India Contract Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

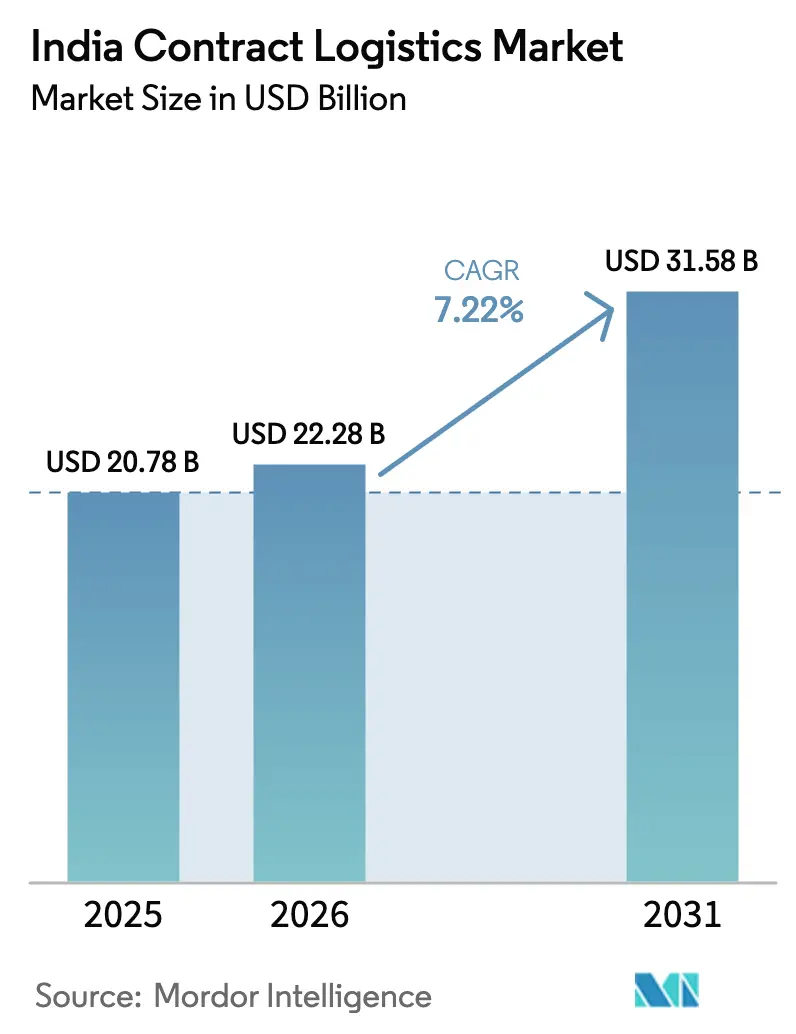

| Base Year Market Size (2025) | USD 20.78 Billion |

| Market Size (2026) | USD 22.28 Billion |

| Market Size (2031) | USD 31.58 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

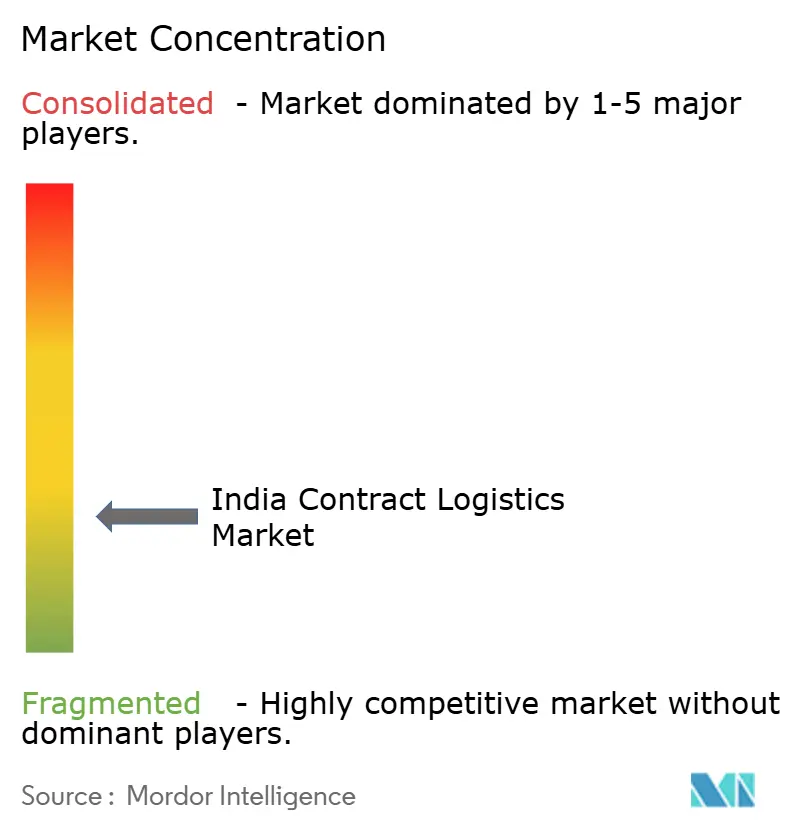

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Contract Logistics Market Analysis by Mordor Intelligence

The India Contract Logistics Market size was valued at USD 20.78 billion in 2025 and estimated to grow from USD 22.28 billion in 2026 to reach USD 31.58 billion by 2031, at a CAGR of 7.22% during the forecast period (2026-2031).

Volume growth aligns with lower logistics costs, which fell to 10% of GDP on the back of expressway build-outs, FASTag-enabled tolling, and policy-driven modal shifts. Demand accelerators include the PM Gati Shakti Master Plan, the National Logistics Policy, and surging e-commerce penetration that now spans tier-II and III cities. Competitive pressure is moderate, with full-service providers strengthening digital control towers while quick-commerce specialists pursue hyperlocal micro-warehousing. Bottlenecks revolve around skilled warehouse labor shortages, high automation CAPEX, and cybersecurity risks, yet sustained policy support and post-GST network consolidation continue to unlock profitability levers for scale players.

Key Report Takeaways

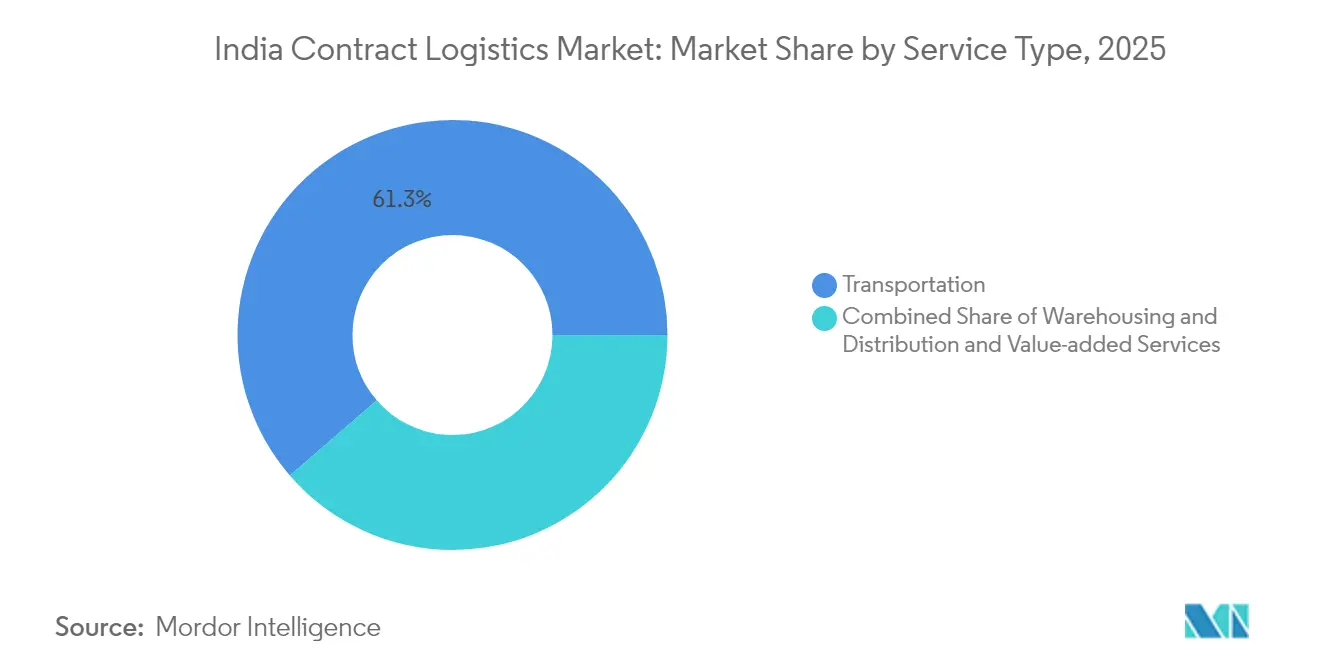

- By service type, transportation services commanded 61.34% of the India contract logistics market share in 2025. Value-added services are forecast to expand at a 6.18% CAGR to 2031.

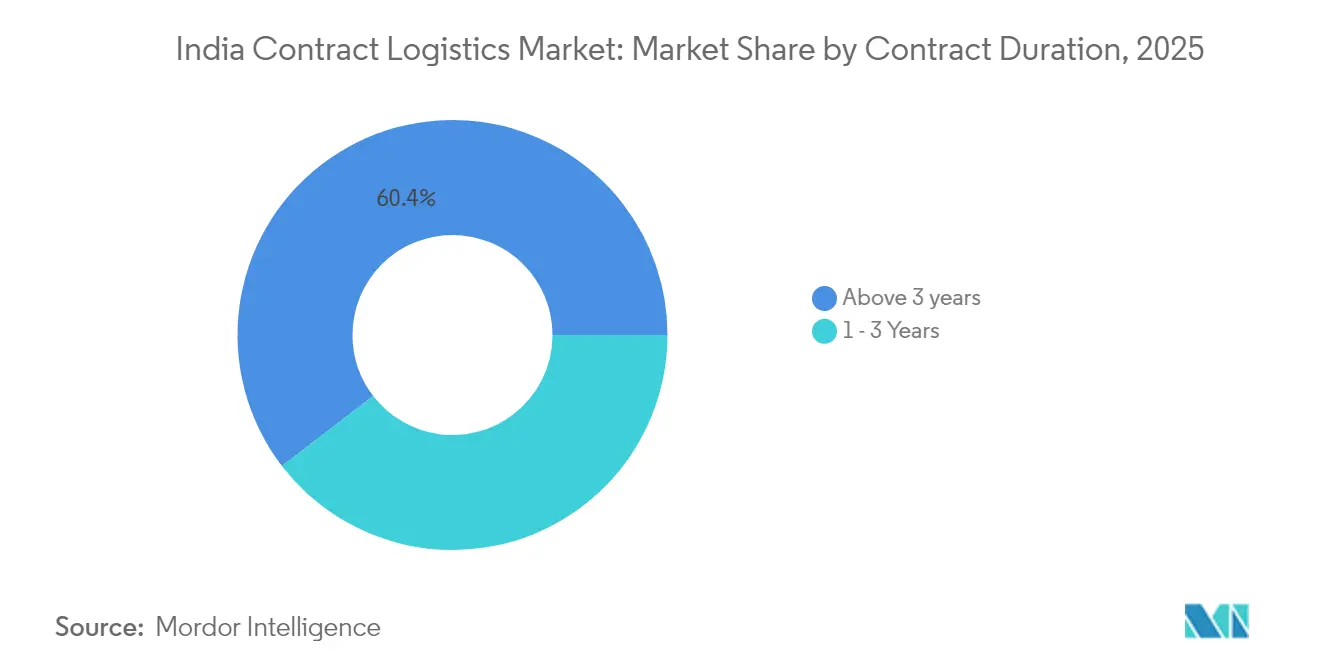

- By contract duration, agreements above 3 years held a 60.42% share of the India contract logistics market size in 2025 and are projected to grow at a 5.98% CAGR through 2031.

- By end-user, retail and e-commerce led with 26.55% revenue share in 2025; healthcare and pharmaceuticals is advancing at a 6.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce & omni-channel retail | +1.8% | National; tier-I expanding to tier-II/III | Medium term (2-4 years) |

| Government infrastructure push (NLP, Gati-Shakti) | +1.5% | National; priority corridors in industrial belts | Long term (≥ 4 years) |

| Rising 3PL outsourcing by manufacturers | +1.2% | Manufacturing hubs in Gujarat, Maharashtra, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Post-GST network consolidation benefits | +0.9% | National; hub optimization in key metros | Short term (≤ 2 years) |

| Tier-II/III hyper-local dark-store boom | +0.8% | Emerging cities such as Pune, Ahmedabad, Kochi, Indore | Medium term (2-4 years) |

| CLaaS demand from D2C & quick-commerce brands | +0.7% | Urban centers with high consumer density | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in e-commerce & omni-channel retail

E-commerce volumes continue to double-digit climb, with online grocery alone tracking toward INR 2.1 lakh crore (USD 24.6 billion) by 2027. More than 4,000 dark stores now dot major metros, and network densification is migrating into tier-II and III clusters where last-mile costs remain elevated. Retailers adopting omni-channel models require synchronized inventory and reverse-logistics flows, prompting 3PLs to deploy micro-fulfillment sites within 2–3 km of customers. The India contract logistics market thus pivots toward dynamic routing software and on-demand capacity to uphold sub-30-minute delivery promises. As organized retail penetration is expected to reach 60% by 2028, integrated service providers that combine B2B replenishment with direct-to-consumer fulfillment gain a competitive edge.

Government infrastructure push (NLP, Gati-Shakti)

The PM Gati Shakti platform has onboarded 44 central ministries, mapping 200+ projects to a single GIS interface to accelerate multimodal corridor execution[1]Press Information Bureau, “PM GatiShakti National Master Plan,” pib.gov.in. Expressway mileage, dedicated freight corridors, and logistics parks receive synchronized clearances, shrinking cross-state transit at erstwhile choke points. The Unified Logistics Interface Platform unifies shipment visibility across ports, railways, and road transport, trimming documentation time that earlier inflated travel duration by 60%. While land acquisition delays persist, standardized asset specifications and digital permits are steadily lifting asset utilization rates for fleet owners and warehouse operators within the India contract logistics market.

Rising 3PL outsourcing by manufacturers

Post-pandemic cost rationalization has nudged manufacturers to outsource non-core logistics. Electronics, pharmaceuticals, and automotive firms tapping Production-Linked Incentives demand Grade-A warehouses with over 10,000-pallet capacity and IoT-enabled material-handling equipment. End-to-end visibility platforms allow real-time SKU tracking, enabling vendors to cut buffer stock days. Integrated providers offering kitting, sub-assembly, and reverse logistics unlock efficiency gains that widen adoption of long-tenure 3PL contracts in the India contract logistics market.

Post-GST network consolidation benefits

Unified GST replaced state-wise tax optimization with demand-driven network design, letting shippers shutter redundant depots and cluster inventory into mega-hubs. Large retailers and steel producers have trimmed logistics outlay by up to 20% and rerouted goods through multimodal corridors radiating from seven metros. E-Way Bills and FASTag reduce dwell times, elevating fleet turns across the India contract logistics market, although residual state-level compliance gaps still curb seamless flow in select corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled warehouse & SCM labor shortage | −1.4% | National; acute in metros and industrial belts | Long term (≥ 4 years) |

| High CAPEX for Grade-A automation | −1.1% | Tier-I cities and industrial corridors | Medium term (2-4 years) |

| Inter-state compliance frictions post-GST | −0.8% | Border states with sector-specific clearances | Short term (≤ 2 years) |

| Cyber-security risks to digital control towers | −0.6% | Cloud-centric logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled warehouse & SCM labour shortage

Only 5% of India’s 150 million blue-collar workforce is formally trained, resulting in chronic shortages for forklift operators, inventory analysts, and robotics technicians[2]“India's Blue-Collar Workers Paradox,” Foundamental, foundamental.com. Employers in manufacturing hubs extend overtime and boost wages to secure talent, inflating operating costs for the India contract logistics market. Automation alleviates repetitive tasks yet raises demand for specialized maintenance roles, reinforcing the training imperative.

High CAPEX for Grade-A automation

Automated storage and retrieval systems cut picking time but carry a steep upfront investment. Clad-rack designs offset civil costs; nonetheless, IoT sensors, AGVs, and WMS licenses push payback periods beyond five years in several tier-II zones. Financing hurdles slow warehouse modernization, constraining service scalability in the India contract logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Road Transport Dominance Drives Automation

Transportation services stood at 61.34% of the India contract logistics market in 2025, with road fleets carrying the bulk of e-commerce and FMCG loads despite rail corridor gains. Value-added services represent the swiftest trajectory, registering a 6.18% CAGR through 2031. The segment benefits from manufacturers outsourcing kitting and labeling to 3PLs equipped with handheld scanners and AI slotting engines. Blue Dart’s Delhi hub, capable of processing 550,000 parcels daily via automated sorters, typifies the shift toward high-throughput nodes.

Warehousing and distribution thrive on GST-driven depot consolidation, lifting large-box Grade-A stock across Mumbai, NCR, and Bengaluru. Modal mix diversification progresses as dedicated freight corridors attract bulk cargo, yet road retains primacy for last-mile flexibility. Tech adoption across service types accelerates; Allcargo Gati introduced machine-learning-guided handheld printers to shave mis-sort errors and boost on-time performance within the India contract logistics market.

By Contract Duration: Long-term Partnerships Strengthen

Contracts exceeding three years captured a 60.42% share in 2025, reflecting shippers’ willingness to lock in capacity and jointly amortize automation investments. Long-tenure deals enable providers to plan robotics rollouts and solar rooftop retrofits that improve energy efficiency. Manufacturers tied to Production-Linked Incentive schemes value stable 3PL alliances that support lean inventories and synchronized replenishments.

One-to-three-year contracts retain relevance for seasonal product launches and pilot dark-store deployments, but the capital intensity of Grade-A assets inclines both parties toward multiyear engagements. Delhivery’s roadmap to adjusted-EBITDA breakeven hinges on such extended agreements, which anchor network utilization in the India contract logistics market.

By End-user Industry: Healthcare Acceleration Outpaces Retail Leadership

Retail and e-commerce preserved 26.55% of 2025 revenue, yet healthcare and pharmaceuticals climb fastest at a 6.63% CAGR through 2031. Pharma’s forecast to hit USD 130 billion by 2030 necessitates GDP-compliant cold chains, serialization, and batch-level traceability. Snowman Logistics scales temperature-controlled space to meet vaccine and biologics flows, mirroring affluent household growth that pushes protein consumption and specialty drug demand.

Automotive, food and beverage, and chemicals sectors contribute steady volumes requiring hazardous-goods handling, returnable packaging, and strict shelf-life adherence. These nuanced requirements spur specialized sub-segments, reinforcing the versatility imperative for operators in the India contract logistics market.

Geography Analysis

Mumbai and the National Capital Region jointly house more than half of India’s Grade-A warehousing stock, underscoring the west-north axis concentration. Western corridors benefit from JNPT port connectivity and dedicated freight corridors funneling cargo toward consumption hubs. Maharashtra alone contributes a sizable slice of industrial GDP, attracting multi-client facilities with cross-dock efficiencies.

Southern clusters, led by Bengaluru and Chennai, leverage electronics and automotive exports; new logistics parks in Chennai integrate rail sidings to cut first-mile drayage. Andhra Pradesh’s deep-sea ports add coastal-shipping options that diversify modal choices within the India contract logistics market.

Northern India capitalizes on population density; Blue Dart’s Bijwasan hub near Indira Gandhi International Airport offers air-road interoperability to speed inbound and outbound e-commerce flows.

Competitive Landscape

The India contract logistics market exhibits moderate fragmentation. Top domestic providers—Delhivery, Allcargo Logistics, and Transport Corporation of India—combine with global multinationals such as Deutsche Post DHL and FedEx to form a diverse service spectrum. Scale players invest heavily in robotics and data lakes; Allcargo Gati recently integrated machine-learning route planners, while Blue Dart’s solar-powered sorting plant reduces carbon footprint. Private-equity inflows, which captured 66% of logistics capital deployment in H1 2024, fund both consolidation and technology pilots.

Quick-commerce entrants intensify hyperlocal competition by promising sub-20-minute deliveries through dense dark-store grids. Start-ups such as CargoFL raise capital for AI-driven platforms serving SMB shippers. Healthcare cold chain and CLaaS modules represent white spaces where specialized certifications offer defensible niches. Compliance proficiency under GST remains a moat for established players, yet cybersecurity posture differentiates best-in-class providers as control-tower digitization deepens within the India contract logistics market.

M&A momentum continues: Delhivery’s planned USD 169 million purchase of Ecom Express signals volume aggregation for network density, pending regulatory nod. CEVA’s acquisition of Stellar Value Chain Solutions underscores foreign interest in local assets. Competitive intensity will hinge on technology resale models, geographic coverage, and ability to service regulated industries at scale.

India Contract Logistics Industry Leaders

Allcargo Logistics Ltd

TVS Supply Chain Solutions

Transport Corporation of India (TCI)

Mahindra Logistics Ltd

Delhivery Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Delhivery announced the acquisition of Ecom Express for INR 1,407 crore (USD 169 million), subject to Competition Commission approval.

- January 2025: Blue Dart opened a 250,000 sq ft integrated hub in Delhi capable of sorting 550,000 parcels daily using automated conveyors.

- January 2025: FedEx launched FedEx Surround in India, delivering real-time shipment visibility powered by AI analytics.

- September 2024: DHL eCommerce earmarked USD 260 million to expand its aircraft fleet and build two hubs by 2030, reinforcing long-haul capacity.

India Contract Logistics Market Report Scope

Contract logistics refers to a long-term partnership that includes a variety of services, from the transportation of goods or replacement parts to the delivery of goods to the final client. The service offerings of contract logistics include the following: warehouses, personnel, appropriate equipment, stock management, dispatch follow-up, and after-sales service, among others. A complete background analysis of the India Contract Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

India's Contract Logistics Market is segmented By Type (Outsourced and Insourced), By End User (Manufacturing and Automotive, Consumer Goods and Retail, High-Tech, Healthcare, and Pharmaceuticals, and Other End Users(Energy, Construction, Aerospace, etc.)). The report offers market size and forecasts in values (USD billion) for all the above segments.

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing & Distribution | |

| Value-added Services (Assembly, Labelling, Kitting) |

| 1 – 3 Years |

| Above 3 years |

| Manufacturing & Automotive |

| Food & Beverage |

| Retail & E-commerce |

| Healthcare & Pharmaceuticals |

| Chemicals |

| Other Industries |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing & Distribution | ||

| Value-added Services (Assembly, Labelling, Kitting) | ||

| By Contract Duration | 1 – 3 Years | |

| Above 3 years | ||

| By End-user Industry | Manufacturing & Automotive | |

| Food & Beverage | ||

| Retail & E-commerce | ||

| Healthcare & Pharmaceuticals | ||

| Chemicals | ||

| Other Industries |

Key Questions Answered in the Report

What is the projected value of the India Contract Logistics Market in 2031?

The market is projected to reach USD 31.58 billion by 2031.

Which service type currently dominates Indian contract logistics?

Transportation services lead, holding 61.34% share in 2025.

Which end-user vertical is expected to grow the fastest?

Healthcare and pharmaceuticals, with a forecast 6.63% CAGR through 2031.

How does the National Logistics Policy influence contract logistics?

It lowers logistics costs via unified digital systems and multimodal infrastructure, boosting 3PL efficiency.

Why are long-term contracts preferred by shippers?

They allow amortization of automation investments and ensure stable capacity amid supply chain volatility.

Page last updated on: