Japan Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

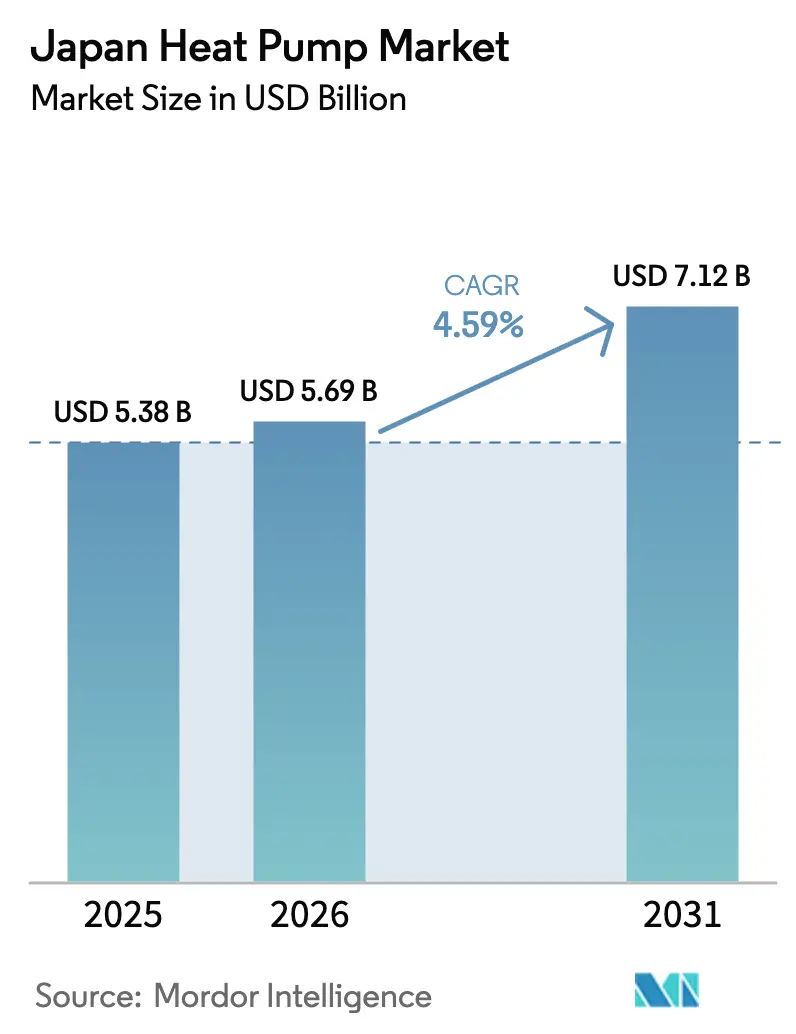

| Base Year Market Size (2025) | USD 5.38 Billion |

| Market Size (2026) | USD 5.69 Billion |

| Market Size (2031) | USD 7.12 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

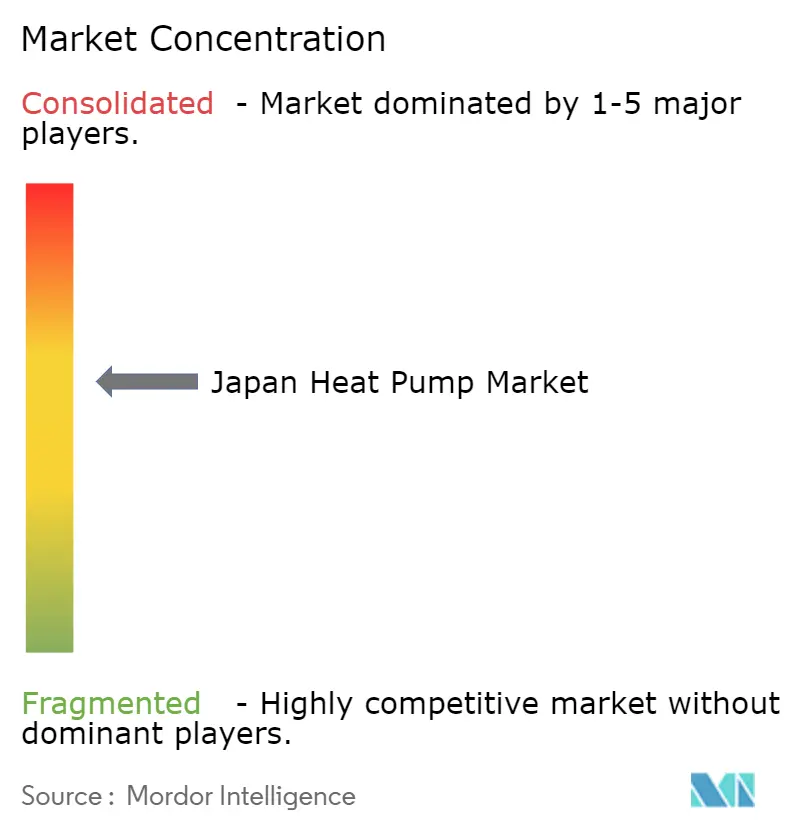

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Heat Pump Market Analysis by Mordor Intelligence

The Japan heat pump market size is expected to increase from USD 5.38 billion in 2025 to USD 5.69 billion in 2026 and reach USD 7.12 billion by 2031, growing at a CAGR of 4.59% over 2026-2031. Steady gains reflect the nation’s pivot toward electrified heating and cooling as carbon-pricing begins, subsidies expand and high-efficiency R-290 and CO₂ systems move into mass production. Hybrid configurations that mix electric and fossil back-up burners are spreading beyond snow-belt prefectures as electricity-price volatility grows, while high-temperature industrial models rated above 130 °C unlock new process-heating opportunities. Competitive tension remains elevated: domestic leaders Daikin, Mitsubishi Electric and Panasonic still command roughly 60% of shipments but now defend share against lower-cost Korean and Chinese inverters. Workforce bottlenecks and installation complexity temper momentum, yet sustained policy incentives and grid-flexibility pilots keep the medium-term outlook favorable.

Key Report Takeaways

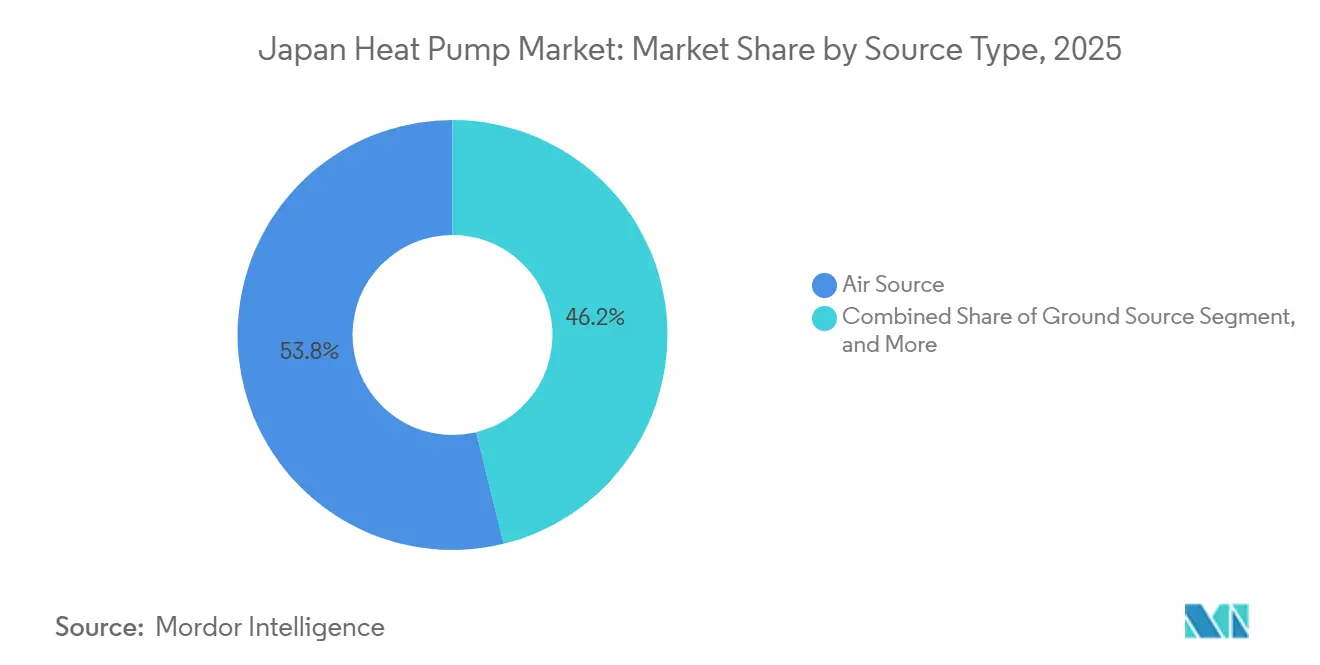

- By source type, Air Source led with 53.81% revenue share in 2025; Hybrid systems record the fastest projected CAGR at 5.31% through 2031.

- By technology, Air-to-Water captured 48.62% revenue share in 2025, while Ground-to-Water is forecast to expand at a 5.02% CAGR to 2031.

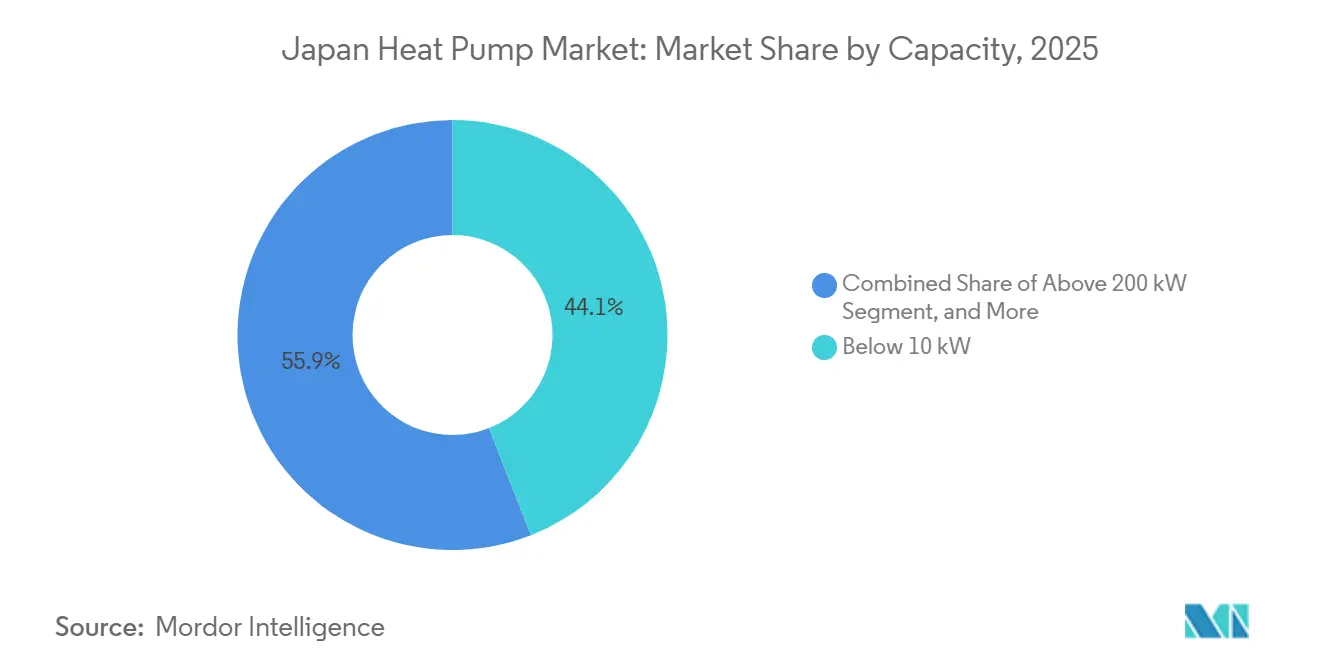

- By capacity, systems below 10 kW held 44.06% of Japan heat pump market share in 2025 and installations above 200 kW are set to advance at a 5.13% CAGR between 2026-2031.

- By application, Domestic and Sanitary Hot Water accounted for a 48.21% share of the Japan heat pump market size in 2025, whereas the Other Applications cluster is projected to climb at a 4.87% CAGR.

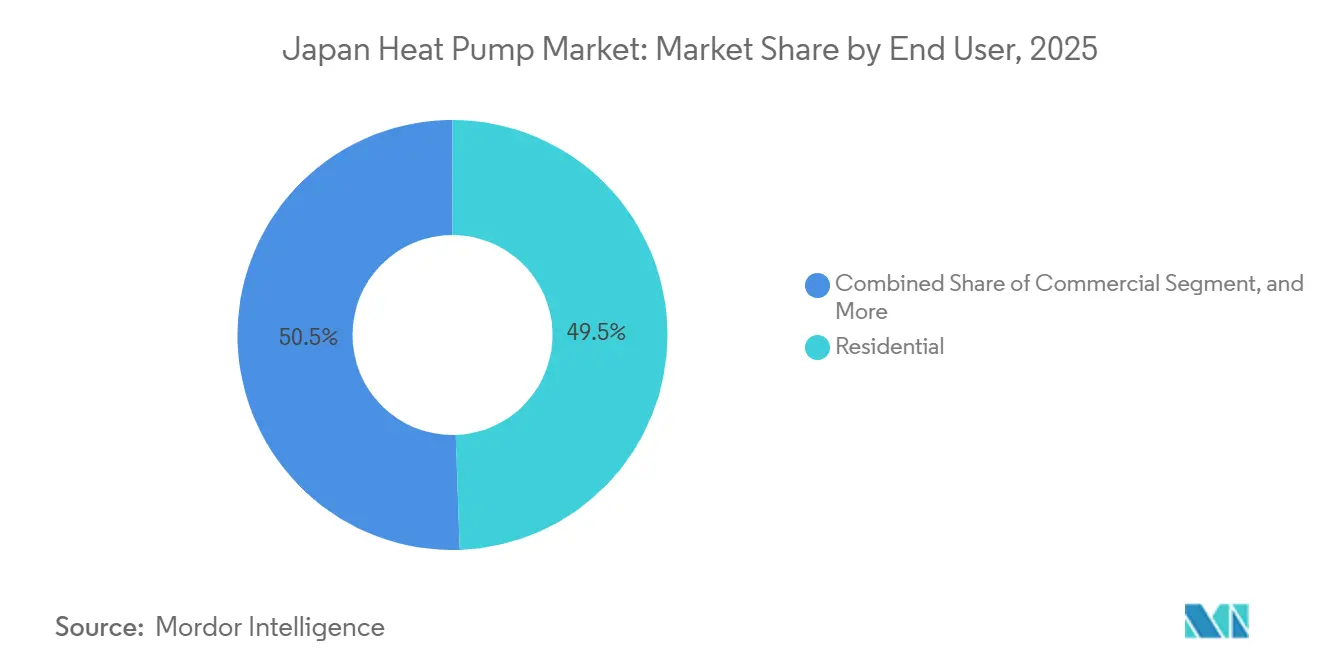

- By end user, Residential represented 49.47% revenue share in 2025, yet Industrial use is poised for the highest CAGR at 5.26% through 2031.

- By installation type, New Installation held 54.12% of 2025 revenue and Retrofit demand is expected to grow at a 4.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation of Government Policies and Incentives Promoting Energy-Efficient HVAC | +1.2% | National, strong in Hokkaido, Tohoku and Tokyo-Osaka corridor | Medium term (2-4 years) |

| Electrification Targets Under Japan's GX Roadmap | +0.9% | National | Long term (≥4 years) |

| Decarbonization of Domestic Water-Heating Demand | +0.8% | National, urban retrofits | Medium term (2-4 years) |

| Growing Use of Heat Pumps Beyond Traditional HVAC | +0.6% | National, early industrial uptake in Chubu and Kansai | Medium term (2-4 years) |

| Emergence of Fourth-Generation District Heating | +0.4% | Regional pilots in Hokkaido and Tokyo | Long term (≥4 years) |

| Expansion of Data Center Waste-Heat Recovery | +0.3% | Tokyo, Osaka and Fukuoka clusters | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Implementation of Government Policies and Incentives Promoting Energy-Efficient HVAC

Generous 2026 subsidies cover up to 40% of equipment and labor for households swapping legacy oil or gas boilers, creating an immediate pull on the order backlog.[1]Ministry of Economy, Trade and Industry, “GX Green Transformation Roadmap,” METI.go.jp Local add-ons in Hokkaido and Aomori shrink net homeowner outlays by another USD 1,000-2,000, overcoming performance anxiety during sub-zero winters.[2]Hokkaido Prefectural Government, “Heat Pump Subsidy Program 2026,” Hokkaido.lg.jp Mandatory energy codes that took force in April 2025 effectively eliminate low-efficiency furnaces from new builds, channeling procurement toward inverter-driven air-to-water units that price roughly 18% higher than past workhorse models. Carbon pricing under the 2026 GX Emissions Trading Scheme puts a USD 17-21 shadow cost on industrial CO₂, nudging factories toward high-temperature heat pumps. Accelerated depreciation granted under the Act on Rationalizing Energy Use sweetens payback for commercial retrofits.

Electrification Targets Under Japan's GX Roadmap

The roadmap assigns heat pumps a leading role in displacing 8 million kL of oil-equivalent by 2030, tying appliance uptake to national net-zero ambitions. A grid-wide demand-response pilot begun in January 2026 pays households up to USD 0.10 per kilowatt-hour for curtailment, cushioning evening peaks that once strained the TEPCO network.[3]Organization for Cross-regional Coordination of Transmission Operators, “Demand Response Pilot 2026,” OCCTO.or.jp Utilities must line up 20 GW of flexible capacity by 2030, and large heat-pump plants paired with thermal storage now qualify for capacity payments, improving project revenue stacks. Real-time pricing analytics co-developed by Daikin and Hitachi trim commercial operating costs by roughly 13% and illustrate the virtuous cycle between smart controls and grid services. Together, these measures tighten the policy-technology loop that underpins long-run demand.

Decarbonization of Domestic Water-Heating Demand

Water heating represents more than one-quarter of household energy, so the pledge to equip 14 million homes with heat-pump boilers by 2030 carries outsized policy weight. Noritz and Nihon Itomic’s CO₂ units reach 90 °C outlet temperature, addressing cultural bathing norms and unlocking cold-season performance gains. A USD 8 million public grant will lift output to 50,000 units per year by 2027. Tokyo Gas, historically wedded to combustion appliances, pivots to hybrid heat-pump marketing ahead of a USD 67-per-ton carbon levy slated for 2033.[4]Tokyo Gas, “Shift to Heat Pump Systems 2025,” TokyoGas.co.jp Panasonic’s Czech expansion adds overseas scale and a cold-climate R and D hub that feeds back into Japanese product lines.

Growing Use of Heat Pumps Beyond Traditional Heating and Cooling

Process heating consumes roughly 40% of manufacturing energy, and vendors now deliver CO₂ and R-1234ze machines producing steam at 130-150 °C.[5]International Energy Agency, “Heat Pumps Deployment Barriers 2025,” IEA.org Mitsubishi Heavy’s 640 kW ETI-W series targets breweries and chemical plants switching off heavy-oil boilers. JEXSYS demonstrates 130 °C COP 3.2 recovery from steel-mill flue gas, while Fuji Electric readies a two-stage 150 °C prototype for 2027 deployment. Daikin’s R-290 models scale to 2 MW, suiting district networks and large campuses. A USD 100 million Green Innovation Fund call now backs pilots that pair heat pumps with hydrogen electrolyzers, lowering electrolysis energy use by up to 10%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficulties in Installation and High Installation Cost | -0.7% | Dense urban zones of Tokyo and Osaka | Short term (≤2 years) |

| Installer Skill Shortages | -0.5% | Rural prefectures with aging technician base | Medium term (2-4 years) |

| Diminishing Renewable Energy Certificate Value | -0.3% | Commercial and industrial buyers nationwide | Medium term (2-4 years) |

| Competition from Solid-State Thermoelectric Modules | -0.1% | Automotive and electronics niches | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Difficulties in Installation and High Installation Cost

Ground-source projects demand 50-100 m boreholes and hydronic retrofits, inflating budgets to USD 20,000-33,000 and stretching schedules by up to six weeks. Tight property lines in metropolitan wards force costly vertical drilling that adds another USD 5,300-8,000.[6]Japan Refrigeration and Air Conditioning Industry Association, “Installer Survey 2025,” JRAIA.or.jp Legacy radiators designed for 80 °C supply water often require upsizing, doubling expenses and lengthening downtime. Concerns over borehole integrity in seismic terrain lead 42% of contractors to avoid these jobs outright. Setback rules under the Building Standards Act further squeeze feasibility for small lots and heighten soft-cost risk.

Installer Skill Shortages

Nearly 4 in 10 certified technicians are older than 55 and annual apprenticeships run 2,000 short of replacement needs Hybrid and ground-source systems require multidisciplinary prowess, yet only 1,200 trainees entered heat-pump tracks in 2025. Lead times for residential installs now stretch past eight weeks, double that of gas furnaces. AI remote-diagnostics can trim service calls, but IoT sensor kits add USD 330-530 to upfront costs and still rely on qualified labor for commissioning. A mandatory 40-hour refrigerant course taking effect in April 2027 may push 15-20% of current installers out of the field.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Systems Bridge Fuel-Switching Flexibility

Air Source units generated 53.81% of 2025 revenue in the Japan heat pump market, a dominance rooted in modest upfront costs and ease of installation across temperate coastal regions. Water and Ground Source variants together remained near 12% because borehole drilling and water-body access add complexity that many urban projects cannot absorb. Hybrid configurations, though still a minority, are scaling at 5.31% annually as homeowners and building managers prize the ability to toggle between electricity and gas when tariffs spike or deep freezes sap efficiency, a pattern most visible in Hokkaido’s harsher winters. Tokyo Gas’ decision to end stand-alone gas water-heater sales from April 2026 both validates and propels this pivot toward dual-fuel resilience.

Grant-backed production of CO₂ hybrid water heaters rated at 90 °C should lift annual output to 50,000 units by 2027, directly addressing bathwater temperature preferences that once discouraged full electrification. Ground Source systems, while small, benefit from year-round COP values above 4.0 and headline research showing potential 35-40% primary-energy savings in fifth-generation district schemes. Sumitomo Forestry’s forthcoming 200-home pilot in Otaru illustrates how municipal, developer and OEM collaboration can unlock ground-coupled economics even in seismic regions. Collectively these trends entrench hybrids as a pragmatic bridge while pure-electric performance edges upward.

By Technology: Ground-to-Water Gains Traction in District Heating

Air-to-Water designs held 48.62% of 2025 revenue owing to their seamless match with Japan’s hydronic radiator base and the wide modulation range offered by inverter drives. Yet Ground-to-Water systems log the swiftest expansion at 5.02% CAGR, fueled by municipal pilots that show seasonal COPs topping 4.5 and primary-energy cuts exceeding 40%. Ogata Village’s 1.2 MW loop demonstrated real-world savings that now influence subsidy scoring, while Otaru’s large-scale seasonal-storage build promises additional proof. Air-to-Air models still dominate unit volumes but contribute less revenue per install because of their simpler bill of materials and quicker replacement cycle.

Water-to-Water remains niche but strategic, with seawater-source machines at coastal data centers capturing waste heat for boiler feedwater, cutting CO₂ by tens of thousands of tons annually. JERA’s 3 MW plant in Yokohama opened boardroom eyes in the broader utilities segment and has raised policy interest in renewable-thermal grants. Meanwhile, Mitsubishi Electric’s modular hydronic line designed for cascading could lower engineering hurdles for multi-building campuses, aligning product strategy with district-scale demand aggregators.

By Capacity: Above 200 kW Segment Captures Industrial Process Heating

Systems below 10 kW represented 44.06% of 2025 revenue, an unsurprising lead given Japan’s predominance of compact single-family homes that seldom require more than 8 kW for combined space and water heating. The mid-tier 10-50 kW bracket supplies small commercial properties and apartment blocks, with rooftop packages easing crane and labor demands during retrofit. Units exceeding 200 kW, while niche today, register the fastest growth at 5.13% as breweries, dairies and steel plants substitute high-GWP boilers with CO₂ or R-1234ze heat pumps that reach 130-150 °C.

Mitsubishi Heavy’s 640 kW platform and JEXSYS’ COP 3.2 demonstration show momentum building around megawatt-scale deployments that dovetail with GX carbon pricing. Signed contracts for multi-megawatt projects suggest that the Japan heat pump market size for this capacity class will keep widening beyond 2031 as corporate decarbonization deadlines near. Vendors targeting process heating above 100 °C thus enjoy an early-mover window before global competitors align offerings.

By Application: Other Uses Surge on Industrial Decarbonization

Domestic and Sanitary Hot Water retained 48.21% of 2025 market revenue, underpinned by the 14-million-home installation goal and tighter building codes that effectively mandate heat pumps in new dwellings. Space Heating and Cooling combined to roughly 38%, with cold-climate prefectures drawing layered subsidies that trim net homeowner costs. The Other Applications bucket, industrial process, district networks and agricultural drying, logs the steadiest climb at 4.87% CAGR on the back of high-temperature CO₂ equipment and carbon-priced industrial retrofits.

The April 2026 GX launch drives factories emitting over 25,000 t CO₂ to evaluate electrified steam, a dynamic that lifts both equipment orders and engineering service demand. Agricultural uses, though small, gain visibility as greenhouse operators report 30-40% fuel savings relative to kerosene burners and qualify for Smart Agriculture grants. Variable refrigerant flow (VRF) systems that pivot between cooling and heating in offices also feed growth, especially now that R-32 refrigerant aligns with the Fluorocarbon Act phase-down.

By End User: Industrial Segment Leads Growth Amid Carbon Pricing

Residential accounted for 49.47% of 2025 revenue thanks to USD 380 million in national subsidies and mandatory efficiency codes for new builds. Commercial buildings, offices, hotels and hospitals, contributed roughly one-third, propelled by tenant pressure to secure CASBEE and LEED credentials and to hedge against tariff volatility through thermal storage. The industrial segment grows fastest at 5.26% as carbon costs bite, with half of surveyed factories citing tax avoidance as their primary adoption driver.

Early orders for Mitsubishi Heavy’s high-temperature units in the food sector show how quickly process heating can swing once project economics pass internal hurdle rates. Commercial buyers increasingly specify heat pumps bundled with storage tanks to arbitrage hourly tariffs and participate in demand-response programs. Meanwhile, cold-climate households embrace models that keep COPs above 2.5 at -20 °C, a performance milestone that neutralizes previous skepticism about winter comfort.

By Installation: Retrofit Gains Momentum as Building Stock Ages

New construction still commands 54.12% of 2025 revenue, reflecting code-driven uptake in metropolitan apartment and office towers. Yet Retrofit installations are advancing at a 4.86% CAGR because two-thirds of Japan’s 68 million-strong building stock predates modern energy codes. The 2026 Housing Renovation Subsidy reimburses up to one-third of heat-pump costs, making replacement more affordable even when legacy radiators need upgrades.

Supply-chain lead times for retrofit components remain longer, as contractors must survey piping and coordinate multiple trades. Panasonic’s retrofit-optimized R and D push aims to deliver higher outlet temperatures without crushing COP, a necessity for older high-temperature radiator loops. Cold-climate retrofits receive extra prefectural top-ups, draining local budget ceilings but accelerating kerosene boiler retirements. Installers, however, flag that multi-trade coordination keeps site schedules and soft costs higher than for greenfield projects.

Geography Analysis

Hokkaido and Tohoku, grappling with sub-15 °C winters, enjoy layered subsidies that cut homeowner investment to roughly USD 5,300-8,000, enabling per-capita adoption rates far above the national mean. Hokkaido alone absorbed 18% of residential shipments in 2025 despite housing only 4% of the population, proving the catalytic effect of strong local incentives. Nearby Akita’s 1.2 MW ground-source district network demonstrates 42% primary-energy savings, inspiring neighboring municipalities to explore similar loops.

Greater Tokyo, Osaka and Nagoya host 52% of commercial heat-pump installs as landlords chase green certifications and tenants demand tariff hedges. JERA’s 3 MW seawater unit in Yokohama data center territory highlights coastal prospects where waste heat meets paradoxically tight urban land. Planned data hubs in Hokkaido will route recovered heat into new-build housing, a template that aligns digital infrastructure growth with neighborhood decarbonization.

Manufacturing belts in Chubu and Kansai accelerate industrial installs after April 2026 carbon fees imposed real penalties on fossil steam. Conversely, rural Kyushu and Shikoku lag, reflecting lower incomes and a thinner installer base, technician density sits 40-50% under the national average, a gap that prolongs lead times and dims subsidy impact. Absent workforce reinforcement, adoption gaps between urban corridors and rural prefectures may widen over the forecast horizon.

Competitive Landscape

Daikin, Mitsubishi Electric and Panasonic together shipped roughly 60% of units in 2025, but falling component prices allow LG, Haier and PHNIX to undercut by 15-20%, squeezing margins in entry-level tiers. Strategic defenses center on vertical integration and refrigerant innovation: Daikin’s R-290 compressor joint venture with Copeland buffers supply risk ahead of the EU F-Gas phase-out. Fujitsu General’s Paloma Rheem buyout secures a 1,200-contractor channel that matters more than ever as installer scarcity shapes sales velocity.

Industrial process heating above 100 °C remains white space, and local players race to lock in early reference sites before European specialists arrive with turbo-compressor technology. District heating also tempts utilities seeking non-fossil capacity credits, yet requires multi-stakeholder orchestration that only a few conglomerates can bankroll. AI-driven diagnostics emerged as a differentiation wedge in 2025, with Daikin-Hitachi pilots cutting runtime costs double digits and opening service-revenue annuities.

Regulatory headwinds favor scale: the April 2027 refrigerant-handling mandate tilts field advantage to firms that can train hundreds of installers and absorb compliance overhead. Meanwhile, automotive supplier AISIN adapts EV heat-sink know-how for building HVAC, signaling peripheral entrants could contest share in the medium term. Taken together, the Japan heat pump market shows moderate concentration but rising churn potential as policy, technology and labor dynamics evolve.

Japan Heat Pump Industry Leaders

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

Panasonic Corporation

Carrier Global Corporation

Fujitsu General Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mitsubishi Electric launched the ecodan Pro modular hydronic line, 50-200 kW, aimed at multi-building campuses.

- March 2026: Mitsubishi Electric introduced the City Multi R32 VRF series that meets the updated Fluorocarbon Act phase-down timetable.

- January 2026: Daikin and Copeland formed a venture to mass-produce R-290 compressors in Europe and the United States, with Japanese rollout slated for late 2026.

- January 2026: OCCTO commenced a demand-response pilot paying residential heat-pump owners up to USD 0.10 per kilowatt-hour for evening curtailment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysts define the Japan heat pump market as revenue generated from electrically driven air-source, water-source, and ground-source systems that transfer thermal energy for space heating, cooling, or domestic hot water across residential, commercial, industrial, and institutional buildings nationwide. Equipment covered includes packaged and split units, monoblocs, hybrids, and exhaust-air variants shipped factory-charged or fully assembled.

Scope exclusions include systems whose primary function is chiller refrigeration, absorption or desiccant HVAC, and district-scale networks without an integral heat-pump core.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

We then ran structured interviews and brief surveys with installers, OEM product managers, utility-rebate officers, and housing-society engineers across Kanto, Kansai, and Hokkaido. Their insights refined load profiles, replacement cycles, and subsidy uptake rates that Mordor analysts fed into our model.

Desk Research

During desk work, we drew shipment volumes from the Japan Refrigeration and Air Conditioning Industry Association, tariff trends from the Agency for Natural Resources and Energy, import codes via Volza, low-carbon policy texts from METI, and patent counts through Questel to map installed base and price shifts. Broader context came from IEA heat-pump dashboards, Statistics Bureau dwelling data, and company filings that disclose segment revenues and ASP movement.

Annual reports, exchange filings, press releases, and respected trade journals helped benchmark efficiency progression, while D&B Hoovers provided vendor-level Japan revenue. The sources above are illustrative only; many additional outlets informed data collection, validation, and assumption testing.

Market-Sizing & Forecasting

Modeling begins with a top-down rebuild that aligns JRAIA shipment data with replacement ratios, new-build completions, and heat-pump penetration into boiler stock. Results are balanced with bottom-up checks such as sampled ASP × volume roll-ups from key suppliers, giving us a defensible baseline. Core drivers include residential floor-area additions, electricity-to-gas price spreads, carbon-reduction targets, seasonal heating degree-days, and incentive budgets. Multivariate regression, cross-validated through ARIMA scenarios, projects each driver before totals roll forward to the forecast period. Data gaps, such as rural retrofit counts, are interpolated with regional census ratios and confirmed through channel feedback.

Data Validation & Update Cycle

Outputs pass variance checks against independent indicators, a two-layer analyst review, and re-contact triggers when policy or pricing shocks breach preset thresholds. Reports refresh annually, and an analyst reruns the workbook just before release so clients receive the latest view.

Why Mordor's Japan Heat Pump Size & Share Analysis Baseline Commands Reliability

Published market values often differ because publishers select varying product baskets, price bases, and refresh cadences.

Key gap drivers here include some studies that blend commercial VRF chillers into heat pumps, others that omit CO₂ 'Eco-Cute' water heaters, and differing currency conversions. Our disciplined scope, yearly refresh, and dual-angle validation keep Mordor's figure balanced and reproducible.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.4 B (2025) | Mordor Intelligence | |

| USD 13.4 B (2024) | Global Consultancy A | Bundles wider HVAC devices and applies list prices without channel discounts |

| USD 3.8 B (2024) | Trade Journal B | Excludes sanitary hot-water systems and relies on limited regional sampling |

The comparison shows that our transparent variable selection and frequent validation create a dependable midpoint buyers can trace back to clear, repeatable data signals.

Key Questions Answered in the Report

What is the current value of the Japan heat pump market?

It stands at USD 5.69 billion in 2026, on course to reach USD 7.12 billion by 2031.

How fast is demand expected to grow in Japan?

The compound annual growth rate is projected at 4.59% for 2026-2031, driven by subsidies, carbon pricing and high-temperature industrial use.

Which segment is expanding the quickest?

Hybrid source systems show the fastest growth, with a 5.31% CAGR expected through 2031 as users seek fuel-switching flexibility.

Why are high-capacity heat pumps gaining attention?

Units above 200 kW can deliver steam over 130 °C, enabling industrial decarbonization and benefiting from the GX Emissions Trading Scheme.

What barriers could slow market adoption?

High installation costs, installer shortages and complex retrofits in dense urban areas remain significant hurdles despite policy support.

Page last updated on: