India Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.81 Billion |

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 4.98 Billion |

| Growth Rate (2026 - 2031) | 9.66% CAGR |

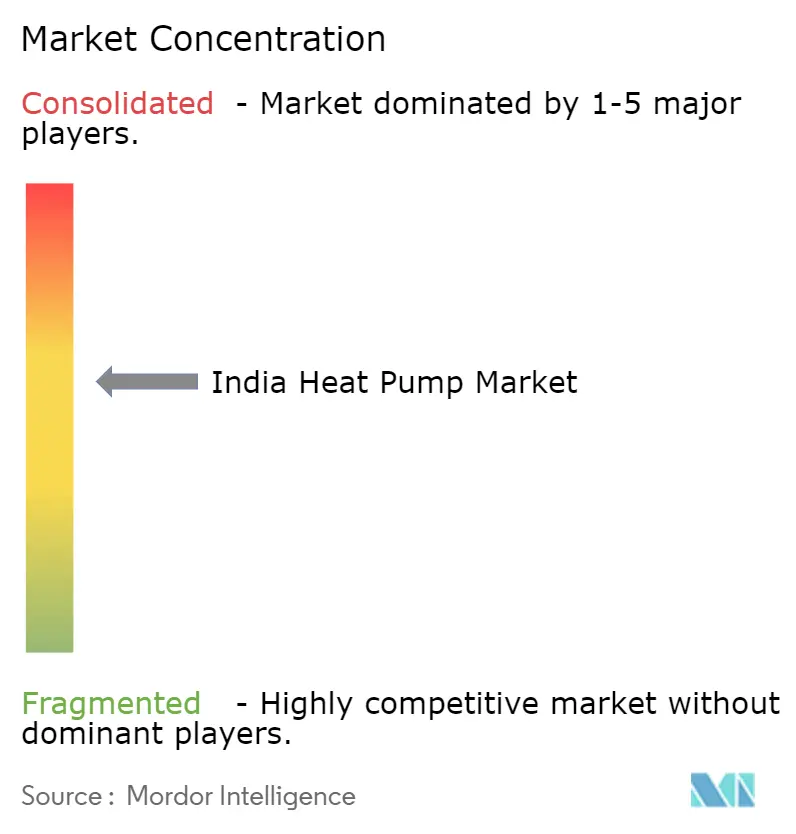

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Heat Pump Market Analysis by Mordor Intelligence

The India heat pump market size is expected to increase from USD 2.81 billion in 2025 to USD 3.14 billion in 2026 and reach USD 4.98 billion by 2031, growing at a CAGR of 9.66% over 2026-2031. Government incentives, data-center expansion, and decarbonization mandates are widening the addressable base for high-efficiency systems, even as grid bottlenecks and technician shortages temper near-term momentum. Residential demand still dominates, yet double-digit industrial growth shows that buyers increasingly value process-heat electrification over comfort cooling. Air source configurations remain the volume backbone of the India heat pump market, although fiscal perks under the National Geothermal Energy Policy are accelerating interest in ground source solutions. Established brands are localizing research and development to address India-specific challenges such as dusty environments and high-ambient temperatures while smaller domestic firms chase white-space opportunities in high-temperature and geothermal niches.

Key Report Takeaways

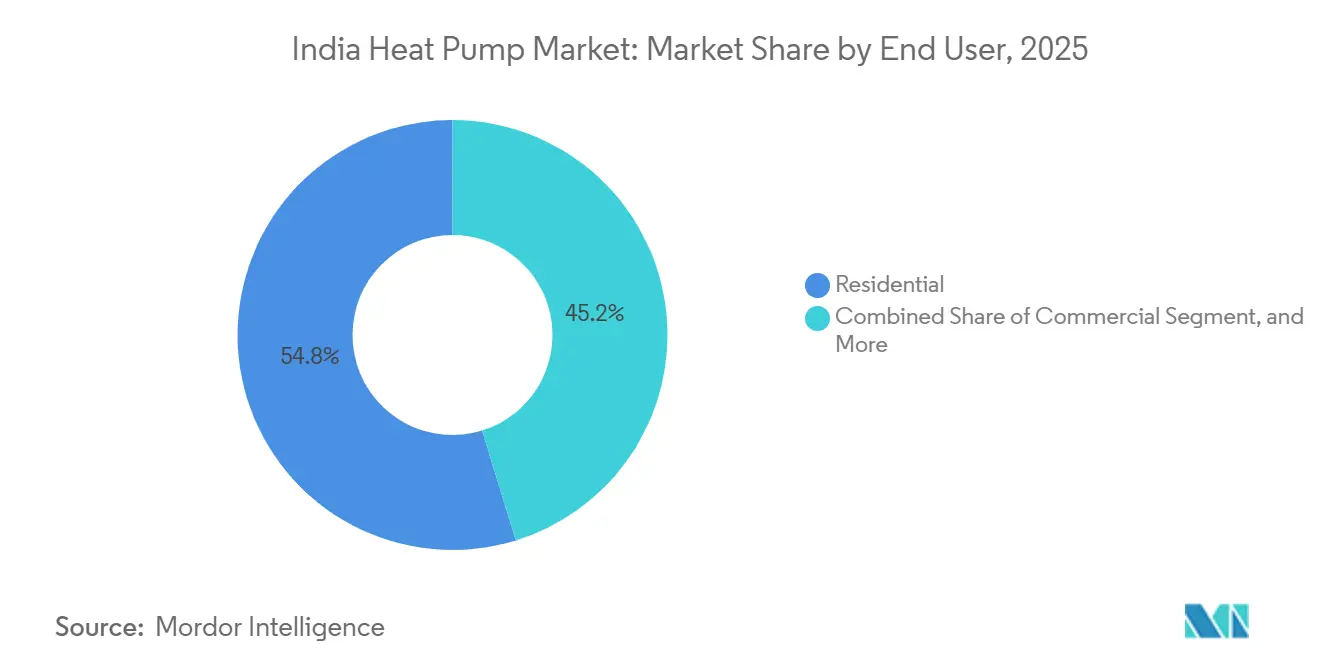

- By end user, the residential segment held 54.78% of the India heat pump market share in 2025, while the industrial segment is forecast to expand at 11.78% CAGR through 2031.

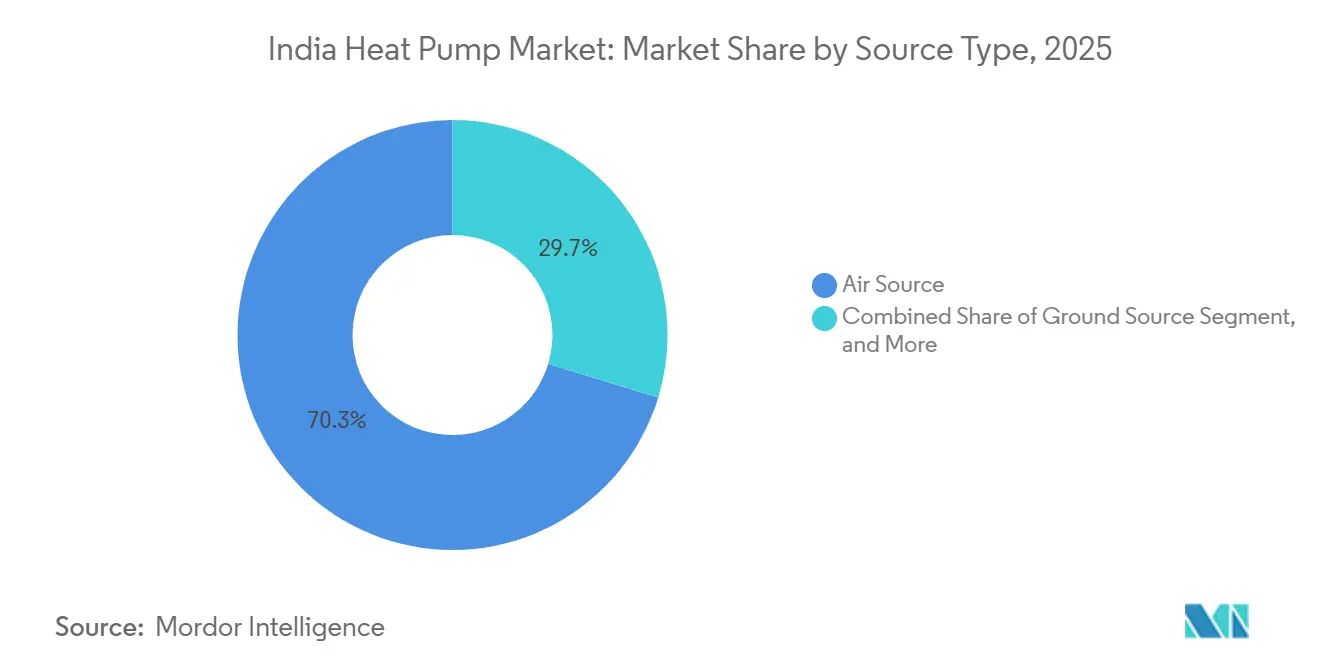

- By type, air source units commanded 70.31% of the India heat pump market share in 2025, whereas ground source units are projected to register an 11.31% CAGR to 2031.

- By technology, air-to-water systems led with 62.29% revenue share in 2025, and ground-to-water solutions are on track for an 11.52% CAGR to 2031.

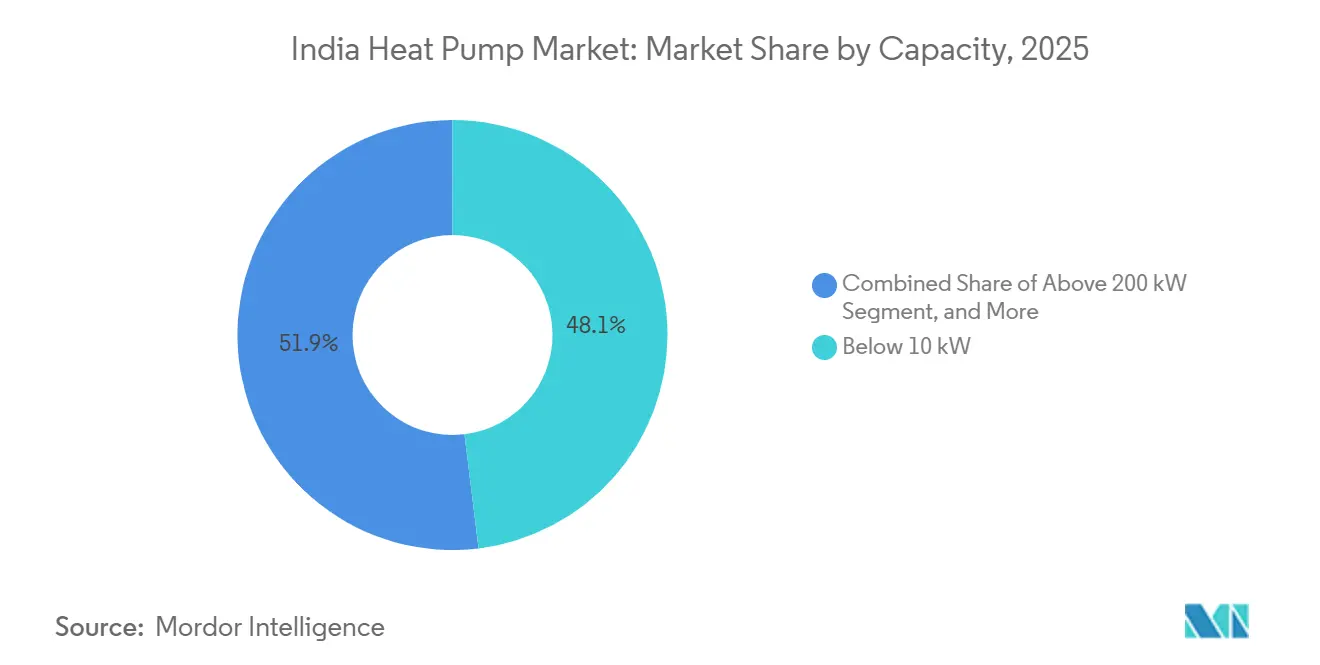

- By capacity, systems above 200 kW are expected to post a 10.27% CAGR between 2026 and 2031, outpacing all other capacity brackets.

- By application, domestic hot-water systems accounted for 40.49% of the India heat pump market size in 2025, yet industrial and process heating is advancing at a 12.03% CAGR through 2031.

- By installation type, new installations represented 60.52% of 2025 shipments, but retrofit activity is expected to rise at a 10.26% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation of Government Incentives such as PLI Scheme and GST Reductions for Energy-Efficient HVAC | +1.8% | National, with early gains in Gujarat, Tamil Nadu, Maharashtra | Short term (≤ 2 years) |

| Rapid Urbanization, Rising Disposable Income and Residential Construction Boom | +2.1% | National, concentrated in Mumbai, Delhi-NCR, Bangalore, Hyderabad, Pune, Chennai | Medium term (2-4 years) |

| Increasing Electricity Costs Driving Demand for High-COP Heating and Cooling Solutions | +1.5% | National, acute in Karnataka, Uttar Pradesh, Himachal Pradesh | Medium term (2-4 years) |

| National Renewable-Energy and Decarbonization Targets Promoting Electrification of Heating | +1.9% | National, with early adoption in Gujarat, Tamil Nadu, Andhra Pradesh | Long term (≥ 4 years) |

| Micro-Utility Heat-Pump Projects in Smart Cities Creating Demonstration Effect | +0.9% | Ladakh, Nagpur, Andhra Pradesh tourism sector, expanding to tier-2 cities | Medium term (2-4 years) |

| Expansion of Data Centers Requiring Low-PUE Thermal Management Using Process Heat Pumps | +1.4% | Mumbai, Chennai, Bangalore, Delhi-NCR, Hyderabad, Pune | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Implementation of Government Incentives such as PLI Scheme and GST Reductions for Energy-Efficient HVAC

Financial support under the Production Linked Incentive framework lowers component import dependence, giving local compressor and heat-exchanger production a cost edge. The September 2025 Goods and Services Tax cut reduced retail prices by up to 12%, shortening payback periods for first-time residential buyers.[1]Goods and Services Tax Council, “GST Rate Reductions for Air Conditioners and Renewable Energy Devices,” gstcouncil.gov.in Stricter Bureau of Energy Efficiency star-rating norms that took effect in January 2026 raised efficiency thresholds, benefitting firms with strong R&D capability but squeezing smaller assemblers. State policies layer additional incentives: Gujarat offers capital subsidies of up to INR 2 million (USD 0.02 million), while Tamil Nadu mandates district-cooling studies in new urban zones, creating uneven regional uptake.[2]Government of Tamil Nadu, “Heat Mitigation Strategy 2024,” tn.gov.in, Gujarat Energy Development Agency, “Integrated Renewable Energy Policy 2025,” geda.gujarat.gov.in Combined, these measures tilt the India heat pump market toward premium, high-efficiency models that comply with new labeling rules.

Rapid Urbanization, Rising Disposable Income and Residential Construction Boom

India adds roughly 10 million urban residents each year, and housing launches grew 21% in 2024, reinforcing demand for compact, plug-and-play air-to-water units. Per-capita income climbed to INR 185,000 (USD 1,985) in FY 2024, enlarging the middle-class cohort that can finance efficient cooling and hot-water solutions. While dense city plots favor air source systems, marquee geothermal projects at Leh Airport and an Indian Army net-zero facility signal that developers of premium projects are testing ground source designs.[3]Airports Authority of India, “Leh Airport Geothermal System Completed,” aai.aero Urban consumers value quiet operation and smart-controls integration, nudging brands to bundle Internet of Things features even in sub-10 kW offerings. As a result, the India heat pump market continues to shift from basic comfort appliances toward connected, high-efficiency solutions.

Increasing Electricity Costs Driving Demand for High-COP Heating and Cooling Solutions

Tariff hikes of 4-8% in Karnataka, Uttar Pradesh, and Himachal Pradesh have sharpened focus on lifecycle cost rather than sticker price. High-temperature heat pumps that deliver 120-200 °C steam can cut industrial fuel bills by up to 50%, yet initial outlays averaging INR 8-12 million (USD 0.085-0.13 million) for 500 kW units slow uptake among small enterprises. Time-of-day tariffs make process-integrated heat pumps attractive when paired with rooftop solar, helping factories dodge peak-hour penalties in Gujarat and Maharashtra. Lifecycle savings and carbon-credit revenue, therefore, are pushing the India heat pump market beyond residential hot-water use into industrial duty cycles.

National Renewable-Energy and Decarbonization Targets Promoting Electrification of Heating

India’s pledge for 500 GW non-fossil capacity by 2030 elevates heat pumps as a primary electrification lever. The National Geothermal Energy Policy offers accelerated depreciation and viability-gap funding, unlocking 10,600 MW of resource potential spread across 381 hot springs.[4]Ministry of New and Renewable Energy, “National Geothermal Energy Policy Launched,” Press Information Bureau, pib.gov.in Early wells at the Puga Valley field in Ladakh underscore prospects for off-grid district heating in extreme cold regions. Carbon credit trading adds a new revenue channel by monetizing verified energy savings.[5]Bureau of Energy Efficiency, “Perform, Achieve and Trade Scheme,” beeindia.gov.in Together, these levers expand the strategic significance of the India heat pump market within national decarbonization roadmaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Installation Costs and Limited Financing Options | -1.2% | National, acute in tier-2 and tier-3 cities, rural areas | Short term (≤ 2 years) |

| Shortage of Certified Heat-Pump Installers and Service Technicians | -0.8% | National, severe in North India, Northeast, rural areas | Medium term (2-4 years) |

| Grid Congestion Penalties Limiting Large-Scale Heat-Pump Adoption in Industrial Clusters | -0.6% | Uttar Pradesh, Bihar, Gujarat, Maharashtra industrial belts | Medium term (2-4 years) |

| Performance Degradation in High-Ambient Dusty Conditions Increasing Maintenance Costs | -0.5% | Rajasthan, Gujarat, Haryana, Delhi-NCR industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation Costs and Limited Financing Options

Industrial-grade systems cost INR 1.5-12 million (USD 0.016-0.13 million) depending on capacity, with integration adding up to 30% extra outlay. Drilling 110-120 m boreholes for ground source projects, such as the 457 holes at Leh Airport, can push project budgets beyond the comfort zone of most developers. Banks classify heat pumps as specialized equipment, sidelining them from standard working-capital credit lines, and subsidized loans remain scarce despite pilot programs by Energy Efficiency Services Limited. Payback periods of 18-48 months exceed the 12-month horizon preferred by small manufacturers, delaying broader penetration of the India heat pump market.

Shortage of Certified Heat-Pump Installers and Service Technicians

Fewer than 50 contractors nationwide possess the drilling and loop-design skills needed for ground source installations. Bosch Home Comfort’s plan to train 2,000 technicians highlights a deficit that the National Skill Development Corporation counts at 150,000 refrigeration and air-conditioning workers by 2027. Poor charging practices and sub-standard components can slash a system’s coefficient of performance by up to 25%, eroding consumer confidence and raising warranty claims. Until certification is mandated nationwide, workmanship gaps will continue to restrain the India heat pump market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominance Masks Ground Source Acceleration

Air source systems held 70.31% of the India heat pump market share in 2025 thanks to lower upfront costs and installer familiarity. Water source units cater to niche district-cooling and industrial loops, whereas hybrids provide backup resiliency but dilute decarbonization gains. Ground source units, however, are projected to grow at an 11.31% CAGR, buoyed by fiscal incentives and headline projects like the 2,500 kW Leh Airport installation that drilled 457 boreholes to maintain stable efficiency in sub-zero winters. The technology’s ability to operate efficiently at ambient extremes positions it well for institutional buyers across high-altitude and high-heat regions.

While air source products dominate residential retrofits, their coefficient of performance drops 2-3% for every 1 °C rise beyond design conditions, challenging operations when summer peaks top 47 °C in the northern plains. Regulatory water-extraction limits in drought-prone states curb wider use of water source designs. Hybrid setups switch to fossil burners during outages, complicating emissions accounting under the carbon-credit framework. Despite higher drilling expenses, accelerated depreciation under the geothermal policy is persuading airports, defense campuses, and premium real-estate developers to opt for ground source solutions, expanding the strategic canvas of the India heat pump market.

By Technology: Air-To-Water Systems Lead, Ground-To-Water Gains Traction For Industrial Heat

Air-to-water designs captured 62.29% share in 2025 by supplying domestic hot water and hydronic heating from compact packages. Air-to-air variants remain common in retail and office cooling, whereas water-to-water units serve closed-loop industrial processes. Ground-to-water solutions are forecast to expand at an 11.52% CAGR, aided by stable ground temperatures that keep coefficients of performance above 4 while delivering up to 65 °C without backup heat. The India heat pump market is also witnessing a pivot to high-temperature carbon-dioxide systems: Triveni Turbines’ 122 °C unit shows a coefficient of performance of 6 for pharmaceutical and food-processing lines.

Residential buyers favor plug-and-play 200-500 L air-to-water cylinders such as Racold’s range, priced between INR 199,999 (USD 2,147) and INR 299,000 (USD 3,220), delivering coefficients of performance above 4.4. In contrast, ground-to-water installations like Nagpur Metro Bhavan’s 175-ton system cut power demand from 1.6 kW/ton for conventional chillers to 0.6 kW/ton, achieving payback in 4.3 years. Water-to-water retrofits in Gujarat’s chemical sector have slashed energy by 38% with 18-month returns, proving that industrial users are ready to adopt once financing hurdles ease. Together, these developments reinforce the upward trajectory of the India heat pump market across diversified technologies.

By Capacity: Residential Units under 10 kW Prevail, Utility-Scale above 200 kW Ascend

Heat-pump systems below 10 kW accounted for 48.07% of the India heat pump market share in 2025, reflecting urban homeowners’ appetite for compact domestic-hot-water and single-room cooling packages. Installations in the 10-50 kW band serve small hotels and multifamily buildings, while the 50-200 kW bracket addresses mid-sized manufacturing plants that integrate rooftop-solar arrays to dodge peak-hour tariffs. Systems above 200 kW, including the 2,500 kW ground-source array at Leh Airport, are forecast to post a 10.27% CAGR through 2031 as data-center and district-cooling investors favor megawatt-scale thermal management.

Below-10 kW products ship through mass-market retail and qualify for consumer-finance schemes, yet they battle low-cost resistance heaters and split air conditioners for wallet share. Mid-range 10-50 kW units gain traction when commercial buyers seek lower operating expenditure and green-building ratings. Installations in the 50-200 kW slot increasingly feature variable-speed compressors and low-global-warming-potential refrigerants to meet Bureau of Energy Efficiency audits. Above-200 kW projects demand custom engineering and multi-month commissioning but deliver the strongest lifecycle economics, especially for data-center builders targeting power-usage-effectiveness below 1.3.

By Application: Domestic-Hot-Water Leads, Industrial Process Heating Accelerates

Domestic and sanitary-hot-water uses held 40.49% of the India heat pump market size in 2025, benefiting from 60%-70% electricity savings versus resistance heaters. Space-cooling dominates absolute electricity consumption in southern and western states, whereas space-heating demand clusters in Himalayan regions. Industrial process-heating applications, projected to rise at a 12.03% CAGR, receive tailwinds from Carbon-Credit-Trading revenues and Perform, Achieve and Trade obligations.

Residential hot-water units, priced up to INR 299,000 (USD 3,220), integrate Internet-of-Things controls to improve user experience and demand-response compatibility. Space-cooling heat pumps adopt inverter-driven compressors that maintain high coefficients of performance even at 47 °C ambient peaks. Ground-source arrays such as the 60 kW PHC Thiksay unit in Ladakh demonstrate year-round comfort in extreme cold . Industrial buyers adopt high-temperature carbon-dioxide designs that deliver 122 °C steam for pharmaceutical, food, and chemical lines, trimming fossil-fuel costs by as much as 50%.

By End User: Residential Still Dominant, Industrial Expands Fastest

Homeowners captured 54.78% of the India heat pump market share in 2025, supported by urban income growth and GST reductions that lowered equipment prices. Commercial buildings, hospitals, hotels, shopping malls, value lifecycle savings and green-certification points, spurring steady orders for air-to-water and variable-refrigerant-flow platforms. The industrial cohort is forecast to advance at an 11.78% CAGR to 2031 due to carbon-credit revenue potential and heightened scrutiny under energy-efficiency audits.

Residential buyers gravitate toward quiet 2-3 kW split packages for apartments, whereas villas adopt 8-10 kW air-to-water cylinders that feed hydronic loops. Commercial property developers, chasing Indian Green Building Council Platinum ratings, specify centralized ground-source arrays for premium offices and retail complexes. Industrial users such as textiles, dairy, and pharmaceuticals choose modular 200-500 kW high-temperature units that retrofit to existing steam headers, cutting coal and furnace-oil bills despite 18-36 month paybacks.

By Installation: New Construction Dominates, Retrofits Gain Momentum

New-build projects represented 60.52% of the India heat pump market in 2025 because integrated design lowers ducting costs and eases compliance with Energy Conservation Building Code 2022. Retrofit demand will grow at a 10.26% CAGR as property owners confront rising power tariffs and aging chiller plants. Energy-service-company contracts spearheaded by Energy Efficiency Services Limited remove capital-expenditure hurdles for public buildings, widening the retrofit funnel.

Developers embed heat-pump loops during construction to differentiate properties and justify higher sale prices. Data-center investors integrate above-200 kW chillers in modular rows to reach power-usage-effectiveness targets, while hotels and hospitals retrofit 50-200 kW systems under guaranteed-savings agreements. Retrofit complexity inflates project budgets by 20%-40%, yet rising carbon-credit valuations and accelerated-depreciation benefits shorten paybacks below three years in energy-intensive industries.

Geography Analysis

Southern states, led by Tamil Nadu and Karnataka, anchor residential and commercial adoption because cooling-degree days exceed 3,000 per year and state incentives reward high-efficiency installations. Tamil Nadu’s Heat-Mitigation Strategy requires district-cooling studies for new townships, nudging developers toward centralized air-to-water plants. Bangalore’s data-center build-out further elevates megawatt-scale demand, cementing the region’s role as the largest contributor to the India heat pump market.

Western India combines residential penetration in Mumbai and Pune with industrial retrofits along Gujarat’s chemical and pharmaceutical corridor. Gujarat’s Integrated Renewable Energy Policy supplies capital subsidies up to INR 2 million (USD 21,470), while technician-training pacts with Bosch Home Comfort aim to close skills gaps. Maharashtra’s electricity-duty exemptions and time-of-day tariff premiums strengthen investment rationale for ground-source and high-temperature solutions in refineries, automotive plants, and logistics parks.

Northern and northeastern territories remain nascent yet strategic. Ground-source arrays deliver reliable heating in Ladakh, Himachal Pradesh, and Uttarakhand where winter lows challenge air-source efficiency. The Puga-Valley geothermal pilot, combined with accelerated-depreciation incentives, signals potential for off-grid military and tourism districts. Uttar Pradesh and Bihar struggle with grid congestion penalties that complicate megawatt-class deployments, but micro-utility pilots in smart-city programs could unlock tier-2 opportunities if transmission upgrades materialize.

Competitive Landscape

Multinationals such as Daikin, Mitsubishi Electric, and LG Electronics control roughly 55%-60% of shipments through localized factories, deep research portfolios, and broad channel reach. Daikin’s INR 50 billion Neemrana campus and Mitsubishi Electric’s INR 21 billion (USD 0.23 billion) Tamil Nadu plant underscore long-term manufacturing bets tailored to India’s dusty, high-temperature environment. Domestic majors Blue Star and Voltas pivot toward data-center cooling and industrial high-temperature applications to escape price wars in residential air-conditioning.

Emergent players exploit white spaces. Triveni Turbines launched a 122 °C carbon-dioxide heat pump that breaks the dominance of imported high-temperature units, while niche integrators such as Tetra Heat and Refman bundle mechanical-vapor-recompression modules for large chemical plants. Less than 50 qualified ground-source contractors nationwide create an entry lane for global specialists like NIBE and Viessmann willing to invest in drilling equipment and installer training.

Technology race intensifies under the Bureau of Energy Efficiency’s January 2026 star-rating revision that forces 10%-15% higher efficiency thresholds. Manufacturers now highlight low-global-warming-potential refrigerants, artificial-intelligence diagnostics, and cloud-linked controls. LG’s Multi V i and Daikin’s AI VRV Alpha families exemplify the pivot toward connected ecosystems that promise 15%-20% energy savings and predictive-maintenance cost reductions.

India Heat Pump Industry Leaders

Daikin Industries Ltd.

Mitsubishi Electric Corp.

LG Electronics India

Fujitsu General Ltd.

Voltas Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Daikin India introduced AI VRV Alpha and R-290 monobloc heat pumps, adding over 60 Bureau-of-Energy-Efficiency-compliant models.

- March 2026: LG Electronics India unveiled Multi V i and data-center chillers with AI-based predictive-maintenance functions at ACREX 2026.

- February 2026: Mitsubishi Electric India inaugurated a INR 21 billion (USD 0.23 billion) Tamil Nadu factory, boosting annual output by 300,000 units and 650,000 compressors.

- February 2026: Blue Star and Voltas announced liquid-cooling systems targeting data centers set to double capacity by 2029.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the Indian heat pump market as all factory-built air-source, water-source, and ground-source systems sold for space heating, cooling, or sanitary hot water in residential, commercial, industrial, and institutional buildings. The revenue pool captures complete packaged units, split systems, and dedicated heat-pump water heaters installed within India, inclusive of hardware, controls, and standard installation labor, as framed by Mordor Intelligence analysts.

Scope exclusion: Portable room air conditioners with a reversible cycle, pure cooling window units, and custom industrial heat-recovery skids are outside this study.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed HVAC contractors, distributor principals, facility engineers, and energy auditors from high-installation states. Respondents validated average system capacities, price corridors, policy awareness, and retrofit demand, filling gaps left by desk work and grounding modeled assumptions.

Desk Research

Our team first compiles supply-side clues from tier-1 public sources such as the Ministry of Power, Bureau of Energy Efficiency, Central Electricity Authority, Directorate General of Commercial Intelligence and Statistics, and ISHRAE newsletters. These provide yearly production, import duty, and building energy code adoption data. We enrich the picture with company 10-Ks, investor decks, and permitted press releases that reveal shipment volumes and typical selling prices.

To check financial realism, we mine D&B Hoovers for OEM revenue splits and pull policy and tariff updates through Dow Jones Factiva, before mapping volumes to state-level housing completions and industrial electrification goals. The sources listed illustrate the breadth consulted; many additional publications aided data gathering and verification.

Market-Sizing and Forecasting

A top-down production plus trade reconstruction yields the national shipment base, which is subsequently checked with bottom-up approximations drawn from sampled project bills of quantities and installer channel checks. Key variables like urban housing starts, commercial floor space additions, average coefficient of performance, electricity to LPG price ratio, and state renewable purchase incentives feed a multivariate regression that projects demand through 2030. Where project-level ASPs were missing, we applied weighted averages from verified distributor quotes to prevent volume overstatement.

Data Validation and Update Cycle

Outputs pass anomaly scans, senior analyst peer review, and a two-step reconciliation against independent building energy and appliance stock statistics. Reports refresh each year, with interim tweaks when policy or macro conditions shift materially.

Why Mordor's India Heat Pump Baseline Is Trusted

Published estimates often vary; definitions, price build-ups, and refresh frequencies rarely align.

We acknowledge these gaps upfront and outline below how differing choices move the final number.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.94 B (2025) | Mordor Intelligence | |

| USD 0.41 B (2024) | Global Consultancy A | Counts only air-source water heaters; excludes install labor; relies solely on customs values |

| USD 2.14 B (2024) | Industry Publisher B | Includes hybrid industrial skids; applies uniform 41% CAGR without policy sensitivity checks |

The comparison shows that scope breadth, cost elements, and forecast logic are the main swing factors. By balancing top-down supply data with on-ground price validation and updating the model each year, Mordor delivers a dependable, decision-ready baseline clients can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the estimated value of the India heat pump space in 2026 and the projection for 2031?

Spending is expected to reach USD 3.14 billion in 2026 and climb to USD 4.98 billion by 2031.

Which capacity band is slated to grow the fastest?

Systems above 200 kW are expected to post a 10.27% CAGR through 2031.

Why are industrial buyers accelerating adoption?

Carbon-credit revenue and Perform, Achieve and Trade mandates make high-temperature heat pumps financially attractive despite higher upfront costs.

How does the National Geothermal Energy Policy influence demand?

Fiscal incentives and accelerated depreciation lower payback periods for ground-source projects, spurring double-digit growth in that segment.

Which regions lead residential installations?

Tamil Nadu and Karnataka dominate because of high cooling-degree days and proactive state incentives.

What is the main restraint facing scale-up?

High upfront installation costs, coupled with limited access to affordable financing, continue to restrain broader adoption.

Page last updated on: