India Middle Mile Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

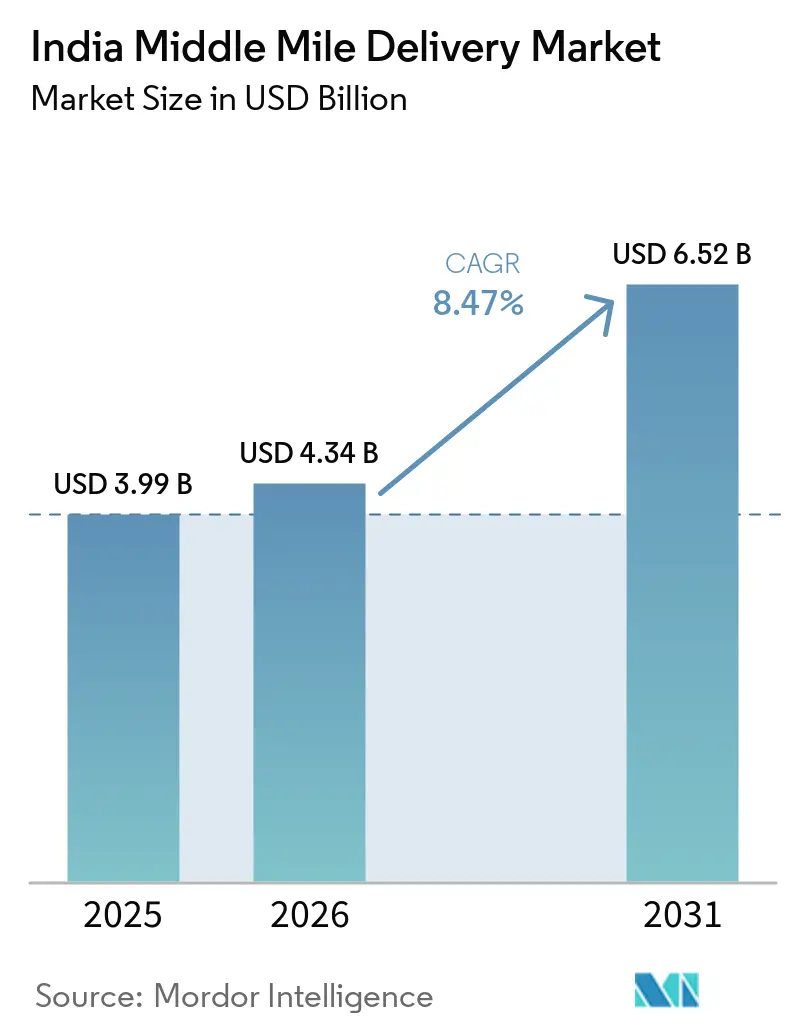

| Base Year Market Size (2025) | USD 3.99 Billion |

| Market Size (2026) | USD 4.34 Billion |

| Market Size (2031) | USD 6.52 Billion |

| Growth Rate (2026 - 2031) | 8.47% CAGR |

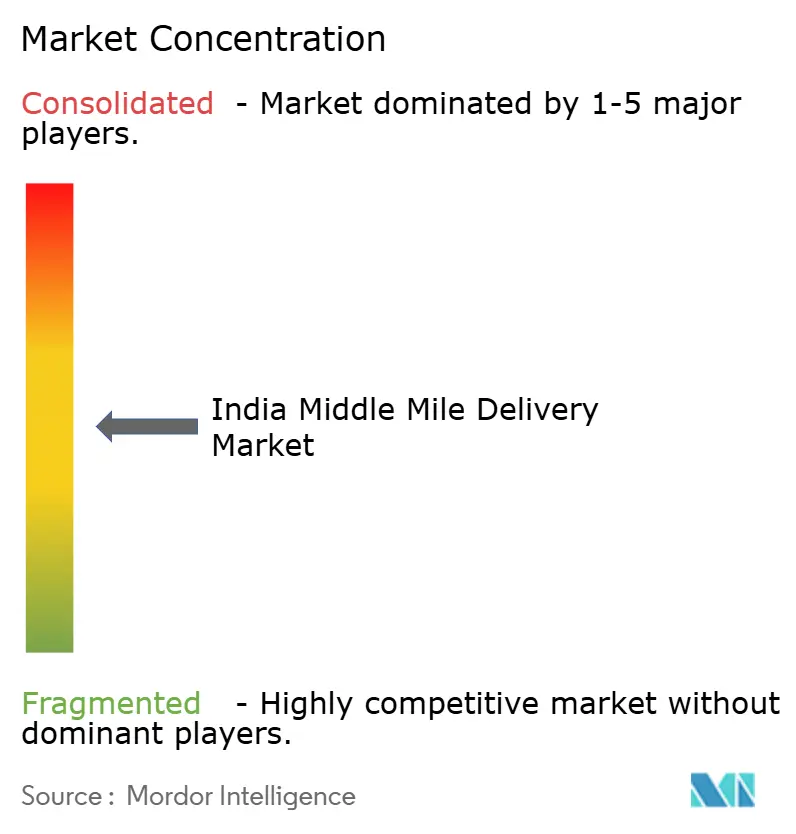

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Middle Mile Delivery Market Analysis by Mordor Intelligence

The India middle-mile delivery market size was valued at USD 3.99 billion in 2025 and is estimated to grow from USD 4.34 billion in 2026 to reach USD 6.52 billion by 2031, at a CAGR of 8.47% during the forecast period (2026-2031).

The India middle-mile delivery market is moving on the back of a broad logistics upgrade that is reducing transit friction across core freight corridors and making organized freight movement viable for a larger shipper base. India’s logistics costs as a share of GDP narrowed to 7.97% in FY24, a decline that came alongside infrastructure expansion, suggesting stronger network efficiency rather than weak freight demand. The rollout of Gati Shakti-linked planning, wider use of the Unified Logistics Interface Platform, and the gradual build-out of multimodal facilities are making route planning, cargo tracking, and corridor-level capacity deployment more predictable. This is widening the addressable market for organized operators in MSME manufacturing, fresh produce movement, and direct-to-consumer retail, where logistics costs previously absorbed too much of the end margin. The same changes are also shifting competition, because operators with corridor-aligned assets and better network control are gaining ground over models that relied mainly on fragmented sourcing of transport capacity.

Key Report Takeaways

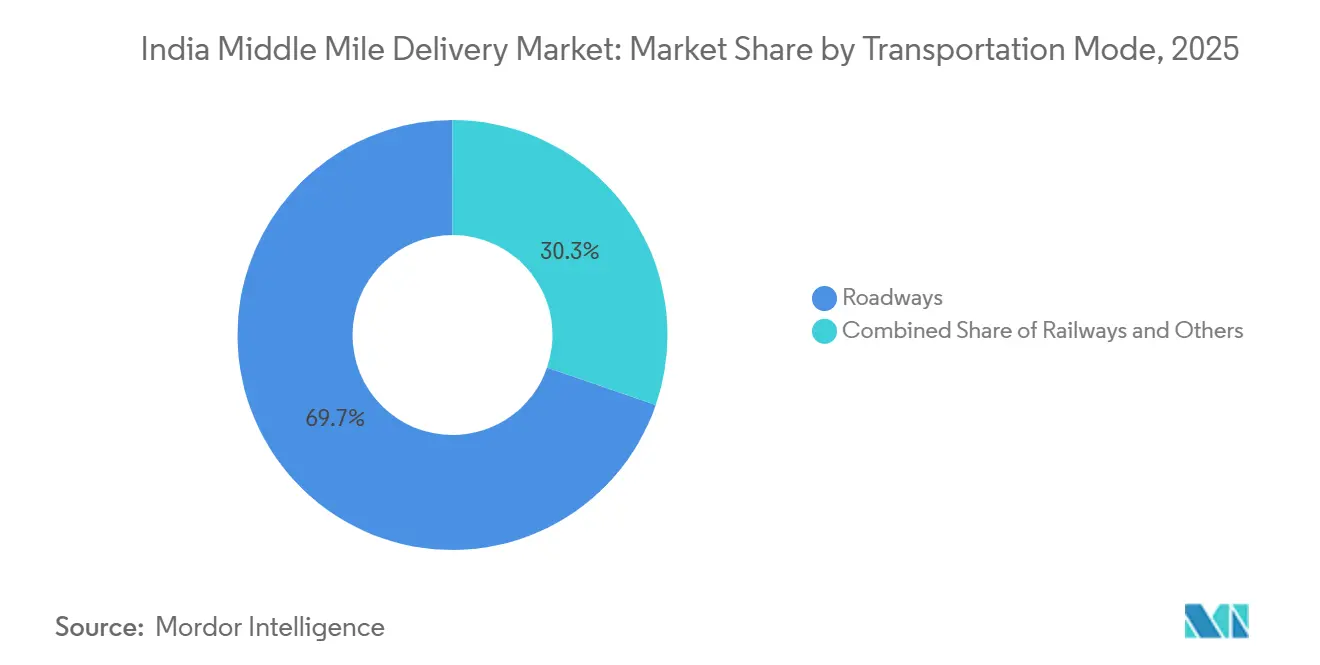

- By transportation mode, roadways led with 69.73% of India middle-mile delivery market share in 2025, while airways are projected to grow at a 10.10% CAGR through 2031.

- By business model, B2C accounted for 72.03% of the India middle-mile delivery market in 2025, while C2C is set to record the fastest CAGR at 10.22% through 2031.

- By temperature control, non-temperature-controlled shipments accounted for 89.11% of India middle-mile delivery market share in 2025, while temperature-controlled logistics is forecast to expand at a 10.38% CAGR through 2031.

- By destination, domestic shipments captured 86.2% of India middle-mile delivery market size in 2025, while international middle-mile shipments are expected to grow at a 12.84% CAGR through 2031.

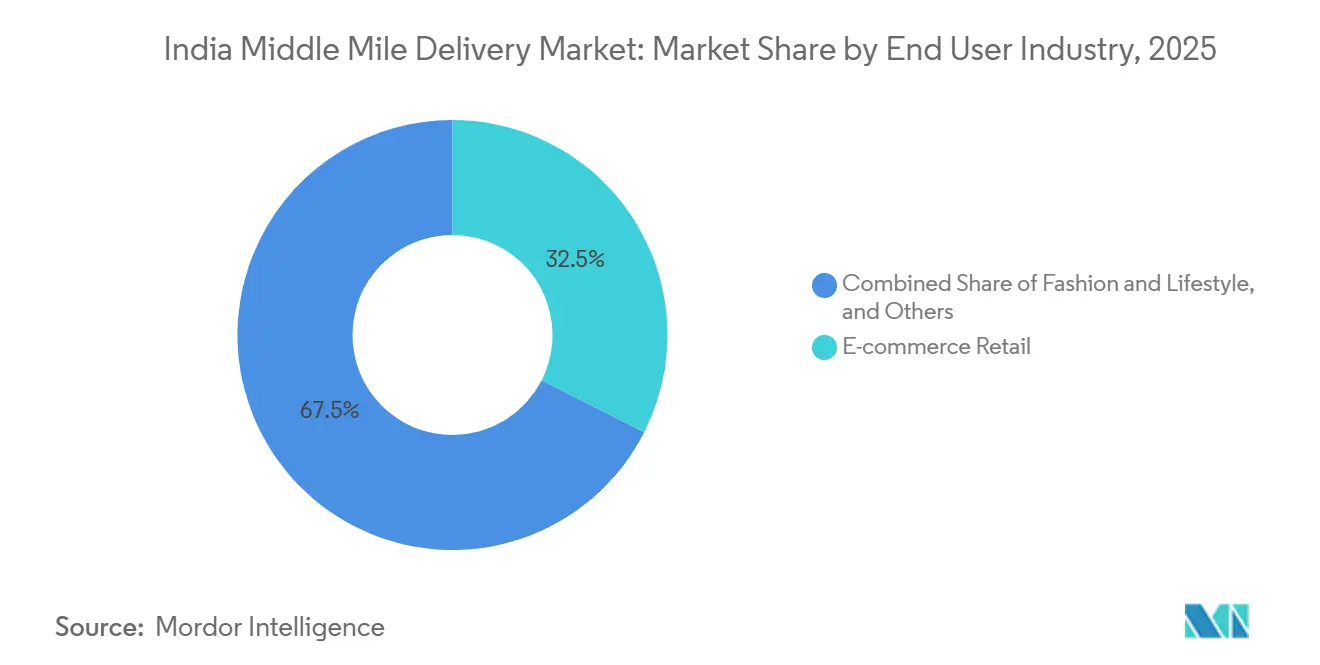

- By end-user industry, e-commerce retail held 32.46% of India middle-mile delivery market size in 2025, while healthcare and medical supplies are projected to advance at a 10.70% CAGR through 2031.

- By geography, the West held 30.1% of the India middle-mile delivery market share in 2025, while North India is forecast to grow at a 9.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Middle Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Logistics Policy And Gati Shakti Push | +2.1% | Pan-India, with early concentration in DMIC and Golden Quadrilateral corridors | Long term (≥ 4 years) |

| E-Commerce And Quick-Commerce Shipment Boom | +2.0% | National, with early gains in metro and Tier-1 cities | Short term (≤ 2 years) |

| Dedicated Freight Corridors: Reducing Rail Transit Cost And Time | +1.2% | EDFC in the North and East, WDFC from the North and West to JNPT | Medium term (2-4 years) |

| AI And IoT Visibility And Optimization Platforms | +0.7% | National, with spill-over into wider APAC-linked supply chains | Short term (≤ 2 years) |

| MSME LTL Cluster Aggregators Unlocking New Volumes | +0.5% | Tier-2 and Tier-3 industrial clusters in North and West India | Medium term (2-4 years) |

| Renewable-Powered Cold-Chain Hubs Lowering OPEX | +0.3% | South and West India, especially Andhra Pradesh and Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Logistics Policy and Gati Shakti Infrastructure Push

The India middle-mile delivery market is benefiting from a planning system that now links transport corridors, industrial clusters, and logistics nodes into a coordinated public framework. PM Gati Shakti integrates 57 ministries and more than 1,700 data layers, enabling freight planning with a stronger spatial basis than earlier corridor decisions[1]Press Information Bureau, “PM GatiShakti National Master Plan, 57 Ministries Onboarded, 1700+ Data Layers,” Government of India, pib.gov.in. The Unified Logistics Interface Platform connects 44 government systems and serves more than 1,700 registered companies, improving real-time cargo visibility across transport modes. This matters for middle-mile operations because route planning, handoffs, and corridor selection become easier when infrastructure and data systems move in the same direction. Operators that place hubs and linehaul assets along these designated corridors are likely to maintain a cost advantage as more multimodal parks and corridor-linked facilities enter full use.

E-Commerce and Quick-Commerce Shipment Boom

The India middle-mile delivery market is also benefiting from the fact that parcel movement now occurs in larger, more frequent waves than it did a few years ago. E-commerce and quick commerce are increasing the need for repeat-hub replenishment, short-cycle sortation, and intercity transfers operating within tighter service windows than conventional parcel movement. This is changing the economics of automation because secondary-city hubs now have enough parcel density to justify faster sortation and more regular linehaul schedules. It is also shifting network design, since demand is moving beyond the largest metros and forcing operators to place capacity deeper into Tier-2 and Tier-3 corridors. As a result, the market is no longer driven only by shipment growth, but also by the need to move smaller, more time-sensitive consignments through a denser network.

Dedicated Freight Corridors Cut Rail Transit Cost/Time

The India middle-mile delivery market is seeing a structural shift in modal economics, with dedicated freight rail becoming a stronger option for time-sensitive long-haul movements. The Western dedicated freight corridor reached full operational status on March 31, 2026, completing the 1,506 km connection between JNPT and Dadri. Freight speeds on the corridor are materially higher than those on conventional mixed-use tracks, improving schedule reliability for intercity freight and making rail more usable for consignments that previously stayed on road. DFCCIL’s Trucks-on-Train service shifted 48,875 trucks to rail on a 636 km WDFC stretch and saved 8.88 million liters of diesel, which shows that operators can lower operating costs when corridor design and service structure line up. This widens the room for railroad network combinations in the India middle-mile delivery market, especially on routes where speed certainty matters more than pure last-mile flexibility.

AI-/IoT-Enabled Visibility and Optimization Platforms

The India middle-mile delivery market is moving toward a model where network visibility is no longer optional for serious operators. CJ Darcl reported a 40% reduction in safety violations and a 20% reduction in unplanned downtime after deploying ADAS and driver fatigue monitoring across its fleet in 2025[2]CJ Darcl Logistics, “Operational Safety and Fleet Technology Report 2025,” CJ Darcl Logistics, cjdarcl.com. FarEye launched its PILOT AI dispatcher in April 2026 to automate load assignment and route optimization for multi-stop middle-mile operations, which cuts planning cycles from hours to minutes for large fleets. Better route orchestration reduces waste in both asset-heavy and asset-light networks, which narrows the cost edge that fleet ownership once offered on its own. That change is important because it allows tech-led challengers to compete more effectively with larger incumbents that built their advantage mainly through physical fleet scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Trucking Base And Driver Shortage | -1.5% | National, with stronger pressure in North and Central India | Long term (≥ 4 years) |

| Fuel-Price Volatility Squeezing Margins | -1.0% | National | Short term (≤ 2 years) |

| Ramp-Up Bottlenecks At Multimodal Logistics Parks | -0.7% | West and Central India, depending on project delays | Medium term (2-4 years) |

| Cold-Chain Compliance Gaps Causing Spoilage Penalties | -0.5% | East India and semi-urban or rural corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Trucking Base and Driver Shortage

The India middle-mile delivery market still faces a structural labor and fleet-organizational problem that limits how quickly capacity can scale during peak periods. The core issue is not only the shortage of qualified drivers, but also the fact that a large share of the fleet remains dispersed across small operators with uneven access to finance, training, and digital systems. That makes throughput harder to scale when shipment demand rises quickly, because operators either commit cautiously or carry higher idle-asset and labor costs. It also slows compliance upgrades in emissions, safety systems, and route technology, which organized shippers increasingly expect as part of service contracts. This keeps service quality uneven and prevents some parts of the India middle-mile delivery market from converting corridor upgrades into fully reliable operational performance.

Fuel-Price Volatility Squeezing Margins

Fuel volatility remains one of the clearest cost-side constraints for the India middle-mile delivery market, especially for road-heavy operators. Diesel continues to account for a large share of operating costs in linehaul movements, meaning even short periods of crude pressure can disrupt route economics and contract profitability. The diesel marketing losses could reach INR 18/liter, or USD 0.21/liter, at crude prices of USD 120-125 per barrel, which would raise the risk of retail price changes and tighter transport margins. Freight-rate pass-through is often delayed in e-commerce and contracted transport, so operators do not always recover these cost jumps at the same pace at which they absorb them. This discourages multi-year fleet expansion and limits near-term capacity additions even when freight demand remains healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transportation Mode: Roads Keep the Core Volumes, While Air Builds a Faster Premium Layer

Roadways held 69.73% of the India middle-mile delivery market share in 2025, leaving them far ahead of other transport modes. That leadership came from the scale of India’s national highway system, which reached 146,572 km and continues to support flexible hub-to-hub movement across industrial and consumption corridors. In the Indian middle-mile delivery market, road remains the default mode for shipments that require broad geographic reach, irregular consignment sizes, or door-to-hub flexibility that rail and air cannot match with the same ease. This is especially relevant for short-haul and intra-regional transfers, where shipment frequency matters more than pure corridor speed.

Airways is set to record the fastest India middle-mile delivery market size CAGR at 10.10% through 2031, reflecting stronger demand from pharmaceutical, perishable, and cross-border freight that places a premium on time certainty. Railways are gaining ground where schedule reliability and long-haul economics now favor corridor-based freight movement. The completion of the Western dedicated freight corridor in 2026 gives rail a stronger role on routes where linehaul efficiency and less congestion matter more than one-leg delivery flexibility. Maritime activity remains tied to port-led and coastal industrial clusters, so its role is concentrated rather than broad.

By Business Model: B2C Holds the Base, While C2C Opens a New Flow Pattern

B2C accounted for 72.03% of the India middle-mile delivery market size in 2025, reflecting the scale that e-commerce platforms and quick-commerce players now bring to organized parcel movement. This model benefits from standardized packaging, repeat routes, frequent inter-hub runs, and the ability to spread automation cost across very large shipment pools. Those operating features make B2C the segment that most clearly rewards dense sortation networks and repeat linehaul schedules. B2B remains important because it anchors steady freight demand from manufacturing, FMCG, and formal distribution contracts, helping operators balance e-commerce seasonality.

C2C is the fastest-growing business model and is projected to expand at a 10.22% CAGR through 2031. The change is tied to recommerce, social selling, and peer-to-peer parcel movement, which are becoming more formal and easier to route through digital networks. In the India middle-mile delivery industry, that means reverse flows, small-batch parcel transfers, and mixed-direction movement are becoming more relevant than before. Operators that built networks only around forward B2C movement may need to redesign hubs to handle more returns, grading, and rerouting capacity. This part of the India middle-mile delivery industry is still smaller than B2C, but it is structurally important because it widens the use cases for national parcel networks.

By Temperature Control: Ambient Freight Dominates Today, While Cold-Chain Moves Faster

Non-temperature-controlled shipments held a 89.11% share in 2025, indicating that ambient cargo still makes up the bulk of intercity freight movement. That outcome is expected because most middle-mile freight in India still comes from categories that do not require controlled temperature conditions during transit. Even so, the balance is shifting as pharmaceuticals, fresh food, and regulated healthcare distribution adopt more formal cold-chain practices.

Temperature-controlled logistics is expected to grow at a 10.38% CAGR through 2031, faster than the broader India middle-mile delivery market. The change is being pushed by compliance as much as by demand. The National Center for Cold-Chain Development has highlighted the role of inadequate refrigerated transport in post-harvest losses, which underlines the cost of leaving the middle-mile cold chain underdeveloped. The same body reported that solar adoption had reached 60% at Type 4 cold-storage facilities in Andhra Pradesh by September 2025, indicating a lower operating-cost base for district-level cold infrastructure. That matters because lower hub operating costs can make temperature-controlled transfers more viable on routes that earlier could not support them. In the India middle-mile delivery market, cold-chain capability is therefore shifting from a niche add-on toward a more meaningful service differentiator.

By Destination: Domestic Density Supports Scale, While International Freight Brings the Faster Upside

Domestic shipments accounted for 86.2% of the India middle-mile delivery market share in 2025, which keeps local intercity movement at the center of network economics. India’s large internal consumption base, dense regional trade flows, and hub-and-spoke parcel systems continue to favor domestic corridor development over export-linked movement. This also explains why route density, backhaul balance, and asset utilization remain the main levers of profitability in the current market structure. Consolidation pressure is strongest here because overlapping domestic routes offer the clearest room for cost reduction when operators combine network capacity and improve hub loading.

The international middle-mile is growing faster and is projected to post a 12.84% CAGR through 2031. The driver is rising cross-border e-commerce and direct-to-consumer exports to nearby markets, especially where air-linked movement matters more than ground flexibility. This shift raises the value of bonded connectivity, airport-linked handling, and compliance-ready freight processes that are less central in purely domestic networks. FedEx’s groundbreaking in February 2026 for an automated air cargo hub in Navi Mumbai, with an investment of INR 2,500 crore (USD 290 million), shows that international and time-sensitive freight is attracting targeted capacity investment. In the India middle-mile delivery market, international freight still starts from a smaller base. Still, it carries a stronger premium profile and is likely to reshape network design at key export gateways.

By End User Industry: E-Commerce Keeps Volume Leadership, While Healthcare Adds Value-Led Growth

E-commerce retail accounted for 32.46% of the India middle-mile delivery market size in 2025, making it the largest end-user category by a wide margin. Its lead reflects the scale of structured B2C fulfillment, the need for repeat inter-hub transfers, and the rising importance of speed-led replenishment networks. Fashion, electronics, home and furniture, and beauty categories continue to support this volume base because they generate both forward shipment demand and meaningful reverse logistics movement. This keeps parcel and part-load systems heavily tied to consumer-led demand cycles.

Healthcare and medical supplies are expected to record the fastest India middle-mile delivery market CAGR of 10.70% through 2031. The reason is not just volume growth, but the formalization of pharma cold chains and stricter handling expectations in healthcare distribution. That shift favors operators that can combine temperature assurance, schedule discipline, and compliance-oriented handling across intercity routes. In the India middle-mile delivery industry, healthcare is therefore becoming a higher-value freight pool, even if it does not yet match e-commerce in absolute volume. The segment is likely to reward specialized operators and diversified national networks more than generalist transport models over the forecast period.

Geography Analysis

The West held 30.1% of India's middle-mile delivery market share in 2025, making it the largest regional market. Its lead comes from the concentration of industrial activity in the Mumbai-Pune-Ahmedabad belt and the region’s close linkage with JNPT and large warehousing clusters. The completion of the Western dedicated freight corridor in 2026 strengthens that position by improving long-haul rail connectivity between western gateway infrastructure and northern demand and production centers. The region also benefits from its mature warehousing base, strong highway connectivity, and a dense mix of manufacturing, export, and consumption demand. These features keep the West central to the India middle-mile delivery market, even as other regions improve their own logistics infrastructure.

North India is the fastest-growing geography and is projected to expand at a 9.29% CAGR through 2031. The region is benefiting from stronger corridor economics as the Eastern dedicated freight corridor improves freight movement from manufacturing clusters in Uttar Pradesh and Haryana into wider national networks. North India also stands to gain from the spread of corridor-linked nodes and more structured linehaul planning under Gati Shakti, which makes new logistics investment easier to anchor around industrial demand. This growth is important because it reflects the creation of new, cost-competitive network capacity rather than simply more use of existing hubs. Central India is also becoming increasingly important as a consolidation hub for north-south and east-west freight movements, reinforcing its role as a transit-oriented logistics zone.

East India remained the smallest regional market in 2025, but its freight potential remains underused relative to the scale of agricultural, textile, seafood, and tea-linked movement in the broader region. The opportunity is stronger for operators that can combine long-haul rail access with disciplined road connectivity, because the region still needs broader network depth more than incremental last-mile density. Mahindra Logistics’ commitment of 4 lakh ft² in Guwahati and Agartala in October 2025 shows that large, organized players are willing to place capacity ahead of full demand normalization in the East and Northeast. South India continues to attract freight linked to healthcare, manufacturing, and export-oriented industries, which supports a stable and maturing logistics base[3]Mahindra Logistics, “Go-East Strategy, 4 Lakh Sq Ft in Guwahati and Agartala,” Mahindra Logistics, mahindralogistics.com. Taken together, these shifts show that the India middle-mile delivery market is widening beyond its traditional western core, even though regional scale and service readiness still differ meaningfully across the country.

Competitive Landscape

The India middle-mile delivery market is moderately fragmented, with the top 5 players accounting for 55% of the market share in 2025. Delhivery, Blue Dart Express, Amazon Transportation Services, XpressBees, and Safexpress form the leading group. Still, none of them controls the market strongly enough to set a dominant industry-wide structure on its own. The remaining share is held by a mix of regional transport operators, tech-enabled platforms, and specialized logistics firms, which keeps pricing, service design, and route specialization active across the field. This means the India middle-mile delivery market rewards density and execution, while still leaving room for mid-tier operators to build a strong position in specific corridors or cargo types. Fragmentation also explains why consolidation, technology investment, and corridor-focused expansion are appearing at the same time rather than one after the other.

A clear competitive pattern is that larger operators are strengthening their networks through infrastructure, digital tools, and new service categories. FedEx India broke ground in February 2026 on a fully automated air cargo hub in Navi Mumbai, investing INR 2,500 crore (USD 290 million), signaling confidence in the growth of premium and cross-border freight. CJ Darcl deployed the MoveX TMS platform across its national fleet in January 2026, and the company reported that transit time variability fell by 25% in the first quarter after deployment[4]CJ Darcl Logistics, “Operational Safety and Fleet Technology Report 2025,” CJ Darcl Logistics, cjdarcl.com. FarEye launched PILOT in April 2026 to automate route planning and dispatch for multi-stop middle-mile operations, which shows how software providers are also shaping network efficiency and service quality. These moves show that competition is no longer only about owning fleet and hubs, but also about how efficiently operators can use the assets they already control.

Another shift in the India middle mile delivery market is the widening gap between operators that can align with structural corridor changes and those that still depend on dispersed, less digitized transport sourcing. The market is placing greater weight on route predictability, cold-chain readiness, intermodal coordination, and technology-based control of linehaul operations. That makes it easier for organized players to defend contracts in healthcare, premium parcel, and corridor-dense B2C freight, while smaller firms remain stronger in narrow regional niches. At the same time, platform-led aggregators continue to matter because they help formal shippers reach fragmented truck capacity without directly building or owning the entire operating base. The result is a market where leadership is meaningful, but the field is still open enough for new share gains through specialization, automation, and corridor-specific execution.

India Middle Mile Delivery Industry Leaders

Delhivery

Blue Dart Express

Amazon Transportation Services

XpressBees

Safexpress

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: FarEye launched PILOT, an AI-powered route dispatcher for multi-stop middle-mile operations; the platform automates load assignment.

- February 2026: FedEx India broke ground on a fully automated air cargo hub at Navi Mumbai; the facility involves an INR 2,500 crore (USD 290 million) investment and a planned capacity of 300,000 ft².

- December 2025: CJ Darcl explored parcel rail services in partnership with CONCOR at Bhiwandi, testing a new asset-light container-on-rail proposition for the western middle-mile corridor.

- October 2025: Mahindra Logistics committed 4 lakh sq ft in Guwahati and Agartala as part of an explicitly stated Go-East geographic expansion strategy, the first systematic capacity commitment to Northeast India by a large national 3PL.

India Middle Mile Delivery Market Report Scope

| Roadways |

| Railways |

| Airways |

| Maritime |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

| Non-Temperature Controlled |

| Temperature Controlled |

| Domestics |

| International |

| E-commerce Retail |

| Fashion and Lifestyle |

| Beauty, Wellness and Personal Care |

| Home and Furniture |

| Consumer Electronics and Appliances |

| Healthcare and Medical Supplies |

| Others |

| North |

| Central |

| West |

| East |

| South |

| By Transportation Mode | Roadways |

| Railways | |

| Airways | |

| Maritime | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Destination | Domestics |

| International | |

| By End User Industry | E-commerce Retail |

| Fashion and Lifestyle | |

| Beauty, Wellness and Personal Care | |

| Home and Furniture | |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Supplies | |

| Others | |

| By Region | North |

| Central | |

| West | |

| East | |

| South |

Key Questions Answered in the Report

How large is the India middle-mile delivery market in 2026, and where is it headed by 2031?

The India middle-mile delivery market stands at USD 4.34 billion in 2026 and is projected to reach USD 6.52 billion by 2031, growing at an 8.47% CAGR over 2026-2031.

Which transportation mode leads freight movement across India’s middle-mile networks?

Roadways led with 69.73% share in 2025 because they offer the broadest route flexibility and the strongest fit for hub-to-hub and intercity freight movement.

Which business model is growing fastest in India’s parcel transfer network?

C2C is projected to grow the fastest at a 10.22% CAGR through 2031, supported by recommerce, social commerce, and more formal peer-to-peer parcel flows.

Why is temperature-controlled freight expanding faster than the broader sector?

Temperature-controlled logistics is projected to grow at a 10.38% CAGR through 2031, as pharma and food supply chains move toward tighter compliance and more formal cold-chain handling.

Which region leads today, and which one is expanding the fastest?

The West led with a 30.1% share in 2025, while North India is expected to grow the fastest at a 9.29% CAGR through 2031.

How concentrated is competition among the leading operators?

The top 5 companies held a 55% share in 2025, indicating a moderately fragmented structure where scale matters but regional and specialized operators still retain meaningful space.

Page last updated on: