Brazil Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.44 Billion |

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Heat Pump Market Analysis by Mordor Intelligence

The Brazil heat pump market size is expected to grow from USD 1.44 billion in 2025 to USD 1.51 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at a 4.26% CAGR over 2026-2031. Demand rides on stricter decarbonization mandates, expanding renewable-power capacity, and urban middle-class growth, yet high consumer credit costs continue to temper residential sales. Air-source units dominate thanks to modest capital needs and installer familiarity, while hybrid configurations gain traction because they meet both cooling peaks linked to El Niño weather and hot-water loads. Commercial and industrial buyers accelerate retrofits to trim energy bills and qualify for ANEEL efficiency incentives, whereas residential adoption remains geographically uneven beyond the Southeast corridor. Meanwhile, global brands deepen local manufacturing and training footprints, widening price competition and gradually normalizing life-cycle cost awareness among buyers.

Key Report Takeaways

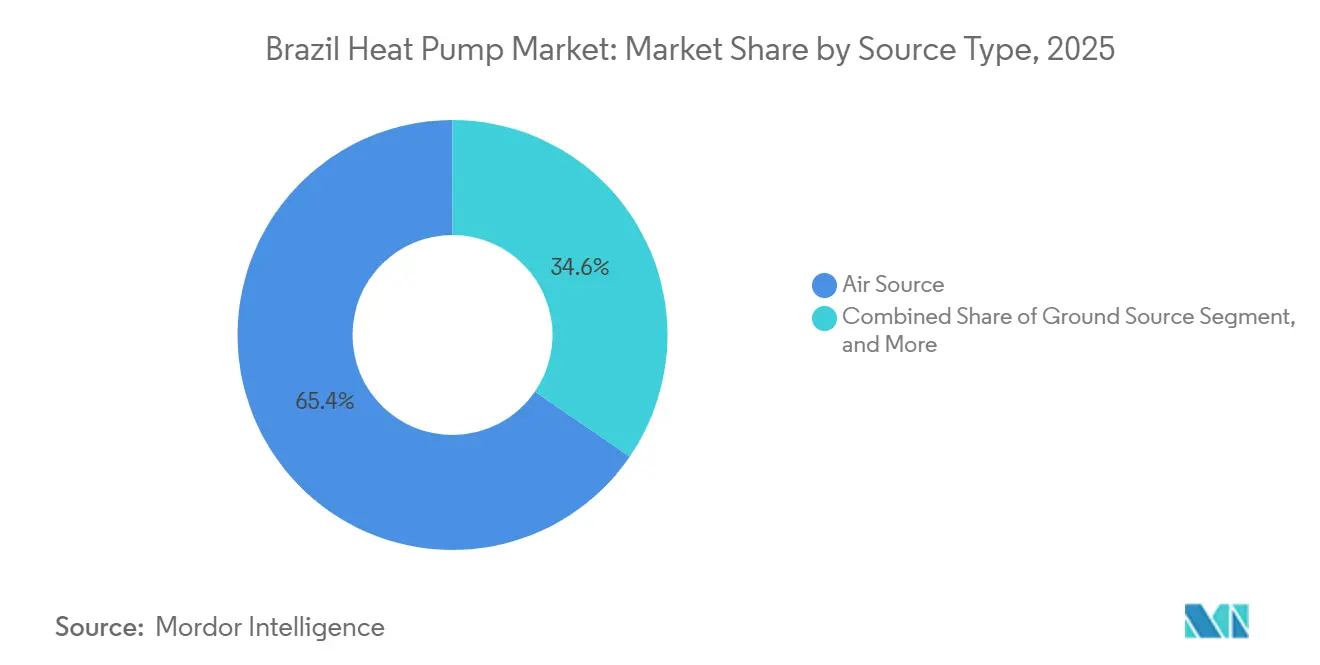

- By source type, air-source units led with 65.42% of Brazil heat pump market share in 2025, whereas hybrid systems record the highest projected 5.18% CAGR through 2031.

- By technology, air-to-water captured 42.31% share of the Brazil heat pump market size in 2025, and ground-to-water is forecast to expand at a 4.82% CAGR to 2031.

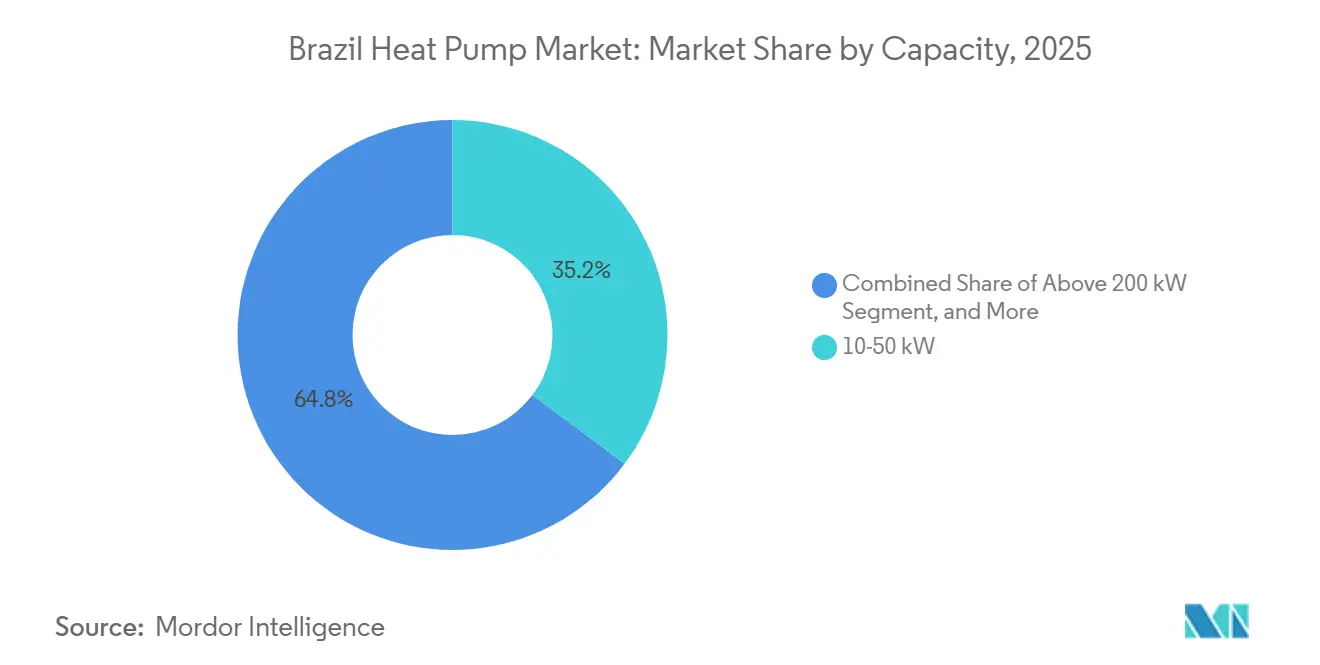

- By capacity, the 10-50 kW range held 35.23% of Brazil heat pump market share in 2025, while the 50-200 kW band is expected to post a 4.61% CAGR between 2026-2031.

- By application, domestic and sanitary hot water contributed 25.82% revenue in 2025, with industrial and process heating projected to grow at a 4.96% CAGR to 2031.

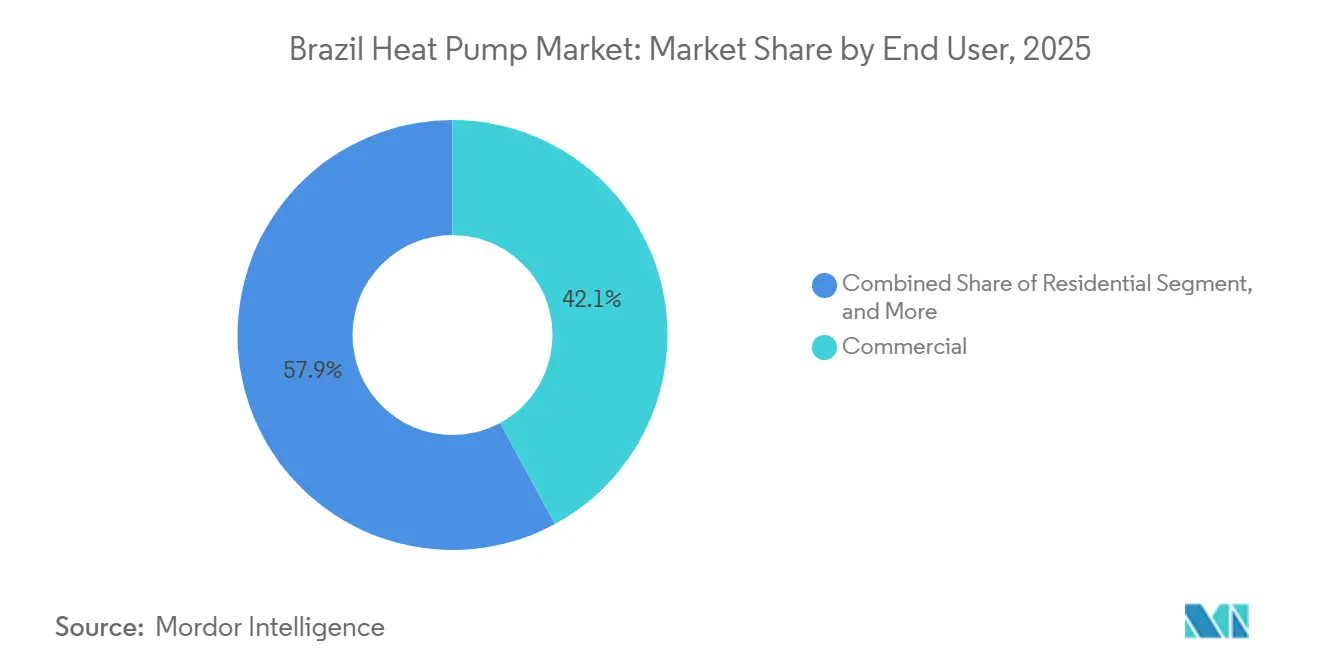

- By end user, commercial customers commanded 42.09% of 2025 revenue, and industrial installations are set to rise at a 4.73% CAGR through 2031.

- By installation type, retrofit projects accounted for 31.43% of sales in 2025, yet new-build deployments are slated for a 4.47% CAGR owing to tougher building codes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives for Residential Decarbonization | +1.2% | National, early gains in São Paulo, Rio de Janeiro, Minas Gerais | Medium term (2-4 years) |

| Growing HVAC Electrification in Tropical Climates | +1.0% | National, concentrated in Southeast and Northeast coastal cities | Short term (≤ 2 years) |

| Falling Hardware Costs From Asian Scale Manufacturing | +0.8% | National, supply-chain benefits across all regions | Short term (≤ 2 years) |

| Hydrothermal-Source Potential in Northeast Lagoons | +0.3% | Bahia, Sergipe, Alagoas | Long term (≥ 4 years) |

| Bundled Carbon-Credit Revenues From Amazon Reforestation Projects | +0.2% | Pará, Amazonas, Acre, spillover to Central-West | Long term (≥ 4 years) |

| El Niño-Driven Cooling-Degree-Day Increase Elevating Dual-Mode Demand | +0.5% | National, strongest in Central-West and interior Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives For Residential Decarbonization

Rising utility obligations funnel fresh capital into efficiency programs, lifting annual funding to roughly BRL 500 million (USD 96 million) that utilities must spend on pilots, rebates, and verification. Concessional BNDES Finem loans stretch repayment to 20 years and compress interest margins, enabling municipalities and housing cooperatives to bundle heat pumps with rooftop solar and meet lifecycle-parity thresholds. Expanded Procel laboratory budgets shorten certification queues, ensuring faster label issuance and broader model availability. Policy documents highlight Brazil’s 90% renewable power mix and pledge tariff relief for lower-income households, positioning efficient electric appliances for mass-market reach. Nonetheless, the lack of federal tax credits keeps adoption patchy, hinging on state or utility programs.[1]Ministério de Minas e Energia, “Brasil, Líder Mundial na Transição Energética,” gov.br

Growing HVAC Electrification in Tropical Climates

Only one in five Brazilian homes owned an air conditioner in 2025, leaving ample headroom for reversible units that supply cooling and hot water. Strong 10% revenue growth in the broader HVAC sector underscores latent demand as urbanization intensifies and comfort expectations climb. IEA studies show buildings already draw 30% of global energy, so leapfrogging gas heaters through direct electrification can slash carbon trajectories.[2]International Energy Agency, “Energy Efficiency 2025 – Buildings,” iea.org Subscription models under trial aim to cut upfront barriers by converting equipment into an affordable monthly service, potentially multiplying residential sales within a decade. Localized mass production by Asian brands injects added price pressure, steering replacement buyers toward efficient dual-mode systems.

Falling Hardware Costs from Asian Scale Manufacturing

Chinese and Korean manufacturers channel global scale into domestic assembly, trimming Brazilian ex-factory prices by as much as one fifth between 2024-2026. A USD 104.26 million lighthouse plant now delivers 1.3 million units yearly, proving that cost declines can coexist with on-site solar and aggressive waste-reduction metrics. Free-trade tax perks and state incentives magnify savings, while material-efficiency innovations such as reclaimed copper curb both cost and footprint.[3]Heat Pump Centre, “IEA HPT Project 65 Task 1 Report,” heatpumpingtechnologies.org Hardware deflation therefore strengthens the total-cost-of-ownership argument even as credit costs rise.

El Niño-Driven Cooling-Degree-Day Increase Elevating Dual-Mode Demand

Warmer anomalies raise cooling loads in interior regions, encouraging households to favor equipment that handles both air conditioning and water heating within one envelope. Hybrid units already post the quickest growth outlook at 5.18% CAGR through 2031, signaling customer appetite for operational flexibility. Grid-interactive controls allow compressors to run during renewable generation peaks, offering valuable demand-side reserves. Nevertheless, hydro-shortfalls during severe droughts can spike spot prices, meaning tariff design and storage solutions will remain pivotal to sustaining economic gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Versus Split AC Plus Gas Heater | -0.9% | National, acute in North and Northeast low-income segments | Short term (≤ 2 years) |

| Scarcity of Trained Installers Beyond Southeast Corridor | -0.6% | North, Northeast, Central-West | Medium term (2-4 years) |

| Rising Compliance Costs From Propane Refrigerant Transition | -0.3% | National, small installers most affected | Medium term (2-4 years) |

| Elevated Consumer Credit Interest Rates Curbing Capex Purchases | -0.7% | National, heavier on residential and small commercial | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Split AC Plus Gas Heater

Heat pump packages still carry 30-50% premiums relative to a split AC paired with resistance or gas water heating, overshadowing lifecycle savings for cash-constrained households. Central-bank moves pushed the SELIC from 10.75% to 12.25% in January 2025 and could touch 15% by mid-2026, inflating monthly payments and lengthening paybacks. Industrial customers dodge this hurdle through subsidized BNDES lines, but a comparable residential mechanism remains absent. Developer-led subscription pilots promise relief, yet long-term viability depends on residual-value certainty and service quality perceptions. Until financing innovation scales, sticker shock will continue to slow mainstream adoption.

Scarcity Of Trained Installers Beyond Southeast Corridor

Proper sizing, refrigerant handling, and hydronic know-how are scarce outside the São Paulo-Rio axis, dampening reliability and customer confidence. Training hubs now operate in Salvador and soon Belo Horizonte, but coverage gaps persist across the North and Central-West where climatic need is rising fastest. Propane certification, newly mandatory under Kigali obligations, adds cost and time that small contractors often cannot absorb. Industrial-focused programs enlarge consultant pools, yet residential crews receive limited support. Without rapid skill-building, installation bottlenecks could eclipse hardware affordability gains, especially in underserved regions.[4]Programa PotencializEE, “Bomba de calor na prática industrial,” programa-potencializee.com.br

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Prevails While Hybrid Ascends

Air-source units claimed 65.42% of Brazil heat pump market share in 2025, benefiting from modest capital outlays, minimal ground works, and broad installer familiarity. Hybrid designs, though smaller in base, are forecast for a brisk 5.18% CAGR because homeowners value the resilience of dual-fuel or dual-electric arrangements that safeguard comfort during grid stress events. Drilling fees and limited hydrogeological data keep ground-source uptake subdued, yet pilot schemes in coastal lagoons could shift future economics.

Manufacturers channel Asia-based economies of scale into local assembly, trimming delivered prices and enabling aggressive promotions that reinforce air-source dominance. Meanwhile, municipality-backed carbon-credit structures under evaluation in Alagoas may help absorb upfront costs for water-source projects, widening the technology mix over the long horizon.

By Technology: Air-to-Water Leads As Ground-to-Water Speeds Up

Air-to-water accounted for 42.31% of Brazil heat pump market size in 2025, favored by hotels, hospitals, and multifamily buildings needing simultaneous cooling and potable water heating. Ground-to-water is poised for the fastest 4.82% CAGR because hydrothermal pilots now underway demonstrate high seasonal performance factors that lure industrial operators with year-round loads.

Air-to-air remains prevalent for retrofit cooling, yet reversible variants remain under-marketed, representing latent upside once financing models stabilize. Water-to-water applications stay niche but could flourish around process-heat clusters if waste-heat integration standards advance and performance data accumulates.

By Capacity: Mid-Range Stays Dominant While Industrial Ratings Rise

The 10-50 kW band captured 35.23% of Brazil heat pump market share in 2025, serving small commercial sites where paybacks fall inside utility incentive windows. Units rated 50-200 kW look set for a 4.61% CAGR as food, beverage, and textiles retrofit boilers to tame fuel logistics and emissions.

Residential sub-10 kW sales lag because credit rates remain elevated, but subscription offerings may unlock latent demand if lenders underwrite equipment residuals. Custom systems above 200 kW require sophisticated engineering and grid-impact studies, so uptake concentrates in flagship industrial parks and district-energy pilots.

By Application: Hot Water Tops Revenues, Process Heat Gains Momentum

Domestic and sanitary hot water produced 25.82% of 2025 turnover, reflecting minimal space-heating need in tropical zones. Industrial process applications should advance at a 4.96% CAGR as manufacturers leverage verified three-year paybacks confirmed in textile and chocolate projects.

Space cooling still outsells every other function in volume but frequently involves non-reversible splits, signaling scope for dual-mode migration. Agricultural drying, aquaculture warming, and pool heating remain peripheral yet could expand once standardized design guides circulate and installer density improves.

By End User: Commercial Heads Today, Industrial Accelerates Tomorrow

Commercial facilities delivered 42.09% of 2025 revenue as hotels, malls, and offices tap ANEEL-funded rebates that compress two-to-four-year capital returns. Industrial buyers will register a 4.73% CAGR on the back of BNDES long-tenor loans and ESCO guarantees that de-risk performance contracts.

Residential customers trail because premiums persist and credit is dear, though concept-store marketing and on-bill repayment pilots may gradually erode hesitation. Public-sector buildings grow in significance as procurement catalogues now include Class A HVAC, signaling steady institutional demand.

By Installation: Retrofit Dominates, Code-Driven New Builds Pick Up Pace

Retrofits held 31.43% of 2025 activity because existing facilities rush to cut energy spend and decarbonize without erecting new shells. New-build installations, expected to run at a 4.47% CAGR, gain impetus from tougher Procel Edifica codes that require efficient HVAC in municipal permits.

Retrofit economics benefit from immediate utility savings but grapple with spatial constraints and downtime risk, while new construction allows optimized pipe runs, storage, and solar coupling that bolster system efficiency over decades.

Geography Analysis

Southeast states, chiefly São Paulo, Rio de Janeiro, and Minas Gerais, account for the bulk of deployments given higher disposable incomes, rich installer ecosystems, and proximity to new manufacturing hubs. Subscription concepts and concept stores cluster here, acting as test beds before roll-outs elsewhere.

Northeast coastal regions exhibit strong latent demand driven by hotter climates and hydrothermal-source prospects, although limited qualified labor and grid reliability issues currently cap penetration. Ongoing training programs in Salvador and carbon-credit pilots around lagoon projects could unlock acceleration.

The South sees cooler winters, making reversible heat pumps attractive replacements for resistance heaters, yet smaller population keeps volumes modest. Central-West agribusiness hubs and North rainforest states harbor long-range potential tied to carbon-linked financing and industrial agro-process uses, though sparse grid and workforce gaps postpone near-term scaling.

Competitive Landscape

Global incumbents such as Daikin, Mitsubishi Electric, Carrier, and Midea share the lion’s slice of Brazil heat pump market, leveraging local factories that exploit free-trade incentives to shorten lead times and curb import duties. Midea’s lighthouse plant exemplifies cost-plus-sustainability strategy, enhancing brand equity while flooding channels with competitively priced SKUs.

European specialists NIBE, Viessmann, Bosch, and Stiebel Eltron trade on efficiency leadership and robust training curricula, concentrating on premium commercial niches where buyers prize lifecycle metrics over first cost. Chinese challengers Gree, LG, and Hisense intensify residential price wars, often bundling financing or smart-home perks to woo first-time owners.

Strategic themes include installer-academy rollouts beyond the Southeast, cloud connectivity for predictive maintenance, and circular-economy design shifts that trim material inputs and ease refrigerant recovery. Emerging ESCO models pair performance contracts with state guarantee funds, widening access for industrial retrofits and sharpening service differentiation.

Brazil Heat Pump Industry Leaders

Daikin Industries Ltd.

Mitsubishi Electric Corp.

Carrier Global Corp.

Bosch Thermotechnology (Robert Bosch GmbH)

Panasonic Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Distribution utilities began complying with higher 0.3% efficiency-spend mandates, opening roughly BRL 500 million for new heat pump pilots and consumer incentives.

- November 2025: Daikin confirmed evaluation of a USD 5-per-month subscription for residential air conditioners, leveraging its 31 concept stores and multi-city training hubs to pilot comfort-as-a-service.

- July 2025: BYD outlined plans to assemble 50,000 electric cars at Camaçari, Bahia, by 2025, reinforcing electrification supply chains that can spill into HVAC component sourcing.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Brazil heat pump market as all factory-built air, water, and ground-source units up to 1 MW that provide space-conditioning or sanitary hot-water functions in residential, commercial, industrial, and institutional buildings. Equipment supplied as part of integrated VRF systems is also counted when the outdoor module performs a reversible heat-pump cycle.

Scope exclusion: Process chillers and chillers driven by absorption or combustion are outside the scope.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Brazilian installers, utility demand-side managers, housing-finance officers, and regional distributors across Sao Paulo, Minas Gerais, and the South. The conversations clarified average selling prices, retrofit share, installer capacity bottlenecks, and rebate uptake, which we then triangulated against desk findings.

Desk Research

We began with public datasets such as ANEEL's residential electricity tariff series, IBGE building-permit statistics, SIN import duty filings, and customs shipment codes (NCM 841861, 841869). Trade association briefs from ABRAVA and Eurovent, peer-reviewed HVAC journals, and company 10-Ks added context on technology mix and pricing. Proprietary inputs came from D&B Hoovers for OEM revenue splits and Volza for shipment-level volume checks. These sources, among others, formed the factual bedrock and helped size the addressable stock; the list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction starts with dwelling and floor-space growth, applies heat-pump penetration rates by climate zone, and multiplies by verified ASPs to yield the 2024 base value. Select bottom-up roll-ups of domestic OEM output and sampled importer volumes are used to stress-test totals before finalizing. Key variables include annual housing completions, mean unit price movements, electricity-to-LPG price differentials, Procel label uptake, installer headcount, and seasonal performance factor trends. A multivariate regression framework links these drivers to shipments; ARIMA smoothing adjusts for weather anomalies. Gap cases in OEM disclosures are bridged with normalized import data and distributor margin benchmarks.

Data Validation & Update Cycle

Outputs pass two rounds of analyst review, variance checks against external energy and appliance indicators, and anomaly flags. Models refresh every twelve months, with ad-hoc updates when subsidy rules or large infrastructure awards materially shift demand.

Why Mordor's Brazil Heat Pump Baseline Earns Trust

Published numbers often diverge because firms vary device scope, import coverage, and forecast cadence.

By anchoring on complete NCM codes, full building segments, and yearly tariff realities, Mordor delivers a balanced, transparent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.38 B | Mordor Intelligence | - |

| USD 315.3 M | Regional Consultancy A | Omits water-source units and systems >50 kW; relies on proxy penetration without import cross-checks |

| USD 627 M | Trade Journal B | Counts only NCM 841861 exports, misses domestic OEM output and channel mark-ups |

The comparison shows that narrower scopes or partial data pulls compress competitor figures, whereas Mordor's disciplined mix of public statistics, selective primary insight, and dual-track modeling provides decision-makers with the most dependable starting point for strategy.

Key Questions Answered in the Report

How large will the Brazil heat pump market be by 2031?

Current projections place it at USD 1.86 billion in 2031, reflecting a 4.26% CAGR from 2026-2031.

Which heat pump source type leads sales in Brazil?

Air-source models led with a 65.42% share in 2025, owing to lower capital costs and installer familiarity.

Why are hybrid heat pumps growing fastest?

Dual-mode systems meet both cooling peaks and hot-water loads, registering a 5.18% CAGR forecast through 2031.

What is driving industrial adoption of heat pumps?

Verified three-year paybacks, BNDES long-tenor loans, and new ESCO guarantees spur retrofits in food, beverage, and textile plants.

How do high interest rates affect residential demand?

The projected 15% SELIC rate by mid-2026 inflates monthly payments, delaying payback periods and tempering household purchases.

Page last updated on: