Philippines Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

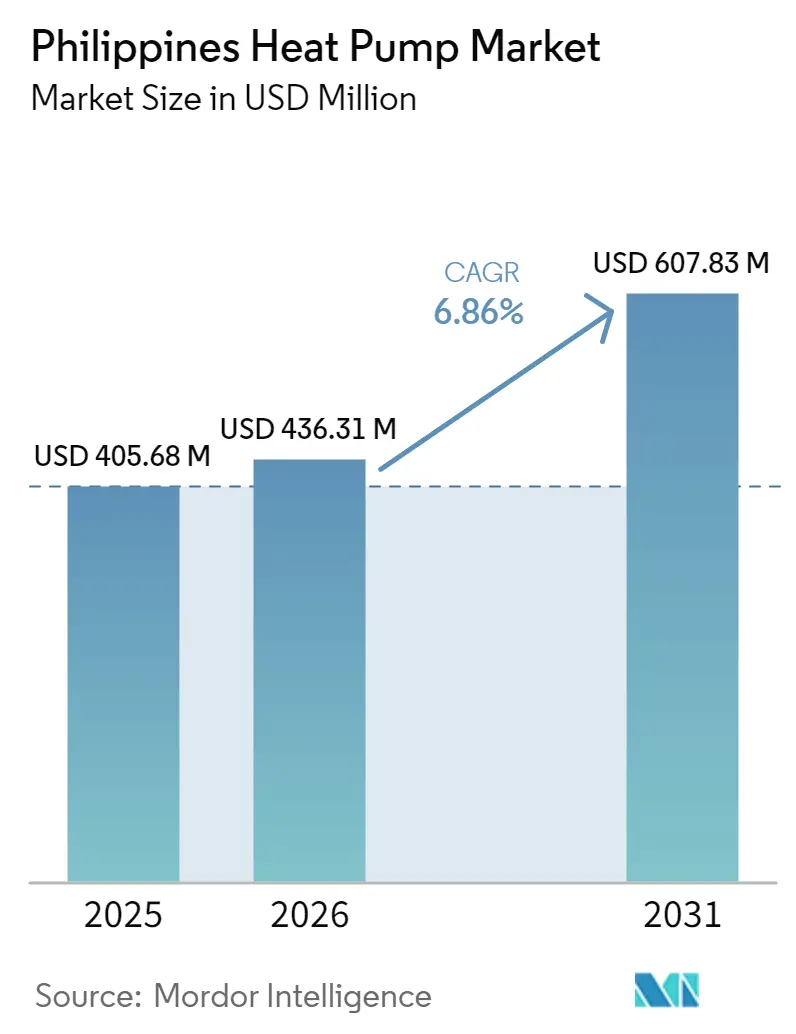

| Base Year Market Size (2025) | USD 405.68 Million |

| Market Size (2026) | USD 436.31 Million |

| Market Size (2031) | USD 607.83 Million |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Heat Pump Market Analysis by Mordor Intelligence

The Philippines heat pump market size is projected to expand from USD 405.68 million in 2025 and USD 436.31 million in 2026 to USD 607.83 million by 2031, registering a CAGR of 6.86% between 2026 to 2031. Penetration is rising as national electrification strategies converge with the Kigali-aligned refrigerant phase-out, while domestic hot-water demand in Metro Manila, Central Luzon and Cebu mid-rise towers offers a near-term volume floor. Commercial and industrial buyers gain from Philippine Economic Zone Authority fiscal privileges, which shorten payback periods and strengthen the business case for switching from liquefied petroleum gas boilers. Off-grid island resorts and agro-industrial parks face some of the country’s highest electricity tariffs, accelerating hybrid heat pump uptake that pairs air-source compressors with solar thermal collectors. Competitive intensity remains moderate, anchored by long-established Japanese and South Korean brands, yet Chinese suppliers are disrupting provincial projects through lower pricing and bundled installation training, shifting price-service expectations across the Philippines heat pump market.

Key Report Takeaways

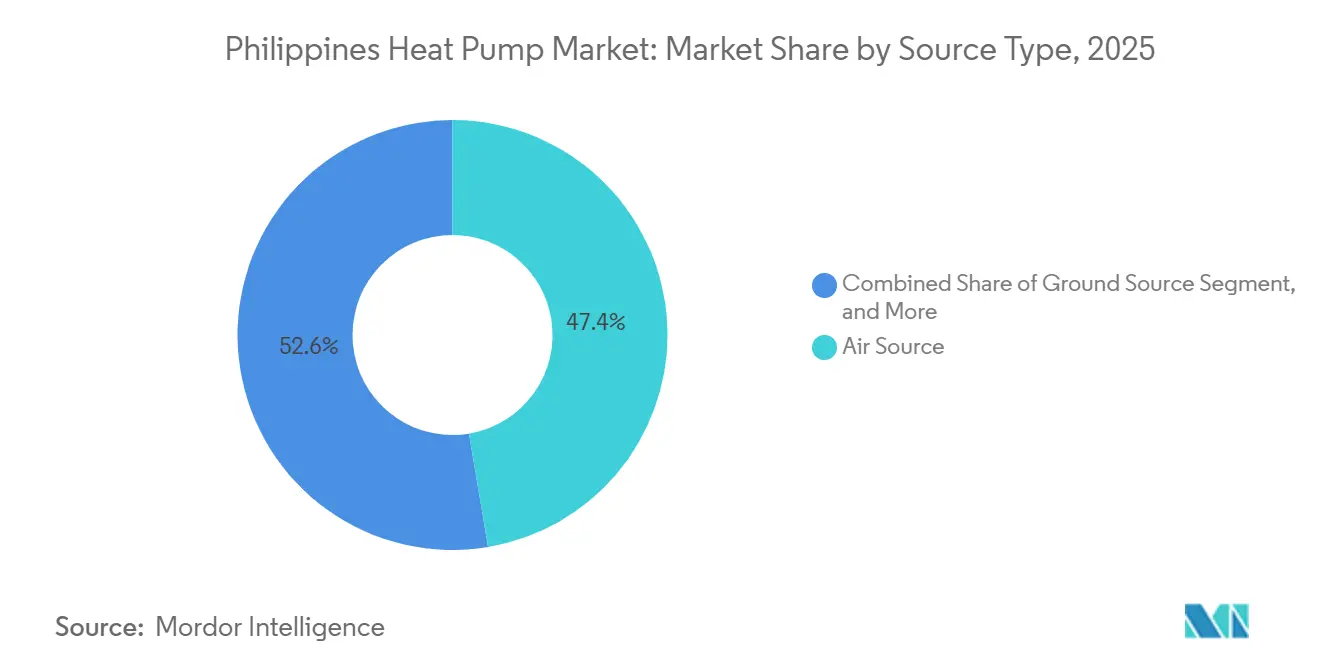

- By source, air source systems led with 47.36% share of the Philippines heat pump market in 2025, while hybrid configurations are forecast to grow at a 7.61% CAGR through 2031.

- By technology, air-to-water technology commanded 40.14% of 2025 demand; ground-to-water solutions are poised for a 7.38% CAGR over the same horizon.

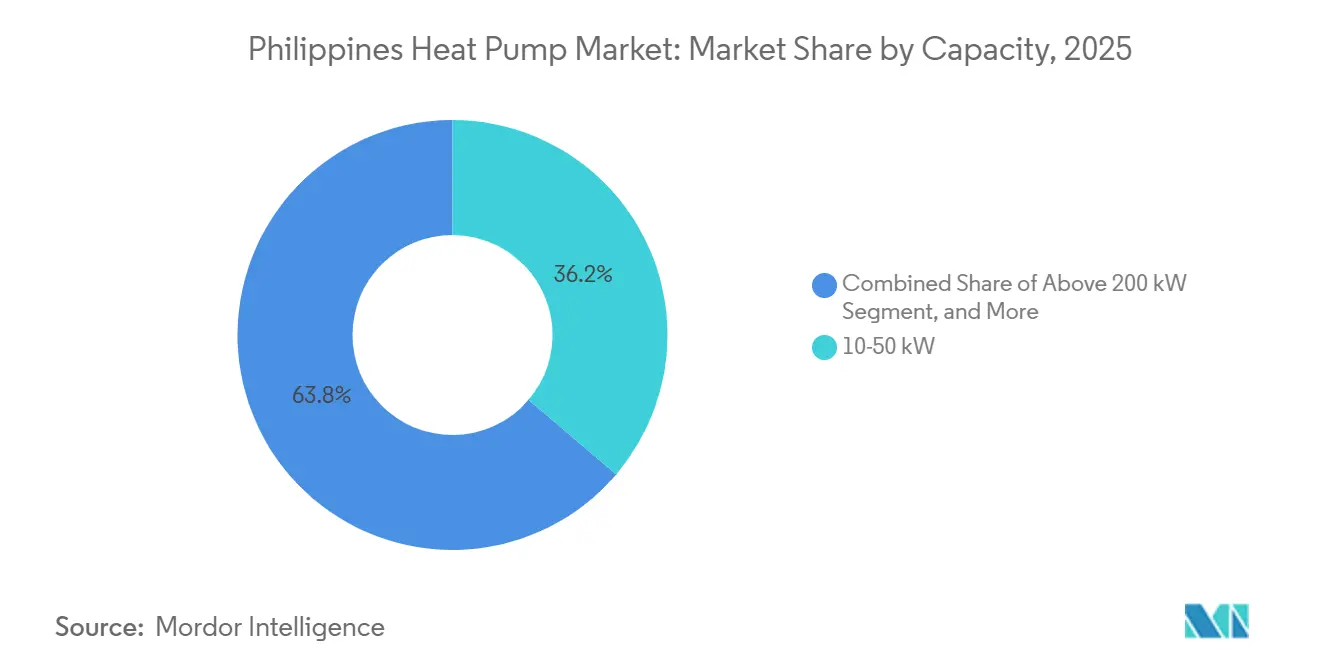

- By capacity, units rated 10-50 kilowatts accounted for 36.23% of 2025 sales; equipment in the 50-200 kilowatt class will post the fastest growth at 7.24% a year.

- By application, domestic and sanitary hot water applications represented 43.87% of 2025 revenues, whereas industrial process heating is set to expand at 7.56% annually to 2031.

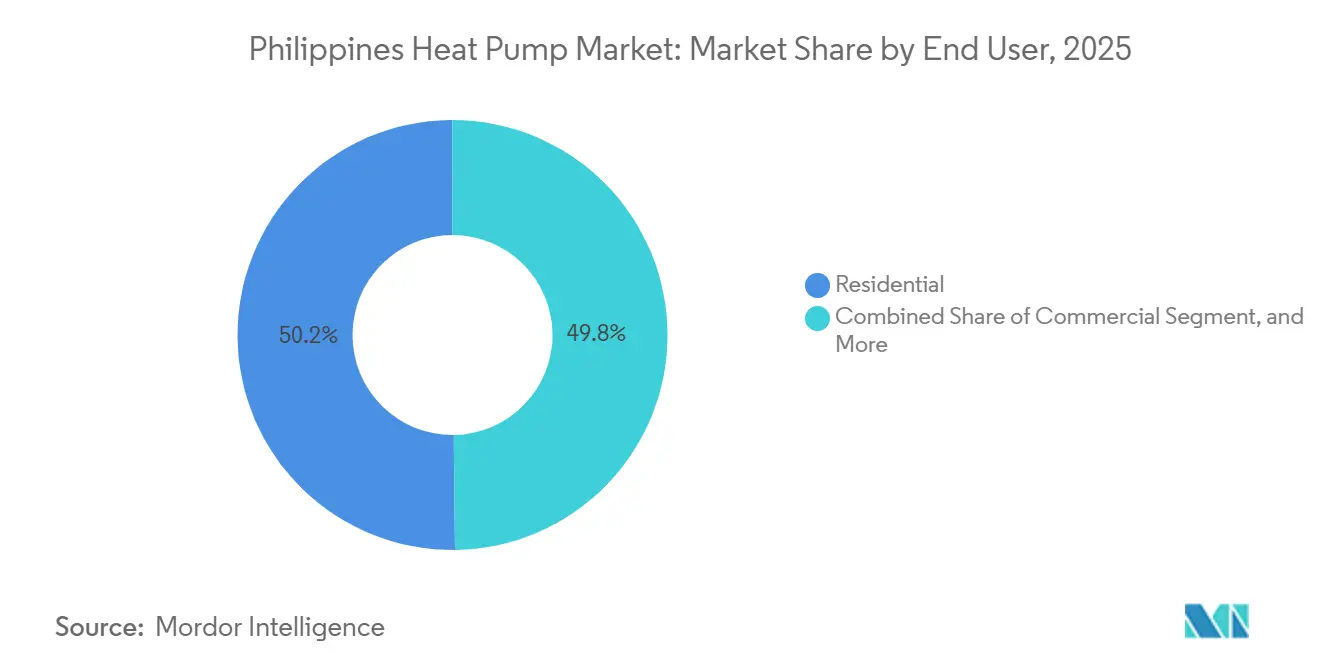

- By end user, residential buyers held 50.19% share of the Philippines heat pump market in 2025, yet industrial users are projected to advance at a 7.03% CAGR.

- By installation, new-build projects captured 53.43% of 2025 installations, but retrofit activity will climb by 6.97% a year as older hotels and factories modernize plant rooms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Use of Heat Pumps Beyond Traditional Heating, Ventilation, and Air Conditioning Applications | +1.2% | National, concentrated in Metro Manila, Central Luzon, Cebu | Medium term (2-4 years) |

| Implementation of Government Incentives for Renewable Heating | +1.0% | National, early gains in Philippine Economic Zone Authority zones | Medium term (2-4 years) |

| Rapid Urbanization and Mid-Rise Residential Boom | +0.9% | Metro Manila, Cebu, Davao, Central Luzon | Short term (≤ 2 years) |

| Nationwide Phase-Out of High Global Warming Potential Refrigerants | +0.8% | National | Long term (≥ 4 years) |

| Electrification of industrial process heating in special economic zones | +0.7% | Central Luzon, Calabarzon, Cebu | Medium term (2-4 years) |

| Surge in off-grid tourism resorts adopting heat pump systems | +0.5% | Palawan, Boracay, Siargao, Bohol | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Use of Heat Pumps Beyond Traditional Heating, Ventilation, and Air Conditioning Applications

Large cold-chain facilities are specifying industrial-scale heat pumps to maintain temperatures that range from -25 °C for ice cream to 13 °C for banana ripening, underpinning diversification away from comfort cooling.[1]Department of Agriculture Philippines, “Bicol Mega Cold Storage Warehouse Inauguration,” DA.gov.ph The 11,728-pallet Mindanao warehouse commissioned in March 2026 integrates renewable power through the Green Energy Option Program, proving out the technology in energy-intensive logistics operations. Hospitality properties such as Park Inn Clark realized 240,000 kWh in annual savings after adopting centralized systems, which validates the operating-expense upside for hotels. Developers of turnkey factory shells inside special economic zones now embed heat pumps as standard utility infrastructure to lure export manufacturers. This widening usage spectrum positions the Philippines heat pump market as a cross-sector solution rather than a single-application product line.

Implementation of Government Incentives for Renewable Heating

The memorandum of understanding on Sustainable Green Industrial Parks grants tax holidays and duty exemptions when factories install energy-efficient equipment, immediately tilting capital-spending decisions toward heat pumps.[2]Philippine Economic Zone Authority, “Sustainable Green Industrial Parks Memorandum of Understanding,” PEZA.gov.ph The Department of Energy consultation on stricter minimum energy performance standards, started in 2025, signals that residential and commercial water heaters will soon face mandatory efficiency floors.[3]Department of Energy Philippines, “Consultation on Minimum Energy Performance Standards for Air Conditioners,” DOE.gov.ph Although direct consumer rebates are absent, the Green Energy Option Program lowers the delivered cost of power for high-load users, narrowing the price gap with liquefied petroleum gas heaters. The Philippine Green Building Council is lobbying for a revised National Building Code that will require centralized heat pump water heaters in mid-rise projects above 10 floors, effectively mandating the technology for most future condominiums. Taken together, the policy stack offers predictable demand visibility that benefits both local distributors and multinational manufacturers in the Philippines heat pump market.

Rapid Urbanization and Mid-Rise Residential Boom

About 930 hectares of new industrial land are entering Central Luzon between 2026 and 2028, bringing with them Samsung Electronics’ USD 1 billion plant and a USD 500 million hyperscale data center, both reliant on high-efficiency heat pump systems. Residential towers in Metro Manila continue to break ground despite 30,000 unsold units, and centralized water-heating is now a baseline feature for differentiation. Cebu office transactions jumped 70% year-over-year in 2025, and most new buildings there specify variable refrigerant flow heat pump solutions that adapt to fluctuating tenant densities. Urban clustering in these three regions allows suppliers to consolidate logistics and service operations, lowering per-unit costs. Secondary cities like Iloilo and Bacolod remain underserved, creating a push-pull dynamic where distribution networks expand to follow construction hotspots.

Nationwide Phase-Out of High Global Warming Potential Refrigerants

National greenhouse-gas inventories show 35.5 million t CO₂-e from refrigeration equipment in 2025, accelerating the shift from R410A to R32-charged units that cut global warming potential by 68%.[4]Department of Environment and Natural Resources, “Greenhouse Gas Inventory for Refrigeration and Air Conditioning Sector,” DENR.gov.ph Panasonic, Daikin and Mitsubishi Electric already ship R32 across their Philippine residential lines, capturing early-mover credibility. Variable refrigerant flow systems are next in line for transition, spurring redesigns that add A2L-rated safety features and lift bill-of-materials cost by up to 12% but future-proof product portfolios. Manufacturers with established R32 supply chains gain a compliance head start while smaller brands face re-tooling pressures. The refrigerant pivot thus works as both an environmental mandate and a competitive filter in the Philippines heat pump market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Installation Cost and Limited Financing | -0.9% | Nationwide, acute in middle-income residential segment | Short term (≤ 2 years) |

| Shortage of Certified Heat Pump Technicians | -0.7% | Nationwide, severe in Visayas and Mindanao | Medium term (2-4 years) |

| Grid instability in rural islands | -0.5% | Off-grid islands in Mindanao, Visayas, Palawan | Long term (≥ 4 years) |

| Fragmented after-sales service ecosystem | -0.4% | Provincial cities outside Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Installation Cost and Limited Financing

Residential heat pump water heaters range from PHP 55,000 (USD 0.98 million per 1,000 units) to PHP 232,500 (USD 4.13 million per 1,000 units), equal to three to twelve months of median household income and thus out of reach for most families without credit support. Stiebel Eltron units sell at 30-40% above local brands, confining them to upper-income buyers. Banks rarely issue green-technology loans to homeowners, so cash purchases dominate, slowing velocity in the Philippines heat pump market. Commercial and industrial buyers offset costs through tax breaks, widening the affordability gap between segments. Until concessional lending or rebate schemes emerge, residential adoption will underperform the headline market growth.

Shortage of Certified Heat Pump Technicians

TESDA’s partnership with TCL certifies roughly 200 technicians per year, versus an estimated 8,000-10,000 annual installations that need commissioning and maintenance.[5]Technical Education and Skills Development Authority, “HVAC Training Center Partnership with TCL,” Tesda.gov.ph LG’s Cebu academy focuses on dealer education but does not fully cover independent service providers. The deficit inflates labor rates, extends warranty response times and occasionally voids coverage when unqualified personnel handle refrigerants. Skills gaps are more acute for ground-source systems, which demand hydrogeologic expertise not taught in conventional HVAC curricula. This manpower bottleneck threatens service quality and could temper brand reputation within the Philippines heat pump market over the next three years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Air-source dominance drives market evolution

Hybrid systems captured a marginal share in 2025 but are forecast to grow at 7.61% annually through 2031, outperforming the Philippines heat pump market by 75 basis points as island resorts and agro-industrial parks seek resilience against tariffs of PHP 16-25 (USD 0.29-0.45) per kWh. Air source platforms provide 47.36% of 2025 demand by leveraging lower first cost and compatibility with Metro Manila electrical infrastructure. Water source solutions serve coastal resorts where inlet temperatures stabilize efficiency above a 4.0 coefficient of performance, though permitting hurdles lengthen project cycles. Ground source adoption concentrates in institutional flagship projects like the December 2025 900 kW geothermal tie-in at Capitol University Medical Center.

Manufacturers now roll out modular lines that toggle between air-source and solar-thermal modes based on spot-market power pricing, optimizing lifetime energy spend. LG’s Multi V Water 5 unit, demonstrated in Cebu, features a wide 20-150 Hz inverter range, widening partial-load efficiency. Air source heat pumps dominate the residential slice of the Philippines heat pump market size equation but face diminishing returns during peak-temperature months. Hybrid and water-based systems fill that performance gap, although higher engineering complexity restricts uptake to projects with sound technical oversight.

By Technology: Ground-to-Water Gains in Geothermal Corridors

Air-to-water units held 40.14% of the Philippines heat pump market share in 2025, mainly due to condominium developers favoring centralized domestic hot water risers. Ground-to-water technology will advance by 7.38% a year, tapping Luzon’s geothermal belt where First Gen operates 1,870 MW of capacity. Air-to-air models play in the residential split-type upgrade cycle, commanding 15-20% price premiums in cooler upland cities. Water-to-water remains confined to industrial process loops requiring tight temperature control.

Daikin’s MARUTTO platform integrates variable refrigerant flow, water heating and building management to recycle data-center waste heat into adjacent residences. Installation cost for bore-hole loops ranges from PHP 8,000-12,000 (USD 143-214) per kW and elongates project timelines, but 20-25% higher seasonal efficiency offsets capex in 15-year asset plans. Air-to-water designs therefore dominate new builds, while ground-to-water wins in owner-occupied facilities committing to long-range operating savings.

By Capacity: Mid-Range Units Anchor Condominium Deployments

Systems rated 10-50 kW made up 36.23% of the Philippines heat pump market in 2025, aligning with the load of 50-100 unit condominium stacks. The 50-200 kW band is on track for a 7.24% CAGR as cold-storage and full-service hotels replace boilers with centralized water heaters that delivered 240,000 kWh savings at Park Inn Clark. Sub-10 kW sales lag because high per-kilowatt prices deter single-family buyers, while above-200 kW projects demand custom engineering.

Haier’s MRV 5 DC Inverter supports 1,000 m piping runs, enabling rooftop placement on 30-story towers without intermediate plant rooms. Commercial buyers increasingly oversize capacity then throttle compressors during off-peak tariffs below PHP 6 (USD 0.11) per kWh, improving lifecycle economics. Mid-range units thus balance scale economies and installation simplicity, sustaining their central role in the Philippines heat pump market size profile.

By Application: Industrial Process Heating Electrifies Special Economic Zones

Domestic and sanitary hot water dominated with 43.87% share in 2025 as condominium developers chased Green Building Code targets. Industrial process heating will climb 7.56% annually, led by food processors and pharmaceutical lines inside Philippine Economic Zone Authority parks that earn renewable-energy credits on electrified steam production. Space heating is minor outside upland resorts, but reversible variable refrigerant flow systems are winning office retrofits needing simultaneous heating and cooling.

The Department of Agriculture’s PHP 500 million Bicol cold-storage hub stipulates blast-freezing at -25 °C, illustrating how cascade heat pump cycles converge with industrial refrigeration demands. Hotels such as Dusit Thani Lubi Plantation reclaim heat-pump waste energy to preheat showers, slicing primary energy 30-40%. Multifunction equipment capable of toggling between water heating, pool heating and space conditioning broadens the application base across the Philippines heat pump market.

By End User: Industrial Segment Capitalizes on Fiscal Incentives

Residential buyers held 50.19% of 2025 revenues, propelled by high-rise condominium projects that lock in scale economies for centralized systems. Industrial users will pace growth at 7.03% a year, driven by semiconductor, cold-chain and data-center clients seeking scope-2 emissions cuts and fiscal incentives. Commercial properties such as hospitals and hotels remain a stable mid-volume tier that values uptime and warranty depth.

Mayekawa’s ammonia-based heat pumps dominate blast-freeze plants, demonstrating industrial appetite for natural refrigerants. LG’s BECON Cloud at SM North EDSA shows retail landlords pursuing predictive maintenance to cut downtime 15-20%. Cross-segment convergence emerges as residential developers adopt commercial-grade gear, while industrial parks pre-install heat pumps to accelerate tenant occupancy.

By Installation: Retrofit Growth Reflects Building Stock Aging

New construction supplied 53.43% of 2025 demand because pipeline projects could integrate centralized systems from day one. Retrofits will edge ahead at 6.97% CAGR as Makati and Ortigas hotels nearing 30 years of service swap resistance heaters for heat pumps, cutting payback to three-five years. Retrofit complexity inflates cost because electrical panels and piping need upgrades, yet operating savings offset hurdles.

Discovery Primea’s chilled-water pump retrofit realized 30% energy cuts and validates bundled modernization packages that pair new equipment with control upgrade. As Metro Manila’s vacancy drags new starts, retrofit spending will cushion equipment distributors, reinforcing the Philippines heat pump market’s resilience.

Geography Analysis

Metro Manila, Central Luzon and Cebu anchor more than half of nationwide sales through dense construction pipelines, mature distributor networks and concentration of fiscal incentives. Condominium developers in Makati and Bonifacio Global City deploy centralized heat pump water heaters to lower common-area expenses despite a 25% vacancy overhang, ensuring baseline equipment turnover. Grade-A offices accredited by the Philippine Economic Zone Authority attract multinationals that specify VRF heat pumps with building-management integration. Central Luzon adds 930 hectares of industrial land by 2028, spearheaded by Samsung’s USD 1 billion plant and G42’s USD 500 million data center, both depending on multi-megawatt heat pump infrastructure. Cebu office leasing surged 70% in 2025, and LG’s Mandaue academy expands contractor capacity across Visayas and Mindanao.

Mindanao shows a dual profile where Davao and Cagayan de Oro enjoy grid stability suitable for commercial adoption, while off-grid islands pay tariffs of PHP 16-25 (USD 0.29-0.45) per kWh that push hybrid solar-heat-pump schemes. GMAC’s 11,728-pallet cold store and the Bicol food hub illustrate government-led cold-chain build-outs that raise industrial demand beyond Luzon. Resort clusters in Palawan, Boracay, Siargao and Bohol pilot hybrid systems pairing evacuated-tube collectors with air-source compressors to hedge against outages. Villa Escudero’s 2024 installation validates tourism applications though absolute volumes remain small.

Secondary cities such as Iloilo, Bacolod and Pampanga now host business-process outsourcing expansions that need 24/7 cooling, fuelling variable refrigerant flow retrofits. Clark Freeport Zone positions itself as a data-center alternative to Metro Manila, yet limited service ecosystems outside the capital compel developers to negotiate factory-direct warranties, inflating project risk. The Department of Agriculture’s national cold-chain budget will add nodes in Cagayan Valley and Eastern Visayas, broadening geographic spread but still reliant on a Manila-Cebu service backbone. Over the forecast horizon, the Philippines heat pump market will remain top-heavy in three core regions while gradually diffusing into industrial corridors and tourism islands.

Competitive Landscape

Market concentration is moderate, with Mitsubishi Electric, Daikin, Panasonic, LG and Samsung controlling dealership primacy in Metro Manila and Cebu through decades-old air-conditioning franchises. Chinese challengers PHNIX, Haier and TCL court provincial special economic zones by undercutting prices 15-20% and bundling extended warranties plus on-site training. LG’s Cebu showroom and TCL’s 500-partner Manila convention highlight a pivot toward contractor education and after-sales robustness in response to the nationwide technician shortfall.

Haier promotes its MRV 5 inverter with 1,000 m piping capability, a feature aimed at high-rise projects that lack intermediate plant rooms, while PHNIX offers all-in-one commercial heat pump water heaters accredited for R32-based safety protocols. European entrants Stiebel Eltron, Vaillant and NIBE pursue upper-income residential buyers with high-COP products and 10-year warranties, positioning themselves as premium alternatives. Mayekawa supplies ammonia packages for blast-freeze plants, commanding a niche in industrial refrigeration that few competitors address.

Strategic differentiation is shifting from efficiency specs to lifecycle service propositions. LG’s BECON Cloud, deployed at SM North EDSA, provides predictive diagnostics that cut downtime 15-20%, creating stickiness with facility operators. Chinese makers scale market share by co-sponsoring TESDA training modules, tightening the feedback loop between equipment supply and workforce readiness. Retrofit white-space in aging Makati hotels and industrial process heating conversions in export parks offer runway for both incumbents and newcomers, yet brands without regional service depth risk warranty erosion in a still-developing after-sales landscape.

Philippines Heat Pump Industry Leaders

Stiebel Eltron GmbH & Co. KG

Viessmann Climate Solutions SE

Glen Dimplex Group

PHNIX Eco-Energy Solution Ltd.

WaterFurnace International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Department of Agriculture inaugurated a PHP 500 million (USD 8.9 million) cold-storage warehouse in Bicol with 2,688 pallet positions, integrating solar power and large-capacity heat pumps.

- March 2026: GMAC Logitech opened an 11,728-pallet cold store in Davao del Norte that shifts to renewable energy via the Green Energy Option Program.

- February 2026: TCL gathered 500 partners at its “AIrfinite Possibilities” event in Manila to unveil AI-enabled HVAC controls and extended warranties.

- February 2026: Haier launched the UV Cool Smart split-type air conditioner and showcased the MRV 5 DC Inverter system at its dealer conference in Bonifacio Global City.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Philippines heat pump market as all factory-built air, water, or ground-source systems of any rated capacity that provide space heating, space cooling, or sanitary hot water in residential, commercial, industrial, and institutional facilities.

Scope exclusion: window-type room air-conditioners that cannot operate in heating mode are outside the estimate.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Conversations with Filipino HVAC contractors, distributor managers, energy auditors, and facility engineers validated price bands, penetration rates in new condominiums, and average replacement cycles. Interviews were spread across Luzon, Visayas, and Mindanao to capture climatic and purchasing differences, allowing us to challenge and refine secondary assumptions.

Desk Research

We began with public data sets from agencies such as the Philippine Statistics Authority, Bureau of Customs, and the DOE's energy efficiency office, pairing them with ASEAN trade statistics and UN COMTRADE shipment codes for HS-8418 equipment. Company filings, tender portals, and utility rebate lists helped map installation trends, while peer-reviewed HVAC journals clarified typical coefficient-of-performance ranges. To size local manufacture volumes, our analysts accessed D&B Hoovers for producer revenues and Dow Jones Factiva for plant announcements. The sources cited above are illustrative; many additional references supported gap checks and context building.

A second pass verified import growth, electricity tariff shifts, and building permit counts, which act as leading indicators for retrofit and new-build demand. This triangulation anchored the historical base before any primary outreach.

Market-Sizing & Forecasting

The model starts top-down: import-export flows and local production are reconstructed into unit volumes, multiplied by channel-checked average selling prices to yield the 2024 value. Select bottom-up cross-checks, installer roll-ups and sampled project BOQs flag divergences and prompt adjustments. Key variables include new residential floor area, hotel occupancy growth, electricity-to-LPG price ratio, equipment SPF improvement, and government tax-incentive uptake. A multivariate regression with these drivers underpins the 2025-2030 forecast; scenario analysis tests policy or fuel-price shocks. Where bottom-up inputs are patchy, substitution patterns from analogous ASEAN peers plug gaps before final balancing.

Data Validation & Update Cycle

Outputs undergo variance screens against historical energy demand, followed by a two-step peer review. Mordor refreshes every twelve months, with interim updates triggered by material events (for example, subsidy revisions). A final analyst check is completed just before publication so clients receive the latest view.

Why Mordor's Philippines Heat Pump Baseline Commands Confidence

Published estimates often diverge because firms apply different geographic scopes, include non-reversible equipment, or project growth from optimistic uptake assumptions.

Key gap drivers here are (a) Mordor's strict exclusion of pure cooling RACs, (b) our moderate 7.27% CAGR anchored to verified building activity, and (c) our annual refresh cadence, whereas others lift multi-year projections without updated trade checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 406.5 million | Mordor Intelligence | - |

| USD 576.9 million | Regional Consultancy A | Bundles reversible air-air ACs and assumes rapid subsidy roll-out |

| USD 50.48 billion (Asia-Pacific) | Global Consultancy B | Uses regional roll-down; Philippines share inferred, not measured |

In short, Mordor analysts anchor values to traceable volumes, realistic penetration paths, and routine validation, giving decision-makers a balanced baseline they can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the projected value of the Philippines heat pump market by 2031?

It is forecast to reach USD 607.83 million, reflecting a 6.86% CAGR between 2026 and 2031.

Which source type is growing fastest in Philippine deployments?

Hybrid configurations that combine air-source compressors with solar thermal collectors are expected to expand at 7.61% a year through 2031.

Why are industrial users adopting heat pumps more rapidly?

Fiscal incentives in Philippine Economic Zone Authority parks and rising scope-2 emissions targets make heat pumps more economical than liquefied petroleum gas boilers for process heating.

How does the refrigerant phase-out affect equipment selection?

Tightening regulations push manufacturers toward R32-charged units, giving early-compliant brands a competitive edge and ensuring lower global warming potential.

What remains the biggest hurdle for residential buyers?

High up-front costs, ranging from PHP 55,000 to PHP 232,500, coupled with limited financing, slow mass-market adoption despite favorable operating economics.

Which regions lead in heat pump installations?

Metro Manila, Central Luzon and Cebu together account for the majority of installations because of dense real-estate pipelines and well-developed distributor networks.

Page last updated on: