Industrial Automation Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

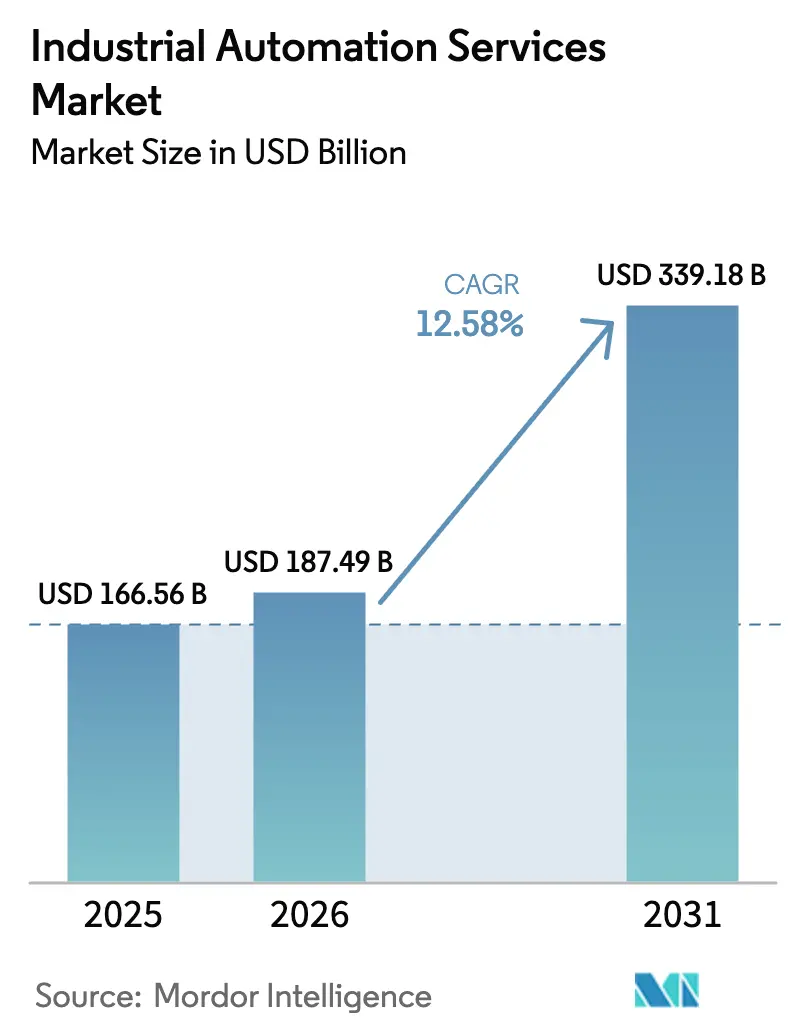

| Market Size (2026) | USD 187.49 Billion |

| Market Size (2031) | USD 339.18 Billion |

| Growth Rate (2026 - 2031) | 12.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Automation Services Market Analysis by Mordor Intelligence

The industrial automation services market size is expected to grow from USD 166.56 billion in 2025 to USD 187.49 billion in 2026 and is forecast to reach USD 339.18 billion by 2031 at 12.58% CAGR over 2026-2031. The 82% value expansion underscores how manufacturers have started shifting away from reactive, component-level support toward predictive, outcome-based service contracts. Growth has been powered by modernization of aging production assets, an acute shortage of skilled technicians, and the widening use of Industrial IoT sensors that enable data-driven maintenance routines. Intensifying energy-efficiency mandates and stricter environmental regulations have further compelled plant owners to outsource automation upgrades to specialists capable of delivering measurable productivity and sustainability gains. Meanwhile, subscription-based delivery models are lowering the capital barrier for small and mid-sized enterprises, accelerating adoption across discrete and process industries.

Key Report Takeaways

- By service type, Maintenance and Support led with 37.62% of industrial automation services market share in 2025, whereas Predictive Maintenance-as-a-Service is projected to grow at a 13.92% CAGR to 2031.

- By delivery model, on-premise deployments held 60.68% of the industrial automation services market size in 2025; cloud/edge services are expanding at a 17.12% CAGR through 2031.

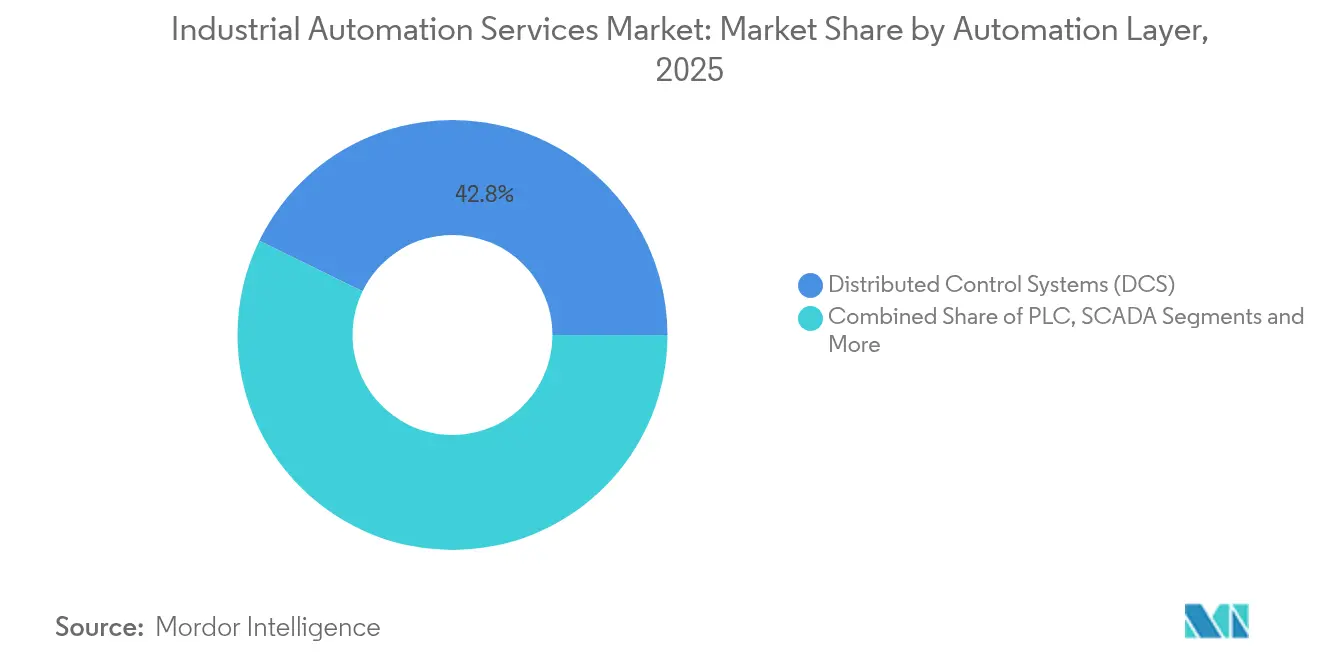

- By automation layer, Distributed Control Systems commanded 42.78% of industrial automation services market size in 2025, yet edge-AI controllers are on track for a 14.88% CAGR.

- By end-user industry, Oil and Gas accounted for 25.84% of industrial automation services market share in 2025, while Automotive and Transportation is forecast to climb at a 12.95% CAGR up to 2031.

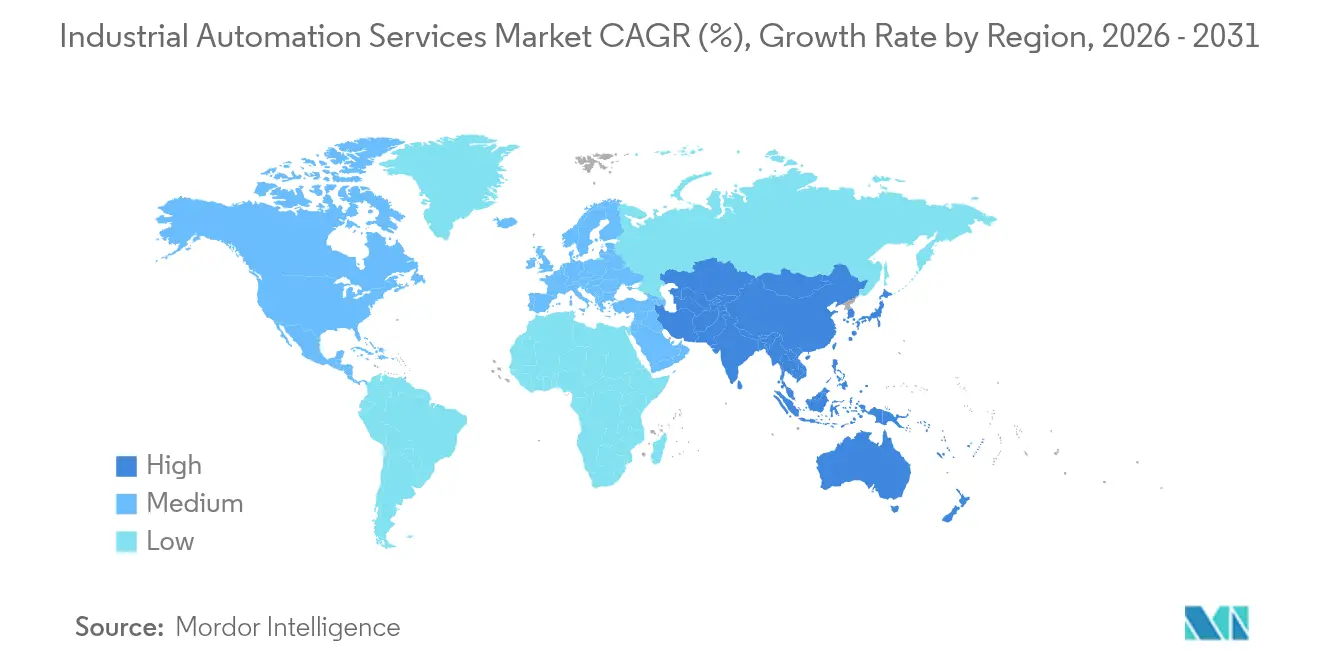

- By geography, Asia-Pacific retained a 42.02% revenue share in 2025 and is set to post the fastest 13.46% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Automation Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of Advanced Technologies | +2.8% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

| Growing Demand for Operational Efficiency | +2.1% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Proliferation of Industrial IoT and Predictive Maintenance | +3.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Aging Workforce Accelerating Automation Adoption | +1.9% | North America and EU, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Rise of No-Code/Low-Code Industrial Automation Platforms | +1.4% | Global, with early gains in developed markets | Medium term (2-4 years) |

| Emerging Automation-as-a-Service Business Models | +1.2% | Global, concentrated in industrial hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration of advanced technologies

Artificial intelligence, machine learning, and edge computing were already redefining service delivery models by 2024. Mitsubishi Electric’s investment in Formic Technologies illustrated how subscription-based robotic cells helped smaller firms overcome labor shortages while avoiding heavy upfront cost[1]Mitsubishi Electric Corporation, “Mitsubishi Electric, ME Innovation Fund Invests in Formic Technologies Inc.,” mitsubishielectric.com. Predictive algorithms embedded within advanced process-control platforms routinely forecasted equipment failures weeks ahead, trimming unplanned downtime by up to 40%. Entire production lines could be virtually commissioned through digital twins before physical build-out, curbing project risks and start-up delays. Pharmaceutical contract manufacturers used AI-powered vision to detect sub-millimeter defects in vials, safeguarding batch integrity in real time. Collectively, these capabilities pushed end users to demand service partners versed in both operational technology and data science.

Growing demand for operational efficiency

Cost pressure and supply-chain volatility intensified the hunt for incremental productivity. Vale’s roll-out of ABB’s Asset Management System yielded 40% savings on reactive maintenance and 12% on preventive work across 6,000 assets. Energy-optimized drives and load-scheduling software cut electricity use by 15-20%, directly improving margins while helping plants meet carbon-emission targets. Service contracts increasingly bundled energy audits with automation retrofits, turning efficiency achievements into contractual key-performance indicators. Manufacturers also pursued standardization—using unified SCADA templates, for example—to shrink engineering hours and accelerate multi-site roll-outs.

Proliferation of Industrial IoT and predictive maintenance

Falling sensor prices had enabled facility-wide condition monitoring by 2024. Rockwell Automation’s deployment at Shandong Mining halved mechanical failure time and slashed failure rates by 70%. Utilities adopted AI-enhanced SCADA to anticipate pump fouling and chemically optimize treatment cycles. Edge nodes processed vibration, pressure, and thermal data locally, guaranteeing millisecond response even during network outages. These successes convinced executives to migrate from calendar-based maintenance to predictive, subscription-funded packages that promise uptime rather than man-hours.

Aging workforce accelerating automation adoption

By 2024, retirement of veteran technicians created knowledge vacuums that automation services sought to fill. In mature markets, open vacancies for controls engineers outstripped graduates several-fold, inflating wage costs and elongating project lead times. Service providers responded by embedding digital work instructions, augmented-reality guidance, and remote-assist channels into every retrofit package. Training and workforce-enablement modules grew from ancillary offerings into core revenue streams, ensuring clients could operate sophisticated new systems without expanding headcount drastically.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Retrofit Costs | -1.8% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Shortage of Skilled Automation Professionals | -1.3% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Cybersecurity and Data-Sovereignty Risks | -0.9% | Global, with regulatory variations by region | Medium term (2-4 years) |

| Legacy System Fragmentation Hindering Integration | -1.1% | Global, concentrated in mature industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High implementation and retrofit costs

Comprehensive upgrades demanded hefty capital outlays, especially when legacy equipment lacked digital interfaces. Many mid-market firms postponed projects or narrowed scopes to fit annual budgets, slowing immediate market uptake. Parallel running of old and new systems during cut-over further inflated costs. Although automation-as-a-service models offered opex-based access, legal complexity around data ownership and cybersecurity still limited uptake outside early adopters.

Shortage of skilled automation professionals

Limited talent drove billing rates higher and stretched project timelines. Scarcity was most acute for cybersecurity, OT-IT convergence, and AI integration specialists. Vendors accelerated internal academies and partnered with universities, yet producing seasoned engineers remained a multiyear endeavour. Consequently, some customers opted for standardized, template-based solutions over bespoke architectures to mitigate resource risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Shift from Break-Fix to Predictive Value

Maintenance and Support dominated revenue in 2025, capturing 37.62% of industrial automation services market share as owners still relied on periodic inspections and emergency call-outs. However, predictive maintenance-as-a-service was already scaling at a 13.92% CAGR, signalling a decisive pivot toward contracts that guarantee uptime rather than labour hours. The industrial automation services market size tied to project engineering and installation stayed resilient as greenfield plants and large retrofits advanced, while commissioning teams handled increasingly complex multi-vendor integrations.

Remote monitoring and diagnostics accelerated in parallel, riding broader IIoT adoption. Asset-performance-management platforms unified historian, CMMS, and ERP feeds to create real-time health indices that optimize spare-parts logistics and technician dispatch. Modernization projects in Europe and North America leveraged these insights to prioritize high-return upgrades first, stretching capital budgets. Consulting practices flourished by mapping digital-transformation roadmaps that bundle technology, process, and workforce planning into a single engagement.

By Delivery Model: Cloud Momentum Gains Credibility

On-premise architectures still held 60.68% of industrial automation services market size in 2025 due to stringent data-sovereignty policies and operator comfort with in-house control. Yet cloud and edge-deployed services were expanding at 17.12% CAGR as cybersecurity frameworks matured and hyperscalers launched industry-specific zones. Early adopters used Microsoft Azure’s industrial modules to deploy AI models at scale without owning large GPU clusters.

Edge appliance subscriptions emerged as a hybrid path, packaging computing, storage, and security into DIN-rail boxes billed monthly. These nodes maintained sub-100-millisecond latency for motion-control loops while syncing noncritical data to cloud analytics engines. Manufacturers with lean IT staffs favored standardized, remotely supported stacks that eliminated patch-management headaches. As more reference sites proved reliability, boardrooms became comfortable shifting capex to opex, broadening the addressable industrial automation services market.

By Automation Layer: DCS Stronghold Faces Edge-AI Disruption

Distributed Control Systems (DCS) commanded 42.78% of industrial automation services market size in 2025 because process industries regarded them as mission-critical. Service revenues stemmed from periodic firmware upgrades, migration of operator stations, and cybersecurity patching. Nonetheless, edge-AI controllers delivered the fastest 14.88% CAGR, embedding analytics at machine level to enable real-time quality correction and micro-stoppage prevention.

Siemens’ Industrial Edge platform illustrated this blending of control and compute, allowing containerized apps to run alongside traditional PLC logic. SCADA and MES vendors likewise embedded AI inference engines, reducing dependence on central data centers. Service providers therefore shifted focus from hardware troubleshooting to lifecycle management of AI models, including retraining and version control. As a result, revenue mix began tilting toward software subscriptions and managed services.

By End-User Industry: Oil and Gas Leads, Automotive Accelerates

Oil and Gas retained the largest 25.84% slice of the industrial automation services market share in 2025 because upstream operators continued to digitalize wells, and downstream refineries prioritized margin gains via advanced process control. Midstream pipeline firms adopted vibration-based leak detection and drone-assisted inspections, expanding service scope.

Automotive and Transportation, however, registered the quickest 12.95% CAGR on the back of rising electric-vehicle output, flexible body-in-white lines, and battery-pack assembly automation. Chery Automobile’s multi-year deal with KUKA exemplified how manufacturers secured turnkey robotics combined with lifecycle support. Pharmaceutical and biotech plants continued deploying serialization, electronic batch records, and clean-in-place automation to comply with stringent quality guidelines. Food and Beverage processors sought hygienic robotics and energy-efficient pasteurization controls to address labor gaps and sustainability audits, further widening the outreach of the industrial automation services market.

Geography Analysis

Asia-Pacific captured 42.02% of 2025 revenues, reflecting China’s smart-manufacturing push and India’s rapid robot uptake. Government incentives such as China’s Made-in-China 2025 and India’s Production-Linked Incentive schemes underpinned plant upgrades, while Japanese and South Korean vendors exported know-how across ASEAN neighbors. The industrial automation services market size linked to Asia-Pacific is predicted to expand 13.46% annually through 2031 as multinationals localize production to shorten supply chains.

North America remained a mature adopter focusing budgets on retrofit programs, cyber-hardening, and reshoring support. The Inflation Reduction Act spurred investments in battery and renewable-energy plants, translating into fresh automation opportunities. United States process industries emphasized open-process-automation standards to avoid long-term vendor lock-in, altering service scopes toward system-integration and middleware development.

Europe’s Industry 4.0 leadership translated into steady demand, particularly for MES, digital twins, and energy-optimization services. German automotive and chemical complexes embraced cloud-connected edge devices to comply with EU sustainability directives. The region also emphasized functional-safety upgrades, driving recurring revenue for TÜV-certified service providers.

Competitive Landscape

The industrial automation services market remained moderately fragmented in 2025. ABB, Siemens, and Schneider Electric leveraged installed base depth, end-to-end portfolios, and global service centers to defend share. Each diversified into software and analytics via acquisitions and in-house platforms—ABB Ability, Siemens Industrial Edge, and Schneider’s EcoStruxure Service Bureau—aiming to convert data into recurring revenue streams.

Second-tier players such as Yokogawa, Emerson, and Rockwell Automation fortified vertical depth, releasing MES and cloud-native diagnostic suites tailored to pharmaceutical, energy, and tire-manufacturing clients. IT giants Microsoft and NTT DATA entered the fray, pairing hyperscale cloud with OT integration expertise; NTT DATA’s 2025 pilot of robot-enabled remote inspections showcased cross-domain collaboration.

Emerging disruptors specialized in AI-based asset intelligence, no-code automation platforms, and pay-per-use robotics. Their agility pressured incumbents to open ecosystems and standardize APIs, reducing vendor lock-in. Price competition intensified in commodity maintenance, but value shifted toward consultative engagements that tie fees to throughput, energy savings, or emissions reductions.

Industrial Automation Services Industry Leaders

Siemens AG

ABB Ltd

Schneider Electric SE

Rockwell Automation Inc

Emerson Electric Co

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mitsubishi Electric planned sample shipments of its 3.3 kV, 1,500 A XB-Series HVIGBT module aimed at heavy industrial drives, cutting switching losses by 15%.

- February 2025: Thames Water adopted AVEVA System Platform across more than 50 sites to unify SCADA databases and improve regulatory compliance.

- January 2025: NTT DATA validated smart-robot inspections over the IOWN all-photonics network, detecting pipe cracks and abnormal vibration remotely.

- December 2024: Mitsubishi Electric invested USD 143.5 million to build a variable-speed compressor factory in Kentucky, backed by USD 50 million from the U.S. Department of Energy.

Global Industrial Automation Services Market Report Scope

The Industrial Automation Market includes many technologies, systems, and services dedicated to automating industrial processes. These advancements enable machinery and tools to operate independently, requiring minimal human intervention. The market's offerings span from robotics and control systems—such as Distributed Control Systems (DCS) and Programmable Logic Controllers (PLC)—to sensors, software, and related services, all designed to improve productivity, efficiency, and safety in industrial operations.

The industrial automation services markets is segmented by service type (project engineering and installation, maintenance and support services, consulting services, operational services), by end-user industry (oil & gas, pharmaceutical, automotive & transportation, food & beverage, power & utilities, chemical & petrochemical, other end-user industries), by geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Spain, and Rest of Europe], Asia-Pacific [India, China, Japan, New Zealand, Australia and Rest of Asia-Pacific], Latin America [Brazil, Mexico, and Rest of Latin America], Middle East and Africa.

The report offers market forecasts and size in value (USD) for all the above segments.

| Project Engineering and Installation |

| Commissioning and Start-up Services |

| Modernization / Retrofit Projects |

| Maintenance and Support (Corrective / Preventive) |

| Remote Monitoring and Diagnostics |

| Asset Performance Management (APM) |

| Consulting and Assessment Services |

| Training and Workforce Enablement |

| Spare Parts and Repairs |

| Outsourced Operations (O-&-M) |

| On-premise |

| Cloud |

| Edge Appliance Subscription |

| Distributed Control Systems (DCS) |

| Programmable Logic Controllers (PLC) |

| Supervisory Control and Data Acquisition (SCADA) |

| Manufacturing Execution / MOM Systems |

| Advanced Process Control (APC) and Optimization |

| Human-Machine Interface (HMI) / Operator Panels |

| Safety Instrumented Systems (SIS) |

| Industrial PCs and Edge Controllers |

| Industrial IoT Analytics Platforms |

| Oil and Gas |

| Pharmaceutical and Biotechnology |

| Automotive and Transportation |

| Food and Beverage |

| Power and Utilities |

| Chemical and Petrochemical |

| Metals and Mining |

| Pulp and Paper |

| Water and Wastewater |

| Semiconductor and Electronics |

| Other Discrete and Process Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Project Engineering and Installation | ||

| Commissioning and Start-up Services | |||

| Modernization / Retrofit Projects | |||

| Maintenance and Support (Corrective / Preventive) | |||

| Remote Monitoring and Diagnostics | |||

| Asset Performance Management (APM) | |||

| Consulting and Assessment Services | |||

| Training and Workforce Enablement | |||

| Spare Parts and Repairs | |||

| Outsourced Operations (O-&-M) | |||

| By Delivery Model | On-premise | ||

| Cloud | |||

| Edge Appliance Subscription | |||

| By Automation Layer | Distributed Control Systems (DCS) | ||

| Programmable Logic Controllers (PLC) | |||

| Supervisory Control and Data Acquisition (SCADA) | |||

| Manufacturing Execution / MOM Systems | |||

| Advanced Process Control (APC) and Optimization | |||

| Human-Machine Interface (HMI) / Operator Panels | |||

| Safety Instrumented Systems (SIS) | |||

| Industrial PCs and Edge Controllers | |||

| Industrial IoT Analytics Platforms | |||

| By End-User Industry | Oil and Gas | ||

| Pharmaceutical and Biotechnology | |||

| Automotive and Transportation | |||

| Food and Beverage | |||

| Power and Utilities | |||

| Chemical and Petrochemical | |||

| Metals and Mining | |||

| Pulp and Paper | |||

| Water and Wastewater | |||

| Semiconductor and Electronics | |||

| Other Discrete and Process Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the industrial automation services market?

The market was valued at USD 187.49 billion in 2026.

How fast will the industrial automation services market grow to 2031?

It is forecast to expand at a 12.58% CAGR, reaching USD 339.18 billion by 2031.

Which region leads the industrial automation services market?

Asia-Pacific held 42.02% of 2025 revenue and is expected to grow at 13.46% CAGR.

Which service segment is growing the fastest?

Predictive Maintenance-as-a-Service is projected to register a 13.92% CAGR through 2031.

Why are edge-AI controllers gaining traction?

They enable real-time decision-making at machine level and are forecast to grow 14.88% annually.

Who are the major players in industrial automation services?

ABB, Siemens, Schneider Electric, Rockwell Automation, Yokogawa, and Emerson dominate, while newer AI-centric firms are emerging rapidly.

Page last updated on: