Industrial AI Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

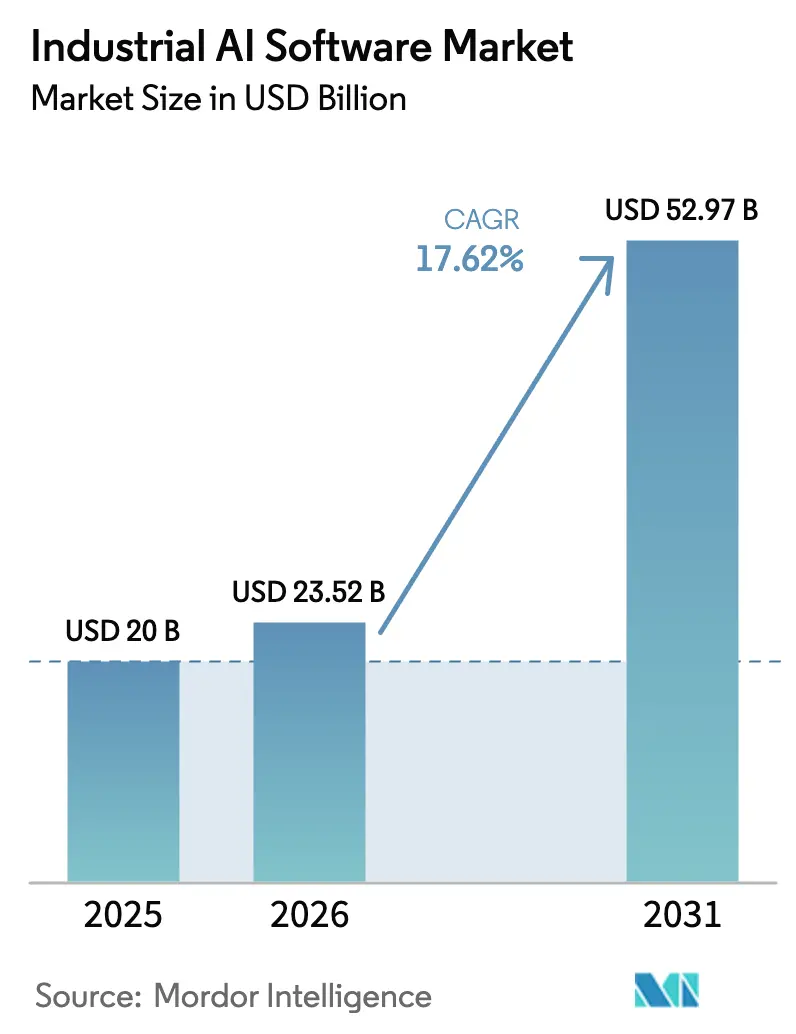

| Market Size (2026) | USD 23.52 Billion |

| Market Size (2031) | USD 52.97 Billion |

| Growth Rate (2026 - 2031) | 17.62% CAGR |

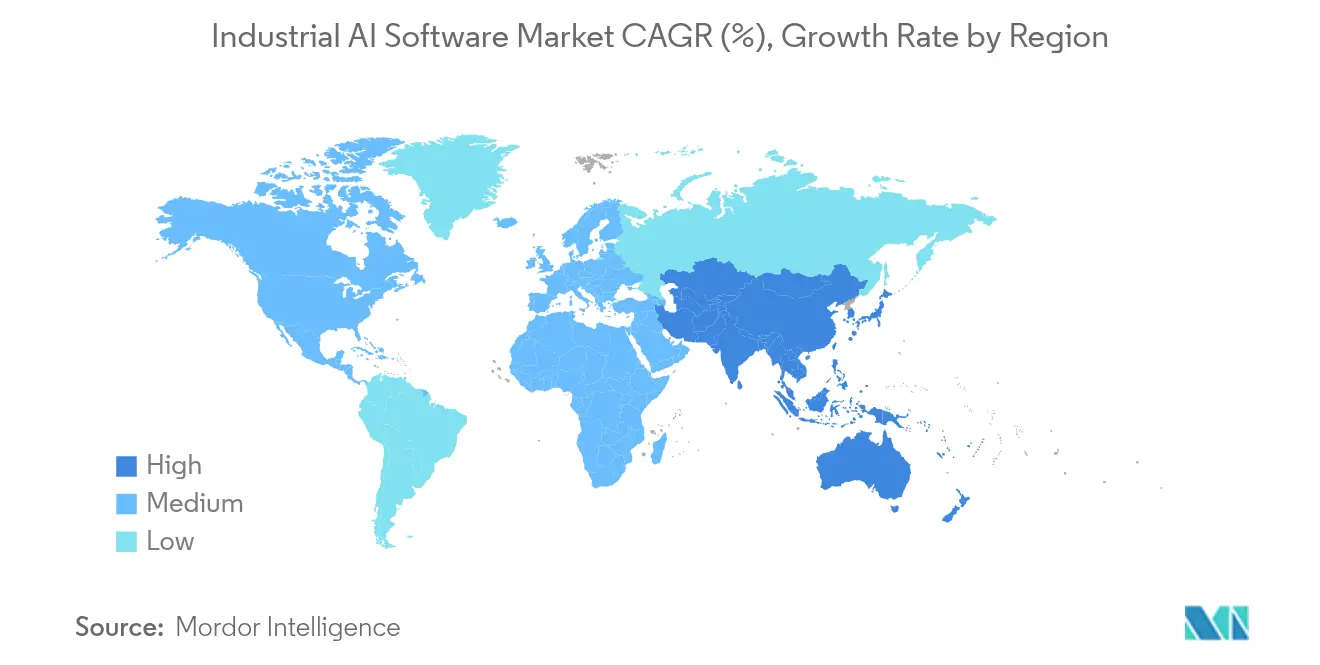

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

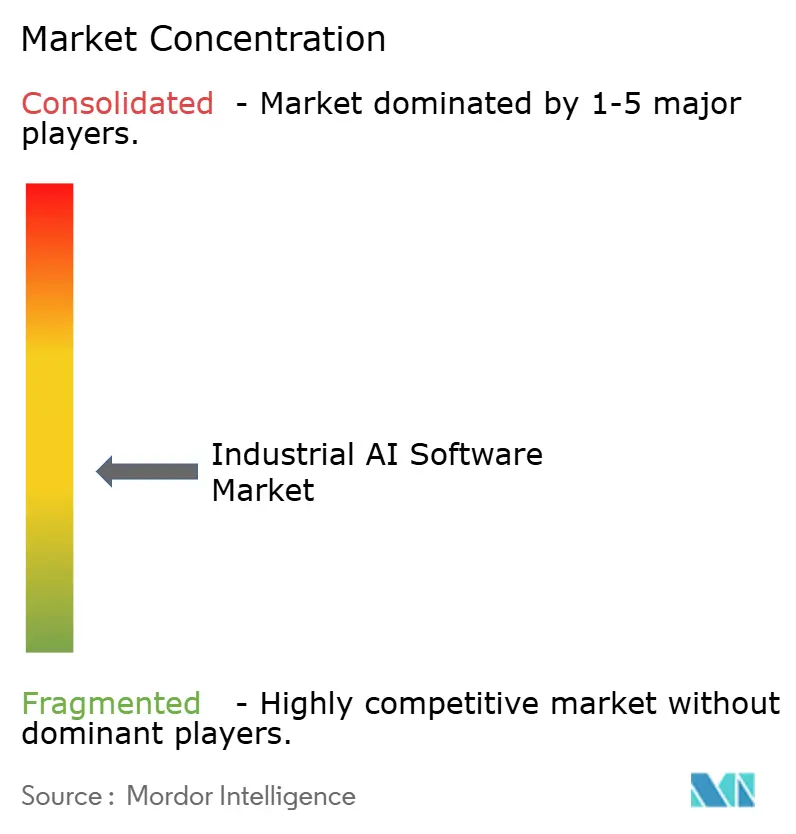

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial AI Software Market Analysis by Mordor Intelligence

Industrial AI Software Market size in 2026 is estimated at USD 23.52 billion, growing from 2025 value of USD 20 billion with 2031 projections showing USD 52.97 billion, growing at 17.62% CAGR over 2026-2031.

This trajectory mirrors the rapid fusion of factory-floor operational technology with advanced artificial intelligence that now steers everything from process optimization to touchless documentation. Generative AI deployments spearhead this shift, Siemens recorded 90% touchless processing of delivery notes within weeks of going live, underscoring AI’s capacity to shrink manual workloads.[1]Roland Busch, “Industrial AI pushes touchless processing to new heights,” siemens.com Widespread investments in hybrid-cloud infrastructure strengthen scalability, while sovereign-cloud zones ease data-residency concerns and speed global rollouts. North America preserves its lead, but APAC’s manufacturing corridors inject the highest velocity, largely on the strength of Japan’s robotics ecosystem and China’s automation spending. Meanwhile, regulatory reforms such as the EU AI Act elevate demand for explainable solutions, encouraging vendors to add audit-grade transparency layers. Market rivalry stays moderate as hyperscalers, automation stalwarts, and niche startups jockey for early wins in predictive analytics and computer vision.

Key Report Takeaways

- By deployment type, cloud-based solutions led with 60.58% of the Industrial AI Software market share in 2025 and are projected to expand at a 19.65% CAGR to 2031.

- By end-user industry, automotive and transportation held 22.48% of the Industrial AI Software market size in 2025, while energy and utilities is poised to grow at a 21.95% CAGR between 2026-2031.

- By application, predictive maintenance was at 20.12% of the Industrial AI Software market size 2025, while the predictive maintenance sector is poised to grow at a rate of 25.75% CAGR between 2026-2031.

- By geography, North America commanded a 36.45% share of the Industrial AI Software market size in 2025; Asia-Pacific is advancing at a 20.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial AI Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Predictive-maintenance adoption cuts downtime | +4.2% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Growing volumes of industrial big-data streams | +3.8% | Global, APAC manufacturing hubs | Long term (≥ 4 years) |

| National Industry 4.0 incentive programs | +3.1% | Europe and APAC, spill-over to North America | Medium term (2-4 years) |

| Generative-AI copilots ease labor shortages | +4.5% | Global, acute impact in developed economies | Short term (≤ 2 years) |

| Carbon-accounting mandates (Scope 3) | +2.4% | Europe and North America, expanding into APAC | Long term (≥ 4 years) |

| Edge-AI deployment for real-time decisions | +2.7% | Global, asset-intensive industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Predictive-maintenance adoption cuts unplanned downtime

Plants now slash maintenance budgets by 25-30% and breakdowns by 70-75% after switching from calendar-based to AI-led routines. Tennessee Valley Authority spared 40,000 customer outages in two months by using AI-driven grid controls, proving that cost avoidance scales well in capital-intensive utilities. Bosch’s Ansbach site moved defect detection to edge-based vision AI, keeping latency low and inspectors focused on higher-value tasks.[2]Bosch Group, “AI Vision systems improve defect detection at Ansbach,” bosch.com Forward-looking operators view these gains as vital because every hour of unplanned stoppage can cost USD 50,000 or more.

Growing volumes of industrial big-data streams

Single factories now generate terabytes of sensor output per day, creating fertile ground for machine-learning models. Ndustrial processes 100 million data points daily across 122 plants, illustrating why data infrastructure is edging toward cloud-native lakes that feed AI pipelines. Yet inconsistent naming conventions and siloed historians remain bottlenecks, urging CIOs to invest in semantic layers that boost model accuracy and shorten training cycles.

National Industry 4.0 incentive programs

Germany’s Innovation Park Artificial Intelligence and Japan’s regional AI sandboxes subsidize pilot projects, lowering risk for small and mid-size manufacturers. Such shared testbeds accelerate learning curves, standardize data-sharing rules, and create positive network effects across supplier tiers.

Generative-AI copilots ease engineering labor shortages

Retiring experts take tacit know-how with them, yet generative AI plugs the gap by translating decades of ladder-logic scripts into modern code within seconds. Siemens Industrial Copilot now sits inside its TIA Portal and halves PLC programming time. Likewise, a Daikin-Hitachi AI agent diagnoses HVAC faults with 90% accuracy in 10 seconds, lifting junior technician productivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and IP-protection concerns | -2.8% | Europe and APAC, regulatory spillover global | Medium term (2-4 years) |

| Scarcity of OT-AI integration talent | -2.1% | Global, acute in developed markets | Long term (≥ 4 years) |

| Legacy automation infrastructure lock-in | -1.9% | North America and Europe, aging asset base | Long term (≥ 4 years) |

| GPU hardware supply volatility | -1.4% | Global, concentrated impact on edge sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty and IP-protection concerns

The EU AI Act categorizes many factory-floor algorithms as high-risk, mandating local data retention and audit trails. Multinational manufacturers, therefore, spin up sovereign clouds, AWS earmarked EUR 7.8 billion for such European zones, to meet residency rules while still tapping hyperscale AI services aws.amazon.com. Separate deployments inflate costs, but firms weigh them against the penalties of non-compliance.

Scarcity of OT-AI integration talent

Industrial AI demands rare hybrids who grasp both legacy PLC networks and modern ML frameworks. Hitachi plans to upskill 50,000 staffers in AI disciplines, highlighting the urgent workforce gap. Without these cross-domain professionals, AI pilots risk stalling at proof-of-concept stages, slowing adoption curves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Accelerates

Cloud-based solutions accounted for 60.58% of the Industrial AI Software market share in 2025 and posted the strongest trajectory at 19.65% CAGR through 2031 as firms consolidate workloads on scalable, pay-as-you-grow platforms. The Industrial AI Software market size for cloud deployments is forecast to reach USD 35.54 billion by 2031, reflecting rising confidence in multi-tenant security models. Hybrid architectures further alleviate sovereignty fears by isolating sensitive datasets on regional nodes while feeding anonymized features to central model training hubs.

On-premise installations remain critical in regulated verticals that demand deterministic latency and strict asset control. Fortune 2000 manufacturers often retain on-site clusters to dodge unpredictable egress fees from cloud activity spikes, yet they increasingly orchestrate these clusters through the same containerized stacks used in the cloud. Consequently, both deployment archetypes now complement rather than cannibalize each other, stimulating continual spending across the Industrial AI Software market.

By End-User Industry: Energy Transformation Leads Growth

Energy and utilities is the breakout performer, advancing at 21.95% CAGR as autonomous refinery trains and self-healing grids transition from pilots to production. ENEOS and Preferred Networks unveiled full AI-run crude distillation units, proving industrial AI can handle multi-variable processes without human intervention. Automotive and transportation still tops revenue at 22.48% of the Industrial AI Software market size due to entrenched investments in autonomous driving and continuous-flow assembly lines.

Electric utilities funnel budgets into grid-aware reinforcement-learning models that shave peak-load spikes and optimize heat-rate efficiency. Conversely, aerospace, healthcare, and retail sectors diversify demand with domain-specific computer-vision and supply-chain tools, ensuring the Industrial AI Software market enjoys growth from multiple industry lanes rather than a single dependency.

By Application: Predictive Maintenance Drives Adoption

Predictive maintenance secures the largest revenue slice as plants realize tangible savings, cost cuts hit 30% and breakdowns plunge 70% after AI implementation. The market benefits because these savings directly fund further AI rollouts across inspection, logistics, and safety. Quality inspection and vision follow, fueled by GPU-accelerated cameras that spot surface anomalies beyond human perception.

Process optimization applications ride on unsupervised-learning models that unearth hidden correlations between temperature curves, vibration signatures, and yield, driving incremental but compounding efficiency. Supply-chain and asset tracking gains momentum where AI fuses indoor RTLS signals with ERP data for end-to-end material visibility. Emerging safety and compliance analytics adds another high-growth pocket, converting video feeds into proactive hazard alerts that curtail workplace incidents.

Geography Analysis

North America contributed 36.45% of the Industrial AI Software market size in 2025, thanks to strong vendor-customer ecosystems and deep cloud penetration. IBM alone booked USD 6 billion in generative-AI orders in 2025 as manufacturers prioritized cognitive upgrades over traditional IT refresh cycles. Microsoft surpassed USD 245 billion in revenue by integrating AI copilots into its software stack, supporting industrial developers with pre-trained models.

Asia-Pacific is the speed leader, expanding at 20.55% CAGR to 2031. Japan’s factories pilot AI-augmented robotics that showcase near-zero downtime, while Chinese state programs funnel subsidies into smart manufacturing clusters. Regional AI investments are set to reach USD 3.4 billion in 2025, nearly triple 2024 outlays, and a 160% bump in China alone illustrates policy-driven urgency.

Europe follows close behind, shaped by rigor around data sovereignty. The Industrial AI Software market here pivots on secure data-spaces such as GAIA-X that let suppliers share telemetry without ceding control to platform operators. Middle East, Africa, and South America charts show mixed but rising adoption. Oil-rich Gulf nations adopt AI to optimize refinery throughput, whereas Latin American producers leapfrog legacy MES layers by directly adopting cloud-native AI suites, sidestepping the technical debt faced in mature economies.

Competitive Landscape

The Industrial AI Software market is moderately concentrated as automation giants, cloud hyperscalers, and deep-tech startups vie for early standard-setting positions. Siemens closed a USD 10.6 billion takeover of Altair Engineering to blend simulation with AI-guided design workflows, showcasing how incumbents acquire niche IP to keep pace with rapid algorithmic advances. IBM spent USD 7.1 billion on HashiCorp to bolster hybrid-cloud tooling that underpins industrial AI deployments.

Startups differentiate by focusing narrowly on pain points, computer-vision firms embed defect-detection models into smart cameras that drop into existing conveyor lines, while predictive-analytics vendors offer subscription models that tie fees to tangible downtime reductions. Partnerships further color the landscape: Honeywell joined forces with Chevron to encode decades of refining know-how into AI-assisted alarms that guide operators in real time. Patent filings spike around edge inference and continuous learning, signaling a race to lock in defensible micro-niches before the market settles.

Despite heightened competition, barriers to entry persist: success demands both domain knowledge and industrial-grade reliability standards such as IEC 62443 security compliance. Vendors that marry AI engines with established SCADA connectors or PLC libraries win easier acceptance, suggesting platform integration is as critical as algorithmic finesse.

Industrial AI Software Industry Leaders

IBM Corporation

Intel Corporation

Nvidia Corporation

Microsoft Corporation

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Daikin Industries and Hitachi initiated trial operation of an AI agent for equipment failure diagnosis at Daikin’s Sakai factory, achieving over 90% accuracy in 10 seconds.

- May 2025: ENEOS and Preferred Networks began the world’s first AI-based autonomous operation of a crude oil processing unit.

- April 2025: IBM reported Q1 2025 revenue of USD 14.5 billion with AI-linked bookings exceeding USD 1 billion.

- March 2025: Siemens completed its USD 10.6 billion acquisition of Altair Engineering to deepen AI-driven simulation.

Global Industrial AI Software Market Report Scope

AI software is a computer program adept of high-complexity tasks, like learning, decision-making, and solving problems. AI software uses machine learning to simulate human intelligence, which can allow the software to complete tasks of increasing nuance and sensitivity. Companies use AI software to help their businesses run more efficiently and find new improvement areas. This can result in the better allocation of human resources, allowing individuals to focus on more strategic and fulfilling tasks.

The industrial AI software market is segmented by type (cloud-based and on-premise), by end-user industries (automotive & transportation, healthcare and life science, aerospace and defense, energy and utilities, retail and consumer packaged goods, and other end-user industries), and by geography (North America, Europe, Asia-Pacific, Latin America and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Cloud-based |

| On-premise |

| Automotive and Transportation |

| Retail and CPG |

| Healthcare and Life Sciences |

| Aerospace and Defense |

| Energy and Utilities |

| Other Industries |

| Predictive Maintenance |

| Quality Inspection and Vision |

| Process Optimization |

| Supply-chain and Asset Tracking |

| Safety and Compliance Analytics |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Deployment Type | Cloud-based |

| On-premise | |

| By End-user Industry | Automotive and Transportation |

| Retail and CPG | |

| Healthcare and Life Sciences | |

| Aerospace and Defense | |

| Energy and Utilities | |

| Other Industries | |

| By Application | Predictive Maintenance |

| Quality Inspection and Vision | |

| Process Optimization | |

| Supply-chain and Asset Tracking | |

| Safety and Compliance Analytics | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the Industrial AI Software market?

The Industrial AI Software market is valued at USD 23.52 billion in 2026.

How fast will the Industrial AI Software market grow?

The market is forecast to post a 17.62% CAGR, reaching USD 52.97 billion by 2031.

Which deployment model grows the fastest?

Cloud-based deployment leads both revenue and growth, expanding at a 19.65% CAGR through 2031.

Which industry segment will be the top growth driver?

Energy and utilities is projected to lead with a 21.95% CAGR as utilities automate grids and refining.

What region shows the highest growth momentum?

Asia-Pacific records the strongest pace at 20.55% CAGR, powered by Japanese and Chinese manufacturing investments.

How does regulation affect adoption in Europe?

The EU AI Act classifies many factory applications as high-risk, driving demand for sovereign-cloud and explainable-AI solutions.

Page last updated on: