India Direct-to-Consumer Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

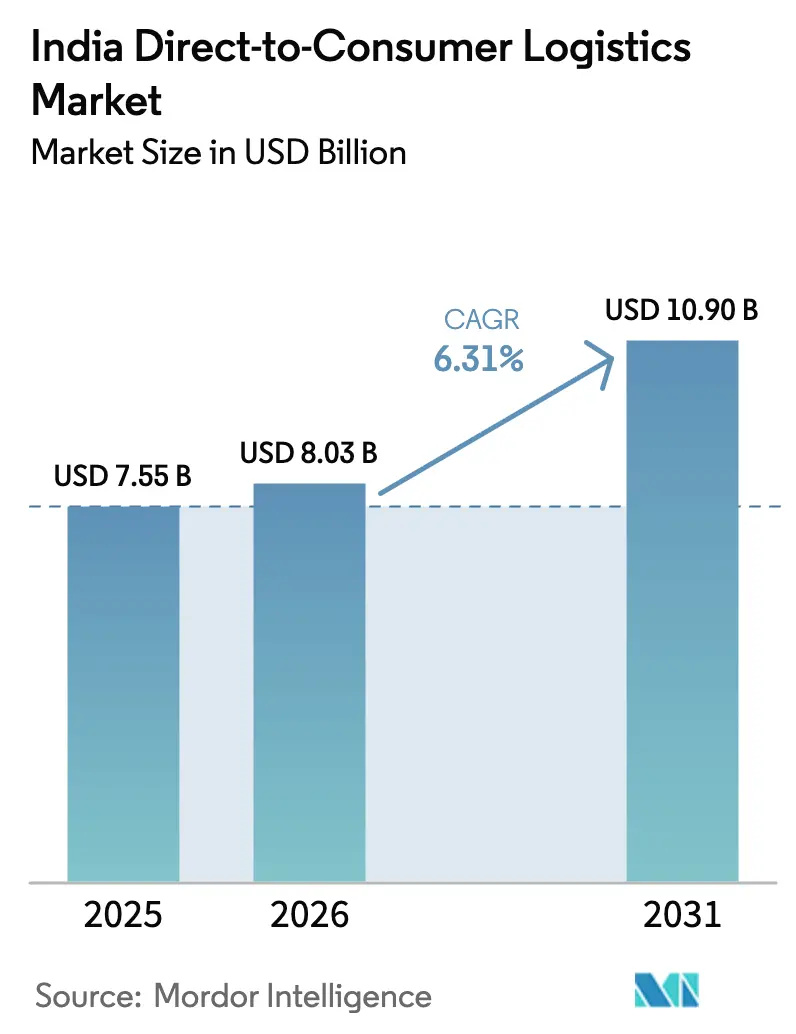

| Base Year Market Size (2025) | USD 7.55 Billion |

| Market Size (2026) | USD 8.03 Billion |

| Market Size (2031) | USD 10.9 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

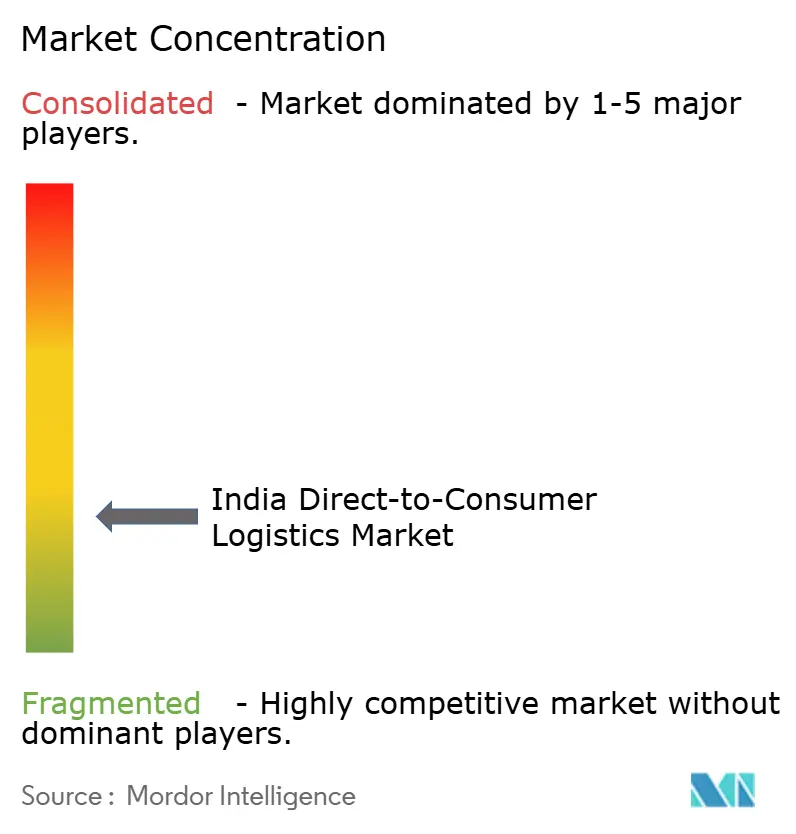

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Direct-to-Consumer Logistics Market Analysis by Mordor Intelligence

The India Direct-to-Consumer Logistics Market size was valued at USD 7.55 billion in 2025 and estimated to grow from USD 8.03 billion in 2026 to reach USD 10.9 billion by 2031, at a CAGR of 6.31% during the forecast period (2026-2031).

Solid growth rests on three pillars: the e-commerce boom, rising demand for ultra-fast fulfillment, and policy-driven cost rationalization. Transportation services remain the revenue anchor, but value-added and technology-enabled offerings record the fastest gains as shippers seek visibility, reverse-logistics support, and data-driven route planning. Quick-commerce models, though still metro-centric, create strong pull-through for dark stores, EV-based last-mile fleets, and automated sortation. Simultaneously, government programs such as the National Logistics Policy (NLP) and Unified Logistics Interface Platform (ULIP) encourage digital integration and capital spending, while the Vande Bharat parcel initiative opens express rail corridors.

Key Report Takeaways

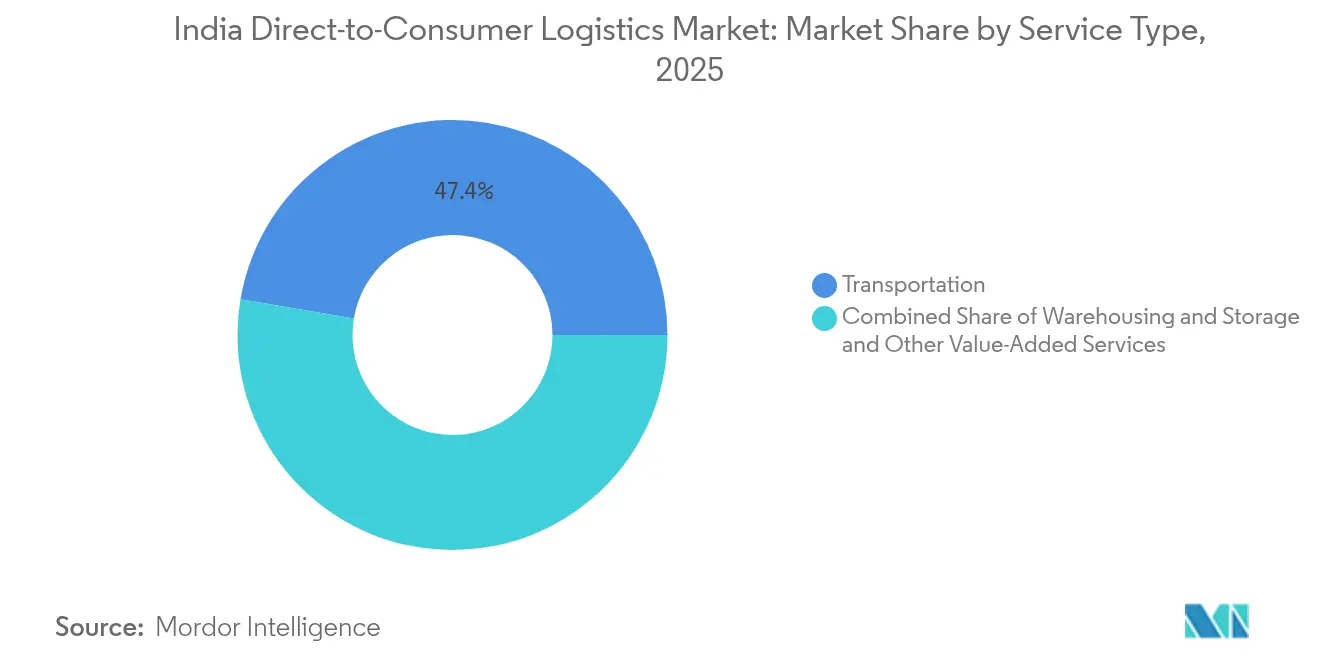

- By service type, transportation captured 47.35% of the India direct-to-consumer logistics market share in 2025, whereas value-added services are expected to post the highest projected 4.82% CAGR through 2031.

- By end user, fashion & lifestyle accounted for 31.45% of the India direct-to-consumer logistics market size in 2025 and is projected to advance at a 4.55% CAGR to 2031.

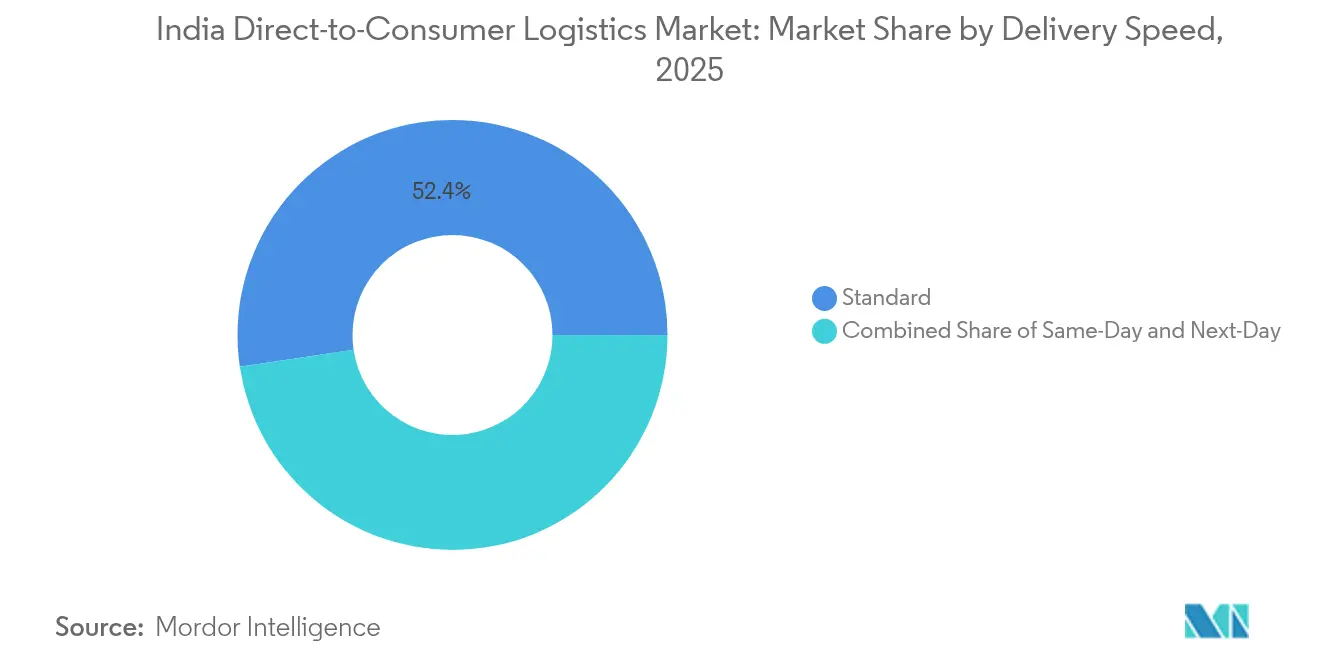

- By delivery speed, standard delivery held 52.35% of the India direct-to-consumer logistics market share in 2025, while it also leads growth at a 4.95% CAGR through 2031.

- By distribution channel, online routes generated 76.35% of the India direct-to-consumer logistics market size in 2025 and are projected to outpace overall sector growth with a 4.12% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Direct-to-Consumer Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce & digital infrastructure boom | +2.1% | National; spillover into Tier-2/3 cities | Medium term (2-4 years) |

| Rise of 10-minute quick-commerce fulfillment | +1.8% | Metros expanding toward Tier-II centers | Short term (≤ 2 years) |

| Expansion into Tier-2/3 cities via omni-channel models | +1.4% | Karnataka, Tamil Nadu, Gujarat early adopters | Long term (≥ 4 years) |

| National Logistics Policy & ONDC enablement | +0.9% | Nationwide roll-out with pilot programs | Medium term (2-4 years) |

| Vande Bharat parcel trains | +0.6% | Delhi–Mumbai and Delhi–Chennai corridors | Long term (≥ 4 years) |

| EV/bike-taxi adoption for last mile | +0.5% | Delhi-NCR leading uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce & Digital Infrastructure Boom

E-commerce payments grew 23.8% in 2024, accelerating volume inflows into parcel networks. Logistics operators responded by automating sortation; a major integrator now runs 20 such centers and handles 1.5 million parcels daily. Government-backed ULIP knits customs, port, and road databases into a single interface, trimming paperwork and enabling real-time track-and-trace. AI adoption spreads quickly: one FMCG shipper cut manual interventions by 80% after deploying predictive routing tools. Collectively, these advances lower error rates, shorten transit windows, and raise customer service benchmarks across the India direct-to-consumer logistics market.

Rise of 10-Minute Quick-Commerce Fulfillment

Quick-commerce platforms scaled annualized sales to USD 1.2 billion within 29 months, validating consumer appetite for impulse delivery. Operators expanded dark-store footprints but face mounting cash burn; a leading player spent INR 5,747 crore (USD 672 million) to earn INR 4,454 crore (USD 520 million) in FY 24, underscoring thin margins. Dense metro clusters deliver up to 85% of orders, whereas smaller cities add only 15-17% yet incur a higher cost per drop. Municipal zoning curbs dark-store density, prompting firms to refine merchandise assortments and leverage AI for sub-15-minute picking routines. Despite hurdles, investor confidence stays firm as valuations factor in eventual scale economies.

Expansion into Tier-2/3 Cities via Omni-Channel Models

More than half of one leading marketplace’s users now hail from Tier-4 towns, confirming latent demand beyond metros. Logistics providers adopt hub-and-spoke designs centered on regional fulfillment hubs, with breakeven points dropping to 800 orders per dark store in Tier-II cities versus 1,300 in Tier-I. ONDC pilots allow neighborhood kirana outlets to double as micro-fulfillment points, improving service radius while adding income streams. Government highway builds under Bharatmala enhance trunk connectivity, yet last-mile gaps linger due to limited warehousing stock and digital-payment penetration.. Customized compliance playbooks remain critical as local licensing, labor norms, and tax structures vary by state.

National Logistics Policy & ONDC Enablement

The National Logistics Policy targets halving logistics costs to 8% of GDP by 2030 through multimodal corridors, unified digitization, and skill programs. ONDC, backed by the Department for Promotion of Industry and Internal Trade, has onboarded thousands of sellers but still refines discovery algorithms after retail orders slipped during beta phases. Some ride-hailing offshoots illustrate ONDC’s potential; a Bengaluru platform captured a 25% share in its first year by crowd-sourcing drivers and bypassing aggregator mark-ups. Large 3PLs integrate ONDC APIs to access MSME traffic, with one major operator building five logistics parks aligned to the PM Gati Shakti masterplan. Standardized data formats and grievance-redressal rules under ONDC foster interoperability, although cybersecurity audits remain a work in progress.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-competitive pricing from e-tail majors & 3PLs | -1.2% | Metro clusters | Short term (≤ 2 years) |

| Infrastructure bottlenecks & supply-chain disruption | -0.8% | National; acute in Tier-2/3 | Medium term (2-4 years) |

| Quick-commerce unit-economics pressure/dark-store risk | -0.7% | High-rent urban pockets | Short term (≤ 2 years) |

| Regulatory uncertainty over gig-economy workforce | -0.4% | Karnataka spearheading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyper-Competitive Pricing from E-Tail Majors & 3PLs

Aggressive discounting compresses margins across fulfilment lanes as leading marketplaces leverage scale to negotiate sub-INR 10 per-parcel rates (USD 0.11 per parcel). Consolidation, highlighted by an INR 1,407 crore (USD 164.5 million) acquisition filing, signals the hunt for density-driven cost dilution[1]Fashion Brand Press Release, “Tier-II Expansion Milestone,” indianretailer.com. Quick-commerce apps post quarterly EBITDA losses exceeding INR 100 crore (USD 11.7 million) even after fee hikes, underscoring razor-thin unit economics. Smaller couriers, therefore, pivot toward niche verticals such as high-value electronics and healthcare to defend yields. The Competition Commission monitors tie-ups to avert monopolistic routing, yet near-term oversupply keeps spot rates volatile.

Quick-Commerce Unit-Economics Pressure/Dark-Store Risk

Dark-store growth cooled markedly after metro saturation; planned outlets for FY 26 hover at 5,000–5,500 versus earlier projections of 8,000. High real-estate rentals lift fixed costs, while sub-300 INR (USD 3.5) basket values cap contribution margins. Operators fight shrinkage by deploying real-time demand forecasts and 15-second pick protocols, but wage disputes with gig riders add complexity. Despite structural challenges, investor valuations remain robust—one brokerage pegs a top brand at USD 18.1 billion, equal to 56% of its parent’s target value—anticipating later-stage profitability pivots.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Drives Express Delivery Innovation

Transportation services controlled 47.35% of the India direct-to-consumer logistics market share in 2025. Express parcel trains, EV fleets, and automated sorters combine to slash lead times, anchoring shipper loyalty. The India direct-to-consumer logistics market size for transportation stood at USD 3.58 billion in 2025 and is forecast to post steady gains through modular fleet expansion and dynamic routing. In parallel, value-added services, though smaller, are expected to post a 4.82% CAGR (2026-2031) on the back of high-touch needs such as reverse logistics, installation, and real-time visibility dashboards.

Warehouse and storage activities evolve toward micro-hubs near consumption centers. Dark-store nodes, many under 3,000 sq ft, facilitate 10-minute fulfilment, while AI-powered inventory systems reduce stock-outs. Regulatory compliance around food safety, temperature control, and data privacy drives investment in certified facilities. Integrated service bundles now blend intercity line-haul, intra-city distribution, and freight-forwarding, further blurring traditional silos in the India direct-to-consumer logistics market.

By End User: Fashion & Lifestyle Leads Omnichannel Transformation

Fashion & lifestyle generated 31.45% of the India direct-to-consumer logistics market size in 2025, rising at a 4.55% CAGR (2026-2031) as omnichannel launches multiply seasonal drops. Quick-commerce platforms pilot premium apparel delivery within two hours, catering to impulse purchases. Brands broaden reach: one lingerie specialist derived 28% of 2024 sales from Tier-II/III towns via franchise roll-outs and D2C portals. Demand for returns management and size-exchange cycles reinforces value-added service uptake.

Consumer electronics remain sizeable due to high-value ticket sizes that justify insured, tamper-proof packaging. FMCG categories show triple-digit growth on quick-commerce rails, pushing for chilled chain nodes and continuous replenishment algorithms. Home & décor items leverage durable packaging innovations and room-of-choice delivery set-ups. Category compliance continues to diversify, with Bureau of Indian Standards codes, battery recycling mandates, and food safety rules shaping operating playbooks.

By Delivery Speed: Standard Delivery Maintains Leadership Despite Quick-Commerce Push

Standard services held 52.35% of the India direct-to-consumer logistics market share in 2025, yet are also expected to deliver the fastest 4.95% CAGR through 2031. Economies of scale in intercity trucking, plus highway projects under the National Infrastructure Pipeline, keep cost-per-parcel competitive. Predictive fleet dispatch, automated toll reconciliation, and consolidated returns allow operators to widen margins even at lower tariffs.

Same-day and next-day tiers capture metros and state capitals. About 31% of urban households now rely on same-day fulfillment for primary grocery baskets. In lower-density districts, next-day remains preferred, balancing cost and speed. Ultra-fast 10-minute sub-category deliveries continue as brand-building levers rather than profit centers, but data pooling across micro-warehouses is expected to cut last-mile kilometers over time.

By Distribution Channel: Online Dominance Accelerates Digital Transformation

Online channels delivered 76.35% of 2025 revenue and are expected to sustain a 4.12% CAGR (2026-2031) as more MSMEs migrate to marketplaces and ONDC storefronts. The India direct-to-consumer logistics market size tied to online fulfillment rose to USD 5.77 billion in 2025. Algorithmic demand shaping, dynamic pricing, and subscription-based free shipping programs deepen digital dependency. EV-based delivery pledges by large e-tailers reinforce sustainability narratives and attract conscious shoppers.

Offline players embrace click-and-collect, ship-from-store, and endless-aisle kiosks to stay relevant. Kirana partnerships unlock hyperlocal coverage, with neighborhood stores doubling as drop points. Third-party logistics firms bridge physical-digital workflows by offering SaaS control towers, API-linked returns modules, and AR-guided warehouse picking. Compliance spheres encompass GST e-invoicing, data-sharing clauses under the Digital Personal Data Protection Act 2023, and disclosure norms for delivery-time promises.

Geography Analysis

Metro corridors—Delhi-NCR, Mumbai, Bengaluru, Hyderabad, and Chennai—command 83-85% of quick-commerce gross merchandise value, reflecting dense demand clusters. Yet Tier-2/3 cities, now contributing 15-17%, grow faster owing to smartphone penetration and improving road networks. Blinkit’s footprint in 44 Tier-II cities illustrates the shift, even as lower-order density challenges cost curves.

Southern and western states emerge as logistics hot-spots. Karnataka pioneers gig-worker welfare legislation, setting precedents that could ripple nationwide. Tamil Nadu incentivizes EV adoption through reduced road tax, fostering greener fleets. Gujarat’s strategic location, coupled with port connectivity, positions it as a freight consolidation hub. Freight-only dedicated corridors boost Delhi–Mumbai speed, while eastern hinterlands benefit from multimodal terminals under Sagarmala.

Competitive Landscape

The India direct-to-consumer logistics industry features moderate fragmentation. A leading integrator covers 18,700 pin codes with automated hubs and has moved to acquire a rival for INR 1,407 crore (USD 164.5 million) to deepen density. Quick-commerce specialists focus on dark-store density; one brand boasts under-10-minute promises across 200+ micro-hubs. SaaS-native platforms such as FarEye log INR 180 crore (USD 21 million) revenue by licensing route-optimization engines to retailers and couriers.

White-space opportunities lie in intra-city B2B haulage and rural distribution. Porter’s asset-light truck-hailing app reached unicorn status while servicing SME freight tasks[3]Porter Corporate Blog, “Series E Funding Announcement,” logisticsinsider.in. ElasticRun addresses rural-kirana restocking through a hub-and-spoke aggregation model backed by USD 462 million funding. Hardware innovators like EVage develop electric trucks with 98.5% motor efficiency, aligning with fleet decarbonization mandates.

Mergers continue: CEVA bought 96% of Stellar Value Chain Solutions to secure temperature-controlled capacity. LEAP India acquired pooling firm CIPL to widen pallet rental services. The Competition Commission scrutinizes large deals to prevent monopolistic pricing, but scale synergies remain attractive as operators chase cost-to-serve reductions through automation, network overlap removal, and end-to-end offerings.

India Direct-to-Consumer Logistics Industry Leaders

Delhivery

DHL

XpressBees

Shadowfax

Mahindra Logistics Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Gati Ltd announced logistics-park projects and ONDC integration to align with PM Gati Shakti and expand direct shipper access.

- April 2025: Delhivery and Ecom Express sought Competition Commission approval for an INR 1,400 crore (USD 164 million) acquisition aimed at integrating volumes and optimizing overlapping line-haul assets.

- September 2024: DHL eCommerce unveiled a USD 260 million India plan covering aircraft additions, two hubs, and selective acquisitions to reinforce cross-border capacity.

- May 2024: Porter achieved unicorn valuation after an internal round, highlighting investor confidence in intra-city truck aggregation.

India Direct-to-Consumer Logistics Market Report Scope

D2C/Direct-to-Consumer (or Consumer-Direct) is a business model for manufacturers, retailers, or distributors to market, sell, and ship their products directly to consumers without relying on traditional brick-and-mortar storefronts or other intermediaries.

India's D2C Logistics market is segmented by end-user (fashion, consumer electronics, beauty, personal care, home decor, and other end-users). The report offers market size and forecasts for India's D2C Logistics market in value (USD) for all the above segments.

| Transportation |

| Warehousing and Storage |

| Value-added Services |

| Fashion & Lifestyle |

| Consumer Electronics |

| FMCG |

| Home & Decor |

| Others |

| Same-Day (Within 24 h) |

| Next-Day |

| Standard |

| Online |

| Offline |

| By Service Type | Transportation |

| Warehousing and Storage | |

| Value-added Services | |

| By End User | Fashion & Lifestyle |

| Consumer Electronics | |

| FMCG | |

| Home & Decor | |

| Others | |

| By Delivery Speed | Same-Day (Within 24 h) |

| Next-Day | |

| Standard | |

| By Distribution Channel | Online |

| Offline |

Key Questions Answered in the Report

How large is India’s direct-to-consumer logistics sector in 2026?

The India direct-to-consumer logistics market size is USD 8.03 billion in 2026, with a 6.31% CAGR outlook to 2031.

Which service segment generates the most revenue?

Transportation holds the lead at 47.35% share in 2025, driven by express parcel demand and network upgrades.

What end-user category grows fastest?

Fashion & lifestyle records a 4.55% CAGR through 2031, supported by omnichannel launches and impulse quick-commerce orders.

Are Tier-2 and Tier-3 cities significant for logistics growth?

Yes; they contribute 15-17% of quick-commerce GMV today and show faster growth due to improving digital infrastructure.

How are policy initiatives affecting the industry?

The National Logistics Policy, ULIP, and ONDC collectively target lower costs, digital transparency, and MSME access, reinforcing long-term efficiency gains.

Page last updated on: