LED Module Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

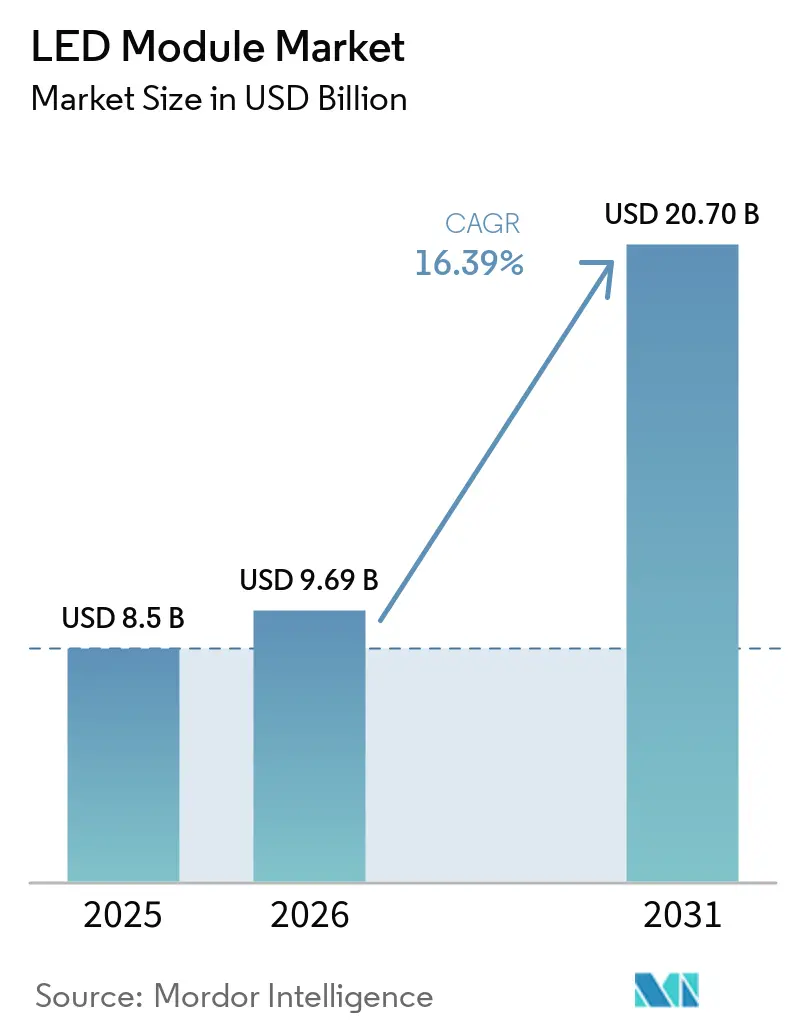

| Market Size (2026) | USD 9.69 Billion |

| Market Size (2031) | USD 20.70 Billion |

| Growth Rate (2026 - 2031) | 16.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LED Module Market Analysis by Mordor Intelligence

The LED module market size was USD 8.50 billion in 2025 and USD 9.69 billion in 2026, and is expected to reach USD 20.70 billion by 2031, growing at a CAGR of 16.39% over 2026-2031. Mounting energy-efficiency mandates, the migration to smart-lighting architectures, and rising demand for adaptive automotive headlamps are accelerating the replacement of legacy sources with solid-state platforms. Component miniaturization has enabled pixel-level control, while on-board driver ICs are shrinking system bill-of-materials and broadening use cases from horticulture to UV disinfection. Competitive intensity is tightening as vertically integrated Asian vendors leverage scale to defend price leadership, yet specialty niches such as UV-C and flexible modules preserve margin headroom. Governments worldwide are tightening minimum-efficacy thresholds, compressing the conversion window, and creating a multi-year retrofit pipeline.

Key Report Takeaways

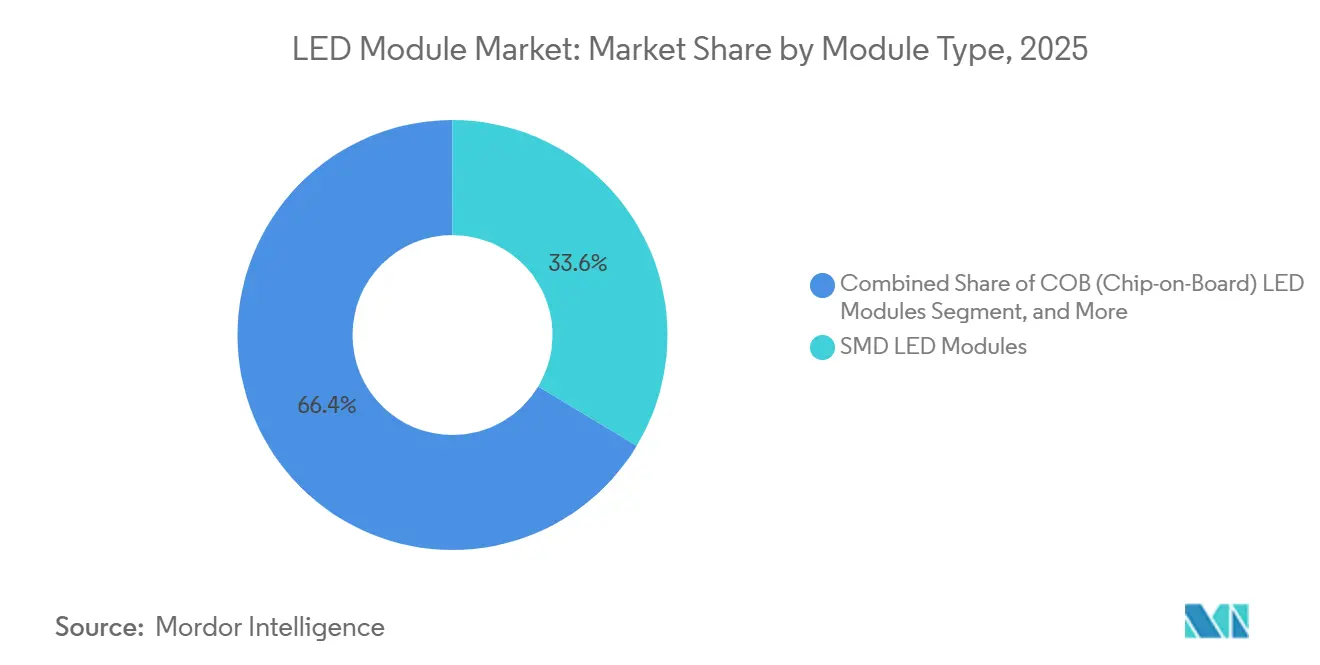

- By module type, SMD modules led the LED module market with a 33.61% revenue share in 2025, while backlight modules are projected to expand at a 16.81% CAGR through 2031.

- By application, general lighting accounted for 42.59% of demand in 2025, whereas display and backlighting segments are expected to advance at a 16.98% CAGR to 2031.

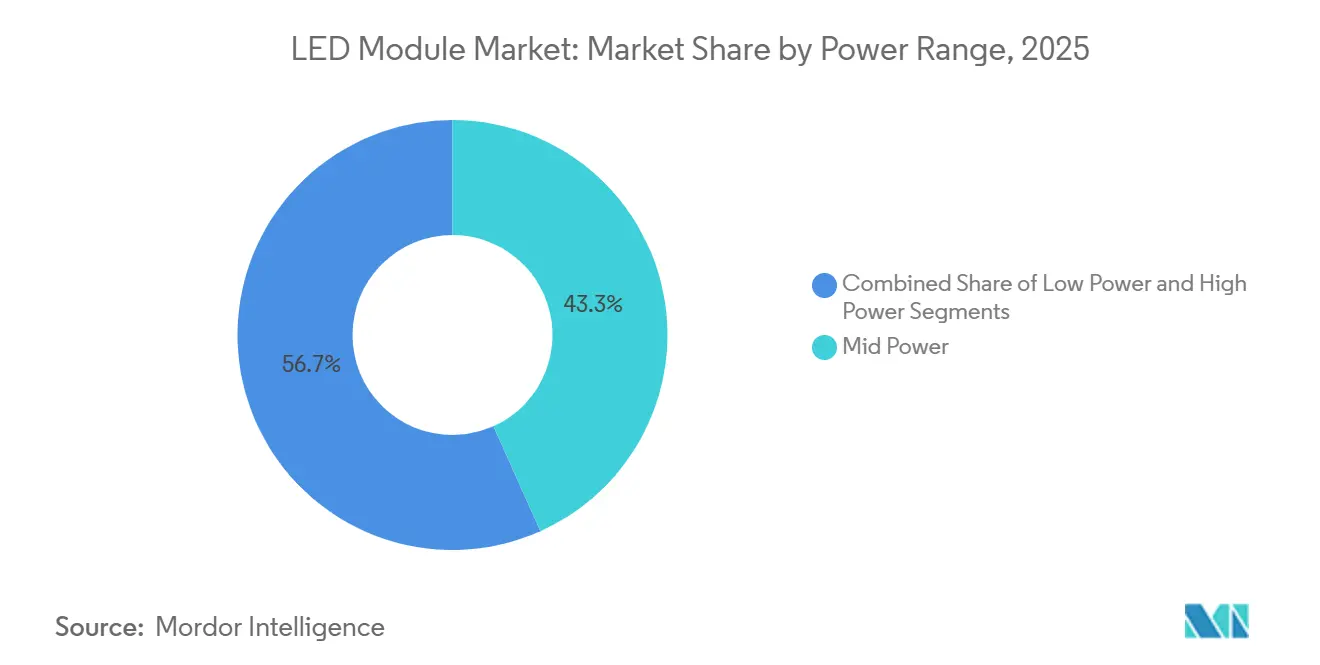

- By power range, mid-power modules captured 43.29% share of the LED module market in 2025, and high-power modules are forecast to grow at a 16.78% CAGR over 2026-2031.

- By form factor, rigid modules held 82.49% of the volume share in 2025, whereas flexible modules are anticipated to grow at a 16.91% CAGR during the same period.

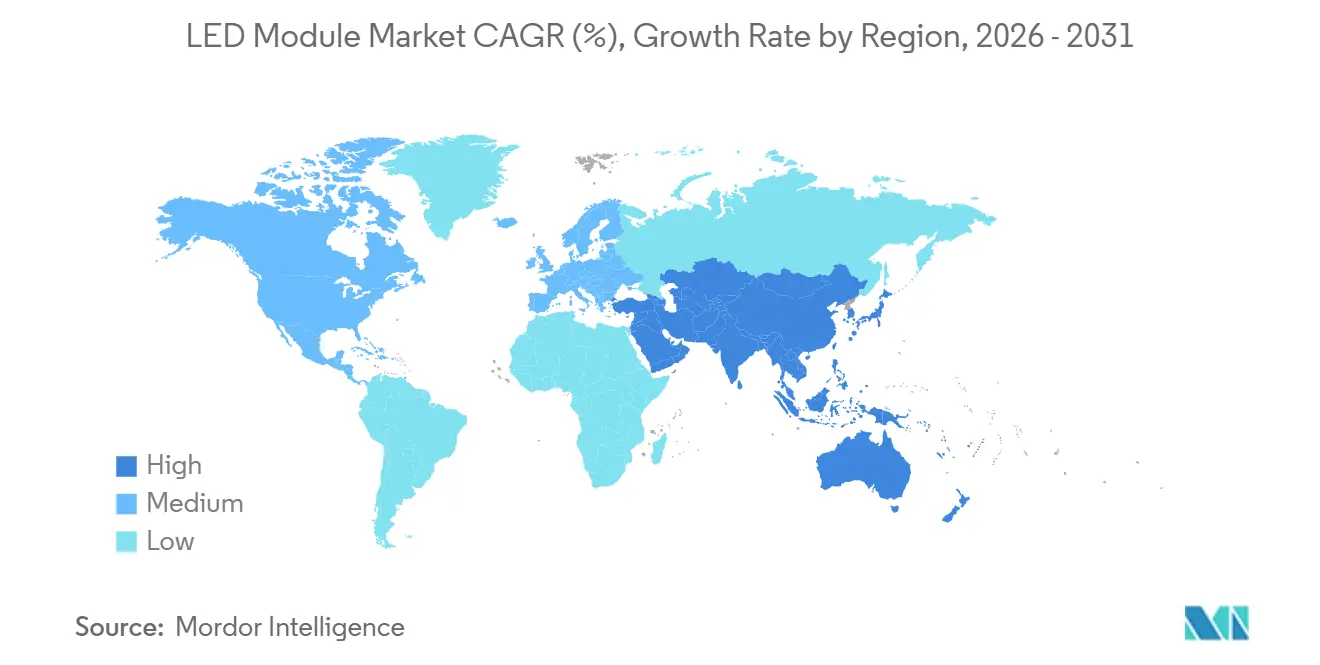

- By geography, Asia-Pacific accounted for 67.73% of the LED module market revenue in 2025 and is projected to register a 17.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LED Module Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid LED Penetration in Residential and Commercial Retrofits | +3.8% | Global, with accelerated uptake in North America and Europe | Medium term (2-4 years) |

| Smart-Lighting Integration with IoT-Enabled Building Systems | +3.2% | North America and Europe core, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Government-Mandated Phase-Out of Inefficient Light Sources | +2.9% | Global, led by EU, United States, and China regulatory timelines | Short term (≤ 2 years) |

| Automotive OEM Shift to LED Headlamps and Interior Modules | +2.5% | Europe and Asia-Pacific, with North America following | Medium term (2-4 years) |

| Miniaturised and Flexible Modules Enabling New Form-Factors | +2.1% | Asia-Pacific manufacturing hubs, global consumer-electronics demand | Long term (≥ 4 years) |

| On-Board Driver IC Adoption Reducing System BOM Cost | +1.8% | Global, with early adoption in premium automotive and commercial lighting | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart-Lighting Integration With IoT-Enabled Building Systems

Commercial construction increasingly embeds networked lighting that treats every LED module as an intelligent edge device collecting occupancy, daylight, and health telemetry. In 2025, sixty percent of new floor space commissioned in North America and Europe funded wireless gateways, sensor arrays, and cloud subscriptions worth more than USD 550 000 per site.[3]California Energy Commission, “Title 24 2025 Update,” energy.ca.gov Measured savings of 30 to 40 percent on electricity and maintenance deliver sub-three-year paybacks, satisfying CFO hurdle rates. The new Matter protocol unifies Zigbee, Thread, and proprietary meshes, slashing commissioning time and calls. Predictive analytics schedule replacements before outages, lifting tenant satisfaction and landlord valuation premiums.

Government-Mandated Phase-Out of Inefficient Light Sources

Legislators on three continents are compressing compliance timelines, converting what was a voluntary efficiency upgrade into a statutory requirement. The European Union banned most halogen stock-keeping units in 2021 and heightened customs enforcement in 2024, blocking non-compliant imports at ports. California’s 2025 Title 24 revision stipulates that 90 percent of installed lighting power in new commercial buildings must originate from LED sources equipped with occupancy sensors and daylight harvesting. China’s 2024 roadmap demands public infrastructure luminaires exceeding 130 lumens per watt by 2026. These synchronized decrees guarantee sustained demand for modular LED retrofit kits and integrated ceiling panels.

Automotive OEM Shift to LED Headlamps and Interior Modules

Automakers are re-positioning LEDs from cost-down enablers to safety and branding features. Audi’s 2025 Q3 platform deploys a ZKW-supplied micro-LED headlamp containing 25,600 addressable pixels that cast navigation symbols onto pavement.[4]ZKW Group, “Audi Q3 Digital Light Module,” zkw-group.comVehicle manufacturers now treat light as data, integrating micro LED arrays with cameras and processors to sculpt beams pixel by pixel. Adaptive driving systems dim specific regions to protect oncoming traffic while projecting symbols that guide drivers through construction zones, snow, or fog. Euro NCAP’s 2025 protocol awards bonus safety points for these functions, driving penetration beyond luxury nameplates into mid-tier sport utility vehicles. Interior cabins follow suit, using programmable strips to synchronize warning alerts with advanced driver assistance systems and ambient wellness modes. Together, exterior and interior innovations raise module value per car and attract semiconductor-level suppliers.

Rapid LED Penetration in Residential and Commercial Retrofits

Falling payback periods made LED retrofits the default option for building operators as energy tariffs rise and carbon rules tighten. The 2024 ballast ban in the United States removed fluorescent replacements, forcing wholesale luminaire changeouts.[1]U.S. Department of Energy, “Fluorescent Lamp Ballast Phase-Out,” energy.govIn Europe, minimum efficacy thresholds of 120 lumens per watt eliminate halogen and compact fluorescent lamps, pushing demand for modular LED kits that drop into existing troffers without rewiring. Asian municipal programs finance millions of street lights, turning LEDs into a grid relief tool. Together, these factors accelerate unit shipments, stabilize factory utilization, and create predictable replacement cycles that extend through the forecast horizon. European directives add momentum; the revised Ecodesign framework sets a 120-lumens-per-watt floor for directional lamps by July 2028, disqualifying halogen and compact fluorescents. Municipal programs in emerging Asia amplify volume, exemplified by the Asian Development Bank’s USD 200 million loan to finance 10 million LED street-lights across India by 2027.[2]Asian Development Bank, “India Municipal Energy-Efficient Lighting Project,” adb.orgResidential adoption is bifurcated between cost-oriented screw-base bulbs and premium renovations that specify tunable-white modules with wireless mesh control. Combined, these factors inject a steady retrofit cadence that underpins the LED module market well beyond the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-Erosion and Margin Pressure Owing to Excess Capacity | -2.3% | Global, concentrated in Asia-Pacific manufacturing base | Short term (≤ 2 years) |

| Thermal Management Challenges in High-Power Modules | -1.6% | Global, acute in industrial and horticulture applications | Medium term (2-4 years) |

| Semiconductor Supply-Chain Volatility for Key Epitaxy Wafers | -1.2% | Global, with Asia-Pacific and North America most exposed | Short term (≤ 2 years) |

| Absence of Universal Module-Level Safety Standards | -0.9% | Global, regulatory divergence between EU, North America, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Thermal Management Challenges in High-Power Modules

High-power modules operating above 30 watts struggle to shed the heat generated by tightly packed emitters, and junction temperatures that drift beyond 125 °C can cut luminous output in half within a few thousand hours. Meeting new IEC 62031:2026 thermal resistance reporting rules forces suppliers to invest in infrared imaging, finite element simulation, and more expensive metal core or ceramic substrates. Passive heat sinks add weight and volume, while active fans raise noise and reliability worries. Horticulture and industrial luminaires feel the impact first because ambient temperatures already sit high, amplifying warranty claims and deterring aggressive overdrive strategies among buyers.

Price-Erosion and Margin Pressure Owing to Excess Capacity

Persistent oversupply in Asia Pacific fabrication plants has pushed LED chip selling prices downward by 10 to 15 percentage points every year since 2020, compressing gross margins for commodity vendors to single digits. Many smaller firms lacked the capital to weather the slide, leading to more than 50 Chinese exits between 2019 and 2022 and a wave of distressed asset sales. Module assemblers face a cost squeeze when wafer contracts decline more slowly than downstream bids, forcing constant redesign to lower the bill of materials. Vertical integration offers a partial buffer, yet pricing pressure remains the dominant brake on profitability and long-term investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: Backlight Modules Lead Growth Trajectory

LED backlight modules are advancing at a 16.81% CAGR from 2026-2031, significantly outpacing overall LED module market growth as Mini-LED technology scales into premium televisions and monitors. SMD modules retained 33.61% of the LED module market share in 2025, buoyed by strong cost-performance in residential and commercial luminaires. Backlight designs tap thousands of Mini-LEDs to achieve greater-than 1,000 local-dimming zones, pushing demand for thin, thermally efficient boards. Meanwhile, chip-on-board (COB) architectures win in automotive headlamps where compact footprints meet 10,000-lumen targets without enlarging reflector housings. Linear modules continue to dominate office troffer retrofits because contractors can replace fluorescent lamps without rewiring, preserving tight project timelines.

The LED module market benefits from new specialty niches: flexible strips illuminate curved signage, and UV-C modules expand into healthcare. COB’s monolithic die reduces thermal resistance and elevates color rendering above 90, fitting museum and retail needs. Cree LED’s L2 PCBA platform packages this benefit with integrated drivers, thereby trimming luminaire OEM design cycles. As automation lowers Mini-LED cost, backlight modules will progressively steal share from SMD in high-brightness displays, reinforcing a mixed portfolio strategy for suppliers.

By Application: Display and Backlighting Outpaces General Lighting

General lighting represented 42.59% of the LED module market size in 2025, yet is ceding relative momentum to display and backlighting, forecast to climb at a 16.98% CAGR through 2031. Direct-lit TV and gaming-monitor refresh cycles fuel replacement demand, while HDR-ready panels push local-dimming counts upward, inflating module content per screen. Commercial lighting still absorbs the largest module volume via office, retail, and hospitality retrofits, but energy regulations are flattening growth relative to screen-based segments.

Automotive exterior lighting, especially adaptive headlamps, commands premium pricing due to rigorous photometric testing. Signage and outdoor advertising install high-brightness modules rated above 5,000 nits and protected to IP65, sustaining demand from smart-city projects. Horticulture and UV-C disinfection form high-margin verticals where spectral tuning or germicidal wavelengths offset lower shipment volumes. Each niche enlarges the addressable LED module market even as the bulb segment matures.

By Power Range: High-Power Modules Gain Industrial Traction

Mid-power devices exceeding 5 W but below 30 W captured 43.29% of the LED module market share in 2025, anchoring commercial retrofits focused on lumen-per-dollar efficiency. High-power modules above 30 W are on track for a 16.78% CAGR over 2026-2031, propelled by warehouse high-bay conversions and sports-field lighting that demand 20,000-lumen outputs.

Advanced metal-core PCBs dissipate heat fast enough to keep junctions below 85 °C even at 50 W, allowing suppliers to push efficacy past 150 lm/W. Industrial buyers substitute 400-W metal-halide fixtures with 150-W LED equivalents, trimming energy by 60% and securing quick payback. Low-power modules, under 5 W, fulfill accent and emergency-exit niches where battery operation or tight spaces prevail. Scaling flexibility, where identical arrays are paralleled to reach new wattages, is simplifying inventories and reinforcing supplier stickiness.

By Form Factor: Flexible Modules Enable Novel Applications

Rigid boards held 82.49% of shipment volume in 2025, yet flexible substrates are expanding at a 16.91% CAGR through 2031. Automotive designers route bendable strips around dashboards and door trims, achieving uniform ambient glows without complex brackets. Curved digital signage leverages flexible modules to shave installation labor by 30% because installers no longer segment rigid PCBs.

Thermal conductivity remains the limiting factor for flexible polyimide, often 40% lower than FR-4, capping continuous power below 10 W per meter. Hybrid designs place rigid high-power LEDs on flexible interconnects, balancing heat spreading with three-dimensional styling freedom. Consumer electronics is the next frontier, with smartwatch builders embedding curved backlights that conform to the wearer’s wrist, delivering differentiation beyond display resolution.

Geography Analysis

Asia-Pacific accounted for 67.73% of the LED module market revenue in 2025 and is projected to post a 17.05% CAGR through 2031. China controls more than 70% of global chip capacity and continues to expand; BOE Huacan’s RMB 2 billion (USD 280 million) wafer plant in Jiangsu will add 500,000 pieces per month, aimed at automotive and Mini-LED backlights BOE.COM. India is emerging as a secondary hub as public-sector street-light tenders scale into the tens of millions of units. Japan retains leadership in UV and micro-LED specialties, leveraging Nichia’s phosphor patents to command price premiums.

North America ranks second by revenue, sustained by regulatory bans on fluorescent ballasts and the accelerating adoption of adaptive LED headlamps. Canada’s rising carbon price moved building owners to allocate 40% of retrofit budgets to lighting upgrades, while Mexican states near the U.S. border expanded module-assembly capacity by 25% during 2025 to serve nearshoring OEMs.

Europe’s strict Ecodesign thresholds guarantee a steady retrofit cadence, with Germany and the United Kingdom spearheading office and municipal conversions. Middle East and Africa markets concentrate on prestige smart-city districts in the United Arab Emirates and Saudi Arabia, whereas South America and Africa see sporadic demand tied to off-grid solar-LED programs. Across all regions, policy pressure and local manufacturing incentives intersect to keep the LED module market on a high-growth trajectory.

Competitive Landscape

The LED module market shows moderate consolidation: the five largest Chinese vendors capture just above half of regional income, yet globally the field remains fragmented. The 2026 completion of San’an Optoelectronics and Inari Amertron’s USD 239 million purchase of Lumileds underscores a pivot toward vertical integration, locking in phosphor and packaging know-how. Patent cross-licensing is replacing litigation as ams OSRAM, and Nichia agreed in October 2025 to share driver-IC and module technologies, speeding time-to-market for automotive and display products.

Cree LED’s February 2026 OptiLamp launch integrates on-board driver ICs, eliminating external converters and trimming system cost by 20%. Specialty verticals yield the highest margins; UV-C disinfection modules combine 265-nm chips with quartz optics to fetch 30-40% gross profit, while horticulture modules differentiate through tunable spectra that boost yields for vertical farms.

Compliance with IEC 62031:2026 has become a competency hurdle, as vendors must now disclose thermal-resistance data and junction-temperature metrics in every data sheet. Suppliers that invest early in simulation and thermal imaging compress validation cycles for OEM customers, winning design-in decisions that translate into multi-year revenue streams. Speedy co-design with luminaire brands, particularly for flexible and micro-LED arrays, is emerging as the decisive competitive lever.

LED Module Industry Leaders

Signify N.V.

ams-OSRAM AG

Samsung Electronics Co., Ltd.

Nichia Corporation

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cree LED launched OptiLamp technology, embedding pixel-level intelligence and on-board driver ICs to cut system BOM by 20% while enabling dynamic CCT tuning for commercial lighting.

- January 2026: Cree LED introduced L2 PCBA chip-on-board solutions with integrated drivers, reducing design cycles from 12 weeks to 4 weeks for retrofit luminaire manufacturers.

- January 2026: San’an Optoelectronics and Inari Amertron completed a USD 239 million acquisition of Lumileds, securing phosphor and packaging IP to target the automotive and premium lighting markets.

- November 2025: BOE Huacan announced a RMB 2 billion (USD 280 million) wafer expansion in Jiangsu to support automotive headlamps and Mini-LED backlights.

Global LED Module Market Report Scope

An LED Module is a pre-assembled, integrated lighting component consisting of one or more light-emitting diodes (LEDs) mounted on a printed circuit board or substrate, along with essential electrical and thermal management elements such as current-limiting circuitry and heat-dissipation structures, designed to operate as a functional light source when incorporated into a luminaire and powered by an appropriate electrical supply.

The Global LED Module Market Report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), Form Factor (Rigid, and Flexible), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| COB (Chip-on-Board) LED Modules |

| SMD LED Modules |

| Linear LED Modules |

| LED Backlight Modules |

| High-Power LED Modules |

| Others, Module Type (Flexible, Mini, Custom Assemblies) |

| General Lighting |

| Residential |

| Commercial |

| Industrial |

| Automotive Lighting |

| Display and Backlighting |

| Signage and Advertising |

| Others, Application (Architectural, Horticulture, UV, Specialty) |

| Low Power (less than or equal to 5 W) |

| Mid Power (greater than 5 W to less than or equal to 30 W) |

| High Power (greater than 30 W) |

| Rigid LED Modules |

| Flexible LED Modules |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East | |

| Africa |

| By Module Type | COB (Chip-on-Board) LED Modules | |

| SMD LED Modules | ||

| Linear LED Modules | ||

| LED Backlight Modules | ||

| High-Power LED Modules | ||

| Others, Module Type (Flexible, Mini, Custom Assemblies) | ||

| By Application | General Lighting | |

| Residential | ||

| Commercial | ||

| Industrial | ||

| Automotive Lighting | ||

| Display and Backlighting | ||

| Signage and Advertising | ||

| Others, Application (Architectural, Horticulture, UV, Specialty) | ||

| By Power Range | Low Power (less than or equal to 5 W) | |

| Mid Power (greater than 5 W to less than or equal to 30 W) | ||

| High Power (greater than 30 W) | ||

| By Form Factor | Rigid LED Modules | |

| Flexible LED Modules | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

What value will LED module demand reach by 2031?

Global sales are projected to climb to USD 20.70 billion by 2031 as solid-state retrofits and Mini-LED backlights accelerate.

Which region leads shipments today?

Asia-Pacific accounts for 67.73% of 2025 revenue and is forecast to grow at a 17.05% CAGR through 2031.

Which segment is growing fastest?

Backlight modules for Mini-LED displays are advancing at a 16.81% CAGR over 2026-2031, outpacing other categories.

Why are high-power modules gaining share?

Industrial high-bay retrofits and sports-field projects demand 20,000-lumen outputs, driving high-power module uptake at a 16.78% CAGR.

Page last updated on: