Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

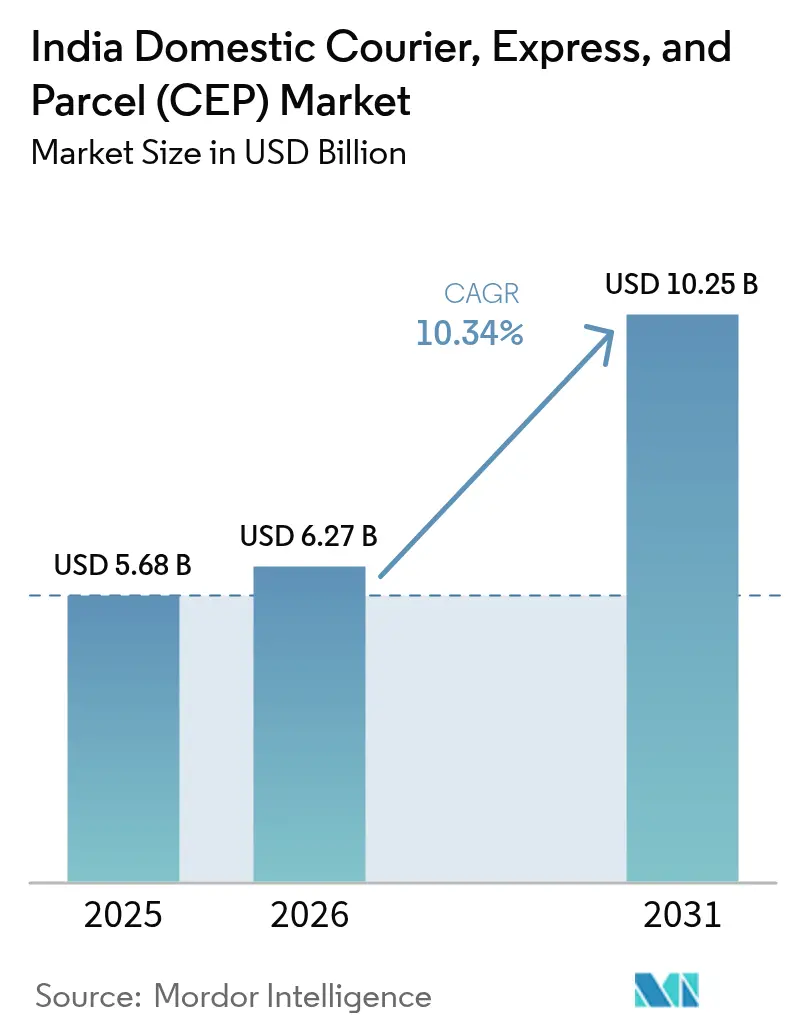

| Base Year Market Size (2025) | USD 5.68 Billion |

| Market Size (2026) | USD 6.27 Billion |

| Market Size (2031) | USD 10.25 Billion |

| Growth Rate (2026 - 2031) | 10.34% CAGR |

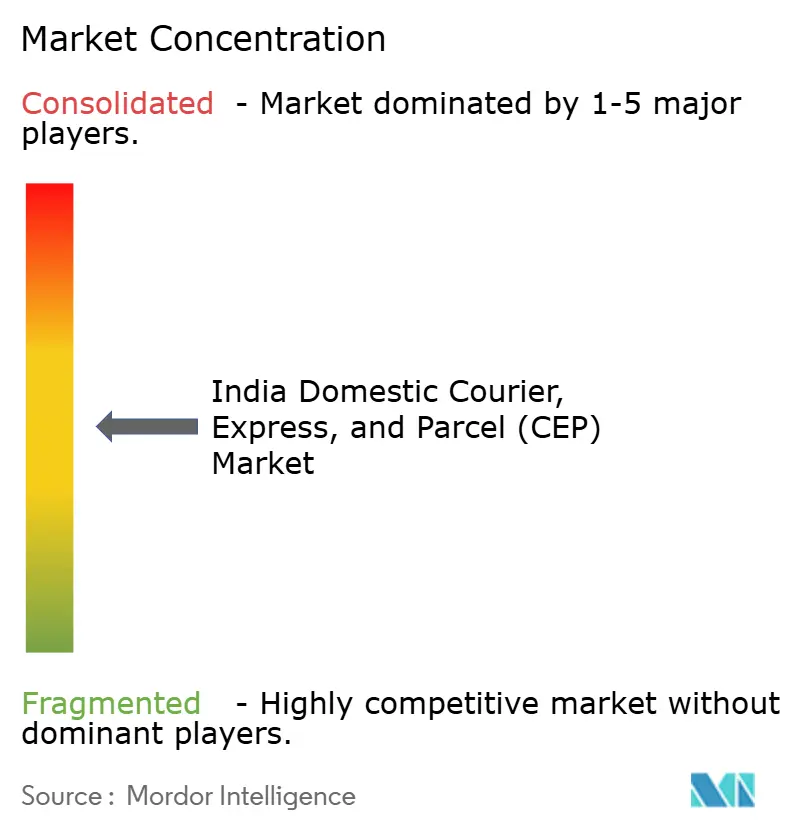

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Domestic Courier, Express, And Parcel (CEP) Market Analysis by Mordor Intelligence

The India Domestic Courier, Express, And Parcel market size in 2026 is estimated at USD 6.27 billion, growing from 2025 value of USD 5.68 billion with 2031 projections showing USD 10.25 billion, growing at 10.34% CAGR over 2026-2031.

Rapid e-commerce penetration in tier-II and tier-III cities, expansion of direct-to-consumer (D2C) brands, and sustained government investment in logistics corridors collectively accelerate parcel volumes and reshape service expectations across the India domestic courier market. Technology adoption—from automated sorters to AI-based route optimization—has lowered sector logistics costs from 16% to nearly 10% of GDP, though the figure still trails global benchmarks and leaves ample headroom for efficiency-driven players in the India domestic courier market. Express services, air cargo capacity additions, and hyperlocal fulfillment networks further strengthen competitive intensity as consumers increasingly view same-day or next-day delivery as the norm in the India domestic courier market. Consolidation momentum favors well-funded operators that can scale automation investments quickly, while smaller courier firms face margin pressure in an ecosystem that prizes data visibility, speed, and service consistency.

Key Report Takeaways

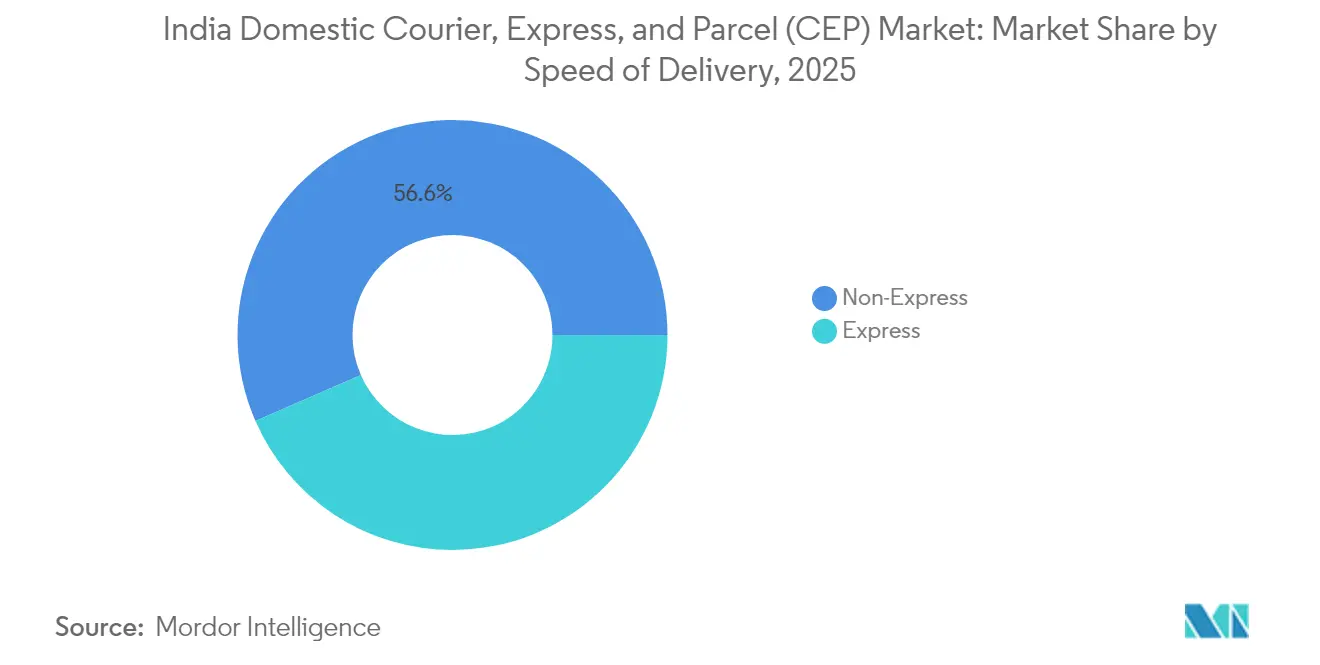

- By speed of delivery, non-express services held 56.55% of the India domestic courier market share in 2025, whereas express services are forecast to expand at an 11.07% CAGR through 2031.

- By shipment weight, light packages accounted for 71.91% share of the India domestic courier market size in 2025, with light-weight consignments advancing at a 10.63% CAGR through 2031.

- By end-user industry, manufacturing led with 32.62% revenue share in 2025; e-commerce is projected to record the highest CAGR at 11.26% to 2031.

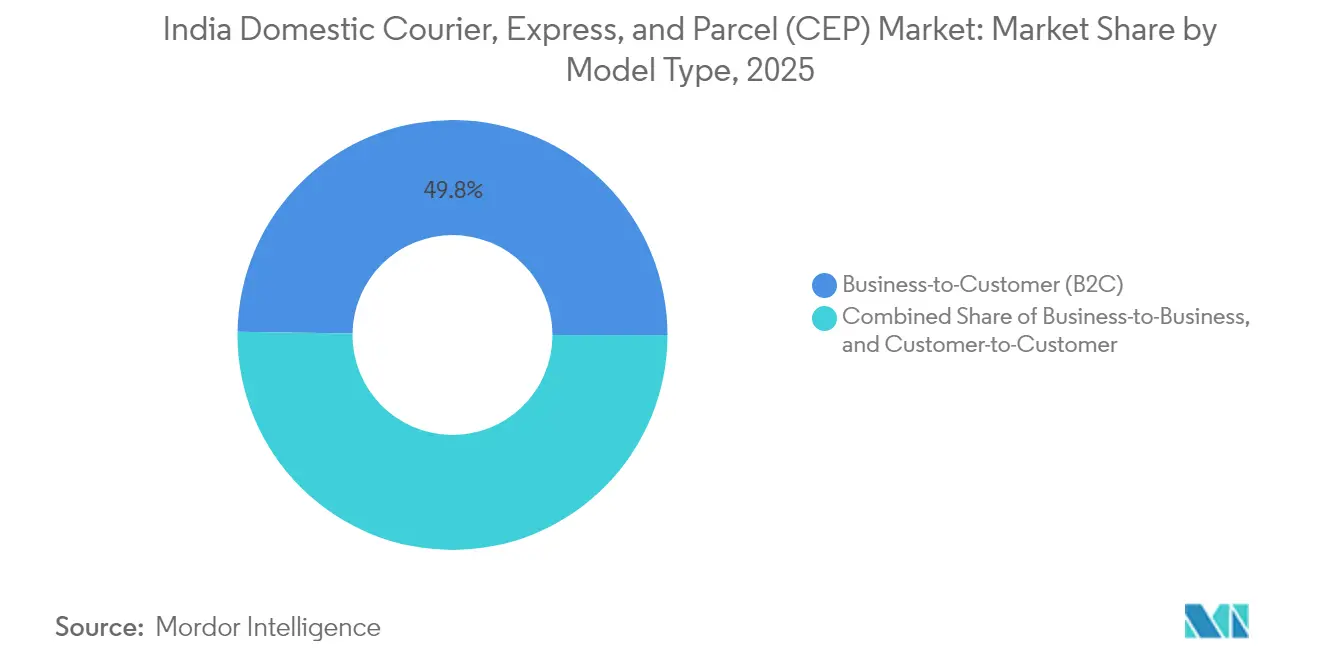

- By model, the B2C segment commanded 49.76% share of the India domestic courier market size in 2025 and is poised to accelerate at a 12.33% CAGR between 2026-2031.

- By mode of transport, road captured 70.27% of the India domestic courier market share in 2025, while air cargo is anticipated to grow at a 10.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Domestic Courier, Express, And Parcel (CEP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and tier-II/III penetration | +2.8% | National, with concentrated gains in tier-II/III cities | Medium term (2-4 years) |

| National Logistics Policy and infra push | +2.1% | National, with early gains in freight corridors and metro connectivity | Long term (≥ 4 years) |

| Warehouse Automation Surge and Foreign Direct Investment Inflows | +1.9% | Metro cities and industrial hubs, expanding to tier-II cities | Medium term (2-4 years) |

| Consumer Demand for Same or Next-Day Delivery | +2.3% | Urban centers, expanding to tier-II cities | Short term (≤ 2 years) |

| D2C brands' shift to B2B parcels | +1.2% | National, concentrated in manufacturing and consumer goods hubs | Medium term (2-4 years) |

| ONDC Open-Network Enablement | +0.8% | National, with stronger impact in smaller cities and rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom and tier-II/III penetration

The India domestic courier market experiences a parcel-volume multiplier as tier-II and tier-III locations now generate more than 60% of new online shoppers. Smartphone affordability and ubiquitous UPI payments compress the digital adoption lifecycle, leading to order frequencies in smaller cities that mirror metro norms within two years of onboarding. Quick-commerce platforms collectively operate in 92 non-metro cities, yet lower order densities—350 parcels per day versus 1,100 in metros—pressure delivery economics. Government programs such as BharatNet and Digital India supply the connectivity backbone that lowers entry barriers for couriers. As a result, branded parcel networks race to establish spoke facilities closer to emerging demand pockets, stimulating job creation and intensifying intra-regional competition across the India domestic courier market[1]“India’s Quick-Commerce Boom Built a Very Expensive Speed Trap,” India Dispatch, indiadispatch.com.

National Logistics Policy and infrastructure push

A unified logistics vision aims to compress sector costs toward an 8–9% share of GDP through multimodal corridor development and 100 planned multimodal logistics parks. Dedicated freight corridors and the Unified Logistics Interface Platform promise a 15–20% cut in paperwork, bolstering transparency and throughput across the India domestic courier market. Capital expenditure of INR 11.2 trillion in FY 26, including INR 1.5 trillion in interest-free state loans, accelerates road, rail, and port upgrades that shrink transit times. The Eastern Dedicated Freight Corridor completion and expansion of 120 regional airports under the UDAN scheme widen modal choice, making it economical to blend air and surface legs for time-sensitive parcels. Enhanced knotting of metro spokes with hinterland hubs is expected to unlock latent rural consumption, lifting CAGR projections by an additional 2.1 percentage points[2]“The Future of Logistics: Startup Landscape in India,” Messe Stuttgart India & EAC Consulting, eac-consulting.de.

Warehouse automation surge and FDI inflows

As labor costs edge higher and accuracy targets tighten, couriers escalate investments in automated guided vehicles, high-speed sorters, and AI-enabled inventory platforms. India drew a record USD 1.1 billion in logistics startup funding during 2014-2023, with 44% of such firms headquartered in tier-II and tier-III cities—evidence of geographic democratization of innovation. Ecom Express earmarked INR 2.35 billion for sorter automation in its IPO filing, signalling sector-wide movement toward lights-out facilities. Cloud migration goals—such as Allcargo targeting 80% of workloads on cloud create real-time visibility that drives higher truckfill rates and better asset returns.

Consumer demand for same- or next-day delivery

Quicker fulfillment commands premium willingness to pay, transforming express delivery from an optional service into an expected baseline in leading metros. Quick-commerce operators collectively manage about 4,000 dark stores, compelling courier partners to adapt to micro-fulfillment models that rely on precise demand forecasts and narrow delivery windows. The India domestic courier market answers by deploying predictive positioning algorithms that pre-stage inventory near consumption hot-spots. Yet economics remain tight in non-metro zones where order density rarely supports sub-15-minute targets. Emerging 10-minute delivery pilots pressure networks to re-architect last-mile fleets, blending two-wheeler riders, electric vans, and parcel lockers to protect margins without compromising speed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics cost-to-GDP and fragmentation | -1.8% | National, with acute impact in rural and remote areas | Long term (≥ 4 years) |

| Rural infrastructure gaps | -1.4% | Rural areas and tier-III cities, affecting last-mile connectivity | Long term (≥ 4 years) |

| Gig-worker attrition | -1.1% | Urban centers and metro cities, with spillover to tier-II cities | Short term (≤ 2 years) |

| Platform in-house delivery bias | -0.9% | National, concentrated in e-commerce hubs and major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High logistics cost-to-GDP and fragmentation

Operational fragmentation persists, with 90% of logistics firms in the unorganized bracket and 67% operating fleets of fewer than five trucks. This structure limits economies of scale, hinders technology uptake, and raises per-shipment costs in the India domestic courier market. State-specific regulatory nuances despite GST create duplicate compliance layers that erode margins. Inconsistent addressing standards cause delivery reroutes and elevate last-mile expenses, while poor modal integration restricts network optimization. Collectively, these inefficiencies subtract roughly 1.8 percentage points from projected market CAGR[3]“Shadowfax to File IPO Papers Under Confidential Route,” The Economic Times, economictimes.indiatimes.com.

Rural infrastructure gaps

Last-mile delivery into rural zones often costs up to 25% more than urban equivalents because of sub-par road quality and dispersed demand nodes. Only 35–40% of warehousing meets Grade-A benchmarks, restricting deployment of automated sorting solutions that could offset higher transport costs. Monsoon-linked disruptions raise trucking rates by as much as 15%, undercutting service reliability during peak agricultural seasons. Cash-on-delivery remains prevalent owing to digital-payment limitations in many villages, inflating working-capital needs and extending reconciliation cycles for courier operators in the India domestic courier market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Speed of Delivery: Express momentum outpaces legacy bulk shipping

Express consignments climbed at an 11.07% CAGR through 2031 as urban consumers normalized same-day and next-day fulfillment, a trend that elevated premium parcel demand within the India domestic courier market size. Quick-commerce platforms account for a growing share of express volumes after collectively opening more than 4,000 dark stores that promise 10- to 30-minute delivery windows in primary metros. Non-express options remain dominant at 56.55% share, especially for B2B manufacturing shipments where cost efficiency outweighs rapidity.

Advanced route-optimization engines and predictive loading enable couriers to lower cost per express parcel, narrowing the historical pricing gap with non-express services. Shadowfax reports operational profitability even with hyperlocal deliveries comprising nearly 30% of its traffic, underscoring technology’s role in defending margins. Nevertheless, lower order densities in tier-II and tier-III cities extend express windows to 15-60 minutes, prompting asset-light models that leverage partner fleets for flexibility across the India domestic courier market.

By Shipment Weight: Light parcels anchor e-commerce expansion

Light-weight shipments captured 71.91% of the India domestic courier market share in 2025, fueled by mobile-first shopping behaviors that generate frequent low-value orders rather than bulk purchases. Pricing models based on dimensional weight encourage couriers to refine packaging algorithms that minimize box volume and reduce air cargo surcharges.

Sustainability considerations add complexity as regulators push for recyclable materials, leading firms to pilot compostable pouches and reusable totes in top cities. Uber’s Courier XL, which transports parcels up to 750 kg in 3- and 4-wheeler vehicles, illustrates a parallel push into heavier segments aimed at balancing vehicle utilization across the India domestic courier market.

By End User Industry: Manufacturing scale meets e-commerce velocity

Manufacturing held 32.62% of total value in 2025, reflecting India’s ascent as a global production hub that demands synchronized inbound and outbound logistics. The India domestic courier market size for manufacturing couriers benefits from industrial corridor upgrades that compress factory-to-port lead times.

E-commerce, however, grows fastest at 11.26% CAGR through 2031 as rural online adoption accelerates; smaller ticket sizes and higher return rates require integrated reverse logistics capabilities. Allcargo’s focus on MSME clusters underscores a strategy that bridges manufacturing and e-retail, enabling hybrid B2B-B2C flows that optimize truckload factors.

By Model: B2C dominance reshapes service playbooks

B2C deliveries led with 49.76% share in 2025 and are forecast to grow at a 12.33% CAGR as D2C brands shortcut traditional retail chains, deepening parcel density in residential neighborhoods. Greater consumer scrutiny of tracking accuracy drives couriers to provide live ETAs, real-time driver communication, and frictionless returns—capabilities that require robust digital cores across the India domestic courier market.

B2B shipments sustain volume heft in industrial belts but expand modestly because supply-chain re-engineering stresses efficiency rather than scale. C2C parcels rise on the back of peer-to-peer resale platforms, pushing couriers to experiment with automated drop-boxes and parcel lockers in gated communities to contain costs without sacrificing convenience.

By Mode of Transport: Road backbone faces strategic airlift expansion

Road transport retained 70.27% share thanks to network redundancy and the flexibility to tap even remote PIN codes within the India domestic courier market. Bharatmala highway expansion and a gradual shift toward electric delivery vans promise lower per-kilometer costs and reduced carbon footprints over the medium term.

Air cargo, while smaller, posts a 10.72% CAGR as newer regional airports under the UDAN scheme boost coverage and give couriers speed options for high-value electronics, fashion, and pharmaceutical products. DHL’s addition of eight aircraft for intra-India loops indicates that time-critical freight warrants dedicated lift capacity. Rail and waterways remain niche due to network gaps and handling constraints, though multimodal trials linked to dedicated freight corridors could unlock specialized opportunities.

Geography Analysis

India’s eight largest metros—Mumbai, Delhi NCR, Bangalore, Chennai, Hyderabad, Pune, Kolkata, and Ahmedabad—collectively generate roughly 83-85% of quick-commerce sales, anchoring the majority of parcel flows within the India domestic courier market. Government infrastructure programs such as PM Gati Shakti aim to knit these metros to tier-II and tier-III cities via freight corridors, multimodal parks, and logistic clusters that promise shorter lead times and lower cost variability.

Tier-II growth hubs—including Surat, Jaipur, Lucknow, Coimbatore, and Indore—record faster parcel-volume upticks than metros, supported by rising disposable incomes, broadband penetration, and local startup ecosystems. Ecom Express now serves 27,000 PIN codes covering 97% of India’s population, signaling that near-comprehensive coverage is no longer the preserve of India Post alone. Manufacturing corridors in Gujarat, Tamil Nadu, and Maharashtra remain B2B strongholds, while tech centers in Karnataka and Telangana tilt toward B2C volumes.

The Northeast, though infrastructure-challenged, gains visibility as new road projects and the Act East Policy deepen trade links with Southeast Asia. Rural markets in Uttar Pradesh, Bihar, and West Bengal carry vast untapped potential but demand tailored logistics strategies—smaller drop-sizes, cash-on-delivery reliability, and localized customer support—to overcome lower average order values and patchy road quality. Partnership models that piggyback on India Post’s rural depot network present a scalable route to penetrate villages without inflating fixed-cost bases across the India domestic courier market.

Competitive Landscape

The India domestic courier market sits at a moderate concentration level, where unicorn-backed operators such as Delhivery, Shadowfax, and XpressBees leverage venture capital to scale nationwide automation footprints, while legacy brands—India Post, Blue Dart, DTDC—capitalize on entrenched infrastructure. Competitive energy revolves around last-mile efficiency; route-optimization algorithms, AI-driven demand forecasting, and parcel locker rollouts determine service reliability and cost leadership.

Strategic differentiation increasingly narrows to vertical specialties. Shadowfax focuses on quick-commerce and hyperlocal payloads; Allcargo Gati designs solutions for MSME clusters; Safexpress positions around temperature-controlled consignments. High capex requirements for automated hubs spur consolidation as smaller courier firms cede share or pivot to niche services rather than chase volume leadership in the India domestic courier market.

Regulatory clarity under GST incentivizes formalization, pushing unorganized players either to adopt digital compliance tools or exit. Allcargo’s cloud-first blueprint—targeting 80% workload migration—demonstrates how technology amortization across multiple businesses can unlock data synergies, faster reconciliation, and sharper dynamic pricing. Market entrants now require both capital depth and differentiated software stacks to win contracts with large e-commerce marketplaces that increasingly favor SLA-driven scorecards.

India Domestic Courier, Express, And Parcel (CEP) Industry Leaders

India Post

Blue Dart Express Ltd

Delhivery Ltd

DHL Express (India) Pvt Ltd

FedEx Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Shadowfax filed for an INR 2,000–2,500 million IPO to finance quick-commerce expansion while maintaining profitability.

- May 2025: Uber introduced Courier XL in Delhi NCR and Mumbai, extending service to 3- and 4-wheeler vehicles for loads up to 750 kg.

- April 2025: India Post rolled out “Gyan Post,” a trackable service aimed at the academic publishing sector.

- January 2025: India Post launched the Independent Delivery Centre program to build 1,850 specialized facilities that enable Sunday deliveries and extended hours.

India Domestic Courier, Express, And Parcel (CEP) Market Report Scope

Courier, express, and parcel (CEP) refer to the collection of services that involves the delivery of various goods and products through different mediums such as air, water, and land across regions. These packages delivered by CEP are mainly non-palletized and collectively weigh around a hundred pounds.

The India Domestic Courier, Express, and Parcel (CEP) Market is segmented by business model (Business-to-Business [B2B], Business-to-Customer [B2C], customer-to-customer [C2C]), type (E-commerce and Non-e-commerce), and end-user (Service, Wholesale and Retail Trade, Healthcare, Industrial Manufacturing, and other end-users). The report offers the market size and forecasts in value (USD billion) for all the above segments.

By Speed of Delivery

| Express |

| Non-Express |

By Shipment Weight

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

By End User Industry

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

By Model

| Business-to-Business (B2B) |

| Business-to-Customer (B2C) |

| Customer-to-Customer (C2C) |

By Mode of Transport

| Road |

| Air |

| Others |

| By Speed of Delivery | Express |

| Non-Express | |

| By Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| By End User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| By Model | Business-to-Business (B2B) |

| Business-to-Customer (B2C) | |

| Customer-to-Customer (C2C) | |

| By Mode of Transport | Road |

| Air | |

| Others |

Key Questions Answered in the Report

How large is the India domestic courier market in 2026?

The India domestic courier market size is USD 6.27 billion in 2026, and it is projected to reach USD 10.25 billion by 2031.

What is the forecast CAGR for India’s courier sector?

The market is expected to grow at a 10.34% CAGR between 2026 and 2031.

Which segment holds the largest share by shipment weight?

Light-weight parcels dominate with 71.91% share, reflecting the surge in e-commerce orders.

Why are express services growing faster than non-express?

Same-day and next-day delivery expectations, quick-commerce expansion, and air-cargo network upgrades boost express-service demand at an 11.07% CAGR.

How is government policy influencing the sector?

The National Logistics Policy and PM Gati Shakti program aim to trim logistics costs, build multimodal corridors, and digitize documentation, thereby unlocking efficiency across parcel networks.

Which business model is expanding the quickest?

B2C deliveries grow fastest at a 12.33% CAGR, driven by D2C brands and social-commerce adoption that deepen residential parcel density.

Page last updated on: