Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.97 Billion |

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Industrial Pump Market Analysis by Mordor Intelligence

The India industrial pump market size was valued at USD 0.97 billion in 2025 and estimated to grow from USD 1.02 billion in 2026 to reach USD 1.28 billion by 2031, at a CAGR of 4.74% during the forecast period (2026-2031).[1]Ministry of Finance, “Union Budget 2024-25,” INDIABUDGET.GOV.IN The solid growth stems from sustained government capex under the National Infrastructure Pipeline, widening wastewater treatment coverage, and the steady shift toward smart, energy-efficient pumping systems. Centrifugal designs still dominate high-volume applications, yet positive-displacement variants are advancing quickly as specialty chemicals, mining, and refinery upgrades call for precise, high-pressure flow. Solar-powered installations are also scaling, aided by falling photovoltaic costs and industrial decarbonization targets under PM-KUSUM, while volatile steel prices and low-cost Chinese imports continue to weigh on profit margins. Competition hinges on service depth, API 610 compliance, and Industrial IoT integration, all of which favour incumbents with R&D and nationwide after-sales networks.

Key Report Takeaways

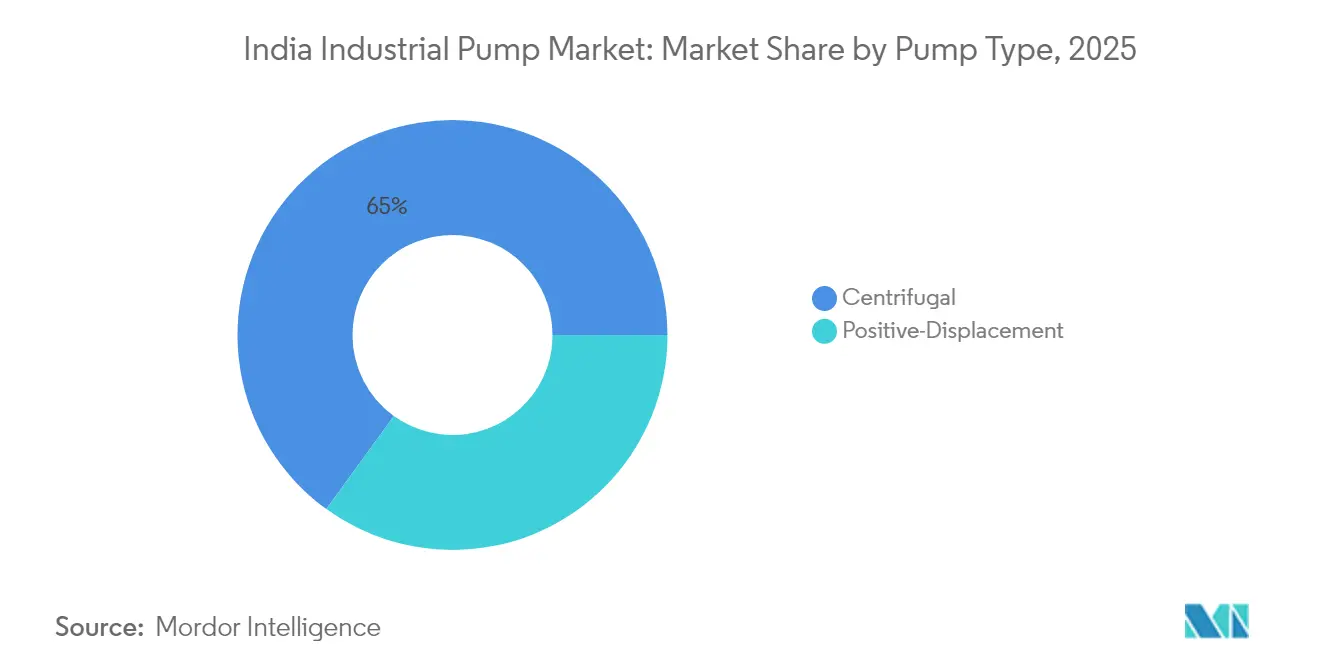

- By pump type, centrifugal models held 65.02% of the India industrial pump market share in 2025, whereas positive-displacement pumps are projected to post a 6.79% CAGR through 2031.

- By end-user, water and wastewater treatment captured 28.86% of the India industrial pump market size in 2025, while mining is expected to expand at a 7.18% CAGR to 2031.

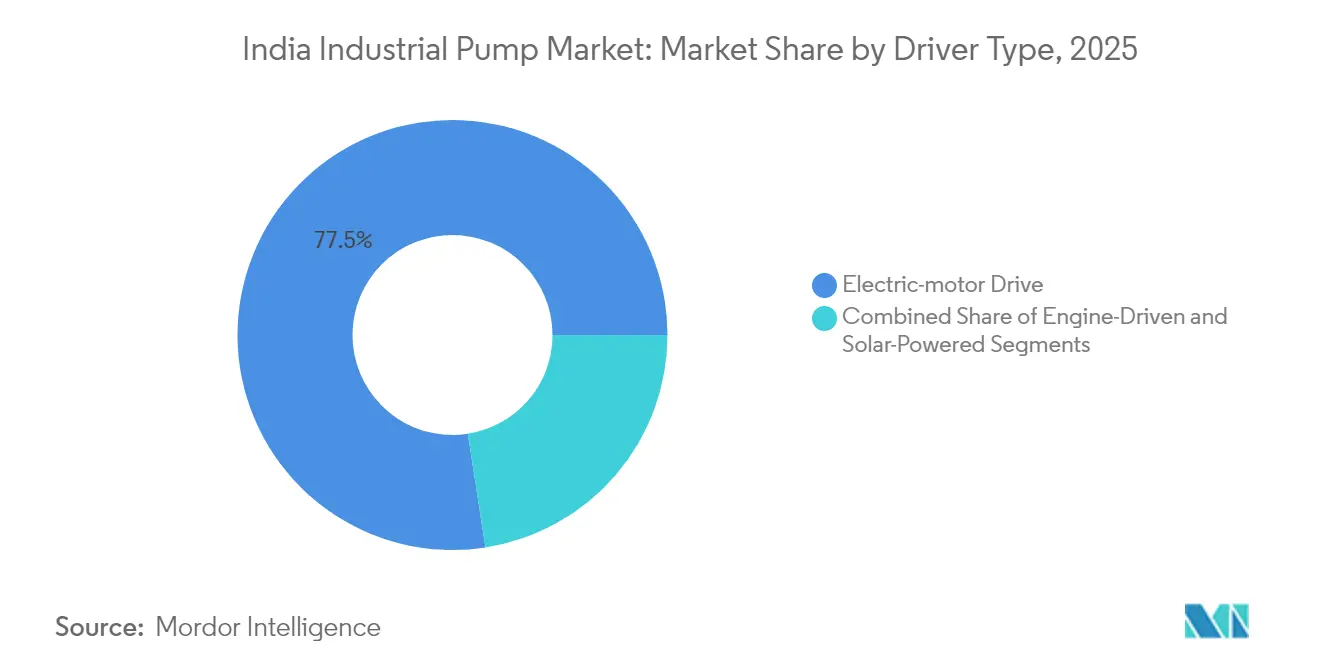

- By driver type, electric-motor units commanded 77.45% of the 2025 value, yet solar-powered systems are on track for an 10.75% CAGR through 2031.

- By installation, surface pumps accounted for 57.52% of 2025 demand; submersible variants are forecast to grow at a 7.28% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Industrial Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government cap-ex under National Infrastructure Pipeline (NIP) | +1.20% | National, with concentration in Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Rapid expansion of wastewater treatment capacity | +0.90% | National, with early gains in Mumbai, Delhi, Bangalore | Short term (≤ 2 years) |

| Brown-field expansion in Indian refineries | +0.70% | Gujarat, Maharashtra, Odisha, Assam | Medium term (2-4 years) |

| Increasing solar-powered pump installations in industries | +0.80% | Rajasthan, Gujarat, Karnataka, Uttar Pradesh | Long term (≥ 4 years) |

| Shift toward API 610/ISO 13709-compliant pumps | +0.50% | National, with focus on petrochemical clusters | Medium term (2-4 years) |

| Industrial IoT-enabled predictive-maintenance adoption | +0.60% | National, with early adoption in automotive, chemicals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Capex Under the National Infrastructure Pipeline Accelerates Industrial Pump Demand

The INR 111 lakh crore National Infrastructure Pipeline (NIP) earmarked through 2025 has permanently changed pump procurement behaviour by embedding digital-performance requirements in every new utility, refinery upgrade, and industrial park. Public-private partnerships now expect suppliers to guarantee uptime metrics, pushing vendors to bundle Industrial IoT sensors, API 610 compliance, and long-term service contracts. Paradip refinery’s INR 24,000 crore brown-field project illustrates the new norm, specifying remote diagnostics and predictive-maintenance dashboards with every pump skid. The model favours enterprises that maintain nationwide service crews and cloud-ready control platforms while elevating entry barriers for low-spec imports lacking data gateways or standardized protocols. As NIP disbursements progress, centrifugal pump retrofits give way to condition-based replacements, sustaining aftermarket revenue even after capital outlays taper.

Rapid Expansion of Wastewater Treatment Capacity Drives Specialized Pump Requirements

Wastewater coverage is slated to reach 70% by 2030 from 37% in 2024, triggering record procurement of corrosion-resistant, solids-handling pumps rated above 75% efficiency. Mumbai Metropolitan Region alone has budgeted INR 25,000 crore for decentralized sewage lifting and sludge dewatering, demanding more than 2,000 precision pumps able to operate unattended in corrosive environments. Operators now stipulate variable-frequency drives to match fluctuating influent loads, creating premium niches for manufacturers with metallurgy know-how and VFD bundles. Tightened Central Pollution Control Board norms further elevate demand for real-time monitoring and redundancy, placing centrifugal offerings with leak-free magnetic drives at a competitive edge.

Brown-field Expansion in Indian Refineries Creates High-Value Pump Opportunities

Over INR 1.2 lakh crore in refinery upgrades through 2030 aims to process heavier crudes and integrate petrochemical chains, raising call-offs for API 610-compliant, high-temperature pumps. Kochi’s 400-pump revamp underscores a shift toward modular packages that fit narrow maintenance windows and tackle variable viscosities. Vendors with rapid-deployment skids, exotic metallurgy, and redundant seal designs win bids as reliability overrides upfront cost. Advanced control logic that optimizes energy draw under fluctuating feedstock qualities is becoming standard, strengthening the position of suppliers offering turnkey automation.

Increasing Solar-Powered Pump Installations Transform Industrial Energy Economics

Industrial solar pump orders crossed the 12,500-unit mark in 2024 after Shakti Pumps won Uttar Pradesh’s INR 450 crore bid. Component-C of PM-KUSUM injects INR 17,500 crore to subsidize rooftop and ground-mount arrays, driving adoption in textile, food, and metals processing plants seeking sub-4-year paybacks. Differing from agricultural kits, industrial solutions require higher head, grid-sync inverters, and battery buffers for peak-shaving. Consequently, pump makers with in-house PV engineering and single-vendor warranties corner the fast-growing segment and lock in aftermarket parts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import surge of low-cost Chinese pumps | -0.80% | National, with higher impact in price-sensitive segments | Short term (≤ 2 years) |

| High total cost of ownership (energy + maintenance) | -0.60% | National, with focus on energy-intensive industries | Medium term (2-4 years) |

| Volatility in steel and copper prices | -0.40% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Lengthy approval cycles in public sector projects | -0.50% | National, with higher impact in infrastructure projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Surge of Low-Cost Chinese Pumps Pressures Domestic Market Dynamics

Chinese models undercut domestic equivalents by 30-40%, capturing commodity water and HVAC orders and compressing gross margins. Shorter lead times and flexible credit terms lure SMEs, compelling Indian producers to automate fabrication and trim overhead. However, inconsistent after-sales service and spares unavailability offer incumbents a service-oriented counterpunch, especially as the Bureau of Indian Standards tightens ISI enforcement.

High Total Cost of Ownership Constrains Market Expansion in Energy-Intensive Applications

Industrial tariffs averaged INR 6.5 per kWh in 2024, pushing lifecycle economics to the fore. Pumps in textiles and chemicals can soak up 15-20% of production expenses, making energy labels and VFD readiness critical. Smaller factories balk at the premium for high-efficiency models even though predictive maintenance tools promise downtime reductions. The resulting volume shift toward mid-efficiency lines dampens revenue growth until tariff reforms or incentive schemes soften paybacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Dominance Faces Positive-Displacement Challenge

Centrifugal models commanded 65.02% of 2025 revenue of the India industrial pump market size, because they efficiently move large flows at moderate heads in water, cooling, and general process loops. Positive-displacement pumps, though only 34.98% of shipments, are set for a 6.79% CAGR by 2031, outstripping centrifugal’s 3.95% pace as specialty chemical and pharma customers demand precise metering under variable viscosities. Vendors are closing the gap by adding magnetic drives and ceramic bearings to centrifugal lines, while PD makers push higher-speed, compact skids for brown-field retrofits. IoT retrofits blur lines further, letting operators benchmark efficiency in real time and switch technologies based on duty cycle analytics. Over the forecast, centrifugal unit volumes will still dwarf PD counts, yet PD value share will rise on premium pricing for exotic alloys and seamless architectures that curb fugitive emissions.

By End-User Industry: Mining Surge Reshapes Demand Patterns

Water and wastewater accounted for 28.86% of the India industrial pump market share in 2025 on the back of Jal Jeevan and urban STP investments valued above INR 3.6 lakh crore. Mining, though only 8.40% of current sales, leads with a 7.18% CAGR as Coal India and steel majors increase mechanized output. Dewatering, slurry, and tailings lines call for abrasion-resistant elastomers and duplex stainless steels, lifting ASPs. Oil and gas remain a steady buyer through refinery upgrades, while chemicals leverage import-substitution policies to spur PD pump adoption. Regional clusters such as Chhattisgarh iron-ore belts or Odisha chromite pits will show double-digit spends, whereas mature thermal power plants mostly allocate capex for replacements rather than expansions.

By Driver Type: Solar Revolution Transforms Energy Landscape

Electric-motor systems formed 77.45% of 2025 shipments, aided by grid reliability in western and southern industrial corridors. Nevertheless, solar pump arrays are racing ahead, set to cross 9% share by 2031 as the India industrial pump industry pivots to onsite renewables. Falling module prices, MNRE subsidies, and stringent ESG audits spur breweries, dairies, and auto OEMs to install hybrid solar-battery packages. Engine-driven units, historically popular for remote mines and standby firefighting, will slip below a 10% share as diesel prices exceed INR 100 per liter and emission norms tighten. Hybrid diesel-solar solutions may emerge in off-grid mines, yet pure solar is expected to outstrip them once battery costs sink another 20%.

By Installation: Submersible Growth Reflects Space Constraints

Surface pumps held 57.52% of billings in 2025, yet city-fringe real-estate premiums and deeper borewells are lifting submersible sales at a 7.28% CAGR. Metro-area factories prefer submersibles for noise abatement and smaller footprints, while mining dewatering benefits from motors located underwater for better cooling. Advanced seal rings and high-chrome casings resolve past reliability doubts, and IoT sensors now relay motor temp and vibration even when submerged. Surface designs maintain relevance where easy maintenance trumps space, particularly in mega-capacity desal plants. The choice increasingly hinges on total installed cost: submersibles tally higher hardware but lower civil works, whereas surface units flip the equation.

Geography Analysis

Gujarat and Maharashtra absorbed 34.62% of 2025 shipments owing to petrochemical giant complexes at Jamnagar and the Pune-Mumbai auto belt. The India industrial pump market in southern states is the fastest growing at 6.05% CAGR to 2031 as Tamil Nadu electronics clusters and Karnataka’s clean-energy hubs demand precision pumps and utility upgrades. Northern states led by Uttar Pradesh and Haryana draw capex from the Delhi-Mumbai Industrial Corridor, funnelling pump orders for effluent treatment and cooling water loops. Eastern territories such as Odisha log healthy mining-related demand but lag in basic infrastructure, capping growth. Electricity tariffs and state pollution norms shape purchasing, strict discharge limits in Maharashtra tilt demand toward corrosion-resistant PD pumps, while relaxed standards in some eastern pockets keep commodity centrifugal units viable. Emerging industrial parks in Rajasthan and Madhya Pradesh offer long-run upside as they court manufacturing diversification away from coastal congestion.

Competitive Landscape

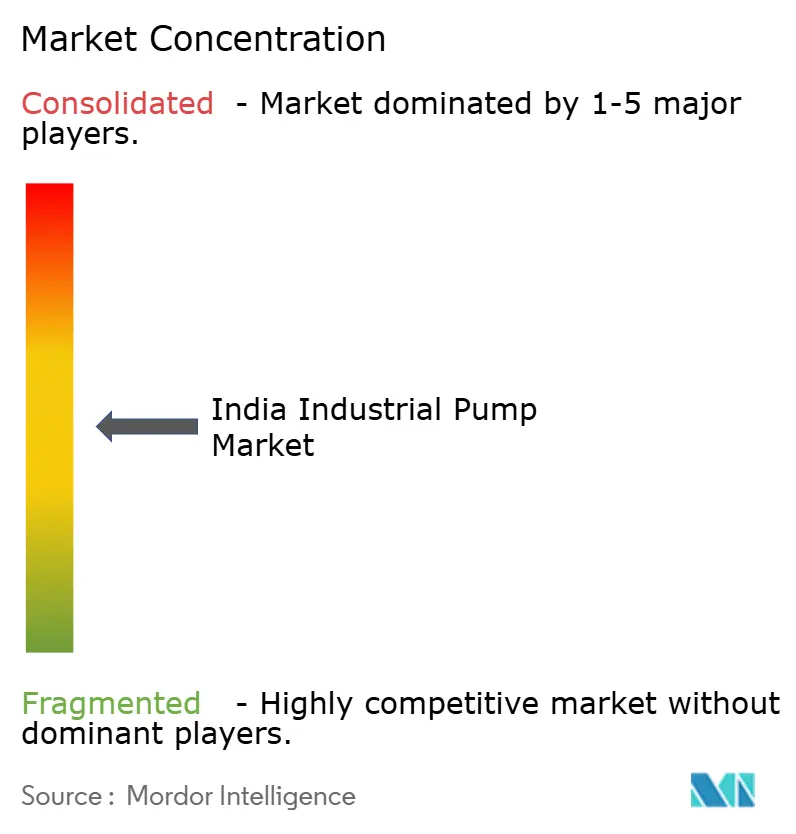

The India industrial pump market displays moderate fragmentation: the top five suppliers control roughly 45%, assigning a 6/10 concentration score. Domestic stalwarts Kirloskar Brothers, CRI, and Shakti Pumps collectively hold close to 25%, leveraging price agility and dense service depots. Multinationals KSB, Grundfos, and Xylem command another 20% by offering API 610-ready skids and advanced analytics platforms. Chinese imports seize share in standard water applications but struggle in lifecycle tenders that mandate service guarantees. Strategic differentiators now include remote diagnostics, energy-efficiency certifications, and turnkey solar integration. Kirloskar’s FY25 profit jump of 89.88% reflects its pivot to high-margin refinery retrofits, while Grundfos and Xylem intensify IoT rollouts targeting OPEX savings. Solar-centric Shakti Pumps is capitalizing on PM-KUSUM orders, whereas V-Guard’s 2025 entry signals impending price battles in mid-duty segments. The race to localize exotic alloys and integrate additive-manufactured impellers may redraw market lines by 2030.[4]ABB, “Water company in Brazil gets 25% energy savings and better uptime,” NEW.ABB.COM

India Industrial Pump Industry Leaders

Usha International Limited

Crompton Greaves Consumer Electricals Limited

CRI Pumps Pvt. Ltd.

Grundfos AS

Kirloskar Brothers Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kirloskar Brothers posted 89.88% profit growth in Q2 FY25 on strong NIP-linked orders

- February 2025: Shakti Pumps won an INR 450 crore contract for 12,537 industrial solar pump sets in Uttar Pradesh

- January 2025: V-Guard Industries announced diversification into industrial pumps, leveraging its consumer brand equity

- December 2024: CRI Pumps expanded its Coimbatore plant by 30% to boost API 610 capacity

India Industrial Pump Market Report Scope

Industrial pumps are mechanical devices designed to move fluids (liquids or gases) from one place to another within industrial settings. They are crucial in various industries, including manufacturing, oil and gas, chemical processing, power generation, water treatment, agriculture, and construction. Industrial pumps are designed to handle different fluids, including water, chemicals, petroleum products, slurry, wastewater, and more. Industrial pumps are characterized by their ability to generate high pressure or flow rates to meet specific application requirements. They come in various types, each suitable for specific applications.

The Indian industrial pump market is segmented by type and end-user Industry. By type, the market is segmented into Centrifugal Pump and Positive Displacement Pump. By end-user Industry, the market is segmented into Oil and Gas, Water and Wastewater, Chemicals and Petrochemicals, Mining, Power Generation, and Other End-user Industries. For each segment, the market sizing and forecasts have been done based on revenue capacity in USD.

By Pump Type

| Centrifugal |

| Positive-Displacement |

By End-user Industry

| Oil and Gas |

| Water and Wastewater |

| Chemicals and Petrochemicals |

| Power Generation |

| Mining |

| Other End-User Industry |

By Driver Type

| Electric-motor Driven |

| Engine-Driven (Diesel/CNG) |

| Solar-Powered |

By Installation

| Surface Pumps |

| Submersible Pumps |

| By Pump Type | Centrifugal |

| Positive-Displacement | |

| By End-user Industry | Oil and Gas |

| Water and Wastewater | |

| Chemicals and Petrochemicals | |

| Power Generation | |

| Mining | |

| Other End-User Industry | |

| By Driver Type | Electric-motor Driven |

| Engine-Driven (Diesel/CNG) | |

| Solar-Powered | |

| By Installation | Surface Pumps |

| Submersible Pumps |

Key Questions Answered in the Report

What is the forecast value of the India industrial pump market in 2031?

The market is projected to reach USD 1.28 billion by 2031 based on a 4.74% CAGR.

Which pump type currently holds the largest share?

Centrifugal pumps account for 65.02% of 2025 revenue due to versatility in water and process duties.

Which end-user segment will grow the fastest through 2031?

Mining is expected to register a 7.18% CAGR as coal and iron-ore projects expand mechanization.

How fast are solar-powered pumps growing?

Solar-powered installations are projected to advance at an 10.75% CAGR through 2031 as firms pursue renewable energy savings.

Which regions are driving the highest demand?

Gujarat and Maharashtra lead with 34.62% combined share, while Tamil Nadu and Karnataka are the fastest expanding at a 6.05% CAGR.

What factors most influence purchasing decisions?

Lifecycle energy costs, API 610 compliance, and Industrial IoT readiness are the top criteria for industrial buyers.

Page last updated on: