Electric Car Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 10.90 Billion |

| Market Size (2031) | USD 21.37 Billion |

| Growth Rate (2026 - 2031) | 14.41% CAGR |

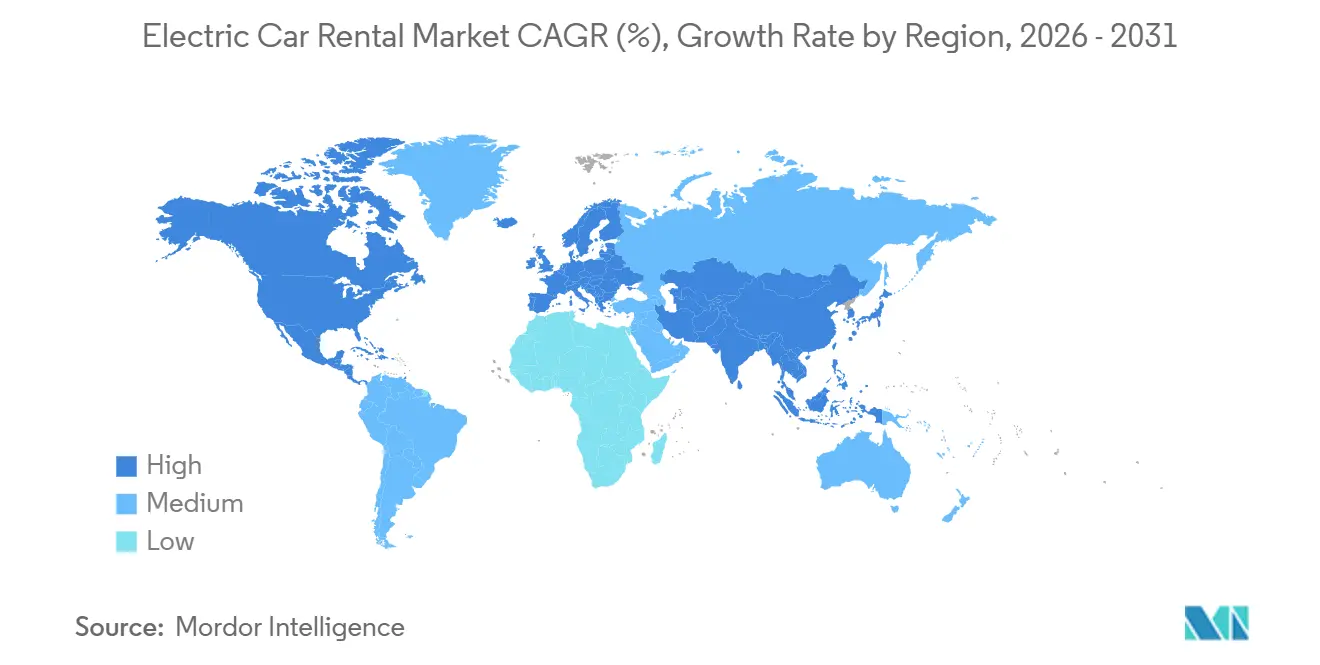

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

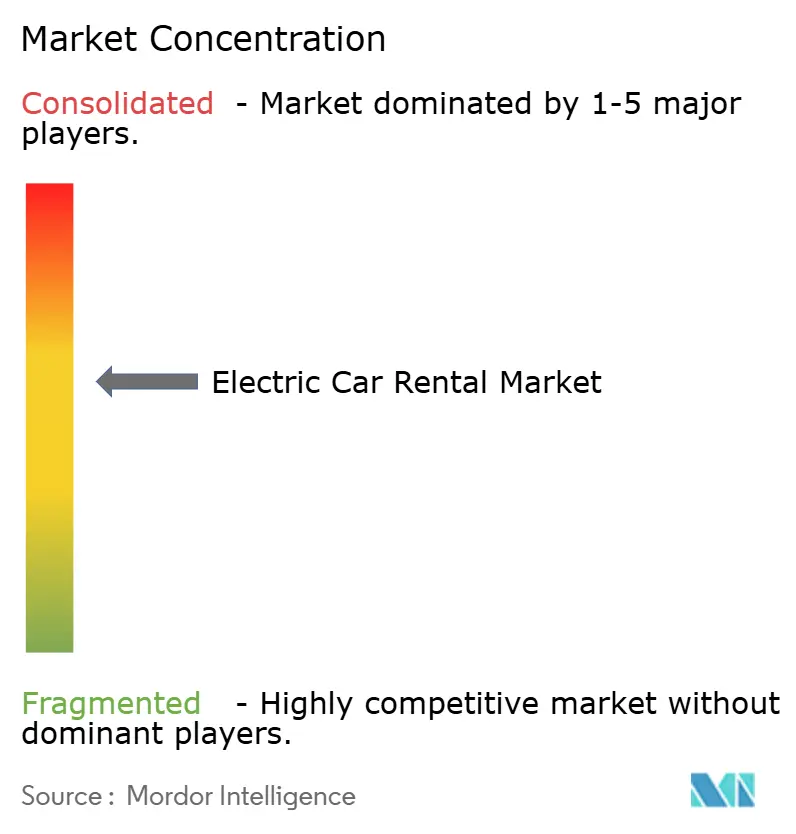

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Car Rental Market Analysis by Mordor Intelligence

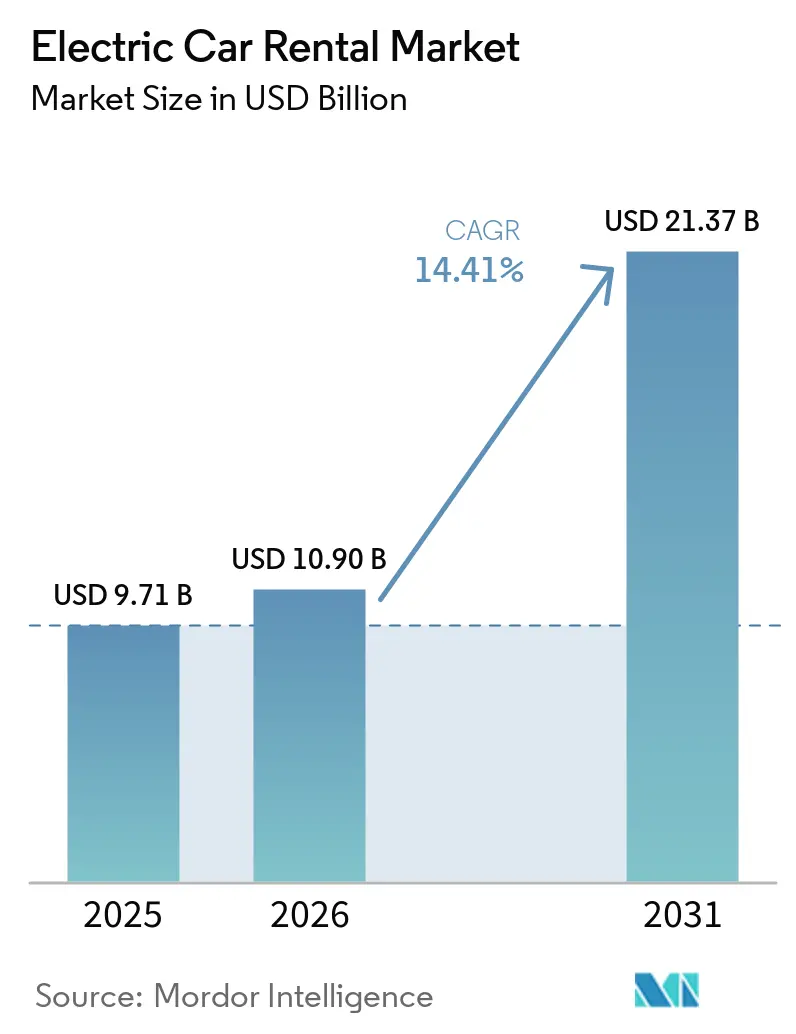

The electric car rental Market size is expected to grow from USD 9.71 billion in 2025 to USD 10.90 billion in 2026 and is forecast to reach USD 21.37 billion by 2031 at 14.41% CAGR over 2026-2031. Fleet electrification momentum, strengthening OEM-rental partnerships, and surging airport fast-charging capacity are reshaping procurement norms as corporate travel managers, municipal entities, and leisure customers adopt battery electric vehicles at scale. Battery electric units already dominate orders because residual-value guarantees from automakers mitigate depreciation risk, while peer-to-peer platforms expand consumer access and intensify price pressure on legacy operators. Regional airport authorities are accelerating infrastructure build-outs to shorten vehicle turnarounds, and carbon-credit monetization now supplements operator cash flow in compliance markets. Competitive dynamics remain intense as digital-first disruptors compete with full-service operators that must balance charging-network investments with residual-value management.

Key Report Takeaways

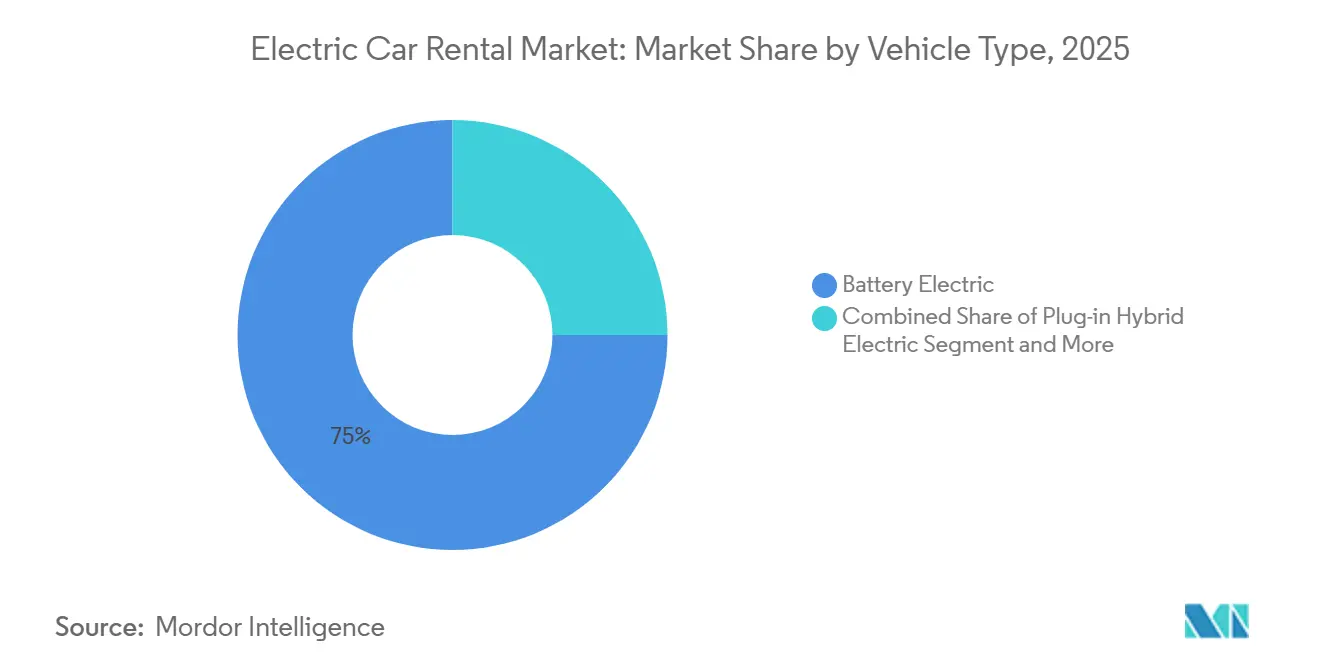

- By vehicle type, battery-electric models led the electric car rental market with 75.02% market share in 2025 and are projected to expand at a 17.85% CAGR through 2031.

- By body style, SUVs commanded a 42.15% share of the electric car rental market size in 2025 and are projected to advance at a 15.48% CAGR through 2031.

- By customer type, leisure/tourism clients held 59.03% share in 2025, while ride-hailing driver subscriptions are forecast to grow at an 18.31% CAGR between 2026 and 2031.

- By booking channel, online reservations accounted for 64.11% of the electric car rental market in 2025 and are set to grow at a 16.84% CAGR through 2031.

- By rental duration, short-term rentals accounted for the largest share of demand in 2025, with a 58.36% share, while long-term subscriptions are expanding at a 15.03% CAGR by 2031.

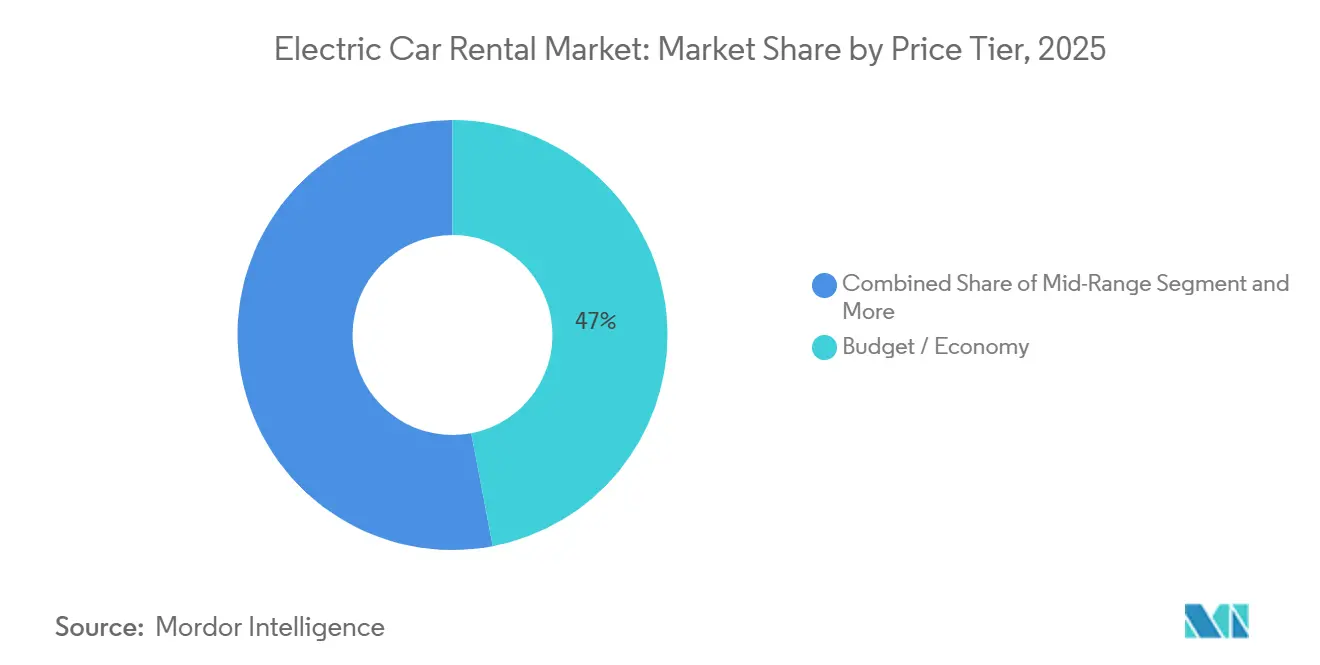

- By price tier, budget/economy cars held 47.01% share in 2025, while the luxury and premium offerings are growing at a 17.22% CAGR through 2031.

- By end use, airport transport rentals dominated with a 50.24% share in 2025, while last-mile delivery is expected to grow at a 16.35% CAGR by 2031.

- By geography, North America captured 40.25% of the electric car rental market share in 2025, whereas Asia-Pacific is on track for the fastest 15.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEVs Reach TCO Parity | +3.2% | Global, early adoption in Norway, California, Netherlands | Short term (≤ 2 years) |

| Government EV-Fleet Mandates | +2.8% | North America, Europe, China | Medium term (2-4 years) |

| Guaranteed OEM Residual Values | +2.5% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Rapid Airport Charging Expansion | +2.1% | North America, Europe, Asia-Pacific hubs | Medium term (2-4 years) |

| Peer-to-Peer EV-Sharing Surge | +1.9% | North America, Europe, Australia | Medium term (2-4 years) |

| Carbon-Credit Monetization | +1.2% | Europe, California, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Falling TCO Parity of BEVs vs. ICE in High-Utilization Rental Cycles

Falling lithium-ion pack prices reached a significant milestone, making fleet-scale battery-electric vehicle (BEV) acquisitions more financially viable than internal combustion engine (ICE) vehicles over their lifecycles. This development has been particularly impactful in regions with high fuel costs, where BEVs offer substantial savings on operational expenses. Rental vehicles, which typically cover extensive distances annually, benefit from lower fuel costs and reduced maintenance requirements. The maintenance savings are notable, as BEVs require fewer service interventions than ICE vehicles, resulting in a significant reduction in overall service expenses during the lease period. In countries like Norway, fleets have reported that BEVs achieve cost parity much faster than ICE vehicles, highlighting the growing economic appeal of electrification in the automotive sector.

Increasing Government EV-Fleet Mandates for Rental Operators

Starting in 2024, California's Advanced Clean Fleets rule requires high-priority fleets to transition exclusively to zero-emission vehicles, significantly accelerating the pace of fleet turnover [1]“Advanced Clean Fleets Regulation,” California Air Resources Board, arb.ca.gov. Similarly, regulatory frameworks in the European Union and pilot programs in Chinese cities are introducing stringent penalties that effectively discourage the procurement of internal-combustion vehicles by operators managing cross-border routes. These measures are reshaping the competitive landscape, as operators unable to manage the high upfront costs associated with battery-powered vehicles face mounting consolidation pressures. In contrast, companies that have established integrated charging networks are gaining a competitive edge, leveraging their infrastructure to secure favorable positions in airport concession bids and other strategic opportunities.

OEM-Rental Partnerships Offering Residual-Value Guarantees

Stellantis and SIXT announced a multi-billion-euro agreement under which SIXT could buy up to 250,000 Stellantis vehicles for its rental fleet across Europe and North America by 2026.[2]“SIXT Press Release,” Sixt SE, sixt.com This arrangement provides stability and predictability for Sixt, allowing the company to focus on its operations without concerns over residual value uncertainties. Similarly, General Motors has established a comparable partnership with Enterprise for its electric vehicle models, offering terms that limit depreciation exposure and provide financial safeguards. These agreements are strategically designed to reduce the financial burden on operators, enabling them to allocate resources more efficiently. Moreover, such collaborations play a pivotal role in driving the adoption of electric vehicles, fostering a faster transition toward sustainable mobility solutions within the industry.

Rapid Expansion of Airport Fast-Charging Concessions

In July 2025, bp pulse opened its most significant U.S. EV charging hub near LAX (about 2 miles away), featuring 48 ultrafast charging bays. This facility includes a dedicated section for rental car turnover, ensuring seamless operations for rental companies and convenience for travelers. The initiative reflects the airport's commitment to sustainability and enhancing the overall passenger experience. Similarly, Heathrow, Narita, and Changi airports have implemented comparable solutions, integrating advanced billing systems that allow rental operators to directly charge travelers for usage. These developments address key concerns such as minimizing vehicle downtime and alleviating range anxiety for visitors. Additionally, they provide airports with an opportunity to diversify their revenue streams through innovative surcharges, aligning with broader operational efficiency and customer satisfaction goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate Charging Infrastructure Suburbs | -1.8% | North America (ex-urban), Southern Europe, Australia | Medium term (2-4 years) |

| Battery Depreciation and Repair Costs | -1.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Insurance-Underwriting Gaps | -1.1% | Global, most pronounced in North America | Short term (≤ 2 years) |

| Volatile Residual Values for EVs | -0.9% | Europe, Southeast Asia, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inadequate Charging Infrastructure at Suburban and Rural Drop-Off Points

Fast chargers in the United States were predominantly concentrated within metropolitan areas, creating significant challenges for travel outside urban centers[3]“Alternative Fuels Data Center,” U.S. Department of Energy, energy.gov . This lack of infrastructure limits the feasibility of one-way itineraries and compels operators to implement geographic surcharges, which discourage potential bookings. Similarly, in regions such as Australia's tourism routes and the rural areas of Southern Europe, the absence of adequate charging networks forces operators to rely on a combination of Internal Combustion Engine (ICE) and Battery Electric Vehicle (BEV) fleets. This dual-fleet approach increases operational complexity and drives up inventory costs, further complicating the adoption of electric vehicles in these areas.

High Battery Depreciation and Repair Costs on Short Rental Cycles

Hertz observed that repairing electric vehicles after collisions is significantly more expensive compared to internal combustion engine vehicles. Furthermore, replacing a full battery pack can become a substantial financial burden when warranty claims are not approved. In rental environments, the frequent use of fast-charging technology accelerates the deterioration of the vehicle's overall health at a much faster rate. This accelerated wear and tear leads to a notable reduction in the perceived value of these vehicles in the secondary market, as buyers tend to apply considerable discounts, thereby compressing their residual values.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Battery Dominance Reshapes Fleet Economics

Battery electric units delivered 75.02% of the fleet share in 2025 and are expected to grow at a 17.85% CAGR through 2031, whereas plug-in hybrids fill rural-route gaps but incur higher maintenance costs. Fuel-cell vehicles remain pilot-only because hydrogen refuelling availability remains limited; for example, the U.S. had 54 open retail hydrogen stations as of 2024, most in California. Pure battery platforms thus anchor the electric car rental market, and OEMs' pivot away from ICE production solidifies this lead.

Early battery cost parity and fast-charging plazas at airports enable operators to retire ICE assets faster than initially forecast, with residual-value guarantees further de-risking the purchase. Plug-in hybrids are likely to plateau below a 20% share as customers gravitate toward BEVs for their simplicity and policy advantages. Fuel-cell volumes stay negligible absent large-scale hydrogen corridors.

By Body Style: SUVs Command Premium for Range and Versatility

Sport Utility Vehicles (SUVs) accounted for 42.15% of 2025 demand and will rise at a 15.48% CAGR, leveraging larger battery housings that deliver 400–500 kilometer real-world range. Sedans and hatchbacks combined are stabilizing around one-third of demand, while MPVs and coupes remain niche. SUVs also achieve 20–30% higher daily rates that amortize their purchase premium over compact body styles.

Fleet managers prefer SUVs because crossover platforms from Tesla, Volkswagen, and Hyundai offer 150-kilowatt charging that restores significant capacity in under 30 minutes, ideal for airport turnover. Sedans lose ground as automakers discontinue ICE variants and prioritize electric crossovers, and hatchbacks dominate only in dense European cores where parking constraints trump range.

By Customer Type: Ride-Hailing Subscriptions Disrupt Legacy Mix

Ride-hailing driver packages are set to grow at an 18.31% CAGR through 2031, converting rental companies into managed-service providers. Leisure travelers generated 59.03% of bookings in 2025, but price sensitivity and seasonality cap revenue per vehicle. Corporate travel sees slower growth because hybrid work reduces trip frequency, yet emissions reporting keeps EVs on preferred lists.

Subscription bundles priced at USD 300–400 per week appeal to drivers who save USD 200–300 on fuel each month, and embedded insurance streamlines the onboarding process. Peer-to-peer hosts, holding a nominal share, profit from localized supply and carbon-offset features that resonate with eco-conscious customers.

By Booking Channel: Mobile Apps Capture Share Through Charging Integration

Online bookings captured 64.11% of 2025 transactions, climbing as mobile apps show real-time battery status and reserve chargers at destination hubs. Online platforms are expected to remain the fastest-growing category, with a 16.84% CAGR, while offline channels are projected to experience a significant decline by 2030. Sixt, Hertz, and Enterprise integrated charge-point networks into apps, offering discounted rates and low-battery alerts that curb towing incidents.

Operators are gradually phasing out paper contracts and introducing convenience surcharges, which have contributed to a noticeable decline in walk-up counter bookings. Desktop interfaces continue to play a significant role, particularly for managing multi-vehicle corporate trips. Meanwhile, mobile platforms are advancing with notable milestones, such as the integration of in-app digital keys and augmented reality charging tutorials, which enhance user convenience and engagement.

By Rental Duration: Long-Term Subscriptions Hedge Spot-Market Volatility

Short-term rentals lasting under a week accounted for 58.36% of the demand in 2025; their growth has been tempered, influenced by leisure patterns tied to weather and seasonal fluctuations. In contrast, subscriptions extending beyond 30 days are projected to surge at a 15.03% CAGR, driven by gig-economy drivers and firms transitioning to electric employee transport without upfront capital investments. These subscriptions have gained popularity as they offer a cost-effective and flexible solution for businesses and individuals seeking long-term mobility without the burden of ownership.

As customers lean towards either flexible short-term rentals or the security of subscriptions, medium-term usage has reached a plateau. This shift reflects changing consumer preferences, where convenience and adaptability play a significant role in decision-making. To enhance utilization and ensure a steadier cash flow—especially in contrast to the peaks of leisure bookings—operators are now bundling insurance and maintenance with their subscriptions. These bundled offerings not only enhance customer satisfaction but also provide operators with a more predictable revenue stream, thereby mitigating the risks associated with seasonal demand fluctuations.

By Price Tier: Luxury Segment Captures Range-Anxiety Premium

The demand for luxury EVs highlights a shift in consumer preferences toward high-performance and feature-rich vehicles. Budget tiers continue to dominate the market, accounting for 47.01% of revenue in 2025. However, their growth potential is constrained by the limited availability of low-cost models, which restricts broader adoption. Meanwhile, luxury electric vehicles (EVs) from brands like Tesla, Porsche, and Mercedes-Benz are experiencing significant growth, with a CAGR of 17.22% by 2031. This expansion is primarily driven by travelers who are willing to pay a premium for advanced features, including a 500-kilometer range and concierge charging services, which enhance convenience and usability.

High-end models are achieving utilization rates that are higher than their internal combustion engine (ICE) counterparts. This superior performance is encouraging operators to allocate more capital toward premium inventory, despite the higher depreciation rates associated with these units. The willingness to invest in high-end models underscores the growing confidence in the profitability and long-term viability of the luxury EV segment.

By End-Use Purpose: Airport Transport Leads While Last-Mile Delivery Surges

Airport transport commands a dominant 50.24% market share in 2025, it faces stiff competition from emerging ride-hailing services and enhanced rail links. The local city-commute car-sharing sector is witnessing a wave of consolidation, and the demand for inter-city outstation services hinges on the availability of fast-charging stations in rural areas. While last-mile delivery rentals surge by 16.35% CAGR, with industry giants Amazon, FedEx, and DHL piloting electric vans on select routes.

Commercial clients, often paying premium daily rates, frequently opt for purchase at the end of their contracts. This trend effectively positions rental firms as key procurement channels for logistics companies. By integrating rental services into their supply chains, logistics companies not only streamline vehicle acquisition but also reduce upfront capital expenditure. Additionally, this approach allows them to test vehicle performance and suitability before committing to full-scale purchases, ensuring operational efficiency and cost-effectiveness.

Geography Analysis

The Asia-Pacific region is expected to register the fastest growth, with a 15.79% CAGR, driven by Chinese municipal quotas setting electrification targets for the near future and Japanese airport concessions integrating seamless billing. North America, with a 40.25% share in 2025, sees growth anchored in West Coast mandates, yet tempered by sparse Midwest charging networks. Singapore EV adoption is rising fast, driven by incentives and electric taxi programs, positioning it as an EV rental hub. Hertz increased its EV disposition plan to 30,000 vehicles intended for sale in 2024, following EV depreciation and repair-cost pressures.

Europe’s dense charging grids drive high penetration, though fragmented incentives across 27 member states complicate cross-border rentals. Norway leads the way with notable fleet electrification, while Italy and Spain lag due to gaps in rural infrastructure. South America and the Middle East are still in the early stages, with Brazil and the United Arab Emirates leading the way in urban fleets but facing high import duties and thermal challenges related to battery performance in hot climates.

Canada mirrors the United States patterns, with British Columbia and Quebec outpacing Alberta. India’s fleet consists of limited rental EVs, but asset-light peer-to-peer models pave the way for scale if infrastructure broadens. Australia confines EV rentals to capital cities because tourist routes lack fast chargers. South Africa’s limited charging grid restricts EV availability to Johannesburg and Cape Town corridors.

Competitive Landscape

Enterprise Holdings, Hertz, Avis Budget, and Sixt dominate the electric car rental market; however, peer-to-peer models and logistics-centric players are intensifying the competition. SIXT charge integrates access to nearly 400,000 charge points. This extensive infrastructure forms a digital moat that smaller competitors find challenging to replicate, further solidifying Sixt's position in the market.

Asset-light disruptors like Turo and Getaround are reshaping the market by incorporating specialized battery coverage into their host policies, effectively addressing the underwriting gaps that continue to challenge traditional rental firms. Meanwhile, Ryder and Penske, leveraging their expertise in commercial trucks, are expanding into the electric van segment. By targeting B2B contracts, these companies are capitalizing on opportunities to secure premium rates, further diversifying their revenue streams, and strengthening their foothold in the electric vehicle rental space.

To remain competitive, successful market strategies are increasingly integrating telematics-driven battery health monitoring with dynamic pricing models. These approaches not only ensure optimal battery performance but also help absorb the impact of fluctuating electricity costs. As the market evolves, such innovations are becoming critical for companies aiming to maintain profitability and adapt to the growing demand for electric vehicles.

Electric Car Rental Industry Leaders

The Hertz Corporation

Avis Budget Group, Inc.

Enterprise Holdings, Inc.

Zoomcar Inc.

Europcar Mobility Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ryde announced plans to deploy up to 400 EVs over six months under a call-option agreement with Guan Chao Holdings and Singapore Electric Vehicles, ensuring priority supply and flexible financing.

- September 2025: Evera launched an app in India offering zero-cancellation electric vehicle rentals for airport transfers, hourly packages, and corporate fleets.

- June 2025: Europcar Mobility Group UK introduced a long-term rental plan for businesses seeking electric and plug-in hybrid models, promising delivery within five working days nationwide.

Global Electric Car Rental Market Report Scope

The scope includes segmentation by vehicle type (battery electric, plug-in hybrid electric, extended-range electric, fuel-cell electric), body style (hatchback, sedan, sports utility vehicles, multi-utility vehicles/multi-purpose vehicles, sports coupe), customer type (leisure/tourism, business/corporate, peer-to-peer host, ride-hailing driver subscription), booking channel (online, offline), rental duration (short-term, medium-term, long-term), price tier (budget/economy, mid-range, luxury/premium), and end-use purpose (local commute, airport transport, inter-city/outstation, last-mile delivery). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, the Middle East, and Africa. Market size and growth forecasts are presented by value in USD.

| Battery Electric |

| Plug-in Hybrid Electric |

| Extended-Range Electric (REEV) |

| Fuel-Cell Electric |

| Hatchback |

| Sedan |

| Sport Utility Vehicle (SUV) |

| Multi-Utility Vehicle (MUV)/Multi-Purpose Vehicle (MPV) |

| Sports Coupe |

| Leisure / Tourism |

| Business / Corporate |

| Peer-to-Peer Host |

| Ride-hailing Driver Subscription |

| Online | Desktop Web |

| Mobile App | |

| Offline |

| Short-Term (Less than 7 days) |

| Medium-Term (7 to 30 days) |

| Long-Term (More than 30 days, subscription) |

| Budget / Economy |

| Mid-Range |

| Luxury / Premium |

| Local Commute |

| Airport Transport |

| Inter-City / Outstation |

| Last-Mile Delivery |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Vehicle Type | Battery Electric | |

| Plug-in Hybrid Electric | ||

| Extended-Range Electric (REEV) | ||

| Fuel-Cell Electric | ||

| By Body Style | Hatchback | |

| Sedan | ||

| Sport Utility Vehicle (SUV) | ||

| Multi-Utility Vehicle (MUV)/Multi-Purpose Vehicle (MPV) | ||

| Sports Coupe | ||

| By Customer Type | Leisure / Tourism | |

| Business / Corporate | ||

| Peer-to-Peer Host | ||

| Ride-hailing Driver Subscription | ||

| By Booking Channel | Online | Desktop Web |

| Mobile App | ||

| Offline | ||

| By Rental Duration | Short-Term (Less than 7 days) | |

| Medium-Term (7 to 30 days) | ||

| Long-Term (More than 30 days, subscription) | ||

| By Price Tier | Budget / Economy | |

| Mid-Range | ||

| Luxury / Premium | ||

| By End-Use Purpose | Local Commute | |

| Airport Transport | ||

| Inter-City / Outstation | ||

| Last-Mile Delivery | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Norway | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the electric car rental market today?

The electric car rental market size stood at USD 10.90 billion in 2026 and is forecast to reach USD 21.37 billion by 2031.

What CAGR is expected for electric car rentals to 2031?

The market is projected to expand at a 14.41% CAGR between 2026 and 2031.

Which vehicle type leads rental fleets?

Battery electric vehicles held 75.02% fleet share in 2025 and are set to grow faster than any alternative powertrain.

Why are SUVs popular in electric car rentals?

Electric SUVs offer larger battery capacities for 400–500 kilometer ranges and command higher daily rates, driving 42.15% share in 2025.

Which region will grow fastest for rentals?

Asia-Pacific is expected to post the quickest 15.79% CAGR due to Chinese municipal quotas and Japanese airport charging concessions.

Page last updated on: