Turkey Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

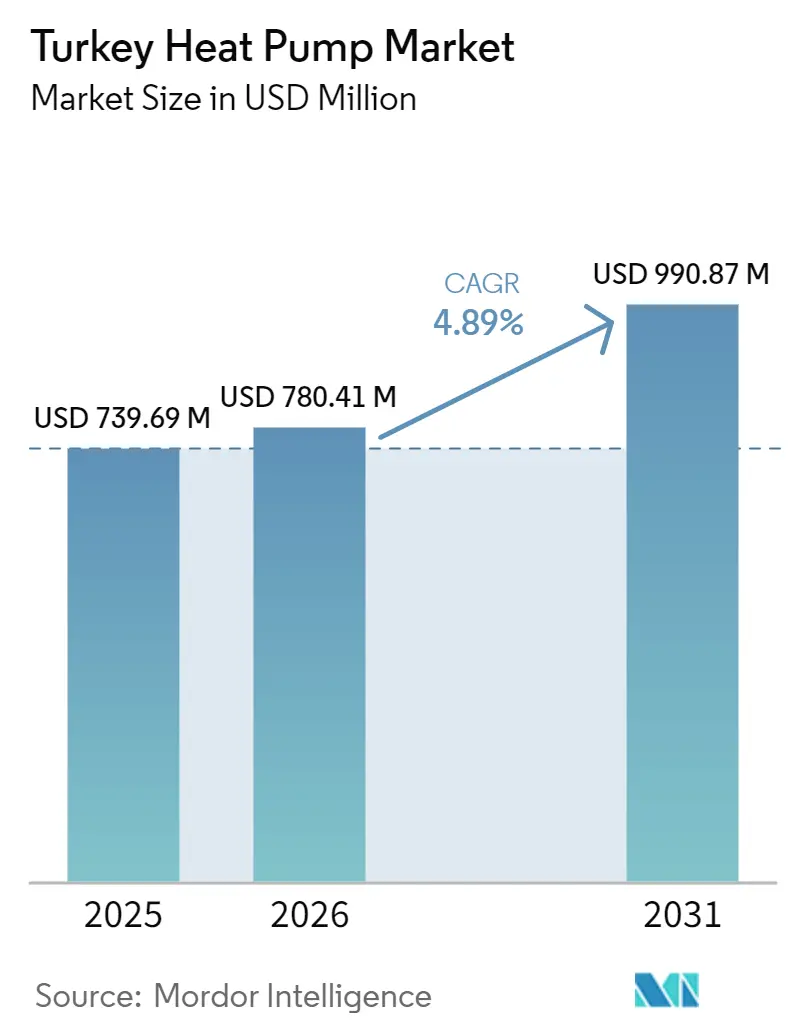

| Base Year Market Size (2025) | USD 739.69 Million |

| Market Size (2026) | USD 780.41 Million |

| Market Size (2031) | USD 990.87 Million |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Heat Pump Market Analysis by Mordor Intelligence

The Turkey heat pump market size is expected to increase from USD 780.41 million in 2026 to USD 990.87 million by 2031, growing at a CAGR of 4.89% over 2026-2031. The near-term rise is anchored in post-2025 building energy standards, industrial fuel-switching triggered by volatile imported gas prices, and reconstruction activity that favors efficient HVAC packages. Demand is further pulled by exporters seeking to comply with the EU Carbon Border Adjustment Mechanism, while a widening menu of state-backed loans brings down financing hurdles. Yet the Turkey heat pump market expands in the shadow of chronic lira weakness, grid bottlenecks in peri-urban zones, and earthquake-related budget shifts that delay deep retrofits. Unlike Western Europe, where subsidies spur mass residential uptake, Turkey relies more on the industrial economics of payback and on regulatory sticks that push large builders toward nearly-zero-energy designs. Competitive dynamics intensify as domestic producers add capacity and global majors scale Turkish plants for regional exports, keeping end-user prices in check and accelerating technology transfer.

Key Report Takeaways

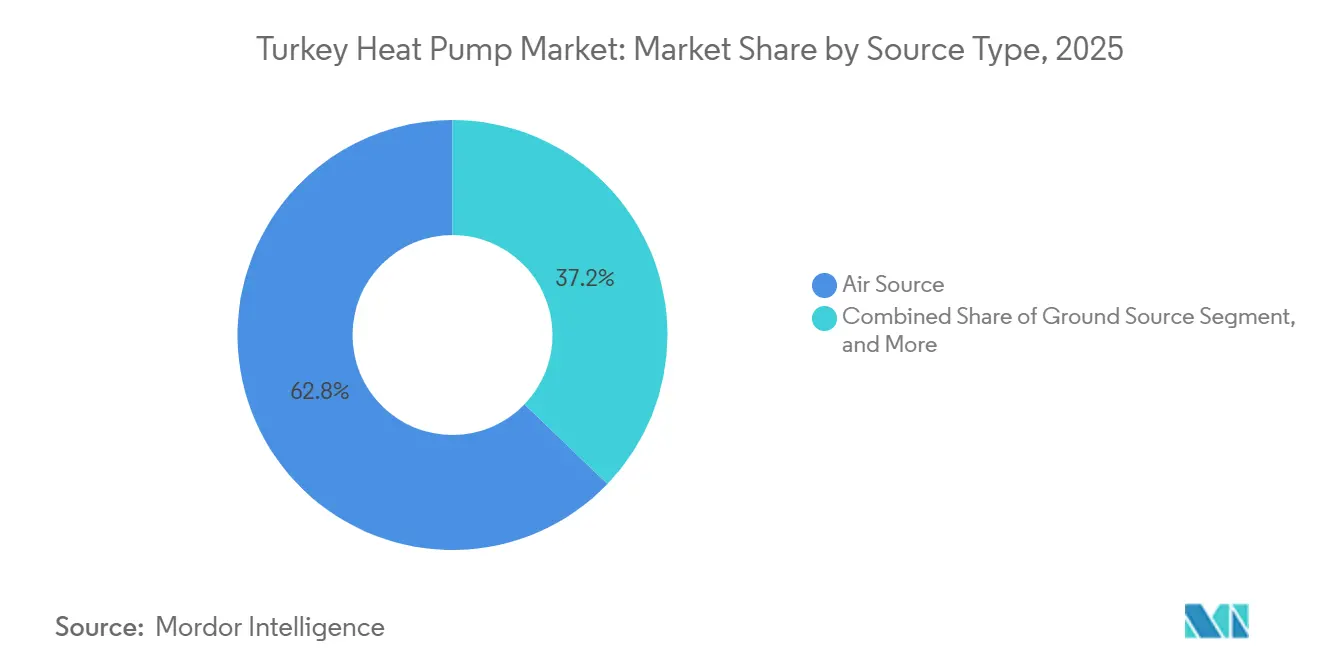

- By source type, air source systems led with 62.82% revenue share in 2025; hybrid configurations are projected to expand at a 5.18% CAGR through 2031.

- By technology, air-to-water models held 47.91% of 2025 revenue, while ground-to-water is forecast to register the fastest 5.31% CAGR to 2031.

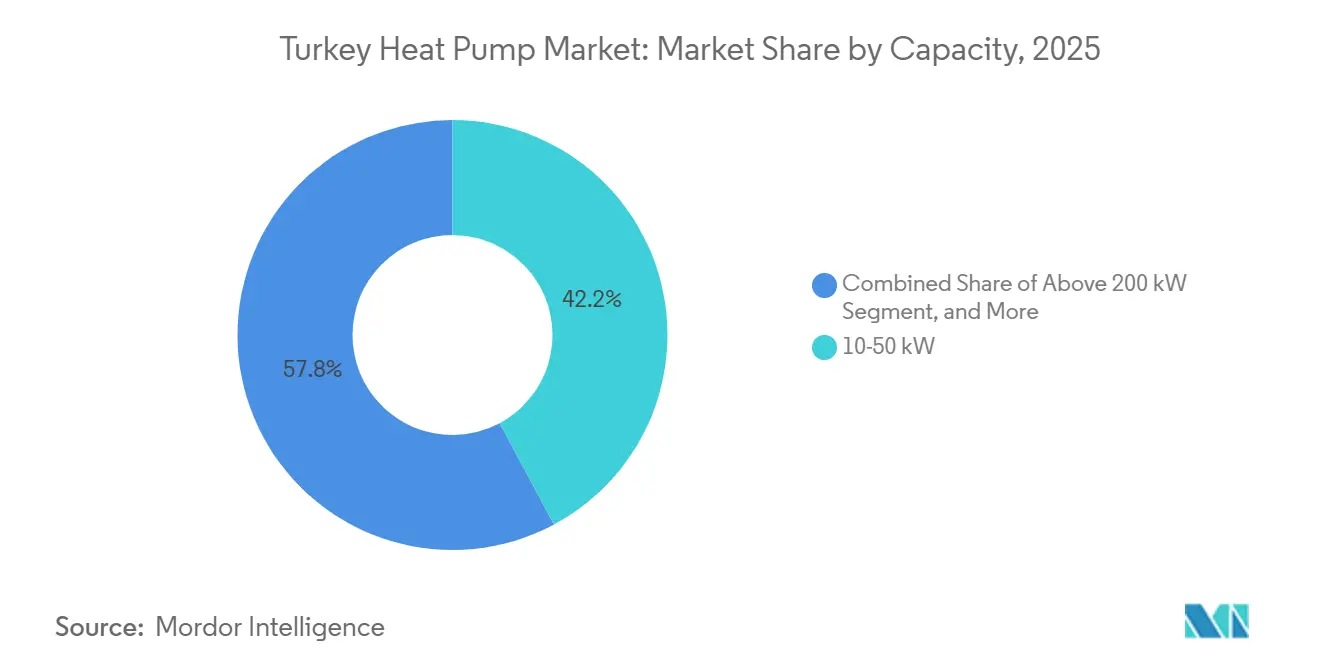

- By capacity, the 10-50 kilowatt band captured 42.17% of 2025 sales, whereas units above 200 kilowatts are set to grow at a 4.98% CAGR.

- By application, space heating accounted for 54.78% of 2025 revenue and industrial process heating is advancing at a 5.56% CAGR through 2031.

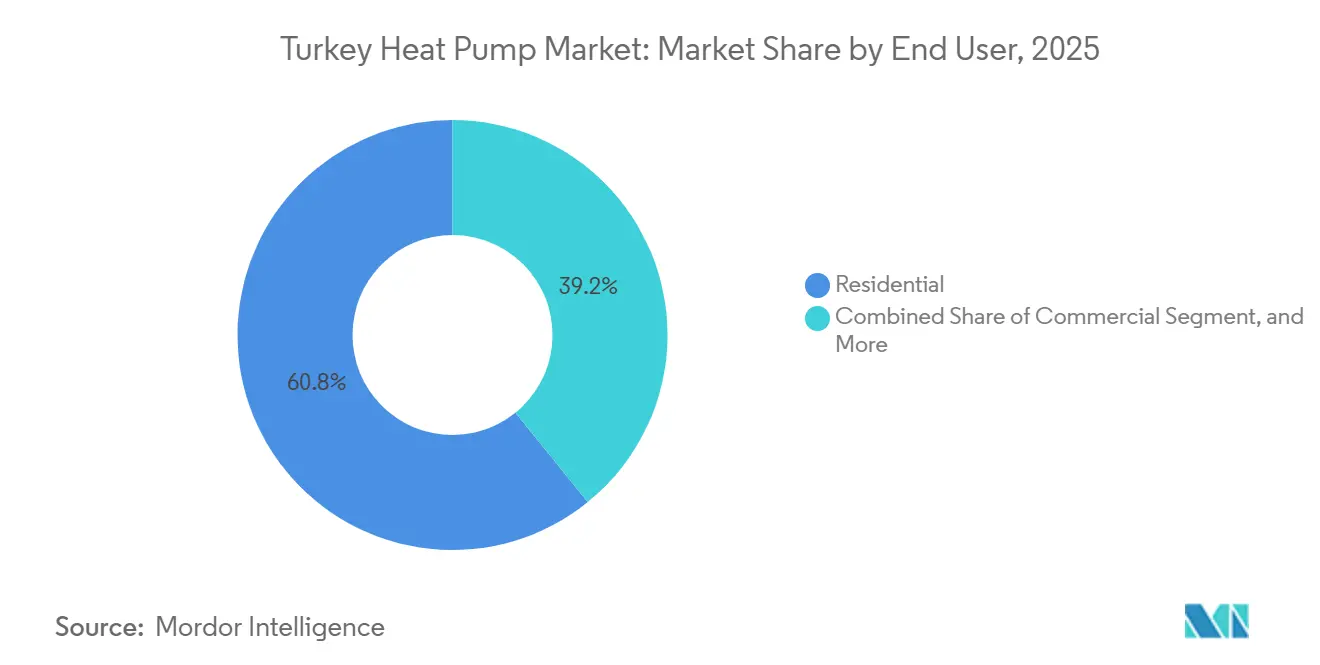

- By end user, the residential segment commanded 60.83% of 2025 demand; industrial customers are forecast to rise at a 5.39% CAGR and close part of that gap.

- By installation, new projects delivered 58.74% of 2025 revenue and retrofit activity is expanding at a 5.07% CAGR on the back of World Bank-financed public building upgrades.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-2025 Revision of Building Energy Performance Regulation | +1.2% | Marmara, Aegean, Mediterranean | Medium term (2-4 years) |

| Gas Import Price Volatility Driving Fuel-Switch | +1.0% | National, strongest in Marmara and Antalya | Short term (≤ 2 years) |

| EU Carbon Border Adjustment Mechanism Pressure on Export-oriented Industries | +0.8% | Marmara and Aegean corridors | Medium term (2-4 years) |

| Expansion of State-Owned Green Transformation Fund Heat Pump Loans | +0.6% | Istanbul, Ankara, Izmir first movers | Medium term (2-4 years) |

| Net-Metering Incentives for Renewable-Heat Coupling | +0.4% | High-irradiation south and southeast | Long term (≥ 4 years) |

| Green Hotel Certification Demands in Tourism Hubs | +0.3% | Mediterranean and Aegean resorts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-2025 Revision of Building Energy Performance Regulation

Revised TS 825 standards effective April 2025 require nearly-zero-energy performance for new buildings over 2,000 m², forcing developers to integrate high-efficiency heat pump packages. Exemptions for hot coastal districts split the Turkey heat pump market into cooling-dominant air-to-air demand along the shore and heating-biased air-to-water demand inland. Compliance hinges on Energy Performance Certificates, and municipal enforcement varies, rewarding suppliers that offer versatile product lines. Domestic firms with modular inverter platforms have already capitalized on this two-speed pattern, giving them a time-to-market edge over import-only competitors.[1]Invest in Türkiye, “Revised TS 825 standards raise efficiency bar,” invest.gov.tr

Gas Import Price Volatility Driving Fuel-Switch

Turkey’s January 2026 gas imports jumped 18.5% year on year, and the March 2026 energy shock pushed crude above USD 118 per barrel, narrowing industrial heat pump payback from 11.9 to 9.2 years. Each USD 10 rise in oil adds roughly USD 5 billion to the current-account gap, squeezing credit but simultaneously making electrified heat more attractive.[2]Reuters staff, “Turkey gas imports rise 18.5% year-on-year,” reuters.com Textile mills, food processors, and chemical plants in the Marmara belt are therefore accelerating retrofit programs, helped by equipment suppliers that now localize larger-capacity models.

EU Carbon Border Adjustment Mechanism Pressure on Export-Oriented Industries

The definitive CBAM phase in 2026 threatens Turkish steel, cement, and aluminum exports with EUR 1.1-1.8 billion in annual levies. Anticipating these costs, factories are installing process heat pumps that reach 80-300 °C at COPs of 2-4, cutting gas consumption and embedded carbon. Early flagship projects, like the 4.8 MW system at an İzmit tire plant, give peer manufacturers proof of concept and reassure lenders that the technology operates reliably without grid upgrades.[3]European Commission, “CBAM definitive phase guidance,” europa.eu

Expansion of State-Owned Green Transformation Fund Heat Pump Loans

The Efficiency Increasing Project and Energy and Carbon Reduction programs, underwritten by World Bank and Asian Infrastructure Investment Bank lines totaling USD 466 million, subsidize up to 30% of capital costs for qualifying heat pump projects. Uptake concentrates in Istanbul, Ankara, and Izmir, where project aggregation and technical advisers are plentiful, but rural penetration remains thin. Still, these loans underpin much of the forecast industrial build-out through 2031.[4]World Bank project team, “Turkey energy efficiency financing lines,” worldbank.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lira Depreciation Inflating Imported Component Costs | -0.9% | Nationwide, hardest on import-heavy assemblers | Short term (≤ 2 years) |

| Post-Earthquake Budget Reallocation Curtailing Social Housing | -0.6% | Kahramanmaraş, Hatay, Gaziantep cluster | Medium term (2-4 years) |

| Fragmented After-Sales Service Network | -0.4% | Central Anatolia, Black Sea | Medium term (2-4 years) |

| Grid Reinforcement Delays For High-Load Units | -0.3% | Peri-urban Marmara and Mediterranean | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lira Depreciation Inflating Imported Component Costs

Although headline inflation eased to 31.5% in February 2026, the lira’s slide lifted compressor and heat-exchanger prices by more than 30% since 2024. With imported parts still 60% of a typical bill of materials, domestic assemblers face squeezed margins and end users confront longer paybacks. High policy rates near 43% further dampen credit appetite, slowing adoption in price-sensitive residential and small commercial segments.[5]ING Economics, “Currency weakness and inflation outlook,” ing.com

Post-Earthquake Budget Reallocation Curtailing Social Housing

The 2023 earthquake rebuilding plan shifted funds toward rapid shelter delivery, sidelining previously earmarked efficiency upgrades. Thousands of new social homes now run on conventional gas boilers, locking in decades of fossil demand and reducing the demonstration effect that large heat-pump-based housing developments could have provided. International financing for efficiency remains available but is trickling in slowly due to procurement hurdles and limited installer depth in affected provinces.[6]World Bank, “Earthquake reconstruction financing update,” worldbank.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Systems Lead While Hybrids Accelerate

Air source units delivered 62.82% of 2025 revenue, a level that highlights their lower upfront cost and simple rooftop or façade placement. That dominance gives the Turkey heat pump market share edge to manufacturers specializing in single-fan monoblocs that fit dense urban plots. Hybrid systems, which couple an air source heat pump with a legacy gas boiler or a solar-thermal loop, are poised to post the fastest 5.18% CAGR through 2031 as owners hedge against peak-hour electricity tariffs that can triple winter evening rates. Water source designs stay niche because inland provinces lack permits for open-loop abstraction, while ground source uptake is curbed by drilling costs above TRL 100,000 (USD 2,240) per borehole and a shortage of IGSHPA-certified installers.

Hybrid popularity stems from the revised net-metering rule that lets households credit monthly photovoltaic exports, improving cash flow when the heat pump is idle in shoulder seasons. Hospitality chains on the Mediterranean coast now specify hybrid cascades that guarantee hot water during grid outages yet let compressors shoulder most of the annual run hours. This pragmatic mix unlocks latent demand in buildings that cannot absorb full electrification risk and gives the Turkey heat pump market size another high-growth pocket outside pure electric formats.

By Technology: Air-to-Water Dominates, Ground-to-Water Gains in Industry

Air-to-water technology captured 47.91% of 2025 turnover because it can deliver both space heating and domestic hot water through the same hydronic circuit. Builders erecting malls over 2,000 m² pivot to these systems to meet the post-2025 nearly-zero-energy code without adding parallel chillers. Ground-to-water solutions hold a smaller base yet are forecast to expand at a 5.31% CAGR as textile, food, and chemical plants in the Marmara belt chase steady COPs above 4.0 even in sub-zero weather. Air-to-air machines still dominate coastal cooling needs but carry lower price tags, limiting their revenue weight.

Water-to-water units appear mainly in district-energy pilots and metro-station waste-heat recovery trials. Recent compressors capable of 75 °C supply temperatures now let hospitals sanitize without electric resistors, widening the addressable industrial envelope. The technology split therefore keeps evolving, and the accelerating ground-to-water slice lifts the overall Turkey heat pump market size tied to high-grade process heat.

By Capacity: Mid-Range Units Prevail, Megawatt-Scale Installs Gain Momentum

Systems rated 10-50 kW produced 42.17% of 2025 sales, mirroring Turkey’s mid-sized retail and light-industrial footprint. Their plug-and-play format lets installers finish within a single workweek, holding labor costs below 25% of the invoice. Capacity bands between 50 kW and 200 kW serve hotels and hospitals yet require hydraulic balancing and noise attenuation, keeping uptake moderate for now. Units above 200 kW are the fastest climber, registering a 4.98% CAGR, because export plants see two-digit gas savings when megawatt-scale compressors displace boilers.

Smart-meter mandates reaching 70% penetration by 2027 support demand-response contracts that reward large users for off-peak operation, trimming payback to single digits. Sub-10 kW split heat pumps must compete with three-million-unit annual mini-split imports, but policy shifts that narrow the tariff gap between gas and electricity could swing homeowners toward electric heating later in the decade. These dynamics protect the current Turkey heat pump market share pattern but leave room for capacity-mix flips if fuel-price spreads change sharply.

By Application: Space Heating Still Commands, Process Loads Surge

Space heating contributed 54.78% of 2025 demand because Ankara, Konya, and Kayseri face 4,000-plus heating degree-days each winter. Retrofits that swap out 20-year-old cast-iron boilers for inverter heat pumps deliver seasonal savings above 30%, enticing condominium boards despite high capital costs. Industrial and process heat logs the quickest 5.56% CAGR as EU carbon pricing bears down on steel and cement exporters. Cooling, bundled in reversible models, earns incremental revenue in Aegean resorts where air-conditioning ownership lags European peers.

Domestic hot water represents roughly 12% of installed units, and suppliers now tout 75 °C outlet temperatures that match Turkish bathing preferences without resistive backup. Agricultural drier heat pumps, which cut energy use 70-80% in fruit and vegetable dehydration, unlock a side stream of rural demand. These new niches combine to elevate the Turkey heat pump market size beyond a pure space-heating narrative.

By End User: Homes Lead but Factories Gain Speed

Residential customers delivered 60.83% of 2025 volume, anchored in natural-gas boiler replacement and new multifamily builds above the 2,000 m² code threshold. Inflation and currency swings lengthen household payback, yet rooftop solar pairings shorten it again as self-consumption rises. Industrial buyers post the fastest 5.39% CAGR because heat pumps slash gas exposure and help dodge future CBAM levies. Commercial real estate sits in the middle, with universities and shopping centers stacking grants under the Green Transformation Fund to hit internal rates above 12%.

Service-contract models that bundle monitoring and maintenance over ten years resonate with factory owners that lack in-house HVAC staff. Meanwhile, social housing rebuilds in quake-hit provinces defaulted to gas boilers, momentarily capping residential upside but leaving latent retrofit potential once reconstruction stabilizes. Net, the Turkey heat pump market share will tilt slowly toward industrial meter points through 2031.

By Installation: Code-Driven New Builds Dominate, Retrofits Close In

New projects made up 58.74% of 2025 revenue as developers race to meet nearly-zero-energy rules without paying carbon penalties later. Prefabricated plant rooms shave weeks off construction calendars and lower interest carry, strengthening the economics of pre-integrated heat-pump-with-storage kits. Retrofits expand at a 5.07% CAGR because World Bank-financed upgrades in 370 public buildings proved 40% energy savings can be captured with off-the-shelf equipment.

Retrofit margins exceed new-build levels because ancillary works, radiator swaps, panel upgrades, glycol fills, boost average ticket sizes. Early adopters in Istanbul’s Grade-III heritage stock report seasonal performance factors above 3.4 even with single-pane glazing, debunking a legacy myth that heat pumps suit only new insulation. As funding widens to secondary cities, retrofit share of the Turkey heat pump market size should edge toward parity with new installations.

Geography Analysis

Marmara, anchored by Istanbul, Bursa, and Kocaeli, generates roughly 45% of national installations, underpinned by export-heavy industry and higher disposable incomes. The region’s dense installer ecosystem and short supply chains reduce soft costs, prompting OEMs to cluster manufacturing nearby. Yet feeder substations lag rising electrification, and builders report multi-month waits for grid approvals on high-load applications. The Turkey heat pump market therefore sees Marmara demand constrained more by infrastructure than by latent preference.

The Aegean and Mediterranean coasts form a cooling-dominant sub-market where tourism properties interplay with green hotel certification and EU package-tour standards. High solar irradiation strengthens the business case for photovoltaic-coupled heat pumps, a pairing that mitigates summer peaks and winter tariff spikes. Nonetheless, milder winters curb absolute heating loads, muting market size versus colder inland provinces. Suppliers that tailor compact, reversible systems with corrosion-resistant coils capture share among seafront hotels coping with salty air.

Central Anatolia and the Black Sea witness slower penetration due to dispersed populations and limited finance reach. However, absent piped gas in many rural towns removes the incumbency barrier that gas boilers pose elsewhere. As installer training expands and on-bill financing pilots roll out, these regions can deliver catch-up growth post-2027, especially in agricultural processing where low-temperature dryers adopt heat pump solutions to tap feed-in incentives for biomass waste heat.

Competitive Landscape

Rivalry in the Turkey heat pump market intensified after 2024 when domestic and foreign players alike announced multi-year capacity additions. COPA’s Bursa facility can now turn out 100,000 units annually, making it the first local firm with European Heat Pump Association membership. Mitsubishi Electric lifted Manisa output to 300,000 air-to-water units per year, and Daikin committed EUR 100 million (USD 110 million) to its Sakarya plant with a Copeland joint venture that will localize compressors by 2026. Baymak, backed by BDR Thermea, logged 90% heat pump revenue growth in 2025 and retooled its Manisa campus into a renewables hub, while Varmeks and Solimpeks ride domestic hot-water and PV-thermal hybrids to double-digit gains.

None of the top suppliers holds more than 15% share, keeping the Herfindahl-Hirschman Index in the moderately concentrated zone. Imported core parts still account for about 60% of a typical bill of materials, so lira depreciation compresses margins even for firms with in-country assembly. That currency risk pushes manufacturers to integrate upstream; COPA has already sourced blower motors locally and is scouting inverter PCB partners, and Mitsubishi is evaluating Turkish copper-tube pullers. Service remains the weakest link, especially east of Ankara, where installers pass on rural calls to metropolitan subcontractors, eroding customer satisfaction and leaving white space for third-party service aggregators.

Energy service companies add another layer of competition. Enerjisa’s 4.8 MW contracting deal at the İzmit tire plant validated an off-balance-sheet model that industrial CFOs find appealing, and Johnson Controls now bundles long-term performance insurance with each 45-700 kW unit shipped from Izmir. As regulatory pressure tightens and grid tariffs swing, the winning formula combines localized hardware, supply-chain hedges, and nationwide after-sales coverage. Those conditions keep price discipline and ensure that scale advantages do not yet translate into dominant Turkey heat pump market share for any single brand.

Turkey Heat Pump Industry Leaders

Carrier Global Corporation

Vaillant Group

Bosch Group

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Enerjisa Enerji and Brisa completed a 4.8 MW industrial heat pump at Brisa’s İzmit tire plant, targeting 4.3 million m³ annual gas savings and 6,180 t CO₂ cuts.

- December 2025: Daikin confirmed completion of EUR 100 million (USD 110 million) multi-year investment at its Sakarya plant and outlined a joint venture with Copeland to localize core components by 2026.

- August 2024: COPA Isı Sistemleri opened a EUR 3.5 million ( USD 4.1 million) Bursa facility with 100,000-unit output, becoming the first Turkish manufacturer admitted to the European Heat Pump Association.

- June 2024: ISKID joined the European Heat Pump Association, formalizing knowledge exchange on installer training and policy advocacy.

Turkey Heat Pump Market Report Scope

| Air Source |

| Water Source |

| Ground Source |

| Hybrid |

| Air-to-Air |

| Air-to-Water |

| Water-to-Water |

| Ground-to-Water |

| Below 10 kW |

| 10-50 kW |

| 50-200 kW |

| Above 200 kW |

| Space Heating |

| Space Cooling |

| Domestic and Sanitary Hot Water |

| Industrial and Process Heating |

| Other Applications |

| Residential |

| Commercial |

| Industrial |

| New Installation |

| Retrofit |

| By Source Type | Air Source |

| Water Source | |

| Ground Source | |

| Hybrid | |

| By Technology | Air-to-Air |

| Air-to-Water | |

| Water-to-Water | |

| Ground-to-Water | |

| By Capacity | Below 10 kW |

| 10-50 kW | |

| 50-200 kW | |

| Above 200 kW | |

| By Application | Space Heating |

| Space Cooling | |

| Domestic and Sanitary Hot Water | |

| Industrial and Process Heating | |

| Other Applications | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Installation | New Installation |

| Retrofit |

Key Questions Answered in the Report

What is the projected value of the Turkey heat pump market in 2031?

Forecasts point to USD 990.87 million by 2031, up from USD 780.41 million in 2026.

How fast is the sector expected to grow between 2026 and 2031?

The compound annual growth rate is projected at 4.89% over the six-year span.

Which source type currently dominates sales?

Air source units lead with 62.82% of 2025 revenue, though hybrids are growing the fastest.

Why are industrial users accelerating adoption?

Volatile imported gas prices and looming EU carbon taxes shorten payback periods, making electrified heat attractive for export-oriented factories.

What is the main restraint on wider residential uptake?

Lira depreciation inflates imported component costs, extending payback and curbing willingness to invest among households.

Are local manufacturers competitive with global brands?

Yes, domestic firms control roughly 35% of revenue thanks to plant expansions, but they still rely on imported compressors and valves, leaving room for further localization.

Page last updated on: