SMD (Surface Mount Device) LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.49 Billion |

| Market Size (2031) | USD 9.05 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

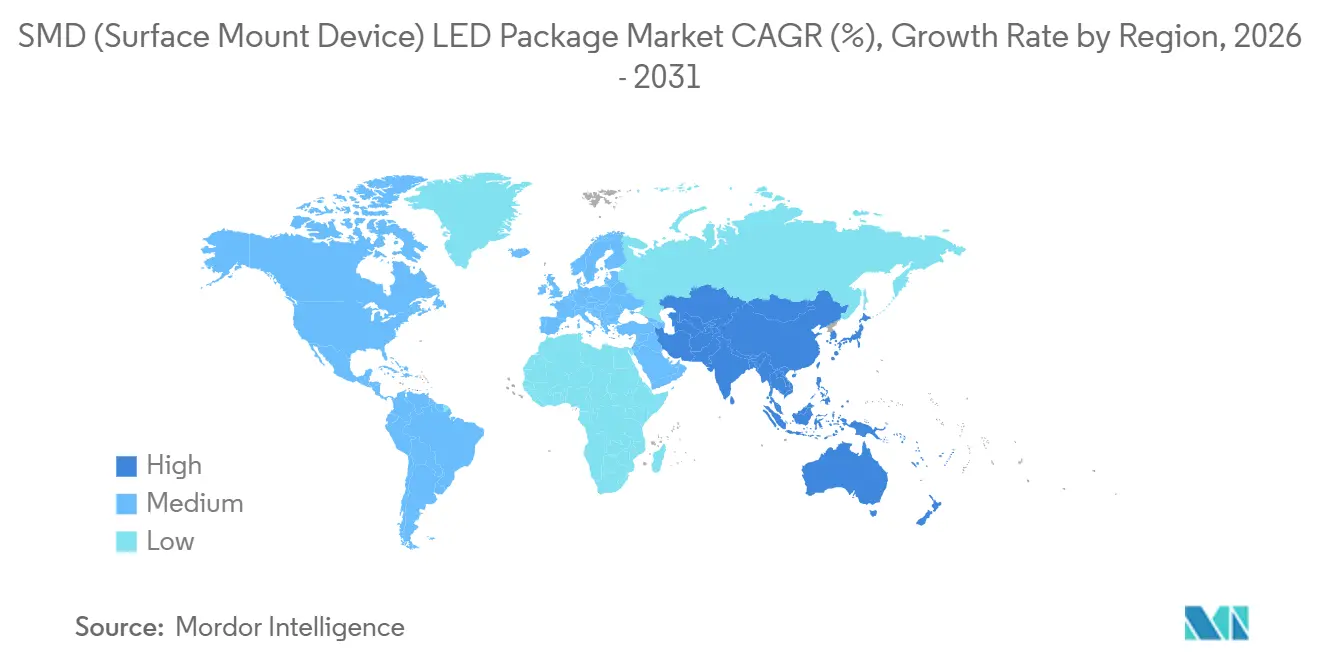

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

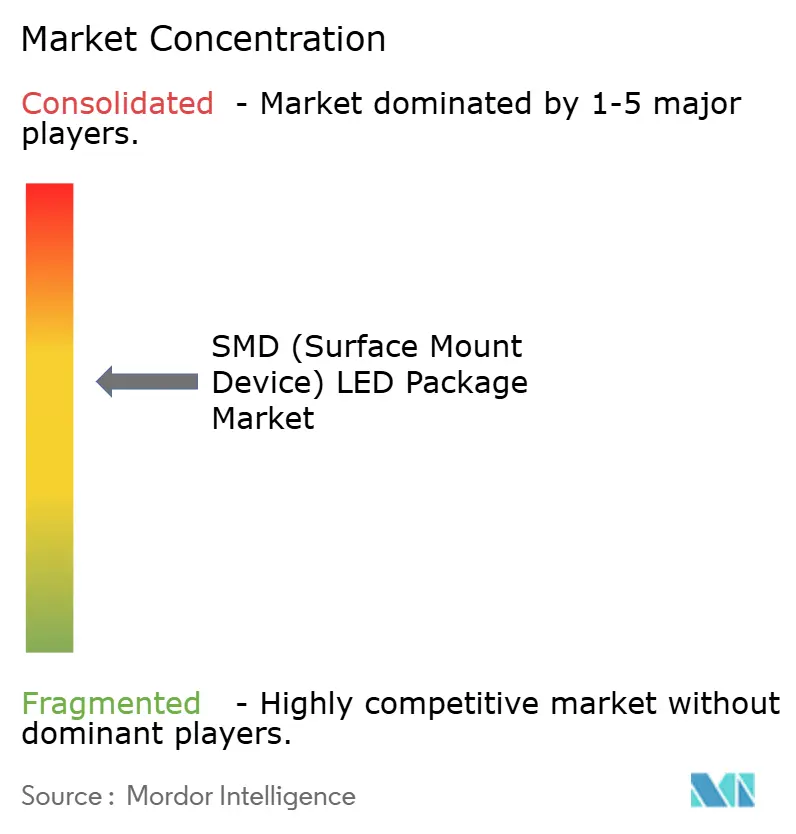

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SMD (Surface Mount Device) LED Package Market Analysis by Mordor Intelligence

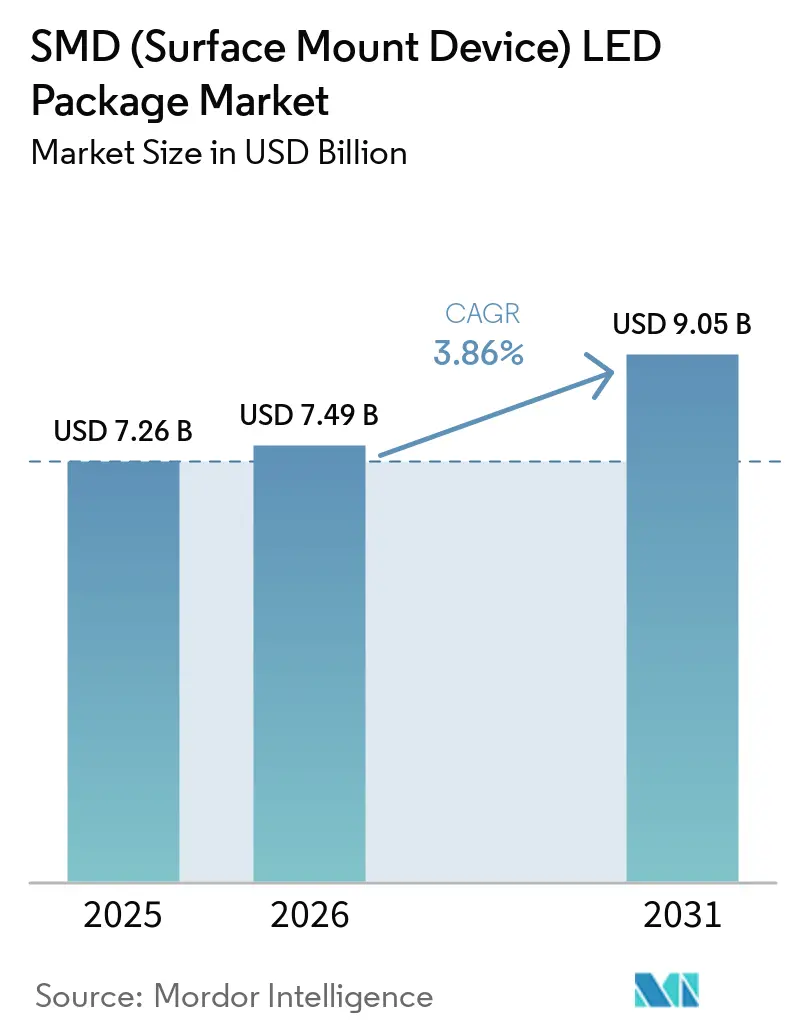

The SMD LED package market size is projected to be USD 7.26 billion in 2025, USD 7.49 billion in 2026, and reach USD 9.05 billion by 2031, growing at a CAGR of 3.86% from 2026 to 2031. A steady topline masks a clear shift in the demand mix, with automotive lighting and ultraviolet (UV) applications expanding faster than general illumination as design rules emphasize beam-forming, sterilization and regulatory-driven efficiency. High-power packages now dominate new automotive platforms that require single-chip addressability below 450 µm in z-height, while mid-power devices remain the workhorses in retrofit lamps and commercial downlights. Asia Pacific continues to anchor two-thirds of global shipments, helped by Chinese provincial incentives that reserve 40% of public-lighting contracts for domestic small and medium enterprises. In the materials stack, phosphor and coating suppliers gain share as quantum-dot alternatives respond to European restrictions on cadmium and lead. Competitive pressure stays intense, flip-chip patent battles between Everlight Electronics and Seoul Semiconductor moved to U.S. federal courts in 2026, underscoring that intellectual-property portfolios rather than sheer capacity additions will tilt margin structures.

Key Report Takeaways

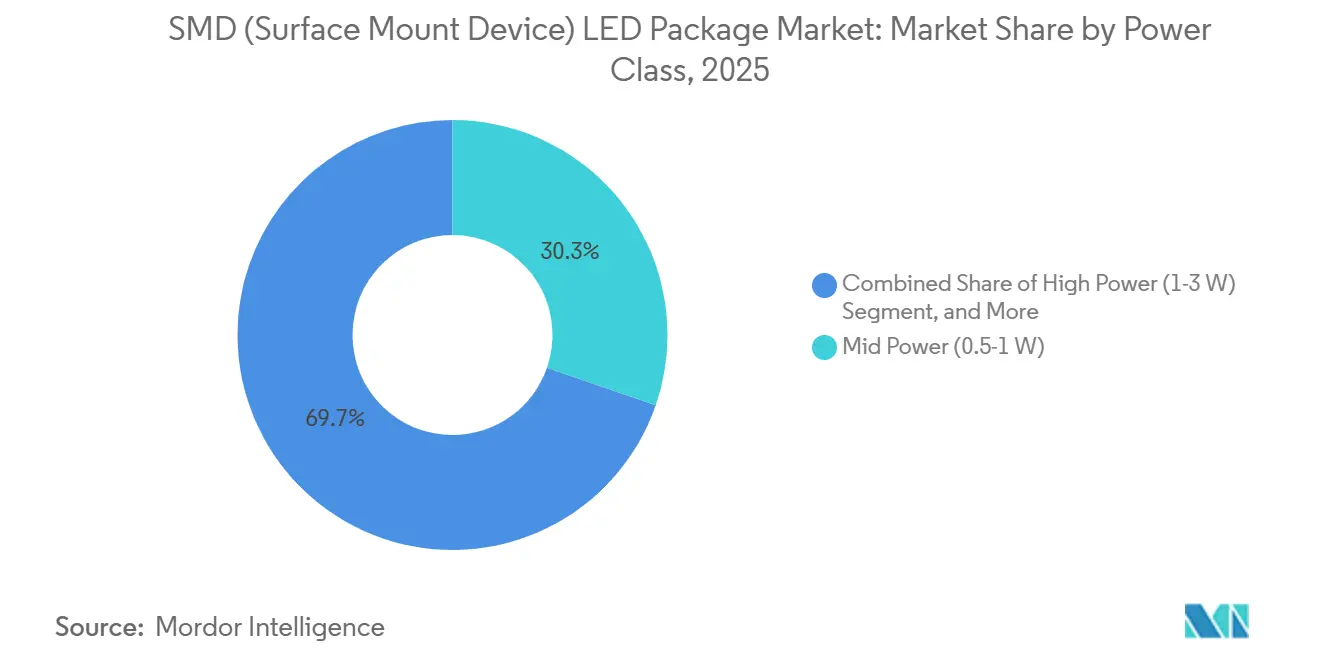

- By power class, mid-power packages captured 30.29% of the SMD LED package market share in 2025, whereas high-power variants are forecast to expand at a 4.22% CAGR through 2031.

- By emission type, visible devices led with 87.38% revenue share in 2025; ultraviolet packages are set to post the fastest growth at a 4.57% CAGR to 2031.

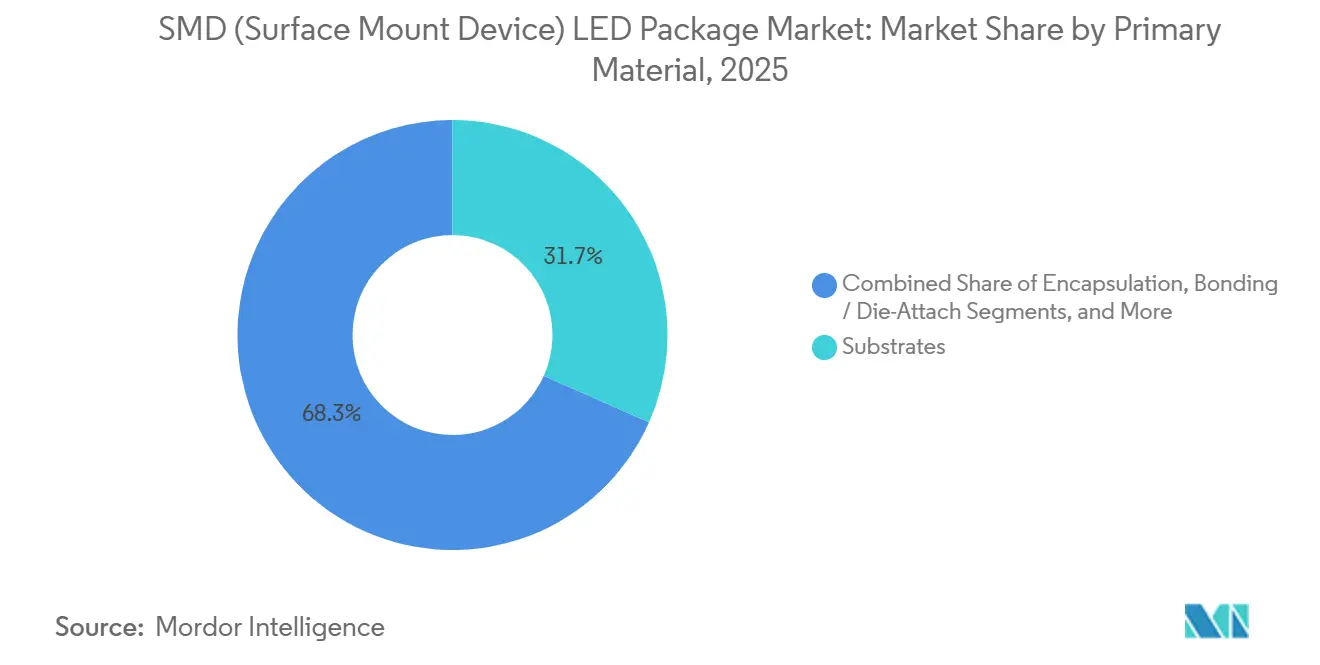

- By primary material, substrates accounted for 31.66% of 2025 sales, while phosphors and coatings will outpace them at a 4.31% CAGR through 2031.

- By application, general lighting held 40.74% of 2025 revenue, and automotive lighting is projected to grow at a 4.06% CAGR through 2031.

- By geography, Asia Pacific commanded 66.85% of global demand in 2025 and is advancing at a 4.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SMD (Surface Mount Device) LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of miniaturized consumer electronics | +0.9% | Global, concentrated in Asia Pacific manufacturing hubs | Medium term (2-4 years) |

| Increasing demand for automotive LED lighting | +1.1% | North America and Europe (regulatory), Asia Pacific (production) | Medium term (2-4 years) |

| Stringent energy efficiency regulations | +0.8% | Europe, North America, spillover to Middle East and Africa | Long term (≥4 years) |

| Rising deployment of smart lighting infrastructure | +0.7% | Europe, North America, Asia Pacific | Medium term (2-4 years) |

| Integration of micro-LED hybrid packages into wearables | +0.3% | Global premium devices | Long term (≥4 years) |

| Supply-chain localization incentives in emerging economies | +0.4% | Asia Pacific, South America, Middle East | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Miniaturized Consumer Electronics

Wearable and smartphone designers are shrinking footprints below 1 mm², forcing SMD LED package makers to deliver sub-0.5 mm z-heights, tighter binning and power densities that hold color shift under 3 MacAdam steps across −10 °C to +60 °C ambient. VueReal’s EcoVue transfer process reached commercial volumes in 2025, enabling the Garmin Fenix 8 Pro to feature full-color micro-LED displays with 30% lower drain than OLED backlights and 10,000-nit outdoor brightness.[1]VueReal, “EcoVue Micro-LED Technology,” vuereal.com AUO and Samsung Display each confirmed dedicated micro-LED lines for 2028 start-ups, signaling long-term demand visibility even at a three-to-five-times cost premium over liquid-crystal alternatives. Thermal loads remain critical; Aismalibar’s phase-change die attach breaks 200 W m⁻¹ K⁻¹ to disperse hotspot gradients. As bezels shrink in consumer devices, these ultrathin packages unlock incremental board space for antennas and sensors, sustaining the driver’s positive CAGR.

Increasing Demand for Automotive LED Lighting

Original equipment manufacturers (OEMs) are moving from static beams to matrix headlights that dim specific emitters in milliseconds, a shift that elevates package requirements for single-chip addressability and junction temperatures below 100 °C. The LUXEON Altilon SMD-A debuted in 2025 with a 433 µm profile, meeting United Nations Regulation 123 criteria for adaptive driving beams in 2026 model-year vehicles.[2]Lumileds, “LUXEON Altilon SMD-A Product Brief,” lumileds.com Down-board, Lumissil’s IS32LT3365 integrates 48 constant-current channels and ISO 26262 diagnostics, while Diodes Incorporated’s AL5958Q adds 16-bit dimming and electromagnetic-interference spread-spectrum features. These electronics, combined with ceramic substrates and sintered-silver attachments, achieve a thermal resistance below 2.5 K W⁻¹, widening the TAM for high-power devices in premium sedans and sport-utility vehicles.

Stringent Energy Efficiency Regulations

January 2026 enforcement of DesignLights Consortium SSL V6.0 lifted minimum luminaire efficacy requirements and established a Premium tier that requires≥140 lm W⁻¹ for outdoor fixtures, instantly filtering out sub-130 lm W⁻¹ mid-power packages in rebate-linked North American projects.[3]DesignLights Consortium, “SSL V6.0 Technical Requirements,” designlights.org Europe’s rescaled A-through-G energy labels push suppliers to hit ≥210 lm W⁻¹ by March 2026, pressuring low-power parts that rely on inexpensive epoxy boards. The International Energy Agency notes that minimum-performance policies now cover 65% of installed lighting, nudging OEM roadmaps toward high-power ceramic footprints that sustain efficacy under tighter ambient limits. Regulations, therefore, keep demand skewed toward premium packages, reinforcing the driver’s positive CAGR lift.

Rising Deployment of Smart Lighting Infrastructure

Municipal retrofits leverage networked luminaires that dim during low-traffic windows, requiring SMD LED packages with L70 lifetimes above 100,000 hours and –40 °C to +85 °C survivability. Telensa’s 55,000-node project in Gloucestershire saved 60% energy in 2025 and cut truck rolls by 40%, evidence that connected fixtures deliver measurable paybacks. Similar wins in Spain and Germany prove that adaptive controls gain share when packages integrate surge protection and wide-range drivers. These installations accelerate replacements and place a recurring tailwind behind durable, mid- to high-power devices that tolerate elevated junction temperatures, justifying the 0.7-point boost to forecast CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal management and heat dissipation challenges | −0.6% | Global, acute in ultra-high power and automotive segments | Medium term (2-4 years) |

| High initial capital expenditure for advanced packaging lines | −0.5% | Asia Pacific, Europe, North America | Short term (≤2 years) |

| Rapid price erosion and margin pressure | −0.4% | Global commodity packages | Short term (≤2 years) |

| Environmental restrictions on antimony-based encapsulants | −0.2% | Europe, spillover to other regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Thermal Management and Heat Dissipation Challenges

Packages exceeding 3 W often drive junctions above 125 °C, halving lumen maintenance to L70 within 30,000 hours and risking catastrophic failure. COFAN’s vertical carbon-nanotube interface hits 1,500 W m⁻¹ K⁻¹ conductivity yet adds USD 0.50-1.00 per unit, too expensive for general illumination.[4]COFAN, “Super Pillar Thermal Interface Material,” cofan.com Even Lumileds’ thermal pad architecture only supports 3.5 W, restricting ultra-high-power adoption to automotive and stadium lighting. Unless passive materials fall to commodity cost levels, thermal bottlenecks will continue to shave 0.6 percentage points off the sector’s CAGR.

High Initial Capital Expenditure for Advanced Packaging Lines

Placement tools with ≤5 µm accuracy and inline phosphor coaters with ±3% uniformity require capital outlays of USD 10 million or more per line, pushing payback periods beyond 5 years for entrants in India and Vietnam. HKC’s USD 1.24 billion Mini-LED campus in Changsha and BOE Jingdian’s USD 690 million automotive panel plant illustrate the scale at which incumbents deploy to amortize tooling costs. Smaller firms face financing hurdles that delay capacity adds, subtracting 0.5 percentage points from achievable growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Class: High-Power Packages Gain Automotive Priority

High-power devices (1-3 W) are set to outpace the broader SMD LED package market at a 4.22% CAGR through 2031 as matrix headlights and high-bay fixtures need single-chip dimming and ceramic thermal paths. The SMD LED package market size for this class will therefore expand faster than mid-power incumbents, which held a 30.29% revenue position in 2025. Mid-power remains indispensable in retrofit lamps where efficacy targets hover near 140 lm W⁻¹, yet low-power devices slip toward indicator niches as OLED and micro-LED displays cannibalize backlight slots. Ultra-high-power (more than 3 W) stays confined to applications with forced-air or liquid cooling, given the severe 125 °C junction ceiling that halves service life.

Automotive specifications amplify demand for high-power formats that stack luminous flux above 450 lm with z-heights under 450 µm. Diodes Incorporated’s AL5958Q and Lumissil’s IS32LT3365 drivers supply 48 dimmable channels that OEMs leverage for glare-free adaptive driving beams in 2026 cars. This drivetrain of optics, drivers and power management sustains the SMD LED package market share momentum for high-power variants while mid-power packages defend commercial downlights, a dichotomy set to widen as DLC thresholds ratchet upward in North America.

By Emission Type: Ultraviolet Packages Move Beyond Pilot Scale

Visible emitters still generate 87.38% of 2025 sales, but UV devices now post the highest slope, rising at a 4.57% CAGR on public-health and water-treatment mandates. The SMD LED package market size tied to UV applications benefits from municipal disinfection plants that replace mercury lamps with 265 nm arrays offering 40% operating-cost cuts. Infrared holds steady around biometric sensing and driver-monitoring, giving suppliers portfolio breadth that cushions pricing swings. Visible packages will continue to dominate shipment counts, yet their growth moderates as efficiency gains approach physical limits and lighting retrofits near saturation.

The arrival of 200 mW UV-C parts from ams OSRAM in late 2026 underscores mainstream acceptance. TrendForce already valued the UV segment at USD 215 million in 2026, up 10% year-over-year, and infrastructure funding pipelines suggest a multi-year capex wave in healthcare and building-air purification. As quantum-dot phosphors push color-rendering of visible products, UV adoption keeps advancing on its separate demand cycle, reinforcing a dual-track outlook across emission types.

By Primary Material: Phosphor Coatings Outpace Substrate Revenues

Substrates accounted for 31.66% of SMD LED package market share in 2025, yet phosphors and coatings are forecast to expand at a 4.31% CAGR through 2031 as quantum-dot alternatives displace antimony-based encapsulants under European restrictions. Ceramic boards with thermal conductivity above 25 W m⁻¹ K⁻¹ are now standard in high-power devices, while epoxy printed-circuit boards recede to indicator and signage niches. Suppliers that automate stencil spraying and inline curing hold a cost edge because they keep thickness variation within ±2%, an increasingly critical spec for color-point stability. Encapsulation chemistry continues to shift toward high-temperature silicones, enabling engine-bay modules to survive 125 °C ambient without yellowing or delamination.

Momentum in the phosphor stack also reflects performance gains, as narrow-band red emitters such as potassium-silicon-fluoride raise color-rendering index above 90 while sustaining efficacy that meets DLC SSL V6.0 premium tiers. Bonding materials move from tin-lead solder to sintered silver, slicing thermal resistance below 0.5 K W⁻¹ and supporting drive currents that push visible flux above 180 lm W⁻¹. These innovations widen the bill-of-materials value pool beyond the die, allowing specialty chemistry suppliers to capture incremental margin even as commodity pricing erodes at the chip level. With every major package maker qualifying at least one cadmium-free quantum-dot formulation for 2027 production, the material hierarchy is expected to tilt further toward coatings over substrates during the forecast window.

By Application: Automotive Lighting Surges Past General Illumination

General lighting accounted for 40.74% of 2025 revenue, but automotive modules are on course to grow at a 4.06% CAGR through 2031, driven by adaptive driving beams that require 48-channel drivers and single-pixel dimming. Matrix headlamps feature high-power packages with z-heights under 450 µm, ceramic substrates, and sintered-silver die attach, effectively doubling average selling prices compared to downlight parts. Regulatory tailwinds amplify demand; United Nations Regulation 123 and FMVSS 108 amendments unlock wider use of glare-free high beams in North America and Europe starting with 2026 model years.

Display backlighting, particularly Mini LED arrays with more than 1,000 local-dimming zones, supplies the next-largest growth pocket as automotive cockpits add curved, high-contrast panels. Specialty segments such as UV disinfection and horticulture post the steepest unit growth yet, yet still finish the period at less than 10% of overall turnover, reflecting their narrow install base, even though revenue per package remains premium. As a result, value migrates from high-volume retrofit bulbs toward high-complexity mobility systems, reinforcing the technology roadmap that prioritizes thermal headroom, driver integration and optical precision over absolute luminous-efficacy gains.

Geography Analysis

Asia Pacific accounted for 66.85% of global SMD LED package revenue in 2025 and is projected to widen its lead, with a 4.16% CAGR through 2031. Chinese provinces such as Guangdong apply procurement quotas reserving 40% of municipal lighting bids for domestic SMEs, guaranteeing local offtake while new facilities in Hunan and Fujian extend substrate self-sufficiency. Regional Comprehensive Economic Partnership tariff relief further integrates Japanese and South Korean chip output with Vietnamese and Thai packaging, shortening lead times and hardening the regional supply moat.

North America and Europe collectively contributed roughly one-quarter of 2025 turnover, but growth remains subdued, constrained by saturation in general illumination and longer commercial-fixture replacement cycles. Even so, policy tightening continues to push value toward high-efficacy parts. The DesignLights Consortium’s SSL V6.0 Premium tier and Europe’s A-grade ≥210 lm/W label require OEM bills of materials to adopt ceramic boards and advanced phosphors, cushioning average selling prices despite flattish volumes. Municipal smart-lighting installations, demonstrated by Telensa’s Gloucestershire rollout and Tridonic’s Darmstadt project, create upgrade waves that modestly offset slowdowns in retrofit sockets.

South America, the Middle East and Africa together hold a small share of global sales but supply-chain localization incentives lift pockets of demand. Vietnam’s USD 500 million Bac Ninh LED cluster and India’s Production-Linked Incentive of 4-6% on incremental sales lure Taiwanese and Korean suppliers into joint ventures. While absolute volumes stay small, regional subsidies peel some assembly away from coastal China, increasing fragmentation and lifting landed costs for global luminaire brands that once relied on single-country sourcing.

Competitive Landscape

Market concentration is moderate. The top five vendors-Nichia, ams OSRAM, Lumileds, Samsung Electronics, and LG Innotek-controlled an estimated half of 2025 revenue, leaving meaningful room for regional challengers. Patent friction intensified in February 2026, when Everlight Electronics sued Seoul Semiconductor in a California federal court, alleging infringement of flip-chip die-attach and thermal-pad patents. The legal volley follows Seoul Semiconductor’s 2025 Supreme Court win in South Korea, which awarded it KRW 5 billion (USD 3.7 million) in damages, illustrating how intellectual property outcomes can realign shares more than capex cycles.

Everlight’s 2024 revenue rose 17.5% to TWD 20.973 billion (USD 647 million) as it pivoted toward infrared sensing and UV disinfection, offsetting margin squeeze in white-light packages. Seoul Semiconductor’s Q2 2025 sales advanced 11% to KRW 284.5 billion (USD 213 million) on its WICOP wire-free architecture that trims thermal resistance below 3 K W⁻¹ and slashes assembly steps. Bridgelux and Dominant Opto Technologies exploit horticulture, curing, and UV niches where 20-30% price premiums persist, while VueReal builds a first-mover beachhead in micro-LED wearables that AUO and Samsung Display aim to industrialize by 2028.

Strategic moves trend toward integration. Lumileds’ LUXEON Altilon SMD-A merges a 433 µm z-height, single-chip addressability and an embedded thermal pad, letting automakers retrofit matrix beams without chassis redesign. Bridgelux’s DriveLux chip-on-board platform co-packages drivers to cut luminaire BOMs by USD 2-3 and simplify wiring. IEC 60598-1:2024’s new photobiological safety rules raise compliance hurdles that favor incumbents with accredited test labs, reinforcing moderate concentration despite an influx of subsidized entrants.

SMD (Surface Mount Device) LED Package Industry Leaders

Nichia Corporation

ams-OSRAM AG

Samsung Electronics Co., Ltd.

Seoul Semiconductor Co., Ltd.

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Everlight Electronics filed a patent-infringement suit against Seoul Semiconductor in U.S. federal court, escalating a decade-long dispute.

- January 2026: DesignLights Consortium SSL V6.0 and LUNA V2.0 became mandatory in rebate programs, lifting efficacy thresholds and introducing blue-light hazard limits.

- December 2025: ams OSRAM announced a 200 mW UV-C LED package for Q4 2026 launch, targeting air purification.

- August 2025: South Korea’s Supreme Court upheld a KRW 5 billion (USD 3.7 million) damages award to Seoul Semiconductor in a technology-theft case against Everlight Electronics.

Global SMD (Surface Mount Device) LED Package Market Report Scope

The SMD LED Package Market refers to the market for surface-mount device (SMD) LED packages, which are compact, energy-efficient light-emitting diode (LED) packages designed for surface-mounting on printed circuit boards (PCBs).

The SMD LED Package Market Report is Segmented by Power Class (Low Power, Mid Power, High Power, and Ultra-High Power), Emission Type (Visible, Infrared, and Ultraviolet), Primary Material (Substrates, Encapsulation, Bonding, and Phosphors), Application (General Lighting, Automotive, Display, and Specialty), and Geography (North America, South America, Europe, Asia Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Low Power (Less than 0.5 W) |

| Mid Power (0.5-1 W) |

| High Power (1-3 W) |

| Ultra-High Power (More than 3 W) |

| Visible LED Packages |

| Infrared (IR) LED Packages |

| Ultraviolet (UV) LED Packages |

| Substrates |

| Encapsulation |

| Bonding / Die-Attach |

| Phosphors / Coatings |

| General Lighting (Residential, Commercial, Industrial, Street) |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche (Horticulture, Medical, UV Disinfection) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Power Class | Low Power (Less than 0.5 W) | |

| Mid Power (0.5-1 W) | ||

| High Power (1-3 W) | ||

| Ultra-High Power (More than 3 W) | ||

| By Emission Type | Visible LED Packages | |

| Infrared (IR) LED Packages | ||

| Ultraviolet (UV) LED Packages | ||

| By Primary Material | Substrates | |

| Encapsulation | ||

| Bonding / Die-Attach | ||

| Phosphors / Coatings | ||

| By Application / End-Use | General Lighting (Residential, Commercial, Industrial, Street) | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche (Horticulture, Medical, UV Disinfection) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the SMD LED package market in 2031?

The market is expected to reach USD 9.05 billion by 2031, reflecting a 3.86% CAGR from 2026.

Which power class is growing fastest in SMD LED packages?

High-power devices in the 1-3 W range are projected to expand at a 4.22% CAGR through 2031, driven mainly by automotive matrix headlights.

Why are ultraviolet SMD LED packages gaining traction?

UV packages grow at a 4.57% CAGR as water disinfection, medical curing and air-purification systems replace mercury lamps and expand municipal use.

How dominant is Asia Pacific in SMD LED package production?

Asia Pacific held 66.85% revenue share in 2025 and remains the fastest-growing region at a 4.16% CAGR to 2031 due to localized subsidies and fabrication clusters.

Which companies lead technological innovation in this field?

Nichia, ams OSRAM, Lumileds, Samsung Electronics and LG Innotek lead, while Everlight and Seoul Semiconductor focus on flip-chip and packageless IP to gain share.

Page last updated on: