Malaysia Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

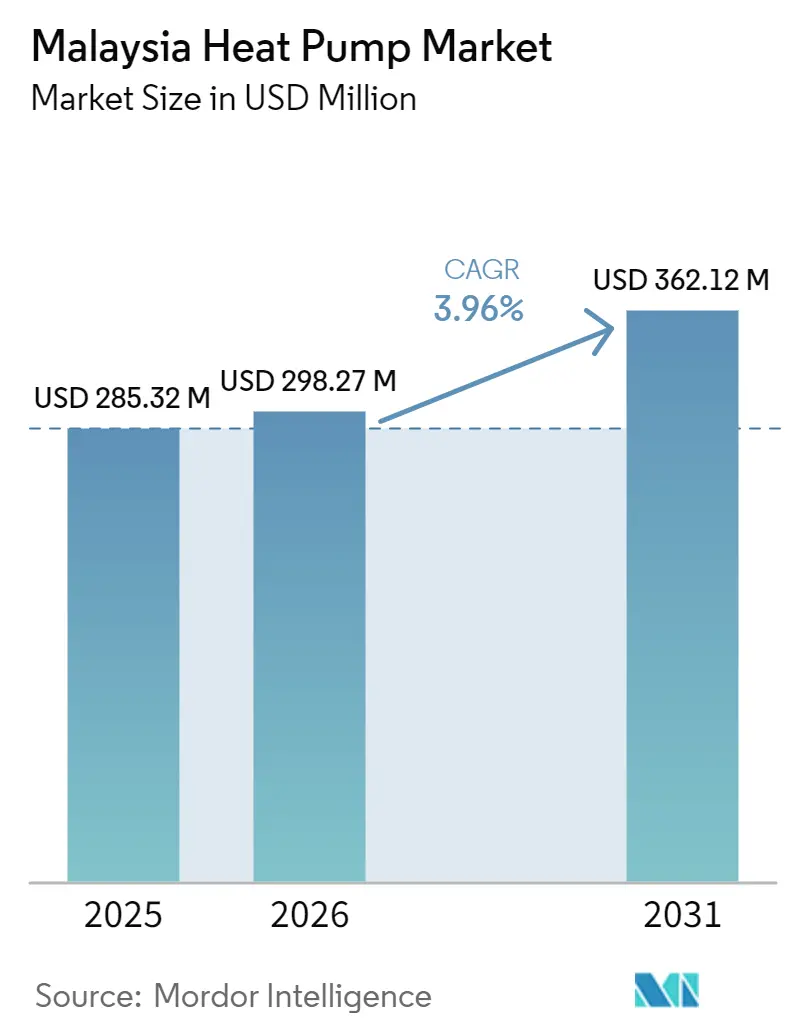

| Base Year Market Size (2025) | USD 285.32 Million |

| Market Size (2025) | USD 298.27 Million |

| Market Size (2030) | USD 362.12 Million |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Heat Pump Market Analysis by Mordor Intelligence

The Malaysia heat pump market size is projected to expand from USD 285.32 million in 2025 and USD 298.27 million in 2026 to USD 362.12 million by 2031, registering a CAGR of 3.96% between 2026 to 2031. Robust electricity-tariff growth, refrigerant phase-out mandates, and an accelerating pipeline of data-center projects are reshaping equipment-selection criteria across commercial and industrial facilities. Buyers now weigh lifecycle operating costs and carbon footprints as heavily as upfront price, which is lifting demand for high-efficiency, inverter-driven systems that rely on natural or low-GWP refrigerants. Tightening green-building standards, especially GreenRE Platinum and Green Building Index certification, further reinforce the switch to integrated chiller-heat-pump solutions. Global manufacturers with Malaysian assembly plants enjoy delivery lead-time and service-quality advantages, yet Chinese brands are gaining traction by pairing aggressive pricing with turnkey installation packages.

Key Report Takeaways

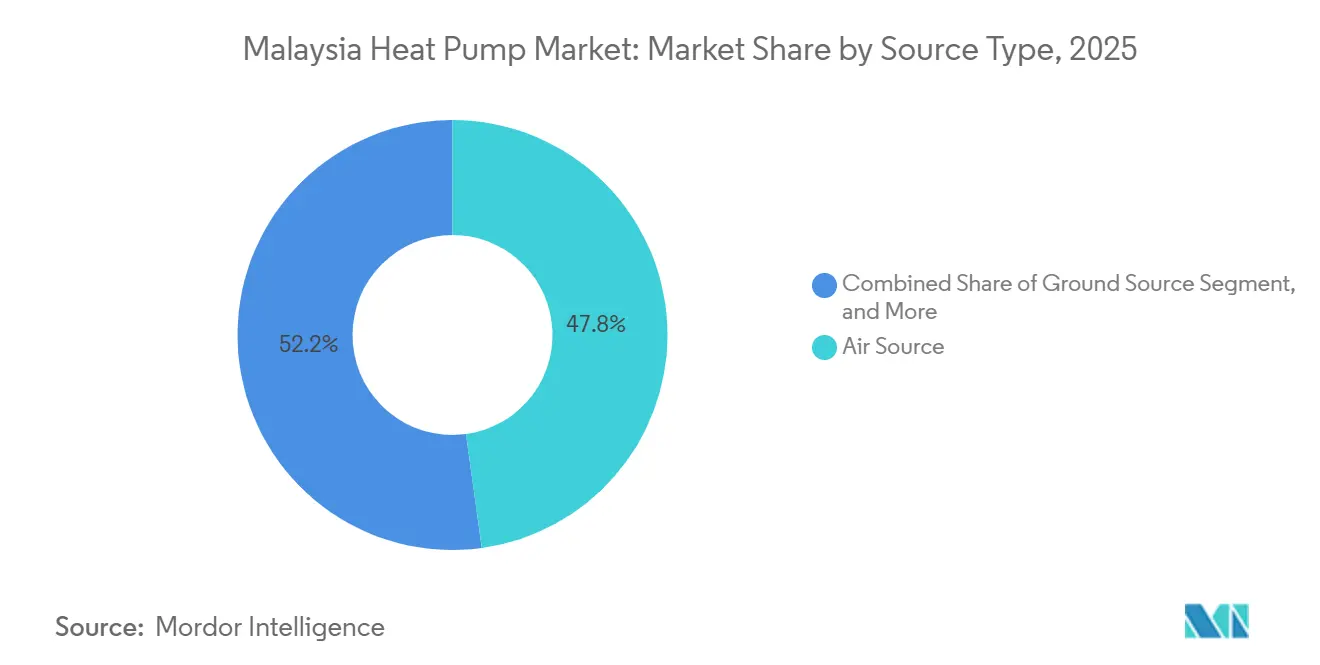

- By source, air source units captured 47.83% of Malaysia heat pump market share in 2025, while hybrid systems are forecast to expand at a 4.82% CAGR through 2031.

- By application, space cooling accounted for 41.78% of 2025 demand, whereas industrial and process heating is advancing at a 5.02% CAGR to 2031.

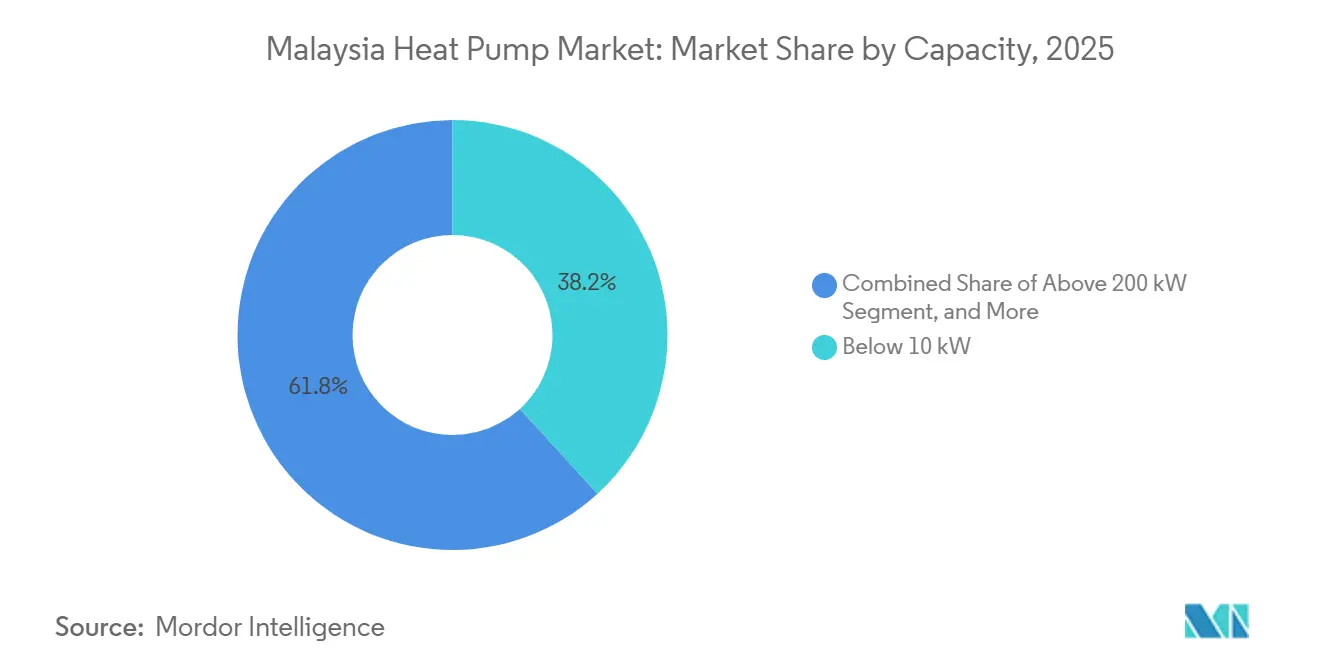

- by capacity, below-10 kW systems led with 38.23% revenue share in 2025; above-200 kW installations are projected to grow at a 4.51% CAGR.

- By technology, air-to-air technology held 40.31% of Malaysia heat pump market size in 2025, whereas ground-to-water solutions are set to register a 4.39% CAGR.

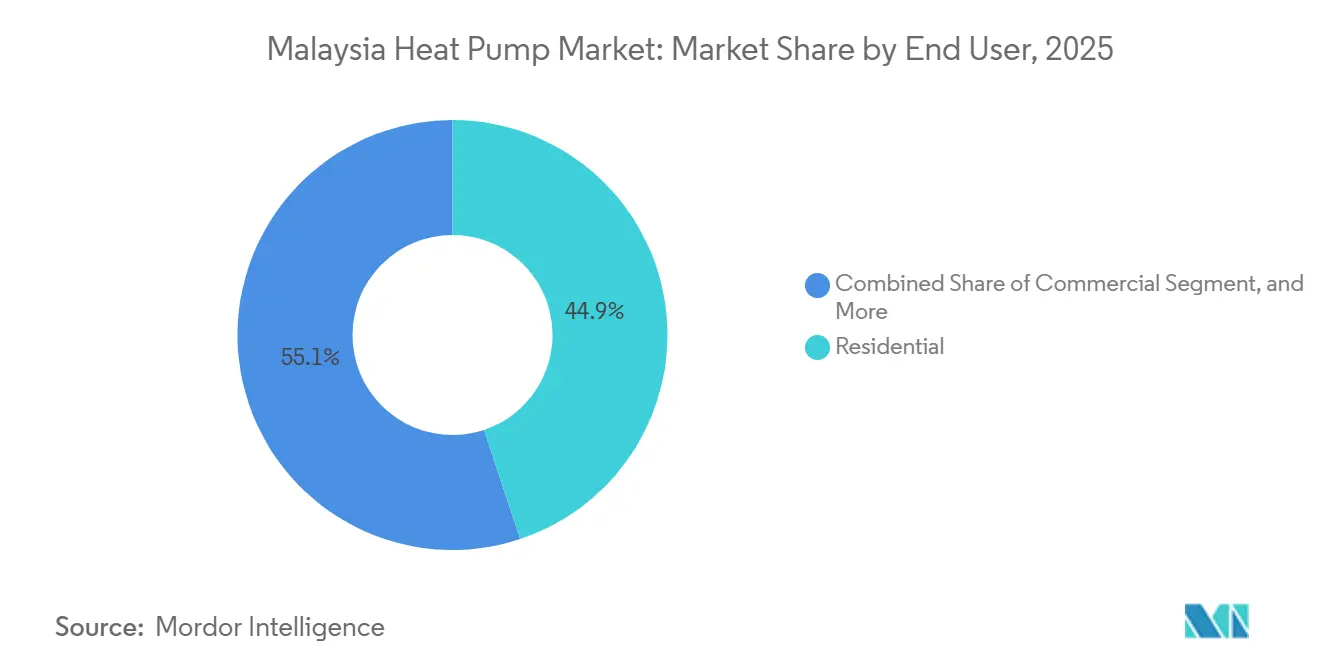

- By end user, residential users represented 44.89% of 2025 sales, yet the commercial segment is on track for a 4.24% CAGR amid green-building mandates.

- By installation, new-build projects commanded 47.91% of installations in 2025 and are poised to rise at a 4.12% CAGR as developers embed heat-pump readiness at design stage.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of Heat Pump Water Heaters in Tropical Climates | +0.9% | National focus on Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| Implementation of Green Technology Financing Scheme 3.0 | +0.7% | Nationwide, led by Malaysian Green Technology and Climate Change Corporation | Short term (≤ 2 years) |

| Rising Electricity Tariffs Driving Shift to High-Efficiency HVAC | +0.6% | Nationwide, most acute for power-intensive users | Short term (≤ 2 years) |

| Mandated Phase-Out of R22 Refrigerant in 2027 | +0.5% | Nationwide under HCFC Phase-out Plan Stage III | Medium term (2-4 years) |

| Growing Demand from Data Centers for Precision Cooling | +0.5% | Johor, Penang, Cyberjaya | Medium term (2-4 years) |

| Increase in Net-Zero Building Certifications | +0.4% | Klang Valley, Penang, Johor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Heat Pump Water Heaters in Tropical Climates

High ambient temperatures above 26 °C enable air-source heat-pump water heaters to deliver coefficients of performance exceeding 4.0, translating into 60-75% electricity savings compared with resistance heaters. Field trials showed Rheem’s RHP-5207C at 4.2 COP and Summer A-TEC’s R290 model at 4.45 COP, demonstrating a clear efficiency edge for natural-refrigerant units. Hotels and hospitals, which devote 15-20% of operating budgets to hot water, are accelerating retrofits, as evidenced by Carrier Malaysia’s five-year agreement with Pelaburan Hartanah Berhad to upgrade 24 buildings nationwide. Residential uptake remains price sensitive, but a USD 15 million federal rebate pool and planned 2026 appliance efficiency standards shorten payback periods to below 4 years, widening the addressable base for landed homes.[1]Carrier Malaysia, “Carrier Announces Collaboration with Pelaburan Hartanah to Enhance Energy Efficiency and Operational Optimization,” carrier.com

Implementation of Green Technology Financing Scheme 3.0

Green Technology Financing Scheme 3.0 offers a 2% interest subsidy and a 60% federal guarantee on loans up to MLR 100 million (USD 24 million), trimming capital costs for large commercial heat-pump projects.[2]R. Sekaran, “Penang Charges Forward With New Renewable Energy Guidelines,” The Star, thestar.com.my Penang extended the concept with a state-level Climate Mitigation Fund in October 2025, unlocking blended finance that improves project internal rates of return by 150-200 basis points. Longer loan tenors of 10-12 years now align amortization schedules with equipment lifecycles, encouraging ground-source and high-capacity installations. The funding framework is accelerating rollout of centralized chiller-heat-pump plants in manufacturing, hospitality, and healthcare complexes, making Malaysia heat pump market adoption less dependent on developer balance-sheet strength.

Rising Electricity Tariffs Driving Shift to High-Efficiency HVAC

Tenaga Nasional Berhad’s 14.2% tariff hike in July 2025, together with a monthly Automatic Fuel Adjustment mechanism, created double-digit bill volatility for medium- and high-voltage customers. Heat pumps that achieve seasonal energy efficiency ratios above 4.0 can curb annual cooling and heating consumption by 40-50%, saving commercial buildings USD 12,000-49,000 per year.[3]LG Electronics, “LG Malaysia Transforms HVAC Landscape With AI-Driven Innovation,” lg.com Data-center operators in Johor face 10-14% cost jumps yet still benefit from Asia-Pacific’s third-lowest power prices, reinforcing a pivot to liquid-cooling heat-pump systems that reclaim waste heat for offices. Manufacturers now rank energy efficiency alongside uptime in procurement scorecards, expanding Malaysia heat pump market penetration.

Mandated Phase-Out of R22 Refrigerant in 2027

Malaysia’s commitment under the Kigali Amendment phases out HCFCs by 2030, with steep R22 quota cuts from 2027. Operators of legacy equipment must upgrade to R32 or R290 systems to remain compliant, driving retrofit waves across malls, hotels, and factories. Viessmann’s R290 Vitocal line offers GWP 3 versus 1,810 for R22, positioning natural-refrigerant heat pumps as a future-proof choice. Upcoming 2026 Minimum Energy Performance Standards will bar low-efficiency units, accelerating turnover toward inverter-driven heat pumps in the Malaysia heat pump market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for Ground-Source Systems | -0.6% | Nationwide, acute outside Klang Valley | Medium term (2-4 years) |

| Limited Skilled Installers Outside Klang Valley | -0.4% | Penang, Johor, Sabah, Sarawak | Short term (≤ 2 years) |

| Intermittent Policy Enforcement Reducing Investor Confidence | -0.3% | Nationwide | Long term (≥ 4 years) |

| Low Awareness Among Residential Consumers of Lifecycle Savings | -0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for Ground-Source Systems

Ground-source installations cost MLR 150,000-400,000 (USD 36,000-97,000) for a 50 kW system, more than double an equivalent air-source setup. Tropical soils have thermal conductivity around 1.1 W·m⁻¹·°C⁻¹, 30-40% below temperate benchmarks, forcing oversized borehole arrays that inflate costs and extend payback to 10-15 years. Year-round cooling loads raise ground temperatures, eroding long-term efficiency unless hybrid rejection fields are added, which further boosts capital outlay. As a result, only institutional campuses and grant-backed pilot projects currently opt for ground-source designs, limiting this slice of Malaysia heat pump market growth.

Limited Skilled Installers Outside Klang Valley

Heat pump deployment demands competencies in variable-speed compressors, low-GWP refrigerant safety, and building-automation integration, yet vocational programs remain concentrated near Kuala Lumpur. Contractors in Penang, Johor, Sabah, and Sarawak often lack R290 certification, elongating commissioning timelines and raising service costs as manufacturers fly technicians from Peninsular Malaysia.[4]International Energy Agency, “Malaysia Energy Policy Review 2025,” IEA, iea.org The skill shortage hampers reliability perceptions among property owners, particularly for complex retrofits, and acts as a brake on Malaysia heat pump market adoption in secondary cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Designs Strengthen Seasonal Performance

Air-source units captured 47.83% of Malaysia heat pump market share in 2025, reflecting the segment’s lower capital intensity, small physical footprint, and ability to slot into split-system infrastructure in dense urban buildings. Hybrid configurations that marry air-source evaporators with ground- or water-loop heat rejection are projected to grow at a 4.82% CAGR through 2031, driven by industrial operators and hyperscale data-center builders that need to stabilize coefficients of performance during monsoon humidity spikes. The hybrid approach also cuts defrost-cycle energy penalties, extends compressor life, and eases grid-demand peaks, a trio of benefits that resonates with owners now facing time-of-use tariffs.

System integrators increasingly bundle modular chillers, liquid coolers, and supervisory controls so facility managers can toggle between air and ground loops in real time. Data-center designers in Johor specify dual-path cooling trains so that maintenance on outdoor coils never jeopardizes rack uptime. Industrial estates in Penang replicate the template by tapping shared bore-fields to trim plant steam bills while retaining air-source redundancy for shutdown periods. As grid regulators publish stricter seasonal-efficiency indices, the hybrid cohort is expected to chip away at the dominant air-source position, broadening Malaysia heat pump market penetration across process-critical facilities.

By Technology: Ground-to-Water Moves From Pilot To Plant Floor

Air-to-air technology accounted for 40.31% of Malaysia heat pump market size in 2025 because residential and light-commercial buyers prize easy installation and ductless flexibility. Ground-to-water systems are forecast to advance at a 4.39% CAGR to 2031 as manufacturers retrofit closed-loop heat exchangers that pre-heat boiler feedwater or supply low-grade process heat. Natural-refrigerant units using R290 or R32 help industrial users hedge against the 2027 R22 ban while unlocking Scope-1 emission cuts.

Industrial parks now rough-in bore-fields during site grading, spreading drilling costs across multiple tenants and shortening project payback windows. Early adopters in palm-oil refining use ground-to-water modules to lift condensate from 50 °C to 80 °C, trimming natural-gas use without re-engineering existing steam headers. Hotel chains, meanwhile, lean on air-to-water packages to meet hot-water loads at COPs above 4.0, replacing electric resistance heaters that once soaked up 15-20% of operating budgets. As local production of compressors and plate heat exchangers expands, technology choice will hinge less on import lead times and more on plant-specific thermal profiles, cementing ground-to-water as a mainstream option.

By Capacity: Large-Class Units Ride The Data-Center Wave

Units below 10 kW represented 38.23% of shipments in 2025, anchored by single-family water heaters and ductless mini-splits. Above-200 kW equipment is set to climb at a 4.51% CAGR because Johor’s hyperscale campuses demand precision liquid cooling that can reclaim rack heat for office conditioning or district loops. The 10-50 kW slice services shop-houses, clinics, and condos, while 50-200 kW machines anchor mid-rise offices and schools.

Campus-scale buyers increasingly issue framework tenders that bundle multi-megawatt heat pumps, thermal-storage tanks, and intelligent dispatch software. OEMs answer with factory-built skids that integrate redundant variable-speed compressors and power-quality monitoring, a design that slashes site labor. For investors, the jump from sub-10 kW to triple-digit capacities magnifies tariff-related savings, reinforcing large-class growth and reshaping Malaysia heat pump market economics toward utility-scale orders rather than retail-style transactions.

By Application: Process Heat Becomes The New Growth Engine

Space cooling held 41.78% of demand in 2025, unsurprising in a tropical climate where indoor comfort is a year-round necessity. Industrial and process heating, however, is projected to expand at a 5.02% CAGR as factories retrofit waste-heat capture loops that elevate condensate or exhaust streams to usable temperatures. This shift trims fossil-fuel bills, earns carbon credits, and frees up boiler capacity for peak output periods.

Palm-oil refineries, oleochemical plants, and food processors pilot modular heat-pump skids that dovetail with existing heat-exchanger banks. Hospitals and hotels, meanwhile, deploy central plants that alternate between chilled-water and hot-water production on a 24-hour cycle, squeezing extra utilization out of shared compressors. As tariff volatility persists and carbon-pricing schemes inch closer, the process-heating niche is expected to widen, giving Malaysia heat pump market size an incremental lift beyond the traditional comfort-cooling baseline.

By End User: Commercial Buyers Accelerate Under Green Mandates

Residential users claimed 44.89% of 2025 sales, propelled by rebates that cut upfront price tags on heat-pump water heaters for landed homes. The commercial segment is forecast to grow at a 4.24% CAGR thanks to stricter GreenRE and Green Building Index thresholds that force hotels, malls, and private hospitals to curb energy-use intensity. Facility owners now regard inverter-driven heat pumps as a compliance shortcut that also shields against tariff spikes.

Office landlords in Kuala Lumpur retrofit chilled-water plants with heat-pump modules to achieve double-digit efficiency gains without gutting tenant spaces. Retail developers pair rooftop solar arrays with centralized heat-pump hot-water systems, a move that monetizes self-consumed PV output during midday peaks. Industrial estates adopt an energy-as-a-service model, outsourcing plant upkeep to vendors that guarantee performance across 10-15-year terms. Together, these patterns shift value away from one-off equipment sales and toward lifecycle service contracts that expand Malaysia heat pump market share for service-savvy OEMs.

By Installation: New-Build Designs Embed Heat-Pump Readiness

New construction commanded 47.91% of 2025 installations and is on course for a 4.12% CAGR because architects now specify oversized electrical risers, dedicated plantrooms, and smart-metering nodes during schematic design. Early coordination reduces change-orders, trims commissioning windows, and locks in full-load efficiencies that exceed retrofit results.

Retrofit projects still battle shallow ceiling plenums, undersized switchgear, and the need to preserve tenant operations, raising costs by 20-30% versus greenfield work. Yet a wave of 1990s office towers nearing chiller end-of-life provides a captive pipeline, especially in Klang Valley and Penang. Performance-guaranteed service contracts reassure owners about payback, and Green Technology Financing Scheme 3.0 lowers borrowing costs, easing retrofit hesitancy. Longer term, a mandatory energy-audit regime could tilt even more square footage toward upgrade, further enlarging Malaysia heat pump market size through 2031.

Geography Analysis

Klang Valley concentrates the bulk of Grade A offices and private hospitals and therefore leads Malaysia heat pump market adoption, aided by Daikin’s enlarged Shah Alam R&D and future applied-factory complex that will tailor systems for humid tropical conditions. Continuous investment in photovoltaic rooftop arrays, such as Panasonic’s 9.2 MW system, cuts manufacturing carbon intensity and underpins local supply of air-to-water equipment.

Johor is emerging as the nation’s data-center nucleus with 42 approved projects in second-quarter 2025 alone. Ibrahim Technopolis and Sedenak’s 7,618 acres of tech-dedicated land, backed by 500 kV grid infrastructure, attract hyperscale builders that deploy large-capacity heat pumps for liquid cooling. Vertiv’s new Johor plant, slated to open in 2026, will add regional manufacturing depth for precision-cooling skids that serve the Malaysia heat pump market and neighboring economies.

Penang leverages stringent rooftop solar mandates and industrial-park expansions to broaden its heat-pump footprint. Silicon Island’s Green Tech Park, designed for 100% renewable power, embeds heat-pump readiness in every lot, while Penang Technology Park allocates 200 MVA base power to anchor OEM assembly lines. Sabah and Sarawak lag due to scarce certified installers and smaller commercial pipelines, yet oil-and-gas projects and palm-oil mills provide isolated opportunities for industrial-scale heat pumps, foreshadowing gradual east-Malaysia uptake in the later forecast horizon.

Competitive Landscape

Japanese majors Daikin, Panasonic, and Mitsubishi Electric anchor manufacturing in Selangor, using local compressor and coil lines to tailor equipment for high humidity while slashing import duties. Their proximity to Klang Valley’s engineering talent enables rapid firmware tweaks when building codes tighten, a responsiveness that sustains premium price points. European specialists Viessmann, NIBE, and Stiebel Eltron focus on institutional retrofits that demand natural-refrigerant units, digital twin modeling, and long warranty windows, carving out a high-margin niche despite smaller shipment volumes.

Chinese challengers PHNIX, Midea, and Shenling widen market access by bundling competitively priced hardware with turnkey install and five-year service clauses, tactics that appeal to budget-sensitive property developers in Sabah and Sarawak. Shenling’s Johor hub assembles modular liquid-cooling skids for data centers, letting the firm promise 48-hour part delivery and undercut freight costs faced by offshore rivals. Midea rides a dealer network that cross-sells household air-conditioners and small heat-pump water heaters to capture the residential upgrade cycle.

Technology rivalry now pivots on digital controls, low-GWP refrigerants, and subscription pricing. LG’s DUALCOOL AI platform uses built-in metering and cloud analytics to enforce demand caps during peak tariffs, while its Subscription program converts capital purchases into operating leases with guaranteed seasonal-efficiency ratios. Panasonic answers with heat-pump units produced using 9.2 MW of on-site solar, enabling buyers to tag equipment as low-embodied-carbon for ESG disclosures. Viessmann pushes propane-charged heat pumps that sidestep future refrigerant bans, banking on early-mover advantage as Malaysia heat pump market migrates toward natural gases.

Service depth is fast becoming a decisive differentiator. Daikin’s planned Shah Alam applied-factory will ship large-tonnage modules with embedded condition-monitoring sensors that feed into a Klang Valley service cloud staffed by multilingual engineers. Vertiv’s forthcoming Johor plant extends the same philosophy to precision cooling, integrating power-quality analytics that spot harmonic distortion before it de-rates compressor output. Collectively, these investments point to a market where reliable after-sales support and data-driven performance guarantees matter as much as nameplate efficiency, sustaining moderate concentration while keeping competitive pressure high.

Malaysia Heat Pump Industry Leaders

Stiebel Eltron GmbH & Co. KG

Viessmann Climate Solutions SE

Glen Dimplex Group

PHNIX Eco-Energy Solution Ltd.

WaterFurnace International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Vertiv unveiled plans for a Johor plant to manufacture power and cooling equipment for high-density data-center and AI workloads, aiming for first output in early 2026.

- March 2026: KJTS Group acquired 70.67% of iHandal Holdings for MLR 10.1 million (USD 24.2 million), integrating the Heatfuse waste-heat recovery platform into its Energy-as-a-Service portfolio.

- February 2026: Daikin committed up to MLR 800 million (USD 192 million) over five years to expand its Sungai Buloh R&D hub and construct a commercial applied-air-conditioning factory in Shah Alam.

- February 2026: Vantage Data Centers confirmed a USD 1.6 billion investment to build a 300 MW hyperscale campus in Sedenak Tech Park, Johor.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Malaysia heat pump market as all electrically driven air-source, water-source, and ground-source units, packaged or split, sold for space conditioning or sanitary hot-water production across residential, commercial, industrial, and institutional premises. Revenues are counted at manufacturer invoice value inside Malaysia and converted to United States dollars using the average 2024 exchange rate.

Scope Exclusion: Chillers, VRF systems without a reversible cycle, aftermarket spares, and purely solar-thermal heaters lie outside this frame.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed heat-pump OEM representatives, national distributors, mechanical contractors, and property developers concentrated in Klang Valley, Penang, Johor Bahru, Kuching, and Kota Kinabalu. The discussions validated market drivers, such as green-building rebates and electricity price trends, typical capacity splits, and installer margins that are rarely disclosed in public reports.

Desk Research

We began with national data sets from bodies such as the Department of Statistics Malaysia, the Energy Commission, and the Sustainable Energy Development Authority, which map building stock, electricity tariffs, and renewable-energy incentives. Customs import codes (HS 8418 & 8419) from UN Comtrade and ASEANstats helped us size cross-border flows, while patent families in Questel flagged emerging technologies. Company filings aggregated in D&B Hoovers, plus installer price lists collected through Dow Jones Factiva news feeds, grounded our average selling price assumptions. These sources are illustrative; many additional publications supported data checks and context building.

Market-Sizing & Forecasting

We start with a top-down build. Dwelling and commercial floor-area stock is multiplied by penetration rates for space-conditioning and hot-water systems, then adjusted for local COP values and retrofit cycles to generate a demand pool. Select bottom-up roll-ups, supplier shipment samples, and channel checks are overlaid to fine-tune totals. Key variables include new housing completions, hotel room inventory, electricity tariff differentials versus LPG, average ambient temperature bands, and government High-Efficiency Appliance rebates. A multivariate regression links these drivers to historic revenue, and ARIMA smoothing projects residuals. Where installer-level data are patchy, ratio gaps are filled using averaged margins from verified respondent ranges.

Data Validation & Update Cycle

Outputs pass variance screens against trade statistics and building-energy intensity benchmarks before senior analyst sign-off. Reports refresh every twelve months, and we trigger interim updates if subsidy rules, large procurement tenders, or currency swings alter the baseline.

Why Our Malaysia Heat Pump Baseline Commands Reliability

Published estimates often diverge; some count installed bases, others bundle ancillary HVAC gear, and refresh cadences vary.

Key gap drivers include differing scope choices, such as inclusion of VRF or hybrid systems, unvalidated ASP progressions, currency conversions taken at spot rather than period averages, and projection models that ignore local building-code stimulus. Mordor's disciplined segmentation and annual refresh cadence limit these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 285.4 million (2025) | Mordor Intelligence | - |

| USD 782.7 million (2024) | Regional Consultancy A | Counts heat-pump ready VRF and high-temperature industrial dryers, inflating base value |

| USD 18.75 billion (2024) | Global Consultancy B | Applies installed-base replacement cost rather than annual shipments, and uses blanket ASEAN average ASP |

| USD 14.04 billion (2025) | Trade Journal C | Focuses on VRF heat-pump systems only, then scales to whole market without capacity mix adjustment |

In short, Mordor Intelligence delivers a balanced, transparent baseline anchored to measurable Malaysian variables, refreshed on a predictable cycle, and traceable to openly verifiable data points, making it the dependable foundation for strategic decisions.

Key Questions Answered in the Report

How large will Malaysia heat pump market size be by 2031?

It is forecast to reach USD 362.12 million by 2031, growing at a 3.96% CAGR from 2026.

Which source type leads sales today?

Air-source units hold 47.83% of Malaysia heat pump market share, thanks to lower upfront costs and easy retrofits.

What is the fastest-growing application segment?

Industrial and process heating is projected to expand at a 5.02% CAGR as factories retrofit waste-heat recovery loops.

Why are data-center projects important for vendors?

Hyperscale campuses in Johor require large-capacity liquid-cooling heat pumps, accelerating demand for above-200 kW systems.

How do rising electricity tariffs affect adoption?

The 14.2% tariff hike in 2025 pushes facility managers to prioritize efficiency, making inverter-driven heat pumps financially attractive within four-year payback windows.

Are financing programs available for buyers?

Yes, Green Technology Financing Scheme 3.0 offers a 2% interest rebate and a 60% federal guarantee, reducing capital barriers for commercial installations

Page last updated on: