Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 43.87 Billion |

| Market Size (2031) | USD 62.9 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

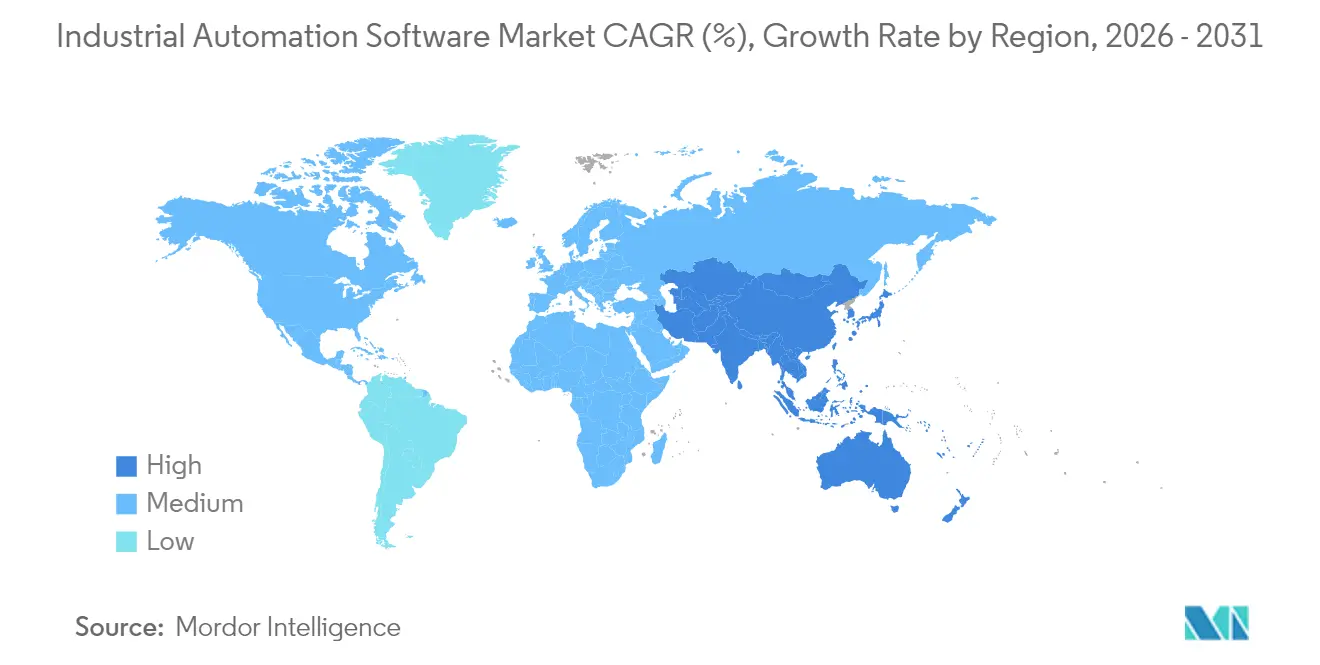

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Automation Software Market Analysis by Mordor Intelligence

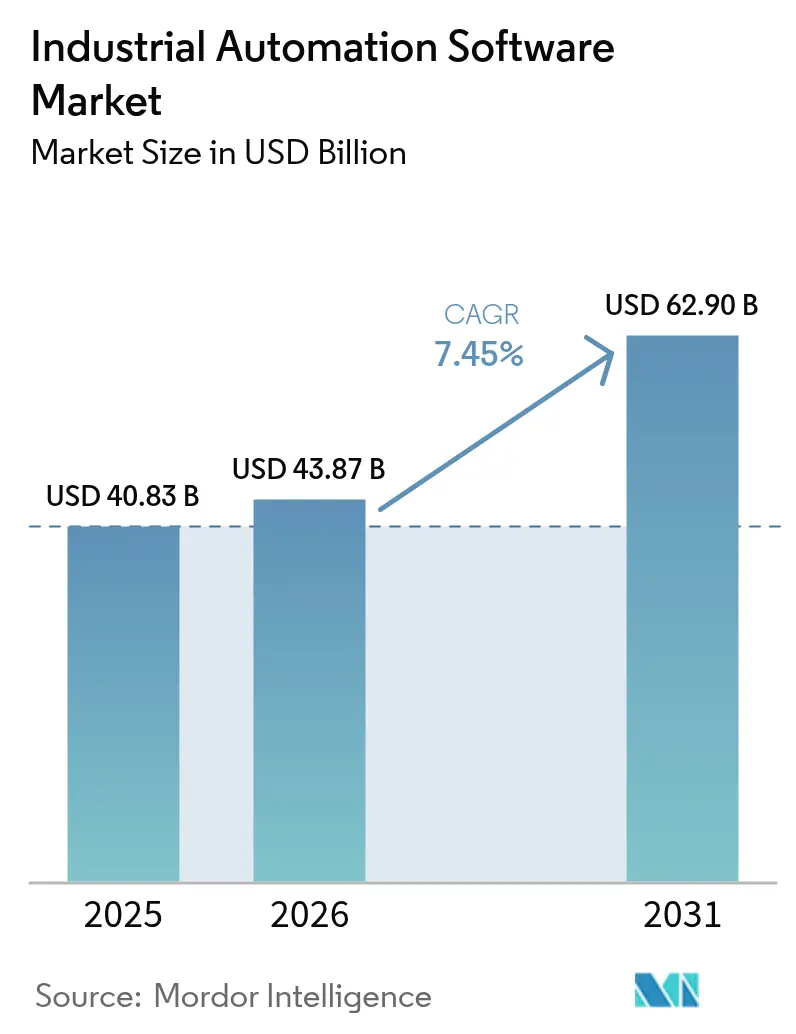

The industrial automation software market size was valued at USD 40.83 billion in 2025 and estimated to grow from USD 43.87 billion in 2026 to reach USD 62.9 billion by 2031, at a CAGR of 7.45% during the forecast period (2026-2031). Manufacturers are accelerating investments as artificial intelligence (AI) tools move from pilot projects to embedded functions inside supervisory control, plant-asset-management and manufacturing-execution platforms. The shift from reactive to predictive operations is being enabled by edge computing that executes control-loop decisions in milliseconds, while cloud analytics orchestrate enterprise-wide optimization. Reinforcement-learning agents are now tuning process parameters continuously, driving yield improvements and energy savings across chemicals, automotive and electronics plants. Market momentum is further buoyed by government-backed Industry 4.0 programs that tie automation upgrades to cybersecurity mandates such as IEC 62443, ensuring capital allocation even in cautious spending climates.

Key Report Takeaways

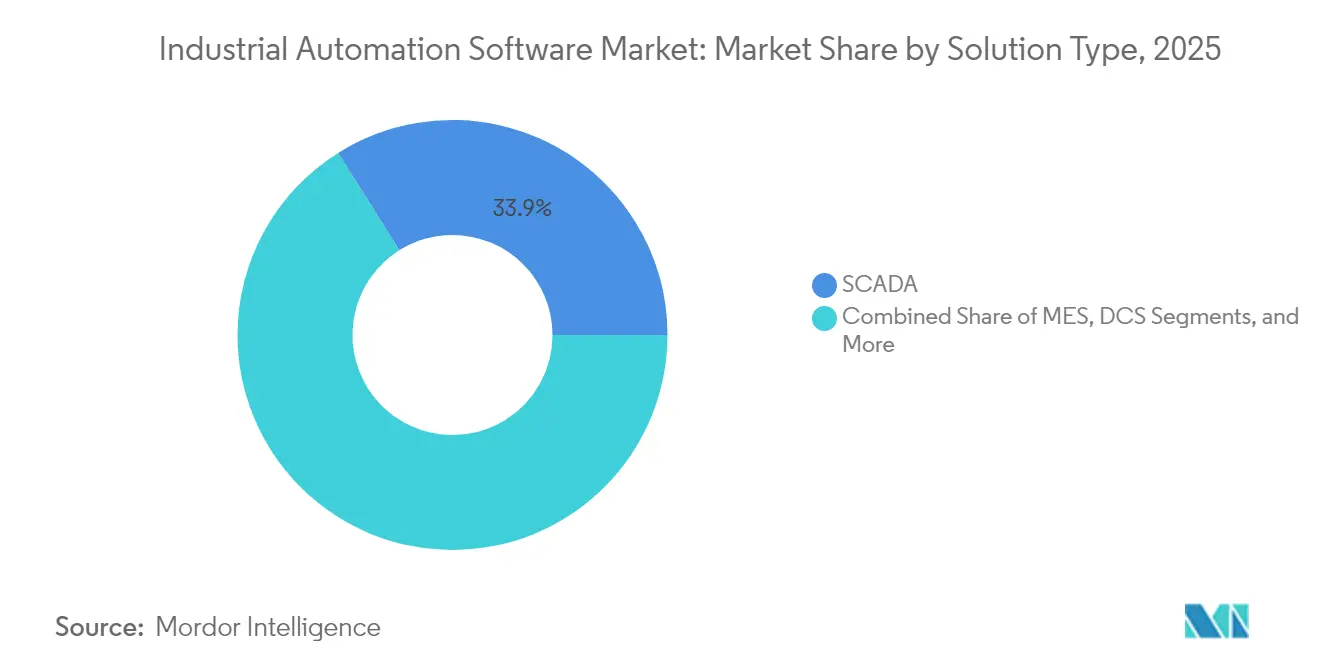

- By solution type, SCADA systems held 33.92% of the industrial automation software market share in 2025. By solution type, plant asset management and analytics platforms are projected to expand at an 8.12% CAGR through 2031.

- By deployment mode, on-premises installations accounted for 55.86% of the industrial automation software market size in 2025. By deployment mode, cloud-based offerings are forecast to grow at 8.31% CAGR between 2026-2031.

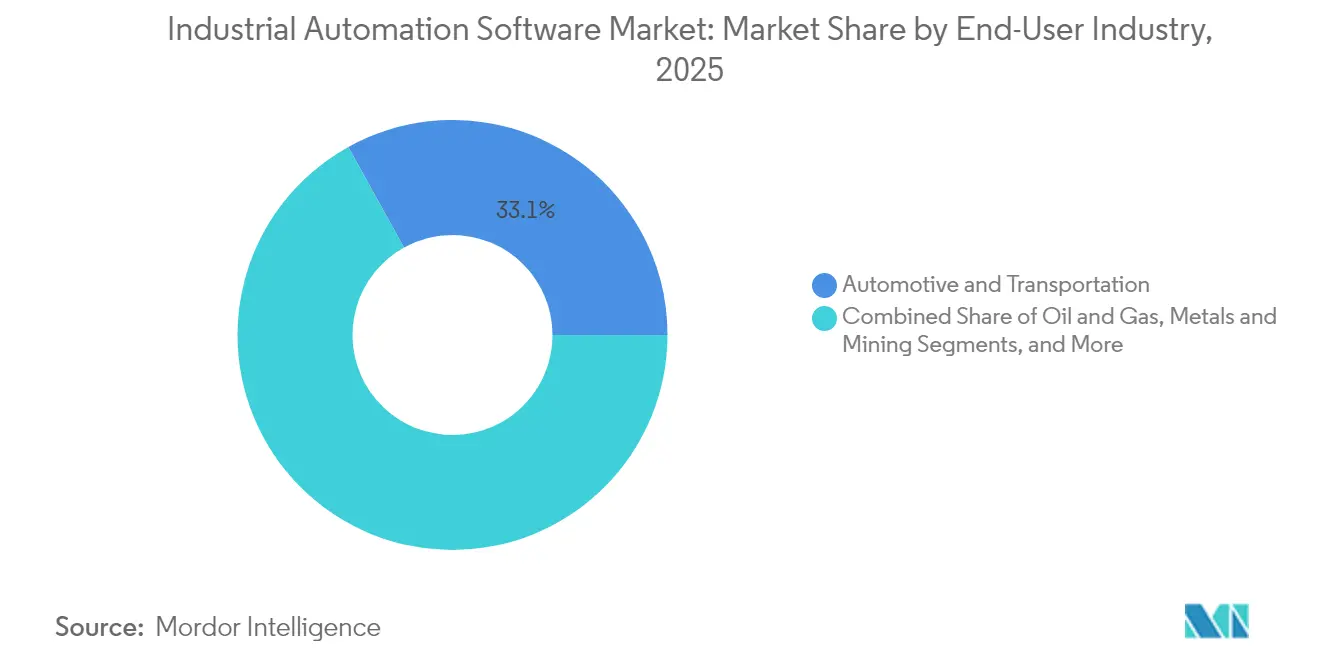

- By end-user, automotive and transportation captured 33.05% of the industrial automation software market share in 2025. By end-user, chemicals and pharmaceuticals are poised for the fastest growth at an 8.02% CAGR through 2031.

- By enterprise size, large organizations commanded 72.05% share of the industrial automation software market size in 2025. By enterprise size, small and medium enterprises are projected to log an 8.41% CAGR from 2026-2031.

- By geography, Asia Pacific dominated with 38.22% of the industrial automation software market share in 2025 and is set to rise at an 8.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Automation Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of Industry 4.0 and smart manufacturing | +2.1% | Global, with APAC and Europe leading | Medium term (2-4 years) |

| Increasing demand for real-time data analytics and IIoT connectivity | +1.8% | Global, concentrated in North America and APAC | Short term (≤ 2 years) |

| Rising labor cost and need for operational efficiency | +1.5% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Growing focus on cybersecurity in critical infrastructure | +1.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Convergence of low-code/no-code platforms with industrial automation | +0.9% | Global, early adoption in North America | Short term (≤ 2 years) |

| AI-driven autonomous process optimization via reinforcement learning | +0.5% | APAC and North America, emerging in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of Industry 4.0 and smart manufacturing

Manufacturers are replacing isolated automation islands with open-architecture ecosystems that let software move freely across controllers and edge devices. ExxonMobil’s commercialization of an IEC 61499 runtime exemplifies how open process automation delivers sub-millisecond response while slashing vendor lock-in costs.[1]International Society of Automation, “Whitepaper: Benefits and Challenges of AI in Mining and Metals,” automation.com Edge nodes now host real-time control, whereas cloud layers handle fleet-wide optimization, allowing plants to decouple hardware refresh cycles from software innovation. Chemical processors are migrating from monolithic distributed-control systems to modular nodes, enabling rapid recipe changes without line shutdowns. Vendor-agnostic frameworks foster competitive bidding and accelerate time-to-value, reinforcing adoption across both brownfield and greenfield sites.

Increasing demand for real-time data analytics and IIoT connectivity

Time-sensitive networking (TSN) integrated with OPC UA synchronizes distributed controllers at microsecond resolution, empowering closed-loop optimization previously hindered by latency constraints.[2]OPC Foundation, “OPC UA with TSN – Technical Overview,” opcfoundation.org Automotive body-shops stream gigabytes of weld-quality data to AI models that adjust gun force on the next cycle, reducing scrap rates. Energy-intensive processes feed live power-pricing signals into control algorithms that shift loads within seconds to cut costs. Edge analytics execute anomaly detection locally, sending only exceptions to the cloud, shrinking bandwidth needs. This distributed-intelligence approach tightens quality control and reinforces resilience against network outages.

Rising labor cost and need for operational efficiency

Asia Pacific is grappling with aging workforces and rapidly climbing wages, prompting manufacturers to deploy AI agents that self-optimize throughput and energy consumption. Reinforcement-learning controllers in pharmaceutical reactors now outperform veteran operators in maintaining critical quality attributes, shrinking batch variability. Cloud-delivered manufacturing-execution software lets small factories access the same orchestration functions as global majors, avoiding capital-intensive servers. Digital twins simulate process tweaks before live deployment, trimming downtime risk. Collectively, these tools lift overall equipment effectiveness while reducing dependency on scarce expert talent.

Growing focus on cybersecurity in critical infrastructure

IEC 62443-2-1:2024 establishes rigorous security-program criteria, pushing asset owners to embed protection mechanisms inside control logic rather than rely on perimeter firewalls.[3]Inductive Automation, “HMI: Human-Machine Interface,” inductiveautomation.com Manufacturers are segmenting networks with software-defined zoning that limits attack blast radius. Real-time monitoring dashboards correlate operational-technology events with IT threat feeds, enabling faster incident response. Procurement policies now mandate compliance evidence from automation-software vendors, effectively making security a competitive differentiator. Increased regulation is translating into budget allocations that favor platforms with native intrusion-detection, patch management and encrypted protocol stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and legacy-system integration complexity | -1.4% | Global, particularly acute in mature industrial regions | Medium term (2-4 years) |

| Shortage of skilled automation-software engineers | -0.8% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Interoperability issues from proprietary vendor protocols | -0.6% | Global, with higher impact in multi-vendor environments | Medium term (2-4 years) |

| Data-sovereignty barriers limiting cloud deployment in regulated sectors | -0.4% | North America and EU, with regulatory spillover to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX and legacy-system integration complexity

Retrofitting multi-vendor control rooms often costs more than the new software because proprietary protocols demand custom gateways. Plants adopt phased rollouts to avoid downtime, stretching ROI timelines. Virtualization promises savings but many operators hesitate to virtualize safety-critical loops. SMEs lack in-house resources to manage migration, so they delay upgrades despite potential efficiency paybacks. Hybrid integration toolkits are emerging, yet their adoption is constrained by perceived reliability risks in mission-critical environments.

Shortage of skilled automation-software engineers

Retirements in North America and Europe are outpacing the supply of graduates fluent in both control theory and cloud architectures. Modern stacks span PLC ladder logic, Python, container orchestration and cybersecurity frameworks, creating steep learning curves. Universities struggle to update curricula fast enough, leading firms to finance upskilling academies. Low-code suites offer partial relief but often fall short in high-speed, high-availability scenarios. The talent gap elevates labor costs and slows project throughput, acting as a structural brake on the industrial automation software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: SCADA Systems Drive Market Leadership

SCADA platforms captured 33.92% of the industrial automation software market share in 2025, underlining their role in centralized monitoring of geographically dispersed assets. Utilities lean on these systems to manage substations and renewable-generation sites, ensuring grid stability during fluctuating supply. The industrial automation software market continues to favor SCADA for its proven reliability and vendor ecosystem, yet demand is gravitating toward analytics-rich overlays that interpret operational data and trigger predictive maintenance workflows. Plant asset management and analytics solutions, growing at an 8.12% CAGR, exemplify this transition toward value-at-the-data-layer.

In process plants, distributed control systems are being modernized with open APIs, enabling third-party applications to interoperate without proprietary silos. Human-machine interface (HMI) tools are integrating augmented-reality features, cutting operator learning curves for complex batch processes. Manufacturing execution systems remain pivotal for real-time scheduling in automotive body-shops, while digital-twin and AI-optimization modules in the “Others” category are redefining how facilities simulate, test and deploy new recipes with minimum downtime.

By Deployment Mode: Cloud Adoption Accelerates Despite On-Premises Dominance

On-premises installations maintained 55.86% of the industrial automation software market size in 2025 as safety-critical industries prefer deterministic latency and full data sovereignty. Even so, hybrid architectures are blurring distinctions: edge appliances host control logic locally, while cloud layers perform fleet analytics and enterprise resource planning synchronization. The industrial automation software market is witnessing an 8.31% CAGR for pure-cloud deployments, powered by subscription models that shift spending from capital budgets to operating budgets.

SMEs favor SaaS MES platforms that pre-configure workflows for discrete manufacturing and require no server maintenance. Large enterprises, meanwhile, pilot multi-cloud strategies that hedge vendor lock-in and comply with cross-border data regulations. Advances in secure tunneling and real-time streaming protocols are easing concerns about remote connectivity, accelerating cloud migration for historian and quality-analytics workloads where microsecond latency is non-critical.

By End-User Industry: Automotive Leadership Drives Digital Manufacturing

Automotive and transportation players held 33.05% of the industrial automation software market share in 2025 by deploying flexible assembly-line software that reconfigures cells for electric vehicle variants within hours. Their early adoption of AI-driven visual inspection tools sets a benchmark other sectors emulate. Chemicals and pharmaceuticals lead growth with an 8.02% CAGR as regulators encourage continuous-manufacturing paradigms that rely heavily on real-time control and traceability.

Food and beverage producers implement MES modules that ensure batch genealogy and allergen segregation, aligning with stricter labeling laws. Oil and gas operators retrofit offshore platforms with predictive-maintenance analytics that anticipate rotating-equipment failure, cutting unplanned shutdown costs. Semiconductor fabs demand nanometer-precision control systems that manage lithography and etching processes, reinforcing software’s role in yield enhancement. Mining firms adopt AI optimizers that raise ore-throughput while trimming energy use, evidencing software’s cross-sector relevance.

By Enterprise Size: SMEs Embrace Cloud-Based Solutions

Large corporations accounted for 72.05% of the industrial automation software market size in 2025, backed by multi-site rollouts and custom integrations that lock in long-term vendor contracts. They deploy enterprise service buses that aggregate shop-floor data into corporate dashboards, enabling synchronized decision-making across continents. SMEs are the fastest movers at an 8.41% CAGR as SaaS platforms democratize advanced capabilities without heavy capex.

Subscription pricing aligns with variable production volumes, a boon for job-shop manufacturers navigating demand volatility. Managed-service providers now offer remote monitoring and periodic application tuning, filling the skills void common among smaller firms. As edge-in-a-box appliances bundle PLC, HMI and historian functions, SMEs gain turnkey pathways to Industry 4.0 compliance, reinforcing grassroots expansion of the industrial automation software market.

Geography Analysis

Asia Pacific contributed 38.22% revenue in 2025 and is on track for an 8.09% CAGR, reflecting policy-driven adoption across China, India, Japan and South Korea. China’s Made in China 2025 roadmap co-funds smart-factory pilots that intertwine AI vision inspection with real-time scheduling. India’s Production-Linked Incentive schemes incentivize automated lines in electronics and automotive clusters. Japan’s robotics heritage accelerates uptake of HMI innovations that blend voice commands with mixed-reality work instructions. South Korea’s semiconductor giants push the envelope on precision process control, while Australia’s mining sector invests in digital twins for ore-processing lines to maximize uptime in remote locations.

North America emphasizes cybersecurity and AI integration over capacity expansion. The United States deploys edge computing nodes in defense supply chains to guarantee on-premises processing of sensitive workloads, while Canadian utilities modernize SCADA for renewable integration. Europe balances efficiency with sustainability; Germany anchors open-automation consortia, France modernizes aerospace assembly with model-based systems engineering, and the United Kingdom upgrades legacy lines to shorten product-development cycles. Regulatory imperatives such as the EU Cyber Resilience Act shape vendor roadmaps, embedding compliance features into software kernels.

South American economies, notably Brazil, begin automating agribusiness processing, albeit tempered by macroeconomic volatility. The Middle East and Africa channel oil-and-gas revenue into refinery digitization projects that deploy predictive-maintenance modules validated for hazardous areas. Across regions, greenfield facilities leapfrog legacy constraints by specifying open, cloud-ready automation architectures from day one, broadening the footprint of the industrial automation software market.

Regulatory Landscape

Cybersecurity and product-security regulation is increasingly shaping industrial automation software requirements across regions, with IEC 62443 frequently used as the core control-system security framework in procurement and audits. IEC 62443-2-1:2024 raised expectations for formal security programs, and IEC PAS 62443-1-6:2025 extended guidance for industrial IIoT environments, which vendors and asset owners use to structure security controls for connected devices, edge gateways, and industrial applications.

In Europe, Regulation (EU) 2024/2847 (the Cyber Resilience Act) adds product-level obligations for digital products, including vulnerability reporting starting September 11, 2026, and broader compliance requirements by December 11, 2027. This increases emphasis on secure-by-design engineering and coordinated vulnerability disclosure processes for industrial software portfolios. The EU AI Act also adds governance requirements for high-risk uses of AI, including certain MES functions tied to critical infrastructure management; amendments approved in June 2026 extended compliance timelines for standalone high-risk AI systems to December 2, 2027 and for safety-critical AI systems to August 2, 2028, shaping vendor roadmaps for embedded AI features inside SCADA, MES, and asset analytics.

Competitive Landscape

Competitive intensity is moderate. Siemens, ABB and Rockwell Automation leverage cross-licensing and cloud partnerships to bundle on-premises control with Azure, AWS and Google Cloud analytics. Their installed bases grant scale economies, but modular architectures and open standards erode vendor lock-in. White-space entrants offer cloud-native platforms that spin up digital twins in minutes, appealing to fast-growing SMEs.

Traditional vendors invest in AI engines that auto-generate control code from process schematics, shortening commissioning times. Mergers target cybersecurity specialists, integrating anomaly detection directly into controller firmware. Hyperscalers co-develop edge runtimes that extend their ecosystems to factory floors, fostering coopetition with automation incumbents.

Open-process-automation movements encourage mix-and-match hardware, enabling niche firms to integrate best-of-breed solutions backed by standards compliance. Hardware commoditization shifts differentiation to software IP, prompting incumbents to shift revenue models toward subscription and outcome-based contracts. As customers prioritize lifecycle value over upfront cost, vendors expand managed-services offerings that guarantee asset uptime, reinforcing continuous engagement in the industrial automation software market.

Industrial Automation Software Industry Leaders

Siemens AG

General Electric Company

Schneider Electric SE

Emerson Electric Co.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is in packaged modernization offers that reduce the integration burden when migrating from monolithic, on-premises automation stacks to hybrid edge-plus-cloud execution. In June 2026, Schneider Electric introduced Industrial Automation Modernization as a Service, integrating EcoStruxure Automation Expert with HPE SimpliVity infrastructure. The move signals demand for outcome-oriented deployments where the vendor bundles software, infrastructure, and lifecycle services into a single delivery model, which is particularly relevant for SMEs and multi-site operators that need faster rollout paths but lack deep internal resources for brownfield integration.

Industrial AI orchestration and software-defined automation are also creating space for platforms that connect plant data to enterprise AI without re-platforming core control systems. In June 2026, Siemens announced Intelligence Center X to link Mendix low-code and RapidMiner AI tooling for enterprise-scale industrial AI deployment. Rockwell Automation released FactoryTalk ResilientEdge (June 2026) to integrate cloud and edge capabilities for continuous operations. In process automation, Emersons DeltaV v16.LTS release in early 2026 highlights commercialization of software-defined controllers and subscription-based scaling, reinforcing customer interest in longer-term support and upgradeable software layers that decouple innovation cycles from hardware refresh cycles.

Recent Industry Developments

- July 2026: Emerson released the Ovation Curation Tool to manage synchronization and version control between control systems and their associated digital-twin environments in power and water operations. The capability tightens governance over model and configuration drift, supporting more repeatable engineering workflows and safer updates in regulated, uptime-critical plants.

- June 2026: Schneider Electric launched Industrial Automation Modernization as a Service, integrating EcoStruxure Automation Expert with HPE SimpliVity infrastructure to deliver software-defined automation modernization. The offer addresses a common barrier in brownfield sites by bundling software, compute, and lifecycle delivery into a standardized path that can shorten migration cycles and simplify multi-site scaling.

- December 2024: Schneider Electric released EcoStruxure Automation Expert v24.1, adding autonomous-control agents and integrated security posture monitoring. The update reinforced the shift toward embedding AI-assisted optimization and cybersecurity controls directly into industrial automation software platforms, strengthening vendor differentiation as compliance requirements rise.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the industrial automation software market covers software used to monitor, control, and optimize industrial machines and processes inside plants and facilities. It includes core control and supervisory layers (for example, SCADA, PLC programming environments, and HMI) used across discrete and process industries.

Scope exclusions: We exclude pure hardware-only automation components and generic enterprise office software that is not used for shop-floor control or industrial process supervision.

Segmentation Overview

- By Solution Type

- Manufacturing Execution System (MES)

- Supervisory Control and Data Acquisition (SCADA)

- Distributed Control System (DCS)

- Human-Machine Interface (HMI) Software

- Programmable Logic Controller (PLC) Software

- Plant Asset Management and Analytics

- Other Solution Types

- By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid

- By End-User Industry

- Automotive and Transportation

- Food and Beverage

- Oil and Gas

- Chemicals and Pharmaceuticals

- Electronics and Semiconductors

- Metals and Mining

- Energy and Utilities

- Other End-User Industries

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the market boundary, decide which software revenue streams are counted, and set realistic ranges for adoption and pricing. We referenced non-paywalled public sources such as US Census Bureau and Eurostat industrial output series, OECD and World Bank macro indicators, UN Comtrade trade statistics (as a directional check for automation-linked equipment flows), and standards and guidance from bodies such as IEC and ISA.

To connect demand with spending, we reviewed annual reports, 10-K style filings, investor presentations, and credible industry association publications that discuss automation investments and the software mix. Patent databases were also used to spot where control, visualization, analytics, and cybersecurity features are moving, which then informed variable selection for the forecast model. These examples are not exhaustive, and many other sources were used to collect data, cross-check assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating what buyers treat as software, how contracts are priced (license, subscription, and support), and how usage is changing with cloud and edge deployments. We spoke with a mix of software decision-makers, plant and engineering roles, and channel or integration stakeholders across major manufacturing and process hubs, so the gaps from desk research could be closed and key assumptions could be stress-tested.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 41% |

| Mid tier: 60% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 15% | Managers: 51% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where industrial production activity, automation intensity in key end-user industries, and software penetration are combined to reconstruct a realistic demand pool. This is then checked with selective bottom-up approximations, such as sampling typical software spend per site, sanity-checking the mix of license versus subscription, and validating implied ASP ranges with channel feedback.

Inputs in the model include indicators such as manufacturing and process output trends, new plant and line additions, the installed base refresh cycle for control systems, the share of sites adopting connected SCADA and advanced HMI features, and the attach rate of cybersecurity and maintenance analytics to control layers. We also track the shift in pricing from perpetual licensing toward subscription and support-heavy contracts, because that changes recognized revenue patterns by year. Where bottom-up signals are thin for a country or niche, gaps are handled using proxy adoption rates from similar industrial structures, followed by interview-based adjustments.

For forecasting, scenario analysis is used around a core time-series path, since adoption and pricing can change quickly when plants accelerate digitization or delay capex. Assumptions on penetration, renewal rates, and ASP movement are reviewed with experts, and the final forecast is kept within ranges explainable against observed industry activity and buying behavior.

Data Validation & Update Cycle

Validation is done through several checks so totals do not rely on a single variable. We compare model outputs against independent signals such as industrial production changes, automation spending commentary in public disclosures, and observed shifts in contract structures, and then anomalies are reviewed before sign-off.

When a country or segment shows an unusual jump, we re-check currency conversion timing, pricing assumptions, and whether a one-time project effect is being mistaken for recurring software revenue. Reports are refreshed annually, and interim updates are made when material events occur, such as large policy shifts, major supply chain resets, or sharp changes in industrial activity. Before delivery, an analyst performs a final pass so clients get the most current view available at that point.

Mordor Intelligence's Industrial Automation Software Market Size Compared With Other Published Estimates

Published market numbers for industrial automation software do not always match, even when the topic label looks the same. The spread usually comes from what each study counts as software, which year is used as the anchor for currency conversion, and how recurring support and subscription revenue is recognized.

A refresh-led factor is also important here, since pricing and contract mix have been changing quickly with cloud-enabled supervisory platforms and bundled support. By re-checking ASP movement, renewal assumptions, and currency timing during the latest update cycle, Mordor Intelligence keeps the 2025 value aligned to the same demand pool and revenue logic used through the forecast.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 40.83 B (2025) | |

| Global Consultancy A | USD 48.50 B (2025) | This figure appears to include services tied to software (such as consulting, training, and support) as part of the market value, which can lift totals versus a software-focused revenue boundary. |

| Publisher B | USD 14.80 B (2025) | This estimate likely uses a narrower product scope or a tighter definition that excludes major control and supervisory layers, or it applies different revenue recognition and pricing logic that reduces counted software spend. |

Overall, the table shows that boundary choices and update assumptions explain most of the difference, rather than a true disagreement on adoption direction. Our approach keeps each year traceable to clear levers, like penetration, contract mix, and ASP ranges, so the final number is easier to reproduce and explain.

Key Questions Answered in the Report

What was the industrial automation software market size in 2026?

It reached USD 43.87 billion, setting the base for subsequent growth.

What CAGR is forecast for the industrial automation software market to 2031?

The market is projected to expand at 7.45% annually through 2031.

Which region leads in revenue and growth?

Asia Pacific both led with 38.22% share in 2025 and is expected to grow fastest at 8.09% CAGR to 2031.

Which solution segment is growing the quickest?

Plant asset management and analytics platforms are forecast to post an 8.12% CAGR through 2031.

Why are SMEs adopting automation software rapidly?

SaaS pricing, reduced capex and managed-service options let smaller firms integrate advanced automation without heavy in-house expertise.

Page last updated on: