China Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.03 Billion |

| Market Size (2026) | USD 16.87 Billion |

| Market Size (2031) | USD 20.91 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

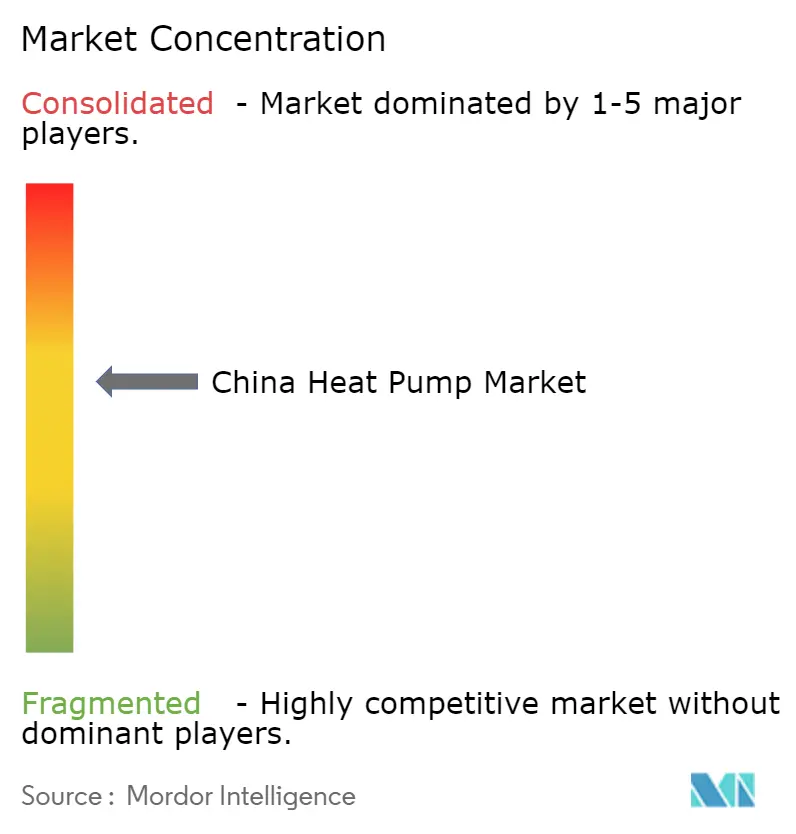

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Heat Pump Market Analysis by Mordor Intelligence

The China heat pump market size is projected to be USD 16.03 billion in 2025, USD 16.87 billion in 2026, and reach USD 20.91 billion by 2031, growing at a CAGR of 4.39% from 2026 to 2031. Converging policy mandates that displace coal, deeper coupling with renewables, and accelerating industrial decarbonization are quietly reshaping thermal energy delivery across the country. Residential renovations, district-scale retrofits, and heat-as-a-service contracts are synchronizing with next-generation compressors and natural refrigerants to lift system efficiency, while subsidy frameworks compress payback periods in both northern heating provinces and southern cooling hubs. Manufacturing clusters clustered in Guangdong, Zhejiang, and Jiangsu provinces continue to benefit from vertical integration of compressors, inverters, and controls, yet rising labor and logistics costs nudge producers to diversify inland. Competitive differentiation is increasingly tied to cold-climate performance certification, magnetic-levitation compression, and AI-enabled optimization that balances grid stress with building comfort.

Key Report Takeaways

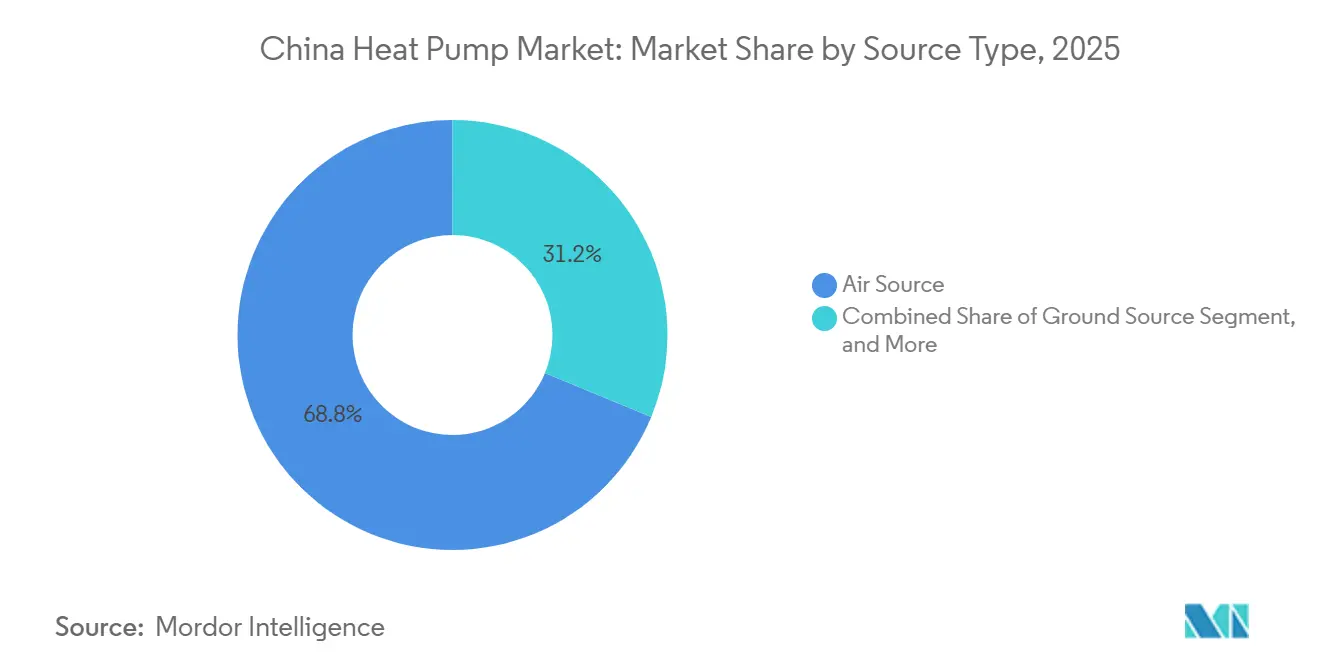

- By type, air source systems led with 68.78% revenue share in 2025, while water source solutions post the fastest 5.26% CAGR through 2031.

- By technology, air-to-water units held 46.59% of the China heat pump market share in 2025; water-to-water platforms are forecast to rise at a 4.82% CAGR to 2031.

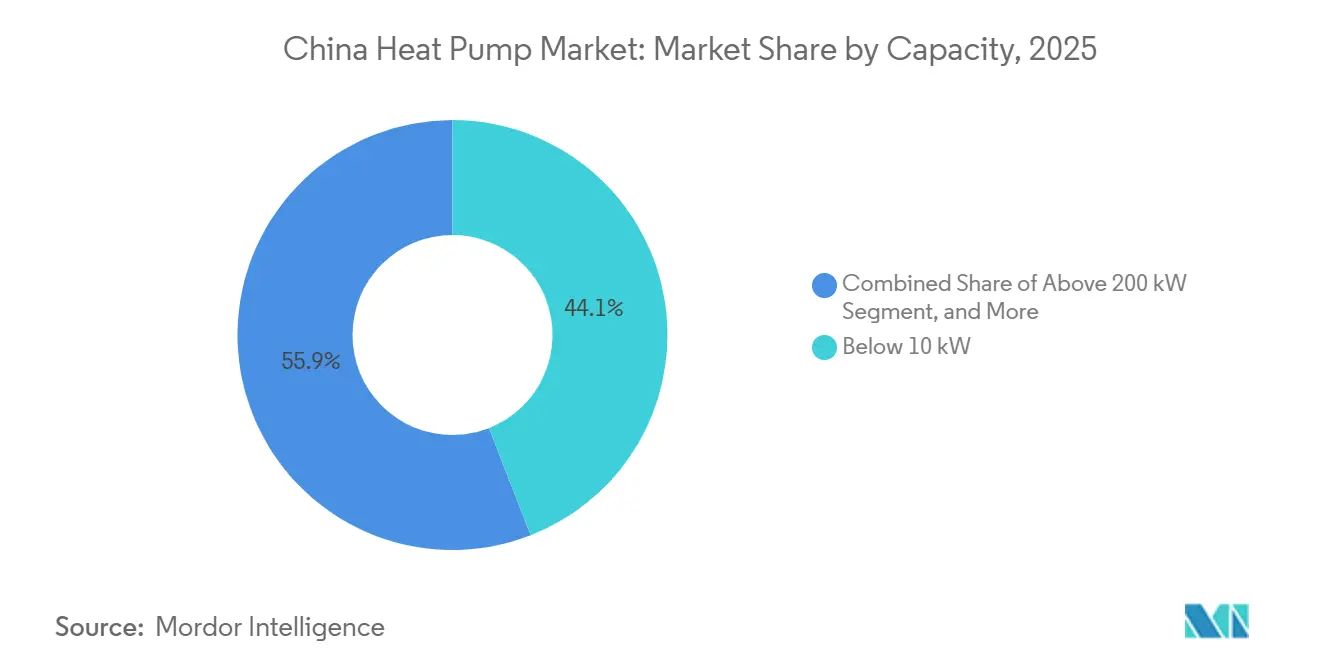

- By capacity, below 10 kW units captured 44.07% of the China heat pump market size in 2025, whereas the 10–50 kW class is expected to expand at 5.02% CAGR.

- By application, space heating controlled 54.21% share in 2025; domestic hot water is advancing fastest at 5.37% CAGR.

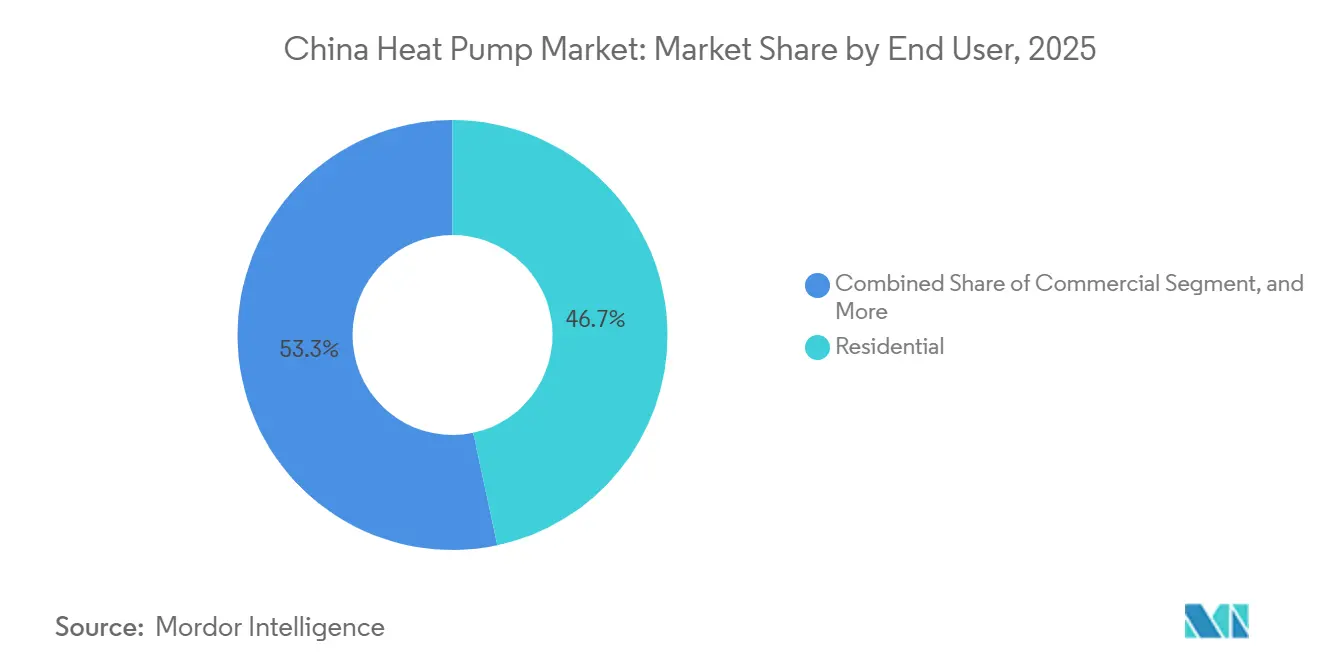

- By end user, residential customers accounted for 46.67% share in 2025, yet commercial facilities record the highest 4.86% CAGR through 2031.

- By installation, new builds dominated with 57.12% share in 2025, while retrofit activity is growing at 5.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Use of Heat Pumps Beyond Traditional Heating and Cooling Applications | +0.8% | National clusters in Yangtze River Delta and Pearl River Delta industrial parks | Medium term (2-4 years) |

| Implementation of Government Policies and Incentives to Promote Energy-Efficient Heating and Cooling Systems | +1.2% | Highest subsidy intensity in Beijing-Tianjin-Hebei, Shandong, and Henan provinces | Short term (≤ 2 years) |

| Rapid Urbanization and Construction of New Buildings | +0.7% | Tier 2 and Tier 3 cities across central and western provinces | Long term (≥ 4 years) |

| Surge in Cold-Climate Air-Source Heat Pump Deployments Enabled by -35 °C Rated Compressors | +0.6% | Northern provinces including Liaoning, Jilin, Heilongjiang, and Inner Mongolia | Medium term (2-4 years) |

| Expansion of Rural Subsidies Replacing Coal Stoves with Heat Pumps | +0.5% | Rural areas in Hebei, Shanxi, Shaanxi, Henan, and Shandong provinces | Short term (≤ 2 years) |

| Integration of Heat Pumps with Rooftop PV and Time-of-Use Tariffs Driving Self-Consumption | +0.4% | Early adoption in Jiangsu, Zhejiang, Guangdong, and Shandong provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Use of Heat Pumps Beyond Traditional Heating and Cooling Applications

Industrial process heat below 200 °C represents a sizeable but under-served opportunity for the China heat pump market, and first movers in textiles, food, and petrochemicals now validate coefficients of performance that exceed 3 for many steam processes.[1]International Energy Agency, “The Future of Heat Pumps in China,” IEA, iea.org Waste-heat-recovery installations at coal-fired units and airports showcase megawatt-scale systems that trim fuel use by two-thirds versus legacy boilers.[2]Energy Innovation, “Industrial Heat Pumps in China: Techno-Economic Analysis,” Energy Innovation, energyinnovation.org Data-center coupling projects in Chengdu demonstrate real-time balancing of server waste heat with nearby commercial loads, cutting standard-coal consumption by almost 8 kilotonnes annually. Successful pilots accelerate bankability for industrial end users that were historically skeptical of electricity-to-gas price volatility. As high-temperature compressors reach market readiness, technical headroom for 165 °C applications offers an incremental addressable market worth billions over the next decade.

Implementation of Government Policies and Incentives to Promote Energy-Efficient Heating and Cooling Systems

The May 2025 household-appliance action plan anchors subsidy streams that reimburse up to 30% of upfront costs, slashing payback periods below five years in Beijing, Hebei, and Henan.[3]National Development and Reform Commission, “Action Plan for High-Quality Development of the Household Appliance Industry,” NDRC, ndrc.gov.cn Trade-in programs direct consumer attention away from electric resistance heaters, while GB 55015 building codes mandate renewable thermal inputs above 10% for large new construction. Energy service companies harness these incentives to roll out heat-as-a-service contracts, freeing building owners from capital budgeting. Provinces also differentiate rebate levels by seasonal performance factor thresholds, nudging manufacturers to surpass baseline efficiency. Together, these carrots and sticks channel sustained demand that underpins the projected expansion of the China heat pump market.

Rapid Urbanization and Construction of New Buildings

A 66.2% urbanization rate in 2024 translates into vast floor-space additions that now specify integrated heat-pump packages straight from factory lines.[4]National Bureau of Statistics, “China Statistical Yearbook 2024,” NBS, stats.gov.cn Prefabricated modules accelerate onsite timelines and allow standardized hydraulics, reducing labor hours by double-digit percentages. District cooling schemes in Shanghai and Shenzhen deploy centralized heat-pump plants with thermal storage, shaving peak grid demand by nearly one-third while elevating system COPs above 4.5. Mixed-use towers increasingly lean on variable-refrigerant-flow networks to recycle waste heat from server rooms into adjacent retail zones. Such architectural and engineering shifts reinforce unit demand across capacity bands.

Surge in Cold-Climate Air-Source Heat Pump Deployments Enabled by -35 °C Rated Compressors

Enhanced vapor-injection and CO₂ cycles push reliable operation to -35 °C, opening north-eastern provinces to high-efficiency replacements for coal boilers.[5]Shenling Technology, “Ultra-Low-Temperature Heat Pump Portfolio,” shenling.com Haier’s Yujia X6, launched in March 2026, retains 80% heating capacity at -30 °C, signaling commercial readiness for ultra-low-temperature models. Provincial clean-heating mandates now reference GB/T 25127 performance certification, effectively disqualifying legacy units that fail to maintain output in extreme cold. Municipal pilots in Dalian document seasonal performance factors topping 3 even at deep-freeze temperatures, fostering investor confidence. Cold-climate adoption thus underpins incremental volume that helps stabilize factory utilization throughout winter.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Installation Cost and Building Retrofit Complexity | -0.5% | Most acute in Tier 3 and Tier 4 cities plus rural areas | Short term (≤ 2 years) |

| Limited Public Awareness and Certified Installer Shortage | -0.4% | Central and western provinces with under-developed training networks | Medium term (2-4 years) |

| Winter Peak-Load Constraints on Rural Grids | -0.3% | Rural districts of Hebei, Shanxi, and Inner Mongolia | Short term (≤ 2 years) |

| Uncertainty in Long-Term Electricity-to-Gas Price Ratios | -0.2% | Industrial parks relying on subsidized coal in Shanxi and Xinjiang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation Cost and Building Retrofit Complexity

Residential air-to-water systems cost three to six times more than gas boilers on a first-cost basis, and extra envelope or electrical upgrades can add another 20-40%.[6]Buildings MDPI, Jia et al., “Strategies for Mitigating Risks of Government-Led Energy Retrofitting Projects in China,” buildings, mdpi.com Retrofit projects must often replace radiators to accommodate lower supply temperatures, stretching construction timetables and disrupting occupants. Financing remains scarce outside provincial subsidies, pushing payback periods above eight years for many rural homes. Older office towers face bespoke engineering to merge new heat-pump loops with vintage chilled-water infrastructure, inflating risk premiums. These economic and technical frictions drag on the otherwise favorable growth trajectory of the China heat pump market.

Limited Public Awareness and Certified Installer Shortage

China accounts for over half of global heat-pump manufacturing jobs, yet lacks enough licensed installers to keep pace with deployment targets. Fragmented provincial certification rules hamper labor mobility, leaving cold-climate regions short-staffed during peak installation seasons. Surveys reveal that fewer than one-third of households in many Tier 3 cities can distinguish a heat pump from a standard air conditioner.[7]China Household Electrical Appliances Research Institute, “Heat Pump Awareness Survey 2024,” cheari.org Skill gaps lead to sub-optimal refrigerant charging and control setting errors that can cut realized efficiency by up to 25%. Bridging this human-capital deficit is critical for sustaining confidence in long-term savings claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Leads, Water Source Accelerates

Air source heat pumps controlled 68.78% of the China heat pump market share in 2025 as developers favored their lower upfront cost, rooftop compatibility, and limited permitting hurdles. Water source units, though still a minority, are projected to grow at a 5.26% CAGR through 2031 because district-heating companies and industrial parks can tap rivers, aquifers, or wastewater streams that deliver seasonally stable temperatures. Hybrid systems that couple air and ground loops are gaining favor in northern provinces where extreme cold can curb air source efficiency and raise grid stress, as evidenced by the 930,000 m² Xingtai Renze scheme that achieved a 3.64 COP under -19 °C ambient conditions. Policymakers have begun spotlighting these hybrid architectures as model cases, signaling regulatory tailwinds that could accelerate diversification away from single-source designs.

District heating utilities are also trialing deep-well water source loops that allow simultaneous space heating and hot-water production, boosting full-load hours and flattening seasonal revenue volatility. In Tianjin and Hebei, Sinopec’s geothermal portfolio already covers more than 120 million m², with seasonal performance factors above 4.0 after water source heat pump integration. Local officials tout these metrics to justify subsidy extensions, thereby enhancing the commercial appeal of water source technology. Although permitting for groundwater extraction remains stringent, the long operational life of well infrastructure aligns with utility investment horizons and supports steady uptake within the China heat pump market.

By Technology: Air-to-Water Platforms Anchor Low-Temperature Districts

Air-to-water platforms held 46.59% of the China heat pump market share in 2025 because fourth-generation district networks increasingly run at 35-45 °C supply temperatures that match these units’ optimal operating range. Hebei Zhaoxian’s 4.3 million m² project validated that clustered air-to-water arrays can displace coal boilers while meeting municipal comfort standards. Water-to-water machines leverage stable geothermal or industrial waste-heat sources to deliver COPs above 5, especially in textile and food parks where simultaneous chilling and heating improve process economics. Ground-to-water units remain niche because drilling costs and groundwater regulations elevate project complexity, but universities and hospitals adopt them for their 50-year exchanger lifespan and immunity to outdoor temperature swings.

Southern provinces still prefer air-to-air heat pumps for cooling-led climates that lack hydronic distribution, yet policy incentives are nudging developers to specify dual coils so systems can upgrade to air-to-water when future retrofits add radiant flooring. Water-to-water penetration is aided by national subsidies that reward simultaneous production of chilled and hot water, improving annualized asset utilization. As the China heat pump market size grows, manufacturers are adding smart controls that let buildings switch dynamically among air, water, and ground sources based on tariff windows and outdoor conditions. This control sophistication boosts seasonal performance factors and reinforces the value proposition of multi-source technology stacks.

By Capacity: Mid-Range Units Ride Commercial Retrofit Wave

Heat pumps under 10 kW captured 44.07% of the China heat pump market size in 2025 because urban apartments and single-family homes demand compact, standardized packages. Demand is tilting toward 10-50 kW units, which are poised to expand at a 5.02% CAGR as malls, schools, and office towers overhaul legacy HVAC and seek modular rooftop replacements that minimize downtime. A Shanxi complex retrofit that added eight 45 kW air-source machines cut energy bills by 20%, reinforcing the payback narrative for mid-range systems. Units above 200 kW remain a specialized slice serving industrial loops and district substations, but custom lead times and factory-commissioning needs limit near-term volume upside.

Below-10 kW devices continue to benefit from mass-production economies that compress cost curves, yet installers report rising interest in 15-30 kW models because mixed-use buildings prefer a handful of larger units over scores of small ones. Suppliers are responding with stackable frames and quick-connect hydraulics that ease craning and wiring on constrained rooftops. For mega-watt projects, designers increasingly deploy arrays of 100 kW modules rather than single monoliths, allowing phased capacity additions in step with floor-space occupancy. This modular approach shortens permitting cycles and supports flexible financing, enhancing market resilience across all capacity tiers.

By Application: Domestic Hot Water Outpaces Space Heating

Space heating accounted for 54.21% of installations in 2025, reflecting northern provinces’ push to replace coal boilers under clean-heating mandates. Domestic and sanitary hot-water applications are projected to grow fastest at 5.37% CAGR as national trade-in subsidies steer households away from electric resistance heaters that carry higher operating costs. In southern provinces, dual-purpose heat pumps replace separate chillers and boilers, simplifying mechanical rooms and reducing maintenance contracts. Industrial process heating remains a smaller slice but is expanding steadily because high-temperature compressors now deliver 80-165 °C steam at COPs of 2.2-3.7, slicing fuel bills by roughly two-thirds in textiles and food processing-.

Swimming-pool heating and greenhouse climate control form niche pockets that grow as component prices fall and installers gain familiarity with specialized defrost cycles. Municipal engineering bureaus increasingly mandate that new residential towers include central heat-pump water heaters feeding smart sub-meters, a move that centralizes maintenance and eases tariff management. Commercial landlords highlight reduced legionella risk because heat pumps maintain stable tank temperatures above 55 °C without direct combustion. Such multipronged benefits keep domestic hot-water upgrades high on retrofit agendas and reinforce year-round load factors that stabilize revenue streams for service providers in the China heat pump industry.

By End User: Commercial Share Rises via Heat-as-a-Service Contracts

Residential buyers held 46.67% share in 2025 because coal-to-electricity programs reimbursed up to 50% of installed cost in northern provinces, accelerating apartment retrofits. Commercial buildings are expected to post a 4.86% CAGR through 2031 as energy-service companies roll out heat-as-a-service contracts that bundle equipment, electricity, and maintenance into a single kilowatt-hour tariff. Office towers, hotels, and malls retrofit variable-refrigerant-flow systems capable of simultaneous heating and cooling, recovering waste heat from kitchens and server rooms to warm adjacent zones. Industrial uptake remains cautious, yet pilot projects in petrochemicals and pulp demonstrate that heat pumps can reliably generate 150 °C steam and achieve three-year paybacks when paired with waste-heat streams.

Educational campuses and hospitals are fast-growing institutional niches because administrators prioritize indoor-air quality and carbon reporting. Retail chains deploy standardized rooftop packages to simplify procurement across multiple sites, creating volume contracts that improve supplier economics. Meanwhile, residential momentum is spreading southward as households recognize lifecycle savings from replacing air conditioners plus electric heaters with one integrated unit. This broader adoption base cushions suppliers against cyclic swings in any single end-user segment and diversifies revenue for the China heat pump market.

By Installation: Retrofits Edge Ahead on Carbon-Peaking Targets

New construction represented 57.12% of 2025 installations because green-building codes embed renewable-thermal targets at the design stage, making heat pumps a default specification. Retrofit demand is forecast to climb 5.06% annually as municipalities prioritize existing stock to meet 2030 carbon-peaking goals, channeling subsidies toward envelope upgrades and panel-board expansions that accommodate heat-pump loads. Heritage facades that restrict exterior alterations favor slim split units or shared hydronic risers, while rural homes often need electrical rewiring before equipment can be energized. The Xingtai Renze project bundled financing, engineering, and operation into a single public-private partnership, proving that third-party business models can surmount homeowner cash-flow hurdles.

Developers of new residential towers integrate central air-to-water systems feeding floor coils, enabling builders to market “all-season comfort” as a lifestyle amenity. Retrofit contractors increasingly stage work during shoulder seasons to minimize tenant disruption, using pre-fabricated piping modules that clamp onto existing risers. Grid operators encourage nighttime commissioning schedules so installers can verify defrost and load-shift functions under low-tariff windows, aligning with broader demand-response programs. These practical tweaks reduce project risk and help retrofit volume close the gap with new-build activity, securing a balanced growth trajectory for the China heat pump market.

Geography Analysis

Northern provinces generated the largest share of the China heat pump market in 2025 because mandatory clean-heating mandates replaced coal boilers across Beijing-Tianjin-Hebei, Shandong, and Henan. Municipal projects, such as Hebei Zhaoxian’s multi-million-square-meter cluster, highlight how air-source arrays can anchor district heating while using off-peak electricity and renewable inputs. Cold-climate certification requirements also catalyze demand for ultra-low-temperature compressors, drawing manufacturers from Zhejiang and Jiangsu to develop –35 °C models.

The Pearl River Delta remains the manufacturing engine, with Guangdong hosting over 70 % of producers and commanding 34 % of national air-source shipments. Foshan and Guangzhou plants integrate inverter drives, IoT controllers, and R290 refrigerant charging on single assembly lines, shortening lead times for both domestic and export orders. Western growth corridors in Sichuan and Chongqing benefit from rapid urbanization and data-center construction, where integrated energy centers merge ground-source loops with server waste heat to cut greenhouse-gas intensity.

Rural districts receive targeted subsidies to swap coal stoves for heat pumps, yet winter peak load constrains undersized distribution grids in Hebei, Shanxi, and Inner Mongolia. Studies show decentralized air-source units can raise low-voltage feeder saturation by 40 % on cold evenings, pressing distribution companies to parallel battery storage or phase retrofits to off-peak seasons. Export-oriented makers increasingly ship CE-certified air-to-water units to Europe, leveraging cost advantages and production scale that solidify China’s role as a global supply hub.

Competitive Landscape

Domestic leaders Midea, Gree, and Haier collectively control roughly 45 % of shipments, yet more than 300 additional manufacturers ensure price pressure remains intense. Haier’s Jiaozhou complex, designed for 5 million units annually, exemplifies the aggressive capacity race that could squeeze margins across mid-range residential models. Vertical integration gives local champions control of compressors, inverters, and even refrigerant filling, insulating them from supply shocks while enabling rapid design iterations tailored to subsidy program thresholds.

International brands like Daikin, Mitsubishi Electric, and Carrier pursue joint ventures to localize swing-rotary compressors and navigate evolving Chinese refrigerant guidelines. The December 2025 Copeland–Daikin agreement to produce inverter swing-rotary compressors for propane heat pumps showcases cross-border technology sharing aimed at both Chinese and European markets. Niche specialists such as PHNIX, Shenling, and OUTES carve out positions in cold-climate and natural-refrigerant niches, exporting CE-certified models that meet European Eco-design benchmarks.

Technology frontiers extend to magnetic-levitation compression, foil-bearing centrifugal units, and AI-driven predictive maintenance. Rena Intelligence’s USD 238 million magnetic-levitation plant and Garrett Motion’s foil-bearing compressor deal with Cling indicate how players from broader HVAC and automotive sectors are entering the value chain. Intellectual-property filings that couple multi-energy controls with hybrid source architectures signal that software orchestration and grid interactivity will become decisive differentiators in the next growth cycle of the China heat pump market.

China Heat Pump Industry Leaders

Gree Electric Appliances

Midea Group

Haier Group

PHNIX Eco-energy Solution Ltd.

SPRSUN

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Haier launched the Yujia X6 central air-conditioning system, engineered for -37 °C to 67 °C operation and aimed at cold-climate retrofits.

- March 2026: Xiaomi debuted the Mi Home central air-conditioning platform with AI-optimized dual-cylinder compression, marking its first foray into heat pumps.

- February 2026: PHNIX introduced the airMono indoor monobloc R290 heat pump at ISH China and CIHE 2025, targeting space-constrained urban apartments.

- February 2026: Garrett Motion secured a serial-production award from Cling for oil-free foil-bearing centrifugal E-Cooling compressors, with volume output from 2027.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China heat-pump market as all factory-built air, water, and ground-source systems, rated below 100 kW, as well as larger commercial units that provide space heating, cooling, or sanitary hot water in buildings or light-industrial processes.

Scope exclusion: stand-alone heat-pump water heaters sold as white goods and integrated HVAC chillers are not counted.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts completed structured interviews with Chinese OEM engineers, provincial energy-efficiency officials, tier-1 distributor managers in Jiangsu and Guangdong, and certified installers serving retrofit programs in Beijing's coal-to-electricity corridor. These conversations clarified subsidy uptake rates, real-world seasonal performance, and channel mark-ups that are seldom published.

Desk Research

We extracted baseline volumes, prices, and building stock from publicly available sources such as the National Bureau of Statistics of China, the China Heat Pump Alliance, the Ministry of Housing and Urban-Rural Development's green-building database, General Administration of Customs shipment records, and peer-reviewed work from Tsinghua University. Macro indicators, tariff trends, and carbon targets were screened in IEA and World Bank datasets, while company financials were verified through D&B Hoovers and Dow Jones Factiva. The references above illustrate, but do not exhaust, the wider pool of secondary inputs consulted.

Market-Sizing & Forecasting

We begin with a top-down reconstruction that scales national production and export statistics to an in-country demand pool, corrected for inventory flow and average selling price. Results are then cross-checked against a bottom-up slice drawn from sampled supplier revenues and distributor throughput. Key variables like annual housing completions, heating-degree days, utility tariff differentials, provincial rebate budgets, and unit COP progression feed a multivariate regression that projects value and volume to 2030. Gaps in bottom-up data, for example, for small rural installers, are bridged using distributor penetration proxies validated in field calls.

Data Validation & Update Cycle

Outputs pass a three-level analyst review; anomaly screens flag any variance above two standard deviations, and findings are re-circulated to selected interviewees for sense-checks. The model is refreshed every twelve months, with interim updates triggered by new subsidy rules or major pricing shifts, ensuring clients receive the latest view.

Why Mordor's China Heat Pump Baseline stands strong in China

Published estimates often differ; scope, pricing assumptions, and refresh cadence rarely align.

Key gap drivers here include: some publishers bundle dedicated heat-pump water heaters or industrial systems above 100 kW, others use conservative ASP progressions that ignore recent R290 models, and several rely on pre-2023 unit-shipment ratios despite the 14th Five-Year retrofit surge. Mordor's definition, annual refresh, and dual-track validation reduce such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.03 B (2025) | Mordor Intelligence | - |

| USD 29.9 B (2024) | Regional Consultancy A | Includes standalone HP water heaters and industrial units >100 kW; ASP derived from Asia-Pacific averages |

| USD 13.9 B (2024) | Trade Journal B | Excludes geothermal segment and retrofit sales; relies on 2022 price benchmarks |

Taken together, the comparison shows that when variables and boundaries are aligned, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to verifiable statistics and repeatable steps.

Key Questions Answered in the Report

How large will China's heat pump market be by 2031?

It is projected to reach USD 20.91 billion by 2031, expanding at a 4.39 % CAGR from 2026.

Which segment is growing fastest within China's heat pump universe?

Water source units post the highest 5.26 % CAGR, propelled by district-heating and waste-heat projects.

Are heat pumps viable for cold northern provinces?

Yes, new ultra-low-temperature compressors sustain 80 % capacity at -30 °C, enabling widespread northern adoption.

What business model is unlocking commercial uptake?

Heat-as-a-service contracts let building owners pay per kilowatt-hour while third-party operators finance equipment.

How does government policy influence purchase decisions?

Subsidies covering up to 30 % of installed cost and mandatory renewable-energy codes make heat pumps the default in many large projects.

What challenges could slow industrial adoption?

High upfront costs and uncertainty over future electricity-to-gas price ratios present headwinds for process-heat applications.

Page last updated on: