Brazil Formwork Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.21 Billion |

| Market Size (2026) | USD 0.22 Billion |

| Market Size (2031) | USD 0.29 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Formwork Market Analysis by Mordor Intelligence

The Brazil Formwork Market size is projected to expand from USD 0.21 billion in 2025 and USD 0.22 billion in 2026 to USD 0.29 billion by 2031, registering a CAGR of 5.68% between 2026 to 2031.

The growth path is supported by Brazil’s broad construction pipeline, with the New Growth Acceleration Program (Novo PAC) committing BRL 1.8 trillion (USD 332.6 billion) through 2030 and BRL 1.3 trillion (USD 240.2 billion) already earmarked by end-2026, which keeps civil works activity visible across transport, sanitation, and urban projects. Infrastructure investment also reaches approximately USD 56 billion in 2026, up from approximately USD 52.3 billion in 2025, supporting longer equipment utilization cycles and favoring suppliers with deeper engineered fleets and greater technical support capacity. Housing activity adds another layer of demand, as the Minha Casa Minha Vida Program now has a BRL 200 billion (USD 37 billion) budget in 2026, and targets 3 million contracted homes by year-end, reinforcing demand for reusable panel systems in repetitive residential construction. The Brazil formwork market is also being shaped by a move away from improvised methods toward systems that reduce labor requirements, improve cycle times, and better align with planned project execution standards on large sites. Competition is therefore centered on engineered system suppliers and rental specialists that can combine product availability, design support, and multi-site fleet coordination across Brazil’s active construction corridors.

Key Report Takeaways

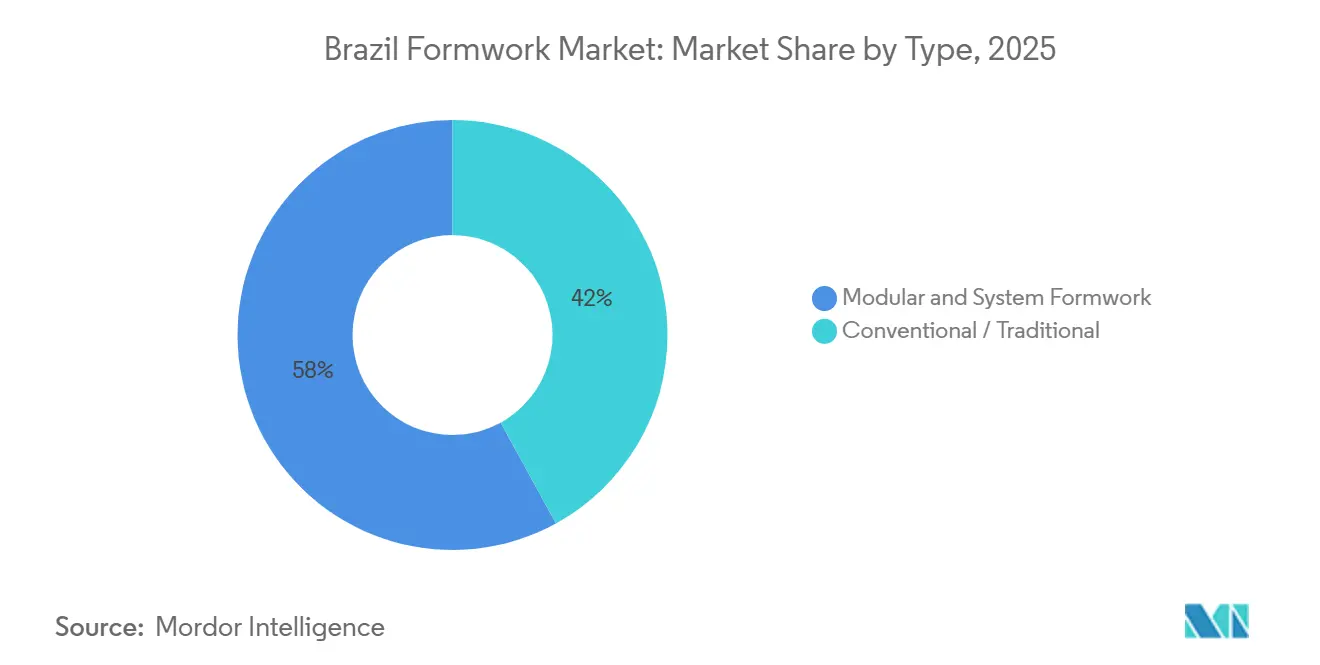

- By type, modular / system formwork held 58% share in 2025 and is forecast to grow at 5.90% CAGR through 2031.

- By configuration, climbing formwork accounted for 28% share in 2025 and is advancing at 6.10% CAGR through 2031.

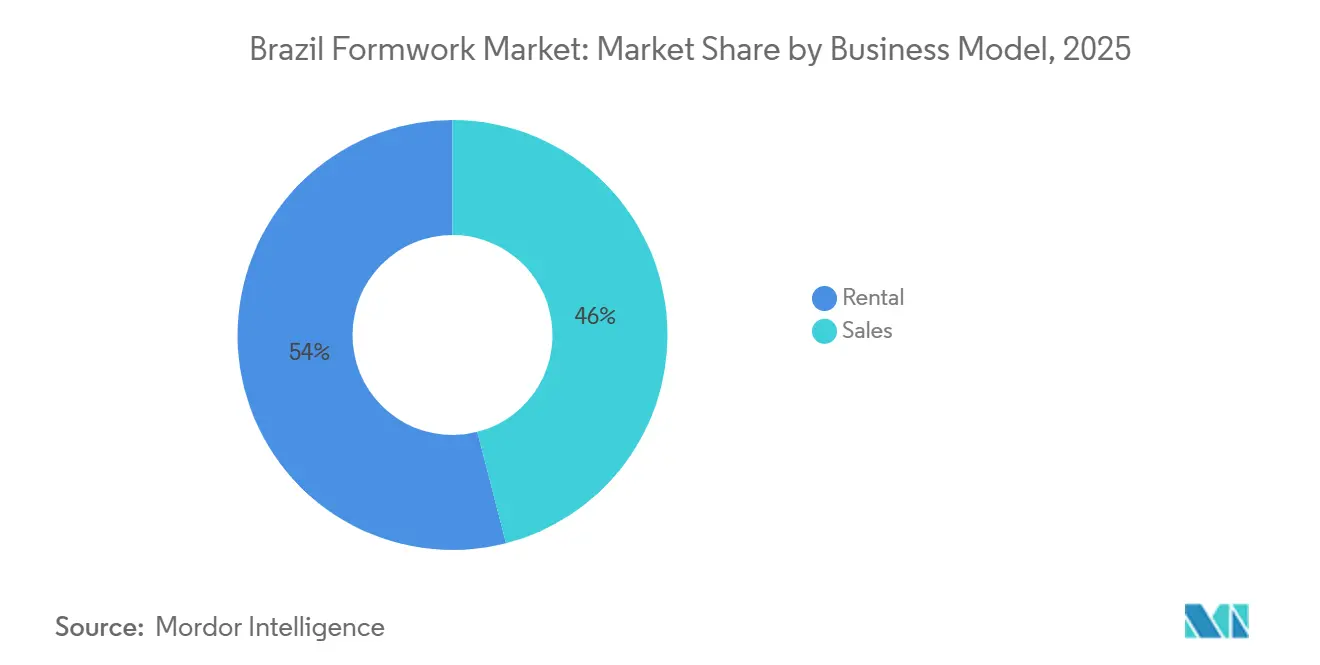

- By business model, rental held 54% of the Brazil formwork market share in 2025 and is projected to expand at 6.50% CAGR through 2031.

- By sector, infrastructure accounted for a 38% share of the Brazil formwork market size in 2025 and is forecast to grow at a 5.80% CAGR through 2031.

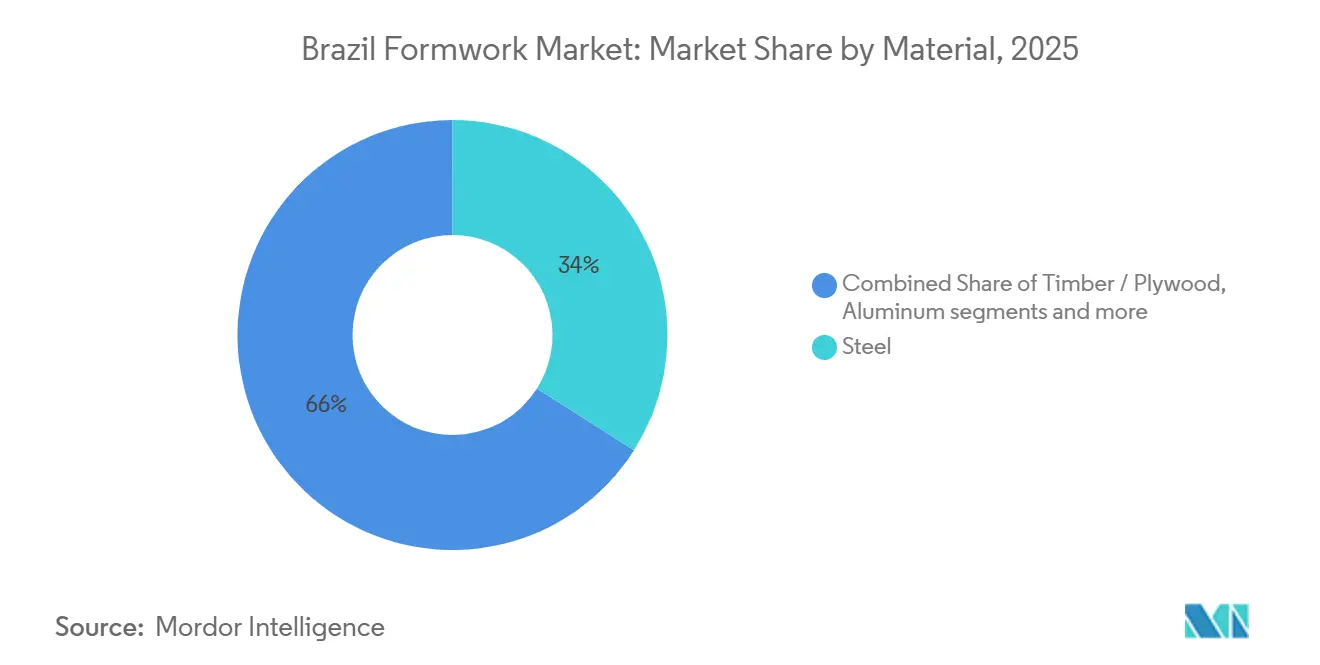

- By material, steel led with 34% share in 2025, while aluminum recorded the highest projected CAGR at 6.05% through 2031.

- By city, Sao Paulo held 31% share in 2025 and is forecast to expand at 6.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Formwork Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Infrastructure and Urban Mobility Project Pipeline | +1.2% | National, with stronger gains in Sao Paulo, Brasilia, and Rio de Janeiro | Medium term (2-4 years) |

| Rising Adoption of Modular and System Formwork in Repetitive Works | +0.9% | National, mainly Sao Paulo, Rio de Janeiro, and Mato Grosso do Sul | Medium term (2-4 years) |

| Growing Rental-Based Procurement by Mid-Sized Contractors | +0.7% | National | Short term (≤ 2 years) |

| Labor Shortages and Pressure to Reduce On-Site Cycle Times | +0.6% | National, with stronger pressure in Sao Paulo and Brasilia | Short term (≤ 2 years) |

| Expansion of Industrial, Logistics, and Energy Construction | +0.5% | Mato Grosso do Sul, Para, Sao Paulo, and nearby states | Medium term (2-4 years) |

| Safety and Quality Compliance Requirements on Major Projects | +0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Infrastructure and Urban Mobility Project Pipeline

Brazil’s infrastructure pipeline remains one of the clearest supports for the Brazil formwork market over the forecast period. The Novo PAC Program provides this support on an unusual scale, with BRL 1.8 trillion (USD 332.6 billion) in public and private commitments through 2030, of which BRL 1.3 trillion (USD 240.2 billion) is already earmarked by end-2026[1]São Paulo State Government, “SP nos Trilhos consolida maior expansão ferroviária da história do Estado com R$ 190 bilhões em investimentos,” Agência SP, agenciasp.sp.gov.br. Brazilian Association of Infrastructure and Basic Industries also expects infrastructure investment to reach BRL 300 billion (USD 56 billion) in 2026, suggesting a sustained civil works pipeline rather than a short project burst. Sao Paulo remains especially important because the SP nos Trilhos Program commits BRL 190 billion (USD 35.1 billion) to more than 40 rail projects and over 1,000 kilometers of new rail lines, supporting tunnel, viaduct, and vertical concrete construction over multiple years. This environment favors suppliers that can mobilize large system volumes across overlapping jobs, as contractors increasingly need consistent availability and technical continuity across multiple projects.

Rising Adoption of Modular and System Formwork in Repetitive Works

The move toward modular systems in the Brazil formwork market is being driven more by jobsite economics than by product preference alone. Repetitive housing and commercial structures benefit from reward systems that shorten pour cycles, reduce repair work, and improve reuse across many identical units. This logic is becoming stronger as the Minha Casa Minha Vida pipeline expands, because the program’s BRL 200 billion (USD 37 billion) budget in 2026 is tied to very large housing volumes that benefit from standardized execution. Large developers have also begun to connect design, sequencing, and procurement more closely, with Measurement, Reporting, and Verification (MRV) using Building Information Modeling (BIM) 4D and 5D workflows that support more disciplined formwork planning on major projects. As these methods spread across broader contractor groups, engineered panels gain an advantage because they fit more easily into repeatable, time-sensitive construction programs.

Growing Rental-Based Procurement by Mid-Sized Contractors

Rental has become a structural feature of the Brazil formwork market because it matches the cost profile of contractors that manage several projects but do not want captive fleets on their balance sheets. The segment already held 54% share in 2025, and the pattern is reinforced by operator performance in 2026. Mills reported a 65% Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margin in its Formas & Escoramentos division in Q1 2026, while rental revenue in that division reached BRL 70.8 million (USD 13.1 million), demonstrating the pricing power that bundled services and fleet control can create. The same company also indicated that long-term contracts accounted for 55% of rental revenues in 2025, suggesting a shift toward planned multi-project allocations rather than short-term spot transactions. This shift matters because mid-sized contractors increasingly value logistics support, engineering guidance, and fleet repositioning as much as the physical formwork itself.

Labor Shortages and Pressure to Reduce On-Site Cycle Times

Labor constraints are pushing the Brazil formwork market toward systems that deliver more output with smaller crews. In February 2026, 41.6% of Brazilian construction companies cited workforce shortages as their main operational obstacle, which made labor availability one of the clearest procurement pressures across active sites. A peer-reviewed study in Revista DELOS also described the shortage as structural, with weaker labor replenishment into construction trades over time. On the jobsite, this makes systems with faster assembly and fewer handling steps easier to justify, even when unit cost is higher than timber. The 2025 launch of ALUPEC by ORPEC (Organizacao Paranaense de Engenharia e Construcao), a Brazilian engineering and construction solutions company, highlighted how suppliers are increasingly focusing on productivity-driven innovation, with the system designed to deliver approximately 40 square meters per hour using a four-person crew. As a result, procurement decisions are increasingly emphasizing labor efficiency and shorter construction cycle times.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Engineered Formwork Systems | -0.8% | National, with stronger pressure in smaller cities and lower-revenue project tiers | Long term (≥ 4 years) |

| Project Delays and Public Investment Volatility | -0.6% | National, concentrated in publicly funded infrastructure projects | Short term (≤ 2 years) |

| Currency Pressure on Imported High-Spec Components | -0.4% | National | Short term (≤ 2 years) |

| Persistent Use of Low-Cost Conventional Timber Systems | -0.3% | Lower-urbanization regions and smaller non-repetitive projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Engineered Formwork Systems

High initial cost remains one of the main brakes on broader system adoption in the Brazil formwork market. Smaller contractors outside major cities still face a steep entry barrier when comparing steel or aluminum modular systems with low-cost timber alternatives. Tight credit conditions magnified this gap through 2025, and CBIC-linked commentary showed that financing pressure remained a major constraint on construction growth[2]O Hoje, “Indústria de materiais de construção reage, mas fecha 2025 no vermelho,” O Hoje, ohoje.com. Even when contractors use rental, mobilization, freight, and technical service fees, engineered systems can look expensive on short or irregular jobs. This leaves the market split between large, well-funded contractors that already use system formwork and a long tail of smaller operators that continue using conventional methods for cost control.

Project Delays and Public Investment Volatility

Execution risk also limits how quickly the Brazil formwork market can convert announced project pipelines into equipment demand. In mid-2025, more than 70% of PAC Selecoes works were still at preliminary stages and only 10% had been completed, despite the scale of public allocations already announced. For suppliers, this creates idle periods between commitment and mobilization, which affects returns on both owned fleets and long-term procurement planning. Public works timing can also shift around electoral and budget cycles, which makes it harder to match fleet deployment with site readiness. On top of that, imported components used in advanced climbing and tunnel systems remain exposed to currency fluctuations, raising replacement cost risks for providers that source some inputs in foreign currency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modular Systems Consolidate Their Hold on Brazil's Concrete Works

Modular / system formwork accounted for 58% of the Brazil formwork market in 2025, making it the leading segment in the country. The same segment is projected to grow at a 5.9% CAGR through 2031, indicating it is expanding from a position of leadership rather than catching up from a small base. This pattern reflects the stronger role of reusable panels in projects that demand repeatability, faster cycles, and more predictable quality across multi-unit construction programs. The segment also fits better with contractors that want tighter sequencing and lower dependency on large onsite carpentry teams. That alignment has become more important as developers try to control labor intensity and reduce delays on active projects.

The residential pipeline is one of the main reasons modular systems continue to strengthen their position. Minha Casa, Minha Vida remains a major anchor, as its 2026 budget reached BRL 200 billion (USD 37 billion), and its target now stands at 3 million contracted homes by year-end. That scale favors standard panel systems that can be reused across many similar units and phases. Conventional formwork remains prevalent in smaller, non-repetitive works and outside the largest urban centers, but its relative importance weakens where project repetition, speed, and coordination carry greater weight.

By Configuration: Climbing Systems Advance on High-Rise and Infrastructure Works

Climbing formwork represented 28% of the Brazil formwork market share in 2025 and posted the fastest configuration growth at 6.10% CAGR through 2031. Its rise is closely tied to Brazil’s concentration of high-rise and infrastructure works in major metropolitan areas. Projects in Sao Paulo, Rio de Janeiro, and Brasília often involve vertical cores, transport structures, and constrained sites where steady upward progress matters more than low upfront setup cost. In these settings, climbing systems help contractors maintain sequencing discipline and reduce the need for repeated crane-dependent repositioning. That makes the configuration useful not only for towers, but also for selected transport and civil works with demanding geometry.

The strength of the Sao Paulo pipeline helps explain why this segment is gaining ground. SP nos Trilhos commits BRL 190 billion (USD 35.1 billion), across a broad rail expansion plan that supports ongoing demand for tunnel, station, and vertical concrete work. At the same time, static formwork still remains widely used in medium-rise buildings and standard slabs, walls, and columns where project complexity is lower. Slipform continues to serve specialized structures such as silos, towers, and selected bridge applications. Tunnel formwork also gains relevance where residential designs are repeated at scale, since that is where its productivity benefit becomes easier to justify over conventional layouts.

By Business Model: Rental Deepens its Structural Grip on Market Economics

Rental held 54% share of the Brazil formwork market size in 2025 and is forecast to expand at 6.50% CAGR through 2031, making it the fastest-growing segment across the full market structure. This result reflects a clear preference for variable-cost access over asset ownership among contractors with active but uneven project pipelines. Rental is especially attractive when firms operate across several sites and need flexibility in timing, transport, and configuration. It also allows contractors to access engineering support, maintenance, and fleet management without carrying the full burden in-house. That combination has turned rental from a temporary choice into a core operating model for much of the market.

The financial profile of leading operators supports this view. Mills’ Formas & Escoramentos division reported BRL 80 million (USD 14.8 million) in net revenue, and a 65% Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margin in Q1 2026, while volume reached 50,100 tons. The company also stated that long-term contracts accounted for 55% of rental revenues in 2025, indicating deeper customer commitment and a more planned fleet allocation. Sales still hold a place among large contractors that can reuse systems over long infrastructure programs and justify ownership economics. Even so, the wider direction of the Brazil formwork market continues to favor rental because project scheduling, support services, and capital discipline matter more for a growing share of buyers.

By Sector: Infrastructure Leads on Scale, Residential Gains Momentum Through Housing Programs

Infrastructure accounted for a 38% share of the Brazil formwork market in 2025 and is forecast to grow at a 5.8% CAGR through 2031. This segment leads because Brazil’s current works pipeline includes transport, sanitation, energy, and industrial civil structures that require large concrete volumes and longer project durations. The scale of planned and active public works creates an infrastructure demand pattern that is both broad and technically demanding. Formwork requirements in this segment often extend beyond basic wall and slab systems into bridge, viaduct, tunnel, and heavy civil applications. That raises the value of engineered systems and specialist support on larger jobs.

Official and company-linked project examples reinforce that position. Infrastructure investment reaches BRL 300 billion (USD 56 billion) in 2026, according to the Brazilian Association of Infrastructure and Basic Industries, while Sao Paulo alone mapped BRL 190 billion (USD 35.2 billion) in railway projects and BRL 62.4 billion (USD 11.5 billion) in second-half 2025 infrastructure auctions. Residential construction is also gaining momentum because Minha Casa, Minha Vida remains the country’s largest-volume housing engine. The program accounted for 85% of all new residential launches nationally, according to the Ministry of Cities, giving formwork suppliers a large, recurring project pipeline beyond heavy civil construction. Commercial activity remains more selective, while industrial and logistics works add support where warehouse, plant, and energy construction is active.

By Material: Steel Anchors Current Volumes, Aluminum Reshapes the Cost Equation

Steel led material segmentation with a 34% share in 2025, reflecting its continued strength in infrastructure and industrial applications. The material remains preferred in jobs that require high load-bearing performance, durability over repeated heavy use, and compatibility with demanding pours. Bridge piers, viaducts, and other heavy civil structures still align well with steel systems because they place greater emphasis on strength and durability than on light handling. This gives steel a stable role in the present market mix, especially while infrastructure remains the largest end-use segment. Its leadership, therefore, comes from where work is concentrated rather than from universal superiority across all project types.

Aluminum, however, is the fastest-growing material, with a 6.05% CAGR through 2031, reflecting different priorities. Repetitive residential projects value lighter systems that can be moved faster, handled with smaller crews, and reused many times across standardized layouts. This is why aluminum becomes more compelling as labor shortages persist and large housing volumes stay active. The Brazil formwork market is therefore seeing a clearer separation between steel-led heavy civil demand and aluminum-led productivity demand in faster-cycle building work. Timber, plywood, and other materials still serve smaller or less repetitive projects, but their competitive space narrows where scale, speed, and reuse increasingly shape contractor decisions.

Geography Analysis

Sao Paulo captured 31% of the Brazil formwork market in 2025 and is on track to grow at a 6.80% CAGR through 2031, keeping it well ahead of every other city market in the country. This lead is rooted in the city’s concentration of transport, housing, and mixed-use construction, which generates sustained demand across several formwork configurations. SP nos Trilhos alone commits BRL 190 billion (USD 35.1 billion) to more than 40 projects and over 1,000 kilometers of rail expansion, thereby creating long-duration demand for tunnel, station, viaduct, and vertical concrete works. The state also mapped BRL 62.4 billion (USD 11.5 billion) in infrastructure auctions for the second half of 2025, reinforcing visibility into near-term fleet deployment.

Sao Paulo also benefits from a dense base of contractors and rental operators, which gives the city a clear mobilization advantage over other regions. Rio de Janeiro is the second major demand cluster because it combines urban mobility, sanitation, port-related infrastructure, and dense urban development. Brasília follows a different pattern, with stable demand tied to public buildings, federal procurement, and housing projects linked to national programs. Both cities tend to favor engineered systems because project execution often requires greater planning discipline and addresses site constraints more than in smaller urban markets. Salvador and the wider Northeast are shaped more strongly by housing and social infrastructure allocations, especially where Minha Casa Minha Vida remains the main residential engine.

The rest of Brazil segment accounts for the majority of geographic volume outside the five named city groupings. It includes Belo Horizonte, Recife, Fortaleza, Curitiba, Manaus, Porto Alegre, and interior industrial hubs. Demand in these locations is more uneven, but it can surge when major plants, logistics facilities, or public works enter active construction. A clear example is Arauco’s Projeto Sucuriu in Mato Grosso do Sul, valued at BRL 25 billion (USD 4.6 billion), which had surpassed 70% civil works completion by April 2026 and was still sustaining heavy construction activity[3]Arauco, Valmet, and Crane Brasil, “Projetada para ser maior planta de celulose do mundo, fábrica da Arauco acelera obras,” Valor Econômico, valor.globo.com. For many of these secondary and interior markets, rental remains the most practical access route to engineered systems because project timing is less continuous than in Sao Paulo.

Competitive Landscape

The Brazil formwork market is moderately fragmented, with international system providers, domestic rental companies, and regional suppliers competing across different project segments. Mills is the leading domestic player in the rental segment, while PERI Brasil, Doka do Brasil, ULMA Brasil, and Alsina Formwork Brazil maintain strong positions through engineering expertise, broad system portfolios, and technical support. As a result, competition is driven by a combination of rental fleet availability, project execution capability, and engineering services rather than product supply alone.

Competitive differentiation is increasingly centered on digital solutions, integrated services, and project-specific engineering. PERI Brasil continues to strengthen its position through Building Information Modeling (BIM)-enabled project planning, while ULMA focuses on productivity-driven solutions for complex industrial and civil construction projects. Mills has also reinforced its service-led model through long-term rental contracts and strong operational performance, reflecting growing customer demand for integrated formwork solutions rather than standalone equipment.

Regional suppliers remain competitive, particularly on projects where local relationships, rapid mobilization, and pricing are key decision factors. At the same time, new entrants such as Lianggong are increasing competition by introducing cost-effective engineered systems for repetitive residential and mid-rise construction. Consequently, the Brazil formwork market is expected to remain moderately fragmented, with suppliers competing through engineering capability, service quality, fleet strength, and regional execution rather than overall market dominance.

Brazil Formwork Industry Leaders

PERI Brasil Formas e Escoramentos Ltda.

Doka do Brasil

ULMA Brasil Formas e Escoramentos Ltda.

Mills Estruturas e Serviços de Engenharia S.A.

Pashal Locadora de Equipamentos Ltda.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Arauco's Projeto Sucuriu, a BRL 25 billion (USD 4.6 billion) cellulose megafactory in Inocencia, Mato Grosso do Sul, surpassed 70% completion of civil works, with the site mobilizing over 11,000 workers and projected to reach 14,000 at peak construction in 2026. The project's electromechanical assembly phase, which began in April 2026, sustains industrial formwork demand through the year.

- March 2026: The Brazilian federal government announced an additional USD 3.7 billion injection into the Minha Casa Minha Vida program, raising the 2026 housing budget to a record USD 37 billion and expanding the program's unit target to 3 million contracted homes by year-end, generating sustained nationwide demand for residential formwork systems.

- August 2025: Yancheng Lianggong Formwork Co., Ltd. entered the Brazilian market at the Concrete Show South America in Sao Paulo, presenting lightweight aluminum frame formwork designed for repetitive mid-rise residential and modular construction.

Brazil Formwork Market Report Scope

The Brazil Formwork Market is Segmented by Type (Conventional / Traditional and Modular / System Formwork), Configuration (Static, Climbing, Slipform, and Tunnel), Business Model (Sales and Rental), Sector (Residential, Commercial, Industrial & Logistics and Infrastructure), Material (Timber / Plywood, and More), and City (Sao Paulo, Rio De Janeiro, Brasilia, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional / Traditional |

| Modular / System Formwork |

| Static |

| Climbing |

| Slipform |

| Tunnel |

| Sales |

| Rental |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fiberglass |

| Others |

| Sao Paulo |

| Rio de Janeiro |

| Brasilia |

| Salvador |

| Rest of Brazil |

| By Type | Conventional / Traditional |

| Modular / System Formwork | |

| By Configuration | Static |

| Climbing | |

| Slipform | |

| Tunnel | |

| By Business Model | Sales |

| Rental | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Material | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fiberglass | |

| Others | |

| By City | Sao Paulo |

| Rio de Janeiro | |

| Brasilia | |

| Salvador | |

| Rest of Brazil |

Key Questions Answered in the Report

What is the 2026 size of the Brazil formwork market?

The Brazil formwork market size stands at USD 0.22 billion in 2026 and is projected to reach USD 0.29 billion by 2031 at 5.68% CAGR.

Which business model leads formwork demand in Brazil?

Rental leads with 54% share in 2025 and is also the fastest-growing business model at 6.50% CAGR through 2031.

Why is modular formwork gaining traction in Brazil?

Modular / system formwork held 58% share in 2025 because repetitive housing and large civil works need faster cycles, reuse, and lower labor intensity.

Which end-use sector creates the most demand for formwork systems in Brazil?

Infrastructure leads with 38% share in 2025, supported by transport, sanitation, and industrial civil works across the national pipeline.

Page last updated on: