India Intra-city Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 33.5 Billion |

| Market Size (2026) | USD 34.93 Billion |

| Market Size (2031) | USD 43.06 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

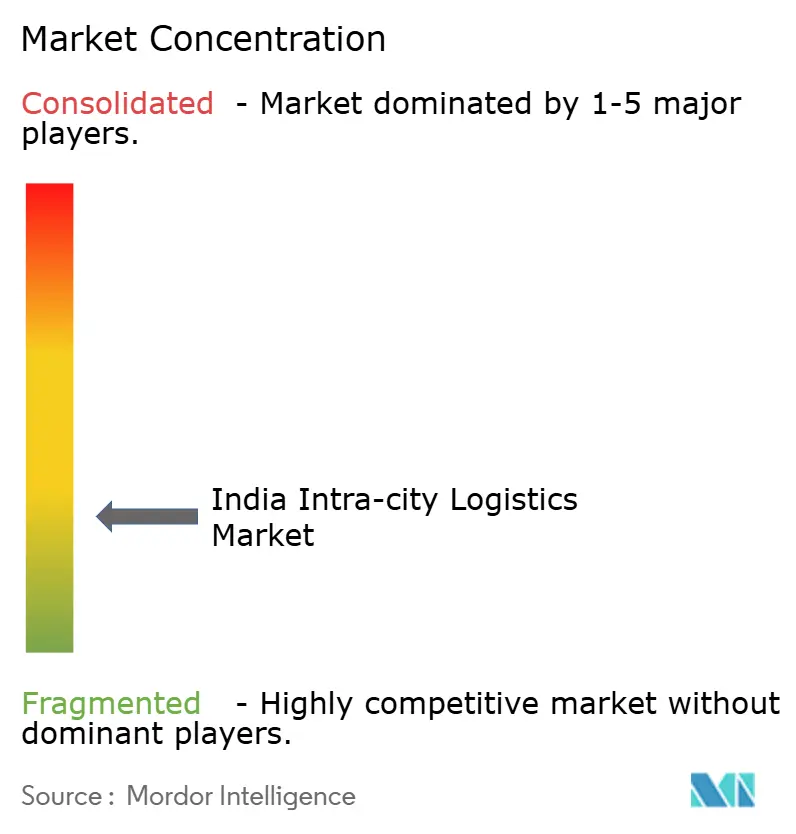

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Intra-city Logistics Market Analysis by Mordor Intelligence

The India Intra-city Logistics Market size in 2026 is estimated at USD 34.93 billion, growing from 2025 value of USD 33.5 billion with 2031 projections showing USD 43.06 billion, growing at 4.26% CAGR over 2026-2031.

Increased e-commerce volumes, government infrastructure programs, and rapid technology adoption underpin this growth, although urban congestion and a fragmented small-fleet operator base continue to pressure margins. Transportation services remain the revenue cornerstone, quick-commerce drives demand for same-day delivery, and policy initiatives such as PM-Gati Shakti are steering investment toward multimodal networks that connect urban nodes more efficiently. Tier-1 metros still dominate activity, but Tier-3 cities are scaling faster on the back of retail digitalization, prompting operators to diversify their geographic footprints. Consolidation, reflected in acquisitions like Delhivery’s purchase of Ecom Express, signals a shift toward integrated platforms able to provide end-to-end urban fulfillment.

Key Report Takeaways

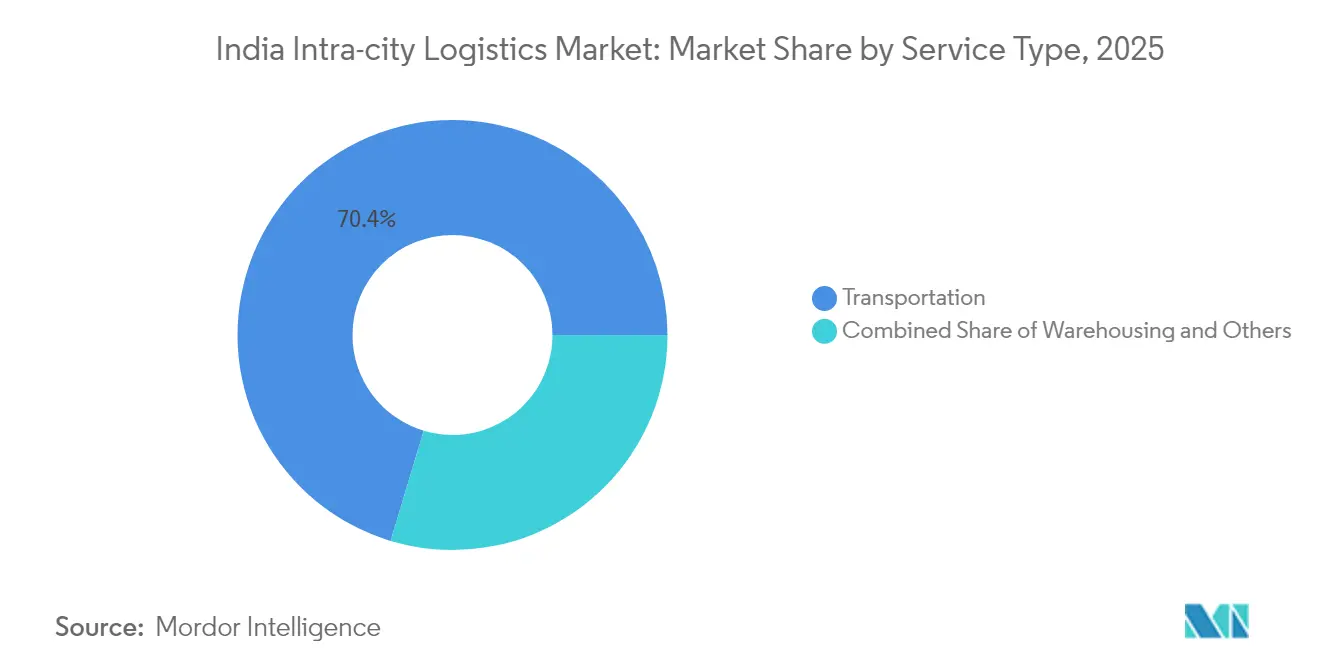

- By service, transportation captured 70.35% of the India intra-city logistics market share in 2025, while value-added services are forecast to grow at a 3.67% CAGR through 2031.

- By business model, the B2C segment held 58.30% of the India intra-city logistics market size in 2025 and C2C is projected to expand at a 3.38% CAGR during 2026-2031.

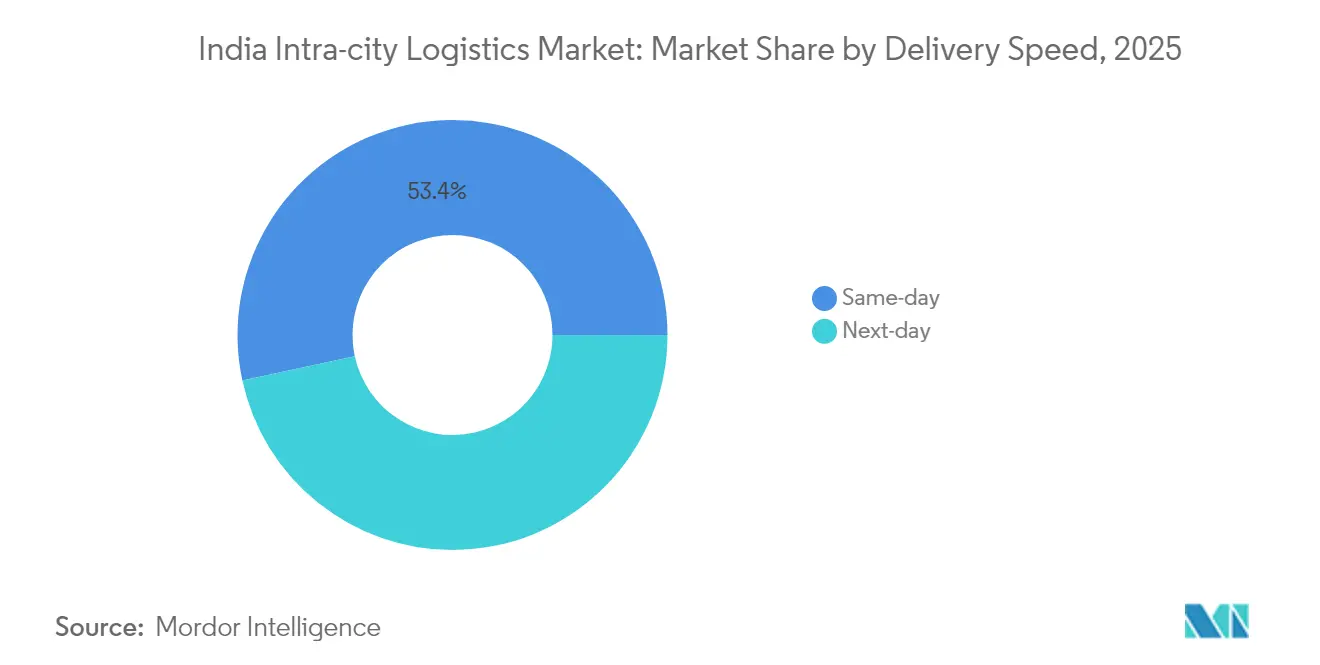

- By delivery speed, same-day services accounted for 53.40% of the India intra-city logistics market share in 2025 and lead growth at a 4.41% CAGR through 2031.

- By end-user, e-commerce retail represented 46.62% of the India intra-city logistics market size in 2025 and is advancing at a 4.73% CAGR to 2031.

- By geography, Tier-1 metros contributed 58.40% revenue share in 2025, whereas Tier-3 cities are registering the highest 4.32% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Intra-city Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce parcel growth | +1.2% | Global, with concentration in Tier-1 metros and rapid Tier-2/3 expansion | Medium term (2-4 years) |

| National Logistics Policy & PM-Gati Shakti implementation | +0.8% | National, with early gains in Delhi NCR, Mumbai, Bengaluru | Long term (≥ 4 years) |

| Urban consolidation centres mandated in city-freight master plans | +0.6% | Tier-1 metros, expanding to major Tier-2 cities | Medium term (2-4 years) |

| Tier-2/3 city retail digitalisation wave | +0.7% | APAC core, spill-over to smaller urban centers | Short term (≤ 2 years) |

| Rapid electrification of last-mile fleets | +0.5% | National, with pilot programs in major metros | Long term (≥ 4 years) |

| ONDC-driven open logistics interoperability | +0.4% | National, with early adoption in tech-forward cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive E-commerce Parcel Growth

Same-day delivery seized 54.0% of the delivery-speed segment in 2024, underscoring consumer expectations for immediacy and fueling the India intra-city logistics market. Quick-commerce firms such as Zepto and Blinkit are leasing Grade A warehouses, pushing nationwide demand beyond 300 million sq ft by 2025. The proliferation of micro-fulfillment centers is redefining last-mile routing, shrinking travel distances, and elevating real-time visibility as an operational imperative. Logistics providers are deploying AI-enabled dispatch tools to optimize fleet utilization and ensure turn-around times under thirty minutes. E-commerce’s 47.0% end-user share establishes it as the pivotal growth catalyst for urban delivery investments[1]“$350 Million Loan Signing Between Government of India and ADB,” Press Information Bureau, pib.gov.in.

National Logistics Policy and PM-Gati Shakti Implementation

Government programs are modernizing multimodal infrastructure and digital governance. The USD 350 million SMILE loan signed in December 2024 is financing smart systems and standard warehousing frameworks that reduce hand-off delays in the India intra-city logistics market. ULIP surpassed 100 crore API calls in March 2025, evidencing rapid data interoperability that cuts paperwork and accelerates vehicle clearances. Multi-modal logistics parks under PM-Gati Shakti link city distribution networks with rail and expressways, trimming first-mile to last-mile transit times. These structural upgrades help the sector move toward the National Logistics Policy target of lowering logistics cost from 14% to 8% of GDP, creating headroom for price competitiveness in urban freight[2]“Warehousing Demand, Rents Witness Surge,” Business Standard, business-standard.com.

Urban Consolidation Centers Mandated in City-Freight Plans

Metropolitan master plans now require consolidation hubs on city fringes to streamline inbound freight. Facilities adjacent to new corridors, including Mumbai Trans Harbour Link and Delhi’s Dwarka Expressway, channel palletized loads into smaller electric vans for the final mile. This hub-and-spoke logic reduces vehicle trips inside congested cores, easing curb scarcity and emissions. Public-private partnerships manage land pooling, while operators deploy slot-booking apps that allocate dock times in ten-minute windows to curb dwell. Early results in Delhi NCR show a 12% reduction in intra-day traffic peaks, supporting smoother parcel flows and higher on-time delivery metrics.

Tier-2/3 City Retail Digitalization Wave

Increasing smartphone penetration and fintech adoption are propelling online commerce in Bhopal, Coimbatore, Surat, and other midsize cities. These centers post the fastest 4.40% CAGR within the India intra-city logistics market as SMEs migrate to online storefronts. Logistics firms that establish micro-hubs early gain cost-advantaged routes and first-mover brand loyalty. Local governments are extending warehousing incentives and simplified zoning clearances, compressing deployment timelines from eighteen to twelve months. Operators are also piloting electric two-wheelers tailored for narrow lanes, lowering delivery costs while meeting sustainability mandates.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe urban traffic congestion & curb scarcity | -0.9% | Tier-1 metros, expanding to major Tier-2 cities | Short term (≤ 2 years) |

| Hyper-fragmented small-fleet operator base | -0.6% | National, with concentration in urban centers | Medium term (2-4 years) |

| Rising land & compliance costs for micro-fulfilment sites | -0.7% | Tier-1 metros and high-growth Tier-2 cities | Long term (≥ 4 years) |

| Pending gig-worker safety / social-security mandates | -0.4% | National, with immediate impact in organized sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Severe Urban Traffic Congestion and Curb Scarcity

Delivery vans face average speeds below 15 km/h in Mumbai and Bengaluru rush hours, eroding fleet productivity and inflating fuel bills. Land transactions climbed to 2,335 acres across 23 cities in 2024, with prices escalating to INR 17 crore per acre USD 20.3 million after conversion complicating terminal development. Scarce loading bays force double-parking that attracts fines and escalates turnaround times. While infrastructure mega-projects pledge relief, their commissioning schedules stretch beyond immediate operational horizons, compelling carriers to overlay dynamic routing software and night-time delivery slots to navigate congestion[3]"Department of Posts and Amazon Sign Landmark MoU to Enhance Logistics Collaboration." Ministry of Communications, Press Information Bureau, pib.gov.in.

Pending Gig-Worker Safety / Social-Security Mandates

Implementation of the Code on Social Security 2020 extends EPFO and insurance benefits to 3 million platform riders. Compliance could add 15-20% to payroll outlays for organized logistics firms, compressing margins in the India intra-city logistics market. Operators must introduce accident-cover premiums, digital attendance systems, and grievance redressal portals. Smaller fleets struggle with administrative overhead, accelerating industry consolidation as larger platforms absorb stand-alone bike owners and standardize benefits programs to retain labor supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Amid Value-Added Growth

Transportation retained 70.35% of the India intra-city logistics market share in 2025, driven by the non-discretionary need for urban freight movement. Growth continues as e-commerce volumes climb and food delivery scales across metros and Tier-2 towns. Warehousing and distribution services are expanding steadily, supported by urban consolidation centers that act as staging points for micro-fulfillment. The value-added segment, while smaller today, is registering a 3.67% CAGR as customers demand reverse logistics, real-time tracking, and white-glove services.

Digitization is reshaping service economics. AI-enabled route optimization lifts vehicle utilization, while automated invoicing reduces back-office cycles for mid-tier operators. The India intra-city logistics industry increasingly bundles transport with inventory management, enabling shippers to outsource integrated workflows. Environmental compliance is another catalyst: shippers value partners that certify fleets to BS6 norms and deploy electric vans, positioning value-added services as a differentiator in contract bids.

By Business Model: B2C Leadership with C2C Emerging

The B2C model dominated the India intra-city logistics market with 58.30% revenue contribution in 2025, a direct result of e-commerce acceleration and consumer preference for doorstep delivery. Amazon’s partnership with Indian Railways, scaling to 120+ intercity routes, illustrates how large platforms integrate national trunk routes with city distribution. B2B shipments remain significant, especially for FMCG and pharma, but their growth is slower relative to retail parcels.

C2C deliveries, although only a single-digit share today, are accelerating at 3.38% as ONDC’s open logistics layer levels entry barriers. Individuals selling on social media can now tap standard parcel networks at near enterprise rates, expanding peer-to-peer shipment volumes. For logistics companies, C2C represents an incremental utilization lever, filling backhaul capacity and smoothing peak workloads.

By Delivery Speed: Same-Day Services Lead Innovation

Same-day offerings held 53.40% of the India intra-city logistics market in 2025 and are projected to grow fastest at 4.41% CAGR. Micro-fulfillment centers within 3-5 km of dense residential clusters enable 30-minute drop-offs for grocery and pharmacy orders. Operators deploy AI to batch orders geographically, cutting dwell time at pick-up nodes.

Next-day (24-48 hour) services sustain relevance for bulkier SKUs and remote suburbs where same-day economics are challenging. Platforms like cityXfer specialize in large-format goods, achieving lower damage rates through trained crews and custom rigging. Market differentiation hinges on service reliability and transparent ETAs rather than speed alone, nudging carriers to invest in IoT tags and customer-facing apps that provide real-time van locations.

By End-user Industry: E-commerce Retail Drives Market Evolution

E-commerce retail accounted for 46.62% of the India intra-city logistics market size in 2025 and is forecast to post a 4.73% CAGR to 2031. Fashion, beauty, and electronics lead SKU throughput, but grocery and health staples are climbing due to consumer trust in online perishables. The healthcare segment gains traction through stringent cold-chain requirements that favor organized players with temperature-controlled micro-hubs.

Reverse logistics is expanding alongside sales, particularly in apparel where return rates exceed 20%. Specialized providers offer doorstep quality checks and instant refunds, enhancing customer experience. White-goods and furniture categories drive demand for two-technician crews trained in assembly and reverse pickup, adding complexity but also high-margin service layers within the India intra-city logistics industry.

Geography Analysis

Regional concentration remains pronounced, yet growth vectors are shifting. Northern and Western India, anchored by Delhi NCR and Mumbai Metropolitan Region, continue to command a large slice of the India intra-city logistics market. Delhi NCR topped 2024 real estate deals at 36 transactions, while Mumbai absorbed 407 acres of industrial land. Both regions benefit from expressways and port linkages that shorten inbound trunk hauls, feeding dense last-mile networks.

Southern states provide the next leg of expansion. Bengaluru’s tech-centric economy fuels premium parcel flows, and Hyderabad’s 340 km Regional Ring Road is opening greenfield corridors for Grade A sheds. Chennai and Delhi NCR together contributed about 50% of warehousing leasing in 2024, mirroring persistent demand for urban consolidation assets. State incentives for solar rooftops and EV charging encourage sustainable facilities that lower lifecycle costs.

The East, though smaller, is picking up speed on the back of port modernization in Kolkata and Paradip. Dedicated freight corridors under Act East policy unlock new hinterland access, letting shippers bypass congested trans-western routes. Odisha’s single-window clearance trims approval cycles for logistics parks, attracting first-wave investors targeting mineral-rich clusters and growing retail bases in Bhubaneswar and Cuttack. Each region’s trajectory underscores the need for network planners to maintain agile asset footprints aligned with local demand granularity.

Competitive Landscape

The India intra-city logistics market is moderately fragmented but consolidating as technology and compliance raise operating thresholds. Delhivery’s Rs 1,407 crore acquisition of Ecom Express enlarges its last-mile reach and diversifies service lines into Tier-3 geographies. Amazon’s deepening partnership with Indian Railways and India Post extends its access to 160,000 branch post offices, filling network gaps where private fleets are thin.

Digital interoperability via ONDC allows small courier firms to plug into unified routing stacks, intensifying price competition while widening parcel coverage. AI-centric specialists like COGOS Technologies use predictive analytics to match loads with idle capacity across 300+ cities, backed by recent seed funding that accelerates platform rollouts. Compliance with environmental norms and gig-worker safety regulations favors capitalized players that can fund BS6 fleet upgrades and social-security schemes, gradually edging out under-capitalized micro-operators.

As market leaders converge on integrated solutions, differentiation shifts to service quality and data transparency. Real-time tracking APIs, customer self-service dashboards, and carbon reporting modules are now baseline expectations in contract tenders. Alliances between freight tech startups and traditional 3PLs are proliferating to combine digital agility with asset density, shaping a landscape where scale and technology co-exist as twin pillars of competitive advantage.

India Intra-city Logistics Industry Leaders

-

Delhivery

-

Blue Dart Express

-

Shadowfax

-

Ekart Logistics

-

cityXfer

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mahindra Logistics partnered with Asian Paints for premium line-haul services under its Pro-Trucking program, deploying BS6 fleet and safety analytics.

- December 2024: Government of India and ADB signed a USD 350 million SMILE program loan to fund multimodal logistics infrastructure.

- October 2024: Department of Posts and Amazon inked an MoU to expand parcel collaboration across 160,000 post offices.

- August 2024: Amazon Transportation Services and Indian Railways scaled parcel trains from one route in 2019 to 120+ routes across 91 cities.

India Intra-city Logistics Market Report Scope

Intra-city logistics is not just about delivering parcels in 30 minutes. It is about solving the business challenges that companies face and building capabilities to seamlessly execute any sort of goods movement irrespective of their scale and size. The Indian intra-city logistics market is segmented by service (transportation, warehousing and distribution, and value-added services) and by city (Delhi, Bangalore, Mumbai, Hyderabad, Chennai, and Others). The report offers market size and forecasts for the Indian intra-city logistics market in value (USD billion) for all the above segments.

| Transportation |

| Warehousing and Distribution |

| Value-added Services |

| B2B |

| B2C |

| C2C |

| Same-day (<24 h) |

| Next-day (24-48 h) |

| E-commerce Retail |

| Fashion and Lifestyle |

| Beauty, Wellness and Personal Care |

| Home and Furniture |

| Consumer Electronics and Appliances |

| Healthcare and Medical Supplies |

| Others |

| Tier-1 Metros |

| Tier-2 Cities |

| Tier-3 and Below |

| By Service | Transportation |

| Warehousing and Distribution | |

| Value-added Services | |

| By Business Model | B2B |

| B2C | |

| C2C | |

| By Delivery Speed | Same-day (<24 h) |

| Next-day (24-48 h) | |

| By End-user Industry | E-commerce Retail |

| Fashion and Lifestyle | |

| Beauty, Wellness and Personal Care | |

| Home and Furniture | |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Supplies | |

| Others | |

| By City Tier | Tier-1 Metros |

| Tier-2 Cities | |

| Tier-3 and Below |

Key Questions Answered in the Report

What is the current value of the India intra-city logistics market?

The market is valued at USD 34.93 billion in 2026 and is forecast to reach USD 43.06 billion by 2031.

Which service segment holds the largest share?

Transportation services command 70.35% of 2025 revenue, underscoring their central role in urban freight.

How fast is e-commerce retail driving growth?

E-commerce retail represents 46.62% of 2025 revenue and is expanding at a 4.73% CAGR through 2031.

Which delivery speed segment is growing the fastest?

Same-day delivery leads with 53.40% share and a 4.41% CAGR as consumers demand immediate fulfillment.

What government initiatives support the sector?

PM-Gati Shakti and the National Logistics Policy are investing in multimodal parks, digital platforms, and cost-reduction frameworks.

How is consolidation affecting competition?

Acquisitions like Delhivery’s takeover of Ecom Express are creating integrated platforms with wider geographic coverage and advanced technology.

Page last updated on: