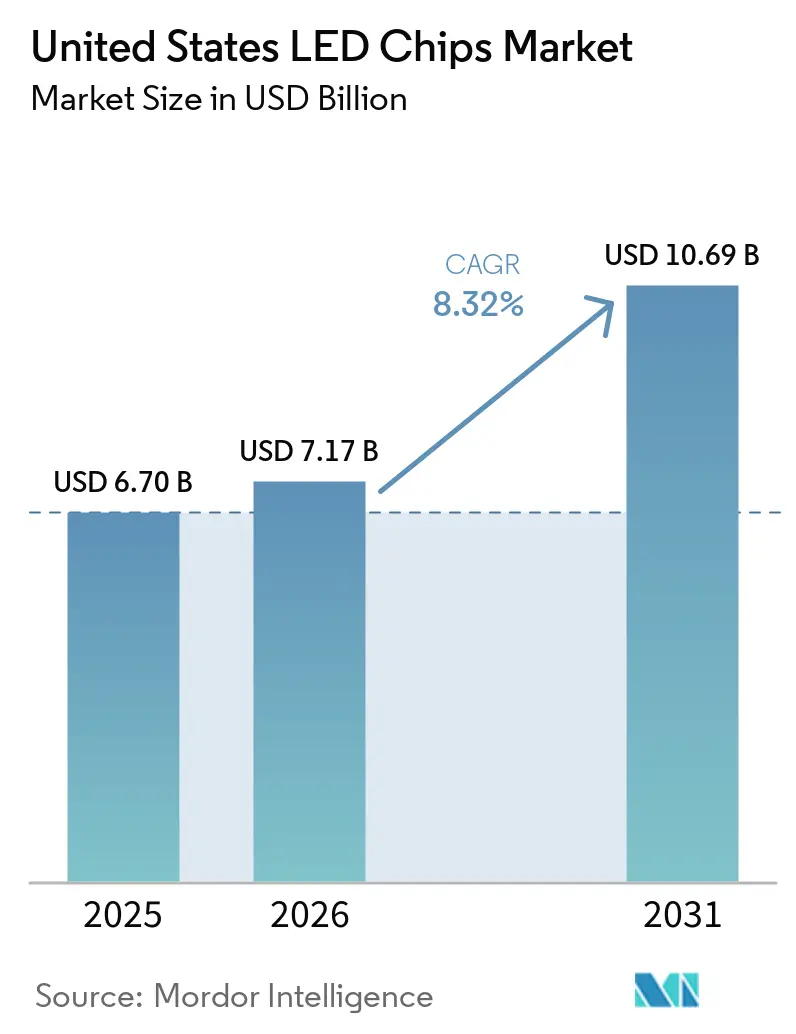

| Base Year Market Size (2025) | USD 6.70 Billion |

| Market Size (2026) | USD 7.17 Billion |

| Market Size (2031) | USD 10.69 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States LED Chips Market Analysis by Mordor Intelligence

The United States LED chips market size was valued at USD 6.70 billion in 2025 and estimated to grow from USD 7.17 billion in 2026 to reach USD 10.69 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031). Federal energy mandates, utility incentives, and swift advancements in automotive pixel lighting and mini LED backlighting fuel this growth. These factors are driving up orders for gallium nitride (GaN) and aluminum gallium indium phosphide (AlGaInP) emitters. By 2035, LED lighting installations nationwide are set to save 569 terawatt-hours annually, equivalent to the output of 92 1-gigawatt power plants. This efficiency target is spurring increased chip volume in general lighting retrofit programs. While conventional emitters held a significant market share in 2025, driven by price-sensitive general illumination programs benefiting from utility rebates, the micro LED segment is on the rise. This growth is carving out a premium niche in automotive adaptive headlamps and near-eye augmented reality displays. Section 179D tax deductions, offering up to USD 5.36 per square foot, are enhancing project returns for warehouse and industrial retrofits. This boost is driving demand for high-bay fixtures, especially those exceeding 130 lumens per watt. Concurrently, automakers are shifting towards adaptive driving beams, utilizing tens of thousands of addressable pixels per vehicle. This transition is driving demand for GaN and AlGaInP, prompting manufacturers to adopt vertical GaN substrates to achieve higher current densities and better thermal management.

Key Report Takeaways

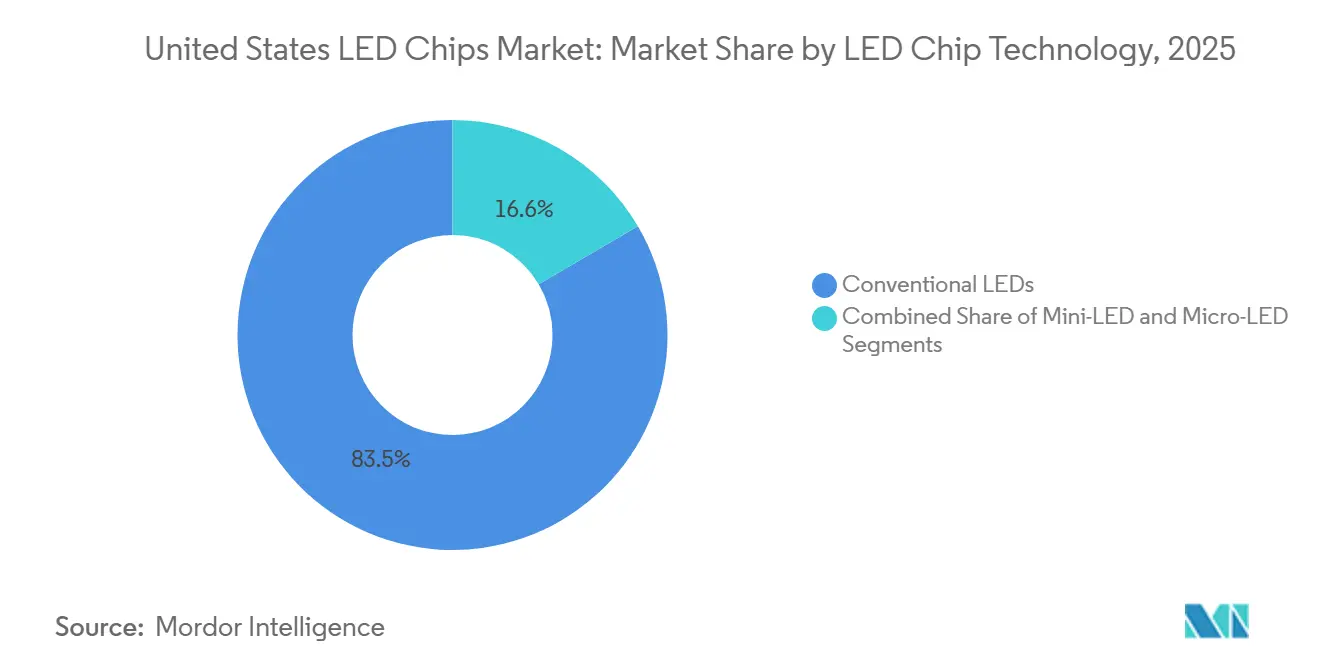

- Conventional LEDs held 83.45% of the United States LED chips market share in 2025, while micro-LED chips are projected to expand at a 11.28% CAGR through 2031.

- Gallium nitride materials held 82.67% of the United States LED chips market in 2025, whereas AlGaInP emitters represent the fastest-growing material group at an 11.78% CAGR over the same horizon.

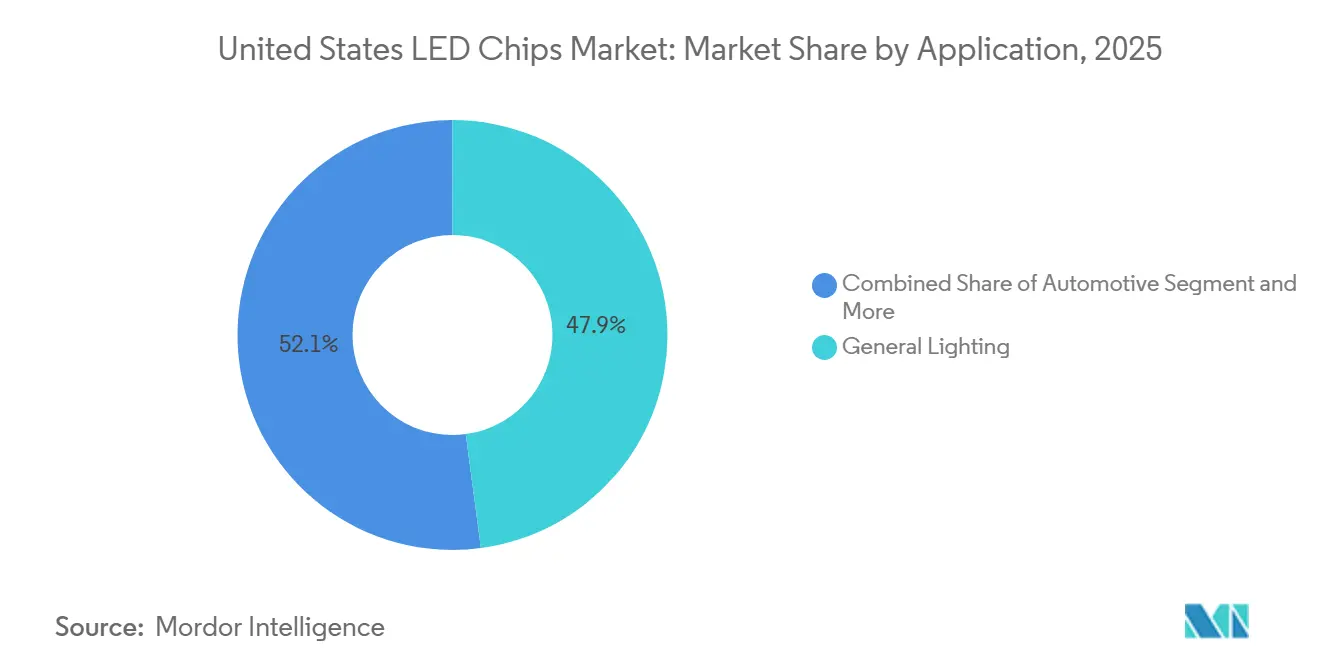

- General lighting accounted for 47.89% of the United States LED chips market in 2025, yet automotive exterior lighting is advancing at a 12.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating Adoption of Mini-LED Backlighting in High-End TVs | +2.1% | National, consumer-electronics hubs in California, Texas, New York | Medium term (2-4 years) |

| Federal and State Energy Efficiency Incentives for Solid-State Lighting | +1.8% | National, strongest in California, New York, Illinois, Texas utility territories | Short term (≤ 2 years) |

| Rapid Decline in Per-Lumen Cost of High-Power GaN Chips | +1.5% | National, benefiting general-lighting and automotive segments | Medium term (2-4 years) |

| Automotive OEM Pivot Toward Exterior LED Pixel Lighting | +1.9% | National, early adoption in premium and electric vehicles | Medium term (2-4 years) |

| Growing Demand for UV-C LED Chips in Disinfection Systems | +0.6% | National, concentrated in healthcare, water treatment, and food processing facilities | Long term (≥ 4 years) |

| Emergence of Smart Farming Requiring Horticultural LED Arrays | +0.4% | Regional, strongest in controlled-environment agriculture states (California, Arizona, Colorado, New York) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Adoption of Mini-LED Backlighting in High-End TVs

Sales momentum accelerated after the 2026 Consumer Electronics Show showcased mainstream 55-inch to 130-inch televisions equipped with thousands of red, green, and blue mini-LED emitters rather than white LEDs with color filters.[1]Consumer Reports, “New TV Technology Coming in 2026,” consumerreports.org Unit shipments for mini-LED TVs surpassed 20 million in 2026, lifting chip density requirements and pressuring domestic suppliers to tighten binning to sub-2-nanometer wavelength windows. Cost reductions of 20-30% logged during 2025 moved the technology from flagship to mid-tier models, widening the total addressable market for GaN emitters with forward-voltage spreads below 0.1 volts. In the United States LED chip market, the cumulative effect is a multi-year uplift, as television, monitor, and gaming hardware brands require higher volumes of tight-pitch chips. RGB mini-LED configurations eliminate quantum-dot layers in several designs, thereby capturing more of the system’s value into the chip bill of materials. Domestic fabs that can guarantee high luminous-flux uniformity across wafer lots are therefore well positioned to win new display contracts.

Federal and State Energy Efficiency Incentives for Solid-State Lighting

Rebate programs covered a significant share of the United States' commercial floor space in 2026, and average prescriptive incentives rose across outdoor categories. Section 179D deductions deliver up to USD 5.36 per square foot, effectively shaving payback periods to below two years for high-efficacy luminaire retrofits in warehouses and cold-storage facilities.[2]Fanxstar, “2026 Guide to Government Rebates for LED Upgrades in the US,” fanxstar.com Utilities are migrating from flat-per-unit rebates to energy-savings performance models, favoring LED chips that help fixtures exceed 130 lumens per watt and qualify for DesignLights Consortium Premium listings. Oregon’s 2025 fluorescent-lamp ban, followed by Hawaii's 2026 ban, further compresses legacy-lamp incentives and channels funding toward LED-to-LED upgrades with networked controls. These measures ensure that the United States LED chip market continues to absorb high volumes for troffer, outdoor, and high-bay fixtures over the next 24 months.

Rapid Decline in Per-Lumen Cost of High-Power GaN Chips

Vertical GaN architecture on bulk GaN substrates unlocks higher current densities, enabling single dies to deliver greater luminous flux and simplifying optics for high-bay and outdoor luminaires.[3]LightNOW, “Vertical GaN Technology May Bifurcate the LED Industry,” lightnowblog.comonsemi’s 2025 debut of vertical GaN power devices, coupled with its memorandum of understanding with Innoscience on 200 mm GaN-on-silicon production, signals an ecosystem shift to larger wafers for both power and lighting chips. Larger wafer platforms drive down the cost per lumen, allowing fixture makers to reduce component counts or add redundancy to meet automotive safety standards. As per-lumen costs ease, the United States LED chip market experiences margin pressure on mature general lighting products but gains upside in premium segments, where smaller, brighter dies enable thinner bezels, lighter fixtures, and advanced optical features.

Automotive OEM Pivot Toward Exterior LED Pixel Lighting

Adaptive driving beam headlights such as Opel’s Intelli-Lux HD, packing 51,200 pixels, illustrate how chip counts per vehicle can jump by orders of magnitude. Ennostar’s April 2026 platform launch highlights chip-on-board arrays with sub-1-mm pixel pitch and 60-µm Slim Core LEDs for ground-projection graphics, expanding the opportunity set for U.S. chipmakers capable of achieving Automotive Electronics Council Q101 reliability ratings.[4]Ennostar, “Pixelated Automotive LED Lighting Platform,” ledinside.com Electric-vehicle brands are early adopters, integrating lighting animations for charging status and vehicle-to-everything communication. The surge drives demand for specialized GaN and AlGaInP for forward, rear, and signature lighting modules, reinforcing the strategic importance of domestic capacity as automakers pursue localized sourcing to comply with Inflation Reduction Act content requirements.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Bottlenecks in Silicon Carbide Substrates | -1.2% | National, automotive and industrial LED segments | Medium term (2-4 years) |

| High Capital Expenditure for Micro-LED Mass Transfer Equipment | -1.6% | National, advanced display and micro-display fabs | Medium term (2-4 years) |

| Intellectual Property Litigation Risk Among Chipmakers | -0.5% | National, affecting cross-border trade and supplier selection | Short term (≤ 2 years) |

| Thermal Management Challenges Limiting Chip Miniaturization | -0.4% | National, impacting high-power and micro-LED applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Bottlenecks in Silicon Carbide Substrates

Silicon-carbide crystal growth remains energy intensive, and the move to 200 mm wafers confronts yield losses that erode effective capacity. [5]HIITIO Semiconductor, “Global Supply Chain Challenges for SiC Components in 2026,” hiitiosemi.com Competition from power-device makers siphons wafer allocations, as electric-vehicle inverters command higher margins than LED epitaxy. Import restrictions on specialty gases and seed crystals, together with regional industrial-policy frictions, add volatility to lead times for AEC-Q101-qualified parts. U.S. chipmakers hedge risk through multi-year wafer offtake agreements and co-development projects aimed at improving crystalline quality, yet smaller entrants lack negotiating leverage and face allocation rationing. Resulting supply tension trims growth potential for high-reliability automotive and industrial LEDs within the United States LED chips market.

High Capital Expenditure for Micro-LED Mass Transfer Equipment

Industry-standard micro-LED transfer yields of 99.9999% require excimer-laser or spatial-light-modulator platforms that each exceed USD 30 million per line and demand micron-level cleanroom conditions. U.S. tariffs imposed in early 2025 on precision photonics equipment added cost and spurred suppliers to shift assembly offshore or to domestic partners, extending procurement cycles and total installed-cost profiles. These economics delay new entrants and push established display makers to secure exclusivity agreements with equipment vendors, constraining the broader diffusion of micro-LED technology. Until fully automated, high-throughput lines reach commercial maturity, the capital barrier will cap short-term market penetration rates, tempering micro-LED’s contribution to the United States LED chips market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Conventional LEDs Anchor Volume, Micro-LED Drives Premium Growth

Conventional emitters retained 83.45% of the United States LED chip market share in 2025, reflecting dominance in troffers, streetlights, and retrofit lamps. In parallel, mini-LED and micro-LED architectures expanded at an 11.28% CAGR, unlocking premium price points in television backlighting, adaptive headlights, and near-eye AR microdisplays. Vertical GaN is emerging as a bridge technology, doubling current handling per die, enabling fixture downsizing, and enhancing thermal performance in high-power modules.

The influx of RGB mini-LED backlights, each television integrating up to 30,000 dies, markedly boosts chip dollar-content even as per-lumen prices fall, effectively counterbalancing commoditization in general lighting. For micro-LEDs, mass-transfer hurdles remain, but pilot programs in defense avionics and premium wearables are validating reliability metrics. Domestic suppliers that combine wafer-level binning with proprietary quantum-dot-free color conversion are positioned to capture early design wins. Collectively, the coexistence of high-volume conventional LEDs and fast-growing micro-LED nodes diversifies revenue streams and insulates the United States LED chips market against single-segment cyclicality.

By Semiconductor Material: GaN Dominance Meets AlGaInP Specialization

GaN and InGaN devices commanded 82.67% of the United States LED chip market in 2025 and remain foundational for white, blue, and green emissions. Continuous advances in epitaxy, including semi-polar orientations and indium-rich quantum wells, push external quantum efficiency above 80% for premium products. AlGaInP emitters logged an 11.78% CAGR, driven by automotive rear lamps, variable-message signs, and horticultural fixtures tuned to photosynthetically active radiation.

Emerging UV-C GaN chips target hospital sterilization and municipal water treatment, with lifetimes projected beyond 20,000 hours at 265 nm. On the red side, distributed-Bragg-reflector thin-film AlGaInP LEDs exceed 50% external quantum efficiency, aligning with the controlled-environment agriculture demand for deep-red bloom lighting. Strategic material diversification, therefore, reinforces supply assurance and broadens application reach across the United States LED chips market.

By Application: General Lighting Leads, Automotive Accelerates

General-lighting deployments still accounted for 47.89% of the United States' LED chip market share in 2025, buttressed by rebate-driven retrofits in offices, warehouses, and streetlights. However, automotive lighting carries the growth baton at a 12.21% CAGR for 2026-2031, thanks to pixelated headlights, dynamic turn indicators, and interior ambient modules.

Backlighting and display applications also leverage high-density mini-LED matrices, and augmented-reality microdisplays are beginning to book engineering-sample volumes. Specialty niches, including UV-C disinfection and horticulture, deliver outsized profit margins despite lower unit demand. The widening application mosaic secures diversified end-market exposure for participants in the United States LED chips market.

Geography Analysis

California, New York, Illinois, and Texas collectively account for over half of rebate-driven retrofit activity, spurred by stringent building-energy codes and utility performance incentives. Title 24 enforcement in California and New York City’s 2025 lighting-upgrade mandate catalyzed immediate procurement waves, while ComEd’s performance-based rebates in Illinois encourage troffer installations. High population density, coupled with early adoption cultures, ensures continued retrofit throughput, anchoring conventional LED run-rate demand in the United States LED chips market.

Automotive chip demand clusters along the Midwest, Michigan, and Ohio, and into Southern states such as Tennessee, Alabama, and South Carolina, where OEMs and tier-one suppliers assemble vehicles fitted with adaptive-beam headlamps. Wolfspeed’s financing enables a North Carolina wafer facility aiming to localize silicon-carbide substrate supply for automotive-grade LEDs, dovetailing with federal CHIPS Act incentives. That regional alignment shortens logistical loops for vehicle programs that increasingly specify domestic content.

The Pacific Northwest and Northeastern technology corridors are spearheading micro-LED R&D as universities and defense contractors pursue high-pixel-density wearable displays. Kopin’s Department of Defense microdisplay contract anchors a Massachusetts pilot line, while West Coast fabless startups partner with Oregon foundries for RGB vertical integration. Controlled-environment agriculture in Arizona and Colorado rounds out geographic demand by placing steady orders for red-blue arrays optimized for high-yield vertical farming. Together, these regional engines sustain a balanced growth pattern across the United States LED chips market.

Competitive Landscape

Top-tier suppliers ams-OSRAM, Nichia, Samsung Electronics, LG Innotek, and Lumileds held significant market share in 2025, leveraging vertically integrated epitaxy, packaging, and phosphor processes to secure automotive and display programs. San’an Optoelectronics’ planned acquisition of Lumileds will bring a Chinese wafer player into the U.S. automotive supply chain, potentially heightening price competition even as regulatory reviews weigh the national security implications.

Intellectual-property enforcement remains pivotal. ams-OSRAM and Nichia renewed their cross-license in 2025 to encompass matrix headlamps, fortifying barriers to entry for emerging rivals. Conversely, Everlight’s 2026 lawsuit against Seoul Semiconductor underscores the litigious environment surrounding flip-chip packages, signaling that legal costs are a fixture for any aspirant seeking to capture high-value automotive sockets.

Technology roadmaps highlight vertical GaN substrates, micro-LED mass-transfer breakthroughs, and UV-C disinfection lines. Q-Pixel claims high transfer yields on 10-µm dies, an innovation that, if scaled, could reshape the premium display segment. Wolfspeed’s silicon-carbide specialty programs aim at high-temperature off-road lighting, while onsemi targets 200 mm GaN-on-silicon economies. Such differentiated bets diversify revenue streams and help incumbent players defend share within the United States LED chips market.

United States LED Chips Industry Leaders

Samsung Electronics Co., Ltd.

ams-OSRAM AG

Lumileds Holding B.V.

Nichia Corporation

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ennostar unveiled its Pixelated Automotive LED Lighting Platform with 60-µm Slim Core LEDs for adaptive driving beams, targeting tier-one suppliers.

- March 2026: Coherent Corp. showcased 400-mW indium-phosphide lasers for co-packaged optics while ramping 6-inch InP wafer output at its Sherman, Texas, fab.

- February 2026: Everlight Electronics filed a patent-infringement suit against Seoul Semiconductor in Texas over flip-chip packaging processes.

- January 2026: RGB mini-LED televisions dominated CES 2026, with shipments projected above 20 million units amid 10,000-nit peak-brightness claims.

United States LED Chips Market Report Scope

The United States LED Chips Market Report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, AlGaInP, and Other Semiconductor Materials), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| By LED Chip Technology | Conventional LEDs |

| Mini-LED | |

| Micro-LED | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| Other Semiconductor Materials | |

| By Application | General Lighting |

| Automotive | |

| Backlighting / Displays | |

| Consumer Electronics | |

| Industrial / Specialty Lighting |

Key Questions Answered in the Report

How fast is the United States LED chips market expected to grow between 2026-2031?

It is forecast to expand at an 8.32% CAGR, rising from USD 7.17 billion in 2026 to USD 10.69 billion by 2031.

Which technology currently dominates U.S. LED chip shipments?

Conventional GaN-on-sapphire LEDs held 83.45% of the market share in 2025, driven by high-volume general lighting retrofits.

What is the most attractive high-growth application for chip suppliers?

Automotive exterior lighting is growing fastest at a 12.21% CAGR, thanks to pixelated adaptive headlamps that dramatically increase chip count per vehicle.

How do federal incentives influence chip demand?

Section 179D tax deductions and widespread utility rebates shorten payback periods, sustaining high retrofit volumes that absorb billions of conventional LEDs annually.

What material system is gaining traction beyond GaN?

AlGaInP chips are expanding at an 11.78% CAGR, supported by automotive rear lamps and horticultural lighting that require red-amber wavelengths.

Which region offers the largest rebate-driven opportunity?

California’s stringent Title 24 rules, coupled with robust utility programs, make it the single largest state market for high-efficacy LED retrofits.

Page last updated on: