Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.39 Billion |

| Market Size (2031) | USD 29.46 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Motors Market Analysis by Mordor Intelligence

The industrial motors market size is expected to grow from USD 22.34 billion in 2025 to USD 23.39 billion in 2026 and is forecast to reach USD 29.46 billion by 2031 at 4.73% CAGR over 2026-2031. This steady trajectory reflects the sector’s pivotal role in digitized manufacturing, electrification, and energy-efficiency mandates. The industrial motors market benefits from deep integration in energy-intensive processes where motor-driven systems account for more than 80% of electricity consumption in refineries and onshore oil and gas facilities. Asia Pacific retains the largest regional share, helped by China’s manufacturing rebound and India’s Production-Linked Incentive programs that accelerate Industry 4.0 adoption. Technology trends highlight a transition from standard AC induction products to smart AC servo models with embedded sensors, while regulatory pressure for IE5 and IE6 efficiency classes spurs synchronous-reluctance and permanent-magnet innovation. Ongoing supply-chain reshoring in North America and Europe also reshapes demand patterns toward locally made, high-efficiency motor-drive packages.

Key Report Takeaways

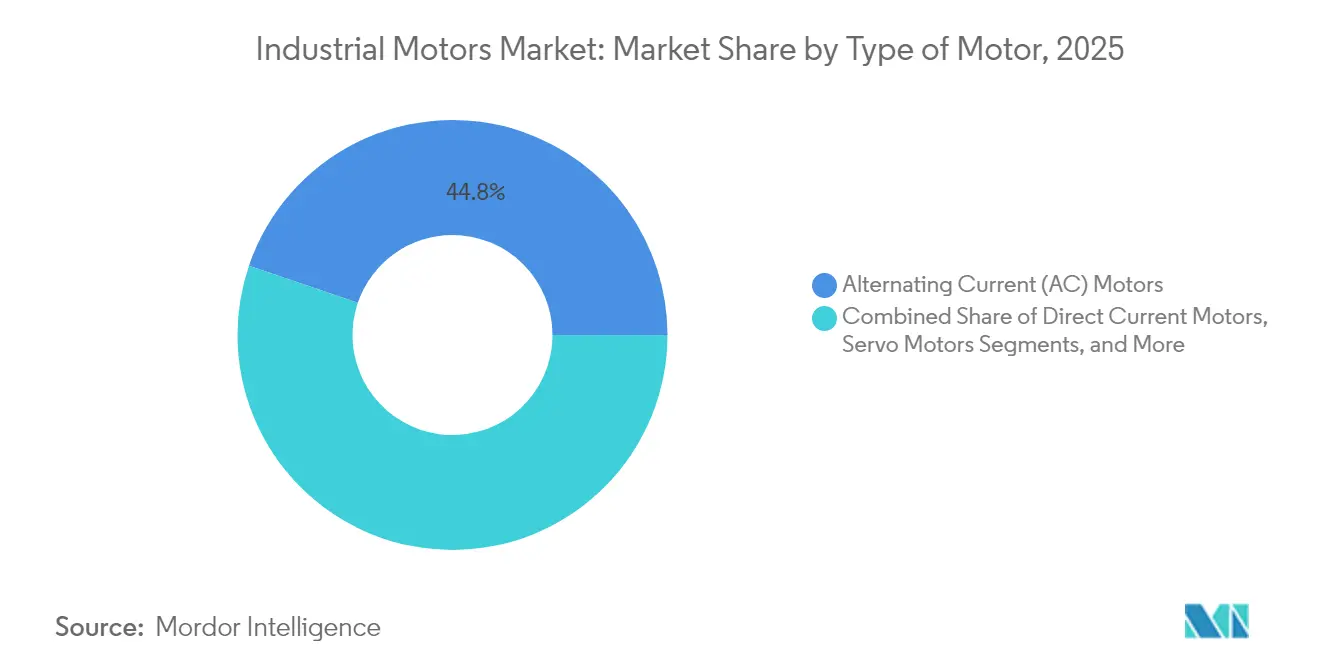

- By type of motor, AC induction held 44.78% of industrial motors market share in 2025, whereas smart AC servo models are projected to deliver the fastest 5.03% CAGR to 2031.

- By voltage, low-voltage units below 1 kV accounted for 62.31% of industrial motors market size in 2025 and are advancing at a 4.91% CAGR to 2031.

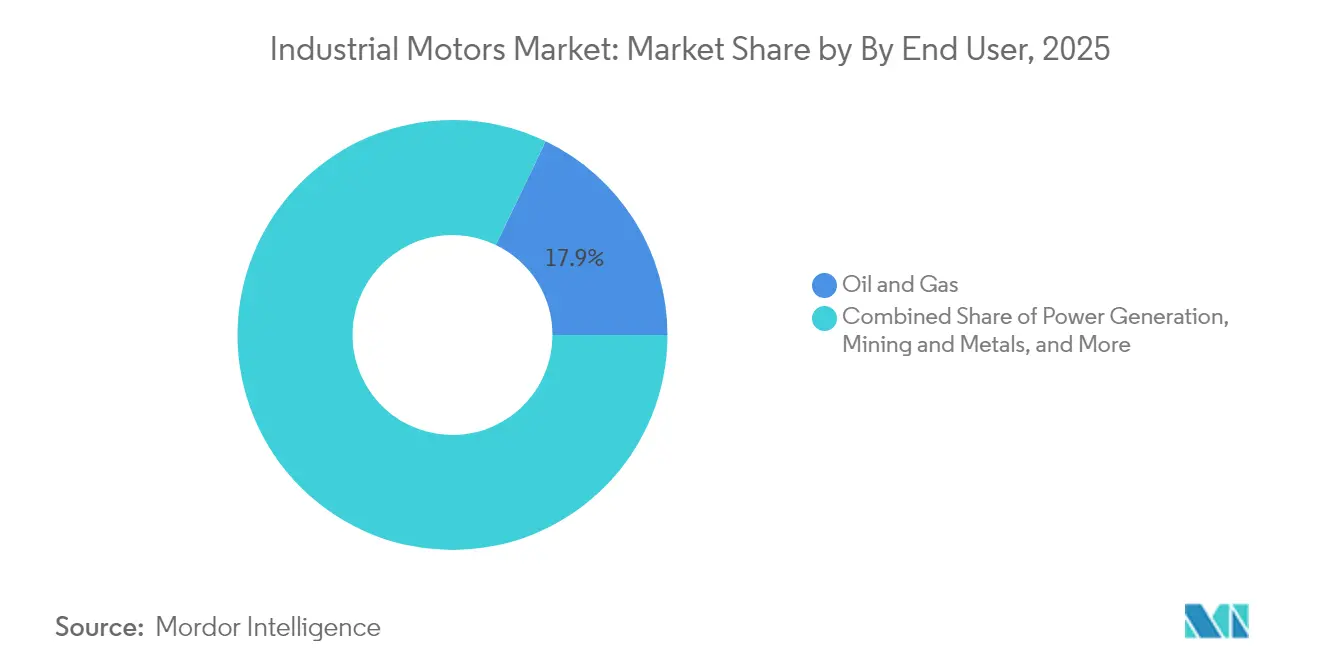

- By end user, discrete manufacturing represented the fastest-growing segment, posting a 5.95% CAGR through 2031 while oil and gas maintained the largest 17.86% revenue share in 2025.

- By geography, Asia Pacific commanded 51.32% of the industrial motors market in 2025; the region is forecast to grow 5.66% annually through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Motors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency regulations | +1.2% | Global, led by EU and North America | Medium term (2-4 years) |

| Smart factory automation demand | +0.9% | Asia Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| Rise of HVAC and water infrastructure | +0.7% | Global, urban centers | Medium term (2-4 years) |

| Trade-tariff-driven reshoring | +0.5% | North America and EU | Short term (≤ 2 years) |

| Edge-AI predictive maintenance | +0.4% | Asia Pacific and North America | Long term (≥ 4 years) |

| IE5 rare-earth-free motors | +0.3% | Europe concentrated, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations

Mandated IE5 and emerging IE6 standards in the EU and updated NEMA Premium rules in the United States push industrial customers toward ultra-efficient replacements. ABB’s hyper-efficiency synchronous-reluctance platform shows energy losses 20% lower than IE5, illustrating how regulation propels technology leaps.[1]ABB, “Low Voltage Motors for Chemical, Oil and Gas,” abb.com Since nearly 70% of industrial electricity use is motor-related, swapping legacy units cuts Scope 2 emissions and qualifies companies for ISO 50001 certification incentives. Chemicals and petrochemicals operators consider verifiable efficiency a procurement prerequisite, turning compliance into a competitive differentiator. Lifecycle transparency and recyclability guidelines also force redesign around sustainable materials, creating demand for rare-earth-free topologies. The resulting multi-year replacement cycle underpins stable volume growth for premium-priced offerings.

Smart Factory Automation Demand

Industry 4.0 strategies require motors that support integrated sensing, edge computing, and rapid reconfiguration. Semiconductor advances enable AI-driven predictive maintenance modules directly on the drive, as evidenced by STMicroelectronics’ embedded solutions highlighted in recent automation showcases.[2]Food Engineering, “SEW-EURODRIVE Introduces DR2C Motor,” foodengineeringmag.comDiscrete manufacturing lines in automotive and electronics now demand synchronized multi-axis motion, fostering incremental revenue from servo, permanent-magnet, and electronically commutated designs. Integrated motor-drive-controller packages simplify commissioning, shorten downtime, and can lower plant energy use by up to 15% compared with legacy speed-control architectures. Cyber-secure digital interfaces also emerge as essential safeguards for connected production assets.

Rise of HVAC and Water Infrastructure

Infrastructure programs channel steady funding toward energy-efficient HVAC and water treatment equipment. The U.S. Infrastructure Investment and Jobs Act earmarked USD 50 billion for safe drinking water, including USD 15 billion to phase out lead service lines, stimulating demand for motorized pumps and actuators.[3]SEB Climate & Sustainable Finance, “The Green Bond: Investing in Water,” sebgroup.com California Water Service Group invested USD 471 million in 2024, installing 26 generator and motor control centers to bolster system resilience. Water-sector automation posts a projected 10% CAGR through 2033, while HVAC retrofits increasingly specify variable-speed drives that enhance building performance and support emerging green-building certification.

Trade-Tariff-Driven Reshoring of Motor Supply Chains

Build America Buy America clauses within recent U.S. infrastructure laws prompt suppliers like Sulzer to expand domestic production, ensuring compliance and shortening lead times. Customers in advanced economies now favor proximate, resilient supply chains over pure cost, opening share-gain opportunities for regional manufacturers with integrated capabilities. Reshoring also enables collaborative engineering with OEMs, accelerating application-specific developments. Reduced transport distance translates into lower embodied carbon, aligning with corporate ESG targets and strengthening bid competitiveness for public procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital outlay | -0.8% | Global, emerging markets most exposed | Short term (≤ 2 years) |

| Supply-chain raw-material volatility | -0.6% | Global, metal-intensive regions | Medium term (2-4 years) |

| Shortage of power-electronics chips | -0.4% | Global, acute in Asia Pacific | Short term (≤ 2 years) |

| Skilled labor gap for digital commissioning | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Outlay

Premium IE5-rated motors cost up to 40% more than standard-efficiency units, stretching the budgets of small and medium enterprises. Upgrades often require complementary investments in variable-frequency drives and digital monitoring, pushing payback horizons beyond three years for low-utilization assets. Limited access to specialized financing in emerging markets further delays replacement decisions. Retrofit projects present added costs for mounting and wiring modifications, making capital expenditure a persistent enrollment hurdle despite favorable lifecycle economics.

Supply-Chain Raw-Material Volatility

Quarterly copper price swings of 20% can escalate production costs and force manufacturers to issue rapid list-price revisions, frustrating procurement cycles. Dependence on China for rare-earth magnets heightens exposure to export restrictions on gallium and germanium, pressuring permanent-magnet motor makers.[4]WTW, “Collateral Damage in Semiconductor Supply Chains,” wtwco.com Specialty steel lamination lead times sometimes extend to 12 months, delaying large-frame builds. Although synchronous-reluctance designs lessen magnet reliance, they require more sophisticated control electronics, neutralizing some cost advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Motor: AC Dominance Faces Servo Disruption

AC induction units retained a 44.78% industrial motors market share in 2025, underscoring their reliability and attractive cost profile. However, smart AC servo technology is expanding at a 5.03% CAGR, fueled by precision automation that values closed-loop feedback and predictive maintenance. The industrial motors market size tied to permanent-magnet synchronous equipment grows as energy-sensitive operations seek compact, high-torque solutions, though rare-earth price volatility injects risk. SEW-EURODRIVE’s DR2C IE5 permanent-magnet launch in 2025 achieved 50% lower losses versus IE3 asynchronous models, confirming the efficiency upside. DC and electronically commutated motors keep niche roles where precise speed control, low acoustic emissions, or maintenance-free brushless designs matter. Manufacturers balance technology roadmaps between magnet-free synchronous-reluctance options and advanced servo architectures to satisfy both cost and performance criteria.

Market demand tilts toward motors with integrated sensors and edge computing that deliver condition monitoring out of the box. This feature set commands premiums yet reduces unplanned downtime, appealing to discrete manufacturers. Servo growth also benefits from broader availability of miniaturized encoders and semiconductor gate drivers. As digital twins and adaptive control proliferate, the competitive gap widens between legacy induction products and intelligence-enabled offerings. Vendors promote lifecycle savings rather than upfront price, repositioning value propositions around uptime assurance and energy visibility.

By Voltage: Low-Voltage Versatility Drives Market Leadership

Low-voltage products below 1 kV captured 62.31% of industrial motors market size in 2025 and are projected to record the quickest 4.91% CAGR through 2031 thanks to their broad applicability in HVAC, water treatment, and conveyor systems. Medium-voltage solutions from 1 kV to 35 kV address heavy-duty pumps, compressors, and refinery equipment where high power density offsets higher cost. High-voltage machines above 35 kV stay concentrated in utility-scale installations and large process-industry drives. The industrial motors market share advantage of low-voltage units derives from standardized IEC and NEMA frames that streamline replacement and inventory for end users. ABB’s MV Titanium concept integrates motor and control in a turnkey powertrain, signaling a push to simplify medium-voltage adoption barriers. Energy savings of up to 54% in pumping duty can justify premium variable-speed packages in the mid-range voltage segment. For low-voltage lines, Internet-connected starters and compact drives are now default options, helping facility managers meet decarbonization targets without disruptive retrofit complexity.

Variable-speed operations continue to replace throttle-valve or bypass strategies, shrinking overall power demand. As grid-interactive buildings proliferate, low-voltage motors paired with smart drives enable demand response and power-quality support. Growth also rides on packaged skid solutions for water utilities and food processing, where OEMs preassemble motors, pumps, controls, and sensors to minimize onsite work. High-voltage adoption remains limited by insulation system cost and specialized maintenance skills, keeping its trajectory stable but slower than lower-voltage tiers.

By End User: Discrete Manufacturing Accelerates

Industrial machinery covered the largest revenue slice at 17.86% in 2025, yet discrete manufacturing shows a brisk 5.95% CAGR through 2031 as automotive and electronics plants pivot to flexible automation. The industrial motors market size attached to oil and gas remains significant for hazardous-area certified models, while water and wastewater utilities drive steady volume through pump and blower upgrades. Discrete lines require rapid start-stop cycles and exact positioning, pushing demand for servo and permanent-magnet solutions with on-motor encoders. Integrated safety over ethernet and PROFINET-ready drives ease compliance for collaborative robotics.

Electrification trends in vehicle assembly generate new torque and speed profiles that legacy induction motors cannot match. In pharmaceutical and food environments, hygienic stainless-steel motors such as ABB’s IP69 Food Safe SP5+ win share due to washdown resilience and ultra-premium efficiency. Chemical and petrochemical operators value explosion-proof certifications and predictive diagnostics suited to continuous duty. Mining applications lean on heavy-frame units with high starting torque to power crushers and conveyors in dusty, high-vibration settings. Each end-user category thus aligns around application-specific performance and compliance needs, spurring portfolio breadth among leading suppliers.

Geography Analysis

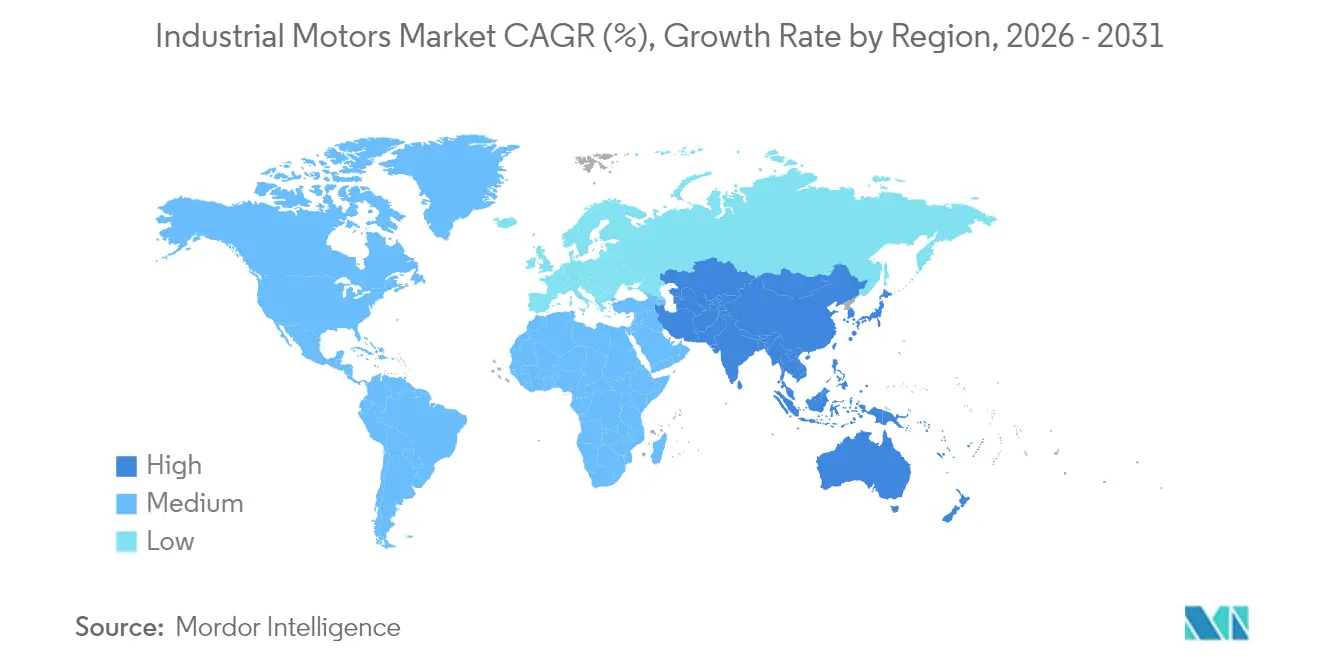

Asia Pacific maintained 51.32% share and posts the fastest 5.66% CAGR to 2031, supported by China’s large installed base and India’s goal to lift manufacturing’s GDP weight from 17% to 21% within seven years. Thailand’s Board of Investment approved investments worth THB 200 billion (USD 5.4 billion) for rail and digital projects, reinforcing Southeast Asian demand. Japan’s machine-tool order recovery above JPY 120 billion (USD 1.06 billion) in February 2025 signals renewed capital expenditure in precision equipment. Asia’s dense supplier ecosystem accelerates technology diffusion, though policy shifts toward sustainability push manufacturers to upgrade efficiency classes.

North America benefits from the Infrastructure Investment and Jobs Act, which funds water-system modernization and propels motor control center upgrades. Build America Buy America rules stimulate domestic capacity expansions, as seen in Sulzer’s U.S. facility investments. European demand emphasizes ultra-premium efficiency and rare-earth-free designs under the Ecodesign Directive. Suppliers compete on verified lifecycle sustainability and advanced digital services, creating higher average selling prices.

Middle East and Africa and South America pursue capacity growth in mining, oil, and water infrastructure. Operators prioritize hazardous-area certified motors with high ingress protection and corrosion-resistant coatings. Global water-security projections of USD 12.6 trillion through 2034 reinforce long haul demand for pump-related motors. Regional strategies thus divide between high-efficiency retrofits in mature economies and capacity additions in developing markets.

Competitive Landscape

The industrial motors market features moderate consolidation: ABB, Siemens, and WEG combine broad portfolios with global service networks that underpin customer loyalty. KPS Capital Partners acquired Siemens’ Innomotics division, positioning the standalone entity to pursue flexible growth outside a conglomerate framework. WEG’s purchase of Volt Electric Motor strengthens its North American reach and NEMA product depth. Technology differentiation centers on efficiency, digital integration, and application-specific packages rather than price alone. ABB’s IE6 synchronous-reluctance line entrenches a premium niche by lowering energy losses 20% versus IE5 peers.[6]ABB, “Low Voltage Motors for Chemical, Oil and Gas,” abb.com

Edge-AI predictive diagnostics emerge as a white-space opportunity; early entrants bundle hardware, firmware, and cloud analytics to deliver subscription revenue. Rare-earth-free motors gain momentum as supply-chain risk persists. Drive makers and automation vendors increasingly blur category lines through joint ventures and vertical integration, simplifying procurement for end users. Medium-size specialists compete via deep application expertise or fast customization lead times. Raw-material volatility and semiconductor shortages pose headwinds, but suppliers leverage multi-sourcing and localized inventory to maintain delivery reliability.

Recent regulatory tightening and sustainability reporting amplify after-sales service importance; lifecycle assessments and refurbishment offerings differentiate brands. Market participants expand digital marketplaces for spare parts and condition-monitoring services, monetizing installed bases. As integrated powertrain concepts mature, competition shifts from individual motor SKUs toward holistic electrified systems that include drives, gearboxes, and software.

Industrial Motors Industry Leaders

ABB Ltd.

Emerson Electric Co.

Nidec Industrial Solutions

Johnson Electric Holdings Limited

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ITT introduced VIDAR, an industrial smart motor optimized for fluid-process reliability.

- March 2025: ABB launched the MV Titanium speed-controlled medium-voltage motor, the world’s first integrated electromechanical powertrain for MV applications.

- March 2025: SEW-EURODRIVE introduced the DR2C IE5 permanent-magnet motor featuring interior PM rotor design and up to 50% lower losses versus IE3 asynchronous alternatives.

- March 2025: Bosch Rexroth unveiled the Hägglunds Thunder PM synchronous torque motor family delivering nominal torque to 200 kNm and peak power to 4,300 kW.

- March 2025: Schneider Electric released the TeSys Deca Advanced contactor with wide-band coil supporting 24 V-500 V AC/DC and one-click wiring.

Global Industrial Motors Market Report Scope

An industrial motor is an electric motor that converts electricity into mechanical energy. These motors produce rotary or linear forces and are typically powered by alternating current (AC) resources such as power grids or generators. However, some may be supplied by direct current (DC) resources like batteries.

The industrial motors market is segmented by type of motor (alternating current (AC) motors, direct current (DC) motors, and other types of motors), voltage (high voltage, medium voltage, and low voltage), end user (oil and gas, power generation, mining and metals, water and wastewater management, chemicals and petrochemicals, discrete manufacturing, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

By Type of Motor

| Alternating Current (AC) Motors |

| Direct Current (DC) Motors |

| Servo Motors |

| Permanent-Magnet Synchronous Motors (PMSM) |

| Electronically Commutated (EC) / BLDC Motors |

By Voltage

| Low Voltage (< 1 kV) |

| Medium Voltage (1-35 kV) |

| High Voltage (> 35 kV) |

By End User

| Oil and Gas |

| Power Generation |

| Mining and Metals |

| Water and Wastewater |

| Chemicals and Petrochemicals |

| Discrete Manufacturing (Automotive, Electronics) |

| Food and Beverage |

| Other End User Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Type of Motor | Alternating Current (AC) Motors | |

| Direct Current (DC) Motors | ||

| Servo Motors | ||

| Permanent-Magnet Synchronous Motors (PMSM) | ||

| Electronically Commutated (EC) / BLDC Motors | ||

| By Voltage | Low Voltage (< 1 kV) | |

| Medium Voltage (1-35 kV) | ||

| High Voltage (> 35 kV) | ||

| By End User | Oil and Gas | |

| Power Generation | ||

| Mining and Metals | ||

| Water and Wastewater | ||

| Chemicals and Petrochemicals | ||

| Discrete Manufacturing (Automotive, Electronics) | ||

| Food and Beverage | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the industrial motors market in 2026?

The industrial motors market size reached USD 23.39 billion in 2026 and is projected to grow steadily through 2031.

Which region leads current demand?

Asia Pacific held 51.32% of global demand in 2025, driven by manufacturing expansion and accelerating automation.

What segment grows fastest through 2031?

Discrete manufacturing shows the highest 5.95% CAGR by adopting flexible, precision-oriented motor-drive packages.

How are efficiency regulations shaping product design?

EU Ecodesign and updated NEMA Premium rules drive the shift toward IE5 and IE6 motors, spurring synchronous-reluctance and magnet-free innovations that lower energy losses by up to 20%.

Why is reshoring relevant for buyers in North America?

Build America Buy America requirements incentivize local production, reducing lead times and aligning with ESG goals by cutting transport emissions.

What technology trend offers new value propositions?

Edge-AI predictive maintenance embedded in motor drives improves uptime and can reduce plant energy use by up to 15% versus traditional control architectures.

Page last updated on: