UAE Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

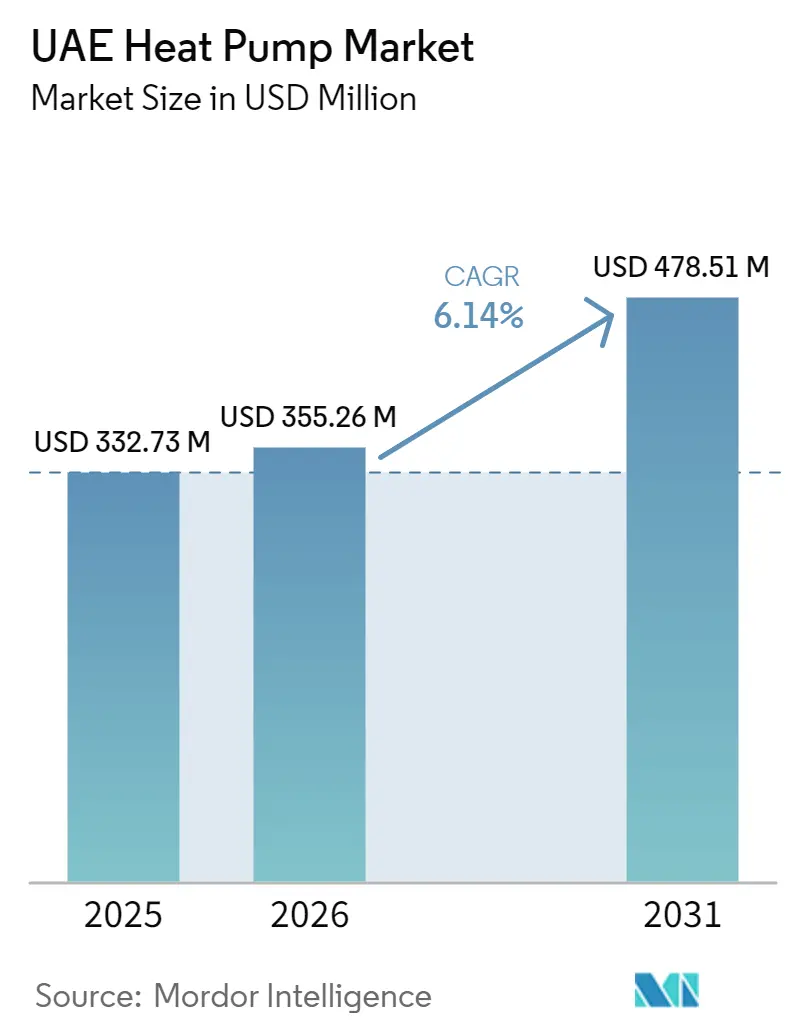

| Base Year Market Size (2025) | USD 332.73 Million |

| Market Size (2026) | USD 355.26 Million |

| Market Size (2031) | USD 478.51 Million |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

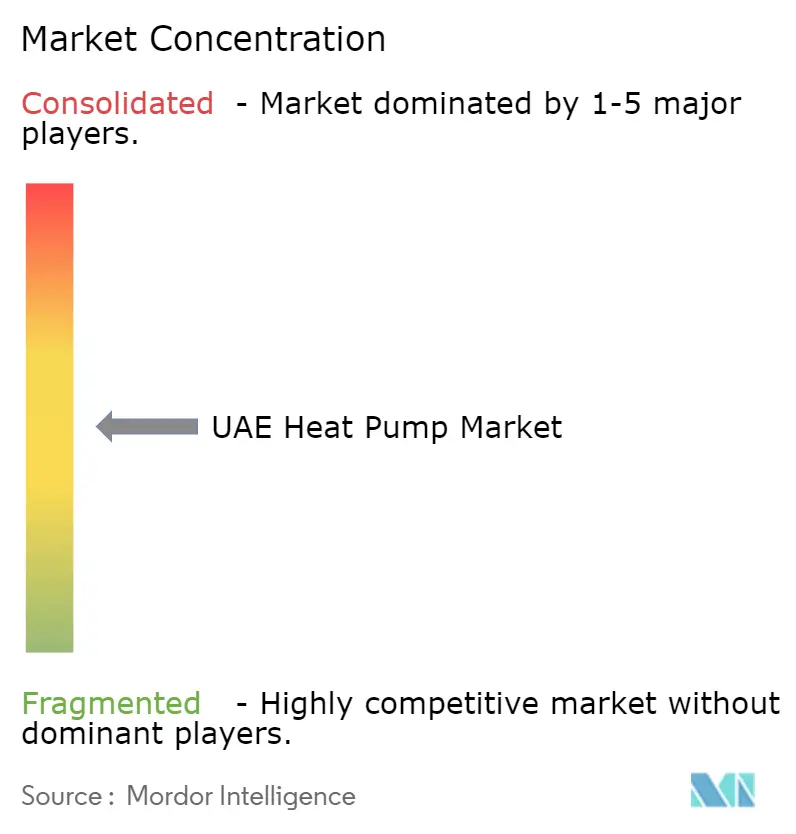

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Heat Pump Market Analysis by Mordor Intelligence

The UAE heat pump market size was valued at USD 332.73 million in 2025 and is estimated to grow from USD USD 355.26 million in 2026 to reach USD USD 478.51 million by 2031, at a CAGR of 6.14% during the forecast period (2026-2031). Persistent federal decarbonization mandates, a tiered electricity tariff that rewards off-peak thermal storage, and a hospitality construction pipeline aligned with Tourism Vision 2031 are steering demand. Developers favor modular air-to-water systems that integrate with chilled-water loops, while district cooling operators increasingly specify high-temperature units capable of simultaneous cooling and heat recovery. Hybrid air-source arrays paired with thermal storage are gaining traction because they maintain output when ambient temperatures exceed 45°C, a frequent occurrence during UAE summers. Equipment able to operate on low-global-warming-potential refrigerants is becoming a procurement prerequisite as suppliers prepare for forthcoming F-gas restrictions.

Key Report Takeaways

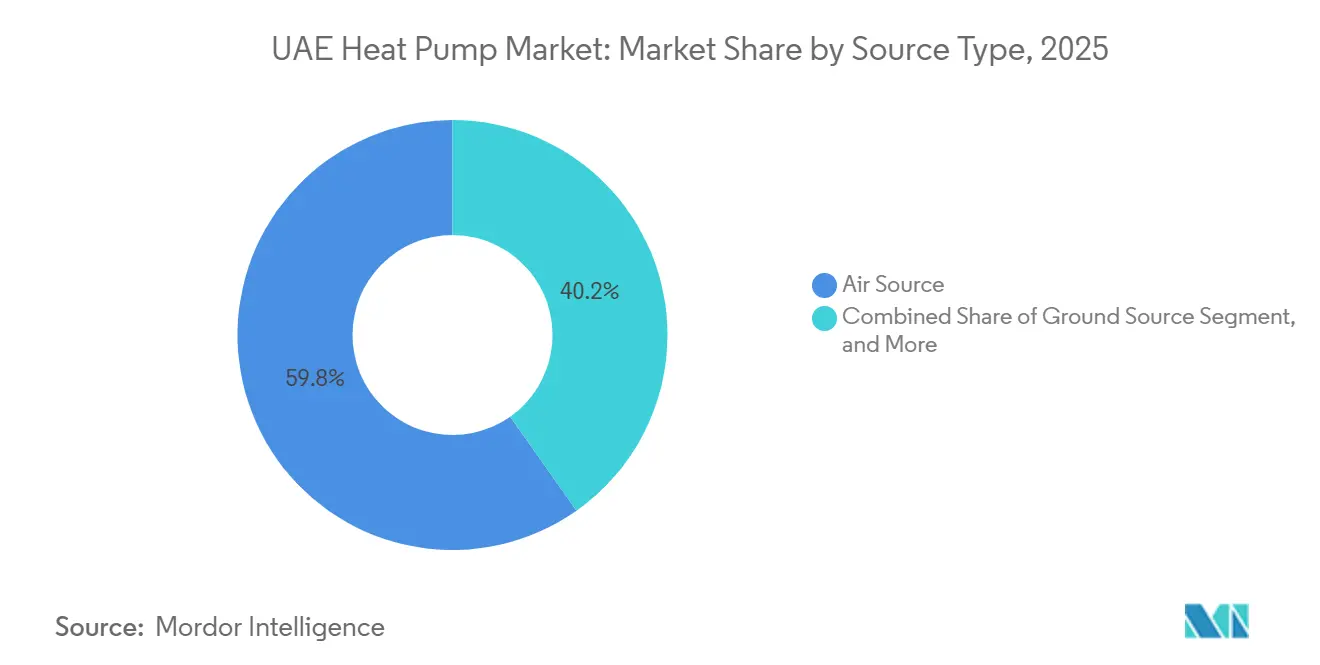

- By source type, air source led with 59.78% of the United Arab Emirates heat pump market share in 2025, whereas hybrid configurations are projected to expand at a 7.04% CAGR through 2031.

- By technology, air-to-water heat pumps accounted for 53.31% of the UAE heat pump market size in 2025 and ground-to-water is advancing at a 6.82% CAGR to 2031.

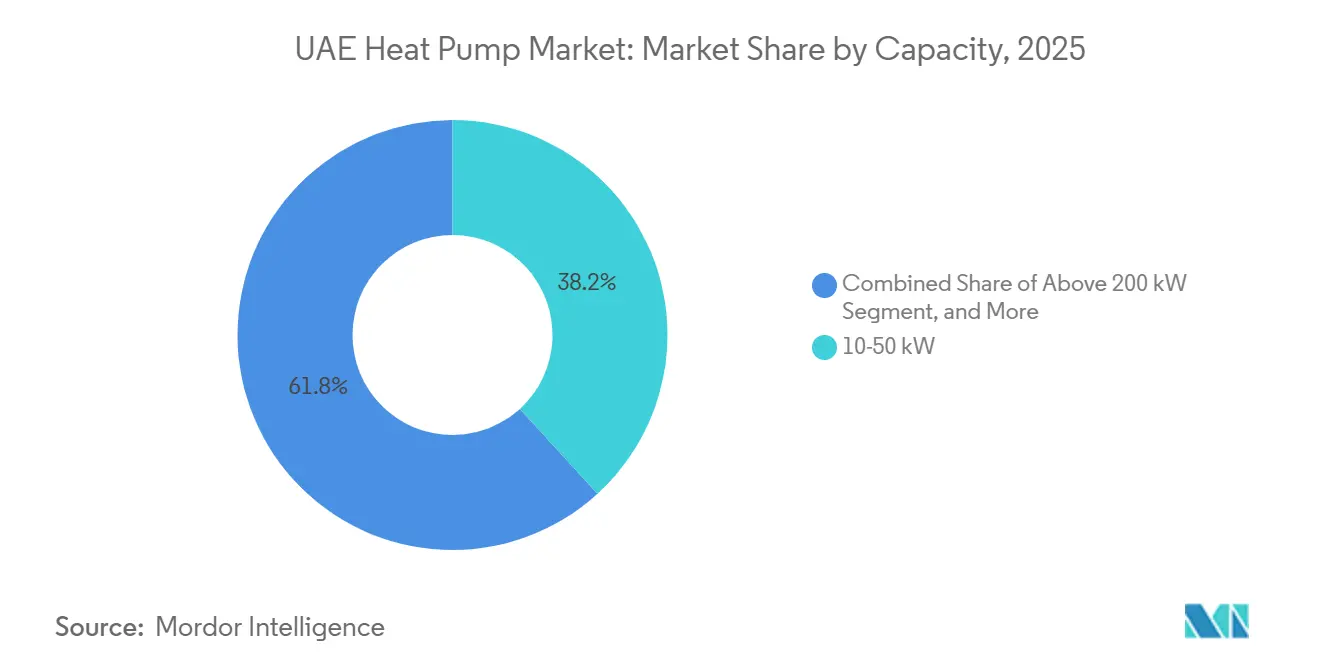

- By capacity, 10-50 kW units held 38.23% share of the United Arab Emirates heat pump market size in 2025, while systems above 200 kW are forecast to grow at a 6.42% CAGR between 2026-2031.

- By application, space cooling captured 46.42% of the UAE heat pump market size in 2025, and industrial and process heating is set to register a 6.71% CAGR through 2031.

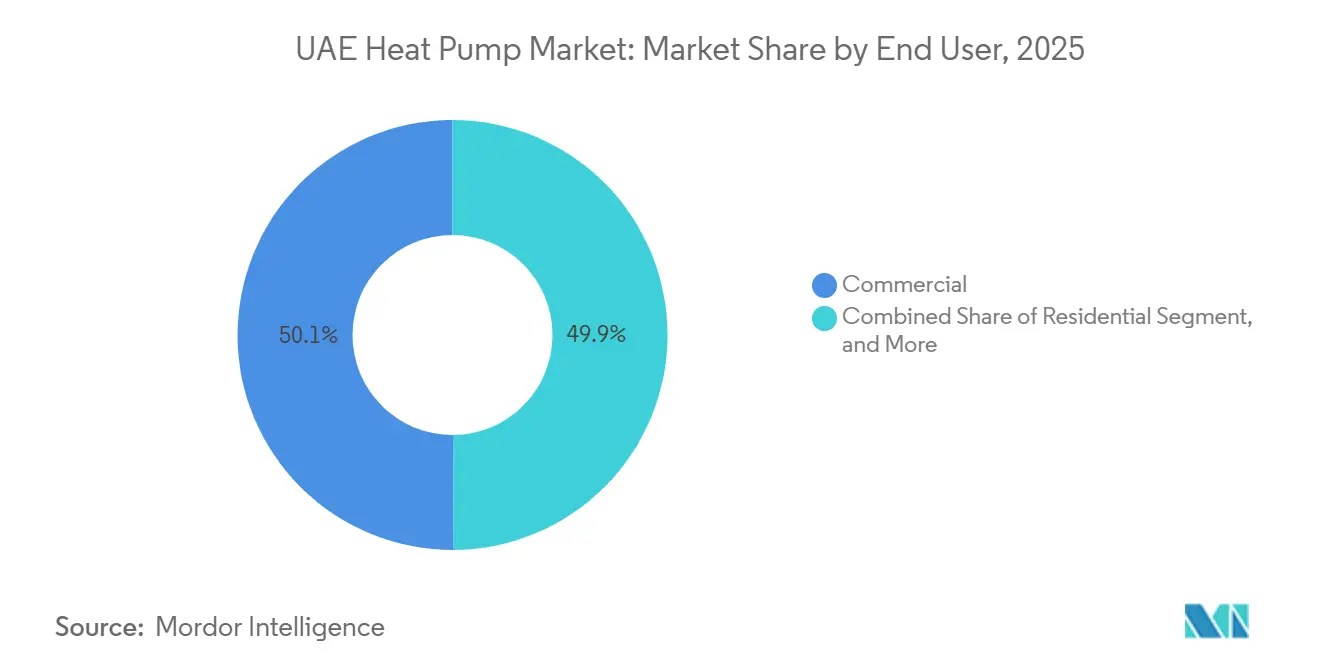

- By end user, the commercial segment commanded 50.09% of the United Arab Emirates heat pump market share in 2025, whereas industrial installations are poised for the fastest growth at 6.78% CAGR over 2026-2031.

- By installation, new builds represented 59.43% of the UAE heat pump market size in 2025, yet retrofits are climbing at a 6.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Adoption Incentives Under UAE Energy Strategy 2050 | +1.2% | National, strong in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Hospitality Construction Boom Fueled by Tourism Vision 2031 | +1.0% | Dubai, Abu Dhabi, Ras Al Khaimah coast | Short term (≤ 2 years) |

| Smart District Cooling Retrofits Mandated by Dubai Supreme Council of Energy | +0.9% | Dubai, spillover to Sharjah and Ajman | Medium term (2-4 years) |

| Peak Electricity Tariff Reform Encouraging Thermal Storage Integration | +0.8% | Dubai and Abu Dhabi, extending to Northern Emirates | Short term (≤ 2 years) |

| Mandatory Building Decarbonization Targets for Freehold Developers | +0.7% | Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Federal Green Financing Programs Lowering Cost of Capital | +0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Adoption Incentives Under UAE Energy Strategy 2050

The UAE Energy Strategy 2050 sets a 50% clean-energy share and a 40% reduction in overall energy use, which anchors stable policy support for efficient HVAC solutions.[1]International Renewable Energy Agency, “Renewable Energy Prospects UAE,” irena.org Dubai Electricity and Water Authority responds with time-of-use tariffs that penalize afternoon peaks, so commercial operators increasingly schedule chilled-water production at night when tariffs are lower.[2]Dubai Electricity and Water Authority, “Time-of-Use Tariff Overview,” dewa.gov.ae Abu Dhabi’s February 2026 solar self-supply manual signals forthcoming minimum coefficient-of-performance thresholds that will formalize heat pumps as baseline equipment for new developments. Field monitoring in Dubai shows modern units deliver coefficients of performance above 4.0, translating to 300-400% efficiency over electric resistance heating. The long planning horizon reduces regulatory risk, enabling vendors to invest in assembly hubs and service centers that localize supply chains.

Hospitality Construction Boom Fueled by Tourism Vision 2031

Tourism Vision 2031 targets 40 million annual visitors, propelling hotel and resort projects that require large chilled-water loads. Emirates Central Cooling Systems Corporation expanded installed capacity to 1.7 million refrigeration tons and posted AED 3.4 billion (USD 925.6 million) revenue in 2025, underscoring hospitality demand for district cooling. The Jumeirah Beach Hills plant went online in December 2024 with 48,000 refrigeration tons and integrated thermal storage that lowers peak grid draw. Operators demand reliability, so heat-pump-based plants using 9°C delta-T and smart controls are becoming standard in new resorts. Phased commissioning lets developers match cooling supply to staged occupancy, favoring manufacturers that offer factory-tested skid-mounted modules. The construction wave thus secures a multiyear pipeline for large-capacity heat pumps tailored to hospitality’s 24-hour cooling profile.

Smart District Cooling Retrofits Mandated by Dubai Supreme Council of Energy

Dubai’s Demand Side Management 2050 strategy identifies existing district cooling networks as priority retrofit targets. Etihad ESCO concluded the UAE’s first energy-savings performance contract in 2024, achieving 35.2 GWh in electricity savings and 14,452 tCO₂ cut across multiple DEWA buildings. Under the performance-contract model, the service company guarantees savings and collects payments via utility bills, eliminating split-incentive conflicts that stall retrofit spending.[3]The Energy Year, “Building Retrofits Deliver Double-Digit Savings,” theenergyyear.com The council aims to retrofit 47 000 buildings by 2030, later expanded to 3.7 TWh savings by 2050, ensuring long-term demand for high-efficiency heat pumps that integrate with treated sewage effluent loops and chilled-water storage. Vendors equipped to underwrite multi-year guarantees secure a competitive edge in this expanding retrofit marketplace.

Peak Electricity Tariff Reform Encouraging Thermal Storage Integration

Dubai’s time-of-use tariff levies peak rates in afternoon hours, giving customers a financial reason to shift load to off-peak periods. Oak Ridge National Laboratory reports thermal storage can trim peak power demand by 30-50% in cooling and up to 60% in heating, yielding annual cost cuts between 5.6% and 26% depending on tariff spread.[4]Oak Ridge National Laboratory, “Thermal Energy Storage Systems,” ornl.gov Empower’s forthcoming 47,000 RT Dubai Science Park plant embeds thermal storage and AI controls to exploit tariff differentials.[5]Emirates Media Office, “Empower to Build Dubai Science Park Plant,” mediaoffice.ae Developers now oversize heat-pump capacity to rapidly charge storage tanks at night, a design that raises capex but shortens payback through electricity-price arbitrage. Consequently, advanced variable-speed compressors and responsive controls are now baseline requirements in high-specification bids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Skilled Installers for Ground-Source Loops | -0.5% | National, acute in Northern Emirates | Medium term (2-4 years) |

| High Up-Front Capital Cost Versus Legacy Chillers | -0.4% | National, especially residential | Short term (≤ 2 years) |

| Performance Degradation in Extreme Desert Conditions | -0.3% | National, intense inland | Long term (≥ 4 years) |

| Fragmented After-Sales Service Network in Northern Emirates | -0.2% | Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, Fujairah | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Skilled Installers For Ground-Source Loops

Ground-source projects inside the UAE heat pump market stall when developers cannot secure drillers familiar with desert geology. Sharjah trials recorded 32 °C sub-surface temperatures and nine-hour thermal-regeneration cycles, conditions that require precise loop sizing and grout selection. Few contractors own deep-drilling rigs, so imported crews drive installation costs higher than projected budgets for master-planned communities. Training programs now focus on chillers and variable-refrigerant-flow equipment, leaving a curriculum gap on borehole hydraulics, soil conductivity testing, and loop commissioning. Until local colleges create accredited modules, developers will continue to favor air-source and hybrid systems for speed-to-market, limiting ground-source penetration and trimming potential gains for the UAE heat pump market.

High Up-Front Capital Cost Versus Legacy Chillers

Even when lifetime electricity savings are proven, a 30-50% capital premium over conventional chillers deters cash-conscious builders in the UAE heat pump market. Energy-service-company contracts help institutional owners, but smaller residential projects struggle because landlords finance equipment while tenants capture lower utility bills. Cheap natural gas in Abu Dhabi sustains gas-fired absorption chillers as a low-capex alternative, splitting the market between green-finance adopters and price-sensitive holdouts. Federal soft-loan programs and Etihad ESCO payment-through-utility-bill models shorten payback to single digits only for large, stable loads. Unless component prices fall or codes tighten, the cost barrier will continue to mute penetration outside premium developments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Retains Majority Share While Hybrid Adoption Rises

Air source units held 59.78% of the UAE heat pump market share in 2025, a position sustained by minimal site work and widespread service infrastructure. Hybrid combinations of air-source heat pumps and thermal storage are growing at 7.04% as developers hedge against afternoon peaks when ambient temperatures exceed 45 °C and tariffs spike.

The UAE heat pump market size attributed to water source systems remains small because projects require proximity to seawater or industrial loops along the Gulf coast. Ground-source installations advance inside gated townships where long ownership horizons justify borehole investment, but the skills gap noted earlier slows broader uptake. As policy pushes for resilience, air source suppliers that offer plug-and-play thermal-storage packages are capturing incremental sales.

By Technology: Air-to-Water Leads While Ground-to-Water Accelerates

Air-to-water platforms represented 53.31% of 2025 shipments, aligning with chilled-water loops already common in towers and district-cooling networks. This technology anchors retrofit programs because mechanical rooms often contain hydronic pumps and buffer tanks that accept new heat-pump modules without re-piping entire floors.

Ground-to-water machines, though just a fraction of the UAE heat pump market size today, are projected to advance 6.82% per year on the back of master-planned communities targeting zero-operational-carbon labels. Air-to-air variants dominate villas, yet their capacity de-rates sharply above 45 °C. Water-to-water models serve food, beverage, and pharmaceutical lines that maintain closed process cooling loops at stable inlet temperatures, enabling coefficients of performance above four throughout the year.

By Capacity: Mid-Range Units Dominate As Large Modular Plants Gain Speed

Systems rated 10-50 kW controlled 38.23% of the UAE heat pump market size in 2025 because they match cooling loads in neighborhood retail and mid-rise apartments. Larger pools in the above-200 kW bracket are registering a 6.42% CAGR as district-cooling concessions adopt modular skid arrays that commission in phases alongside property handovers.

Sub-10 kW equipment competes directly with split AC units, so penetration remains limited to eco-branded villas. The 50-200 kW tier bridges single-building and campus applications, with uptake guided by availability of rooftop space or plant rooms. Vendors bundling predictive-maintenance subscriptions win bids by guaranteeing availability for mixed-use complexes that value uptime over first cost.

By Application: Cooling Leads While Process Heating Logs Fastest Growth

Space-cooling needs accounted for 46.42% of 2025 demand because every occupied structure in the Emirates requires year-round air conditioning. Industrial and process heating is forecast to expand at 6.71%, the quickest among applications, as petrochemicals, aluminum, and packaged-food plants target Scope 1 cuts by replacing gas boilers with 95 °C heat pumps.

Domestic hot-water systems in hotels and multifamily blocks recycle waste heat from chillers, reducing energy bills by over 70 % in pilot retrofits. Space heating stays niche because winter lows seldom drop below 15 °C, yet healthcare and cold-storage facilities install reversible units to handle shoulder-season humidity control, presenting a small but stable revenue stream for the UAE heat pump market.

By End User: Commercial Sites Remain Prime Buyers, Industrial Adoption Surges

Commercial properties represented 50.09% of 2025 installations, buoyed by office, retail, and hospitality pipelines aligned with Tourism Vision 2031. The industrial category is set for a 6.78% CAGR as high-temperature units replace steam in cleaning-in-place, pasteurization, and desalination pre-heaters.

Residential penetration is highest in master-planned enclaves where developers integrate chilled-water loops from the outset. Split-incentive economics keep mass-market landlords cautious, but government discussions on building-energy-rating disclosure hint at future regulations that could tip the balance in favor of efficient equipment across the broader UAE heat pump market.

By Installation: New Builds Prevail As Retrofit Pipeline Accelerates

New projects formed 59.43% of the UAE heat pump market share in 2025 because mega-developments can optimize HVAC during design. Retrofits, however, are clocking a 6.93% CAGR due to Dubai Supreme Council of Energy mandates and Etihad ESCO contracts that bundle financing with savings guarantees.

Upgrading legacy chilled-water plants to air-to-water heat pumps avoids tenant disruption and leverages existing hydronic distribution, making retrofits cost-effective even when space is tight. Innovative micro-piled boreholes tested in downtown Dubai hint at future retrofit feasibility for ground-coupled systems once installer training expands.

Geography Analysis

Dubai maintains the largest slice of the UAE heat pump market because Al Sa'fat green-building rules and time-of-use tariffs favor efficient, storage-enabled HVAC. Empower’s 47,000 RT Dubai Science Park plant, breaking ground in Q1 2026, embeds artificial-intelligence dispatch and chilled-water storage to arbitrage tariff spreads, reinforcing Dubai’s role as the national innovation hub. Developer familiarity with performance contracts means retrofit decisions often default to air-to-water heat pumps whenever plant rooms come due for renewal.

Abu Dhabi follows closely, guided by the Estidama Pearl framework and the February 2026 solar self-supply policy that foreshadows minimum heat-pump performance thresholds. ENGIE Solutions’ Al Zeina retrofit cut hot-water energy use 73%, signaling to other master-planned communities that lifecycle economics now justify electrified heating even where subsidized gas remains available. The emirate’s refining and petrochemical belt in Ruwais offers a frontier for 95 °C heat pumps that can displace once-through steam, but bespoke engineering and financing structures are still evolving.

Sharjah, Ajman, Ras Al Khaimah, Umm Al Quwain, and Fujairah trail because after-sales networks are thin and district-cooling concessions limited. Ground-source pilots in Sharjah reveal potential but face loop-drilling logistics and high groundwater salinity. Coastal hotels in Ras Al Khaimah evaluate seawater-source heat pumps, yet project scales remain too small for multinational OEMs to warehouse spares locally. As Dubai and Abu Dhabi demonstrate proven business models, replication across the Northern Emirates should accelerate, albeit from a modest base within the broader UAE heat pump market.

Competitive Landscape

Global manufacturers dominate large contracts inside the UAE heat pump market. Daikin, Mitsubishi Electric, Carrier, Trane Technologies, and Johnson Controls leverage decades-long developer ties and are first to certify equipment for 52 °C ambient operation with low-GWP refrigerants. Daikin’s January 2026 Burj Azizi award and its Jeddah hydronic-heat-pump plant shorten lead times, boosting regional responsiveness. Tabreed’s March 2026 framework with Johnson Controls packages variable-speed drives and refrigerants under GWP 100, signaling tightening environmental procurement clauses.

District-cooling operators such as Empower, Tabreed, and Emirates District Cooling function as anchor customers and quasi-competitors, sourcing bulk volumes while promoting centralized plants that vie with distributed building-level systems. Mitsubishi Heavy Industries has shipped more than 56,000 RT of centrifugal units to Empower since early 2025, illustrating the heft of single-buyer influence in the UAE heat pump market.

Local engineering houses Al-Futtaim Engineering and DANA Group carve share by wrapping OEM equipment with financing, commissioning, and long-term service contracts calibrated to Dubai’s performance-guarantee culture. Technology niche players, including Rheem Middle East with its Centurion waste-heat-recovery package, differentiate through simultaneous cooling and 70 °C hot-water production, advertising up to 84 % energy savings for hotels and hospitals. As developers demand turnkey risk transfer, suppliers able to underwrite multiyear energy-savings guarantees will outpace catalog-only competitors.

UAE Heat Pump Industry Leaders

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

Trane Technologies plc

Carrier Global Corporation

Bosch Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Tabreed signed a framework agreement with Johnson Controls to supply variable-speed, low-GWP centrifugal chillers for upcoming district-cooling projects.

- February 2026: Ras Al Khaimah Wastewater Authority finalized a USD 300 million PPP with an EWE-Saur-TAQA consortium to build a low-carbon wastewater network that could incorporate heat pumps for effluent reuse.

- January 2026: Daikin secured the HVAC package for Burj Azizi, a flagship mixed-use tower in Dubai.

- November 2025: Daikin Middle East and Africa inaugurated a Jeddah plant producing chillers and hydronic heat pumps to serve Gulf markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, our study defines the United Arab Emirates heat pump market as all factory-built air-source, water-source, and ground (geothermal) source heat pump units rated up to one megawatt that provide space conditioning or sanitary hot water across residential, commercial, and industrial facilities in the seven Emirates.

Scope Exclusions: Standalone chillers, cooling-only VRF systems, and improvised retrofit kits are excluded from this assessment.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Analysts then interviewed district cooling operators, licensed HVAC installers, facility managers, and utility rebate officers across Dubai, Abu Dhabi, and Sharjah. These interactions validated coefficient of performance assumptions, retrofit cycle lengths, and average selling prices and filled gaps that secondary data could not address.

Desk Research

We began with open-access datasets from the UAE Federal Competitiveness and Statistics Center, Dubai Municipality green building permits, Abu Dhabi Department of Energy tariff bulletins, UN COMTRADE import codes, and the IEA heat pump sales dashboard, which together revealed the historic installed base, average capacity mix, and landed price bands. Primary regulations, such as ESMA's Minimum Energy Performance standards and Dubai's Clean Energy Strategy targets, provided the policy cadence that shapes rebate timing and retrofit urgency. Company filings, respected trade journal articles, Gulf HVAC Society white papers, and news flows captured through Dow Jones Factiva were layered on, while D&B Hoovers supplied shipment-level revenue splits that helped Mordor analysts reconcile vendor statements with customs volumes. The sources named illustrate the mix; many additional publications informed data gathering, cross-checks, and narrative clarity.

Market-Sizing & Forecasting

The 2025 market value was first derived through a top-down production and trade construct that scales declared imports and local assembly output by weighted average selling price. Results were corroborated with selective bottom-up roll-ups of distributor invoices and sampled project bills of quantity to fine-tune totals. Key variables in the model include new floor space additions, retrofit penetration, average COP, electricity tariff outlook, and Clean Energy Strategy milestones; each variable is forecast through multivariate regression, and missing bottom-up observations are tempered using three-year moving averages before integration.

Data Validation & Update Cycle

Outputs undergo anomaly checks against building permit and customs data, followed by dual analyst review before sign-off. Reports refresh every twelve months, with interim updates triggered when subsidies, import duties, or building code thresholds materially change.

Why Our UAE Heat Pump Baseline Commands Confidence

Published UAE heat pump estimates often diverge because firms choose different capacity bands, mingle HVAC products, or project tariffs in conflicting ways.

Our disciplined scope selection, annual field checks, and dual-path model limit such drift and keep results reproducible.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 332.8 M (2025) | Mordor Intelligence | - |

| USD 218.7 M (2024) | Regional Consultancy A | Excludes units above 100 kW and carries 2019 price points forward |

| USD 1.46 B (2024) | Global Consultancy B | Blends heat pumps with boilers and furnaces and applies regional average prices |

| USD 690 M (2024) | Industry Journal C | Counts announced projects as booked revenue and lacks import reconciliation |

The comparison shows that Mordor's variable-level calibrations, clear exclusions, and annual refresh cadence deliver a balanced, transparent baseline that decision makers can rely on with confidence.

Key Questions Answered in the Report

What is the current size of the UAE heat pump market and what growth rate is expected?

The UAE heat pump market was valued at USD 332.73 million in 2025, is estimated at USD 355.26 million in 2026, and is forecast to reach USD 478.51 million by 2031, registering a 6.14% CAGR between 2026-2031.

What share do air source units hold in the UAE heat pump market?

Air source systems captured 59.78% of 2025 installations, maintaining the largest slice among source types.

How quickly are retrofit projects expanding across the Emirates?

Retrofit installations are growing at a 6.93% CAGR over 2026-2031, driven by Dubai Supreme Council of Energy mandates and energy-service-company financing.

Which application segment shows the fastest growth momentum?

Industrial and process heating is advancing at a 6.71% CAGR as manufacturers replace steam boilers with high-temperature heat pumps.

Why are hybrid heat-pump systems favored for new hospitality developments?

They combine air-source units with chilled-water storage, ensuring reliable cooling during 45 °C summer peaks while shifting energy use to lower-cost off-peak hours.

What remains the main obstacle to scaling ground-source heat pumps in the UAE?

A shortage of certified drillers and loop-design specialists raises upfront costs and lengthens project timelines, limiting deployments to master-planned communities.

Page last updated on: