Flip-Chip LED Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

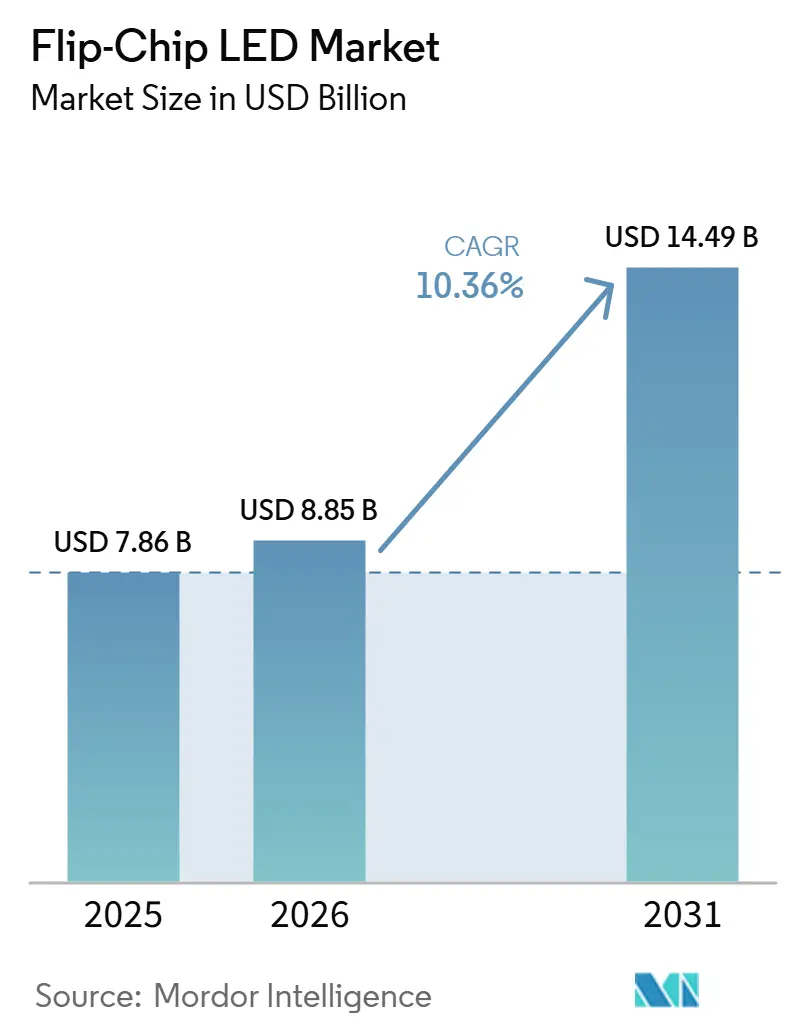

| Market Size (2026) | USD 8.85 Billion |

| Market Size (2031) | USD 14.49 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

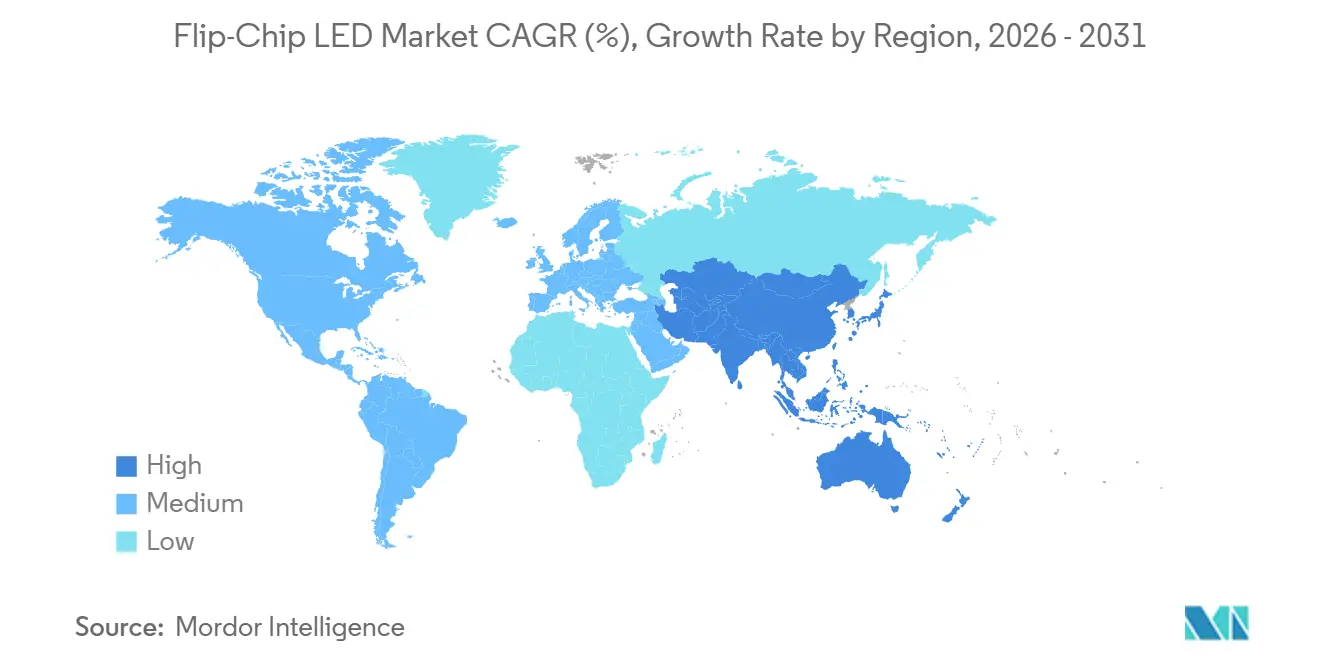

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

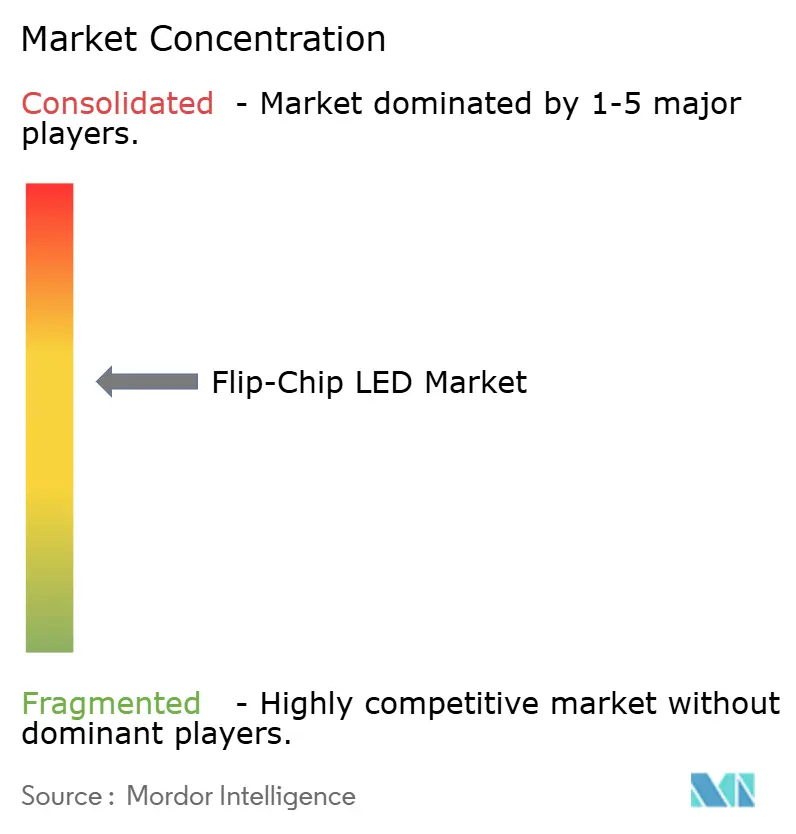

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flip-Chip LED Market Analysis by Mordor Intelligence

The Flip-Chip LED market size is expected to increase from USD 7.86 billion in 2025 to USD 8.85 billion in 2026 and reach USD 14.49 billion by 2031, growing at a CAGR of 10.36% over 2026-2031. Sustained demand from automotive adaptive lighting, mini-LED backlighting in large-format televisions and monitors, and specialty defense emitters supports this growth trajectory. OEM migration toward matrix headlamps and high-zone-count backlight units has validated the flip-chip architecture because eliminating wire bonds lowers thermal resistance and enables tighter die spacing. Energy-efficiency mandates in Asia-Pacific and Europe accelerate solid-state lighting adoption, while wafer-level packaging innovations reduce assembly time and improve unit economics for high-volume displays. Competition from vertical thin-film GaN exists, yet incumbents continue to favor flip-chip lines when luminous density, shock tolerance, and lifetime outweigh marginal cost premiums.

Key Report Takeaways

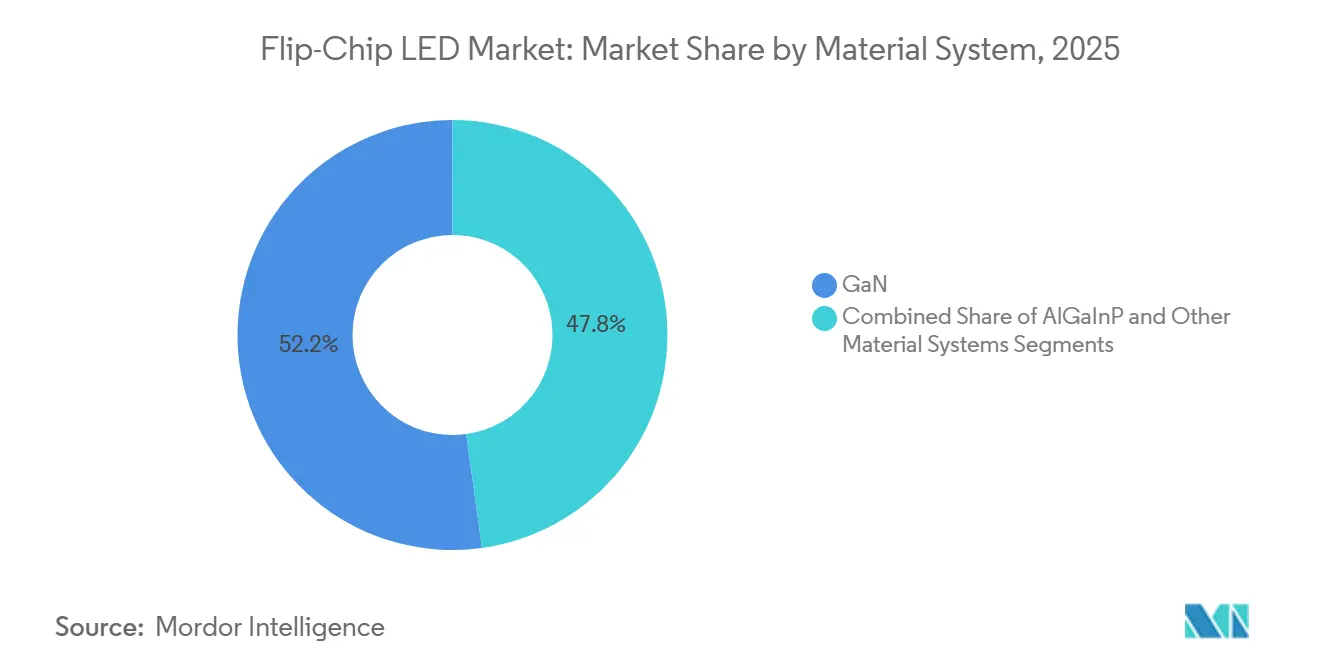

- By material system, gallium nitride captured 52.19% of 2025 revenue, while ultraviolet and infrared specialty material systems are projected to expand at a 10.85% CAGR through 2031.

- By wavelength, blue devices held 41.52% of 2025 revenue share, whereas green emitters are forecast to post the fastest 10.91% CAGR between 2026-2031.

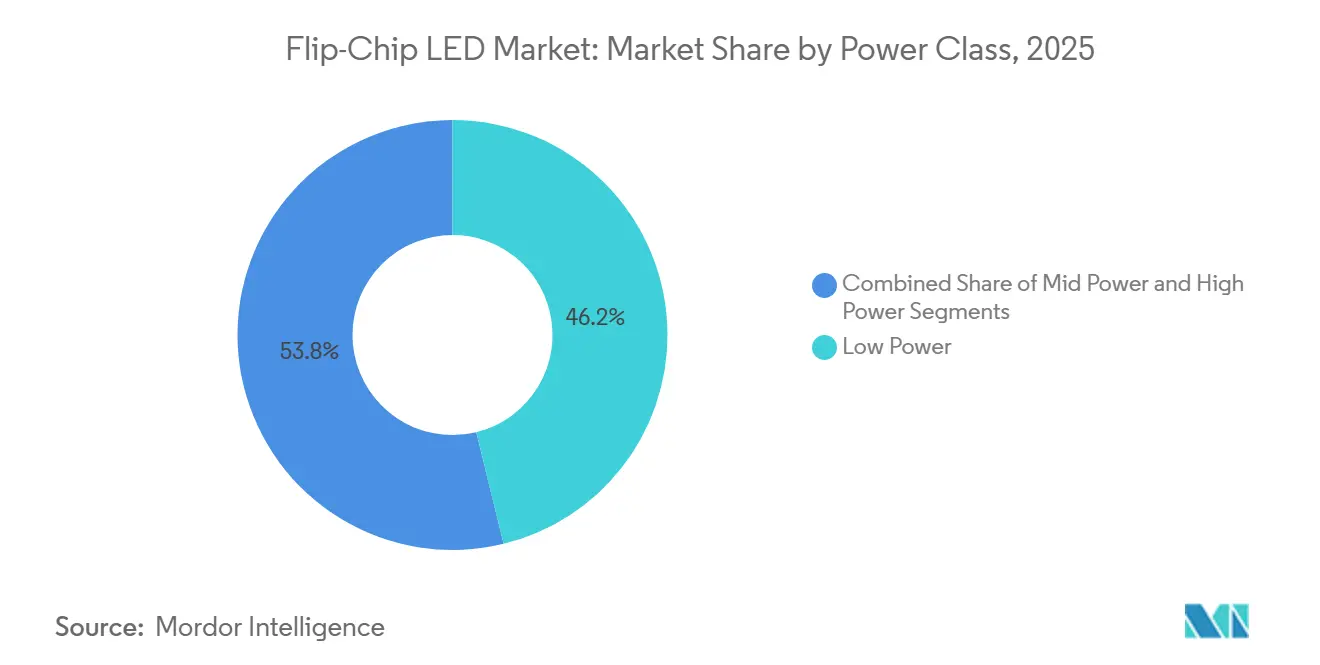

- By power class, low-power packages accounted for 46.18% of 2025 revenue, yet high-power packages above 3 watts are expected to grow at an 11.27% CAGR over the forecast period.

- By application, general lighting led with 44.39% of 2025 revenue, and automotive lighting is positioned to record the highest 11.06% CAGR through 2031.

- By geography, Asia-Pacific held 42.72% of 2025 revenue and is projected to expand at an 11.14% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flip-Chip LED Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated mini-LED adoption in large-format displays | +2.8% | Global, APAC core with spill-over to North America | Medium term (2-4 years) |

| Rapid penetration in automotive adaptive lighting modules | +2.5% | Global, Europe and North America lead regulatory adoption | Medium term (2-4 years) |

| Energy-efficiency mandates across Asia-Pacific and Europe | +1.9% | Asia-Pacific and Europe | Long term (≥ 4 years) |

| Lower total-cost-of-ownership versus wire-bond LEDs | +1.4% | Global | Long term (≥ 4 years) |

| Micro-LED pilot production driving wafer-level flip-chip demand | +1.1% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Defense and aerospace push for high-g hard-mounted emitters | +0.7% | North America, Europe, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Mini-LED Adoption in Large-Format Displays

Demand for premium televisions and monitors has shifted to direct-lit mini-LED backlighting with more than 10,000 local dimming zones, driving a sharp rise in high-density flip-chip die shipments.[1]Display Industry Analysis, “Mini-LED Backlight Market 2025,” displayindustryanalysis.com Eliminating wire bonds lets manufacturers position emitters closer together, which is critical when thousands of dice populate a single module. Better thermal paths permit each pixel to operate at higher current without early lumen depreciation, enabling HDR peak luminance above 2,000 nits. Flip-chip mini-LEDs also reduce module thickness by 15-20%, resulting in slimmer bezels and lower shipping costs. These advantages reinforce the Flip-Chip LED market leadership position in premium display backlights.

Rapid Penetration in Automotive Adaptive Lighting Modules

Adaptive driving beam systems require pixelated arrays that modulate individual emitters in milliseconds, and flip-chip bonding maintains current density and heat flux within compact headlamp enclosures. Automotive-qualified packages, such as the LUXEON Altilon SMD-A, achieve luminous intensity above 1,200 lumens while meeting stringent AEC-Q102 reliability targets.[2]Lumileds, “LUXEON Altilon SMD-A,” lumileds.com European ECE Regulation 123 mandates glare-free high beams on new vehicle types from 2026, accelerating procurement of flip-chip LED arrays that deliver precise beam shaping. Volume contracts awarded to Seoul Semiconductor and others confirm that adaptive lighting demand boosts the Flip-Chip LED market well into the forecast horizon.

Energy-Efficiency Mandates Across Asia-Pacific and Europe

Stage 4 of the European Ecodesign Regulation lifted minimum efficacy thresholds for directional and non-directional lamps in September 2025, forcing luminaire makers to redesign products around higher-performing LEDs ec.europa.eu. Australia and New Zealand introduced comparable rules under the Greenhouse and Energy Minimum Standards Act, and China updated GB 30255-2019 to accelerate mercury-free fluorescent lamp replacement. Because flip-chip packages dissipate heat more efficiently, they maintain efficacy at elevated junction temperatures, an attribute that aligns with tightening standards. Government procurement programs and retrofit incentives, therefore, channel demand toward the Flip-Chip LED market across both residential and commercial segments.

Lower Total-Cost-of-Ownership Versus Wire-Bond LEDs

Component-level prices for flip-chip LEDs are 20-30% above those of wire-bond alternatives, yet total lifecycle assessments favor flip-chip assemblies when smaller heatsinks, simpler drivers, and reduced maintenance are included. The direct die-to-substrate path reduces junction-to-case thermal resistance by almost half, allowing designers to eliminate fans in industrial luminaires and thereby lower system bills of material by 15-20%. Flip-chip packages also endure more than 3,000 thermal cycles in JEDEC-defined stress tests, triple the fatigue limit of wire bonds, a resilience that reduces warranty claims and truck rolls. These economics strengthen the adoption curve for the Flip-Chip LED market in both retrofit and new-build projects.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive flip-chip packaging lines | -1.6% | Global, acute in emerging markets | Medium term (2-4 years) |

| Competitive pressure from vertical thin-film LEDs | -1.2% | Global, APAC and North America manufacturing hubs | Long term (≥ 4 years) |

| Sub-P0.5 repairability and yield losses | -0.9% | APAC core, display manufacturing regions | Short term (≤ 2 years) |

| Indium bump reliability under thermal cycling | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Flip-Chip Packaging Lines

Equipment sets for high-volume flip-chip assembly require die bonders, underfill dispensers, and reflow ovens that collectively cost USD 15-25 million, a hurdle that delays capacity expansion in emerging markets.[3]Semiconductor Packaging Equipment Market, “Market Analysis 2025,” semiconductorpackagingequipment.com Tool lead times stretched to 12-18 months during 2025, and backlogs at Besi and ASM Pacific Technology exceeded six quarters, constraining second-tier packagers. Process windows are narrower than for wire bonds, demanding cleanroom upgrades and inline metrology that raise operational expense by 30-40%. These capital barriers slow new-entrant participation, tempering Flip-Chip LED market growth in cost-sensitive geographies.

Competitive Pressure from Vertical Thin-Film LEDs

Vertical thin-film GaN devices bond the epitaxial layer to a reflective metal carrier, eliminating current-spreading losses that limit lateral flip-chip designs at high current densities. Analysts forecast that vertical LEDs could capture up to 20% of the high-power segment by 2028, particularly in cost-driven general lighting.[4]LED Industry Forecast, “Vertical Thin-Film LED Market Share 2025,” ledindustryforecast.com Manufacturers therefore face strategic uncertainty about whether to invest simultaneously in both lateral and vertical platforms, and any misstep risks stranding capital. This rivalry moderates the long-term growth rate of the Flip-Chip LED market, despite robust demand for niche specialty wavelengths.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material System: GaN Dominance Coupled with Specialty Momentum

Gallium nitride controlled 52.19% of 2025 revenue, underscoring its status as the workhorse substrate for blue and white emitters that dominate general illumination. The wide bandgap, high thermal conductivity, and mature epitaxial recipes of GaN underpin efficient emission across visible wavelengths, reinforcing its primacy in the Flip-Chip LED market. Scaling to 300 millimeter GaN-on-silicon wafers may cut die cost per lumen in the coming years, further solidifying the material’s value proposition.

Other material systems, chiefly ultraviolet, infrared, and short-wave infrared, are forecast to grow at a 10.85% CAGR. Water purification modules using ultraviolet-C flip-chip emitters and non-invasive biosensing devices employing indium phosphide infrared dice illustrate how specialty materials outpace the broader Flip-Chip LED market. Defense and aerospace requirements for shock-resistant packages further expand demand for niche wavelengths that flip-chip bonding supports through superior mechanical robustness.

By Wavelength: Blue Leadership with Accelerating Green Upside

Blue Dice supplied 41.52% of revenue in 2025, leveraging decades of process refinement to achieve commercial efficacy beyond 150 lumens per watt at a 85 °C junction temperature. These devices underpin phosphor-converted white light and serve as the baseline backlight for LCDs, guaranteeing continued bulk volume for the Flip-Chip LED market. Red phosphide retains importance in signaling and horticulture but expands more slowly due to temperature-sensitive efficiency.

Green emitters are set to grow at a 10.91% CAGR following a 2025 laboratory breakthrough that delivered 65% external quantum efficiency using aluminum-treated quantum wells. Closing the historic green gap elevates micro-LED display performance, as green sub-pixels dominate perceived luminance. This technical leap positions green flip-chip LEDs for rapid share gains, reinforcing overall Flip-Chip LED market momentum toward high-resolution direct-view panels.

By Power Class: High-Power Packages Capture Upside

Low-power packages under 1 watt took 46.18% of 2025 revenue, serving bulbs, downlights, and consumer electronics backlights that prioritize cost efficiency. Mid-power devices between 1 and 3 watts serve architectural lighting and automotive daytime running lamps, balancing luminous output and thermal dissipation in compact form factors; Lumileds' LUXEON Altilon SMD DT series, rated at 3 watts and delivering 335 lumens in cool white, exemplifies this category with AEC-Q102 qualification and dual-color capability for automotive front turn and DRL applications.

High-power packages exceeding 3 watts are expected to post an 11.27% CAGR, driven by automotive forward lighting and stadium luminaires that demand over 1,000 lumens per package. Flip-chip bonding sustains these drive currents thanks to lower series resistance, a benefit that is boosting Flip-Chip LED market share in high-power classes as OEMs consolidate emitter counts to shrink optics and assembly time.

By Application: Automotive Surging Past General Lighting

General illumination accounted for 44.39% of 2025 revenue, as retrofit programs and stricter efficiency rules spurred the replacement of early wire-bond lamps. Circular-economy directives in Europe updated in 2024 mandate that lighting products sold after 2026 must support component-level repair and recycling, favoring flip-chip packages with standardized footprints and solder-based attachment over adhesive-bonded wire-bond modules.

Automotive lighting is poised to register an 11.06% CAGR, the fastest of all applications, because adaptive beam regulations effectively require pixel-addressable arrays that only flip-chip configurations can support. Win rates for suppliers such as Nichia, ams-OSRAM, and Seoul Semiconductor confirm that headlamp and signal modules will remain the growth engine of the Flip-Chip LED market through 2031.

Geography Analysis

Asia-Pacific controlled 42.72% of 2025 revenue and is projected to grow at an 11.14% CAGR through 2031, powered by capacity expansions in China, Taiwan, and South Korea. San’an Optoelectronics operates the world’s largest MOCVD fleet and broadened flip-chip output after acquiring Lumileds, an integration that secures automotive customer pipelines. Taiwan’s Epistar and Lextar pivoted toward mini-LED and micro-LED, capitalizing on the same high-density attributes that differentiate the Flip-Chip LED market. Japan’s Nichia and South Korea’s Samsung continue to lead breakthroughs in efficacy that quickly migrate into mass production.

Europe and North America jointly contributed a significant share of 2025 revenue. The European Union’s Stage 4 Ecodesign rules accelerated retrofits, while ECE Regulation 123 guarantees future demand for adaptive headlights that rely heavily on flip-chip arrays. North American manufacturing rationalized in 2025 when Cree Lighting outsourced assembly while retaining engineering oversight, illustrating how local producers adjust cost structures while safeguarding intellectual property. Despite some reshoring initiatives, most headlamp LED modules destined for U.S. and European vehicles still originate from Asia-based packagers, reinforcing cross-regional supply interdependence within the Flip-Chip LED market.

Middle East and Africa, South America, and other emerging regions together held a small share of 2025 revenue but show above-average growth. Smart-city rollouts in Saudi Arabia and the United Arab Emirates specify flip-chip streetlights capable of withstanding 50 °C ambient temperatures. Sub-Saharan retrofit programs financed under multilateral energy-access schemes replicate Asia’s early LED adoption curve, promising steady upside for the Flip-Chip LED market once supply chain constraints ease. South American demand is concentrated in Brazil and Argentina, where harmonization with European automotive lighting standards opens a direct channel for adaptive headlamp modules.

Competitive Landscape

The Flip-Chip LED market exhibits moderate concentration; the top five suppliers held a significant share of 2025 revenue. Nichia and ams-OSRAM signed a broad patent cross-license in October 2025 that reduces litigation exposure and accelerates next-generation product co-development. Samsung leverages vertical integration across epitaxy, packaging, and module assembly to defend its television and handset franchises, while Seoul Semiconductor exploits hot-binned flip-chip technology to grow automotive share.

Emerging challengers such as PlayNitride are pushing wafer-level flip-chip micro-LED solutions that eliminate die pick-and-place, reducing assembly cost by up to 50%. Equipment vendors respond by refining high-accuracy wafer bonders that narrow underfill void fractions, which directly benefits all participants in the Flip-Chip LED market. At the same time, vertical thin-film GaN threatens to siphon high-power sockets if substrate removal yields improve and cost converges.

Raw material risk looms over indium bump supply, with prices oscillating between USD 200 and USD 350 per kilogram during 2024-2025. Any export disruption could shift demand toward vertical thin-film LEDs that avoid indium solder, a scenario closely watched by automotive Tier-1s that require long-term contracts for mission-critical headlamp modules. Vendors therefore hedge by qualifying alternative bump chemistries and dual-sourcing substrates, a trend that shapes future competitive dynamics within the Flip-Chip LED market.

Flip-Chip LED Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd.

Seoul Semiconductor Co., Ltd.

Penguin Solutions Inc. (Cree Inc.)

Osram Opto Semiconductors GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cree Inc. launched OptiLamp packages with embedded sensors that automatically fine-tune current and luminance for adaptive lighting and predictive maintenance.

- February 2026: Cree Inc. entered a long-term U.S. manufacturing partnership to regain delivery reliability in industrial and outdoor fixtures.

- January 2026: Cree Inc. introduced L2 PCBA Solutions, a turnkey board assembly that bundles flip-chip LEDs, drivers, and thermal substrates for rapid luminaire integration.

- October 2025: Nichia and ams-OSRAM finalized a wide-ranging patent cross-license covering GaN LEDs, laser diodes, and flip-chip packages for automotive matrix headlamps.

Global Flip-Chip LED Market Report Scope

The Flip-Chip LED Market refers to the industry focused on the production, development, and application of flip-chip light-emitting diodes (LEDs). These LEDs feature a unique design in which the chip is mounted upside down, enabling improved thermal management, higher efficiency, and better performance than traditional LED designs.

The Flip-Chip LED Market Report is Segmented by Material System (GaN, AlGaInP, and Other Material Systems), Wavelength/Color (Blue, White, Red, Green, and Other Wavelengths/Colors), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Displays and Signage, Backlighting, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| GaN |

| AlGaInP |

| Other Material Systems |

| Blue |

| White |

| Red |

| Green |

| Other Wavelengths / Colors |

| Low Power |

| Mid Power |

| High Power |

| General Lighting |

| Automotive Lighting |

| Displays and Signage |

| Backlighting |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Material System | GaN | |

| AlGaInP | ||

| Other Material Systems | ||

| By Wavelength / Color | Blue | |

| White | ||

| Red | ||

| Green | ||

| Other Wavelengths / Colors | ||

| By Power Class | Low Power | |

| Mid Power | ||

| High Power | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Displays and Signage | ||

| Backlighting | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Flip-Chip LED market by 2031?

The Flip-Chip LED market is forecast to reach USD 14.49 billion by 2031 based on current growth projections.

Which region is expected to post the fastest growth through 2031?

Asia-Pacific is projected to expand at an 11.14% CAGR, the highest among all regions during 2026-2031.

Why are flip-chip LEDs preferred for automotive adaptive headlights?

They allow individually addressable pixels, manage high current densities, and meet AEC-Q102 reliability thresholds, enabling precise glare-free beam control.

Which material system dominates flip-chip LED revenue?

Gallium nitride remains the leading material, accounting for 52.19% of 2025 revenue due to its efficiency across the visible spectrum.

What technology trend could challenge flip-chip LEDs in high-power lighting?

Vertical thin-film GaN LEDs may erode share if their cost and yield improve, as they remove lateral resistance and indium bump reliance.

Page last updated on: