Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

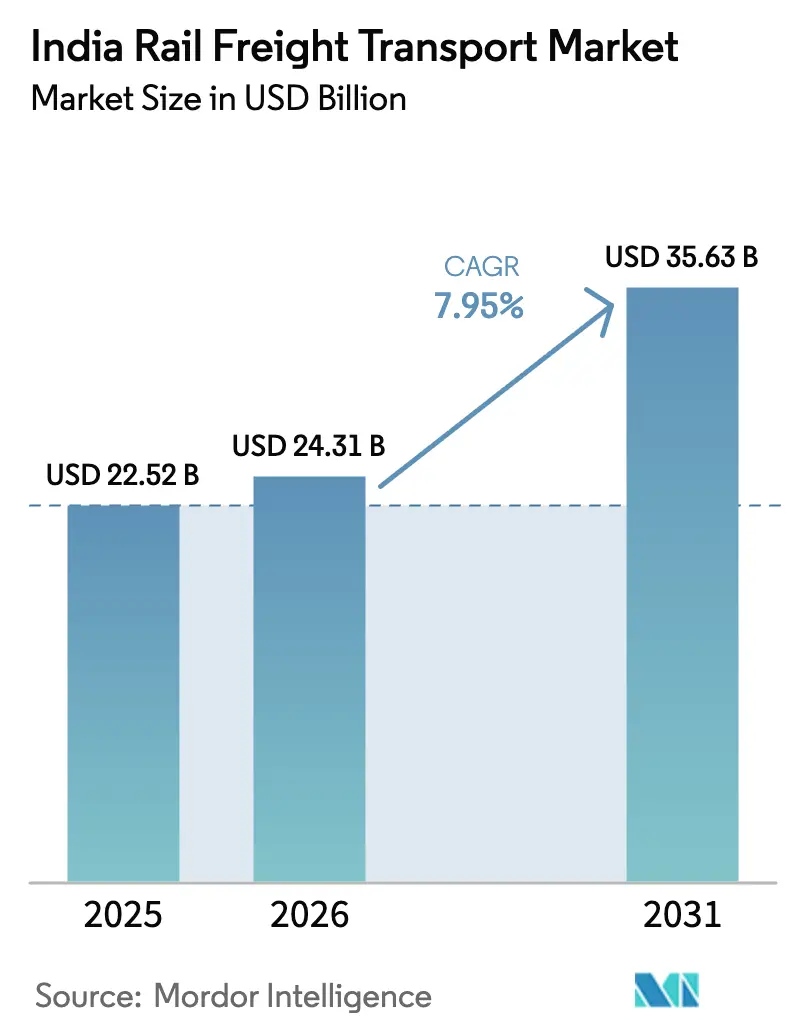

| Base Year Market Size (2025) | USD 22.52 Billion |

| Market Size (2026) | USD 24.31 Billion |

| Market Size (2031) | USD 35.63 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

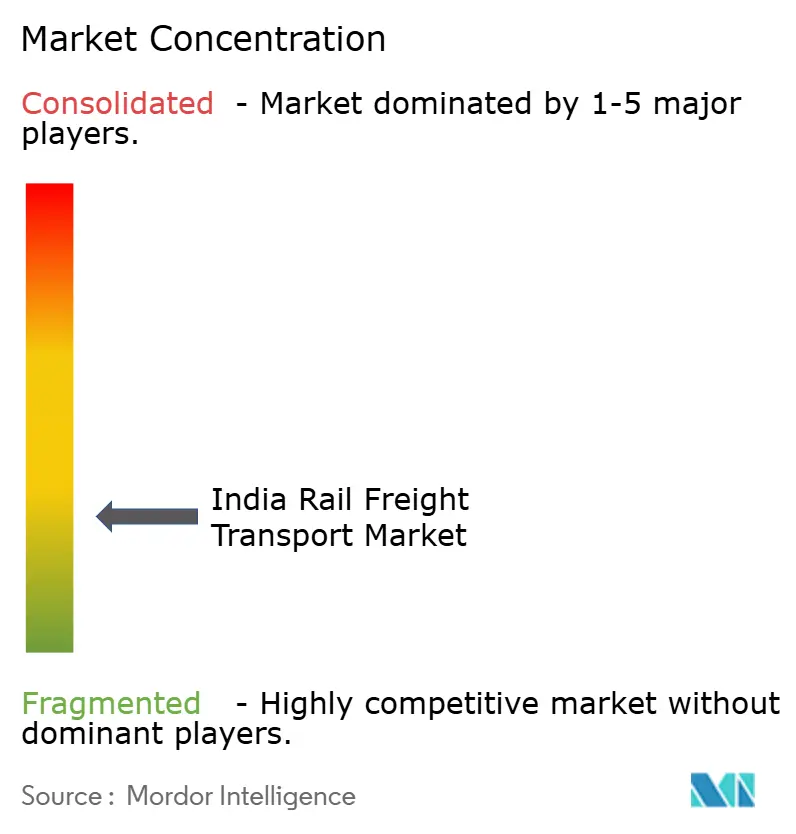

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Rail Freight Transport Market Analysis by Mordor Intelligence

The India Rail Freight Transport Market size is expected to grow from USD 22.52 billion in 2025 to USD 24.31 billion in 2026 and is forecast to reach USD 35.63 billion by 2031 at 7.95% CAGR over 2026-2031.

The surge reflects the public goal of lifting rail’s freight modal share to 45% by 2030, a target that is driving unprecedented capital spending, network electrification, and pricing reforms through the new Rail Tariff Authority. Dedicated Freight Corridors, which already carry more than 10% of national freight volumes, now run trains at 60 km/h—well above the legacy network’s 25 km/h—thereby shrinking transit times and slashing shipper costs. The PM Gati Shakti digital platform further accelerates project approvals, while 98% network electrification reduces diesel exposure and improves service reliability. Growing e-commerce alliances with Amazon and others underscore a decisive pivot from coal toward containerized cargo, and new multimodal logistics parks worth USD 24.10 billion promise integrated rail-road-port solutions that cut logistics expenses and emissions.

Key Report Takeaways

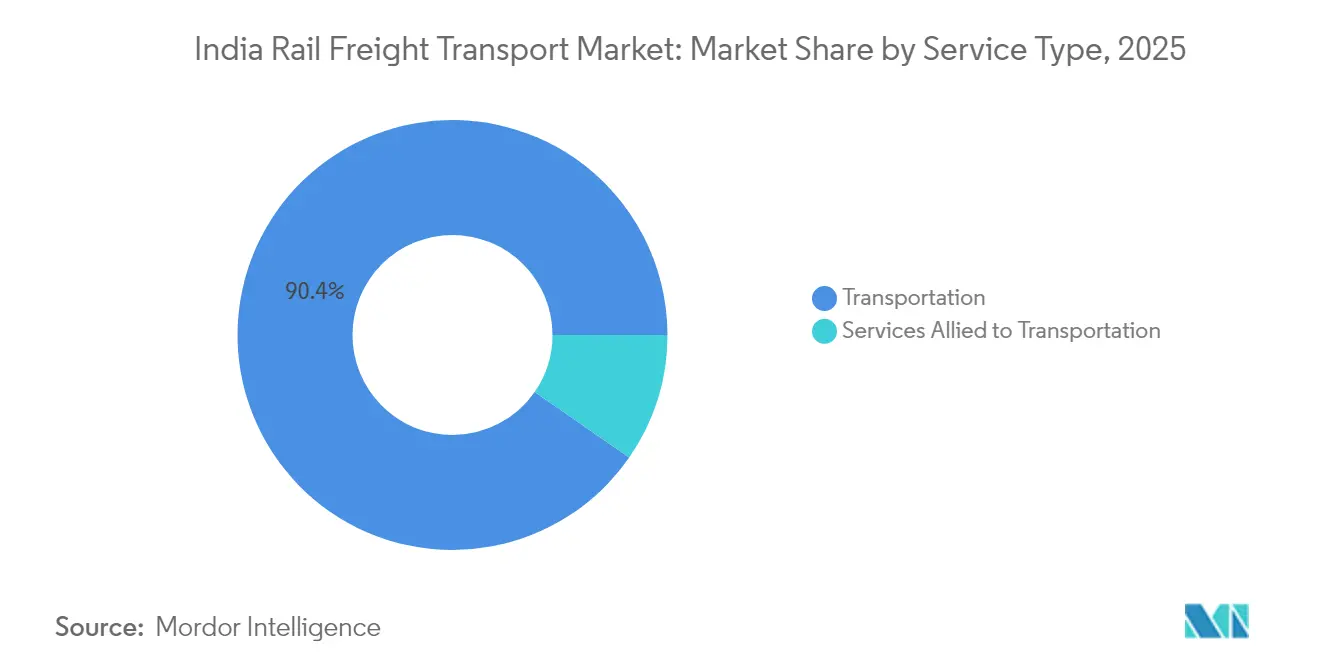

- By service type, transportation services held 90.35% of the India rail freight transport market share in 2025, whereas services allied to transportation are projected to post a 6.05% CAGR through 2031.

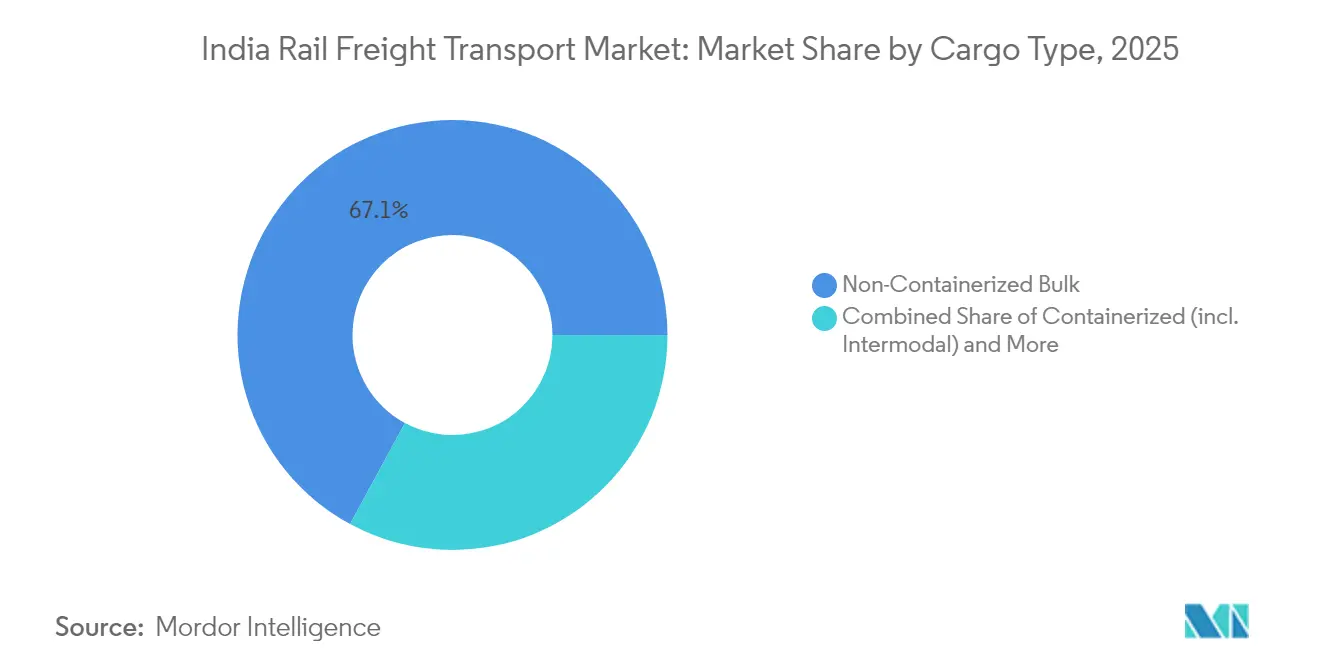

- By cargo type, non-containerized bulk commanded 67.10% of the India rail freight transport market size in 2025, while containerized freight is set to expand at a 6.28% CAGR to 2031.

- By destination, domestic operations captured 91.25% of the India rail freight transport market share in 2025, whereas international freight is forecast to climb at a 5.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Rail Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dedicated freight-corridors coming online | +2.1% | National, concentrated in Delhi-Mumbai and Ludhiana-Sonnagar routes | Medium term (2-4 years) |

| National Logistics Policy & Gati Shakti push | +1.8% | National, with early gains in major industrial corridors | Long term (≥ 4 years) |

| Rapid coal-to-container mix diversification | +1.5% | National, particularly benefiting western and southern regions | Long term (≥ 4 years) |

| Rail-linked industrial corridors and MMLPs | +1.3% | Regional, focused on industrial clusters and port connectivity | Medium term (2-4 years) |

| AFTO scheme boosting finished-vehicle moves | +0.9% | National, with concentration in automotive manufacturing hubs | Short term (≤ 2 years) |

| Dynamic km-based pricing pilots | +0.6% | National, with initial focus on competitive route segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dedicated Freight Corridors Coming Online

The nearly complete Eastern and Western Dedicated Freight Corridors now handle 391 freight trains per day, allow double-stack containers, and raise average speeds to 60 km/h, cutting Delhi–Mumbai transit time by half. With the Vaitarna–JNPT stretch due by December 2025, exporters gain a seamless rail path to India’s busiest container port. Economic modeling by Indian Railways estimates USD 1.93 billion in annual savings from lower fuel use and reduced inventory dwell. Encouraged by these gains, detailed studies for three new corridors—East Coast, East-West, and North-South—have been submitted, with the World Bank and JICA expressing funding interest.

National Logistics Policy & Gati Shakti Push

The Gati Shakti geospatial portal fuses datasets from 44 ministries and every state, trimming rail project approval cycles to weeks instead of months. Rail track construction increased to 14 km per day in FY 2023, yielding 5,423 km of new lines. Forty-eight cargo terminals are live and 91 more are in advanced stages, accelerating the policy goal of driving logistics costs below 10% of GDP by 2030. Rail planners now synchronize siding locations, road links, and port access within a single workflow, eliminating historical hand-offs that stalled projects[1]Ministry of Railways, "Dedicated Freight Corridor Implementation Status Report," dfccil.com.

Rapid Coal-to-Container Mix Diversification

Coal still produced 45% of tonnage in 2024, but revenue focus is shifting to higher-margin container traffic. The Automobile Freight Train Operator scheme moved 1 million cars last year, up from 1% of output a decade ago. Amazon alone leapt from one train in 2019 to more than 120 dedicated runs in 2025, exploiting the Western Corridor to guarantee next-day delivery between Delhi and Mumbai. Double-decker cargo coaches that carry parcels above passenger seating illustrate rail’s pursuit of premium, time-sensitive freight.

Rail-Linked Industrial Corridors and MMLPs

Thirty-five multimodal logistics parks, backed by USD 24.10 billion, are slated to process half of India’s freight by 2030 while cutting transport costs 10% and CO₂ emissions 12%. The flagship Chennai park, built on 184 acres, couples a four-lane highway spur with an on-site rail siding that can handle 7.17 million t annually. Private groups such as Reliance and Allcargo are investing in sidings, inland depots, and container terminals, signaling confidence in an integrated rail-centric logistics model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Network congestion on golden quadrilateral | -2.2% | National, concentrated on Delhi-Mumbai, Delhi-Howrah, Mumbai-Chennai routes | Short term (≤ 2 years) |

| Road-freight cost advantage < 500 km hauls | -1.4% | National, particularly affecting regional and short-haul freight segments | Medium term (2-4 years) |

| Wagons idle-time due to first/last-mile gaps | -1.1% | National, with acute impact on port connectivity and industrial sidings | Medium term (2-4 years) |

| Dependence on coal (> 45%) exposes volumes | -0.8% | National, concentrated in eastern coal belt and power generation corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Network Congestion on Golden Quadrilateral

The golden quadrilateral corridors move 70% of national freight on just 25% of track, leading to 115–150% capacity utilization and average freight speeds below 25 km/h. Mixed passenger-freight operations force long signal blocks and yard holds, eroding schedule reliability. The government has sanctioned 155 line additions and 235 doubling projects, but commissioning lags mean congestion will persist in the near term. Until DFC bypasses are fully operational, shippers of time-sensitive cargo still shift to trucks for certainty.

Road-Freight Cost Advantage < 500 km Hauls

For distances under 500 km, door-to-door trucking stays cheaper because it avoids first- and last-mile drayage plus terminal handling. Rail’s base rate of INR 1.36 (~USD 0.016) per t-km inflates once siding fees and minimum-distance rules apply. Idle wagons at terminals average 20 hours, compounding opportunity cost. Without faster mechanized unloading and better road links to industrial estates, rail cannot fully challenge the flexibility small manufacturers enjoy with trucks

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates Revenue Generation

Transportation services accounted for 90.35% of the India rail freight transport market share in 2025 as Indian Railways shifted 1.4 billion t of cargo over its 68,103 km network. Revenue remains shipment-led, yet services allied to transportation—terminal handling, warehousing, and documentation—are poised for a 6.05% CAGR to 2031, reflecting shippers’ preference for turnkey solutions. Private cargo-terminal developers operating under the Gati Shakti framework have already commissioned 97 facilities that each generate USD 12.05 million of annual revenue without revenue-sharing obligations to Indian Railways. The India rail freight transport market size for allied services is set to expand further as e-commerce and FMCG shippers demand integrated storage, labeling, and reverse-logistics options within rail terminals.

Allied services growth is accelerated by policy changes permitting 100% foreign ownership in terminal infrastructure. DHL, Maersk, and Reliance are piloting temperature-controlled storage at railheads to attract pharmaceuticals and perishables, cargo traditionally hauled by road. As these value-added offerings mature, the India rail freight transport market is expected to witness a progressive shift in revenue mix, although pure play transportation will still hold the lion’s share through 2031.

By Cargo Type: Containerization Drives Future Growth

Non-containerized bulk loads such as coal, iron ore, and cement held a 67.10% share of the India rail freight transport market size in 2025, underscoring the railway’s legacy role in moving energy and industrial commodities. However, containerized freight will outpace all other categories at a 6.28% CAGR to 2031, lifted by DFC double-stack capability and automated inland container depots. The India rail freight transport market share for containers is bolstered by Amazon, Flipkart, and manufacturing exporters that prize predictable lead times. Indian Railways’ “truck-on-train’’ program on the Western Corridor now shifts 250 trucks daily onto flat-wagons, reducing carbon emissions and repositioning empty trucks faster.

Liquid bulk remains a niche but critical segment, where specialized tank wagons support petroleum and chemical supply chains. Policy incentives for bio-fuels and green hydrogen could introduce new liquid cargo flows, broadening the commodity mix. As container penetration deepens, asset utilization of flat-cars will rise, elevating yields and diversifying rail’s revenue beyond coal.

By Destination: Domestic Operations Anchor Market Foundation

Domestic traffic captured 91.25% of the India rail freight transport market share in 2025, mirroring the sheer size of India’s internal demand. Coal deliveries from Odisha and Jharkhand to powerplants nationwide, iron-ore runs to steel mills, and hinterland port shuttles constitute core lanes. Despite dominant domestic volumes, international (EXIM) rail is forecast to log a 5.96% CAGR to 2031 as new cross-border routes mature. The India rail freight transport market size for EXIM traffic is rising through the revived Haldibari–Chilahati link with Bangladesh, now exchanging 20 freight trains monthly.

Regional partners see the line as a gateway for Bhutanese and Nepalese trade, while the upcoming Agartala–Akhaura rail will cut Northeast-to-Chattogram transit by two-thirds. Looking west, India’s participation in the Trans-Caspian International Transport Route promises land-bridge access to Europe once the Rasht–Astara rail in Iran completes. These corridors could gradually lift rail’s share in India’s USD 770 billion merchandise trade, offering exporters a viable alternative to congested ocean routes.

Geography Analysis

Domestic operations dominate the 68,103 km India rail network, which lifted 1.4 billion t in 2024, with bulk movements from mineral-rich east-central states to industrial belts in the north and west. The Eastern DFC, running Ludhiana to Sonnagar, relieves the saturated Delhi–Howrah trunk and gives steelmakers a faster path to ports. The Western DFC links JNPT to Dadri, creating a high-speed spine for finished goods, auto parts, and refrigerated cargo destined for consumption centers. Together, both corridors now handle more than 10% of national freight while operating at much higher speeds.

Regional disparities shape flows: the golden quadrilateral—Delhi, Mumbai, Chennai, Kolkata—moves 70% of freight on a quarter of track length, reflecting concentrated industrial output and import-export activity. Western India enjoys port proximity and container depots, making it the fastest adopter of rail-road multimodal solutions. Eastern India relies on coal but faces exposure to the energy transition, prompting diversification into steel and container flows as DFC connectivity matures. Northern transit lanes also benefit cross-border trade with Bangladesh, where monthly train exchanges climb steadily.

International rail freight, currently 8.75% of volumes, grows on the Bangladesh and Nepal gateways. The restored Haldibari–Chilahati corridor trims Kolkata–Dhaka cargo time to one day, spurring garment and FMCG trade. Future plans envisage linking to Central Asia via Iran’s Rasht–Astara segment, promising sub-15-day transit to Europe under the International North-South Transport Corridor. As these projects move ahead, exporters of engineering goods and perishables will find rail increasingly viable for global deliveries, reinforcing the India rail freight transport market’s strategic latitude.

Competitive Landscape

The market remains moderately fragmented, with Indian Railways owning track and rolling stock, yet policy shifts invite private investment in terminals, rakes, and allied services. Gati Shakti Cargo Terminals permit 100% private capital and no revenue sharing, luring over 90 investors that each earn about USD 12.05 million per site. This trend chips away at the traditional state monopoly and seeds competitive service models anchored in speed, transparency, and niche cargo specialization. Container Corporation of India and Adani Logistics leverage port loyalties to scale rail-linked depots, challenging each other on transit guarantees and value-added warehousing.

Technology is the newest battleground. Indian Railways’ Kavach safety system now equips 1,548 route km, enabling higher speeds and reducing accidents, while Wabtec’s Evolution locomotives roll out of the Marhowra plant for both domestic service and planned exports to Africa. Wagon manufacturers are consolidating: Texmaco’s USD 615 million buyout of Jindal Rail Infrastructure makes it the top wagon producer, anticipating a boom from missions to triple freight tonnage by FY 2027. Global suppliers partner with local yards to meet rising demand for aluminum hopper cars and bi-level auto carriers[3]Competition Commission of India, "Market Structure Analysis of Indian Railways Sector," cci.gov.in.

New entrants exploit digital channels. Amazon charters entire container trains, using predictive analytics to sync warehouse inventory with rail schedules. Start-ups provide SaaS platforms for real-time wagon tracking, temperature monitoring, and carbon-footprint reporting, giving rail an edge with ESG-minded clients. As these niches scale, competition shifts from haulage price to total-cost-of-ownership, with reliability, visibility, and emissions data emerging as decisive factors in modal choice.

India Rail Freight Transport Industry Leaders

-

Indian Railways

-

Container Corporation of India (CONCOR)

-

Adani Logistics Ltd

-

Gateway Rail Freight Ltd

-

OM Logistics Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Indian Railways produced 1,681 locomotives in FY 2024-25, up 19%, reinforcing domestic capacity.

- March 2025: Network electrification reached 98% of broad-gauge track, saving 3.6 billion USD in diesel imports since 2023.

- February 2025: Dedicated Freight Corridor averaged 391 trains daily in January, maintaining throughput during the Maha-Kumbh Mela.

- January 2025: Indian Railways partnered with Ramakrishna Forgings and Titagarh Rail for forged wheels, targeting 80,000 units annually.

India Rail Freight Transport Market Report Scope

From a point of loading or a goods station to a point of unloading, goods are transported by rail. These products, such as coal, building supplies, iron, and steel, are frequently large and heavy. Along with the transportation of large items, the rail freight market also offers this service. Service providers provide value-added services and logistics. Loading and documentation, unloading, services, and packaging are a few of them. A complete background analysis of the India Rail Freight Transport Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The India Rail Freight Transport Market is Segmented by Cargo Type (Containerized (Intermodal), Non-containerized, and Liquid Bulk), Destination (Domestic and International) and Service Type (Transportation and Services Allied to Transportation). The report offers market size and forecasts for India Rail Freight Transport Market in value ( USD Billion ) for all the above segments.

By Service

| Transportation |

| Services Allied to Transportation |

By Cargo Type

| Containerized (incl. Intermodal) |

| Non-containerized / Bulk |

| Liquid Bulk |

By Destination

| Domestic |

| International (EXIM) |

| By Service | Transportation |

| Services Allied to Transportation | |

| By Cargo Type | Containerized (incl. Intermodal) |

| Non-containerized / Bulk | |

| Liquid Bulk | |

| By Destination | Domestic |

| International (EXIM) |

Key Questions Answered in the Report

How large is the India rail freight transport market in 2026?

It is valued at USD 24.31 billion and is projected to reach USD 35.63 billion by 2031.

What CAGR is expected for rail freight in India through 2031?

The market is anticipated to grow at a 7.95% CAGR during 2026-2031.

Which cargo segment is growing fastest on Indian Railways?

Containerized freight is forecast to expand at a 6.28% CAGR thanks to e-commerce and DFC connectivity.

How much of India’s rail freight remains coal-based?

Coal still accounts for about 45% of tonnage, although its share is gradually declining.

What role do Dedicated Freight Corridors play?

The Eastern and Western corridors already carry over 10% of national freight and cut transit times by half, boosting rail competitiveness.

Are private companies allowed to run rail terminals?

Yes, Gati Shakti Cargo Terminal policies permit 100% private investment with no revenue sharing, attracting more than 90 operators so far.

Page last updated on: