Size and Share of AI Market In Call Center Applications

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

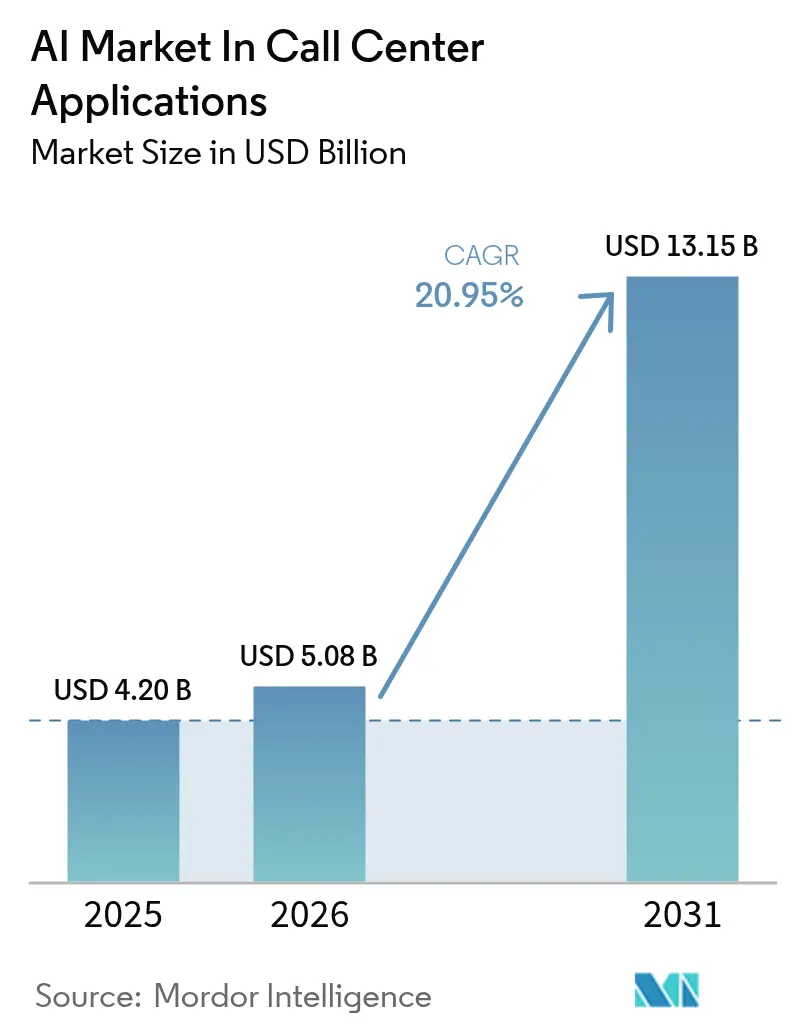

| Market Size (2026) | USD 5.08 Billion |

| Market Size (2031) | USD 13.15 Billion |

| Growth Rate (2026 - 2031) | 20.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of AI Market In Call Center Applications by Mordor Intelligence

The AI Market size in Call Center Applications market is expected to grow from USD 4.20 billion in 2025 to USD 5.08 billion in 2026 and is forecast to reach USD 13.15 billion by 2031 at 20.95% CAGR over 2026-2031. Investment momentum is building around transformer-based language models that automate multi-turn voice and text interactions once handled only by live agents. Enterprises are shifting budgets from legacy IVR to cloud contact-center-as-a-service suites that embed generative AI, while cloud providers bundle GPU capacity to meet real-time inference requirements. Voice biometrics, outcome-linked pricing, and multilingual large language models are accelerating adoption across banking, telecom, and retail. At the same time, the AI in Call Center Applications market faces cost headwinds as real-time speech inference consumes 5-10 times more compute than text chat, making model optimization and hybrid deployment strategies critical.

Key Report Takeaways

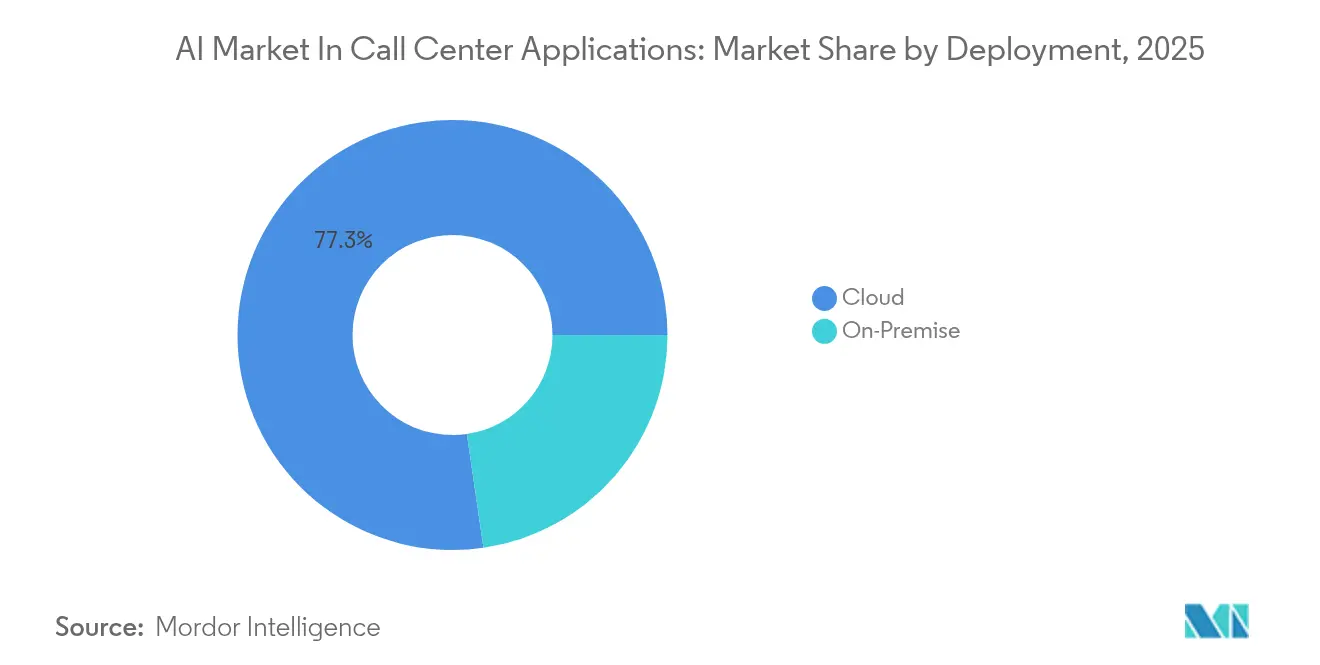

- By deployment model, cloud solutions commanded 77.30% of the AI market in call center applications industry share in 2025; the cloud segment is expanding at a 24.6% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance led with 27.40% revenue share in 2025, while telecommunications is projected to post a 22.4% CAGR to 2031.

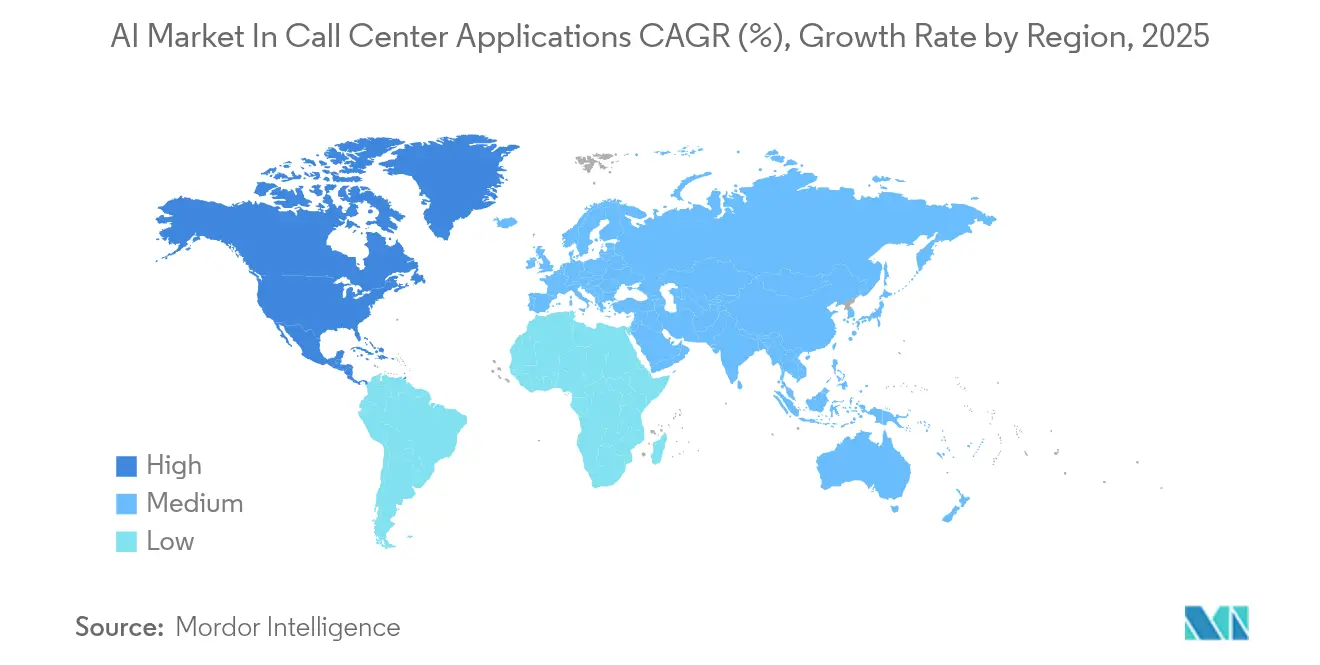

- By geography, North America held 40.30% of the AI market in call center applications industry size in 2025, whereas Asia-Pacific is growing at a 23.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of AI Market In Call Center Applications

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Gen-AI deployments in CCaaS platforms | +4.20% | Global, led by North America and Asia Pacific | Medium term (2-4 years) |

| Shift to outcome-based pricing by AI solution vendors | +2.80% | North America, Europe | Short term (≤2 years) |

| Voice biometrics adoption for fraud mitigation | +3.10% | Global, strongest in BFSI markets | Medium term (2-4 years) |

| Social-media-led escalation volumes | +1.90% | Global urban centers | Short term (≤2 years) |

| Hyper-personalized, sentiment-aware routing | +2.40% | North America, EU, advanced Asia Pacific CX hubs | Medium term (2-4 years) |

| CX-linked ESG scorecards for enterprises | +1.20% | Europe, North America, Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Gen-AI deployments in CCaaS platforms

Generative AI is moving contact centers beyond scripted chatbots to autonomous agents that maintain conversation context, retrieve customer records, and resolve issues end-to-end. Five9’s Genius AI reduced average handle time by 40% during beta programs. CCaaS vendors are re-architecting stacks around transformers, giving early adopters measurable cost savings and higher customer satisfaction.

Shift to outcome-based pricing by AI vendors

Vendors now tie invoices to metrics like first-call resolution rather than per-seat licenses. Zendesk introduced performance-linked billing in 2024, lowering buyer risk and aligning provider incentives with business outcomes.[1]Zendesk, “Outcome-Based Pricing for AI Agents,” zendesk.com The model increases pressure on suppliers to improve model accuracy and continuously tune deployments.

Voice biometrics for fraud mitigation

Banks, insurers, and telcos are deploying voice print checks that analyze acoustic signatures and caller behavior. Pindrop’s Continuous Scoring engine improved fraud-catch rates by 22% in trials. The surge in AI-generated voice scams makes biometric verification an urgent defense.

Social-media-led escalation volumes

Customers increasingly air complaints on public channels, forcing contact centers to ingest tweets and posts into case workflows. T-Mobile partners with OpenAI to merge social sentiment with account data, enabling proactive outreach before churn risk escalates.[2] CX Today, “T-Mobile Taps OpenAI for Customer Experience Engine,” cxtoday.com This omnichannel visibility is raising demand for large language models that understand context across platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty restrictions on audio storage | -2.70% | Europe, China, India | Medium term (2-4 years) |

| Skills gap in conversational AI tuning | -1.80% | Global, acute in emerging markets | Short term (≤2 years) |

| Model hallucination risk in regulated verticals | -1.60% | BFSI, healthcare, government workloads | Medium term (2-4 years) |

| Rising energy cost of real-time inference | -1.10% | Global cloud-first enterprises | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty restrictions on audio storage

Financial and healthcare regulators now demand that voice recordings stay within national borders, forcing enterprises to run region-specific AI stacks. The Bank for International Settlements notes that biometric content in speech drives stricter residency mandates. Localized deployments raise capital costs and limit the scale efficiencies of public cloud processing.

Skills gap in conversational AI tuning

Few professionals combine customer-service expertise with prompt engineering and model alignment skills. Contact Center Pipeline reports elongated rollouts and heavier dependence on managed services as firms scramble for talent. The shortage inflates project budgets and slows time-to-value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Infrastructure Drives AI Scalability

Cloud deployments held 77.30% of 2025 revenue, confirming their dominance in the AI market in call center applications industry share. The segment is tracking a 24.6% CAGR to 2031 as enterprises favor elastic GPU clusters for low-latency inference. On-premise solutions persist in finance and healthcare, yet their share is eroding as vendors introduce secure virtual private cloud zones that satisfy residency laws. Rising energy costs push interest in hybrid patterns that park routine IVR workloads locally while bursting complicated calls to the cloud.

Cloud vendors differentiate through specialized accelerators and model-hosting frameworks. Google’s Contact Center AI scales to 10 times peak call volume without provisioning delays, underscoring cloud resilience. The AI in Call Center Applications market size attached to the cloud is projected to reach USD 10.2 billion by 2031, cementing its role as the nerve center for voice analytics and agent assist functions.

By End-user Industry: BFSI Leads While Telecom Accelerates

The BFSI segment accounted for 27.40% of 2025 revenue, the largest slice of the AI market in call center applications industry. Banks justify AI investment through fraud prevention efficiencies and high customer lifetime value. The telecommunications segment, however, is registering the fastest 22.4% CAGR between 2026-2031 as 5G rollouts trigger surging support traffic.

Telcos report that first-call resolution rates have risen to 60% after the introduction of AI, compared to 35% for manual operations. Retail and healthcare follow closely, tapping AI for upselling, appointment scheduling, and claims management. The AI in Call Center Applications market size within telecom is forecast to triple by 2031, reflecting the sector’s need for scalable, multilingual agent assistance.

Geography Analysis

North America captured 40.30% of 2025 revenue, giving it the largest regional position in the AI market in call center applications industry. Early adoption of voice biometrics, well-funded technology buyers, and mature vendor ecosystems drive share. Key programs include T-Mobile’s OpenAI partnership that aggregates social-media cues with CRM data to pre-empt churn, and Five9’s Agentic CX launch illustrates the region’s rapid productization of generative AI. Energy and inference-cost concerns are nudging firms toward hybrid architectures that ground routine tasks on local edge nodes while sending complex queries to hyperscale GPUs, keeping operating margins steady.

Asia-Pacific is the fastest-growing region at a 23.8% CAGR through 2031, supported by government incentives and digital-first banks that deploy hundreds of AI models to personalize service. DBS Bank runs more than 800 models in production, while Commonwealth Bank pilots ChatGPT-style assistants for multilingual support. Telecom operators across India, Japan, and Korea lean on AI to manage 5G-related ticket spikes, stimulating regional spend. Linguistic diversity increases demand for models fine-tuned on local dialects, prompting Forrester to predict that 60% of APAC enterprises will train or license regional language models by 2025.As a result, the AI in Call Center Applications market size in APAC is poised to surpass USD 4.05 billion by 2031.

Europe and the Middle East show mixed drivers. European buyers emphasize GDPR-compliant deployments, spurring interest in federated learning that keeps voice data resident. The Gulf Cooperation Council stands out with 75% of businesses already using generative AI and more than 57% dedicating over 5% of tech budgets to AI projects. Saudi Arabia’s Vision 2030 program provides tax incentives for AI call-center rollouts, while regional telcos experiment with small language models optimized for Arabic. Collectively, these forces anchor a steady 16.4% CAGR in the wider EMEA corridor.

Competitive Landscape

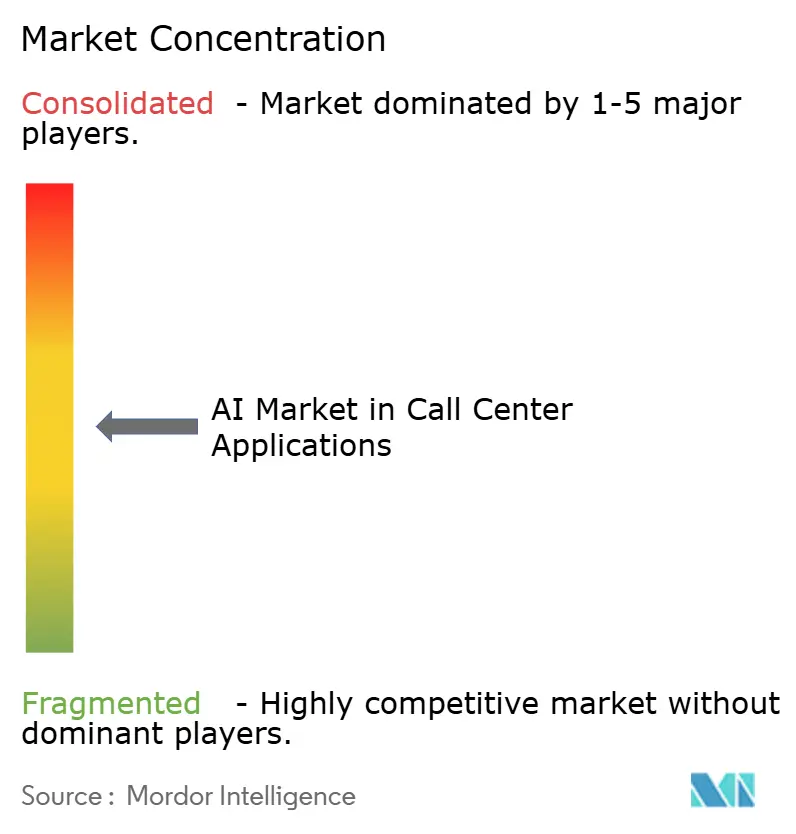

The AI in Call Center Applications market is moderately fragmented, with traditional CCaaS leaders, AI-native specialists, and cloud hyperscalers pursuing divergent strategies. NICE, Genesys, and Five9 integrate transformer-based dialog managers into mature telephony stacks, giving existing customers a low-friction upgrade path. Startups such as ASAPP, Uniphore, and Level AI focus on autonomous agent orchestration and sentiment analysis, pushing innovation cycles to quarterly cadences. Cloud providers like Google and Microsoft bundle GPU credits and managed model services into broader platform deals, lowering adoption hurdles for mid-size enterprises.

Mergers and acquisitions signal consolidation. Salesforce acquired Tenyx for voice AI, CallMiner bought VOCALLS to deepen conversation intelligence, and Calabrio picked up Echo AI to bolster quality management. Partnerships also surface; Uniphore teamed with Konecta to co-develop emotion detection suites tailored for the U.S. and UK. Patent filings around multi-modal agent workflows and latency-optimized inference pipelines are climbing, underscoring competitive intensity.

Strategic differentiation now rests on three pillars: platform breadth, vertical specialization, and cost-efficient inference. Providers armed with proprietary GPUs or cached execution engines can undercut rivals on runtime costs, while firms with domain-tuned small language models court regulated industries. The combined top-five vendor share sits near 45%, indicating a market concentration score of 5 and leaving room for niche entrants focused on compliance automation or energy-aware model serving.

Leaders of AI Market In Call Center Applications

SAP

Oracle

Google

Microsoft

IBM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CallMiner bought VOCALLS, enhancing multi-channel conversation intelligence with voice-first technology

- June 2025: Five9 launched Agentic CX with governance controls that let businesses decide where and how AI can act.

- May 2025: Weave Communications paid USD 35 million for TrueLark to embed 24/7 AI receptionist capabilities into its platform.

- February 2025: Five9 introduced AI Agents within its Genius AI suite to automate personalized self-service across channels.

Scope of Report on AI Market In Call Center Applications

The AI Market in Call Center Applications Market is Segmented by Deployment (Cloud and On-Premises), End-user Industry (BFSI, Retail and E-Commerce, Telecom, Travel and Hospitality, Healthcare, Public Sector, and Others), and Geography (North America, Europe, South America, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| BFSI |

| Retail and E-Commerce |

| Telecom |

| Travel and Hospitality |

| Healthcare |

| Public Sector |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment | Cloud | ||

| On-Premise | |||

| By End-user Industry | BFSI | ||

| Retail and E-Commerce | |||

| Telecom | |||

| Travel and Hospitality | |||

| Healthcare | |||

| Public Sector | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the AI Market in Call Center Applications?

The market stands at USD 5.08 billion in 2026 and is on pace to reach USD 13.15 billion by 2031, growing at 20.95% annually.

Which deployment model is leading the market?

Cloud platforms hold 77.30% of 2025 revenue due to scalable GPU clusters that support real-time speech inference.

Which industry vertical invests the most in AI call-center solutions?

Banking, financial services, and insurance account for 27.40% of 2025 revenue, driven by fraud-mitigation and high transaction values.

Which region has the biggest share in AI Market in Call Center Applications Industry?

In 2025, the North America accounts for the largest market share in AI Market in Call Center Applications Industry.

Which region is growing fastest?

Asia-Pacific is expanding at a 23.8% CAGR through 2031, supported by digital-first banking and government AI incentives.

What is the biggest restraint facing the market?

Data-sovereignty laws that require local storage of voice recordings add infrastructure costs and slow cross-border deployments.

Page last updated on: