AI In Oil And Gas Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

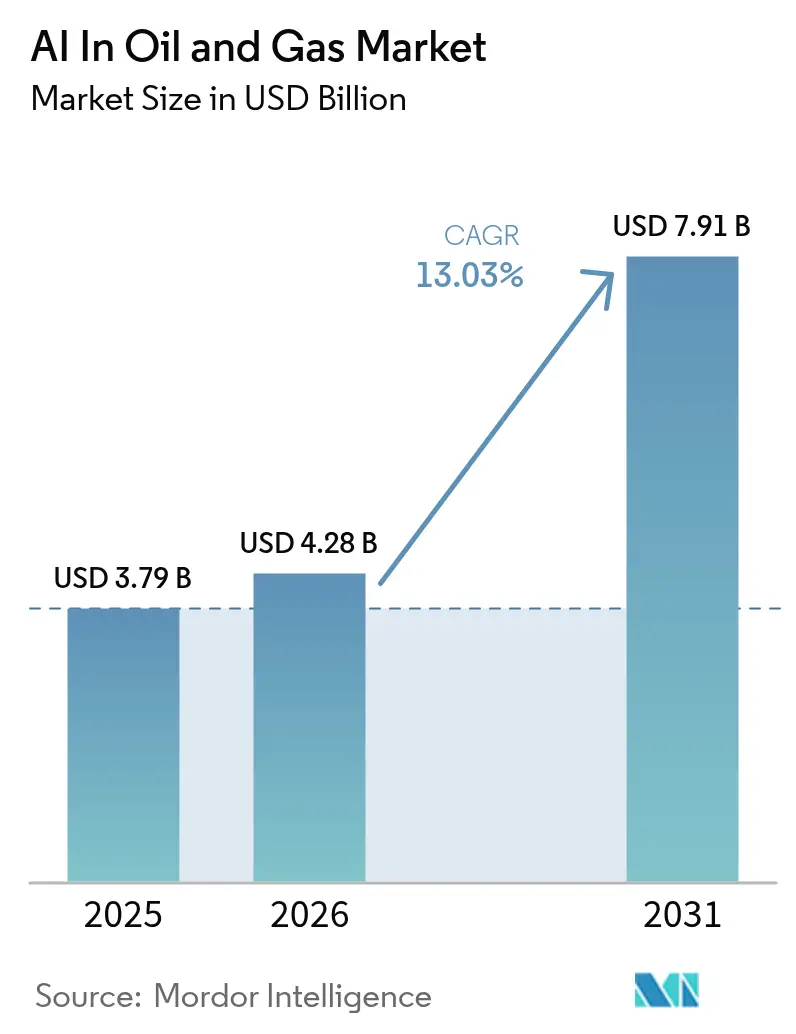

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 7.91 Billion |

| Growth Rate (2026 - 2031) | 13.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Oil And Gas Market Analysis by Mordor Intelligence

The AI in the oil and gas market size was valued at USD 3.79 billion in 2025 and estimated to grow from USD 4.28 billion in 2026 to reach USD 7.91 billion by 2031, at a CAGR of 13.03% during the forecast period (2026-2031). Market growth is being propelled by real-time hydraulic-fracturing control enabled through edge analytics, autonomous drilling systems that trim crew exposure in deepwater projects, and predictive-maintenance programs that curb unplanned downtime. Cloud–edge convergence is shortening model-deployment cycles, while physics-informed models are yielding faster subsurface insights that sharpen well-placement accuracy. Competitive activity is heating up as oilfield service majors embed AI into integrated platforms and cloud hyperscalers launch energy-specific tool sets. Capital-intensive platform rollouts and a thin pool of domain-aware data scientists temper near-term adoption, yet rising ESG requirements for methane-leak detection offer a widening demand runway.

Key Report Takeaways

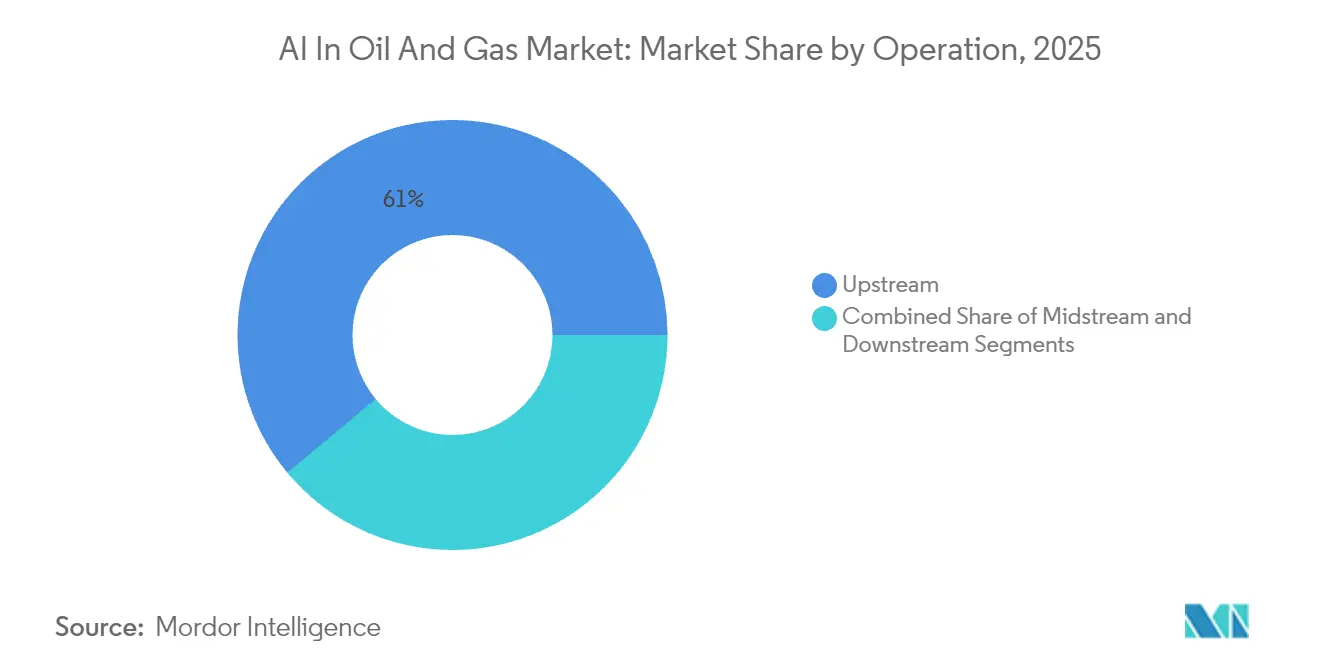

- By operation, upstream held 61.05% of the AI in the oil and gas market share in 2025, while downstream is expanding at a 14.12% CAGR through 2031.

- By solution type, services accounted for 65.80% of the AI in oil and gas market size in 2025, but platform revenues are rising at a 13.74% CAGR.

- By asset location, onshore operations controlled 63.10% of the AI in the oil and gas market size in 2025; offshore activities are growing fastest at a 13.85% CAGR.

- By application, predictive maintenance captured 37.60% of the AI in the oil and gas market share in 2025, whereas HSE compliance is set to advance at a 14.34% CAGR to 2031.

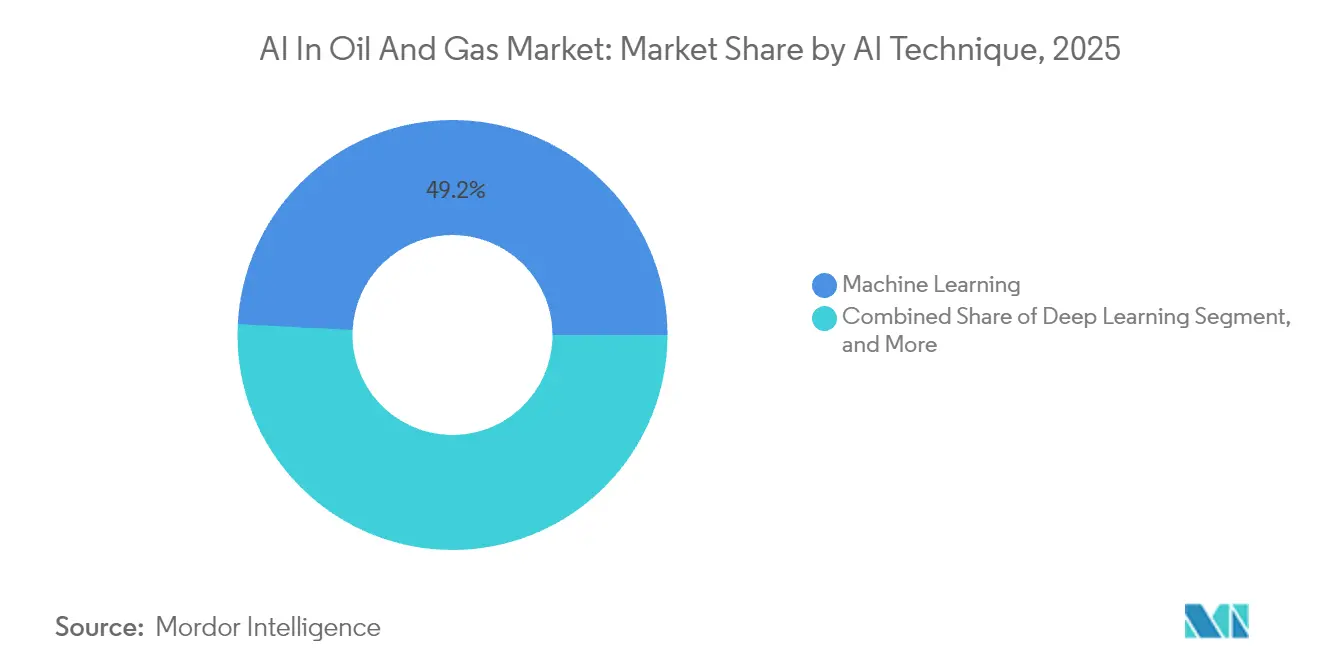

- By AI technique, machine-learning approaches led with 49.20% of 2025 revenue of the AI in the oil and gas market, yet deep-learning methods are projected to register a 14.68% CAGR.

- By deployment mode, on-premises solutions dominated with a 56.50% share in 2025 of the AI in the oil and gas market; edge installations are on track for a 14.15% CAGR.

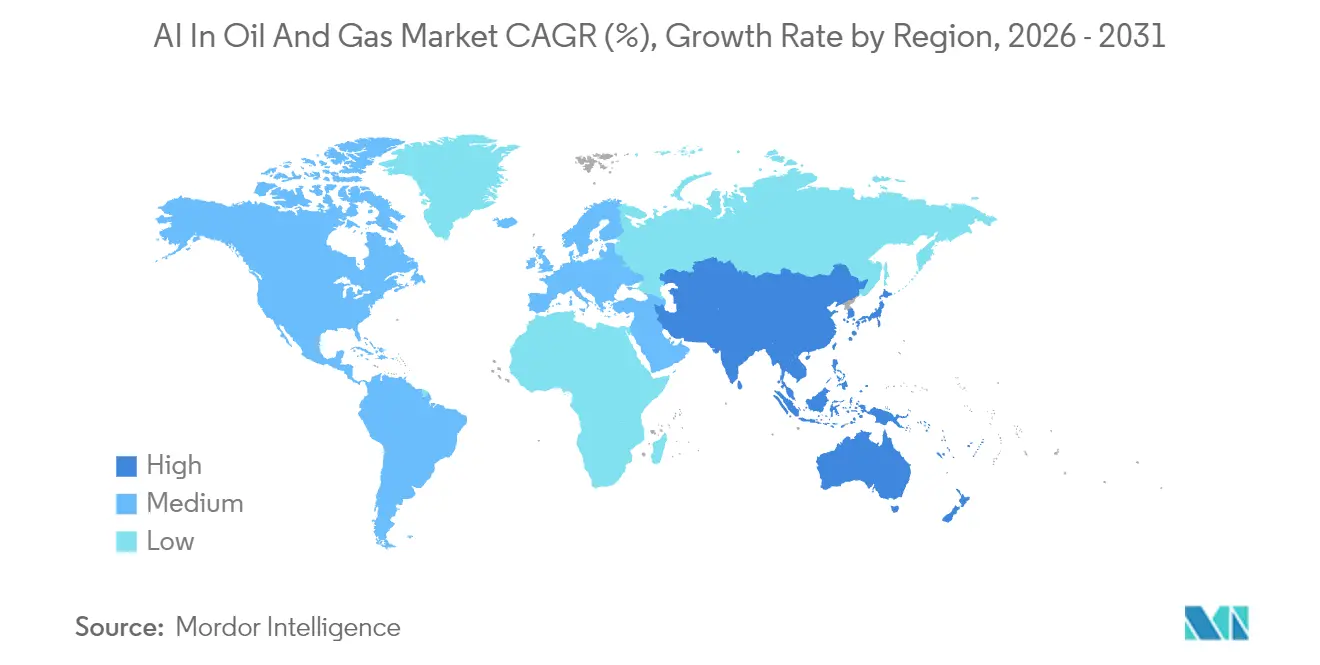

- By geography, North America commanded 35.95% of the 2025 revenue of the AI in the oil and gas market, while Asia-Pacific is projected to post a 14.41% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI In Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex subsurface big-data processing | +3.2% | North America, Middle East, global | Medium term (2-4 years) |

| Lifting-cost pressure amid price swings | +2.8% | North America shale, global | Short term (≤2 years) |

| Predictive-maintenance downtime reduction | +2.1% | Europe, North America, global | Medium term (2-4 years) |

| Fiber-optic sensor AI for frac optimization | +1.9% | North America, emerging Middle East unconventionals | Short term (≤2 years) |

| Methane-leak AI monitoring for ESG mandates | +1.7% | United States, European Union, global | Long term (≥4 years) |

| Autonomous AI deep-water drilling systems | +1.3% | Gulf of Mexico, North Sea, Brazil | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Ability to Process Complex Subsurface Big Data

Seismic archives exceeding 1,500 petabytes at leading operators now require AI accelerators capable of parsing decades of drilling, petrophysical, and production data within hours, lifting drilling-location accuracy by 70% compared with manual methods. ADNOC’s ENERGYai agents trimmed geological-model build times by 75% through autonomous seismic analysis, allowing reservoir engineers to test multiple frac-cluster scenarios in minutes. [1]Carrington Malin, “ADNOC & AIC announce ENERGYai, first-of-its-kind Agentic AI solution,” Middle East AI News, middleeastainews.com The fusion of physics-informed neural networks with historical well data is enabling faster history matches across unconventional plays, directly improving capital-efficiency metrics for large pad developments.

Pressure to Cut Lifting-Costs Amid Price Volatility

Price swings continue to squeeze margins, prompting operators to pursue 25–50% drilling-cost reductions through AI-guided automation. Nabors Industries recorded 30% faster penetration rates after deploying automated drilling controls, while integrated production-optimization software slashed decision-cycle times from days to hours for Permian assets. [2]Blake Wright, “AI Is Here, and It's Helping With Predictive Maintenance in the Oil Field,” Journal of Petroleum Technology, jpt.spe.org Tachyus reported notable gains in artificial-lift efficiency by dynamically adjusting rod-pump parameters using reinforcement-learning algorithms. Mature-field operators increasingly view AI-assisted recovery as essential for extending economic lifespans.

Predictive-Maintenance Driven Downtime Reduction

Unplanned interruptions cost the sector nearly USD 50 billion annually, a gap now addressed by AI-based condition-monitoring platforms that marry IoT sensor streams with edge analytics. Shell’s exception-based surveillance has raised equipment reliability, and Wood PLC’s maint.AI targets 10% downtime cuts and 20–40% maintenance-cost savings. Offshore units gain outsized benefit because helicopter-based crew access is limited, and repair delays carry safety and environmental risk.

Fiber-Optic Sensor + AI for Real-Time Frac Optimization

Distributed acoustic sensing combined with machine-learning models now interprets fracture-propagation signatures in real time, guiding pump-rate and proppant-schedule adjustments that boost recovery factors by 15–20%. Edge processing keeps latency to milliseconds, enabling mid-stage design tweaks during a single frac job. Continuous model retraining on prior completions enhances prediction fidelity, reducing water use and lowering per-barrel lifting costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front CAPEX for AI platforms | −2.1% | Smaller operators worldwide | Short term (≤2 years) |

| Scarcity of oil-and-gas domain data scientists | −1.8% | Developing regions, global | Medium term (2-4 years) |

| Cyber-risk at offshore edge layer | −1.2% | Offshore assets worldwide | Medium term (2-4 years) |

| Legacy SCADA interoperability gaps | −0.9% | Mature fields, global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Up-Front CAPEX for AI Platforms

Enterprise-scale deployments often carry multimillion-dollar price tags for compute clusters, data lakes, and specialized licensing, deterring small independents from adopting full-stack solutions. Data-modernization projects frequently double costs, as siloed SCADA and historian systems must be harmonized before analytics can proceed. Cloud-native offerings such as Azure Data Manager for Energy give operators a consumption-based alternative, yet data sovereignty and latency concerns keep many critical workloads on-premises. [3]“Azure Data Manager for Energy—OSDU Data Platform,” Microsoft, azure.microsoft.com

Scarcity of Oil-and-Gas Domain Data Scientists

Only 15% of reservoir engineers actively apply machine-learning methods, illustrating a narrow talent base. Aramco’s in-house training of 6,000 AI developers and similar university partnerships highlight the growing emphasis on joint upskilling programs. Talent scarcity lengthens project timelines and inflates consulting costs, becoming a structural hurdle for widespread AI penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operation: Upstream Dominance Drives Market Leadership

Upstream activities contributed 61.05% to the AI in the oil and gas market size in 2025, due to seismic interpretation, drilling automation, and production optimization workflows that require sophisticated analytics. These use cases demand pattern-recognition models capable of integrating petrophysical, geomechanical, and drilling parameters to improve well-placement and completion design. As unconventional reservoirs proliferate, upstream operators continue scaling AI-enabled workflows across pad developments, thereby cementing their share leadership within the AI in oil and gas market.

Downstream operations, in contrast, are forecast to post the segment’s fastest 14.12% CAGR through 2031 as refineries adopt model-predictive control for fuel blending and virtual sensors for real-time quality assurance. Generative-AI-powered document processing is shortening regulatory-report cycles, and computer-vision algorithms now track corrosion hotspots inside distillation columns. The trajectory signals greater AI democratization beyond exploration and production, reflecting a shift toward integrated optimization across the entire value chain of AI in the oil and gas industry.

By Solution Type: Services Lead While Platforms Accelerate

Services captured 65.80% of AI in the oil and gas market revenue in 2025, showcasing operators’ preference for domain experts to tailor models to asset-specific constraints. Advisory, data engineering, and model-maintenance contracts form the backbone of service revenues as companies iterate toward continuous-improvement loops.

Integrated platforms, however, are expanding at a 13.74% CAGR as operators look to standardize data ingestion, model management, and application orchestration. SLB’s Lumi and Baker Hughes’ Cordant™ suites typify multi-domain environments that embed large language models, computer-vision pipelines, and physics-informed simulators. The trend suggests a future transition from labor-intensive deployments to configurable platforms that scale enterprise-wide, a key inflection for the AI in oil and gas market.

By Asset Location: Onshore Operations Lead, Offshore Accelerates

Onshore sites made up 63.10% of 2025 revenue due to North American shale basins, where mobile rigs, pad drilling, and robust 4G/5G coverage simplify sensor rollout. The relative accessibility allows rapid iteration of well-optimization models and continuous production-surveillance loops, supporting strong cash-flow generation and reinvestment in digital programs.

Offshore installations, though smaller in current share, are projected to log a 13.85% CAGR as autonomous robotics and remote-operations centers mitigate crew-change costs and safety risks. TotalEnergies’ remotely controlled robots and SLB’s AI-enhanced deep-water drilling contracts illustrate demand drivers where latency-sensitive edge nodes execute control logic near subsea BOPs. The result is a widening array of high-value offshore use cases, strengthening the growth outlook for AI in the oil and gas market.

By Application: Predictive Maintenance Dominates, HSE Compliance Accelerates

Predictive-maintenance held 37.60% of 2025 spending, underpinned by clear ROI in turbine, compressor, and PCP monitoring. Operators leverage anomaly-detection models to align overhaul windows with logistics schedules, driving material savings in offshore FPSO campaigns. The practice remains foundational for digital programs across the AI in the oil and gas market.

HSE compliance is projected to deliver the fastest 14.34% CAGR as methane-leak surveillance, computer-vision PPE checks, and fatigue-detection wearables gain regulatory traction. U.S. methane-emitters must deploy continuous monitoring under new EPA rules, and computer-vision systems now track safety-critical valve positions with sub-second latency using enhanced YOLO V8 networks. The uptick shows how external mandates can unlock budget lines for AI programs beyond efficiency gains, expanding the value proposition of the AI in the oil and gas industry.

By AI Technique: Machine Learning Leads, Deep Learning Accelerates

Machine-learning algorithms generated 49.20% of 2025 spending, reflecting their maturity in time-series regression, clustering, and classification tasks that dominate equipment and production analytics. Gradient-boosting and random-forest models remain the workhorses for structured SCADA datasets and are embedded in most commercial predictive-maintenance offerings.

Deep-learning networks, however, are on a 14.68% CAGR ascent courtesy of vision-based valve monitoring, large language models for document extraction, and transformer-based seismic interpretation. ADNOC’s 70-billion-parameter seismic agent validates the scalability of foundation models in domain-specific contexts. The blend of traditional and neural techniques within unified MLOps frameworks signals a maturation phase for AI in the oil and gas market.

By Deployment Mode: On-Premises Dominates, Edge Computing Surges

On-premises architectures retained a 56.50% share in 2025, given operator control over sensitive reservoir and production data and the deterministic performance guarantees achievable with local hardware. High-bandwidth imaging workloads such as 4D seismic inversion continue to run in operator data centers where latency to petabyte-scale stores is minimal.

Edge computing is forecast to surge at a 14.15% CAGR as ruggedized devices execute models on drill ships, unmanned platforms, and isolated gas plants where connectivity is intermittent. Sensia’s oilfield-hardened edge units integrate zero-trust security layers and FPGA accelerators for low-power inference. Hybrid patterns that federate learning in the cloud and inference at the edge are poised to become mainstream, reshaping deployment economics across the AI in oil and gas market.

Geography Analysis

North America held 35.95% of 2025 revenue, anchored by prolific shale developments and wide adoption of automated rigs, predictive-maintenance suites, and methane-leak analytics. Companies such as ExxonMobil, Chevron, and Pioneer Natural Resources run cloud-native subsurface workflows at petabyte scale, supported by mature fiber and 5G backbones. Government stimulation packages for infrastructure modernization further underpin digital uptake, while a thriving startup ecosystem accelerates tool creation for AI in the oil and gas market.

Europe maintains a technologically advanced yet smaller share, with North Sea operators focusing on offshore robotics and CCS monitoring. Regulations on carbon intensity and methane emissions propel AI-enabled environmental compliance, particularly in Norway and the Netherlands. Cross-sector collaboration on open data standards like OSDU fosters interoperability, reducing integration friction across installations.

Asia-Pacific is the fastest-growing region at a 14.41% CAGR, fueled by upstream investments in India, Indonesia, and China. PTTEP’s portfolio of 65 digital features and Indian refiners’ predictive-maintenance pilots illustrate a regional shift toward enterprise-wide digitization. Rising LNG demand, energy-security objectives, and a swelling pool of software engineers provide structural tailwinds for AI rollout across the AI in oil and gas market.

The Middle East and Africa region leverages sovereign AI programs and megaproject budgets to scale data centers and supercomputing clusters. ADNOC’s generation of USD 500 million in AI value during 2024, along with Aramco’s METABRAIN LLM initiative, signals rapid capability uplift. Government mandates for economic diversification and net-zero commitments are translating into expanded funding for leak-detection, drilling automatio,n and flare-reduction analytics, strengthening regional momentum within the AI in oil and gas market.

Competitive Landscape

The marketplace is moderately concentrated, with oilfield service majors, supermajors, and cloud hyperscalers driving platform standardization. SLB’s collaborations with NVIDIA, TotalEnergies, and Geminus AI demonstrate a strategy of combining high-performance compute with physics-based model builders for full-value-chain coverage. [4]“SLB awarded multi-region contracts by Shell to deploy AI-enhanced deepwater drilling,” World Oil, worldoil.com Baker Hughes is deepening Azure-enabled Cordant modules for production optimization, while Halliburton embeds micro-services into its iEnergy platform to streamline reservoir-model orchestration.

Specialist vendors supply niche capabilities such as Ambyint’s rod-lift optimization and Welligence’s decision-support analytics. Venture funding remains active, with Ambyint securing USD 26.5 million and Welligence attracting USD 41 million, underscoring the appetite for focused solutions targeting well-specific pain points. Cybersecurity pure-plays are emerging to protect edge nodes in offshore settings where attack surfaces expand with every sensor addition.

Competitive dynamics are shifting from isolated pilots toward enterprise-scale rollouts that necessitate MLOps, data-governance, and change-management expertise. Players capable of bundling platforms, advisory, and managed services under a single commercial construct are best positioned to capture wallet share as the AI in the oil and gas market matures.

AI In Oil And Gas Industry Leaders

C3.ai Inc.

SparkCognition Inc.

Uptake Technologies Inc.

Tachyus Corporation

Akselos SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Aramco deployed comprehensive AI systems, partnering with Qualcomm on generative-AI inferencing centers and training 6,000 developers as part of its METABRAIN initiative.

- January 2025: SLB launched the Lumi data and AI platform featuring large language models optimized for energy workflows.

- December 2024: SLB and ADNOC Drilling formed Turnwell Industries LLC to complete 144 unconventional wells by Q4 2025 using AI-driven smart-drilling designs.

- December 2024: AIQ, ADNOC, Baker Hughes, and CORVA commenced a real-time rate-of-penetration optimization project leveraging historical drilling data.

- November 2024: ADNOC and AIQ unveiled ENERGYai with a 70-billion-parameter LLM and autonomous seismic agents that cut model-build times by 75%.

Global AI In Oil And Gas Market Report Scope

The oil and gas industry is increasingly turning to artificial intelligence (AI) as a cost-saving measure. AI applications, ranging from boiler diagnostics to drilling operations, are becoming integral in optimizing processes across the industry's upstream, midstream, and downstream segments. In the exploration and production areas, AI is leveraged for tasks like quality control, predictive maintenance, and planning. The report also delves into AI services, encompassing both professional and managed services.

This study evaluates the revenue generated by AI solutions from various industry players. The report not only scrutinizes market size but also delves into key parameters, growth drivers, and major vendors, all crucial for estimating market trends and growth rates during the forecast period.

The AI in oil and gas market is segmented by operation (upstream, midstream, and downstream), type (platform and services), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in value terms (USD) for all the above segments.

| Upstream |

| Midstream |

| Downstream |

| Platform |

| Services |

| Onshore |

| Offshore |

| Quality Control |

| Production Optimisation |

| Predictive Maintenance |

| HS&E Compliance |

| Exploration and Drilling |

| Other Applications |

| Machine Learning |

| Deep Learning |

| Computer Vision |

| Natural Language Processing |

| Other AI Techniques |

| Cloud |

| On-Premises |

| Edge |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Operation | Upstream | ||

| Midstream | |||

| Downstream | |||

| By Solution Type | Platform | ||

| Services | |||

| By Asset Location | Onshore | ||

| Offshore | |||

| By Application | Quality Control | ||

| Production Optimisation | |||

| Predictive Maintenance | |||

| HS&E Compliance | |||

| Exploration and Drilling | |||

| Other Applications | |||

| By AI Technique | Machine Learning | ||

| Deep Learning | |||

| Computer Vision | |||

| Natural Language Processing | |||

| Other AI Techniques | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| Edge | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How quickly is artificial intelligence adoption growing across global oil and gas operations?

Spending is advancing at a 13.03% CAGR, with the AI in oil and gas market forecast to expand from USD 4.28 billion in 2026 to USD 7.91 billion by 2031.

Which operational segment captures the largest share of digital-intelligence spending?

Upstream dominates with 61.05% of 2025 revenue because data-heavy exploration and production workflows benefit most from advanced analytics.

What application currently delivers the clearest return on investment?

Predictive-maintenance programs lead, representing 37.60% of 2025 spending and delivering documented cuts in unplanned downtime and maintenance costs.

Why is edge computing receiving heightened attention?

Edge deployments are growing at a 14.15% CAGR because low-latency inference is essential for remote drill ships, frac sites and offshore platforms with limited connectivity.

Which region is expanding fastest in digital-energy investments?

Asia-Pacific is projected to log a 14.41% CAGR through 2031, driven by upstream investment in India, Indonesia and China and aggressive digital-transformation agendas.

What is the main barrier restricting broader AI rollout among independents?

High up-front CAPEX for platform deployment, coupled with a shortage of domain-savvy data scientists, constrains adoption among smaller operators.

Page last updated on: