India Last Mile Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

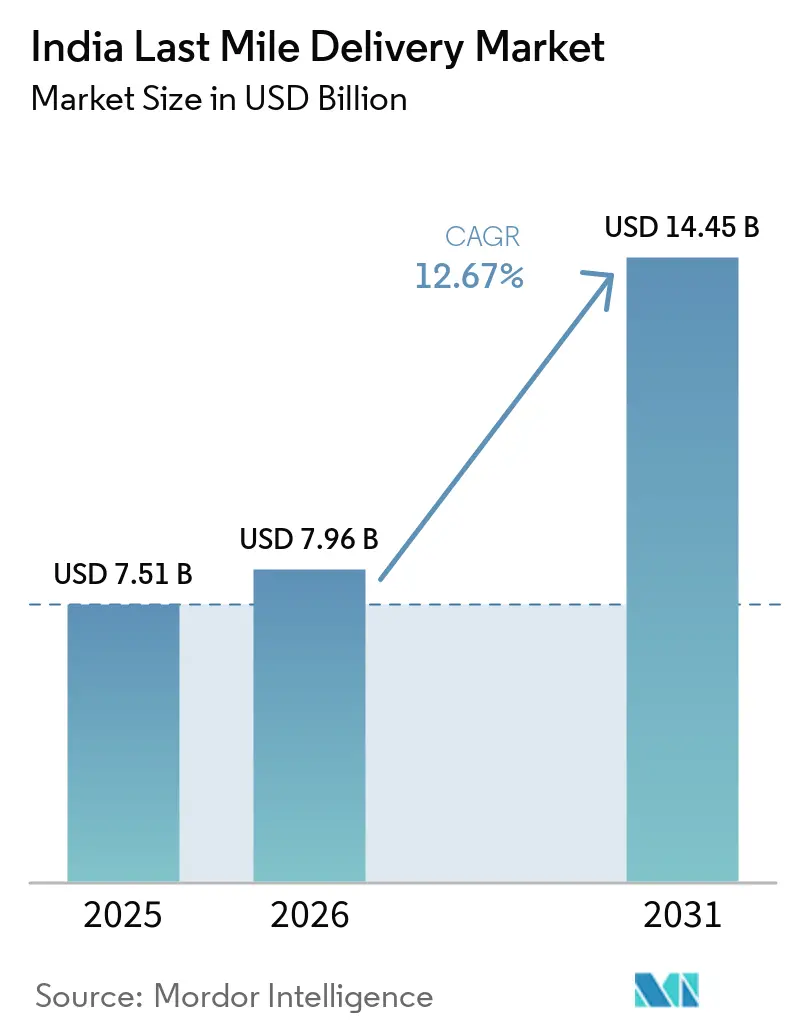

| Base Year Market Size (2025) | USD 7.51 Billion |

| Market Size (2026) | USD 7.96 Billion |

| Market Size (2031) | USD 14.45 Billion |

| Growth Rate (2026 - 2031) | 12.67% CAGR |

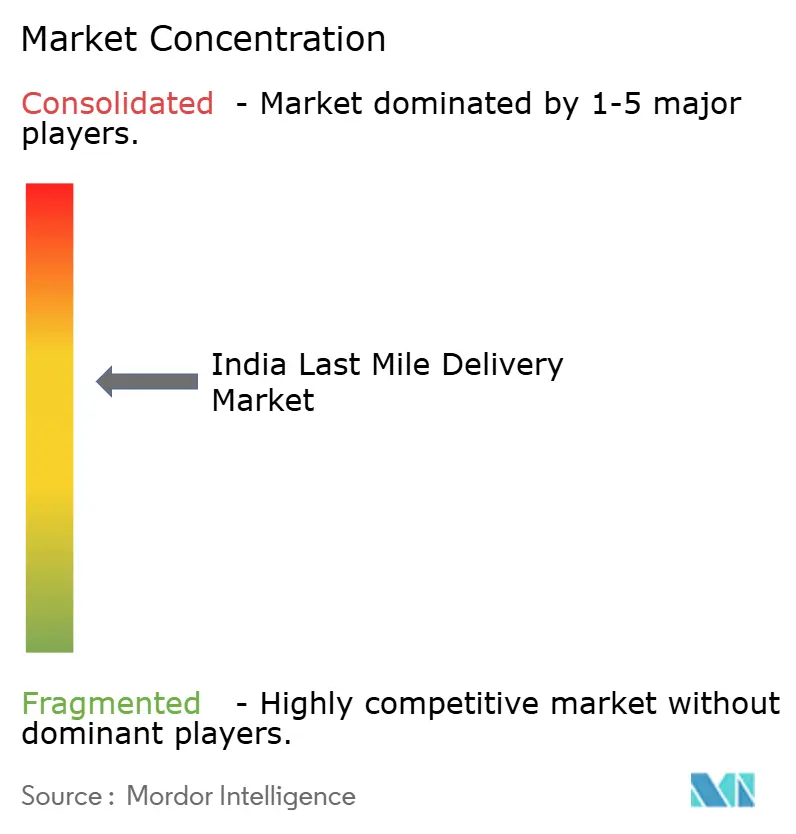

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Last Mile Delivery Market Analysis by Mordor Intelligence

The India last mile delivery market size is projected to expand from USD 7.51 billion in 2025 and USD 7.96 billion in 2026 to USD 14.45 billion by 2031, registering a CAGR of 12.67% between 2026 to 2031.

Rising disposable income in Tier-2 and Tier-3 cities is swelling e-commerce gross merchandise value, while quick-commerce platforms are normalizing sub-15-minute delivery windows in metro catchments, pushing network planners to build dense micro-fulfillment footprints. Regulatory tailwinds from the National Logistics Policy are reducing inter-state dwell times and spurring corridor-linked warehousing, even as urban congestion is raising per-stop costs by up to 22% in Delhi, Mumbai, and Bengaluru. Consolidation has accelerated since Delhivery acquired Ecom Express, a deal that immediately combined 35% of third-party parcel flows and signaled that technology scale will decide future leadership. At the same time, the Unified Logistics Interface Platform’s open-API architecture is lowering compliance friction for digitally mature carriers, widening the performance gap with legacy operators.

Key Report Takeaways

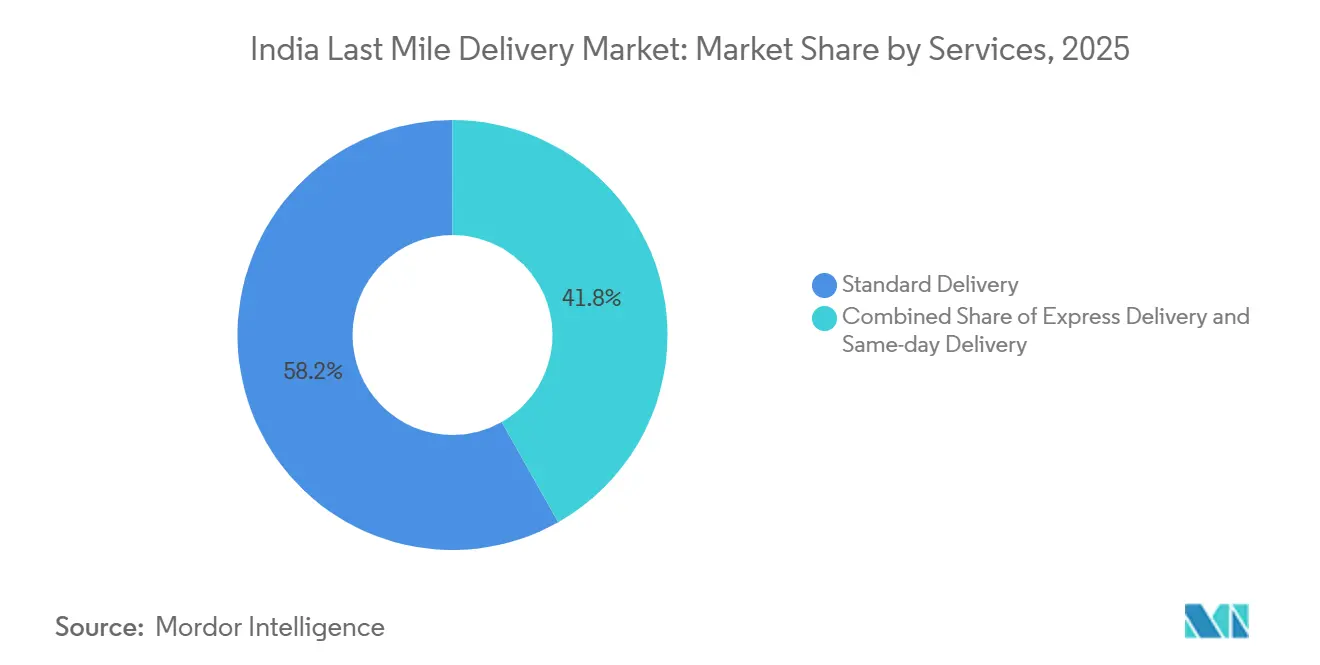

- By service, standard delivery led with 58.19% of the India last mile delivery market share in 2025, while same-day delivery is projected to post the highest 14.32% CAGR through 2031.

- By business model, business-to-consumer flows accounted for 69.88% of the India last mile delivery market size in 2025, yet customer-to-consumer logistics is forecast to expand at a 14.44% CAGR, driven by the booming resale economy.

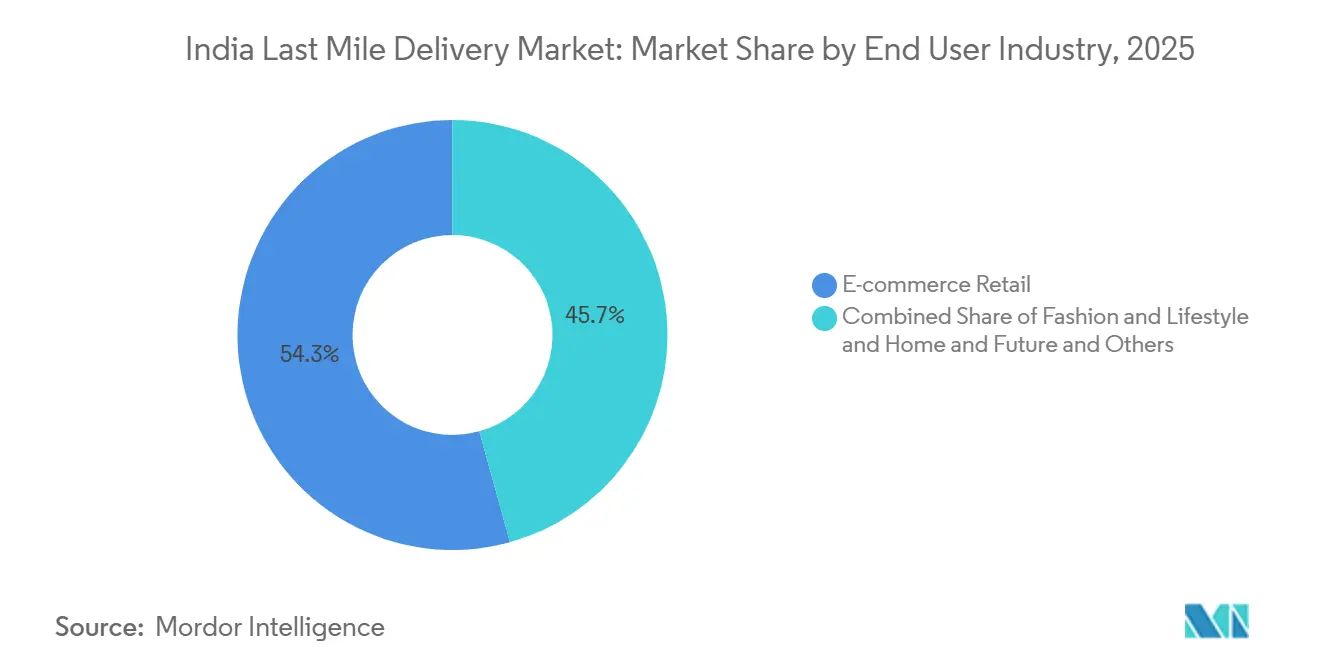

- By end-user industry, e-commerce retail accounted for 54.3% of the India last mile delivery market share in 2025. In contrast, healthcare and medical supplies will advance at the fastest 14.60% CAGR on the back of biologics cold-chain mandates.

- By region, the West accounted for 28.71% of the India last-mile delivery market size in 2025. Central India is expected to grow the fastest, at a 13.15% CAGR, as multimodal parks in Madhya Pradesh shorten inland lead times.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive E-Commerce GMV Surge in Tier-2/3 Cities | 2.8% | National, with concentration in Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| Rapid Expansion of Quick-Commerce and Dark Stores | 2.5% | Metro markets (Mumbai, Delhi-NCR, Bengaluru, Hyderabad, Pune), spillover to Tier-1 cities | Short term (≤ 2 years) |

| National Logistics Policy and Corridor Build-Out | 1.8% | National, early gains in PM GatiShakti pilot corridors across Central and North India | Long term (≥ 4 years) |

| AI-Driven Routing and Fulfillment Optimization | 1.2% | National, with advanced adoption in metros and Tier-1 cities | Medium term (2-4 years) |

| Electric 2-Wheeler-as-a-Service Unlocking Gig Capacity | 1.0% | Delhi-NCR, Maharashtra, Karnataka (states with EV subsidies and charging infrastructure) | Medium term (2-4 years) |

| ULIP Open-API Data Platform Streamlining Compliance | 0.7% | National, phased rollout across logistics service providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive E-Commerce GMV Surge in Tier-2/3 Cities

Tier-2 and Tier-3 GMV expanded by 42% in 2025, far outstripping metro growth, as smartphone penetration crossed 61% in rural areas and vernacular apps lowered entry barriers for first-time buyers. Flipkart’s Ekart expanded its pin-code coverage from 19,000 to 23,500, compressing the two-day delivery coverage across Jaipur, Lucknow, and Visakhapatnam[1]Flipkart Investor Relations, Flipkart, flipkart.com. At the same time, ElasticRun’s kirana network model has reduced last-mile costs by 30% in Uttar Pradesh and Bihar. Parcel density now justifies direct truck routes, reducing reliance on hubs and spokes, though 40% of addresses still lack standardized building numbers, adding 8-12 minutes per stop. The Indian last-mile delivery market is therefore pivoting to adopt intelligent engines to improve first-attempt success rates. Carriers that crack rural geocoding will secure loyalty in the fastest-growing demand pockets.

Rapid Expansion of Quick-Commerce and Dark Stores

Dark-store count hit 1,489 by March 2026, up 67% in fifteen months as Blinkit, Zepto, and Swiggy Instamart raced to maintain 10-15-minute delivery promises. Funding inflows Zepto’s USD 1 billion in 2025 and Blinkit’s integration within Zomato underscore investor confidence that high order frequency offsets smaller baskets. Real estate premiums of 35% in Andheri and Koramangala highlight the strategic value of hyperlocal nodes. Category expansion into electronics lifted average order values to INR 485 (USD 5.13), pushing contribution margins positive in select micro-markets. Draft FSSAI norms on temperature logs for perishables are likely to create compliance hurdles, favoring platforms with cold-chain readiness[2]Food Safety and Standards Authority of India, “Draft Guidelines for Quick-Commerce,” fssai.gov.in .

National Logistics Policy and Corridor Build-Out

The Policy’s INR 1.4 lakh (USD 1,481) crore outlay is funding 35 multimodal parks and four freight corridors that promise 20-30% reductions in transit time between production and consumption hubs. Early wins include Pithampur and Indore parks, which attracted INR 2,300 (USD 24.34) crore private investment by mid-2025. The Bharatmala program’s 8,200 km of economic corridors have reduced road-freight costs by up to 15% on the Delhi-Mumbai and Chennai-Bengaluru axes. Compliance enablers such as GPS-linked electronic waybills are further eroding invisible border wait times. As these corridors mature, the India last mile delivery market will benefit from lower linehaul volatility and deeper inland warehousing.

AI-Driven Routing and Fulfillment Optimization

Machine-learning route engines delivered 12-18% fuel savings and lifted on-time performance to 91% among early adopters. Flipkart’s neural model assigns parcels to the closest fulfillment node, shaving average delivery time in Tier-1 cities from 52 hours to 38 hours. Locus processed over 1.2 billion transactions in 2025, signaling a scale threshold that small carriers struggle to match. Integration gaps in legacy transport systems limit data-driven gains among fragmented players, prompting a technology divide that could spur further consolidation in the India last-mile delivery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Metro Quick-Commerce Saturation and Discount Wars | -1.5% | Mumbai, Delhi-NCR, Bengaluru, Hyderabad, Pune (metro markets) | Short term (≤ 2 years) |

| High RTO Rates from Tier-2/3 Address Quality Gaps | -1.2% | Tier-2 and Tier-3 cities across Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan, Odisha | Medium term (2-4 years) |

| Urban Congestion & Parking Shortages Inflating Costs | -0.8% | Delhi, Mumbai, Bengaluru, Kolkata, Chennai (major urban centers) | Short term (≤ 2 years) |

| Sparse EV-Charging/Financing Slowing Green Fleets | -0.5% | Tier-2 and Tier-3 cities, rural areas with limited charging infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Metro Quick-Commerce Saturation and Discount Wars

Penetration among online grocery shoppers crossed 38% in Mumbai, Delhi-NCR, and Bengaluru by March 2026, near maturity levels seen in South Korea, driving customer-acquisition costs up 62% year on year[2]Mumbai Traffic Police, “Parking Statistics 2025,” traffic.mumbaipolice.gov.in. The collective cash burn of INR 3,200 (USD 33.86) crore in FY 2025-26 slashed gross margins to 11%, down from 18% a year earlier. Average order values fell to INR 440 (USD 4.66) as consumers cherry-picked discount SKUs, undermining category-expansion strategies. The Competition Commission has opened a probe into alleged predatory pricing, stoking uncertainty. Platforms are pivoting toward Tier-1 cities where density is lower and delivery promises can stretch to 20-30 minutes, but the economics remain unproven.

High RTO Rates from Tier-2/3 Address Quality Gaps

RTO averaged 27% for cash-on-delivery parcels in 2025, against 12% in metros, bleeding INR 2,800 crore (USD 296.8 million) in wasted costs. Non-standardized landmark-based addresses thwart machine geocoding, leaving first-attempt delivery success as low as 73% before Delhivery’s INR 100 crore (USD 11.9 million) address-intelligence engine pushed it to 84% in Kanpur, Patna, and Bhopal. Cash-on-delivery still accounts for 55% of Tier-2 transactions owing to lower card penetration, which compounds refusal risk. Without rapid digitization of address data, India's last-mile delivery market will continue to bear the costs of costly reverse logistics in growth regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Speed Premiums Reshape Pricing

Standard delivery led with 58.19% of the Indian last-mile delivery market share in 2025, while same-day delivery is projected to post the highest 14.32% CAGR through 2031. Standard delivery’s 2025 lead rests on its suitability for non-perishable categories that tolerate 3-5-day windows. Express delivery bridges the gap for fashion orders where next-day delivery matters but premium fees deter same-day uptake. Carriers are channeling capex into AI sortation lines, such as Delhivery’s Bengaluru gateway, which handles 1.2 million parcels daily. These shifts will gradually shift the India last-mile delivery market toward faster tiers without erasing the cost-efficient standard segment.

Network differentiation now hinges on dark-store density and data-driven slot-allocation. Amazon’s Prime Now processed 42 million shipments in 2025, sustaining a 35% price premium that Indian consumers are willing to pay to avoid stockouts[3]Amazon India Annual Report 2025, Amazon, amazon. in. Blue Dart’s Tier-2 express surge during the 2025 festive season underscores the hinterland's appetite for a predictable next-day service. As AI-enabled dynamic routing proliferates, carriers that balance cost and speed will capture incremental market share in India's last-mile delivery market.

By Business Model: C2C Gains as Resale Booms

Business-to-consumer accounted for 69.88% of the India last-mile delivery market share in 2025, yet margin compression from discount wars is nudging carriers to court higher-yield B2B and C2C flows. The C2C segment is set for a 14.44% CAGR, fueled by OLX, Cashify, and Meesho’s 18 million peer-to-peer annual shipments, as well as regulatory Extended Producer Responsibility targets for electronics take-back. ElasticRun’s 1.2 million-store network highlights B2B’s ability to undercut B2C's last-mile cost by 30% through shared retail footfall. Carriers that tailor settlement cycles and reverse-pickup capabilities can tap the swelling circular-economy opportunity inside the Indian last-mile delivery market.

Resale-driven parcel diversity challenges legacy hub operations, pressing the need for parcel-level visibility and fraud detection. Done and Porter now derive 22% of revenue from C2C pickup-drop, a strategic hedge against maturing metro quick-commerce. Collectively, these shifts diversify revenue streams and dilute exposure to subsidy-heavy B2C e-grocery traffic.

By End User Industry: Healthcare Outpaces Retail

Healthcare and medical supplies will grow fastest at 14.60% CAGR as online pharmacies scale, and biologics demand strict 2-8 °C control. Medikabazaar’s funding round to deploy temperature-controlled fleets across 450 cities exemplifies investment momentum. E-commerce retail, already capturing 54.3% of the Indian last-mile delivery market size in 2025, will continue to expand, but at a moderated clip as metro demand plateaus. Fashion’s high 35% return rate pressures margins, prompting surcharges for reverse logistics that could temper share growth.

Consumer electronics benefit from low returns and high ticket size, ensuring premium fee tolerance. Beauty and personal care leverage high gross margins to absorb same-day surcharges, reinforcing speed differentiation. Home and furniture remain a niche yet lucrative niche due to assembly needs and white-glove expectations. The Indian last-mile delivery market, therefore, displays end-user heterogeneity that underpins multiple service tiers.

Geography Analysis

The West delivered 28.71% of 2025 revenue, buoyed by JNPT’s 5.8 million TEU throughput and Pune’s deep manufacturing base. Quick-commerce penetration in Mumbai reached 42%, intensifying competition in micro-fulfillment. Central India, projected to grow at a 13.15% CAGR, is fast catching up, with Pithampur and Indore logistics parks shortening lead times to 52 million consumers. South India’s 26% share reflects Bengaluru’s 1.8 million daily deliveries and Chennai’s USD 48 billion manufacturing exports.

North India combines Delhi-NCR’s dense quick-commerce grid with Uttar Pradesh’s Tier-2 boom, though weak address hygiene elevates RTO. East India is lagging due to road-density deficits and patchy 4G coverage. Yet, the Eastern Dedicated Freight Corridor now cuts Kolkata-Delhi rail to 28 hours, improving linehaul economics. As BharatNet closes the digital gap by 2027, last-mile reliability across underserved eastern districts should improve, redistributing an incremental share of the Indian last-mile delivery market.

South India’s policy push for electric fleets, including Karnataka’s INR 15,000 (USD 159) subsidy, spurred the deployment of 12,000 EVs in Bengaluru by March 2026, making the city a test bed for zero-emission last-mile pilots. Hyderabad’s pharma corridor fuels cold-chain fleet growth, while Chennai port expansions strengthen container connectivity. North India’s dual profile of metro density and Tier-2 expansion underpins quick-commerce experimentation beyond megacities.

Competitive Landscape

The India last-mile delivery market is characterized by moderate fragmentation, with the top five players accounting for roughly 48% of third-party parcel volume. Delhivery’s April 2025 buyout of Ecom Express granted the combined entity a 35% e-commerce share, prompting Shadowfax to raise an INR 1,907 crore (USD 202 million) IPO to bankroll automation and green fleets. Technology remains the decisive moat; Locus routing cut fuel 12-18% for adopters, while Flipkart’s AI allocation trimmed Tier-1 delivery time by 27%.

B2B specialists such as ElasticRun leverage kirana relationships to unlock unit economics unreachable for metro-centric firms. Loadshare turned profitable in December 2025 by monetizing same-day payment reconciliation, underscoring niche innovation potential. India Post’s alliance with DTDC seeks to extend private-courier SLAs into 155,000 rural outlets, though integration complexity lingers[4]India Post, “MoU with DTDC 2025,” indiapost.gov.in .

Hyperlocal newcomers remain acquisition targets for capital-rich incumbents looking for dark-store capacity and category diversification. EBITDA margins have compressed to 4-6% for pure-play logistics, giving vertically integrated e-commerce captives a cushion. Regulatory GPS and e-POD mandates favor organized fleets, hastening market exit for analog operators. Collectively, these forces forge a landscape in which scale, data, and electrification strategies dictate the trajectories of India's last-mile delivery market share.

India Last Mile Delivery Industry Leaders

Delhivery

Ecom Express

Xpressbees

Ekart Logistics

Shadowfax

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Shadowfax raised INR 1,907 crore (USD 202.1 million) in an NSE IPO to fund 18 new automated sorters and triple its EV fleet.

- January 2026: TVS Supply Chain Solutions bought Swamy & Sons 3PL for INR 88 crore (USD 9.33 million), adding 450,000 ft² and 220 vehicles in South India.

- June 2025: Competition Commission cleared Delhivery’s INR 1,407 crore (USD 149.1 million) Ecom Express acquisition, consolidating 35% e-commerce volume.

- May 2025: Celcius Logistics raised INR 250 crore (USD 26.5 million) to grow its temperature-controlled fleet to 2,800 vehicles across 450 cities.

India Last Mile Delivery Market Report Scope

| Same-day Delivery |

| Express Delivery |

| Standard Delivery |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

| E-commerce Retail |

| Fashion and Lifestyle |

| Beauty, Wellness and Personal Care |

| Home and Furniture |

| Consumer Electronics and Appliances |

| Healthcare and Medical Supplies |

| Others |

| North |

| Central |

| West |

| East |

| South |

| By Service | Same-day Delivery |

| Express Delivery | |

| Standard Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End User Industry | E-commerce Retail |

| Fashion and Lifestyle | |

| Beauty, Wellness and Personal Care | |

| Home and Furniture | |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Supplies | |

| Others | |

| By Region | North |

| Central | |

| West | |

| East | |

| South |

Key Questions Answered in the Report

What is the projected value of the India last mile delivery market by 2031?

The India last-mile delivery market size is forecast to reach USD 14.45 billion by 2031, growing at a 12.67% CAGR over 2026-2031.

Which service type is growing the fastest through 2031?

Same-day delivery is expected to register the highest CAGR of 14.32% as enterprises pay a premium for faster inventory velocity.

Which business model shows the highest growth potential?

Customer-to-consumer logistics is projected to expand at a 14.44% CAGR, driven by resale platforms and circular-economy mandates.

Which end-user segment will outpace others in growth?

Healthcare and medical supplies will grow at a 14.60% CAGR, driven by the expansion of online pharmacies and the need for biologics cold-chain requirements.

Which region is forecast to record the quickest growth in last-mile delivery?

Central India is set to post a 13.15% CAGR to 2031 as new multimodal parks in Madhya Pradesh improve inland connectivity.

Who are the leading players in India’s last-mile delivery space?

Delhivery, Ecom Express, Blue Dart, DTDC, and Xpressbees collectively account for roughly 48% of third-party parcel volume, giving them significant influence over service standards.

Page last updated on: