High-Brightness LED Chip Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.73 Billion |

| Market Size (2031) | USD 38.74 Billion |

| Growth Rate (2026 - 2031) | 8.53% CAGR |

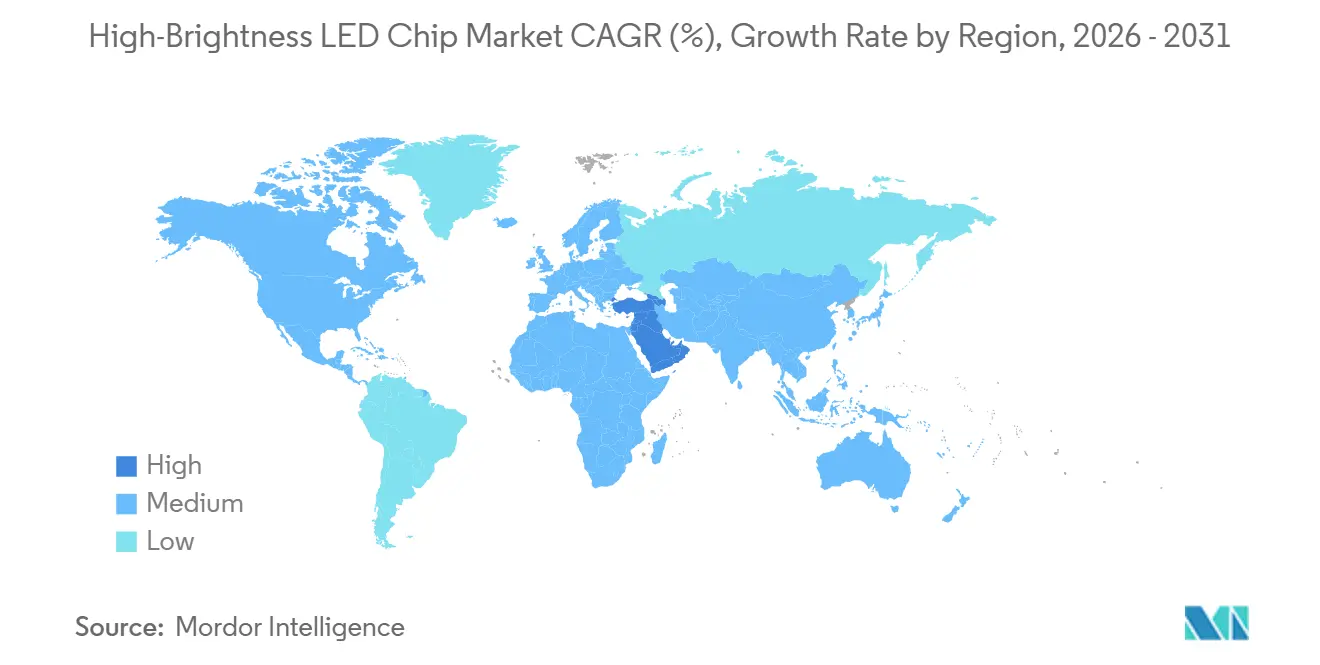

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

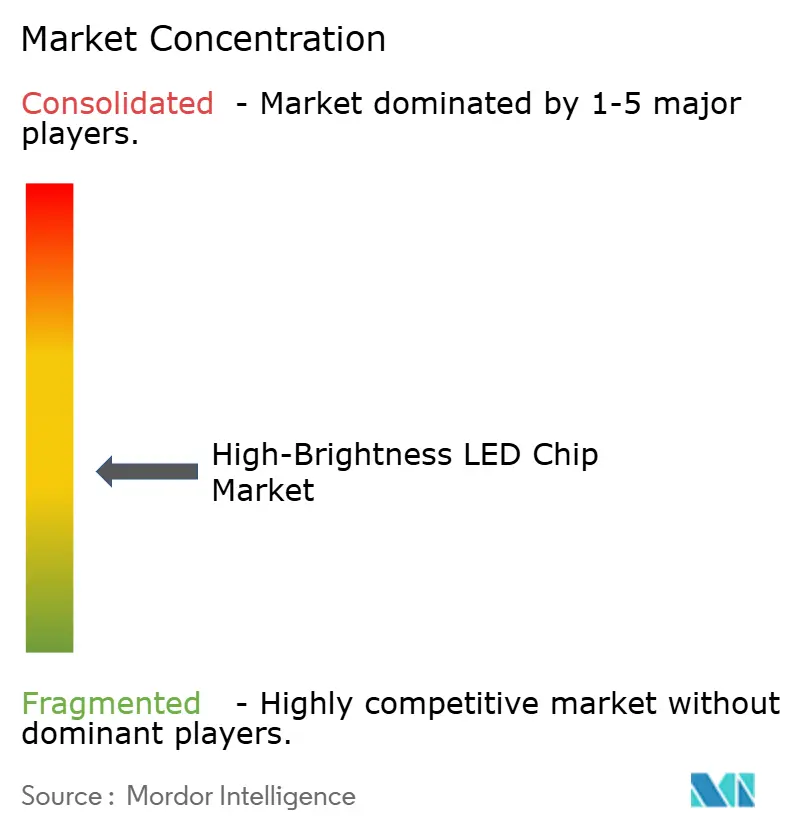

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Brightness LED Chip Market Analysis by Mordor Intelligence

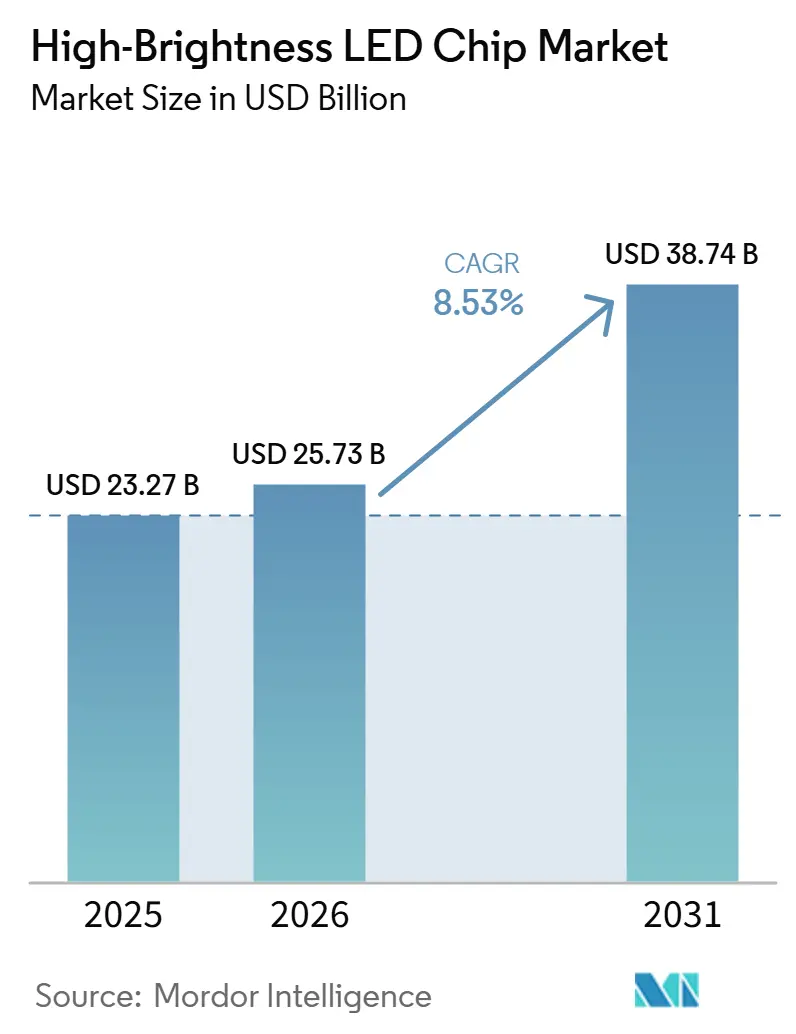

The high-brightness LED chip market size is expected to increase from USD 23.27 billion in 2025 to USD 25.73 billion in 2026 and reach USD 38.74 billion by 2031, growing at a CAGR of 8.53% over 2026-2031. Structural shifts in global lighting policies, swift automotive adoption of full-LED systems, and rapid gains in chip efficacy collectively push the high-brightness LED chip market toward higher value creation. Breakthroughs in gallium nitride (GaN) passivation have already pushed laboratory efficacies beyond 300 lumens per watt, encouraging premium pricing in architectural, medical, and horticultural luminaires. At the same time, on-wafer AI metrology is cutting scrap rates, allowing vendors to defend gross margins even as overcapacity in China drives aggressive price competition. Strategic gallium stockpiling programs in the United States and allied regions further insulate defense and automotive supply chains from raw-material shocks, anchoring long-term demand for domestic production capacity.

Key Report Takeaways

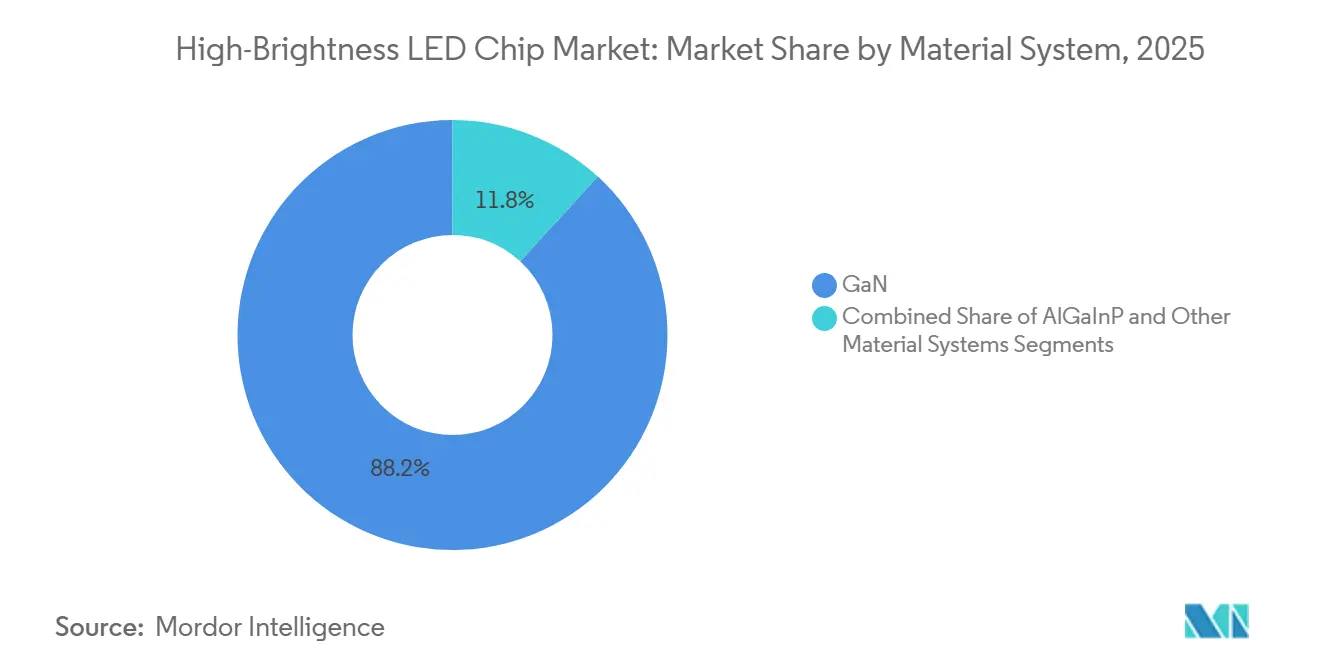

- By material system, GaN led with 88.18% of high-brightness LED chip market share in 2025; it is forecast to expand at a 9.26% CAGR through 2031.

- By wavelength, blue chips captured 54.39% revenue share in 2025, while green devices are projected to advance at a 9.58% CAGR to 2031.

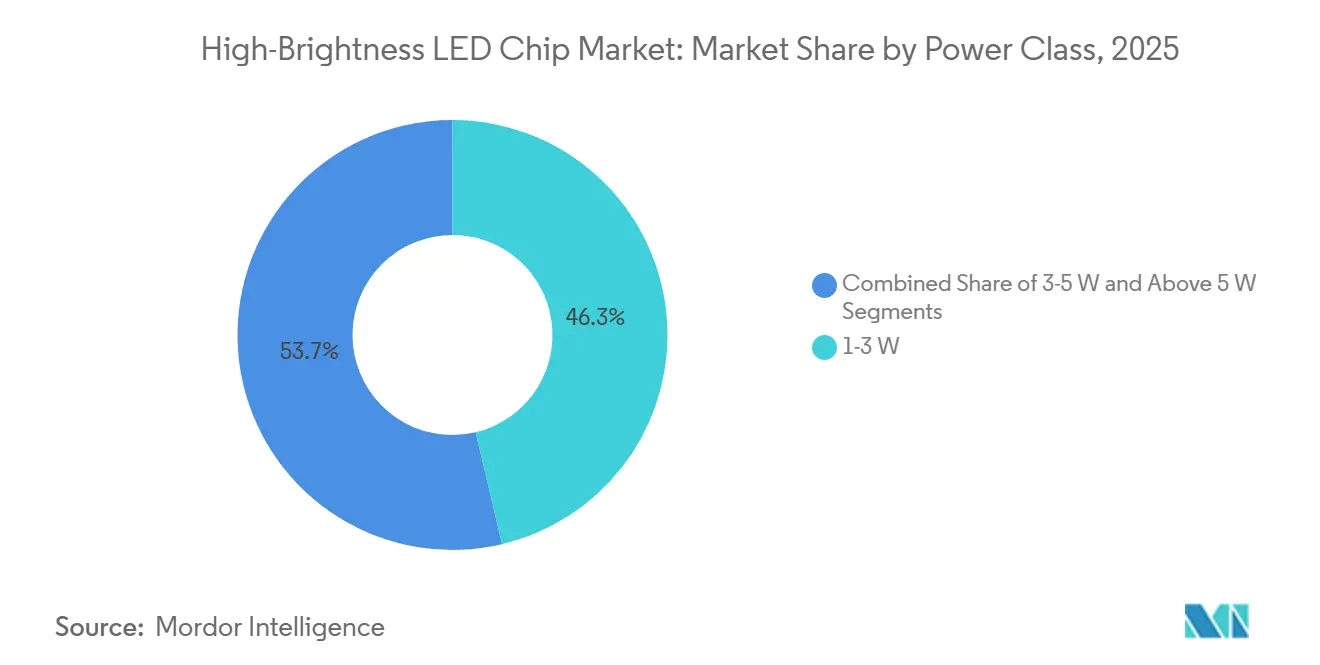

- By power class, 1-3 W devices held 46.29% of the high-brightness LED chip market size in 2025, whereas the above-5 W segment is climbing at a 9.17% CAGR through 2031.

- By application, general lighting represented 39.16% of demand in 2025 and automotive lighting is progressing at an 8.88% CAGR through 2031.

- By geography, Asia-Pacific maintained 62.73% share in 2025 and the Middle East is set to register the highest regional CAGR at 8.96% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-Brightness LED Chip Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Efficiency Regulations Accelerating LED Adoption | +1.8% | Global, with strongest enforcement in European Union and North America | Medium term (2-4 years) |

| Rapid Decline in Cost per Lumen of HBLED Chips | +1.5% | Global, with largest volume gains in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Automotive OEM Shift to Full-LED Exterior and Interior Lighting | +1.3% | Global, led by China, Europe, and North America premium segments | Medium term (2-4 years) |

| Integration of Tachyon Surface Passivation Enabling 300+ lm/W Chips | +0.9% | Japan, South Korea, and select European R&D hubs | Long term (≥ 4 years) |

| On-Wafer AI Metrology Cutting Epi-Wafer Scrap Rates | +0.7% | Asia-Pacific manufacturing clusters, spillover to North America | Short term (≤ 2 years) |

| Strategic Gallium Stockpiling by Defense Agencies | +0.5% | United States, European Union, and allied Pacific nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations Accelerating LED Adoption

Governments worldwide continue to tighten minimum efficacy thresholds, retiring fluorescent and halogen technologies from public procurement catalogs. In the European Union, the Ecodesign for Sustainable Products Regulation, which entered into force in July 2024, compels fixture manufacturers to meet more demanding lumen-per-watt targets, pushing buyers toward premium, high-brightness LED chips. Similar updates to energy-labeling schemes in South Korea and Taiwan during 2024-2025 broadened the addressable market, while U.S. federal buildings reference ISO 50001 audits to favor high-efficacy retrofits. These regulatory catalysts shorten payback periods and accelerate volume ramps in municipal and commercial sectors. As public tenders increasingly bundle lighting projects with performance-based energy contracts, chip makers that can certify sustained lumen maintenance at elevated temperatures unlock premium demand.

Rapid Decline in Cost per Lumen of HBLED Chips

Process-equipment scale, larger wafer diameters, and tighter bin sorting have cut cost-per-lumen metrics by more than 50% since 2015. Chinese fabs, spearheaded by San’an Optoelectronics, expanded microLED capacity six-fold in 2025, driving unit prices down across global channels.[1]China Daily, “San’an Optoelectronics Announces USD 5 Billion Quanzhou LED Base,” chinadaily.com.cn Lower chip costs translate into more affordable luminaires, opening the high-brightness LED chip market to price-sensitive regions in South America and Africa. As module assemblers pass efficiency gains to end users, the total cost of ownership for LED systems slides below that of legacy discharge technologies even at modest burn hours. The resulting volume gain reinforces economies of scale, creating a virtuous cycle of cost erosion and wider adoption.

Automotive OEM Shift to Full-LED Exterior and Interior Lighting

Premium vehicle platforms now integrate adaptive LED arrays that provide pixel-level beam shaping, road-surface projections, and turquoise Level-3 autonomy indicators. BMW’s 2,850-zone Mini LED cockpit, showcased at CES 2025, exemplifies how display suppliers leverage high-brightness chips for immersive dashboards. Chinese automakers such as NIO, Li Auto, and Zeekr accelerated Mini LED adoption in 2025-model vehicles, stimulating domestic fabs to refine automotive-grade binning and traceability practices.[2]TrendForce, “Mini LED Automotive Display Penetration to Reach 6% by 2028,” trendforce.com Strict reliability and color-stability specifications raise average selling prices, enabling the high-brightness LED chip market to expand faster than unit shipments in the automotive channel. As Level-2⁺ and Level-3 autonomy proliferate, signal-lighting requirements will further intensify demand for tightly controlled, high-flux emitters.

Integration of Tachyon Surface Passivation Enabling 300+ lm/W Chips

Nichia’s 325 lm/W GaN prototype, demonstrated in late 2025, validated tachyon surface passivation as a viable pathway to suppress non-radiative recombination at chip perimeters. The method complements patterned sapphire substrates and photonic-crystal layers, lifting extraction efficiency without incurring significant equipment overhauls. As atomic-layer deposition tool suppliers scale throughput and cut precursor costs, mainstream fabs in Japan and South Korea are expected to adopt the process in pilot lines by 2027. Early commercial insertion is likely in surgical headlights and museum lighting, where color rendering and lumen maintenance justify premium prices. Over time, cascading design wins will filter into general lighting, gradually redefining performance benchmarks across the high-brightness LED chip market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Price Erosion from Chinese Overcapacity | -1.2% | Global, with acute margin pressure in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Supply-Chain Disruption Risks for Gallium and Indium | -0.8% | Global, with highest exposure in North America and Europe | Medium term (2-4 years) |

| EU Digital Product Passport Rules Raising Compliance Costs | -0.5% | European Union, with spillover to exporters in Asia-Pacific | Medium term (2-4 years) |

| Blue-Light Hazard Limits on Consumer Luminaire Luminance | -0.3% | Global, with strictest enforcement in European Union and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Erosion from Chinese Overcapacity

China added substantial epitaxial capacity between 2023 and 2025, triggering double-digit price drops that squeezed margins for Japanese, Korean, and European incumbents. San’an’s USD 5 billion Quanzhou expansion, announced in August 2025, illustrates the capital firepower underpinning this supply surge. Low-cost output forces non-Chinese vendors to retreat into specialty niches such as ultraviolet disinfection or to accelerate vertical integration into modules. Persistent oversupply also discourages fresh investment in next-generation reactors outside China, risking technological divergence that could entrench regional supply imbalances. Unless demand growth absorbs excess capacity, profit erosion may curb R&D budgets needed for breakthrough efficiency gains.

Supply-Chain Disruption Risks for Gallium and Indium

Gallium supplies are highly concentrated, with China historically providing more than 90% of refined output. Beijing’s 2023 export-licensing regime exposed the vulnerability of Western LED and RF manufacturers, prompting the U.S. Department of Defense to launch Project Vault stockpiles.[3]Atlantic Council, “Securing Critical Minerals: The Pentagon’s Project Vault Initiative,” atlanticcouncil.org Indium exhibits similar concentration, amplifying risk as microLED and Mini LED demand rises. Shipping-route chokepoints, geopolitical frictions, or pandemic-related mine shutdowns could spike raw-material costs and elongate delivery lead times. While recycling initiatives and secondary extraction from bauxite tailings are under evaluation, scalable mitigation remains years away, keeping material-supply risk on executive dashboards throughout the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material System: GaN Dominance Anchored by Efficiency Gains

Gallium nitride held 88.18% of high-brightness LED chip market share in 2025, a lead sustained by superior thermal stability and multi-wavelength versatility. Recent tachyon passivation advances and photonic-crystal extractions are expected to raise commercial GaN efficacy to 300 lm/W in select luminaires by 2028. AlGaInP continues to serve red and amber functions but faces intrinsic droop above 85 °C junction temperature, limiting penetration in high-heat automotive lamp housings. Emerging materials such as indium phosphide quantum dots remain in laboratory phases, implying that the high-brightness LED chip market will stay predominantly GaN-centric through the forecast period.

Equipment amortization and process maturity further lower GaN unit costs, widening the gap versus competing chemistries. GaN-on-sapphire maintains cost-performance balance for general lighting, while GaN-on-silicon garners interest in price-sensitive bulbs despite slightly lower efficacy. Specialty GaN-on-SiC structures target UV-C disinfection and high-power spotlights where thermal limits are stringent. As material innovation proceeds, vendors will segment their portfolios by substrate and passivation stack to balance performance against bill-of-materials constraints.

By Wavelength and Color: Blue Leads, Green Accelerates

Blue LEDs provided 54.39% of revenue in 2025, reflecting their role as the conversion base for white light in phosphor blends. Meanwhile, green devices are tracking a 9.58% CAGR to 2031 as nanowire geometry and optimized quantum-well thickness mitigate the historic “green gap.” Porotech’s 20% external quantum-efficiency milestone in June 2025 validates the commercial trajectory of green InGaN emitters. Red and amber chips retain essential regulatory roles in automotive signal lighting, even as quantum-dot color converters press into display backlights.

Across consumer electronics, tri-color microLED arrays use discrete red, green, and blue dice, fueling additional demand for high-flux monochromatic chips. Ultraviolet and deep-red horticultural segments remain small in absolute dollars but command premium ASPs, shielding vendors from commodity price swings. Color-mix strategies in automotive interiors and smart-home luminaires will increasingly specify matched efficiency across RGB wavelengths, pressuring green chip advances to stay in sync with blue and red emission performance.

By Power Class: Mid-Power Dominates, High-Power Surges

Devices rated 1-3 W accounted for 46.29% of the high-brightness LED chip market in 2025, balancing flux and thermal performance for downlights and troffers. Yet the above-5 W class is expanding at 9.17% CAGR as horticulture farmers, stadium operators, and adaptive headlamp designers demand higher radiant flux from compact footprints. Fluence Bioengineering fixtures already deliver photosynthetic photon flux densities over 2,000 µmol m-² s-¹ using strings of high-power chips. Vapor-chamber heat sinks and graphene-impregnated substrates keep junction temperatures below 100 °C, preserving lumen maintenance across 50,000-hour duty cycles.

The 3-5 W bracket serves transitional needs such as outdoor area lights and retail track spots, where moderate drive currents strike a cost-to-output balance. As chip architectures shrink pitch while raising amperage thresholds, boundaries between traditional power classes will blur, allowing OEMs to tailor optical and thermal modules with finer granularity.

By Application: General Lighting Largest, Automotive Fastest

General lighting absorbed 39.16% of 2025 demand, thanks to retrofit programs in office, industrial, and municipal buildings. Replacement cycles lengthen as early LED installs enter mid-life, but smart-control upgrades and human-centric lighting schemes sustain baseline volumes. Automotive lighting, registering an 8.88% CAGR, advances fastest on the strength of pixelated headlamps, dynamic signaling, and high-resolution cockpit displays. Mercedes-Benz Digital Light modules incorporate 25,000 micro-LEDs per lamp to project navigational cues, demonstrating the design latitude unlocked by high-brightness dice.

Mini LED backlighting in premium televisions, laptops, and vehicle infotainment panels further diversifies application demand. Outdoor advertising embraces fine-pitch LED walls under 1 mm pixel spacing, battling LCD and OLED with unmatched brightness and durability. Niche usages in medical devices, UV-C germicidal irradiation, and machine-vision inspection command higher ASPs and stringent binning, reinforcing multi-tier pricing across the high-brightness LED chip market.

Geography Analysis

Asia-Pacific retained 62.73% share in 2025, underpinned by China’s vertically integrated clusters that span epitaxy, chip fabrication, and module assembly. San’an Optoelectronics, HC SemiTek, and Nationstar shipped high volumes to both domestic and export customers, leveraging state incentives and proximity to display and lighting OEMs. Japanese and South Korean players, including Nichia and Seoul Semiconductor, specialize in automotive and specialty niches, protecting margins through patents and sustained R&D investment.

The Middle East is the fastest-growing region, with a 8.96% CAGR, propelled by smart-city retrofits aligned with Vision 2030 agendas. Qatar’s Ashghal authority committed in 2024 to convert all public street lights to smart-LED systems by 2027, integrating adaptive dimming and remote diagnostics. Saudi Arabia’s NEOM megaproject specifies premium LED solutions that can withstand desert temperature swings and integrate IoT sensors for asset management.

North America and Europe register slower unit growth as baseline penetration nears saturation, but they remain attractive for high-margin automotive, medical, and architectural segments. The European Union’s Digital Product Passport rules, effective from 2026, impose traceability obligations that favor suppliers with robust ISO 9001 and IATF 16949 systems. South America and Africa offer incremental upside through rural electrification and climate-resilience infrastructure, although exchange-rate volatility and grid limitations temper near-term volumes.

Competitive Landscape

The high-brightness LED chip market shows moderate concentration, with the top five suppliers controlling a sizable slice of premium revenue, while dozens of Chinese firms flood the commodity segments. Nichia’s 325 lm/W laboratory record cements its reputation for materials leadership. Samsung Electronics leverages vertical integration, using captive chips in televisions and smartphone flash modules, while Lumileds’ automotive pedigree now sits within San’an’s expanding Chinese ecosystem after the January 2026 takeover.

Competitive intensity is magnified by Chinese oversupply that compresses general-lighting margins, forcing Japanese, Korean, and European incumbents to double down on specialty niches such as UV-C disinfection and laser-excited phosphor modules. Cree LED’s 2024 rebrand to Wolfspeed LED and pivot toward silicon-carbide power semiconductors illustrates portfolio realignment away from commodity lighting dice. Patent race activity centers on atomic-layer deposition passivation and photonic-crystal extraction, with Nichia, Osram, and Seoul Semiconductor leading granted claims.

Module assemblers negotiate long-term, capacity-guaranteed contracts, compelling chip vendors to invest in AI-enabled inspection systems from KLA and ASML that raise yield and consistency. Compliance burdens, including IEC 62471 blue-light hazard limits and European traceability mandates, further thin the supplier roster by elevating overhead for smaller foundries. The resulting landscape favors scale players capable of funding both process innovations and global regulatory certification.

High-Brightness LED Chip Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd.

Lumileds Holding B.V.

Osram Opto Semiconductors GmbH

Penguin Solutions Inc. (Cree Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: San’an Optoelectronics finalized its USD 239 million acquisition of a 74.5% stake in Lumileds, unlocking automotive IP synergies and capital for expansion.

- December 2025: San’an Optoelectronics expanded microLED capacity from 250 to 1,400 wafers per month to supply Samsung’s display division.

- November 2025: Nichia disclosed a 325 lm/W GaN prototype enabled by tachyon passivation.

- September 2025: Mercedes-Benz secured U.S. regulatory approval for turquoise automated-driving marker lights.

Global High-Brightness LED Chip Market Report Scope

The High-Brightness LED Chip Market refers to the industry focused on the production, development, and application of LED chips with high luminous intensity. These chips are categorized based on material systems, wavelength and color, power class, and their use across various applications such as general lighting, automotive lighting, backlighting, signage and displays, among others.

The High-Brightness LED Chip Market Report is Segmented by Material System (GaN, AlGaInP, and Other Material Systems), Wavelength and Color (Blue, Green, Red, Amber and Yellow, and Other Wavelength and Colors), Power Class (1-3 W, 3-5 W, and Above 5 W), Application (General Lighting, Automotive Lighting, Backlighting, Signage and Displays, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| GaN |

| AlGaInP |

| Other Material Systems |

| Blue |

| Green |

| Red |

| Amber / Yellow |

| Other Wavelength / Colors |

| 1-3 W |

| 3-5 W |

| Above 5 W |

| General Lighting |

| Automotive Lighting |

| Backlighting |

| Signage and Displays |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| ASEAN | |

| Oceania | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| North Africa | |

| Rest of Africa |

| By Material System | GaN | |

| AlGaInP | ||

| Other Material Systems | ||

| By Wavelength / Color | Blue | |

| Green | ||

| Red | ||

| Amber / Yellow | ||

| Other Wavelength / Colors | ||

| By Power Class | 1-3 W | |

| 3-5 W | ||

| Above 5 W | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Backlighting | ||

| Signage and Displays | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Oceania | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| North Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the high-brightness LED chip market by 2031?

The market is forecast to reach USD 38.74 billion by 2031, expanding at an 8.53% CAGR from 2026-2031.

Which material system dominates current high-brightness LED chip production?

Gallium nitride commands 88.18% share and is projected to maintain leadership thanks to superior efficacy and thermal stability.

Why are green LEDs gaining momentum?

Nanowire architectures and optimized quantum-well designs have narrowed the historic efficiency gap, enabling a 9.58% CAGR for green chips through 2031.

Which region offers the fastest growth opportunity?

The Middle East is set to post an 8.96% CAGR as Gulf nations roll out smart-city LED retrofits aligned with Vision 2030 goals.

What is the main supply-chain risk for LED chip makers?

Concentrated gallium and indium production creates vulnerability to export controls and geopolitical disruptions, as highlighted by the U.S. Project Vault initiative.

Page last updated on: