KSA Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

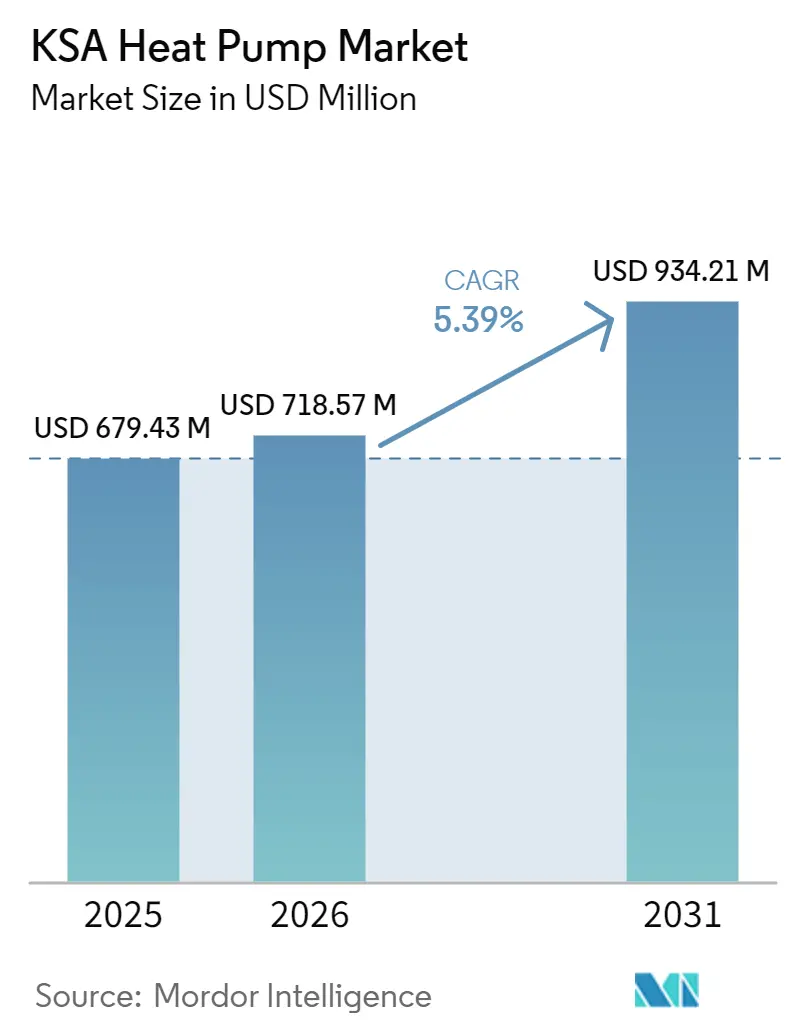

| Base Year Market Size (2025) | USD 679.43 Million |

| Market Size (2026) | USD 718.57 Million |

| Market Size (2031) | USD 934.21 Million |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

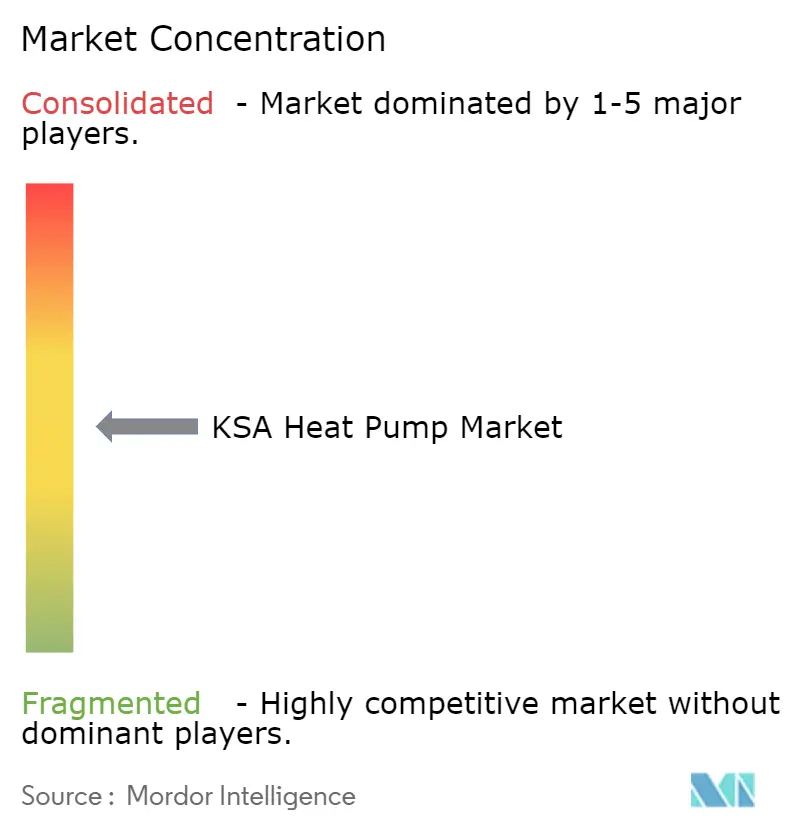

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

KSA Heat Pump Market Analysis by Mordor Intelligence

The KSA heat pump market size was valued at USD 679.43 million in 2025 and is estimated to grow from USD 718.57 million in 2026 to reach USD 934.21 million by 2031, at a CAGR of 5.39% during the forecast period (2026-2031). Expanding giga-project construction, rising electricity tariffs that penalize inefficient cooling, and Vision 2030 efficiency mandates are steering buyers toward electric heat pump solutions. Extreme summer temperatures that routinely top 50 °C intensify cooling demand, while process industries look to recover waste heat for hot-water and steam duties. Global and regional suppliers are localizing production to meet preference for Saudi content, and installer training programs are gradually easing the skills gap that previously delayed project commissioning. Although variable refrigerant flow (VRF) systems still dominate many commercial specifications, comparative lifecycle economics are shifting decisively in favor of high-ambient-rated heat pumps.

Key Report Takeaways

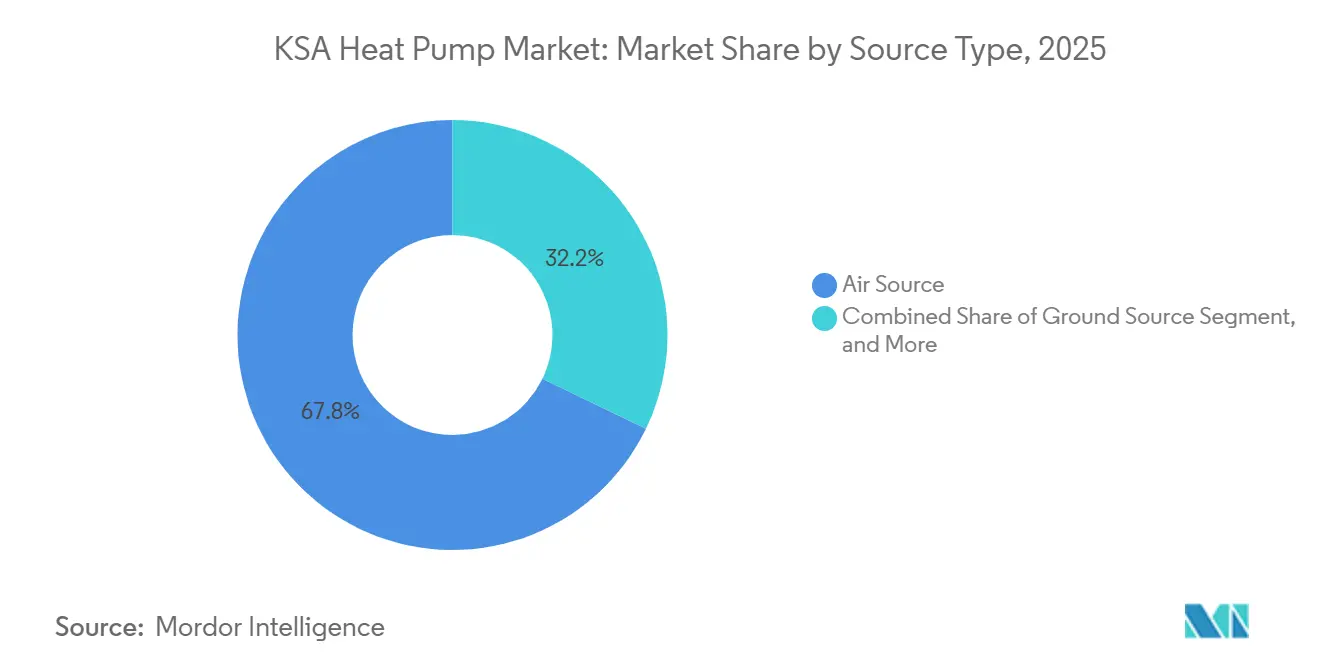

- By source type, air source systems led with 67.81% revenue share in 2025, while hybrid configurations are forecast to post the fastest 5.82% CAGR through 2031.

- By technology, air-to-air technology accounted for 54.42% share in 2025, and ground-to-water units are projected to expand at a 5.02% CAGR over 2026-2031 in the Saudi Arabia heat pump market.

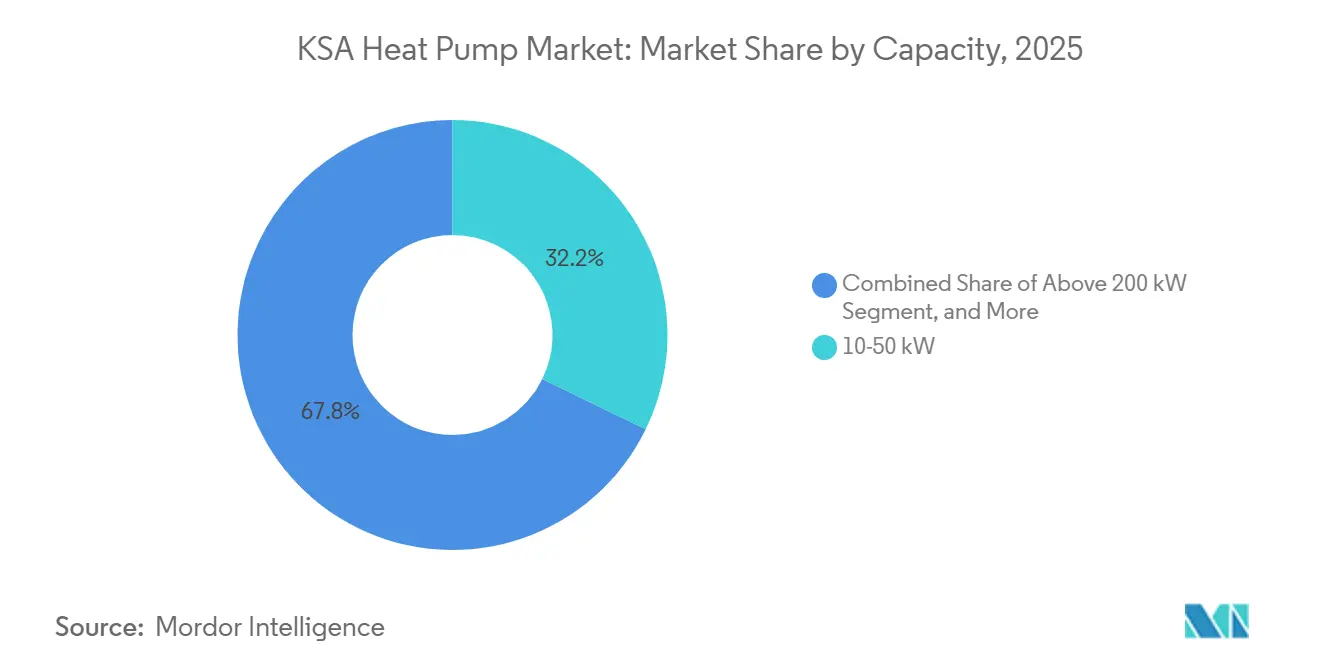

- By capacity, the 10-50 kilowatt band captured 32.23% of the KSA heat pump market share in 2025, and above-200 kilowatt industrial units are positioned to grow at 5.93% CAGR to 2031.

- By application, space cooling dominated with 59.82% of the KSA heat pump market size in 2025, whereas industrial and process heating is set to advance at a 5.76% CAGR during the forecast window.

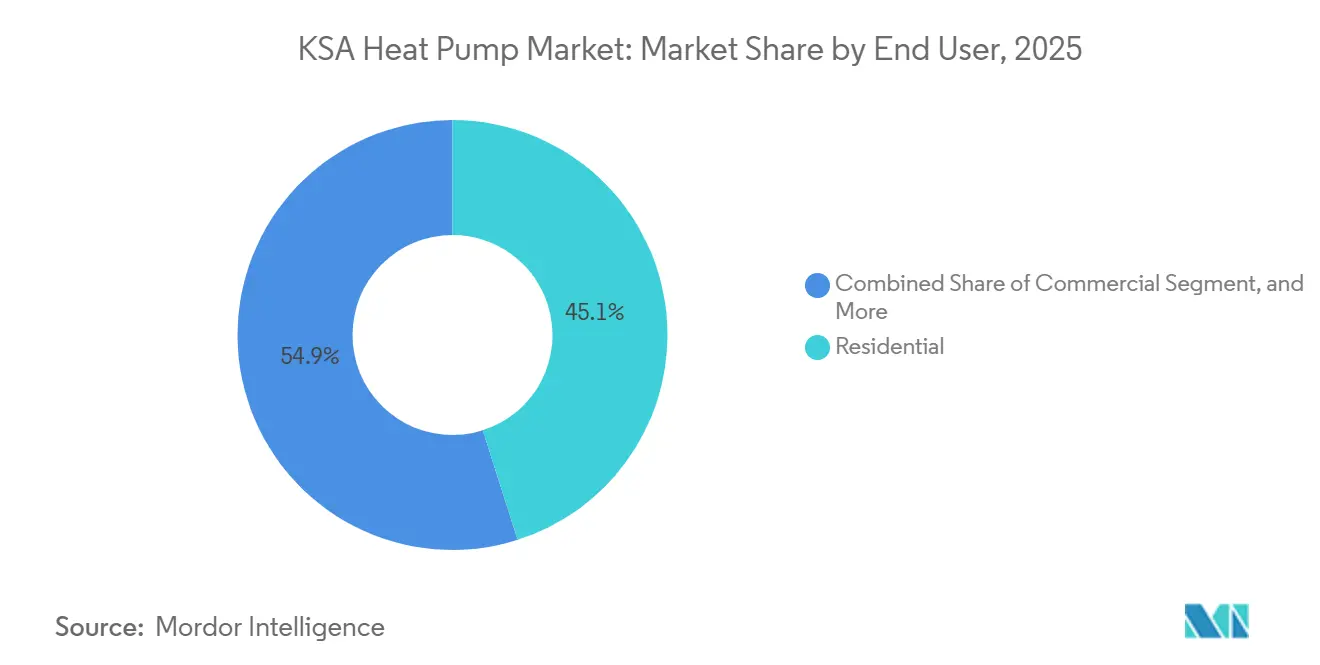

- By end user, residential users held 45.09% share in 2025, while industrial facilities are projected to register the fastest 5.47% CAGR in the Kingdom of Saudi Arabia heat pump market.

- By installation, retrofit projects commanded 55.43% of 2025 installations, and new-build deployments are forecast to rise at a 5.56% CAGR as giga-project master plans specify heat pumps from day one.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

KSA Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NEOM and Other Giga-Project Construction Pipeline Continues to Drive HVAC Demand | +1.2% | National, concentrated in NEOM, Red Sea Project, Qiddiya | Medium term (2-4 years) |

| Rising Electricity Tariffs Following Energy Subsidy Reforms Encourage Energy-Efficient Heat Pumps | +0.9% | National, high impact in commercial and industrial segments | Short term (≤ 2 years) |

| Extreme Summer Temperatures Up to 50 °C Increase Cooling Loads | +0.7% | National, peak in Riyadh, Eastern Province, inland deserts | Long term (≥ 4 years) |

| Saudi Vision 2030 SEEP Rebates Promote Heat Pump Adoption | +0.6% | National, early uptake in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| District-Cooling Operators Adding Heat-Recovery Loops Opening Hybrid Opportunities | +0.4% | Riyadh, Jeddah, Dammam, King Abdullah Economic City | Medium term (2-4 years) |

| Green Hydrogen Desalination Plants Specifying Industrial Heat Pumps for Waste-Heat Utilization | +0.3% | NEOM, Ras Al-Khair, Yanbu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NEOM and Other Giga-Project Construction Pipeline Continues to Drive HVAC Demand

Saudi Arabia’s multibillion-dollar developments, NEOM, Qiddiya, and the Red Sea resorts, embed net-zero operational targets that specify electrified thermal systems, creating a steady requirement for high-ambient-rated heat pumps. Master plans allocate centralized district cooling capacity with integrated heat-recovery loops, a configuration that elevates hybrid heat pump economics.[1]NEOM Company, “The Line and OXAGON Sustainable Building Standards,” neom.com Procurement rules favor local manufacturing, prompting Daikin, LG, and Carrier to break ground on Saudi plants that will supply hydronic and air-source units directly into giga-project supply chains. Construction timelines stretching well into the next decade anchor demand in the medium term, yet phased township rollouts ensure volume beyond 2030. The continuous stream of mixed-use, hospitality, and industrial parcels under the giga-project umbrella provides contractors with predictable workload, which in turn accelerates installer skill development. As early phases go live, operating data from high-ambient test beds is expected to validate performance claims and spur replication across second-wave zones.

Rising Electricity Tariffs Following Energy Subsidy Reforms Encourage Energy-Efficient Heat Pumps

Tariff reforms lifted commercial rates to SAR 0.22-0.32 (USD 0.06-0.08) per kWh, altering lifetime cost comparisons in favor of heat pumps that deliver coefficients of performance above 3.0.[2]Saudi Electricity Company, “Tariff Guide 2025,” se.com.sa Shopping malls, hospitals, and hotels are retrofitting aging chillers with air-to-water units that trim peak charges exceeding SAR 60 (USD 15) per kW during summer months. Industrial operators exploiting condenser heat for simultaneous hot-water duties report effective COP values above 5.0, compressing payback periods to as low as three years. Utility-mandated energy audits under Tarshid add regulatory urgency, nudging laggards toward high-efficiency retrofits. Although residential savings per household are smaller, multi-family developers now adopt central heat pumps to comply with Saudi Building Code performance thresholds. The price signal is immediate and nationwide, making this driver particularly potent in the short term.

Extreme Summer Temperatures up to 50 °C Increase Cooling Loads

Ambient peaks above 50 °C in Riyadh and Dammam test the limits of conventional air conditioning; compressors derate and refrigerants degrade under continual thermal stress. New high-ambient models such as Mitsubishi Electric Trane’s ecodan Pro CAHV, rated for 55 °C operation, sustain nameplate output and reduce failure rates.[3]Mitsubishi Electric Trane HVAC, “ecodan Pro CAHV Product Sheet,” mitsubishielectric-trane.com The harsh climate also amplifies the value of heat recovery, as waste heat from kitchens and data centers can be redirected to domestic hot-water storage rather than rejected outdoors. Climate models from the National Center for Meteorology project an additional 1.5-2.0 °C rise by 2040, extending the cooling season and underpinning long-run demand. Regional disparities emerge; inland cities adopt high-temperature-tolerant units first, while coastal zones focus on dehumidification efficiency. Manufacturers able to guarantee stable capacity at peak ambient conditions gain a decisive competitive edge.

Saudi Vision 2030 SEEP Rebates Promote Heat Pump Adoption

The Saudi Energy Efficiency Program reimburses 20-30% of incremental equipment costs for residential and small commercial buyers that replace legacy units with high-efficiency heat pumps.[4]Saudi Energy Efficiency Center, “SEEP Incentive Scheme,” seec.gov.sa Rebates of up to SAR 3,000 (USD 800) per eligible residential system lift affordability in the price-sensitive villa market. Commercial incentives structured as tax credits reward projects exceeding SAR 500,000 (USD 133,000) in qualifying spend, steering mid-sized offices, hotels, and retail complexes toward centralized air-to-water solutions. Alignment between SEEP, Saudi Standards SASO 2874:2025, and municipal permitting streamlines compliance; installers deliver pre-certified equipment confident that inspections will clear without delay. Utilities layering time-of-use tariffs on top of rebates further improve the business case by rewarding off-peak operation. The combination of financial and regulatory levers sustains momentum in the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Heat Pump Installers Limits Quality Assurance | -0.5% | National, acute outside Riyadh-Jeddah-Dammam corridor | Short term (≤ 2 years) |

| Dominance of VRF Systems in Commercial Buildings Crowds Out Heat Pumps | -0.4% | Urban commercial districts in Riyadh, Jeddah, Dammam, Al Khobar | Medium term (2-4 years) |

| High Upfront Capital Costs Versus Conventional AC-Chiller Systems | -0.3% | National, affects price-sensitive residential and small commercial buyers | Short term (≤ 2 years) |

| High Salinity Groundwater Hampers Ground-Source Loop Efficiency Outside Eastern Province | -0.2% | Western Province, Northern Border, Tabuk | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Heat Pump Installers Limits Quality Assurance

The installer base, historically trained on split air conditioners, often lacks competence in refrigerant charging, hydronic balancing, and controls commissioning. Eurovent Middle East’s F-Gas program certified fewer than 500 Saudi technicians by 2025, well below the 5,000-7,000 needed to sustain forecast installation growth.[5]Eurovent Middle East, “F-Gas Certification Uptake Report 2025,” eurovent-me.eu Skill shortages drive callback costs from leaks and sensor misplacement, eroding buyer confidence, especially in the residential segment where technical oversight is minimal. Manufacturers have opened training centers; LG partnered with the Technical and Vocational Training Corporation to develop a tropical-climate HVAC curriculum, yet the first graduating cohorts will not meaningfully swell the workforce until after 2027. In secondary cities such as Tabuk and Hail, limited contractor capacity delays project timelines, prompting some developers to import labor at higher cost. A coordinated upskilling push remains critical to unlocking near-term volume.

Dominance of VRF Systems in Commercial Buildings Crowds Out Heat Pumps

VRF captured an estimated USD 0.194 billion of Saudi commercial HVAC spend in 2024, offering modular scalability and zone-level control that designers know well. Carrier’s joint venture with PIF-backed Alat to manufacture VRF units locally strengthens incumbency by ensuring supply certainty under Vision 2030 content rules.[6]Carrier Global Corporation, “Alat JV Announcement,” carrier.com Heat pumps that rely on hydronic distribution face specification resistance because chilled-water pipes and plant rooms add design complexity and floor-area penalties. Mechanical engineers under schedule pressure default to the familiar VRF template even where lifecycle models show lower total cost of ownership for heat pumps. Vendors now market air-to-air heat pumps that mimic VRF refrigerant routing while offering heat-recovery benefits, but acceptance remains limited in Riyadh’s and Jeddah’s high-rise pipelines. Without stronger policy nudges or proof-of-concept showcases, VRF may continue to siphon demand in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominance Meets Hybrid Innovation

Air source units secured 67.81% of 2025 installations, underscoring their fit for retrofit jobs where rooftop package replacements avoid drilling or water-side works. Product standardization across 5-200 kW ratings and factory-preset controls reduces commissioning errors and shortens project cycles. The KSA heat pump market benefits from Daikin, LG, and Panasonic partnerships that channel localized production through established distributors, keeping lead times low. Hybrid systems, which combine air source heat pumps with boilers or solar thermal panels, are forecast at a brisk 5.82% CAGR as district-cooling operators retrofit heat-recovery loops. Water source configurations remain niche due to fouling and maintenance risks in Saudi’s saline water, while drilling costs of SAR 400-600 per meter constrain ground source roll-outs beyond Eastern Province aquifers. Ground-to-water pilots at healthcare sites demonstrate seasonal efficiency gains but await sustained cost reduction to scale.

Growing investor appetite for local manufacturing has spurred Panasonic’s alliance with Alessa to expand residential air-source inventories, and Mitsubishi Electric Trane’s 55 °C-rated models now address peak-temperature derating. As giga-project phases progress, hybrid air-water plants that satisfy both space cooling and domestic hot-water demand are set to widen market share without displacing the entrenched air-only base. Standardized, high-ambient-rated platforms provide a technology bridge until drilling and corrosion challenges of geothermal loops are economically resolved.

By Technology: Air-To-Air Leads, Ground-to-Water Gains Traction

Air-to-air solutions held 54.42% share in 2025, reflecting the dominance of space cooling in villas, apartments, and small commercial premises. Their plug-and-play nature lets contractors swap units quickly, lowering downtime. Conversely, air-to-water and ground-to-water designs deliver both chilled and hot water, suiting applications with simultaneous cooling and sanitary hot-water loads. Ground-to-water is the fastest-growing at 5.02% CAGR as NEOM pilots showcase consistent performance across summer peaks and mild winters. Innovations such as polymer-coated heat-exchanger loops counter high-salinity corrosion, while closed-loop glycol circuits avoid aquifer contamination.

Meanwhile, Olympic Village’s 2025 pool complex in Jeddah demonstrated an integrated heat-recovery scheme that slashed resistance-heater energy by 75%. Manufacturers now promote hybrid architectures that recapture condenser heat, pushing effective COPs above 5.0 in commercial kitchens and laundries. Within five years, growth of ground-to-water solutions may increasingly come from industrial estates where borehole drilling can be shared among clustered factories, further diversifying the technology mix in the KSA heat pump market.

By Capacity: Mid-Range Dominates, Industrial Scale Accelerates

Mid-sized 10-50 kW units represented 32.23% of the KSA heat pump market size in 2025, aligning with typical loads for restaurants, clinics, and multi-family blocks. Their popularity stems from readily available rooftop footprints and electrical service compatibility. Above-200 kW systems depict the steepest growth path at 5.93% CAGR, fueled by petrochemical, desalination, and food-processing retrofits that need high-temperature steam or hot water. Megawatt-scale platforms such as HEATEN’s HeatBooster deliver 180-200 °C process heat and can substitute natural-gas boilers entirely.

Manufacturers advocate modular parallel configurations of 50-100 kW chassis to build redundancy and phase capital outlay. Sub-10 kW residential machines face saturation and stiff price competition from commodity split air conditioners, muting volume upside. Demand from NEOM’s green hydrogen electrolysis facilities is likely to add multi-megawatt orders as operators seek to recover electrolyzer waste heat, indicating that industrial scale will gradually carve a larger slice of the KSA heat pump market beyond traditional building-services boundaries.

By Application: Cooling Prevails, Industrial Heating Emerges

Space cooling accrued 59.82% of demand in 2025, a direct response to relentless desert heat. Typical office cooling loads of 200-250 W per m² in summer keep compressors running nearly year-round. Yet process industries now recognize the economic potential of high-temperature heat pumps for steam duties; industrial heating is projected to rise at a 5.76% CAGR to 2031. Recent pilot rigs at petrochemical plants validated that condenser heat previously dumped to atmosphere can drive desalination pre-heaters or cleaning baths. Domestic hot-water systems in hotels and hospitals embed heat-recovery loops that push system COPs above 5.0 when both cooling and hot-water outputs are monetized.

Space heating stays marginal outside northern winters, though luxury villas are installing under-floor systems for December-February comfort based on low-temperature water circuits. Greenhouse agriculture, pool heating, and data-center waste-heat reuse represent newly forming niches. Even though individually small, these applications attract premium margins and highlight diversified growth avenues for providers in the KSA heat pump market.

By End User: Residential Leads, Industrial Surges

Residential customers commanded 45.09% share in 2025, supported by SEEP rebates lowering upfront barriers and by villa owners chasing lower electricity bills. Developers of multi-family towers integrate centralized heat pumps to satisfy Saudi Building Code targets without expanding electrical service connections. Industrial buyers exhibit the fastest 5.47% CAGR, catalyzed by diversification into non-oil manufacturing segments that demand simultaneous cooling and clean process heat.

Commercial buildings, malls, offices, hospitals, form a mature channel where heat pumps contend with entrenched VRF networks; nevertheless, energy service companies offering heat-pump-as-a-service contracts are unlocking deferred retrofit pipelines. LG’s partnership with Shaker Group and Bosch’s acquisition of Johnson Controls’ HVAC business intensify competition, bringing localized manufacturing scale and broader after-sales coverage that reassure conservative industrial purchasing committees.

By Installation: Retrofit Dominates as New-Build Adoption Accelerates

Retrofit projects captured 55.43% of the KSA heat pump market share in 2025, reflecting owners’ urgency to replace aging chillers and split units that now incur higher electricity charges. The segment benefits from standardized rooftop and packaged replacements that fit existing footprints, so contractors avoid structural alterations and lengthy permitting. SEEP rebates covering up to 30% of incremental equipment cost further cut payback periods, while rising peak-demand fees push malls, hospitals, and villas to prioritize high-efficiency swaps. Installer familiarity with air-source platforms has reduced commissioning errors and shortened downtime, encouraging facility managers to phase retrofits building by building. As tariff reform matures, retrofit momentum is expected to hold steady even as new-build volumes climb.

New installations are forecast to expand at a 5.56% CAGR through 2031, riding the giga-project pipeline that hard-codes heat pumps into master specifications from day one. NEOM, Qiddiya, and Red Sea developments insist on electrified thermal systems to meet net-zero targets, so designers size hydronic loops and electrical service for heat pumps rather than VRF or boiler-chiller combinations. Modular plantrooms that stack multiple 50-100 kW units allow phased capital outlay and redundancy, easing developer concerns about first-cost premiums. Standardized product platforms and factory-set controls now blur the historical complexity gap between heat pumps and VRF, moving the KSA heat pump market size for new-builds closer to retrofit volumes over the forecast horizon. Continued growth in local manufacturing and installer training will further narrow cost differentials, positioning new construction as an equal contributor to long-term demand.

Geography Analysis

Riyadh and the broader central region anchor early adoption thanks to dual extremes of scorching summers and chilly winter nights. Giga-projects such as Qiddiya embed district cooling schemes with heat-recovery loops, providing showcase data for hybrid configurations. Local aquifers of moderate salinity enable pilot geothermal bores like Strataphy’s hospital project, offering proof points for ground-source viability

The Eastern Province, home to refinery, petrochemical, and desalination clusters, leads industrial heat-pump deployment. Waste-heat integration into steam and hot-water circuits at Jubail plants cuts natural gas reliance while satisfying corporate carbon targets. Coastal humidity creates high latent loads, a condition where heat pumps outperform direct-expansion chillers. Lower aquifer salinity further favors ground-source investments; EDF’s 2025 memorandum with Taqa explores geothermal district cooling in the region.

Western Province tourism hubs, especially Jeddah and Red Sea resorts, focus on air-to-water systems that channel heat rejection into pool and domestic-hot-water duties. Ground-source adoption lags due to seawater intrusion raising salinity beyond tolerances, yet hybrid air-source options thrive in luxury hotels eager to display sustainability credentials. NEOM in Tabuk merges coastal breezes with desert expanses, deploying electrified HVAC across residential, industrial, and transportation zones as part of its net-zero blueprint, reinforcing long-term demand in the northwest corridor.

Competitive Landscape

Global incumbents, Daikin, Mitsubishi Electric, Carrier, Trane Technologies, and LG Electronics, share a mid-concentration arena with European specialists and mass-market Asian suppliers. Vision 2030 localization requirements drive greenfield factories: Daikin’s Jeddah hydronic line, LG’s 750,000-unit Riyadh plant with Shaker Group, and Carrier’s VRF venture with Alat collectively tilt share toward firms willing to invest domestically. Bosch’s USD 8 billion purchase of Johnson Controls’ HVAC arm consolidated controls, chillers, and after-sales portfolios under one roof, heightening rivalry for industrial and commercial accounts.

NIBE, Stiebel Eltron, GREE, and Midea target niches such as ground-source and high-temperature platforms but must still widen service networks to match incumbents’ reach. Technology differentiation pivots on refrigerant choices able to sustain capacity at 50 °C plus ambient; Mitsubishi Electric Trane’s R454C-based offerings set new benchmarks for high-ambient rated equipment.

District-cooling heat-recovery retrofits and megawatt-scale process-heat applications remain under-served white spaces that newcomers like HEATEN and Upheat exploit with 150-200 °C capable machines. Compliance with SASO efficiency standards acts as a gating factor; players with in-house testing laboratories expedite certification and capture rebate-qualified orders, further consolidating share.

KSA Heat Pump Industry Leaders

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

Trane Technologies plc

Carrier Global Corporation

Bosch Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mitsubishi Electric Trane HVAC launched the ecodan Pro CAHV line, a 40 kW heat pump using R454C refrigerant rated for 55 °C ambient and 74 °C outlet water.

- November 2025: Carrier and Google Cloud unveiled an AI-powered home-energy platform that pairs heat pumps with battery storage for grid resilience.

- November 2025: Panasonic Marketing Middle East and Africa partnered with Alessa to expand distribution of air-source systems across Saudi Arabia.

- September 2025: Saudi Standards, Metrology and Quality Organization raised minimum seasonal energy efficiency thresholds under

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabian heat pump market as all electrically driven air, water, or ground source systems (including reversible units) that provide space conditioning or sanitary hot water in residential, commercial, industrial, and institutional facilities. Equipment sales, installation revenue, and service agreements booked domestically, whether imported or locally assembled, form the value pool.

Scope Exclusions: portable air conditioning units, solar thermal collectors without vapor compression stages, and industrial waste heat recovery loops are kept outside the boundary.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and structured surveys with local HVAC contractors, project consultants, utility representatives, and equipment distributors helped us verify typical installed costs, replacement cycles, and the share of retrofits in NEOM and Red Sea giga projects. Conversations across Riyadh, Jeddah, Dammam, and Tabuk ensured geographic balance while clarifying incentive uptake under the SEEP program.

Desk Research

We drew on energy balance statistics from Saudi Arabia's Ministry of Energy, customs data from the Saudi Zakat, Tax and Customs Authority, and building permit releases by the Municipal, Rural Affairs and Housing Ministry, which signal annual floor space additions. Further inputs came from regional trade bodies such as the Gulf Cooperation Council Interconnection Authority for grid tariffs, the International Energy Agency for efficiency benchmarks, and patent filings accessed via Questel to track refrigerant and compressor innovations. Company filings, investor decks, and reputable business press complemented these public sources. The examples above illustrate the breadth of reference material; numerous additional documents were reviewed for cross-checks and context.

Market-Sizing & Forecasting

A top down reconstruction based on electricity sales allocated to cooling heating loads was first completed, then validated with sampled average selling price × volume estimates from distributor channel checks. Key variables include average cooling degree days by province, new dwelling completions, hotel room inventory growth, grid tariff escalators, and typical seasonal coefficient of performance improvements. Multivariate regression relating these indicators to historical shipment data underpins the forecast; scenarios were stress tested with primary experts before finalizing a 5.8 % CAGR to 2030. Any gaps in channel data were bridged through capacity roll ups from leading OEMs and normalized against import declarations.

Data Validation & Update Cycle

Model outputs pass variance thresholds versus independent metrics, after which a senior analyst reviews assumptions. Reports refresh annually, with mid cycle updates triggered by policy shifts or demand shocks, and every delivery is preceded by a fresh data sweep so clients receive the latest view.

Why Our KSA Heat Pump Baseline Earns Confidence

Published figures diverge because firms pick different scope filters, assume varied tariff paths, or refresh data on uneven schedules.

Key Gap Drivers include: some studies quote installed base rather than annual revenue, others exclude retrofit sales, and a few apply flat ASP growth that over or understates the impact of inverter adoption and local assembly incentives.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 679.5 M (2025) | Mordor Intelligence | - |

| USD 454.3 M (2024) | Regional Consultancy A | Omits retrofit segment and uses constant exchange rate |

| USD 10.2 M (2023) | Trade Journal B | Focuses solely on industrial heat pumps, excludes residential and service revenue |

Taken together, the comparison shows that Mordor analysts balance realistic scope, timely price updates, and dual validation steps, providing decision makers with a dependable, transparent baseline for strategic planning.

Key Questions Answered in the Report

What is the current and projected value of the KSA heat pump market through 2031?

The sector was worth USD 679.43 million in 2025, is estimated at USD 718.57 million in 2026 and is expected to reach USD 934.21 million by 2031, reflecting a 5.39% CAGR.

Which capacity range is most popular in Saudi Arabia's heat pump landscape?

Systems rated 10-50 kW led 2025 installations with 32.23% share because they suit restaurants, clinics and multi-family buildings.

How do recent electricity tariff reforms influence adoption of heat pumps in Saudi Arabia?

Commercial rates of SAR 0.22-0.32 per kWh cut payback to 3-5 years, prompting many owners to replace aging chillers with high-efficiency heat pumps.

Which application is growing fastest for heat pumps beyond space cooling?

Industrial and process heating is on track for a 5.76% CAGR as petrochemical, food and desalination plants switch to high-temperature electric units.

What hurdles still slow wider use of heat pumps in commercial buildings?

Limited numbers of certified installers and the entrenched preference for VRF systems delay commissioning and deter some project engineers.

How are giga-projects like NEOM shaping future demand for heat pumps?

Net-zero design rules at NEOM, Qiddiya and Red Sea resorts mandate electrified HVAC, creating a multi-year pipeline for high-ambient-rated, locally-built heat pumps.

Page last updated on: