India Warehouse Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

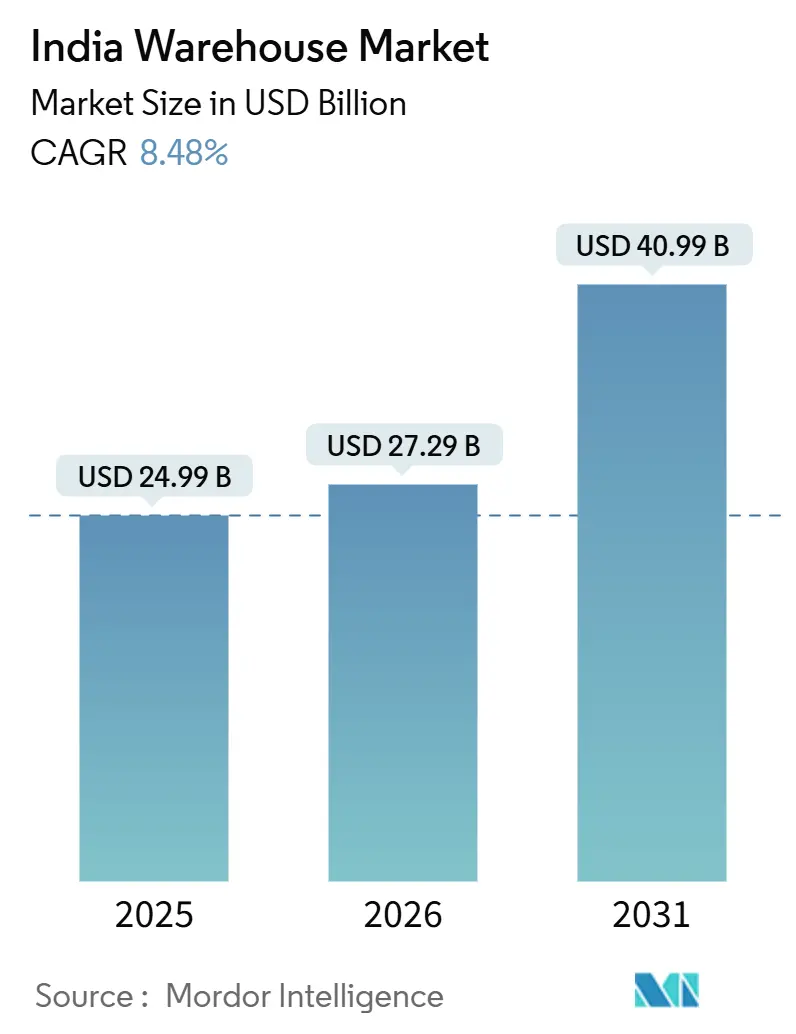

| Base Year Market Size (2025) | USD 24.99 Billion |

| Market Size (2026) | USD 27.29 Billion |

| Market Size (2031) | USD 40.99 Billion |

| Growth Rate (2026 - 2031) | 8.48% CAGR |

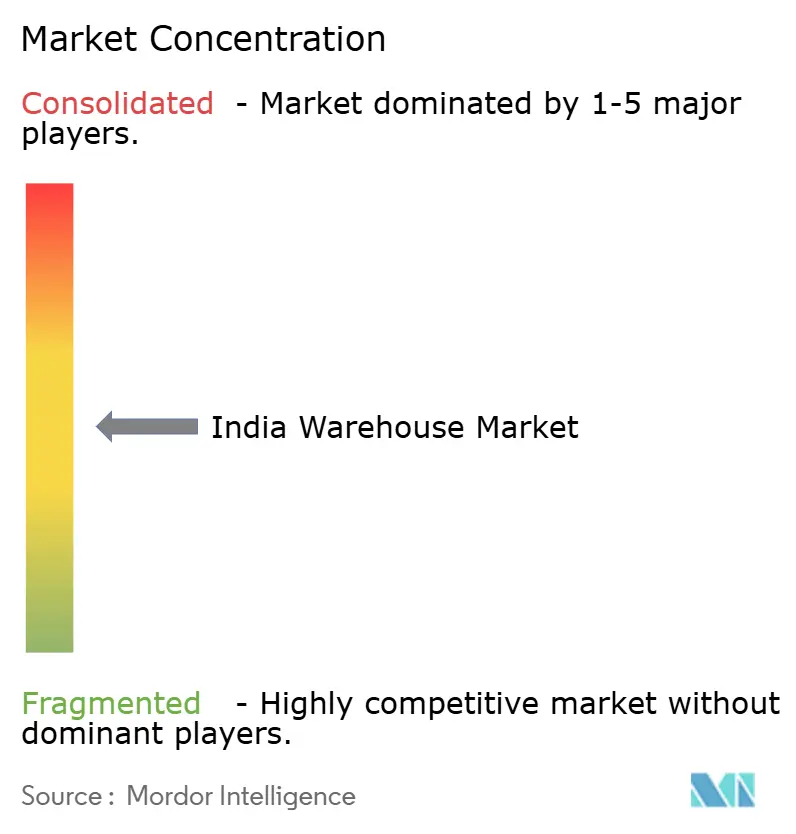

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Warehouse Market Analysis by Mordor Intelligence

The India warehouse market size is expected to grow from USD 24.99 billion in 2025 to USD 27.29 billion in 2026 and is forecast to reach USD 40.99 billion by 2031 at 8.48% CAGR over 2026-2031.

Infrastructure policy reforms, dedicated freight corridors, and production-linked incentives are compressing transportation times, lowering per-unit logistics costs, and enlarging the viable catchment for Grade-A facilities. Institutional investors are channeling capital into compliant, ESG-certified parks that promise stable yields and faster lease-up. Cold chain gaps, omni-channel retail, reverse-logistics complexity, and green-warehouse mandates are segment-specific catalysts that collectively deepen demand pools. Simultaneously, rising fire-insurance premiums and protracted environmental clearances raise execution risk for developers yet create scarcity-driven rent premiums for compliant stock.

Key Report Takeaways

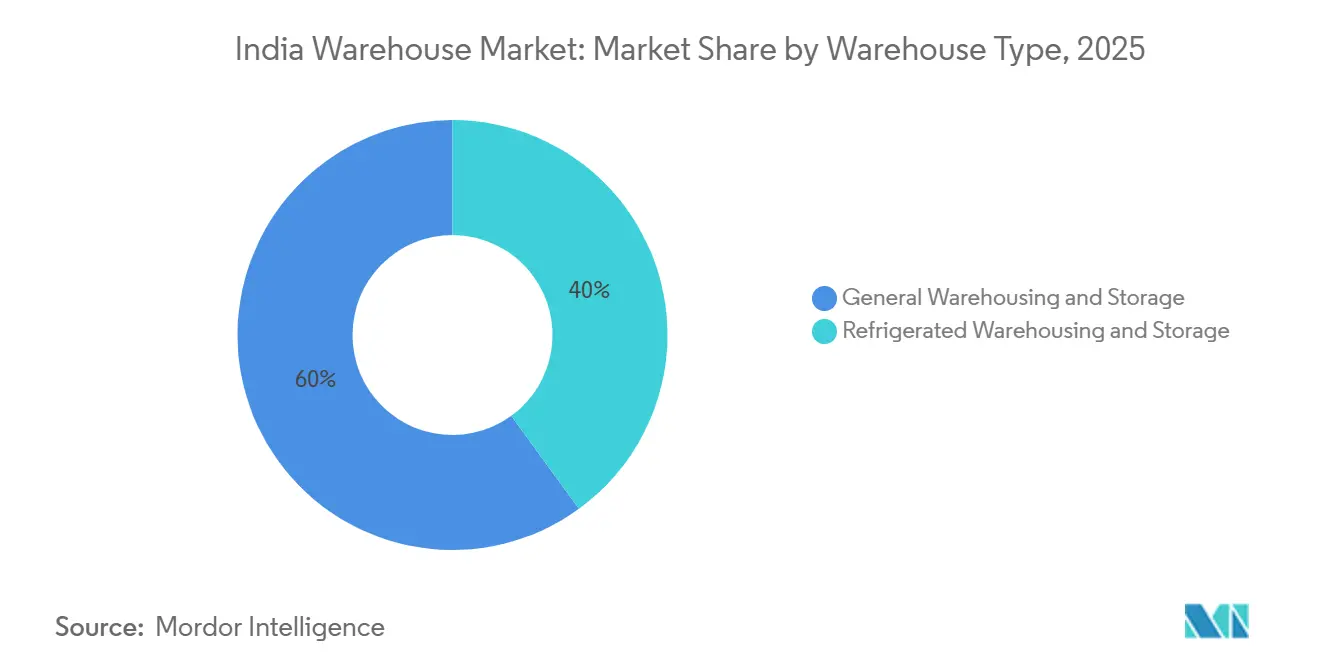

- By warehouse type, general warehousing and storage led with 60.01% of India warehouse market share in 2025. Refrigerated warehousing and storage is projected to post the fastest growth at 12.94% CAGR through 2031.

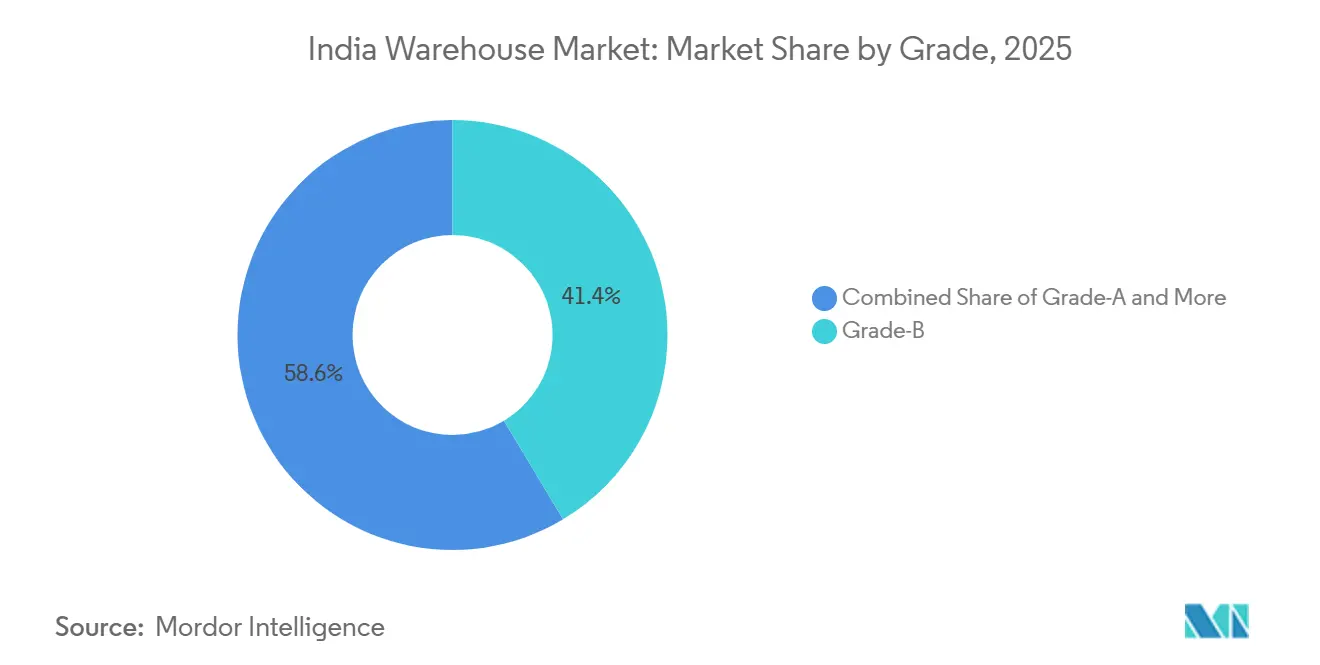

- By grade, Grade-B facilities contributed 41.4% to the India warehouse market size in 2025. Grade-A warehouses are expanding at 13.85% CAGR over 2026-2031.

- By end user, e-commerce and retail commanded 26.02% of India warehouse market share in 2025, while pharma and healthcare is advancing at 13.71% CAGR.

- By geography, West India captured 35.19% of the India warehouse market size in 2025, whereas South India is forecast to grow at 12.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Warehouse Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation of national logistics policy | +1.5% | Nationwide logistics clusters | Medium term (2-4 years) |

| Commissioning of dedicated freight corridors and multi-modal logistics parks | +2.0% | Western & Eastern corridors | Long term (≥ 4 years) |

| Production-linked incentive schemes | +1.8% | Major manufacturing states | Medium term (2-4 years) |

| Omni-channel retail micro-fulfillment | +1.2% | Tier-I & Tier-II cities | Short term (≤ 2 years) |

| ESG-compliant green warehouses | +0.8% | Institutional-grade assets | Medium term (2-4 years) |

| Reverse-logistics and returns processing | +0.9% | National e-commerce hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Implementation of National Logistics Policy (NLP-2022)

The policy targets a logistics-cost reduction to below 8% of GDP by 2030, spurring organized warehousing investment. State-level CLAPs have introduced single-window clearances that shorten approval cycles, especially in Maharashtra, Gujarat, and Tamil Nadu. ULIP’s integration of 36 central and state systems offers real-time visibility of cargo and capacity, enabling dynamic space allocation for 3PLs. The mandated 35 multi-modal logistics parks, backed by INR 46,000 crore, embed warehousing, customs, and transport nodes, widening the radius of feasible hinterland sites. Tenants gain faster access to rail-road interfaces, cutting overall dwell time and improving inventory turns[1]“National Logistics Policy,” Ministry of Commerce & Industry, commerce.gov.in.

Commissioning of Dedicated Freight Corridors & Multi-Modal Logistics Parks

By 2025, the Western and Eastern corridors reached 96.4% completion, enabling 352 daily freight trains running at 100 km/h and slicing Delhi-Mumbai and Ludhiana-Kolkata transit times by up to 40%. Occupiers now favor sites within 30 km of corridor nodes, evidenced by robust absorption in Luhari and Bhiwandi. Developer announcements, such as IndoSpace’s 1.7 million sq ft Bhiwandi park and Welspun One’s 1.2 million sq ft Talegaon project, specifically cite proximity to DFC interchanges and planned MMLPs[2]“Project Progress Update,” Dedicated Freight Corridor Corporation of India, dfccil.com.

Production-Linked Incentive Schemes Boosting Manufacturing Inventory

PLI approvals worth INR 2.16 lakh crore have catalyzed sectoral clusters for electronics, automotive, and pharmaceuticals. Manufacturers co-locate component stores within 15 km of plants to support just-in-time lines, while last-mile fulfillment centers rise near consumption hubs, jointly enlarging demand for hybrid warehouses with higher power loads and mezzanine office blocks. High-bay racking designs in new facilities accommodate light assembly, tightening the overlap between factory and warehouse real estate.

Omni-Channel Retail’s Push for Decentralized Micro-Fulfilment Centers

Same-day and two-hour delivery pledges of quick-commerce firms trigger a hub-and-spoke architecture of 2,000-5,000 sq ft dark stores in city peripheries. Regional replenishment lines now lease large single-tenant blocks, for example, Swiggy’s 580,700 sq ft contract in Bhiwandi, to feed micro-fulfilment nodes efficiently. Traditional retailers mirror the model; Avenue Supermarts’ 66,250 sq ft facility in Panvel demonstrates long-tenure, metro-adjacent warehousing that minimizes last-mile logistics cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental-impact & fire-safety clearances | −0.7% | Eco-sensitive & urban peripheries | Short term (≤ 2 years) |

| Intermittent grid power | −0.6% | Tier-II/III clusters | Medium term (2-4 years) |

| Skilled automation technician shortage | −0.5% | Nationwide | Medium term (2-4 years) |

| Escalating insurance premiums | −0.4% | High-density or flood-prone zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy Environmental-Impact & Fire-Safety Clearance Timelines

Facilities exceeding 20,000 sq m require EIA approval under MoEFCC guidelines, extending project gestation by up to 12 months. High-rack structures also face strict sprinkler and hydrant compliance under NBC-2016. Developers sometimes phase projects below the EIA threshold to mitigate delays, sacrificing economies of scale. The 2024 WDRA handbook aims to harmonize technical norms, yet adoption varies across states[3]“Draft Energy Performance Standards for Warehouses,” Bureau of Energy Efficiency, beeindia.gov.in .

Intermittent Grid Power Jeopardizing Automation Uptime

Tier-II nodes endure 2-4 hours of daily load shedding, pushing operators to install diesel generators or battery energy storage, which inflate capital intensity by 10-15%. Unplanned outages disrupt AS/RS and conveyor systems, reducing throughput and elevating manual handling error rates. Some Grade-A parks now incorporate rooftop solar with four-hour battery back-up, but this adds USD 9-14 per sq ft to build cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Cold Chain Gains as Pharma, Perishables Expand

General warehousing and storage controlled 60.01% of India warehouse market share in 2025, serving e-commerce, FMCG, and engineering goods. Refrigerated warehousing is forecast to grow at 12.94% CAGR on the back of vaccine distribution, QSR expansion, and perishable exports. Snowman Logistics augmented capacity from 154,330 to 160,230 pallets across 22 cities by March 2026, adding new Pune and Patna sites. Refrigerated facilities command rent premiums of up to 60% over ambient warehouses and achieve 85-90% occupancy due to stringent compliance gaps. The India warehouse market size for the cold chain sub-segment is thus projected to outpace ambient space additions through 2031.

Pharmaceutical occupiers demand WHO-GDP-validated environments with continuous monitoring, sustaining long-duration leases and higher yields for specialized operators. General warehousing remains vital, but commoditization and micro-market oversupply temper rent growth, pushing landlords to retrofit automation and ESG features[4]“Pharmaceuticals Sector – GDP and Storage Guidelines Support,” Department of Pharmaceuticals, pharmaceuticals.gov.in.

By Grade: Institutional Capital Propels Grade-A Expansion

Grade-B sites formed 41.4% of the India warehouse market size in 2025, appealing to cost-sensitive SMEs at monthly rents of INR 18-25 per sq ft. Grade-A stock, however, is expanding at 13.85% CAGR as sovereign funds and pension-backed platforms deploy capital into high-spec parks with 10-meter clear heights, 5 T/m² loading floors, and IGBC or LEED certifications. National Grade-A absorption totaled 41.7 million sq ft in 2025, with Delhi-NCR alone delivering almost one-third of new completions.

The wider flight-to-quality narrative sees occupiers consolidating dispersed Grade-C sheds into fewer automation-ready Grade-A boxes, improving throughput and lowering insurance premiums. While Grade-C assets still service low-value goods in Tier-III towns, regulatory tightening on fire safety and green norms is accelerating obsolescence, pushing landlords either to upgrade or exit altogether.

By End-User Industry: E-Commerce Leads, Pharma Surges on Compliance

E-commerce and retail provided 26.02% demand of the warehouse industry in India in 2025, driven by platform-led fulfillment for same-day and quick-commerce deliveries. Amazon’s leases in Luhari and Hoskote underscore the scale of national networks. Pharma and healthcare, though smaller in base, is growing at 13.71% CAGR, underpinned by PLI-boosted vaccine and biologics production that requires strict temperature control.

Food and beverage tenants straddle ambient and chilled zones, expanding especially near consumption centers to reduce spoilage. Automotive and engineering firms favor first-mile warehouses near plants to facilitate just-in-sequence deliveries. Multi-client 3PL models now account for 45% of large-format leasing, pooling seasonally-volatile demand and lifting utilization rates above 85%.

Geography Analysis

West India anchored 35.19% of the India warehouse market size in 2025. Bhiwandi alone absorbed 4.9 million sq ft of Grade-A supply owing to proximity to JNPA port and Mumbai’s dense consumer base. IndoSpace’s 66-acre park and Welspun One’s Talegaon investment exemplify developer conviction in sustained trade flows through western ports. Gujarat’s Vapi and Mundra corridors benefit from petrochemical and export-oriented manufacturing, while Pune’s Chakan-Talegaon belt services the automotive cluster with automation-ready facilities.

South India is projected to record a 12.56% CAGR to 2031. Chennai alone absorbed over 8 million sq ft in 2025, fueled by electronics and automotive OEMs clustered in Oragadam. DHL Supply Chain’s 350,000 sq ft lease in Polivakkam enhances contract-logistics reach. Bengaluru’s western corridor drew 1.7 million sq ft in H1 2025, half of it from e-commerce, while Hyderabad leveraged Outer Ring Road connectivity to strengthen pharma and IT distribution hubs.

North India, led by Delhi-NCR, contributed significantly to national absorption, with Luhari and Manesar favored for DFC adjacency. Amazon and Honda leased blocks of 500,000 sq ft each in Grade-A parks, signaling confidence in NCR as a gateway for north-west distribution. East India is emerging: Mahindra Logistics’ 400,000 sq ft Go-East rollout in Guwahati and Agartala positions the firm for cross-border trade with Bangladesh, while Snowman’s Patna site will bolster cold chain capacity for seafood and pharma. Central India remains nascent but gains traction on lower land costs and Bharatmala highways, highlighting the scope for a first-mover advantage as pan-India networks densify.

Competitive Landscape

The India warehouse market hosts a moderately fragmented set of players where the top five developers and 3PLs together control roughly 45-50% of Grade-A stock. Institutional platforms such as IndoSpace, ESR, and Welspun One scale pan-regional parks with clear heights of greater than 10 m, ESG features, and multimodal access.

Specialized operators like Snowman Logistics and ColdEx dominate temperature-controlled warehousing, leveraging pharma compliance to secure long-tenure contracts. Mahindra Logistics, Delhivery, and TCI integrate transport, last-mile, and warehousing to offer one-stop solutions, limiting tenant churn. Digital aggregators, including Warehouzez and Godamwale, match excess warehouse capacity with on-demand occupiers, improving market liquidity.

With in the warehouse industry in India, automation and technology adoption differentiate leaders: AS/RS, IoT sensors, and AI-enabled WMS enhance throughput and accuracy, while labor upskilling initiatives ensure uptime. ESG compliance further shapes competition; parks with IGBC or LEED ratings achieve 8-12% rent premiums and attract pension-fund capital. Quick-commerce firms internalize micro-fulfilment centers to control last-mile costs. White-space opportunities persist in Tier-III towns where Grade-A penetration is under 15%, in reverse-logistics hubs for e-commerce returns, and in hybrid warehouse-cum-light-assembly facilities near PLI manufacturing clusters.

India Warehouse Industry Leaders

DHL Group

Mahindra Logistics, Ltd.

TVS Supply Chain Solutions

IndoSpace

Allcargo Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Snowman Logistics began constructing a 6,500-pallet temperature-controlled warehouse in Patna, targeting seafood, QSR, and pharma distribution.

- January 2026: DHL Supply Chain leased 350,000 sq ft at Value Spaces Logistics and Industrial Park near Chennai to strengthen its southern fulfillment network.

- December 2025: Welspun One secured 46 acres in Talegaon MIDC, Pune, to develop a 1.2 million sq ft Grade-A logistics park with INR 550 crore investment.

- October 2025: Mahindra Logistics launched 300,000 sq ft in Guwahati and 130,000 sq ft in Agartala under its Go-East expansion.

India Warehouse Market Report Scope

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

| Grade-A |

| Grade-B |

| Grade-C & Unorganised |

| E-commerce and Retail |

| Food and Beverage |

| Pharma and Healthcare |

| Automotive |

| Manufacturing and Engineering Goods |

| Others |

| North India | Delhi-NCR |

| Punjab | |

| Haryana | |

| Others | |

| South India | Karnataka |

| Tamil Nadu | |

| Telangana | |

| Others | |

| West India | Maharashtra |

| Gujarat | |

| Others | |

| East India | West Bengal |

| Odisha | |

| Others | |

| Central India | Madhya Pradesh |

| Chhattisgarh |

| Segmentation by Warehouse Type (Value) | General Warehousing and Storage | |

| Refrigerated Warehousing and Storage | ||

| Segmentation by Grade (Value) | Grade-A | |

| Grade-B | ||

| Grade-C & Unorganised | ||

| Segmentation by End-User Industry (Value) | E-commerce and Retail | |

| Food and Beverage | ||

| Pharma and Healthcare | ||

| Automotive | ||

| Manufacturing and Engineering Goods | ||

| Others | ||

| Segmentation by Region (Value) | North India | Delhi-NCR |

| Punjab | ||

| Haryana | ||

| Others | ||

| South India | Karnataka | |

| Tamil Nadu | ||

| Telangana | ||

| Others | ||

| West India | Maharashtra | |

| Gujarat | ||

| Others | ||

| East India | West Bengal | |

| Odisha | ||

| Others | ||

| Central India | Madhya Pradesh | |

| Chhattisgarh | ||

Key Questions Answered in the Report

What is the projected value of the India warehouse market in 2031?

The market is forecast to reach USD 40.99 billion by 2031.

Which warehouse type is growing fastest?

Refrigerated warehousing and storage is projected to expand at 12.94% CAGR through 2031.

Why are Grade-A facilities attracting more investors?

Grade-A warehouses offer higher clear heights, ESG certifications, and compliance features, enabling faster lease-up and premium rents.

Which region is expected to record the highest growth rate to 2031?

South India is forecast to grow at 12.56% CAGR, driven by electronics, automotive, and pharma clusters.

How do dedicated freight corridors influence warehouse location?

They cut intercity transit times by up to 40%, prompting occupiers to site warehouses within 30 km of corridor nodes to reduce transport costs and improve inventory turns.

What are the main challenges for warehouse automation adoption?

Intermittent grid power and a shortage of skilled technicians increase capital and operational costs, slowing automation rollouts.

Page last updated on: