Infrared Emitter And Receiver Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

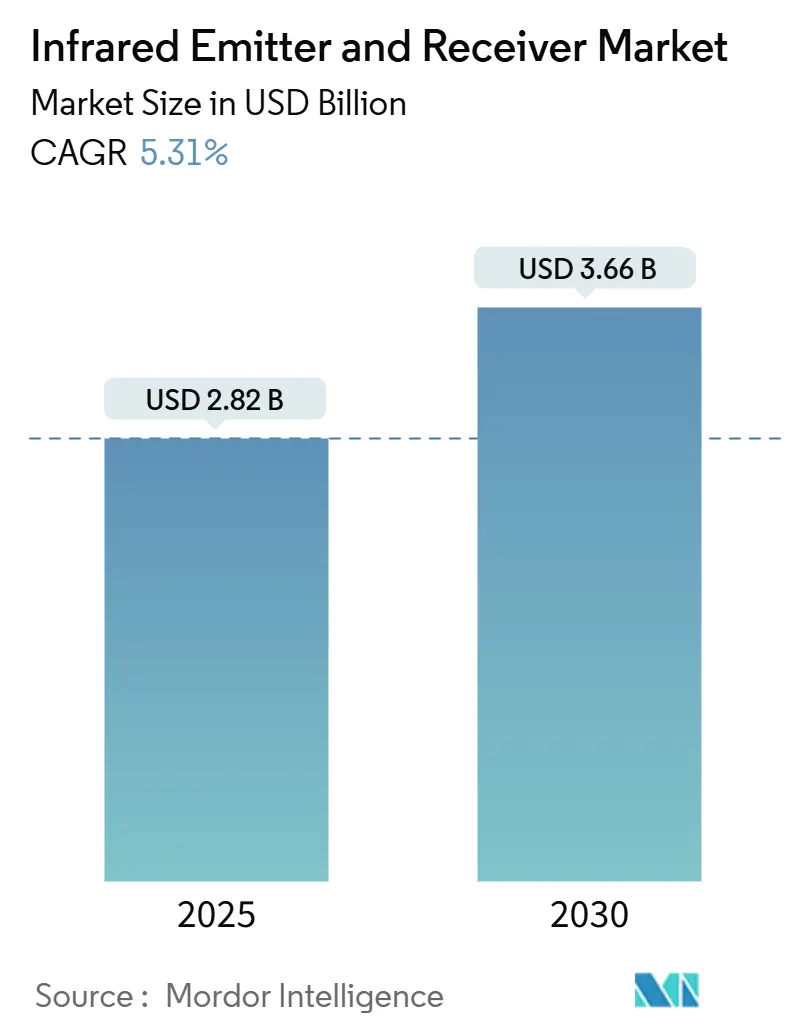

| Market Size (2025) | USD 2.82 Billion |

| Market Size (2030) | USD 3.66 Billion |

| Growth Rate (2025 - 2030) | 5.31% CAGR |

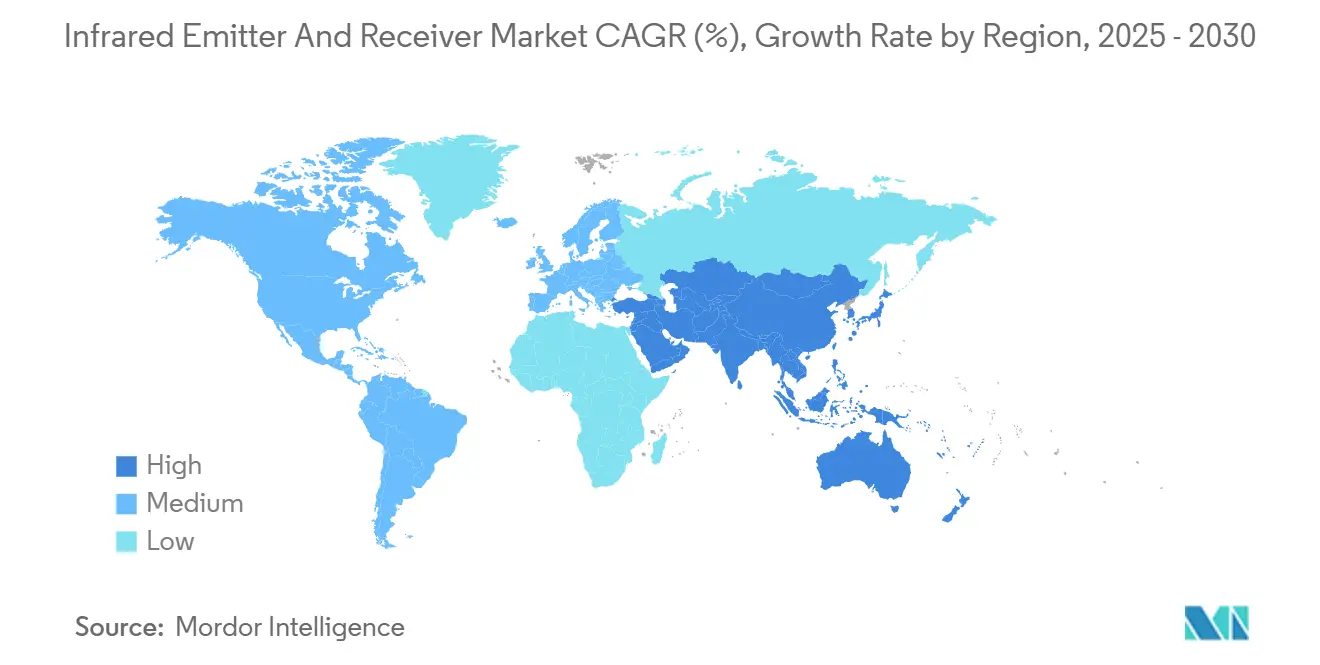

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infrared Emitter And Receiver Market Analysis by Mordor Intelligence

The infrared emitter and receiver market size reached USD 2.82 billion in 2025 and is projected to increase to USD 3.66 billion by 2030, representing a 5.31% CAGR. This steady climb reflects the sector’s successful migration from niche sensing roles to broad deployment in automotive safety, consumer electronics, and factory automation. The regulation-driven adoption of thermal cameras in new vehicles, continued demand for smartphones with 3D depth capture capabilities, and the expansion of predictive-maintenance programs on factory floors are the primary drivers. Cost declines in near-infrared sensors, paired with design wins for compact vertical-cavity surface-emitting lasers (VCSELs), encourage faster design cycles in gesture interfaces and biometric log-ins. Meanwhile, rising venture funding for smart-agriculture and space-based observation platforms adds new end-use pull, reinforcing a resilient demand outlook across economic cycles.

Key Report Takeaways

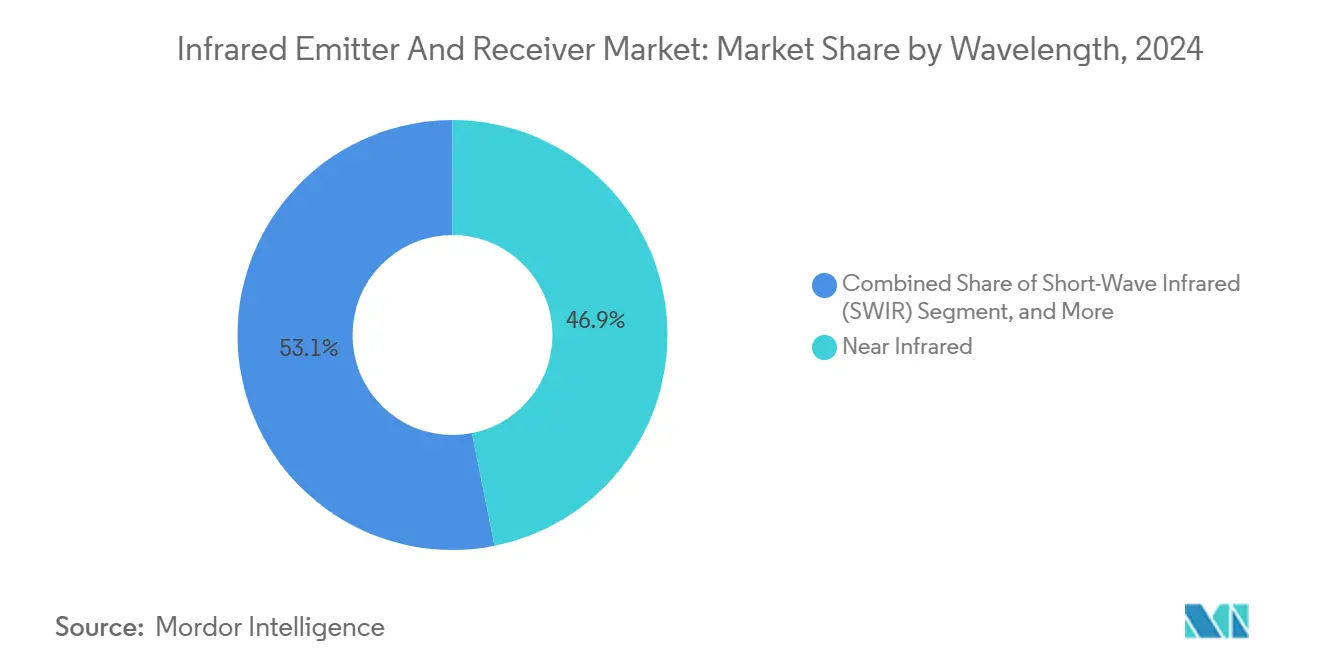

- By wavelength, near-infrared led with 46.87% revenue share in 2024, while short-wave infrared is forecast to expand at a 6.07% CAGR through 2030.

- By component, infrared emitters held 61.79% of the infrared emitter and receiver market share in 2024; receivers are projected to grow at a 5.69% CAGR to 2030.

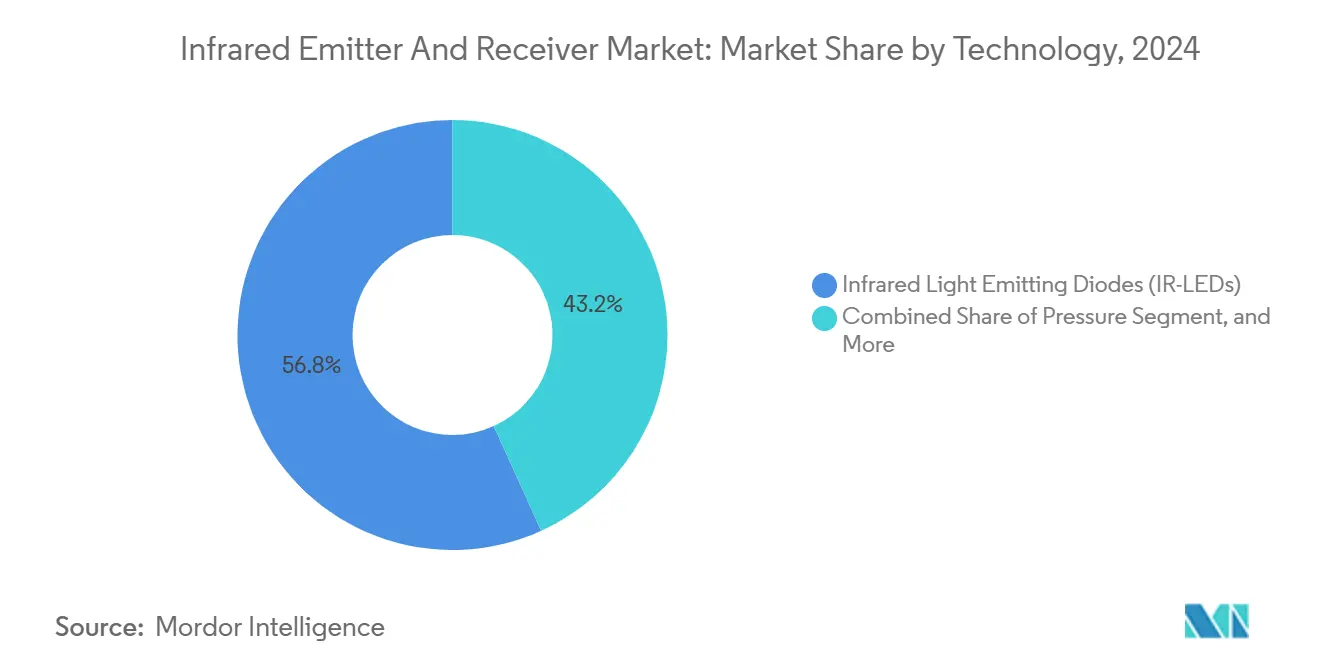

- By Technology, LED solutions commanded 56.78% of the infrared emitter and receiver market size, and laser diodes are projected to advance at a 5.89% CAGR through 2030.

- By application, consumer electronics captured 35.83% of the 2024 revenue, whereas automotive applications are accelerating at a 6.13% CAGR through 2030.

- By geography, the Asia Pacific accounted for 42.37% of the 2024 turnover, while the Middle East is set to grow the fastest at a 5.91% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Infrared Emitter And Receiver Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption in Advanced Driver Assistance Systems (ADAS) | +1.8% | Global, with early gains in Europe, North America | Medium term (2-4 years) |

| Proliferation of Gesture Control in Consumer Electronics | +1.2% | Global, concentrated in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Expansion of 3D Sensing in Smartphones | +1.0% | Global, spill-over from premium to mid-range segments | Short term (≤ 2 years) |

| Increased Industrial Automation and Robotics | +0.9% | Asia Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Emerging Demand from Smart Agriculture Monitoring | +0.3% | Global, with early adoption in precision farming regions | Long term (≥ 4 years) |

| Rising Investments in Space-Based Infrared Surveillance | +0.2% | North America, Europe, select Asia Pacific nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption in Advanced Driver Assistance Systems (ADAS)

Infrared cameras now underpin driver monitoring and pedestrian detection functions required under the European General Safety Regulation, which took effect in mid-2024. Automakers integrate long-wave thermal imagers that can recognize pedestrians or animals at a distance of 300 m, supporting higher autonomy levels and enhancing night-driving safety.[1]European Commission, “Revision of the General Safety Regulation for Motor Vehicles,” ec.europa.eu Heavy-duty fleets in North America retrofit thermal sensors to meet forthcoming federal blind-spot rules. Technology suppliers bundle VCSEL emitters and CMOS receivers into single-package modules, cutting integration times for Tier 1 suppliers. As over-the-air software updates unlock new heat-signature analytics, OEMs treat infrared arrays as essential redundancy alongside radar and lidar. The resulting hardware pull delivers the largest single-driver uplift to the infrared emitter and receiver market.

Proliferation of Gesture Control in Consumer Electronics

Smartphone and tablet brands embed compact infrared time-of-flight modules that register hover and wave commands, addressing hygiene-sensitive use cases in public kiosks and medical settings. Apple’s TrueDepth array refines Face ID accuracy by pairing dual-wavelength emitters with higher-resolution receivers, extending the effective sensing range while lowering power draw.[2]Apple, “AVFoundation Camera and Media Capture,” developer.apple.com Gaming consoles and smart-TV remotes now rely on emitter-receiver pairs to enable mid-air volume control. Module suppliers report sub-0.1 mm depth precision on new 940 nm VCSEL parts, enabling watch-sized devices to add pinch-and-zoom gestures. Rapid design cycles in Asia-Pacific contract-manufacturing hubs sustain a strong near-term demand for high-volume components.

Expansion of 3D Sensing in Smartphones

Premium handset makers have pushed structured-light and time-of-flight infrared sensing into mass adoption, and the cost curve now supports rollout across mid-tier models. Infrared depth maps enhance portrait photography, augmented-reality object placement, and laser-autofocus speed, particularly in low-light conditions.[3]Springer Nature, “Time-of-Flight Sensing for Mobile Applications,” nature.com Dual-wavelength arrays combine near-infrared technology for biometric unlock with short-wave infrared technology for material discrimination, enabling counterfeit detection in mobile payment workflows. Integration with on-device neural processors yields sub-50 ms latency for depth perception. As sensor suppliers transition to stacked-wafer architectures, unit cost reductions will accelerate the diffusion of these components across tablet and laptop categories, thereby increasing overall component volumes.

Increased Industrial Automation and Robotics

Factory-floor adoption of infrared thermography has reduced unplanned downtime by up to 30% in industries ranging from steel mills to semiconductor fabs. Collaborative robots rely on proximity-sensing infrared rings to detect human presence and dynamically slow movements, facilitating shared workcells without cages. Quality-control stations deploy short-wave infrared cameras to inspect silicon wafers for sub-surface voids that visible optics cannot reveal. As global capacity-expansion plans for electric-vehicle battery plants proceed, demand for non-contact thermal mapping in gigafactories strengthens medium-term growth prospects for the infrared emitter and receiver market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Short-Wave Infrared Sensors | -0.8% | Global, particularly affecting price-sensitive markets | Medium term (2-4 years) |

| Supply Chain Disruptions of Compound Semiconductors | -0.6% | Global, concentrated in Asia Pacific supply chains | Short term (≤ 2 years) |

| Stringent Export Controls on Dual-Use IR Components | -0.4% | International trade, US-China technology restrictions | Long term (≥ 4 years) |

| Heat Management Challenges in Miniaturised Packages | -0.3% | Global, affecting mobile and wearable applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Short-Wave Infrared Sensors

InGaAs substrates cost more than USD 2,000 per wafer, and sub-70% yield rates inflate finished detector prices, making short-wave solutions beyond the reach of budget-sensitive consumer devices. As a result, adoption remains largely restricted to machine-vision inspection and scientific instruments where performance trumps price. Foundry initiatives to transition from 100 mm to 150 mm wafer lines have begun, but are not expected to materially lower costs before 2027. The price gap versus silicon-based near-infrared sensors is therefore likely to suppress some of the infrared emitter and receiver market’s upside during the forecast period.

Supply Chain Disruptions of Compound Semiconductors

Gallium and germanium export curbs imposed by China in 2024 tightened supplies of essential feedstocks for infrared diodes and detectors. Gallium output concentration above 80% in a single country leaves Western fabs exposed to multi-quarter lead-time spikes and spot-price surges. While Japanese and European firms are building recycling loops to capture gallium from LED scrap, meaningful tonnage will not reach the market before 2026. Any prolonged geopolitical escalations could further delay shipments, prompting OEMs to dual-source or redesign products around alternative wavelengths.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wavelength: Multispectral Designs Accelerate Performance Gains

Near-infrared accounted for USD 1.32 billion of the infrared emitter and receiver market size in 2024, representing a 46.87% revenue share, thanks to its seamless integration with low-cost silicon CMOS detectors. Consumer electronics champions near-infrared for proximity sensing because of its lower power draw and mature driver-IC ecosystem. However, short-wave infrared revenue is on track to grow at a 6.07% CAGR to 2030, fueled by machine-vision and food-sorting lines that benefit from deeper material penetration and reduced atmospheric scattering.

Mid-wave infrared retains traction in gas-leak detection and military imaging, leveraging the 3-5 µm atmospheric window for long-range clarity. Long-wave infrared continues to serve building diagnostics and medical thermography. Automakers increasingly adopt dual-band designs, pairing near-infrared cabin monitors with long-wave external cameras in consolidated sensor modules. This multispectral pivot diversifies supplier revenue streams and anchors long-term demand for the infrared emitter and receiver market.

By Component: Detection Sensitivity Drives Receiver Uptake

Emitters delivered 61.79% of 2024 sales, underscoring their ubiquity in every active-sensing chain. VCSEL arrays, edge-emitting laser diodes, and high-power LEDs provide structured light, eye-safe ranging, and basic proximity cues across consumer and industrial devices. Yet receiver shipments are expanding at a 5.69% CAGR as end-users seek longer detection ranges and higher depth accuracy.

Photodiode suppliers are pushing quantum-efficiency improvements beyond 85%, while avalanche photodiodes deliver gain factors exceeding 100 for long-range lidar and surveillance applications. CMOS-based focal-plane arrays lower the cost per pixel, allowing handheld thermal cameras to retail for under USD 300. As signal processing moves on-chip, board real estate shrinks, allowing for novel form factors in smart glasses and wearables, which in turn bolsters the infrared emitter and receiver market.

By Technology: Laser-Diode Momentum Builds in Precision Domains

LEDs secured a 56.78% revenue share in 2024, favored for their low cost in flood illumination and general-purpose sensing. However, laser diodes are the fastest-growing technology at a 5.89% CAGR, driven by solid-state lidar, eye-safe ranging, and coherent-beam steering in industrial robotics. Photodiodes remain indispensable on the receive side, with new backside-illuminated designs doubling sensitivity in the 940 nm band.

Phototransistors, although niche, remain relevant in budget consumer goods that require on-device gain without the need for external amplifiers. CMOS sensors integrate multispectral capture alongside on-chip deep-learning accelerators, providing edge analytics that reduce system-level latency. The push toward single-chip depth-sensing modules reinforces a technology shift that is expected to sustain the infrared emitter and receiver market through 2030.

By Application: Automotive Gains While Consumer Electronics Consolidates

Consumer electronics retained the largest allocation in 2024, at 35.83% of global revenue, encompassing smartphone Face ID arrays, tablet gesture sensors, and laptop privacy detectors. The segment benefits from billion-unit annual volumes, lockstep design cycles, and rapid miniaturization. Automotive, however, is on track to outpace all other verticals with a 6.13% CAGR to 2030, as regulators mandate driver-attention monitoring and autonomous-driving stacks demand thermal redundancy.

Industrial automation represents a robust third pillar, employing infrared cameras for predictive maintenance and plastic-sorting robotics. In healthcare, non-contact thermometry and wound-healing assessment tools leverage long-wave arrays to avoid infection risks. Security and smart-city deployments employ multi-wavelength cameras for perimeter protection and traffic monitoring. Emerging smart-agriculture pilots in North America and Latin America trial crop-stress detection via short-wave imagers, foreshadowing an additional revenue flank for the infrared emitter and receiver market

Geography Analysis

The Asia Pacific captured 42.37% of global revenue in 2024, largely due to China, South Korea, and Taiwan hosting integrated foundries that fabricate emitters, detectors, and driver ICs under one roof. Smartphone OEM proximity to component vendors shortens design cycles and cuts logistics costs, reinforcing regional stickiness. Government subsidies in China’s “Made in China 2025” and South Korea’s “K-Semiconductor Belt” continue to draw investment into compound-semiconductor fabs that underpin the infrared emitter and receiver market.

North America and Europe remain technology leaders, emphasizing premium automotive safety, defense ISR, and Industry 4.0 deployments. U.S. demand benefits from public procurement of thermal imagers for border surveillance, while European automakers internalize cabin-monitoring sensors to meet 2024 safety mandates. Those regions face supply-chain vulnerabilities in gallium and indium, intensifying their push for reshoring or friendly-shoring initiatives.

The Middle East is the fastest-growing theater, with a 5.91% CAGR, anchored by Saudi Vision 2030 and the UAE's smart-city blueprints, which integrate infrared cameras for traffic-flow optimization and energy-efficient building management. South American agritech and mining companies deploy ruggedized short-wave imagers for crop stress analytics and equipment health monitoring. African uptake remains nascent, but policymakers' interest in infrastructure safety suggests a gradual rise through 2030. Together, these regional dynamics reinforce a diversified demand base for the infrared emitter and receiver market.

Competitive Landscape

The market exhibits moderate concentration, with the top five vendors collectively controlling approximately 55% of 2024 sales. OSRAM Opto Semiconductors, Hamamatsu Photonics, and Vishay Intertechnology anchor the high-end. Each invests heavily in vertically integrated compound-semiconductor lines, supporting moat-building through process know-how and patent depth. OSRAM’s Malaysia fab expansion is expected to lift automotive-grade LED output by 40% by 2026, thereby buffering OEMs against supply scarcity. Hamamatsu’s InfraTec acquisition broadens its European footprint in thermal arrays, while Vishay’s new VCSEL line directly targets lidar units for Level 3 autonomy.

Chinese challengers, such as II-VI Zhuhai, and South Korean entrants, like Seoul Semiconductor, harness lower labor costs and agile design cycles to capture price-sensitive consumer electronics wins. Western incumbents respond by offering full-stack reference designs that integrate optics, drivers, and firmware, thereby reducing customer time-to-market. Differentiation now pivots on power efficiency, miniaturized packages, and supply-chain resilience rather than pure sensor resolution.

Opportunities remain open in underserved niches, such as smart agriculture, space-based surveillance, and neurodiagnostic imaging. Players that can tailor wafer processes to exotic wavelengths or integrate AI edge-compute blocks stand to outpace sector averages. Continued M&A activity is likely as firms seek to plug capability gaps, as evidenced by Teledyne FLIR’s military-grade thermal-sensor contract, which leverages synergies between focal-plane design and system-level assembly.

Infrared Emitter And Receiver Industry Leaders

OSRAM Opto Semiconductors GmbH

Hamamatsu Photonics K.K.

Vishay Intertechnology, Inc.

Excelitas Technologies Corp.

LITE-ON Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Hamamatsu Photonics entered a USD 200 million partnership with BMW Group to co-develop short-wave infrared sensors for the automaker’s Level 4 autonomous platform, targeting commercial rollout in 2027 with stronger object recognition in poor weather.

- September 2025: OSRAM Opto Semiconductors secured a USD 180 million supply contract from Tesla to deliver 940 nm infrared LED arrays for the company’s full self-driving hardware upgrade, covering driver-monitoring and exterior pedestrian-detection functions.

- August 2025: Vishay Intertechnology completed its USD 320 million acquisition of French specialist Sofradir EC, adding cooled and uncooled thermal detector lines that expand its defense and industrial imaging portfolio.

- July 2025: Seoul Semiconductor introduced quantum-dot infrared LEDs that raise efficiency by 40% and lower production cost by 25%, with mass production scheduled for Q1 2026 after successful pilot runs with major smartphone manufacturers.

Global Infrared Emitter And Receiver Market Report Scope

| Near Infrared (NIR) |

| Short-Wave Infrared (SWIR) |

| Mid-Wave Infrared (MWIR) |

| Long-Wave Infrared (LWIR) |

| Infrared Emitters |

| Infrared Receivers |

| Infrared Light Emitting Diodes (IR-LEDs) |

| Infrared Laser Diodes |

| Photodiodes |

| Phototransistors |

| Complementary Metal-Oxide Semiconductor (CMOS) Sensors |

| Consumer Electronics |

| Automotive |

| Industrial Automation |

| Healthcare |

| Security and Surveillance |

| Other Application |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Wavelength | Near Infrared (NIR) | ||

| Short-Wave Infrared (SWIR) | |||

| Mid-Wave Infrared (MWIR) | |||

| Long-Wave Infrared (LWIR) | |||

| By Component | Infrared Emitters | ||

| Infrared Receivers | |||

| By Technology | Infrared Light Emitting Diodes (IR-LEDs) | ||

| Infrared Laser Diodes | |||

| Photodiodes | |||

| Phototransistors | |||

| Complementary Metal-Oxide Semiconductor (CMOS) Sensors | |||

| By Application | Consumer Electronics | ||

| Automotive | |||

| Industrial Automation | |||

| Healthcare | |||

| Security and Surveillance | |||

| Other Application | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the infrared emitter and receiver market?

The global market stood at USD 2.82 billion in 2025 and is projected to reach USD 3.66 billion by 2030.

Which segment is growing the fastest?

Automotive applications are expanding at a 6.13% CAGR through 2030, outpacing all other verticals.

Why are short-wave infrared sensors still expensive?

They require costly InGaAs substrates and suffer lower manufacturing yields, keeping unit prices high relative to silicon-based near-infrared detectors.

Which region dominates production?

Asia Pacific holds 42.37% of global revenue thanks to concentrated semiconductor manufacturing in China, South Korea, and Taiwan.

How are regulations affecting demand?

European mandates for driver-monitoring systems and emerging North American blind-spot rules are driving accelerated adoption of infrared cameras in vehicles.

What technological trend is reshaping product design?

The shift toward laser-based VCSEL arrays and on-chip AI processing is enabling thinner modules with lower power draw and faster depth-sensing capabilities.

Page last updated on: