Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 338.46 Billion |

| Market Size (2031) | USD 505.88 Billion |

| Growth Rate (2026 - 2031) | 8.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

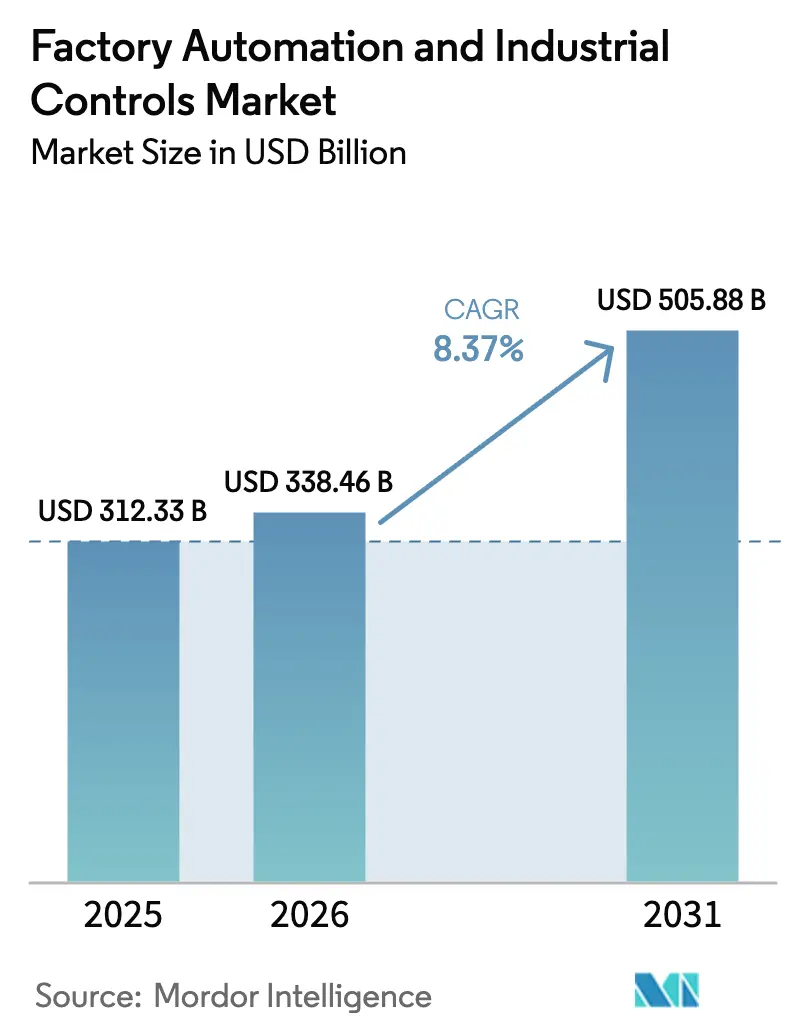

The Factory Automation And Industrial Controls Market size is expected to increase from USD 312.33 billion in 2025 to USD 338.46 billion in 2026 and reach USD 505.88 billion by 2031, growing at a CAGR of 8.37% over 2026-2031. Momentum is shifting from isolated task automation toward data-driven, cyber-physical production lines that enable real-time optimization and quicker product changeovers. Edge-based inference is expanding as the European Union and China mandate on-device artificial intelligence, lifting demand for high-performance controllers and deterministic networking. Labor shortages in Germany and Japan are accelerating investments in collaborative robots and vision systems, shortening historical replacement cycles. Meanwhile, strict energy-efficiency rules, escalating electricity prices, and dual-carbon commitments are compelling manufacturers to upgrade variable-frequency drives, IE4 motors, and intelligent power management platforms. Heightened cyber risks round out the growth equation, steering capital toward secure-by-design controllers that meet IEC 62443 guidelines.

Key Report Takeaways

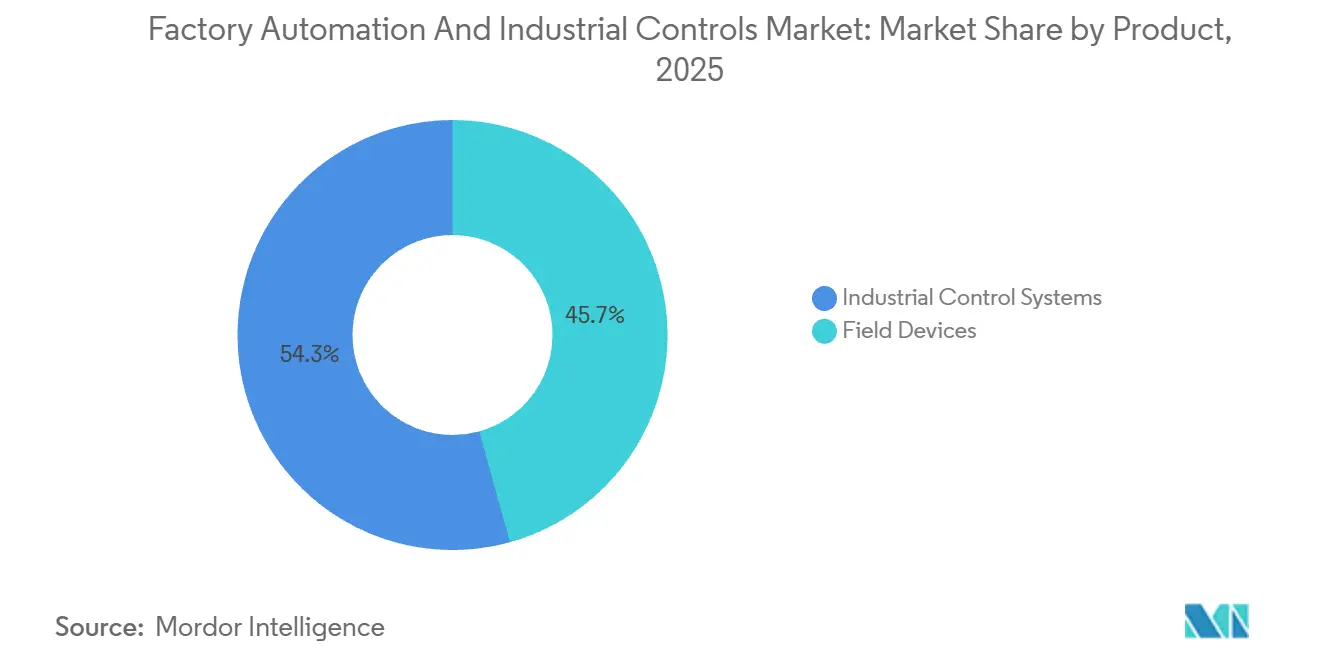

- By product category, industrial control systems held 54.31% of the factory automation and industrial controls market share in 2025, while field devices are forecast to expand at a 9.71% CAGR to 2031.

- By component, hardware accounted for 68.17% of the factory automation and industrial controls market in 2025, and software is advancing at a 10.93% CAGR through 2031.

- By end-user industry, automotive manufacturing led with 23.76% revenue share in 2025; pharmaceuticals are projected to record the highest CAGR at 9.43% through 2031.

- By control system architecture, proprietary ecosystems commanded a 49.54% share in 2025, whereas open and interoperable architectures are poised for a 10.21% CAGR to 2031.

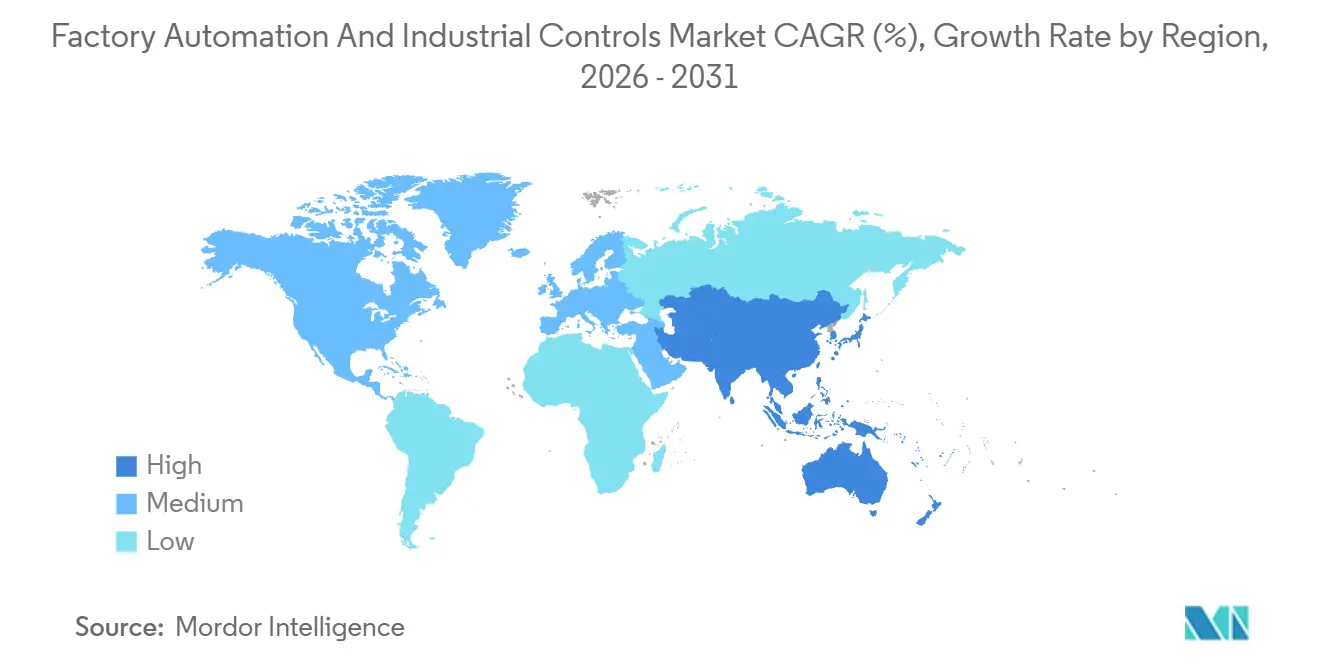

- By geography, Asia Pacific captured 37.68% share of the factory automation and industrial controls market in 2025 and is expected to grow at a 9.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 Adoption Acceleration | +2.1% | Germany, Japan, South Korea, United States | Medium term (2-4 years) |

| Energy-Efficiency Mandates and Cost Pressure | +1.4% | Europe, North America, China | Long term (≥ 4 years) |

| Rising Labor Shortages in Manufacturing | +1.8% | Japan, Germany, United States, Southeast Asia | Short term (≤ 2 years) |

| Government Stimulus for Digital Factories | +1.3% | China, India, Singapore, United States | Medium term (2-4 years) |

| Low-Code / No-Code Automation Platforms | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| AI-Driven Predictive Quality Control Upgrades | +1.2% | Germany, United States, China, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 Adoption Acceleration

Manufacturers are converting legacy “automation islands” into synchronized cyber-physical ecosystems that link machines, logistics, and quality loops in real time, yielding shorter changeovers and higher overall equipment effectiveness. Digital-twin deployments jumped to 68% of surveyed German plants in 2025, up from 41% two years earlier, with typical payback falling below 18 months. Japan budgeted JPY 120 billion (USD 800 million) in grants for small and midsized enterprises to install collaborative robots and IoT sensors, expanding automation beyond mega-plants. The emphasis on retrofit projects is stimulating demand for modular edge gateways, time-sensitive networking, and protocol-agnostic controllers capable of coexisting with 20-year-old equipment. As a result, capital spending is spreading across thousands of mid-tier facilities, cementing a broad, sustainable growth path for the factory automation and industrial controls market.

Energy-Efficiency Mandates and Cost Pressure

The European Union’s Ecodesign Regulation 2024/1781 and updated United States motor standards are pressing manufacturers to adopt IE4-IE5 motors, variable-frequency drives, and advanced power analytics, reducing electricity use by 15-25%. Average industrial power prices in Europe reached EUR 0.28 per kWh (USD 0.30 per kWh) in 2024, more than double pre-2022 levels, putting energy optimization at the center of board-level discussions.[1]Eurostat, “Electricity Price Statistics,” ec.europa.eu Automation vendors are translating the regulations into commercial traction; Schneider Electric reported a 22% rise in EcoStruxure-enabled drives in 2025 as customers raced to certify plants under ISO 50001. The replacement wave is especially strong in energy-intensive segments such as chemicals and metals, lifting recurring software revenue tied to energy dashboards and AI-based load balancing. These factors add durable lift to the factory automation and industrial controls market.

Rising Labor Shortages in Manufacturing

Japan’s manufacturing workforce shrank by 1.2 million between 2019 and 2024, pushing the average factory-floor age to 47 years. German plants faced 320,000 unfilled jobs in 2024, mostly in machining and quality inspection roles. To sustain production, automotive suppliers grew collaborative-robot fleets by more than one-third in 2024, placing flexible cobots alongside human teams on tasks that demand dexterity but little oversight. Autonomous mobile robots, machine vision, and adaptive grippers that can migrate across lines are displacing fixed-path capital. The structural nature of labor shortages elevates the value proposition from cost reduction to business continuity, ensuring multiyear demand for field devices within the factory automation and industrial controls market.

Government Stimulus for Digital Factories

Capital subsidies are removing financial friction from automation projects. The United States CHIPS and Science Act earmarked USD 39 billion in grants and USD 75 billion in loan guarantees, contingent on real-time monitoring and predictive maintenance integration.[2]U.S. Department of Commerce, “CHIPS Act Funding,” commerce.gov India disbursed INR 45 billion (USD 540 million) to pharmaceutical manufacturers installing automated bioreactors and continuous plants. China’s dual-circulation policy boosted domestic PLC shipments by 28% in 2024 as firms localized control technology. These programs reward measurable productivity gains, steering adopters toward software-defined architectures that can be upgraded over the air. Subsidies therefore act as both demand accelerator and technology roadmap catalyst, reinforcing long-term expansion of the factory automation and industrial controls market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX of Automation Projects | -1.6% | Global, especially South America, Africa, Southeast Asia | Short term (≤ 2 years) |

| Cyber-Security Vulnerabilities in OT Networks | -0.8% | North America, Europe, global critical infrastructure | Medium term (2-4 years) |

| Fragmented Interoperability Standards | -0.7% | Global, multi-vendor brownfield sites | Long term (≥ 4 years) |

| Semiconductor Supply Volatility for Controllers | -1.1% | Global, severe in automotive and electronics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX of Automation Projects

Integrated MES-SCADA deployments often require USD 2-8 million per site, with paybacks exceeding three years in thin-margin sectors such as food processing. Access to low-cost financing is uneven, particularly in South America and parts of Southeast Asia where interest rates remain above 12%. Although leasing and automation-as-a-service models promise lower entry hurdles, customers remain wary of data ownership and long lifecycle dependencies. ABB disclosed that subscription-based robotics accounted for only 9% of its 2025 robotics revenue, underscoring the early stage of alternative financing. Consequently, capital constraints could dampen near-term adoption across smaller manufacturers, trimming growth of the factory automation and industrial controls market.

Cyber-Security Vulnerabilities in OT Networks

Forty-seven vulnerability advisories targeted SCADA and HMI products in 2024, including flaws in popular platforms that enable remote code execution. A ransomware assault on a European chemical plant halted output for 11 days and cost EUR 35 million (USD 38 million) in damages. Uptake of zero-trust segmentation remains below one-third of manufacturers, keeping the attack surface wide. Compliance with IEC 62443 can add 8-12% to total project cost, elongating approval cycles. Until secure-by-design controllers and encrypted protocols become standard, cybersecurity anxieties will curb speed of adoption in critical infrastructure segments, tempering expansion of the factory automation and industrial controls market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Field Devices Sustain Double-Digit Expansion

Field devices are expected to be the fastest-growing product category over the forecast period and are set to expand at 9.71% through 2031, outpacing industrial control systems that held 54.31% of the factory automation and industrial controls market share in 2025. Robot installations reached 553,000 units in 2024, with automotive and electronics buyers taking 62% of shipments. Machine-vision revenue climbed 18% at Cognex during 2024 on the strength of AI-powered defect detection. These investments illustrate an industry pivot from programmable logic controllers toward intelligent endpoints that carry local analytics and 5G or IO-Link Wireless connectivity.

This transition reshapes value propositions. Controller differentiation now turns on ecosystem compatibility and software toolchains rather than scan-time benchmarks. Human-machine interfaces add augmented-reality overlays that cut batch changeovers by up to 30% in mid-volume lines. Hybrid control architectures mix deterministic PLC loops with cloud analytics, sidestepping full rip-and-replace costs. As older SCADA systems approach obsolescence, upgrade discussions increasingly center on seamless migration paths instead of pure hardware refresh, anchoring multi-cycle revenue for the factory automation and industrial controls market.

By Component: Software Captures a Growing Slice

Hardware still represented 68.17% of revenue in 2025, yet software is projected to rise at a 10.93% clip, the highest among components. Subscription models now dominate rollouts, illustrated by Siemens, whose MindSphere and Xcelerator portfolios drove 16% software growth in 2025 while hardware rose only 4%. Emerson’s recurring software topped 22% of automation sales in 2024, delivering gross margins above 70%, versus the mid-30% range for hardware.

Low-code configuration tools such as EcoStruxure Automation Expert 2.0 reduce engineering hours by up to half, broadening user bases to process engineers and operations managers. Services revenue, long dominated by on-site commissioning, is shifting toward remote diagnostics and AI-assisted troubleshooting, which lowers travel costs and carbon footprints. Collectively, these dynamics deepen software’s pull-through effect on controllers and drives, reinforcing hybrid platform strategies across the factory automation and industrial controls market.

By End-User Industry: Pharmaceuticals Pace the Upswing

Automotive lines maintained 23.76% of 2025 revenue, reflecting long-standing automation density. The pharmaceutical segment, however, is forecast to expand at 9.43% through 2031, buoyed by continuous bioprocessing, real-time release testing, and stringent FDA guidance on process analytical technology.[3]U.S. Food and Drug Administration, “Process Analytical Technology Guidance 2024,” fda.gov Eli Lilly allocated USD 4.5 billion in 2024 to a fully automated biologics campus that employs digital twins and inline chromatography to trim batch cycles by 40%.

Beyond life sciences, chemical complexes are layering advanced process control onto legacy distributed control systems to shave energy costs amid volatile natural-gas prices. Food-and-beverage processors deploy wash-down-rated robotics to meet traceability mandates, while semiconductor fabs demand vacuum-compatible motion systems with sub-micron accuracy. The spread of sector-specific templates and validated libraries allows vendors to reuse code across plants, curbing commissioning risk and amplifying addressable scope inside the factory automation and industrial controls market.

By Control System Architecture: Open Standards Progress Rapidly

Proprietary architectures still accounted for 49.54% of revenue in 2025, yet open frameworks built on OPC Unified Architecture are slated for a 10.21% CAGR through 2031. The OPC Foundation certified more than 15,000 OPC UA server implementations by late 2024, a testament to rising multi-vendor integration. Volkswagen now mandates OPC UA compliance for all new production assets, driving ripple effects across tier-1 suppliers.

Hybrid arrangements that embed proprietary safety loops but expose non-time-critical data through open middleware balance determinism with flexibility. While integration overhead persists, the ability to deploy best-of-breed robots, sensors, and analytics outweighs the cost for most greenfield projects. Accordingly, ecosystem alignment rather than hardware speeds will determine winners in the factory automation and industrial controls market.

Geography Analysis

Asia Pacific accounted for 37.68% of the factory automation and industrial controls market in 2025 and is projected to post a 9.56% CAGR through 2031, underscoring its dual role as a manufacturing hub and policy engine. China’s dual-circulation push triggered a 28% rise in domestic PLC and drive shipments in 2024 as producers localized supply chains. India disbursed INR 120 billion (USD 1.44 billion) in production-linked incentives for electronics, pharmaceuticals, and auto components, subject to minimum automation thresholds. Japan granted JPY 120 billion (USD 800 million) to small and mid-sized enterprises to support robot adoption, extending automation beyond the automotive nucleus. South Korea sponsored 3,200 smart-factory projects in 2024, spanning semiconductor, display, and battery facilities.

North America remains pivotal despite slower growth, powered by federal incentives that tether funding to Industry 4.0 practices. The CHIPS Act’s USD 39 billion grant pool obliges real-time monitoring and predictive maintenance in new fabs. Mexico and Canada are benefiting via near-shoring, funneling orders to motion-control suppliers. Europe commands mature penetration yet maintains leadership in digital twins and energy-efficient retrofits; 68% of surveyed German plants had adopted at least one digital-twin application by 2025. High power prices propel upgrades to IE5 motors and drives, reinforcing refresh velocity.

South America, the Middle East, and Africa collectively trail in spending but register strong point projects tied to extractive industries. Brazil’s Petrobras earmarked USD 2.1 billion for digital oilfield platforms in 2024, including autonomous drilling and SCADA upgrades. Gulf refineries adopt advanced process control to meet energy-intensity targets, while South African miners deploy wireless sensor networks to improve asset uptime. Although volumes are smaller, the installed base is younger, providing an opening for open-standard architectures and cloud-native analytics to leapfrog legacy solutions. Collectively, geographic diversification underpins a resilient trajectory for the factory automation and industrial controls market.

Competitive Landscape

The factory automation and industrial controls market is moderately concentrated; the top ten suppliers account for roughly 55-60% of global revenue. No company exceeds 12% share, reflecting the domain’s sweep across discrete and process industries, hardware, software, and services. Siemens, ABB, Rockwell Automation, and Schneider Electric are leveraging installed bases to pivot toward high-margin software, even as Chinese peers such as Hollysys and Delta Electronics offer comparable PLCs at 30-40% lower prices. Emerson’s USD 8.2 billion acquisition of NI in 2024 tied laboratory test to plant-floor optimization, illustrating vertical integration into data and AI layers.

Younger entrants challenge incumbents with API-first platforms. Beckhoff’s PC-based controllers run on x86 processors under real-time Linux, winning orders in packaging cells that value computational headroom over proprietary chipsets. Certification of 1,200-plus OPC UA products lowers switching costs and boosts multi-vendor ecosystems.[4]OPC Foundation, “Product Certification Database,” opcfoundation.org Patent filings underscore the shift toward software; Siemens registered 87 AI-related automation patents in 2024, compared with 52 security-focused filings at Rockwell Automation.

Strategic differentiation now tilts to breadth of ecosystem, cloud partnerships, and domain templates rather than sheer hardware performance. Vendors that fail to supply end-to-end lifecycle solutions risk relegation to component suppliers. Conversely, firms able to unite edge devices, AI, cybersecurity, and lifecycle services are best positioned to command premium pricing and sticky recurring revenue inside the factory automation and industrial controls market.

Factory Automation And Industrial Controls Industry Leaders

ABB Limited

Siemens AG

Rockwell Automation Inc.

Schneider Electric SE

Mitsubishi Electric Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Siemens announced a EUR 1.2 billion (USD 1.3 billion) expansion of its Amberg Electronics Plant to produce edge controllers and industrial PCs, aiming for a 30% lead-time reduction by 2027.

- November 2025: ABB closed its EUR 180 million (USD 195 million) purchase of ASTI Mobile Robotics, adding autonomous mobile robots to its intralogistics lineup.

- October 2024: Rockwell Automation and Microsoft formed a partnership to fuse FactoryTalk with Azure AI, targeting USD 500 million in joint bookings by 2027.

- September 2024: Schneider Electric launched EcoStruxure Automation Expert 2.0, a software-defined platform that deploys IEC 61499 logic on third-party hardware.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global factory automation and industrial controls market as the aggregate revenue generated from hardware, software, and services that sense, command, and optimize manufacturing or process equipment. In scope are programmable logic controllers, distributed control systems, SCADA, HMI, industrial PCs, drives, motors, robots, machine-vision systems, sensors, manufacturing execution software, and the associated engineering and maintenance services deployed across discrete and process industries.

Scope exclusions: We deliberately leave out standalone enterprise IT platforms, non-industrial building automation, and aftermarket repair parts.

Segmentation Overview

- By Product

- Industrial Control Systems

- Distributed Control System (DCS)

- Programmable Logic Controller (PLC)

- Supervisory Control and Data Acquisition (SCADA)

- Product Lifecycle Management (PLM)

- Human-Machine Interface (HMI)

- Manufacturing Execution System (MES)

- Enterprise Resource Planning (ERP)

- Other Industrial Control Systems

- Field Devices

- Machine Vision Systems

- Industrial Robotics

- Sensors and Transmitters

- Motors and Drives

- Other Field Devices

- Industrial Control Systems

- By Component

- Hardware

- Software

- Services

- By End-User Industry

- Automotive

- Chemical and Petrochemical

- Utility

- Pharmaceutical

- Food and Beverage

- Oil and Gas

- Electronics and Semiconductor

- Aerospace and Defense

- Other End-User Industries

- By Control System Architecture

- Proprietary / Vendor-Specific

- Open / Interoperable

- Hybrid Architecture

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Singapore

- Australia

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

To ground the numbers, we interviewed control-system integrators, plant engineers, software vendors, and regional distributors in Asia, North America, Europe, and the Gulf. Their views on project budgets, component ASP shifts, and retrofit cycles helped us adjust secondary estimates and challenge early model outputs.

Desk Research

Our desk analysis starts with tier-1 statistics from bodies such as the International Federation of Robotics, Eurostat's production index, United Nations COMTRADE (HS 8537, 8479), the U.S. Census M3 survey, and NIST ICS-CERT advisories. We enrich these with trend data from trade associations like VDMA, peer-reviewed journals tracking Industrial IoT uptake, and corporate 10-Ks that detail automation capex. We then mine D&B Hoovers for company-level revenue splits, tap Dow Jones Factiva for deal flow, and screen patent families in Questel to map innovation hotspots. This list is illustrative; many additional open and paid sources assisted our evidence build.

Market-Sizing & Forecasting

Our model first applies a top-down 'manufacturing value-added × automation intensity' construct, which is cross-checked with sampled bottom-up roll-ups of vendor shipments and channel checks. Key variables include robot installations, global PMI, average controller ASPs, electrical-energy prices, wage inflation, and plant start-ups, each forecast independently. Multivariate regression aligns these drivers with historical spend before ARIMA projections extend the trend through 2030. Where supplier roll-ups fall short, we gap-fill using calibrated penetration ratios agreed during expert calls.

Data Validation & Update Cycle

Before any figure is locked, Mordor analysts run variance checks against external benchmarks, reconcile currency conversions, and escalate anomalies for team review. Reports refresh once a year, with interim updates triggered by material events such as mega-mergers or fiscal stimulus packages, so clients always receive a current view.

Why Mordor's Factory Automation & Industrial Controls Baseline Earns Stakeholder Confidence

Published market values often diverge because studies adopt different product baskets, geographies, and price assumptions. We acknowledge this upfront and preview the usual suspects: scope breadth, base-year choice, and exchange-rate treatment that move totals.

We find gaps widen when others omit field-device revenue, apply list prices without channel discounts, or freeze models on older trade data. Mordor's broader scope, annual refresh, and dual-path validation limit such drift and give decision-makers a firmer anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 311.9 B | Mordor Intelligence | - |

| USD 226.8 B | Global Consultancy A | Excludes field devices; minimal primary interviews |

| USD 276.6 B | Industry Data Service B | Uses list-price ASPs; 2024 base year frozen |

Taken together, the comparison shows that Mordor's disciplined scope selection, fresh primary intelligence, and transparent validations deliver a balanced baseline clients can retrace and reuse with confidence.

Key Questions Answered in the Report

What is the projected value of the factory automation and industrial controls market in 2031?

The market is expected to reach USD 505.88 billion by 2031, growing at an 8.37% CAGR.

Which region is forecast to grow fastest to 2031?

Asia Pacific is set to expand at a 9.56% CAGR, driven by policy incentives in China, India, and Japan.

Which product segment will outpace others over the forecast period?

Field devices, including robots and machine-vision systems, are projected to rise at 9.71% per year through 2031.

Why are pharmaceuticals adopting automation faster than other industries?

Continuous manufacturing mandates, real-time release testing, and stringent FDA guidance are boosting automation in drug production, resulting in a 9.43% CAGR.

How are energy-efficiency regulations influencing market growth?

Rules such as Ecodesign 2024/1781 and U.S. motor standards push upgrades to IE4-IE5 motors and intelligent drives, lowering energy use by up to 25% and accelerating replacement cycles.

What cybersecurity challenges affect adoption of industrial controls?

Increasing ransomware and SCADA vulnerabilities add 8-12% to project costs and lengthen approval timelines, making secure-by-design controllers essential.

Page last updated on: