Indonesia Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Heat Pump Market Analysis by Mordor Intelligence

The Indonesia heat pump market size is projected to be USD 1.02 billion in 2025, USD 1.09 billion in 2026, and reach USD 1.46 billion by 2031, growing at a CAGR of 6.02% from 2026 to 2031. An early policy pivot toward renewable electricity, a rising share of inverter-based HVAC imports, and improving grid reliability underpin this steady expansion of the Indonesia heat pump market. Commercial building owners favor equipment that meets the updated Energy Conservation Regulation because non-compliance now carries financial penalties. Meanwhile, Daikin’s USD 206 million factory in West Java is localizing production, trimming delivery lead times, and shortening payback periods for buyers that previously relied on imported air-source units. Grid modernization investments worth USD 500 million, approved in September 2025, will add 300 MW of rooftop solar and upgrade distribution assets for 20 million people in Java, Madura, and Bali, further reducing the operational risk of electrified thermal systems. At the same time, the cold-chain industry’s push to cut logistics expenses from 17% of GDP to single digits favors high-efficiency refrigeration, adding another demand stream for the Indonesia heat pump market.

Key Report Takeaways

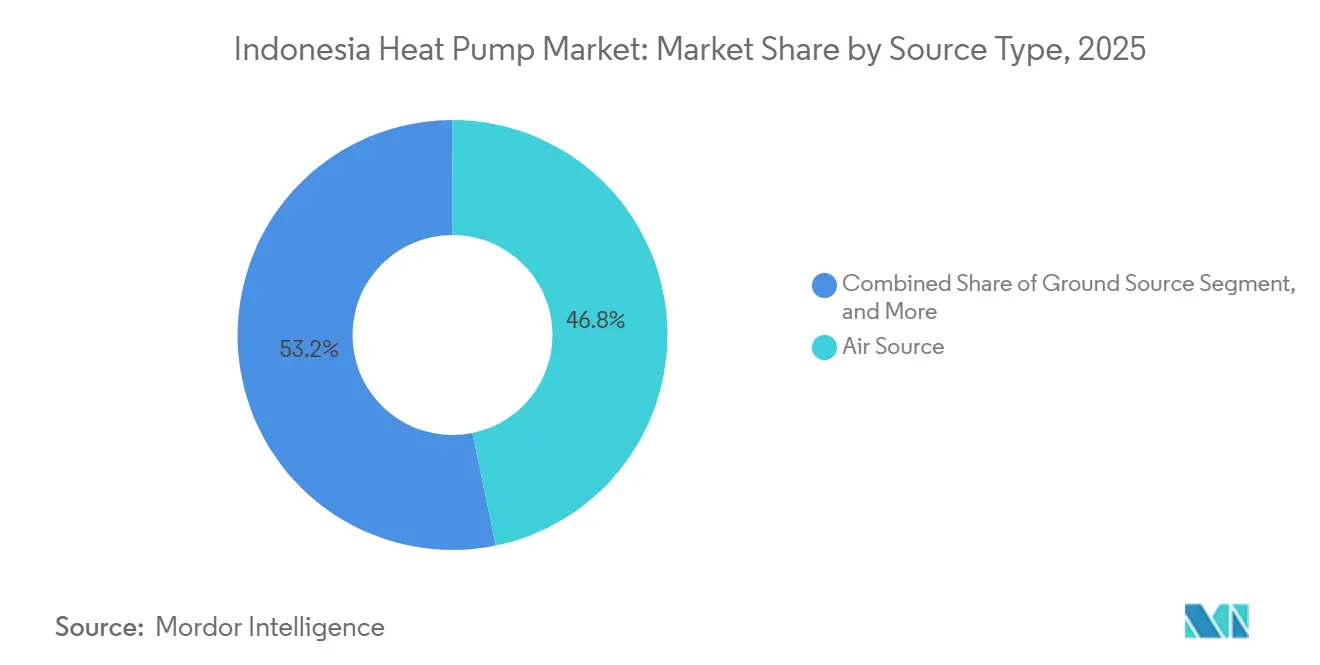

- By type, air source systems led with 46.78% Indonesia heat pump market share in 2025 while ground source units are forecast to advance at a 7.31% CAGR through 2031.

- By technology, air-to-water configurations accounted for 42.59% of the Indonesia heat pump market size in 2025 and ground-to-water is projected to expand at a 7.03% CAGR between 2026-2031.

- By application, domestic and sanitary hot-water captured 41.21% of revenue in 2025 and is set to grow fastest at 16.27% CAGR to 2031.

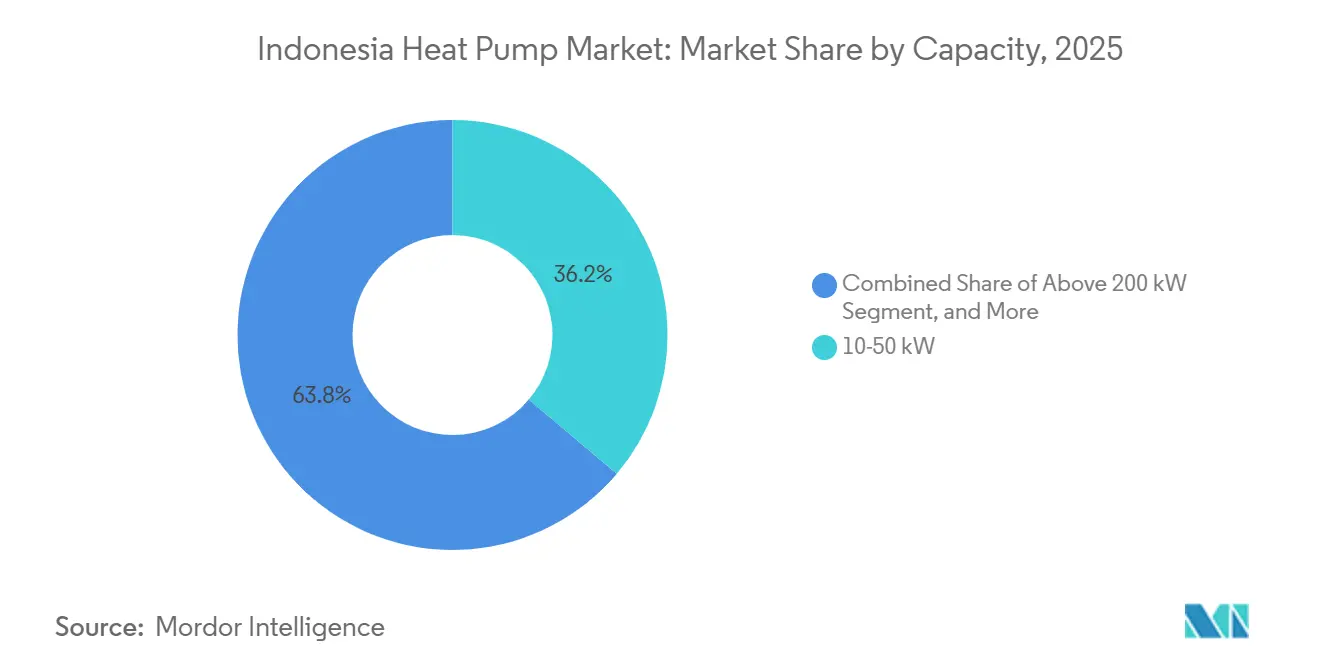

- By capacity, 10-50 kW systems commanded 36.17% Indonesia heat pump market share in 2025 and will post a 6.58% CAGR over the forecast horizon.

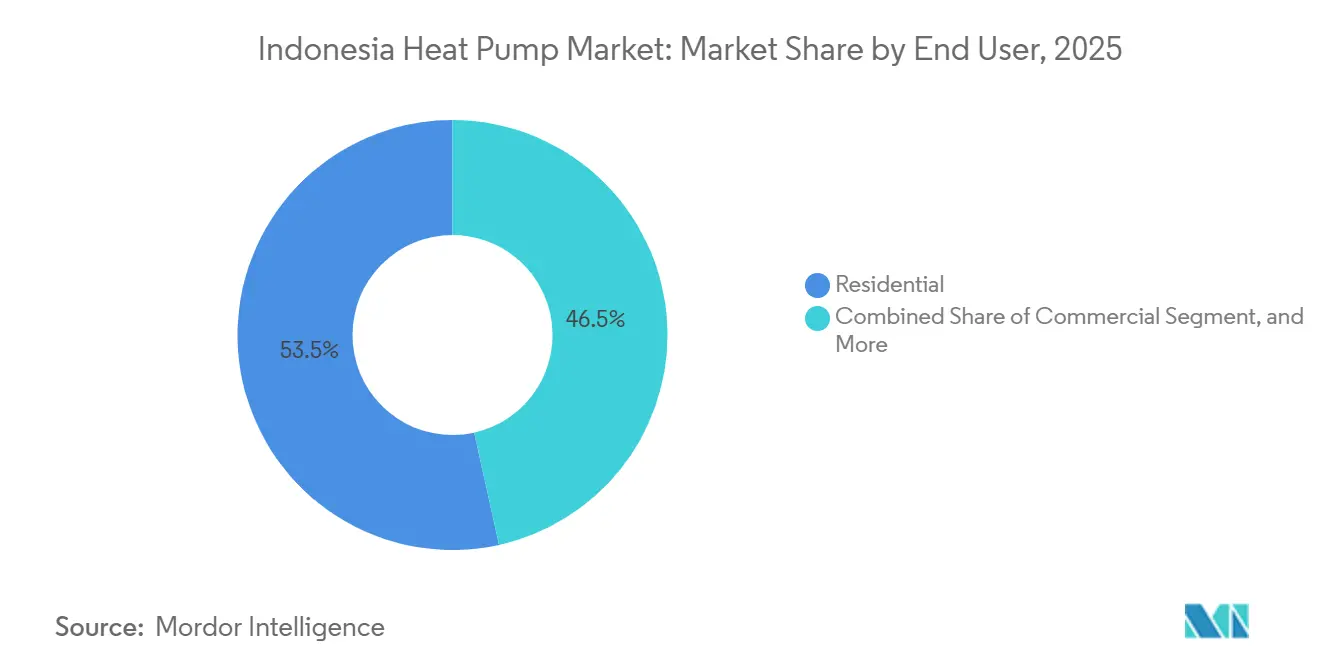

- By end user, the residential segment held 53.47% of 2025 revenue while commercial retrofits are on track for a 6.53% CAGR through 2031.

- By installation, new-build projects generated 61.12% of 2025 sales, yet retrofit demand will outpace at 6.53% per year.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation of Government Incentives for Heat Pump Adoption | +1.2% | National, early gains in Java, Madura, Bali | Medium term (2-4 years) |

| Rapid Urbanization and Rising Construction of Energy Efficient Buildings | +1.5% | Jakarta, Surabaya, Bandung corridors | Long term (≥ 4 years) |

| Declining Upfront Costs and Higher Seasonal Performance of Inverter Based Units | +1.3% | National | Short term (≤ 2 years) |

| Increasing Electricity Access and Grid Reliability | +0.9% | Java, Madura, Bali with spillover to Sumatra and Kalimantan | Medium term (2-4 years) |

| Surge in Distributed Solar Heat Pump Hybrid Installations in Remote Resorts | +0.4% | Nusa Tenggara, Maluku, Papua | Long term (≥ 4 years) |

| Push from Cold Chain Fishery Exports Requiring High Efficiency Process Cooling | +0.6% | Java ports, Sulawesi, Sumatra | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Implementation of Government Incentives for Heat Pump Adoption

Revised Energy Conservation rules lower mandatory energy-management thresholds, bringing a broader mix of factories, malls, and hotels under audit requirements that now emphasize heat-pump retrofits over resistance heaters.[1]International Energy Agency, “Energy Management Implementation Under the Energy Conservation Regulation,” iea.org Blended-finance from the Green Climate Fund adds USD 105 million of concessional capital and USD 142.7 million of co-financing, trimming project risk for banks that previously hesitated to lend against energy-savings cash flows.[2]Green Climate Fund, “Supporting Innovative Mechanisms for Industrial Energy Efficiency Financing in Indonesia,” greenclimate.fund The Indonesia heat pump market gains directly because audits identify hot-water, laundry, and process-heat loads where paybacks now fall under five years. Penalties for non-compliance also drive management teams to invest before enforcement actions escalate. The main drag is the limited pool of accredited energy-service companies, but the framework proves bankable use cases that other lenders will replicate.

Rapid Urbanization and Rising Construction of Energy Efficient Buildings

Buildings already absorb 23% of Indonesia’s final energy use and could touch 40% by 2030 if efficiency lags. The Jakarta Green Growth forum in April 2025 secured 165 voluntary commitments from property owners to cut emissions 10%, signaling stronger market pull for certified HVAC upgrades.[3]Global Green Growth Institute, “Driving Low-Carbon Transition,” gggi.org Minimum Energy Performance Standards for lighting and air conditioning promise savings equal to IDR 1.9 trillion (USD 121 million) per year and prevent 84 million tons of CO₂ by 2030, so capital-markets pressure on developers is intensifying. National programs to build or retrofit one million green homes by 2030 mandate efficient hot-water solutions, inserting the Indonesia heat pump market into housing policy. Enforcement gaps persist, only 1.45% of buildings met energy-management standards in 2025, but the medium-term signal is clear and supports long-run demand growth.

Declining Upfront Costs and Higher Seasonal Performance of Inverter Based Units

Automation at Daikin’s new Cikarang plant, combined with removal of one-star air conditioners in October 2024, drives volume-based cost declines that narrow the price premium between inverter heat pumps and fixed-speed split ACs. Field trials showed ground-source systems cut electricity use 21-45% and raised coefficients of performance to around four, reinforcing lifecycle-cost arguments.[4]Indonesia Association of Geologists, “Indonesian First Geo-Heat Pump System Application for Space Cooling,” iagi.or.id Refrigerant shifts to R290 and R32 also future-proof new units against environmental regulation. With better factory-gate pricing and bigger energy savings, bankers now see shorter paybacks, unlocking term loans that were unavailable two years earlier. The lingering obstacle remains a tenfold price gap for heat-pump water heaters versus electric tanks, yet this spread is tightening as domestic assembly scales.

Increasing Electricity Access and Grid Reliability

A USD 500 million grid-modernization loan links 20 million new or improved customers and integrates 300 MW of rooftop solar generation, bolstering voltage stability for compressor-heavy loads that once stalled during brownouts. Proposed grid-code revisions, low-voltage ride-through, harmonic limits, and reactive-power compensation, will allow heat pumps to participate in demand-response markets. The government’s 100 GW solar roadmap, of which 26 GW is decentralized PV plus storage, lowers marginal electricity emissions and improves the carbon narrative for electrified heating.[5]Institute for Essential Services Reform, “Indonesia Energy Transition Outlook 2025,” iesr.or.id Collectively, these measures reduce curtailment risk, enable tariff reform, and pave the way for dynamic pricing that rewards efficient thermal equipment, adding momentum to the Indonesia heat pump market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Installation Cost and Limited Financing Options | -1.1% | National | Short term (≤ 2 years) |

| Shortage of Skilled Heat Pump Technicians | -0.7% | National, acute in outer islands | Medium term (2-4 years) |

| Fragmented After Sales Service Network in Outer Islands | -0.4% | Maluku, Papua, Nusa Tenggara, Kalimantan | Long term (≥ 4 years) |

| Customer Preference for Cheap Split AC and Water Heater Combos | -0.9% | National, strongest in residential segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Installation Cost and Limited Financing Options

Heat-pump water heaters still cost roughly ten times electric tanks, and most commercial loans top out at seven-year tenors with 7-12% interest rates, suppressing uptake among cash-constrained buyers. Only about 25 active energy-service companies existed nationwide in 2024, limiting project aggregation and performance-contracting solutions that could offset high capex. Banks rarely accept energy-savings cash flows as collateral, so the Indonesia heat pump market relies on donor-supported programs like Energy Savings Insurance and UOB’s U-Energy platform that guarantee performance and front capital. These schemes are promising but remain small relative to nationwide demand, so cost barriers will persist in the near term.

Shortage of Skilled Heat Pump Technicians

Indonesia’s 100 GW solar plan outlines 5,000 fast-track technical certifications, yet heat-pump curricula are still absent, leaving installers to learn informally. Cold-chain research highlights weak understanding of temperature management, while HVAC manufacturers confirm that outer-island service calls often require flying technicians from Java, a costly delay. Daikin’s Cikarang plant will train 2,500 workers, but factory skills do not directly translate to field installation. Without a national database of certified professionals or standardized continuing-education credits, quality assurance remains uneven, capping the growth trajectory of the Indonesia heat pump market outside core urban centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Ground Source Gains Momentum Despite Air Source Dominance

Air-source heat pumps delivered 46.78% of market value in 2025, demonstrating the Indonesia heat pump market share lead of a technology that balances moderate tropical temperature swings with relatively simple installation. Institutional pilots at Universitas Gadjah Mada and PT Geoenergis point to a 7.31% annual growth runway for ground-source units that tap Indonesia’s estimated 23,766 MW shallow geothermal resource.[6]Fakultas Teknik Universitas Gadjah Mada, “Riset Geothermal dan Ground Source Heat Pump,” ft.ugm.ac.id Two horizontal-loop demonstrations recorded coefficients of performance near four, saving 21-45% electricity over split ACs.

Air-source equipment keeps its large installed base because distributors stock spare parts nationwide and permits are minimal. Yet government energy-audit mandates favor lifecycle cost metrics, tilting future public procurements toward ground loops in hospitals and universities. Water-source and hybrid solutions stay niche, limited by available ponds or high control complexity. With regulators considering carbon pricing, deep reductions may outweigh first-cost hurdles, making ground-source momentum structurally durable inside the Indonesia heat pump market.

By Technology: Air-to-Water Leads As Ground-to-Water Accelerates

Air-to-water configurations earned 42.59% of 2025 revenue, illustrating how hotel, hospital, and apartment operators value a package that dovetails with existing hydronic lines. Variable refrigerant flow upgrades in hotels raised cooling energy efficiency ratios to 5.40, further validating inverter compressor advantages. Ground-to-water systems mirror overall ground-source tailwinds, clocking a 7.03% forecast CAGR that is poised to outstrip other formats.

Air-to-air heat pumps contend with the deeply entrenched split-AC culture for cooling, which still dominates consumer mindshare despite higher operating costs. Water-to-water and hybrid solar-thermal or biomass couplings remain confined to industrial estates with specialized engineering staff. As building codes tighten, architects specify hydronic loops that future-proof properties, sustaining air-to-water leadership inside the broader Indonesia heat pump market size narrative.

By Capacity: Mid Range Dominates Across Applications

Systems rated 10-50 kW secured 36.17% of 2025 sales and will progress at 6.58% a year, supplying neighborhood clinics, schools, and mid-rise apartments. Larger 50-200 kW units move into shopping malls and light-manufacturing workshops, piggybacking on Green Climate Fund guarantees that reduce perceived investment risk.

Below 10 kW units could gain traction if the Green Affordable Housing Program mandates heat-pump water heaters, yet price differentials still steer most households toward electric tanks. Above 200 kW systems fill district-cooling and warehouse niche roles, but require advanced control layers to interact with smart-grid signals. Capacity choice increasingly incorporates demand-response readiness, a factor regulators reward as solar penetration rises, reinforcing mid-band dominance within the Indonesia heat pump market.

By Application: Domestic Hot Water Outpaces Space Conditioning

Domestic and sanitary hot-water held 41.21% revenue in 2025 and is on a 16.27% CAGR path, reflecting low-grade tropical heating needs that align with high heat-pump coefficients of performance. Space-cooling uptake lags because millions of consumers default to cheaper split ACs, while industrial process heat projects require complex integration and longer paybacks.

Ministry rules phasing out one-star ACs open a back door for reversible heat-pump models that supply both cooling and water-heating from the same compressor, an efficiency gain that resonates with hotel operators seeking Green Building credits. Over time, process-heat retrofit pilots in palm-oil mills and food plants will clarify economics, supporting gradual diversification of the Indonesia heat pump market.

By End User: Residential Leads, Commercial And Industrial Follow

Residential buyers contributed 53.47% of 2025 turnover, propelled by urban middle-class demand for stable hot-water supply. Yet buyer sensitivity to first price keeps split AC plus electric heater combos popular, muting growth relative to commercial retrofits, which clock a 6.53% CAGR as hotels and offices chase certification points.

Industrial facilities fall under mandatory energy audits that single out boiler and chiller upgrades. Cold-chain logistics, now 17% of GDP costs, highlight efficiency gaps that heat pumps can fill. The challenge is limited technician coverage in Sulawesi, Maluku, and Papua, where response times extend into weeks, constraining the Indonesia heat pump market outside Java.

By Installation: Retrofit Gains As New-Build Slows

New-build projects generated 61.12% of 2025 income because it is cheaper to specify heat-pump hydronic loops during initial design. Nevertheless, retrofits grow faster at 6.53% per year, driven by hotel modernization and mandatory audits in factories subject to the Energy Conservation Regulation.

Financiers like UOB structure energy-as-a-service contracts that shift capital risk off balance sheets, a model particularly attractive to shopping-mall landlords and aging high-rise managers. Scaling this approach to outer-island provinces remains difficult, yet policy carrots plus donor guarantees increasingly bridge the gap, locking in a steady retrofit contribution to the Indonesia heat pump market size outlook.

Geography Analysis

Java, Madura, and Bali dominate current installations because 20 million residents are slated for upgraded distribution lines and 300 MW of rooftop solar that directly improve supply quality for compressors. West Java’s Cikarang industrial corridor, home to Daikin’s 1.5 million-unit plant, hosts concentrated supply chains and certified installers, giving the region first-mover advantage.

Sumatra and Kalimantan follow as grid-expansion finance under the Sustainable Least-Cost Electrification-2 program connects 3.5 million people and deploys 540 MW of wind and solar, lowering tariffs and improving payback for electrified heating. Sulawesi’s fishery ports need efficient process-cooling to support export targets, pushing regional wholesalers to test heat-pump refrigeration.

Nusa Tenggara, Maluku, and Papua register the fastest relative growth off a small base, thanks to diesel-displacement solar-hybrid resorts that now meet up to 85% of demand with on-site PV and batteries, freeing capacity for heat-pump water heaters. However, spare-parts logistics and technician shortages constrain service-level agreements, slowing adoption until regional service hubs mature. Outer-island uptake therefore hinges on government-led OandM trust funds and bundled procurement that guarantee lifecycle support, a mechanism now under discussion for the 100 GW solar plan.

Competitive Landscape

The Indonesia heat pump market is moderately fragmented. Global incumbents, Daikin, Mitsubishi Electric, Panasonic, Carrier, Trane, and Johnson Controls-Hitachi, jockey with regional assemblers for distributor shelf space. Daikin’s USD 206 million Cikarang plant targets 40% local component content by 2025 and signals a pivot from import reliance to domestic sourcing, cutting delivery lead times and qualifying products for public-sector tenders that mandate local value addition.

Johnson Controls-Hitachi’s air365 Max variable refrigerant flow line markets a 47% energy-cut claim plus remote diagnostics via airCloud Pro, positioning service contracts as margin drivers in the Indonesia heat pump market. Emerging disruptors are energy-service companies and lender-integrator consortia under the U-Energy platform, which bundle financing, equipment, and performance guarantees. Technology differentiation shifts toward R290 or R32 refrigerants, inverter compressors, and controllers that talk Modbus, BACnet, or KNX, a must-have once demand-response tariffs roll out.

Ground-source engineering remains a white space where specialized drillers and geothermal start-ups can gain share before bigger OEMs scale their installer networks. Compliance audits that enter into force in July 2025 under Ministry regulation will also squeeze gray-market imports lacking certification, indirectly raising the quality bar across the Indonesia heat pump market.

Indonesia Heat Pump Industry Leaders

Daikin Industries Ltd.

Mitsubishi Electric Corp.

Panasonic Heating & Cooling Solutions

Fujitsu General Ltd.

Johnson Controls-Hitachi Air Conditioning

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Daikin Industries Indonesia opened a USD 206 million factory in Cikarang, West Java with 1.5 million-unit capacity and 2,500 new jobs.

- February 2026: Johnson Controls-Hitachi launched a hotel-focused campaign for air365 Max variable refrigerant flow systems quoting 47% energy savings.

- February 2026: Institute for Essential Services Reform released the 100 GW solar implementation framework projecting USD 70 billion investment and 118,000 green jobs.

- December 2025: Universitas Gadjah Mada partnered with PT Geoenergis and Project Innerspace on a shallow-geothermal heat-pump feasibility study.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Indonesia heat pump market as all electrically driven air-source, water-source, and ground-source units up to 30 kW that are factory-built and sold for space conditioning or sanitary hot-water duties in residential, commercial, institutional, and light-industrial buildings across the archipelago.

Scope exclusion: Single-function electric resistance heaters and heat-pump components embedded in household appliances (e.g., tumble dryers) lie outside this scope.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

To ground assumptions, Mordor interviewed HVAC contractors, national distributors, and facility managers in Java, Sumatra, Kalimantan, and Sulawesi. Conversations focused on annual unit off-take, installation mix, prevailing margins, and regulatory bottlenecks. Short online surveys with residential installers validated adoption rates and price dispersion uncovered in desk work.

Desk Research

Mordor analysts began with statutory data from the Ministry of Energy & Mineral Resources, Statistics Indonesia building-permit files, and ASEAN Centre for Energy policy trackers, which map the addressable building stock and efficiency mandates. Monthly import flows under HS 841861/841869 from Indonesia Customs, patent analytics retrieved through Questel, and price trends gathered via Dow Jones Factiva newsfeeds supplied the quantitative spine. Company 10-Ks, distributor presentations, and trade-association notes such as GAPENSI then helped us benchmark selling channels and average system capacities. The sources illustrated here are indicative; many additional publications were reviewed for cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down construct starts with domestic production plus net imports, which are then adjusted for average capacity and channel mark-ups to derive 2024 value. Results are pressure-tested with selective bottom-up roll-ups of supplier shipments and sampled ASP × volume estimates. Key model drivers include new dwelling completions, commercial floor-space starts, electricity-tariff trajectories, building-code efficiency milestones, and subsidy envelopes announced in the National Energy Policy. Forecasts (2025-2030) stem from multivariate regression blended with ARIMA seasonality to capture monsoon-linked cooling demand, and scenario analysis mirrors policy or tariff swings flagged by our primary respondents. Data gaps on informal refurbishments are bridged by applying calibrated penetration ratios derived from installer interviews.

Data Validation & Update Cycle

Each iteration passes three tiers of review: automated variance scans, peer analyst checks, and senior sign-off. We reconcile model outputs with import paperwork, grid-connection statistics, and manufacturer guidance; anomalies trigger re-calls to field experts. The report refreshes annually, with mid-cycle tweaks if policy shocks or major plant launches occur.

Why Mordor's Indonesia Heat Pump Baseline Commands Confidence

Published market values vary because studies diverge on product mix, price ladders, and refresh cadence. We anchor our baseline to verifiable trade data, broaden it with domestic assembly counts, and apply moderate uptake curves that mirror real-world installation capacity.

Key gaps arise when some publishers exclude locally assembled split systems, assume uniform ASP compression across sizes, or stretch compound growth from limited installer polls. Mordor's balanced view, updated every year and re-ratified with on-ground voices, avoids both under-scoping and headline-grabbing growth leaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.34 B (2025) | Mordor Intelligence | |

| USD 0.63 B (2024) | Regional Consultancy A | Counts import value only; omits domestic assembly and aftermarket replacements |

| USD 1.30 B (2024) | Trade Journal B | Focuses on residential installs, ignores commercial retrofits and uses installer price lists without tariff normalization |

In short, Mordor's disciplined scope selection, dual-source modelling, and yearly refresh give decision-makers a dependable, transparent baseline they can reproduce with publicly verifiable signals.

Key Questions Answered in the Report

What is the projected heat-pump market size for Indonesia in 2026?

The Indonesia heat pump market size is estimated at USD 1.09 billion in 2026.

Which technology currently generates the most revenue?

Air-to-water systems contributed 42.59% of 2025 revenue and remain the largest revenue generator through 2026.

Which application segment is expanding the quickest?

Domestic and sanitary hot-water is forecast to grow at a 16.27% CAGR between 2026-2031, making it the fastest-rising use case.

How are government policies supporting adoption?

Revised Energy Conservation rules impose audits and penalties, while blended-finance from the Green Climate Fund lowers project risk, together boosting installations.

Why do upfront costs still act as a barrier?

Heat-pump water heaters cost roughly ten times electric tanks and local financing often carries high interest and short tenors, slowing payback for households and SMEs.

Which manufacturers are investing locally?

Daikin, Mitsubishi Electric, Panasonic, Carrier, Trane, and Johnson Controls-Hitachi have all localized assembly or launched Indonesia-specific product lines, led by Daikins USD 206 million Cikarang plant.

Page last updated on: