Industrial Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

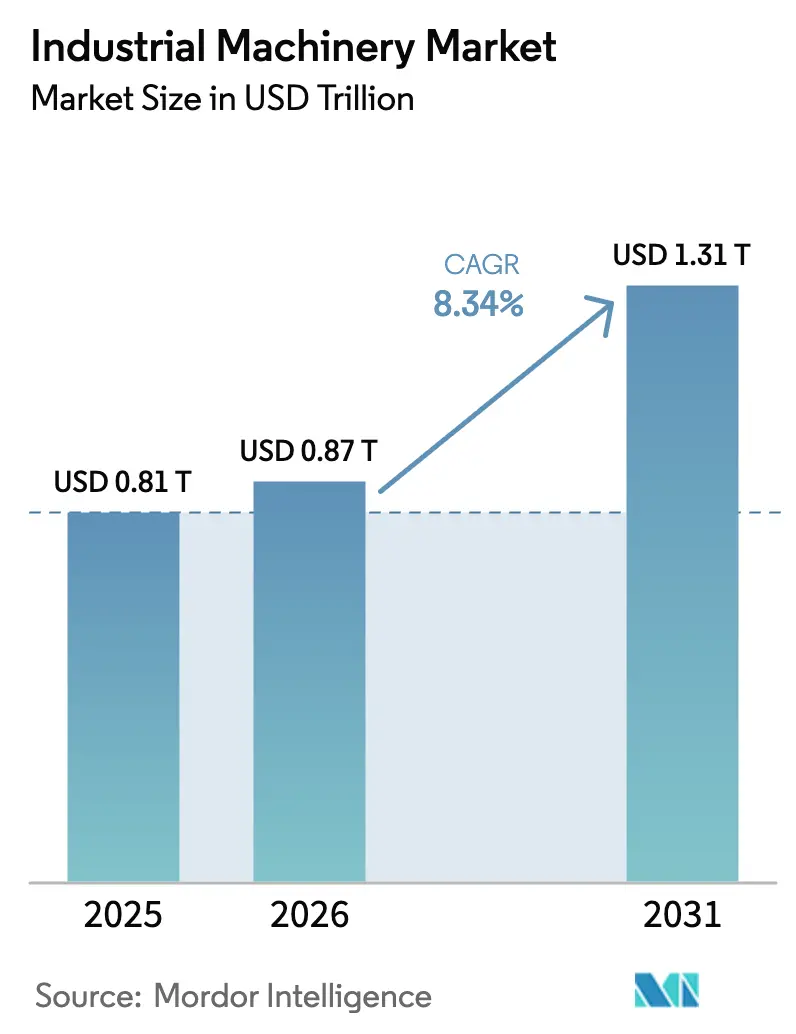

| Market Size (2026) | USD 0.87 Trillion |

| Market Size (2031) | USD 1.31 Trillion |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Machinery Market Analysis by Mordor Intelligence

The industrial machinery market size is projected to expand from USD 0.81 trillion in 2025 and USD 0.87 trillion in 2026 to USD 1.31 trillion by 2031, registering a CAGR of 8.34% between 2026 to 2031. The industrial machinery market is transitioning from one-off capital-equipment purchases toward modular retrofits that embed Industry 4.0 sensors, edge-computing gateways, and software-defined controls. Suppliers win orders by proving that their machinery can collect actionable data, enable outcome-based service contracts, and support predictive-maintenance programs that lower unplanned downtime. Demand is amplified by sustained infrastructure spending, reshoring incentives, and zero-emission mandates that accelerate the replacement of diesel platforms with electric or hybrid alternatives. Competitive dynamics favor vendors able to bundle financing, localized service networks, and interoperable software, a combination that resonates with cost-sensitive buyers across emerging economies.

Key Report Takeaways

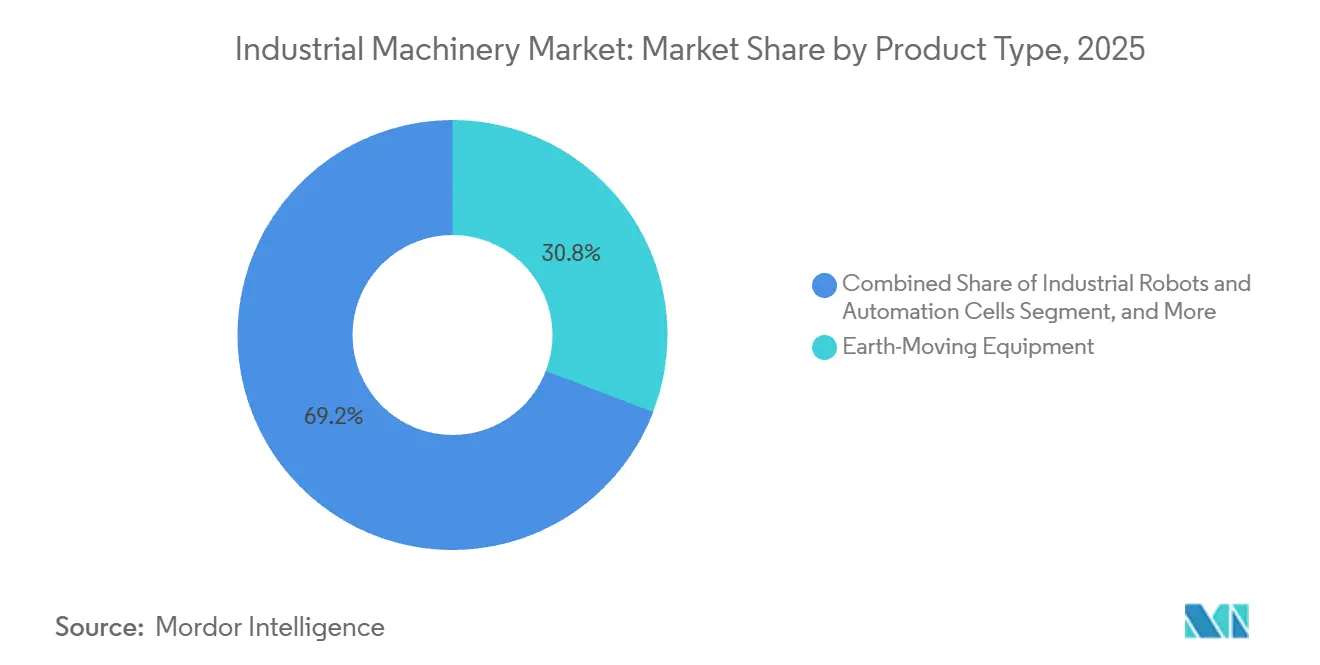

- By product type, earth-moving equipment held 30.84% of the industrial machinery market share in 2025, while robots and automation cells are projected to expand at a 9.43% CAGR through 2031.

- By application, construction and mining accounted for 32.63% of the industrial machinery market size in 2025, whereas pharmaceuticals are forecast to grow at a 10.63% CAGR between 2026 and 2031.

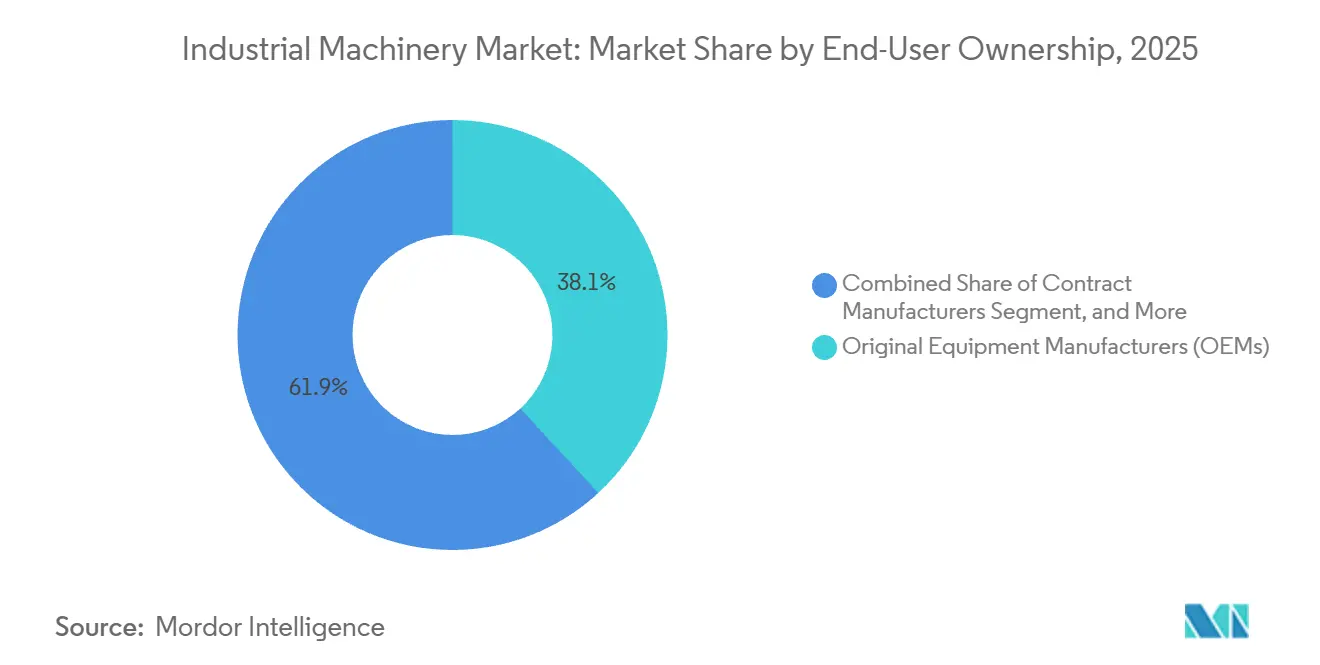

- By end-user ownership, original equipment manufacturers captured 38.14% of the industrial machinery market in 2025, yet contract manufacturers are advancing at a 9.76% CAGR through 2031.

- By automation level, semi-automated and CNC platforms led with 45.68% of the industrial machinery market share in 2025, but fully automated lights-out cells are progressing at a 9.59% CAGR over 2026-2031.

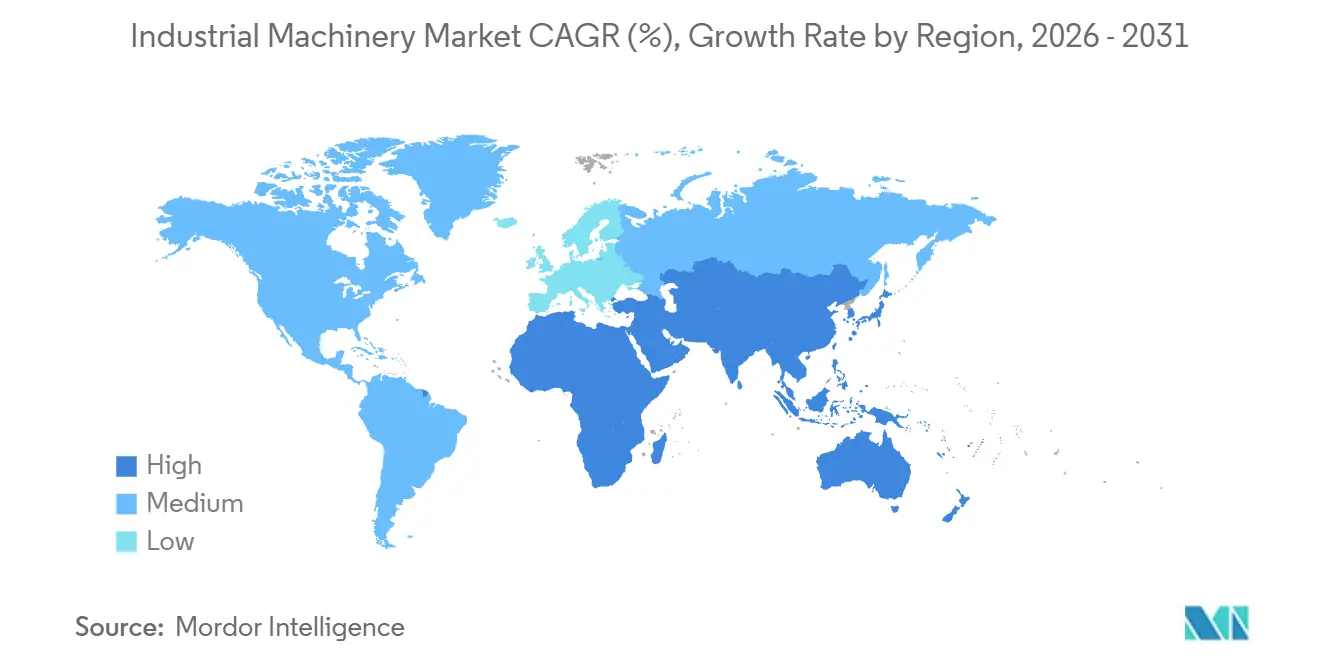

- By geography, Asia-Pacific commanded 40.56% of the industrial machinery market in 2025 and is rising at a 9.81% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of Industry 4.0-Ready Retrofits in Brownfield Facilities | +1.8% | Global, led by Europe and North America legacy plants | Medium term (2-4 years) |

| Construction Super-Cycle Fueled by Clean-Energy and Resilient Infrastructure Spend | +1.6% | North America, Middle East, Europe | Long term (≥ 4 years) |

| Shift Toward Outcome-Based, Predictive-Maintenance Service Contracts | +1.4% | Global, led by North America and Europe early adopters | Medium term (2-4 years) |

| Reshoring Drives Demand for Flexible, Multi-Process CNC Platforms | +1.2% | North America, Europe, spillover to Mexico and Eastern Europe | Medium term (2-4 years) |

| Rapid Uptake of Compact, Zero-Emission Machinery for Urban Retrofit Projects | +1.0% | Europe, Asia-Pacific urban centers, select North American cities | Short term (≤ 2 years) |

| Surge in Defense and Critical-Minerals CAPEX Elevates Heavy-Duty Equipment Orders | +0.9% | North America, Australia, select Middle East nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Industry 4.0-Ready Retrofits in Brownfield Facilities

Retrofitting legacy equipment now absorbs a growing share of automation budgets because installing edge gateways, wireless vibration sensors, and cloud connectors costs far less than replacing entire lines. ABB’s February 2025 purchase of Sevensense proved the value of drop-in navigation technology that works around fixed factory layouts.[1]ABB Ltd., “ABB Acquires Sevensense to Strengthen Autonomous Mobile Robotics Portfolio,” abb.com Roland Berger’s March 2025 outlook anticipates a V-shaped rebound from 2026 as manufacturers exhaust incremental efficiency gains and invest in digital twins to unlock new productivity plateaus.[2]Roland Berger, “Industrial Automation Outlook: V-Shaped Recovery 2026-2030,” rolandberger.com Suppliers differentiate by offering protocol-agnostic controllers that pull data from mixed-vintage assets, allowing plants to modernize without wholesale equipment swaps. The business case strengthens further when retrofits qualify for energy-efficiency tax credits and accelerate ISO 9001 compliance audits.

Construction Super-Cycle Fueled by Clean-Energy and Resilient Infrastructure Spend

Long-horizon commitments to grid upgrades, renewable-energy build-outs, and climate-resilient transport corridors sustain orders for excavators, cranes, and concrete pumps. The U.S. Infrastructure Investment and Jobs Act funnels billions into roads, bridges, and broadband while the European Union’s REPowerEU plan accelerates wind and solar installations.[3]U.S. Department of Transportation, “Infrastructure Investment and Jobs Act Overview,” transportation.gov Dealer inventories normalized in late 2025, enabling Caterpillar and peers to fulfill large earth-moving tenders without the delivery bottlenecks seen in 2024. Middle Eastern megaprojects deploy fleets of autonomous haul trucks that rely on GPS-guided grading systems, lifting demand for telematics and remote-operations software. The sheer scale and multi-year timelines of these projects give OEMs revenue visibility that justifies investments in electric and hydrogen-fuel-cell powertrains.

Shift Toward Outcome-Based, Predictive-Maintenance Service Contracts

Unscheduled downtime can cost operators USD 50,000-250,000 per hour, prompting a move from calendar-based maintenance to sensor-driven service. Platforms such as Honeywell Forge, Siemens MindSphere, and Sulzer BLUE BOX charge customers for guaranteed uptime rather than parts shipped. Cummins extended this logic to hydrogen fuel cells in 2024, embedding algorithms that flag failures a month in advance and auto-dispatch parts kits. Deloitte’s 2025 survey found that 62% of buyers now favor performance-guaranteed contracts, forcing OEMs to build data-science capabilities that support advanced analytics. ISO 55000 asset-management norms intensify the trend by formalizing total-cost-of-ownership metrics in procurement decisions.

Reshoring Drives Demand for Flexible, Multi-Process CNC Platforms

Supply-chain shocks and trade tensions motivate firms to relocate production closer to end-markets, yet higher labor costs oblige plants to rely on highly automated, quick-change machinery. The U.S. CHIPS and Science Act steers USD 52 billion toward domestic semiconductor fabs that need nanometer-precision CNC grinders.[4]U.S. Department of Commerce, “CHIPS and Science Act Implementation,” commerce.gov European machine-tool builders logged a 14% order jump in early 2025 as automotive suppliers reshored battery-pack assembly lines. Open-architecture controllers that integrate with enterprise resource planning systems enable just-in-time workflows without bloated inventories. Vendors offering modular tool heads and additive-manufacturing attachments gain an edge because they consolidate multiple machining steps into a single platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital-Expenditure and Long Payback Horizons for Advanced Automation | -1.1% | Global, acute in small and medium enterprises | Short term (≤ 2 years) |

| Volatile Raw-Material Pricing Compresses OEM Margins and Buyer Budgets | -0.9% | Global, stronger where steel and copper are imported | Short term (≤ 2 years) |

| Acute Skilled-Labor Shortage for Smart-Machine Programming and Service | -0.8% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Cyber-Security Vulnerabilities in Connected, OT-IT Converged Equipment | -0.7% | Global, heightened in critical-infrastructure sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital-Expenditure and Long Payback Horizons for Advanced Automation

Fully automated cells often cost USD 2-10 million with payback periods of five to seven years once integration, training, and licenses are considered. Elevated interest rates in 2025 deterred many small and medium enterprises from signing multi-year lease or purchase agreements. Roland Berger’s March 2025 analysis confirmed that mid-tier manufacturers deferred automation, awaiting clearer demand before drawing down credit lines. Equipment-as-a-service contracts ease cash-flow pressure but carry higher effective financing costs and restrictive covenants. Sectors with low operating margins, such as food processing and textiles, feel the squeeze most acutely, prolonging reliance on semi-manual processes.

Volatile Raw-Material Pricing Compresses OEM Margins and Buyer Budgets

Steel and copper swung 20-30% in 2025, squeezing gross margins by as much as 200 basis points for machinery builders that locked in fixed-price contracts. Reuters reported that several OEMs passed surcharges downstream, prompting buyers to delay orders or downgrade to smaller-capacity units. Caterpillar renegotiated supplier contracts and explored alternative alloys to contain costs, yet uncertainty still ripples through quoting cycles. Reduced batch sizes undermine economies of scale, elevating unit costs and further pressuring demand. The feedback loop dampens capex appetites, particularly in emerging markets dependent on imported metals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robots And Automation Cells Outpace Legacy Categories

Robots and automation cells are projected to grow at 9.43% over 2026-2031, the fastest rate among product classes, as manufacturers automate welding, assembly, and quality-inspection workflows. The industrial machinery market size for robots benefited from 542,000 installations in 2024 and forecasts surpassing 700,000 units by 2028, underpinned by automotive, electronics, and pharmaceutical demand. Earth-moving equipment remained the leader with a 30.84% share in 2025, sustained by long-duration infrastructure projects and resilient-infrastructure mandates. Material-handling systems such as automated guided vehicles ride the wave of e-commerce warehouse expansion, where multilevel fulfillment centers require vertical lift modules and conveyor arrays. Agricultural machinery growth is more cyclical because unit sales still hinge on commodity price swings, although precision-farming upgrades add software-driven value to combines and tractors.

Localization reshapes competitive hierarchies inside the industrial machinery market as Chinese producers climb the technology curve, capturing 57% of domestic robot demand by bundling financing and localized spares. Established Japanese and European makers respond with advanced vision packages, force-torque sensors, and ISO/TS 15066 compliant safety functions. Meanwhile, the line between metal-cutting tools and additive-manufacturing systems blurs, since modern CNC centers integrate powder-bed or directed-energy deposition heads. Hybrid platforms promise shorter cycle times and less material waste, yet their adoption depends on certification pathways that validate mechanical properties for aerospace and medical parts. Across categories, buyers gravitate toward machines that output standardized data, making software interoperability a decisive procurement criterion.

By Application Industry: Pharmaceuticals Lead, Construction Anchors Volume

Construction and mining commanded 32.63% of the industrial machinery market in 2025 thanks to road, rail, and renewable-energy megaprojects that require large excavators, cranes, and pumps. In contrast, pharmaceuticals are forecast to expand at 10.63% between 2026 and 2031 as continuous-manufacturing lines, single-use bioreactors, and real-time quality analytics become regulatory expectations. The U.S. FDA’s December 2025 strategy framework validated digital production methods, unlocking budgets for automated fill-finish cells and isolator systems that minimize human contact. Food and beverage processors also accelerate automation to reduce contamination risk and manage broad product portfolios that include plant-based proteins. Automotive OEMs reconfigure body shops for electric-vehicle platforms, spurring demand for flexible welding robots that can switch between steel and aluminum without lengthy retooling.

Chemical processing and power generation primarily fund retrofit programs because many assets have 20-year lifecycles, making incremental upgrades to pumps, valves, and control systems more economical than wholesale replacement. Aerospace, electronics, and general fabrication contribute steady baseline demand yet fluctuate with sector-specific cycles such as aircraft order backlogs or consumer-device refresh rates. Across every vertical, corporate sustainability targets drive preference for machinery that supports low-energy operation, closed-loop cooling, and predictive maintenance that prevents material waste. Suppliers that document life-cycle emissions gain an edge as customers prepare for emerging scope-3 reporting obligations under global climate-disclosure rules.

By End-User Ownership: Contract Manufacturers Gain Share

Original equipment manufacturers held 38.14% of the industrial machinery market in 2025, reflecting centuries-old practices of vertically integrated production. Contract manufacturers, however, are projected to grow at a 9.76% CAGR toward 2031 as brand owners outsource capital-intensive and compliance-heavy operations. These partners amortize robotic cells, cleanrooms, and quality-management certifications across multiple clients, lowering per-unit costs and accelerating time-to-market. Rental and leasing firms widen access by converting capex into opex, a model attractive to buyers uncertain about technology obsolescence cycles. Government and municipal entities remain a stable but smaller customer group because procurement hinges on multiyear budget approvals and competitive tendering.

Equipment-as-a-service contracts blur traditional ownership definitions because manufacturers retain asset title and invoice based on hours run or units produced. This model aligns supplier incentives with uptime but forces OEMs to manage residual-value risk and fund larger balance sheets. Vendors respond by embedding telematics that track utilization, condition, and environmental exposure, data points that support dynamic residual-value calculations. Contract manufacturers leverage similar analytics to optimize machine scheduling across client workloads, improving overall asset-turn ratios. As a result, finance teams increasingly influence machinery selection, evaluating total-life-cycle economics alongside technical fit.

By Automation Level: Lights-Out Cells Gain Ground

Semi-automated and CNC platforms dominated with 45.68% of the industrial machinery market share in 2025 because they balance productivity with human oversight for complex tasks and quality inspections. Fully automated lights-out cells are forecast to climb at 9.59% over 2026-2031 as pharmaceuticals, food processors, and electronics assemblers target contamination control, labor cost reduction, and 24-hour runtime. Collaborative robots that meet ISO/TS 15066 safety thresholds accelerate adoption by enabling phased automation without extensive safeguarding investments. Even manually operated machines integrate bolt-on digital readouts and IoT sensors, creating a continuum rather than a binary divide between manual and automated operations.

Achieving true lights-out production requires more than robotics; it demands robust process control, predictive-maintenance routines, and remote diagnostics to prevent downtime during unattended shifts. Vendors that package machinery, software, and field service into unified platforms capture premium pricing because customers value single-throat-to-choke accountability. Hybrid cells, where robots handle repetitive steps and technicians oversee changeovers and troubleshooting, remain the dominant model in high-mix, low-volume facilities. In developing markets, the cost of full automation still exceeds labor savings, but rising wages and safety regulations drive incremental upgrades that pave the way for gradual adoption. Across all automation levels, interoperability with enterprise systems assures end-users that data generated on the shop floor informs planning, quality, and supply-chain decisions.

Geography Analysis

Asia-Pacific controlled 40.56% of the industrial machinery market in 2025 and is advancing at a 9.81% CAGR through 2031, propelled by China’s domestic robot surge and infrastructure build-outs across India, Vietnam, and Indonesia. China installed 295,000 robots in 2024, representing 54% of global volume, as local firms such as SANY and XCMG bundled financing, after-sales support, and spare-parts logistics into turnkey packages. India reported 9,100 installations in 2024 as production-linked incentives stimulated electronics and automotive investments. Japan and South Korea maintain leadership in precision machinery and hydrogen-ready construction equipment, while Thailand attracts smart-agriculture investment exemplified by Kubota’s October 2025 R and D center. Southeast Asian governments courting supply-chain diversification deploy mid-tier automation solutions that bridge labor-cost advantages with quality-control expectations.

North America and Europe exhibit slower but sizable growth, underwritten by reshoring legislation, climate-aligned infrastructure projects, and stringent emissions rules. The U.S. CHIPS and Science Act and Infrastructure Investment and Jobs Act funnel more than USD 100 billion toward fabs and transport systems, driving orders for ultra-precision machine tools and electric excavators. Komatsu’s USD 285 million Chattanooga expansion shows suppliers localizing production to satisfy rapid service demands and Buy-America provisions. European Union carbon targets accelerate the shift to electric compact loaders and hybrid excavators, favoring OEMs with reverse-logistics networks that enable remanufacturing. Eastern Europe gains manufacturing share as labor-intensive assembly migrates from higher-cost Western states, spurring demand for flexible CNC machinery that supports quick model changeovers.

The Middle East and Africa present bifurcated prospects. Gulf states channel oil revenues into autonomous haul trucks and crawler cranes for renewable-energy parks, while sub-Saharan buyers rely on refurbished equipment because financing and service infrastructure remain thin. South America faces macro-volatility, yet Brazil’s large soybean and corn operations sustain demand for high-capacity combines and precision planters. CNH Industrial’s acquisition of Raven Industries bolsters its ability to deliver variable-rate and automated-steering solutions to growers seeking input-cost efficiencies. Across all regions, procurement decisions converge on machinery that captures operational data, enabling predictive maintenance and granular cost analytics once unattainable with analog systems.

Competitive Landscape

The industrial machinery market is fragmented. Western incumbents such as Caterpillar, Komatsu, Deere, and Volvo Construction Equipment defend margins by bundling equipment, telematics, and outcome-based service packages that guarantee uptime. Chinese manufacturers, including SANY, XCMG, and Zoomlion, gain ground by integrating financing and local parts hubs into single contracts that lower total-cost-of-ownership for cost-sensitive buyers in Southeast Asia and Africa. CMBI estimated that domestic suppliers now command 57% of China’s industrial-robot segment, reflecting successful localization strategies.

Strategic differentiation increasingly hinges on software and analytics. ABB’s Sevensense acquisition enhanced autonomous mobile robot navigation, illustrating the pivot from mechanical to digital IP. Patent trends highlight growth in predictive-maintenance algorithms and digital-twin simulations as equipment becomes data-centric. IEC’s acceleration of 62443 cybersecurity standards raises entry barriers by requiring embedded security operations capabilities. Mid-tier automation integrators find opportunity in retrofits that upgrade legacy CNC machines with open-architecture controllers, delivering sub-three-year paybacks that appeal to small and medium enterprises unable to fund full replacements.

Investment announcements underscore the race toward electrification and localization. Komatsu pledged USD 285 million to expand electric excavator production in Tennessee, Hitachi signed a USD 150 million autonomous-haul-truck deal in Australia, and AGCO launched its first fully electric compact tractor for European vineyards. Liebherr’s Dubai parts hub improves response times on fast-track Gulf megaprojects, while Sandvik’s precision-grinding acquisition positions it for semiconductor and medical tooling demand. Collectively, these moves reveal an industry balancing legacy mechanical expertise with digital, electric, and service-driven growth levers.

Industrial Machinery Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Deere & Company

Hitachi Construction Machinery Co., Ltd.

CNH Industrial N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Hitachi Construction Machinery secured a USD 150 million contract to supply autonomous haul trucks across three Australian iron-ore mines, including telematics and predictive-maintenance services.

- January 2026: Komatsu committed USD 285 million to expand its Chattanooga, Tennessee plant for electric excavators and hybrid wheel loaders, creating 400 new jobs by 2027.

- January 2026: AGCO launched the Fendt e100 Vario, a fully electric compact tractor for European vineyards and orchards, offering 4-6 hours of runtime on a 100 kWh battery.

- December 2025: The U.S. FDA published a strategic framework encouraging continuous manufacturing and real-time quality analytics in pharmaceuticals, catalyzing automation investments.

Global Industrial Machinery Market Report Scope

Industrial machinery encompasses the heavy equipment, tools, and devices employed across various sectors, including manufacturing, construction, agriculture, and mining. These machines are engineered for intricate, large-scale operations, demanding substantial power, precision, and automation.

The Industrial Machinery Market Report is Segmented by Product Type (Earth-Moving Equipment, Material-Handling Equipment, Agricultural Machinery, Industrial Robots and Automation Cells, and Other Product Types), Application Industry (Construction and Mining, Chemical, Automotive, Food and Beverage, Pharmaceuticals, Power Generation, and Other Application Industries), End-User Ownership (Original Equipment Manufacturers, Contract Manufacturers, Rental and Leasing Companies, and Government and Municipalities), Automation Level (Conventional Manually-Operated, Semi-Automated/CNC, and Fully-Automated/Lights-Out Cells), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Earth-Moving Equipment |

| Material-Handling Equipment |

| Agricultural Machinery |

| Industrial Robots and Automation Cells |

| Other Product Types |

| Construction and Mining |

| Chemical |

| Automotive |

| Food and Beverage |

| Pharmaceuticals |

| Power Generation |

| Other Application Industries |

| Original Equipment Manufacturers (OEMs) |

| Contract Manufacturers |

| Rental and Leasing Companies |

| Government and Municipalities |

| Conventional Manually-Operated |

| Semi-Automated / CNC |

| Fully-Automated / Lights-Out Cells |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Product Type | Earth-Moving Equipment | ||

| Material-Handling Equipment | |||

| Agricultural Machinery | |||

| Industrial Robots and Automation Cells | |||

| Other Product Types | |||

| By Application Industry | Construction and Mining | ||

| Chemical | |||

| Automotive | |||

| Food and Beverage | |||

| Pharmaceuticals | |||

| Power Generation | |||

| Other Application Industries | |||

| By End-User Ownership | Original Equipment Manufacturers (OEMs) | ||

| Contract Manufacturers | |||

| Rental and Leasing Companies | |||

| Government and Municipalities | |||

| By Automation Level | Conventional Manually-Operated | ||

| Semi-Automated / CNC | |||

| Fully-Automated / Lights-Out Cells | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue trajectory is expected for the industrial machinery market between 2026 and 2031?

The industrial machinery market size is forecast to move from USD 0.87 trillion in 2026 to USD 1.31 trillion by 2031, reflecting an 8.34% CAGR.

Which region is likely to contribute the most incremental sales through 2031?

Asia-Pacific is projected to add the largest incremental value, growing at a 9.81% CAGR on top of its 40.56% base-year share.

Which product class is set for the fastest unit growth?

Robots and automation cells lead with a projected 9.43% CAGR to 2031 as factories automate welding, assembly, and inspection tasks.

Why are contract manufacturers expanding faster than OEMs?

Brand owners outsource capex-intensive production, allowing contract manufacturers to spread robotic and cleanroom investments across multiple clients, driving a 9.76% CAGR.

What is driving demand for fully automated lights-out cells?

Pharmaceuticals, food and beverage, and electronics firms seek contamination control and labor-cost relief, supporting a 9.59% CAGR for lights-out automation.

How are raw-material swings influencing machinery budgets?

Steel and copper volatility cut OEM margins by up to 200 basis points in 2025, prompting price surcharges and delaying some purchase decisions.

Page last updated on: